Structural Vector Autoregressive Approach to Evaluate the Impact of Electricity Generation Mix on Economic Growth and CO2 Emissions in Iran

Abstract

:1. Introduction

- How does electricity generated by renewable sources contribute to the economic growth of Iran?

- How is carbon dioxide affected by unit standard deviation shock of renewable electricity?

- What is the contribution of renewable electricity in explaining forecast error variance decomposition of economic growth and carbon dioxide emissions?

- What is an appropriate energy policy for Iran as an energy driven country?

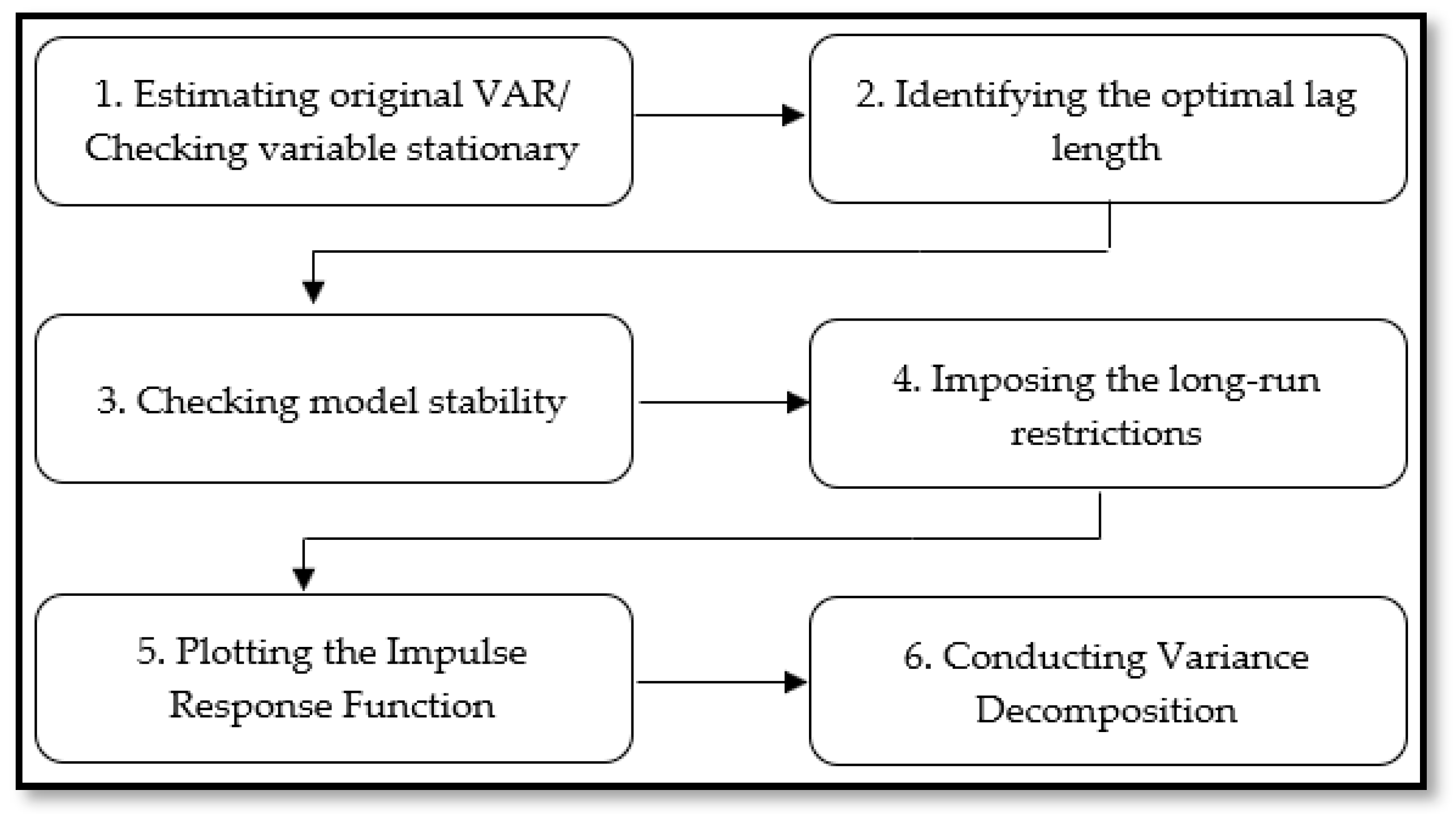

2. Methodology

- Checking variables stationary through conducting KPSS unit root tests [29] and estimating the original VAR model.

