Spatial Effects and Nonlinear Analysis of Energy Consumption, Financial Development, and Economic Growth in China

Abstract

:1. Introduction

2. Literature Review

2.1. Energy Consumption and Economic Growth

2.2. Financial Development and Economic Growth

2.3. Energy Consumption, Financial Development and Economic Growth

2.4. Summary of the Aforementioned Literature

3. Methodology

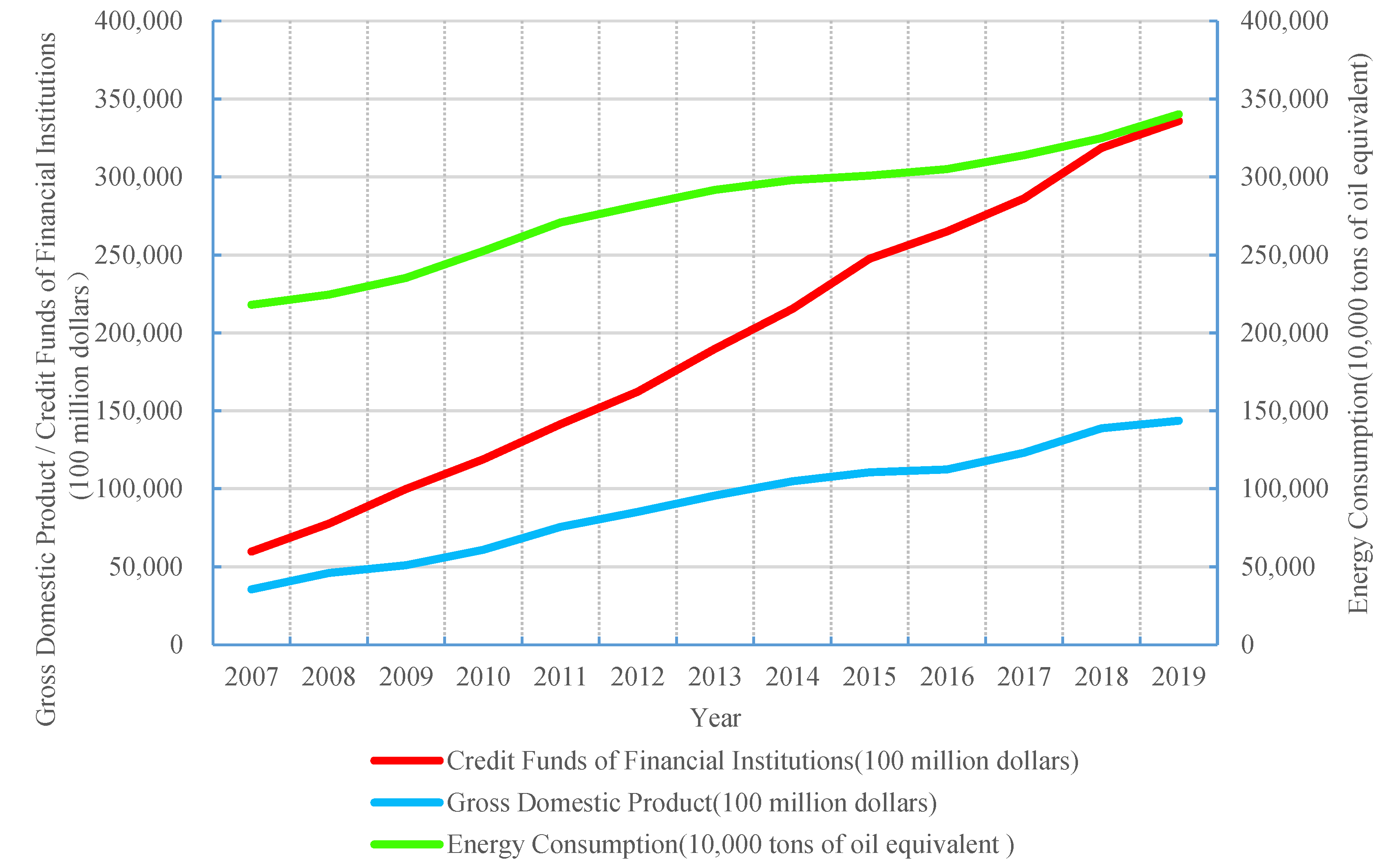

3.1. Variables and Data

3.2. Spatial Econometric Methods

3.3. Selection of Spatial Weight Matrix

3.4. Nonlinear Econometric Methods

4. Results and Discussion

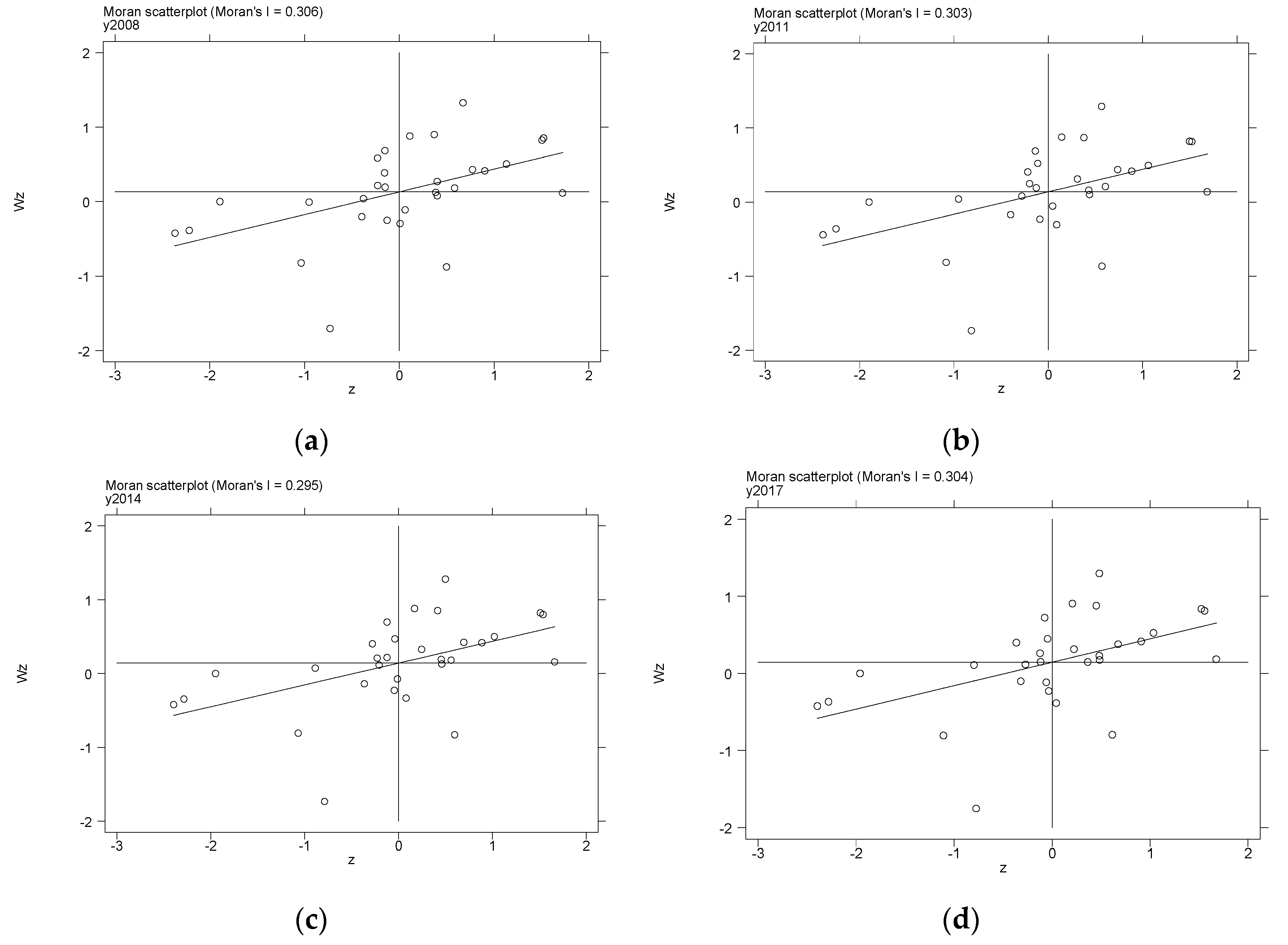

4.1. Spatial Correlation Tests

4.2. Analysis of Spatial Econometric Models

4.3. Analysis of Spatial Spillover Effects

4.4. Analysis of Threshold Effects

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

| Authors | Countries | Periods | Methodologies | Main Conclusion |

|---|---|---|---|---|

| Energy Consumption and Economic Growth | ||||

| Acheampong (2018) | 116 countries | 1990–2014 | PVAR and S-GMM | EC→GDP |

| Wang et al. (2015) | China | 1990–2012 | Cointegration and granger causality tests | EC↔GDP |

| Liu and Hao (2018) | 69 countries of the Belt and Road | 1970–2013 | VECM, FMOLS and DOLS | Energy use ↔ GDP per capita (in the long run) |

| Shahbaz et al. (2018) | 10 countries | 1960Q1–2015Q4 | Quantile-on-quantile approach | GDP→EC (with variations across each country) |

| Aydin and Esen. (2017) | 12 countries | 1991–2013 | Dynamic panel threshold analysis | EC GDP (energy intensity ≥ 0.44%), EC GDP (energy intensity ≤ 0.44%) |

| Hao et. al.(2018) | China | 1995–2010 | VECM, FMOLS, IRF | Rural GDP ↔ rural EC (in the short run) |

| Financial Development and Economic Growth | ||||

| Yang (2019) | 49 mid-income countries | 1960–2016 | Granger causality | FDGDP |

| Sassi and Gasmi (2014) | 27 European countries | 1995–2012 | OLS, GMM panel | FDGDP |

| Law and Singh (2014) | 87 countries | 1980–2010 | Dynamic panel threshold | There is a threshold effect in the finance–growth relationship |

| Yang(2014) | China | 1987–2009 | Panel threshold model | Threshold effect and diminishing marginal efficiency |

| Liu and Zhang (2018) | China | 1996–2013 | Panel quantile regression | FD→GDP(different with different regions and stages) |

| Energy Consumption, Financial Development, and Economic Growth | ||||

| Eren et al. (2019) | India | 1971–2015 | Cointegration test, DOLS and granger causality test | REC and GDP are FD driven in the long run. REC↔GDP |