- Identifying the optimal lag length using several criteria.

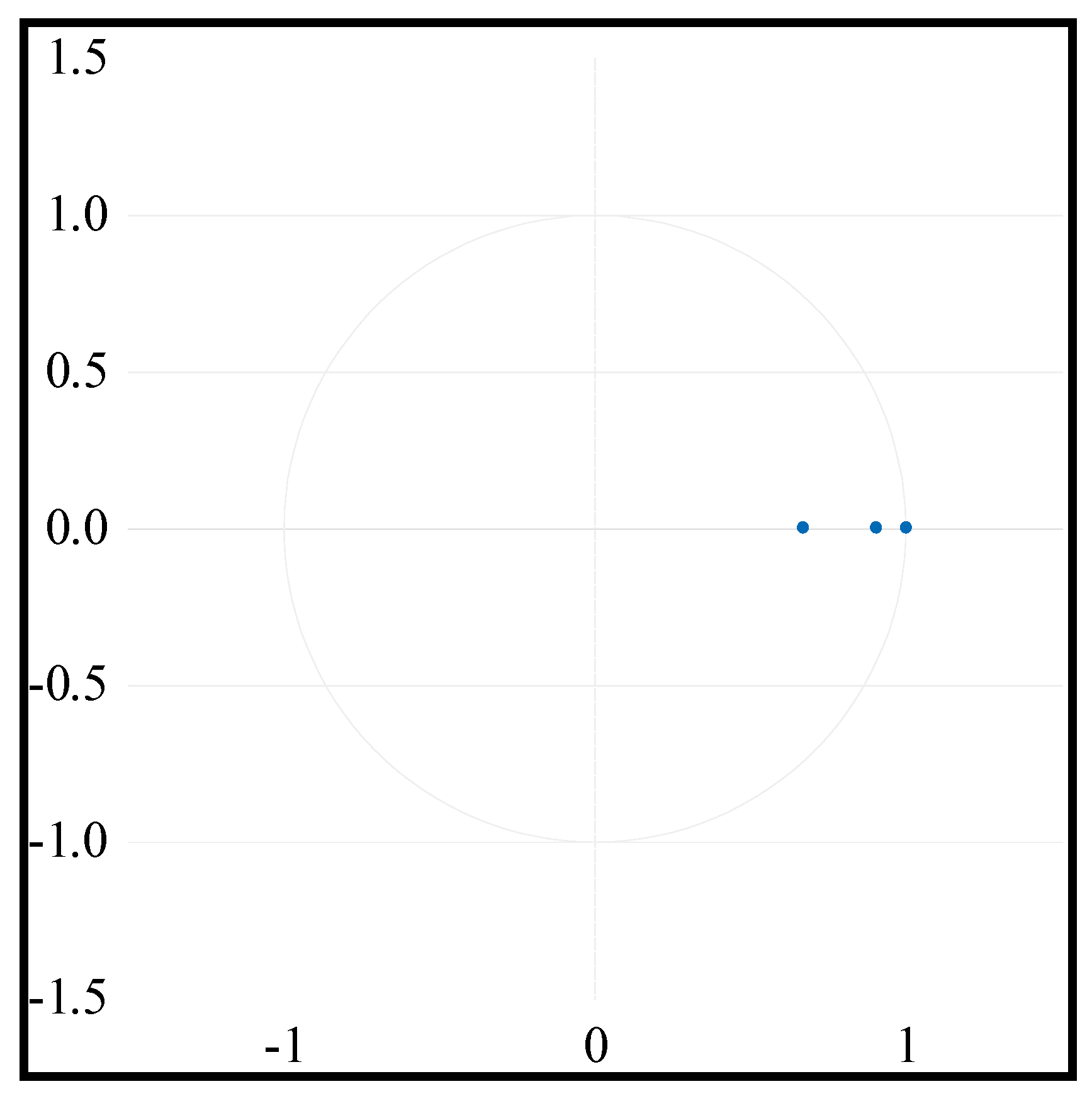

- Checking model stability by employing inverse roots of the characteristic polynomials.

- Imposing the Blanchard and Quah long-run restrictions [30] based on the literature review and economic theory.