| Ouyang and Li (2018) | China | 1996Q1–2015Q4 | GMM panel VAR and PCA | FDGDP, EC→GDP, FD→EC(↓) |

| Shahbaz et al. (2017) | India | 1960Q1–2015Q4 | A nonlinear and asymmetric analysis | (only negative shocks) FD→GDP, (only negative shocks)EC→GDP |

| Komal and Abbas (2015) | Pakistan | 1972–2012 | S-GMM | EC→GDP, FDEC |

| Khan et al. (2019) | 193 countries | 1990–2017 | 3SLS, dynamic model 2-step GMM, S-GMM | EC→FD(↓) |

| Variables | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|

| Economic Growth(lnGDP) | 9.343 | 0.920 | 6.681 | 11.227 |

| Total Energy Consumption(lnEC) | 9.319 | 0.686 | 6.963 | 10.569 |

| Financial development (lnFD) | 9.592 | 0.964 | 6.581 | 11.745 |

| The Intersection (lnEC*lnFD) | 89.856 | 14.126 | 49.530 | 121.966 |

| Capital Investment of Provinces(lnK) | 9.098 | 0.915 | 6.179 | 10.919 |

| Labor Input(lnL) | 5.995 | 0.766 | 3.815 | 7.588 |

| The level of Openness (lnOpen) | 8.897 | 2.220 | 3.840 | 14.311 |

| Fiscal expenditure (lnFis) | 7.922 | 0.731 | 5.488 | 9.618 |

| Year | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| lnGDP | 0.315 | 0.316 | 0.315 | 0.318 | 0.314 | 0.308 | 0.307 | 0.306 | 0.306 | 0.309 | 0.314 |

| Z-value | 2.918 | 2.926 | 2.917 | 2.939 | 2.908 | 2.867 | 2.855 | 2.848 | 2.851 | 2.875 | 2.919 |

| p-value | 0.002 | 0.002 | 0.002 | 0.002 | 0.002 | 0.002 | 0.002 | 0.002 | 0.002 | 0.002 | 0.002 |

| Test | Statistic (Independent Model) | Statistic (Synergistic Model) |

|---|---|---|

| Lagrange Multiplier (error) | 33.061 *** | 41.409 *** |

| Robust Lagrange Multiplier (error) | 20.081 *** | 15.657 *** |

| Lagrange Multiplier (lag) | 38.575 *** | 127.031 *** |

| Robust Lagrange Multiplier (lag) | 25.595 *** | 101.280 *** |

| Type | F-Value | p-Value | Critical Values | Threshold Estimation Value | 95% Asymptotic Confidence Interval | ||

|---|---|---|---|---|---|---|---|

| 10% | 5% | 1% | |||||

| Single threshold | 74.910 | 0.000 | 27.575 | 31.404 | 50.128 | 9.705 | [9.696, 9.715] |

| Double threshold | 26.670 | 0.067 | 24.642 | 28.215 | 37.697 | 9.660 | [9.655, 9.665] |

| 10.116 | [10.094, 10.124] | ||||||

| Type | F-Value | p-Value | Critical Values | Threshold Estimation Value | 95% Asymptotic Confidence Interval | ||

|---|---|---|---|---|---|---|---|

| 10% | 5% | 1% | |||||

| Single threshold | 14.880 | 0.822 | 37.520 | 45.114 | 65.473 | 8.032 | [7.751, 8.074] |

| Double threshold | 12.470 | 0.684 | 30.234 | 35.228 | 43.194 | 8.969 | [8.941, 8.972] |

| 9.892 | [9.839, 9.893] | ||||||

References

- Zhou, H.; Qu, S.; Wu, Z.; Ji, Y. A study of environmental regulation, technological innovation, and energy consumption in China based on spatial econometric models and panel threshold models. Environ. Sci. Pollut. Res. 2020, 27, 37894–37910. [Google Scholar] [CrossRef] [PubMed]

- Eren, B.M.; Nigar, T.; Korhan, K.G. The impact of financial development and economic growth on renewable energy consumption: Empirical analysis of India. Sci. Total Environ. 2019, 663, 189–197. [Google Scholar] [CrossRef]

- National Bureau of Statistics of China. Statistical Communiqué of the People’s Republic of China on the 2019 National Economic and Social Development. National Bureau of Statistics of China website. 2020. Available online: http://www.stats.gov.cn/english/PressRelease/202002/t20200228_1728917.html (accessed on 7 August 2020).

- Rafindadi, A.A.; Ozturk, I. Effects of financial development, economic growth and trade on electricity consumption: Evidence from post-Fukushima Japan. Renew. Sustain. Energy Rev. 2016, 54, 1073–1084. [Google Scholar] [CrossRef]

- Shahbaz, M.; Khan, S.; Tahir, M.I. The dynamic links between energy consumption, economic growth, financial development and trade in china: Fresh evidence from multivariate framework analysis. Energy Econ. 2013, 40, 8–21. [Google Scholar] [CrossRef]

- Shahbaz, M.; Hoang, T.H.V.; Mahalik, M.K.; Roubaud, D. Energy consumption, financial development and economic growth in india: New evidence from a nonlinear and asymmetric analysis. Energy Econ. 2017, 63, 199–212. [Google Scholar] [CrossRef] [Green Version]

- Khan, S.; Peng, Z.; Li, Y. Energy consumption, environmental degradation, economic growth and financial development in globe: Dynamic simultaneous equations panel analysis. Energy Rep. 2019, 5, 1089–1102. [Google Scholar] [CrossRef]

- China Statistical Yearbook. Available online: http://www.stats.gov.cn/tjsj/ndsj/ (accessed on 18 September 2020).

- Wang, S.; Li, Q.; Fang, C.; Zhou, C. The relationship between economic growth, energy consumption, and CO2 emissions: Empirical evidence from China. Sci. Total Environ. 2015, 542 Pt A, 360–371. [Google Scholar] [CrossRef]

- Liu, Y.; Hao, Y. The dynamic links between CO2, emissions, energy consumption and economic development in the countries along “the belt and road”. Sci. Total Environ. 2018, 645, 674–683. [Google Scholar] [CrossRef]

- Hao, Y.; Wang, L.; Zhu, L.; Ye, M. The dynamic relationship between energy consumption, investment and economic growth in china\”s rural area: New evidence based on provincial panel data. Energy 2018, 154, 374–382. [Google Scholar] [CrossRef]

- Acheampong, A.O. Economic growth, CO2 emissions and energy consumption: What causes what and where? Energy Econ. 2018, 74, 677–692. [Google Scholar] [CrossRef]

- Gozgor, G.; Chi, K.M.L.; Zhou, L. Energy consumption and economic growth: New evidence from the oecd countries. Energy 2018, 153, 27–34. [Google Scholar] [CrossRef] [Green Version]

- Song, M.; Wang, S.; Yu, H.; Yang, L.; Wu, J. To reduce energy consumption and to maintain rapid economic growth: Analysis of the condition in china based on expended ipat model. Renew. Sustain. Energy Rev. 2011, 15, 5129–5134. [Google Scholar] [CrossRef]

- Yuan, C.; Liu, S.; Fang, Z.; Xie, N. The relation between Chinese economic development and energy consumption in the different periods. Energy Policy 2010, 38, 5189–5198. [Google Scholar] [CrossRef]

- Shahbaz, M.; Zakaria, M.; Shahzad, S.J.H.; Mahalik, M.K. The energy consumption and economic growth nexus in top ten energy-consuming countries: Fresh evidence from using the quantile-on-quantile approach. Energy Econ. 2018, 71, 282–301. [Google Scholar] [CrossRef] [Green Version]

- Aydin, C.; Esen, Ö. Does the level of energy intensity matter in the effect of energy consumption on the growth of transition economies? Evidence from dynamic panel threshold analysis. Energy Econ. 2017, 69, 185–195. [Google Scholar] [CrossRef]

- Bekun, F.V.; Emir, F.; Sarkodie, S.A. Another look at the relationship between energy consumption, carbon dioxide emissions, and economic growth in South Africa. Sci. Total Environ. 2019, 655, 759–765. [Google Scholar] [CrossRef]

- King, R.G.; Levine, R. Finance and growth: Schumpeter might be right. Q. J. Econ. 1993, 108, 717–738. [Google Scholar] [CrossRef]

- Yang, F. The impact of financial development on economic growth in middle-income countries. J. Int. Financ. Mark. Inst. Money 2019, 59, 74–89. [Google Scholar] [CrossRef]

- Diallo, B.; Al-Titi, O. Local Growth and Access to Credit: Theory and Evidence. J. Macroecon. 2017, 54, 410–423. [Google Scholar] [CrossRef]

- Wang, C.; Zhang, X.; Ghadimi, P.; Liu, Q.; Lim, M.K.; Stanley, H.E. The impact of regional financial development on economic growth in Beijing–Tianjin–Hebei region: A spatial econometric analysis. Phys. A Stat. Mech. Appl. 2019, 521, 635–648. [Google Scholar] [CrossRef]

- Sassi, S.; Gasmi, A. The effect of enterprise and household credit on economic growth: New evidence from European union countries. J. Macroecon. 2014, 39, 226–231. [Google Scholar] [CrossRef]

- Ouyang, Y.; Li, P. On the nexus of financial development, economic growth, and energy consumption in China: New perspective from a GMM panel VAR approach. Energy Econ. 2018, 71, 238–252. [Google Scholar] [CrossRef]

- Liu, G.; Zhang, C. Does financial structure matter for economic growth in China. China Econ. Review. 2018, 61, 1–19. [Google Scholar] [CrossRef]

- Law, S.H.; Singh, N. Does too much finance harm economic growth? J. Bank. Financ. 2014, 41, 36–44. [Google Scholar] [CrossRef] [Green Version]

- Guender, A.V. Credit Prices vs. Credit Quantities as Predictors of Economic Activity in Europe: Which Tell a Better Story? J. Macroecon. 2018, 57, 380–399. [Google Scholar] [CrossRef] [Green Version]

- Yang, Y. Financial Development and Economic Growth: Based on China’s Financial Development as Threshold Variable. J. Financ. Res. 2014, 404, 59–71. [Google Scholar]

- Chen, K.C.; Wu, L.; Wen, J. The relationship between finance and growth in china. Glob. Financ. J. 2013, 24, 1–12. [Google Scholar] [CrossRef]

- Huang, H.C.; Lin, S.C. Non-linear finance–growth nexus: A threshold with instrumental variable approach. Econ. Transit. 2009, 17, 439–466. [Google Scholar] [CrossRef]

- Al-Mulali, U.; Sab, C.N. The impact of energy consumption and co2 emission on the economic and financial development in 19 selected countries. Renew. Sustain. Energy Rev. 2012, 16, 4365–4369. [Google Scholar] [CrossRef]

- Komal, R.; Abbas, F. Linking financial development, economic growth and energy consumption in pakistan. Renew. Sustain. Energy Rev. 2015, 44, 211–220. [Google Scholar] [CrossRef]

- Mirza, F.M.; Kanwal, A. Energy consumption, carbon emissions and economic growth in pakistan: Dynamic causality analysis. Renew. Sustain. Energy Rev. 2017, 72, 1233–1240. [Google Scholar] [CrossRef]

- Hansen, B.E. Threshold effects in non-dynamic panels: Estimation, testing, and inference. J. Econ. 1999, 93, 345–368. [Google Scholar] [CrossRef] [Green Version]

- LeSage, J.; Pace, R.K. Introduction to Spatial Econometrics; Peking University Press: Beijing, China, 2014; pp. 50–52. [Google Scholar]

- Tobler, W.R. A computer movie simulating urban growth in the detroit region. Econ. Geogr. 1970, 46, 234–240. [Google Scholar] [CrossRef]

- Moran, P.A.P. Notes on continuous stochastic phenomena. Biometrika 1950, 37, 17–23. [Google Scholar] [CrossRef] [PubMed]

- Anselin, L.; Bera, A.K.; Florax, R.; Yoon, M.J. Simple diagnostic tests for spatial dependence. Reg. Sci. Urban Econ. 1996, 26, 77–104. [Google Scholar] [CrossRef]

| Type | OLS | SAR | SEM | SDM | ||||

|---|---|---|---|---|---|---|---|---|

| Model (1) | Model (2) | Model (3) | Model (4) | Model (5) | Model (6) | Model (7) | Model (8) | |

| lnEC | 0.199 *** | −0.041 | 0.175 *** | 0.123 *** | ||||

| lnFD | 0.283 *** | 0.228 *** | 0.172 *** | 0.181 *** | ||||

| lnEC*lnFD | 0.024 *** | 0.016 *** | 0.020 *** | 0.018 *** | ||||

| lnK | 0.244 *** | 0.228 *** | 0.038 *** | 0.040 ** | 0.032 ** | 0.023 ** | 0.051 *** | 0.035 *** |

| lnL | 0.524 *** | 0.528 *** | 0.111 *** | 0.097 *** | 0.087 *** | 0.082 *** | 0.094 *** | 0.073 *** |

| lnOpen | 0.027 *** | 0.033 *** | 0.003* | 0.008 *** | 0.020 *** | 0.017 *** | 0.018 *** | 0.026 *** |

| lnFis | −0.150 *** | −0.104 *** | 0.178 *** | 0.194 *** | 0.202 *** | 0.263 *** | 0.158 *** | 0.210 *** |

| constant | 0.373 *** | 2.402 *** | ||||||

| W * lnEC | −0.485 *** | |||||||

| W * lnFD | 0.003 | |||||||

| W * (lnEC * lnFD) | −0.0118 *** | |||||||

| W * lnK | −0.403 * | −0.067 ** | ||||||

| W * lnL | −0.013 | 0.0272 | ||||||

| W * lnOpen | −0.022 *** | −0.021 *** | ||||||

| W * lnFis | 0.034 | −0.071 * | ||||||

| 0.232 *** | 0.245 *** | 0.843 *** | 0.714 *** | 0.499 *** | 0.650 *** | |||

| Sigma2 | 0.001 *** | 0.001 *** | 0.001 *** | 0.001 *** | 0.001 *** | 0.001 *** | ||

| Adj R2 | 0.973 | 0.974 | 0.986 | 0.983 | 0.977 | 0.981 | 0.989 | 0.983 |

| Log-L | 636.693 | 618.868 | 638.833 | 642.638 | 700.557 | 661.966 | ||

| Type | Independent Model | Synergistic Model | ||||

|---|---|---|---|---|---|---|

| Direct Effect | Indirect Effect | Total Effect | Direct Effect | Indirect Effect | Total Effect | |

| lnEC | 0.061 * | −0.759 *** | −0.698 *** | |||

| lnFD | 0.194 *** | 0.163 *** | 0.357 *** | |||

| lnEC*lnFD | 0.018 *** | 0.000 | 0.018 *** | |||

| lnK | 0.050 *** | −0.024 | 0.027 | 0.023 * | −0.116 * | −0.093 |

| lnL | 0.099 *** | 0.059 | 0.158 ** | 0.092 *** | 0.187 ** | 0.279 *** |

| lnOpen | 0.017 *** | −0.022 *** | −0.005 * | 0.025 *** | −0.010 * | 0.014 ** |

| lnFis | 0.174 *** | 0.204 *** | 0.378 *** | 0.226 *** | 0.167 * | 0.392 *** |

| Variables | Fe (Robust) | Fe (Ordinary) | OLS | EC Threshold | FD Threshold |

|---|---|---|---|---|---|

| FD/EC (qit ≤ γ1) | 0.283 *** | 0.059 | |||

| FD/EC (γ1 < qit ≤ γ2) | 0.288 *** | 0.067 | |||

| FD/EC (qit < γ2) | 0.292 *** | 0.073 ** | |||

| lnEC | −0.139 * | −0.139 *** | 0.199 ** | ||

| lnFD | 0.306 *** | 0.306 *** | 0.283 *** | ||

| lnK | 0.024 | 0.024 | 0.244 *** | 0.021 | 0.045 *** |

| lnL | 0.143 *** | 0.143 *** | 0.524 *** | 0.154 *** | 0.113 *** |

| lnOpen | 0.003 | 0.003 | 0.027 *** | 0.006 *** | 0.010 *** |

| lnFis | 0.273 *** | 0.273 *** | −0.151 | 0.232 *** | 0.457 *** |

| constant | 4.438 *** | 4.438 *** | 0.373 | 3.577 *** | 3.931 *** |

| R2 | 0.984 | 0.984 | 0.974 | 0.985 | 0.982 |

| F | 602.65 *** | 135.22 *** | 513.67 *** | 131.19 *** | 129.67 *** |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhou, H.; Qu, S.; Yuan, Q.; Wang, S. Spatial Effects and Nonlinear Analysis of Energy Consumption, Financial Development, and Economic Growth in China. Energies 2020, 13, 4982. https://doi.org/10.3390/en13184982

Zhou H, Qu S, Yuan Q, Wang S. Spatial Effects and Nonlinear Analysis of Energy Consumption, Financial Development, and Economic Growth in China. Energies. 2020; 13(18):4982. https://doi.org/10.3390/en13184982

Chicago/Turabian StyleZhou, Huan, Shaojian Qu, Qinglu Yuan, and Shilei Wang. 2020. "Spatial Effects and Nonlinear Analysis of Energy Consumption, Financial Development, and Economic Growth in China" Energies 13, no. 18: 4982. https://doi.org/10.3390/en13184982