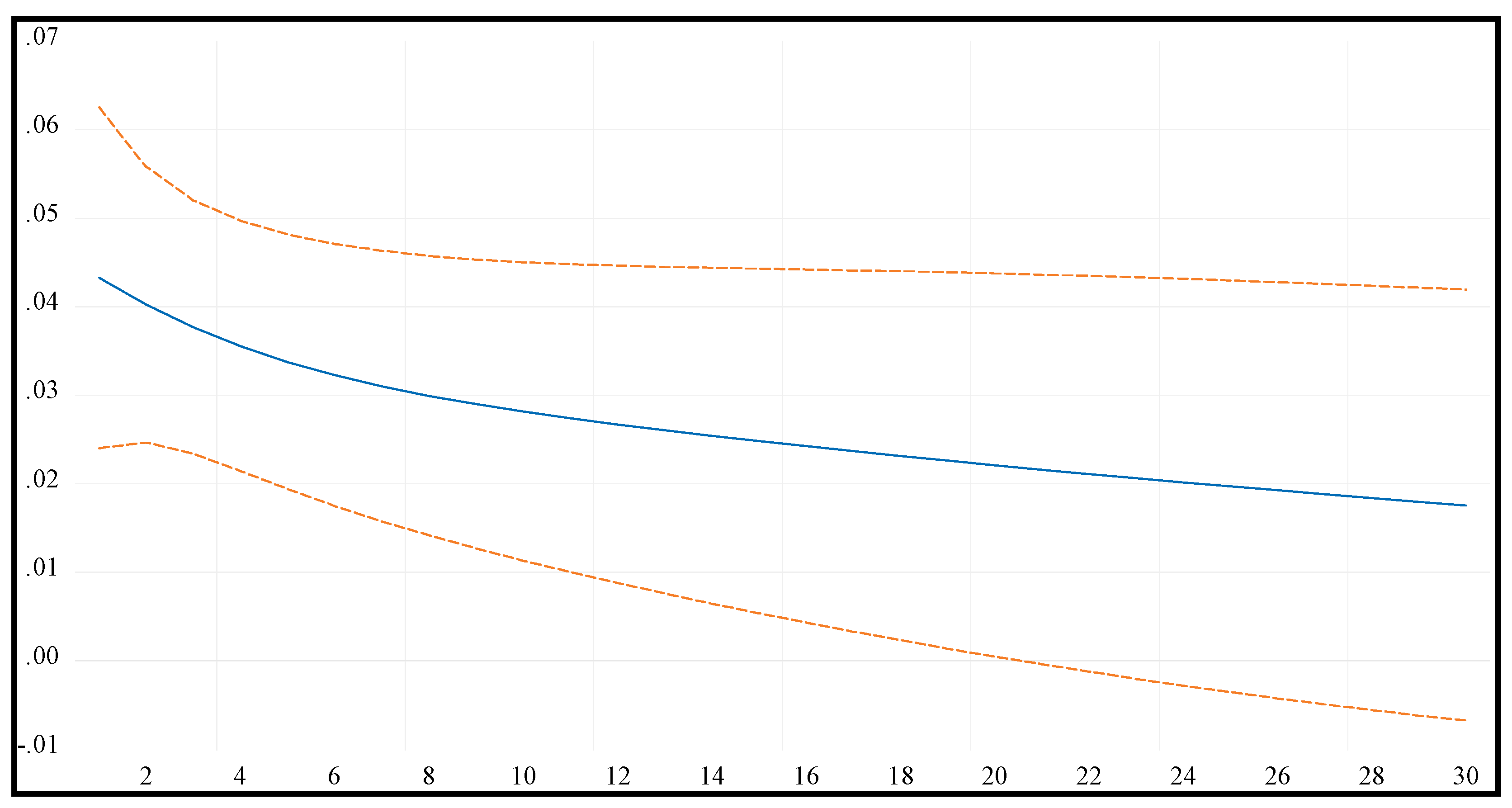

- Plotting the IRFs to consider the dynamic responses of endogenous variables to a unit standard deviation shock of some of the other variables in the system over time.

- Conducting VD to identify the importance of each exogenous shock in explaining the forecast error variance of each variable.

2.1. Structural Vector Autoregressive Model

2.2. Imposing Long-Run Restrictions

2.3. Model Specification

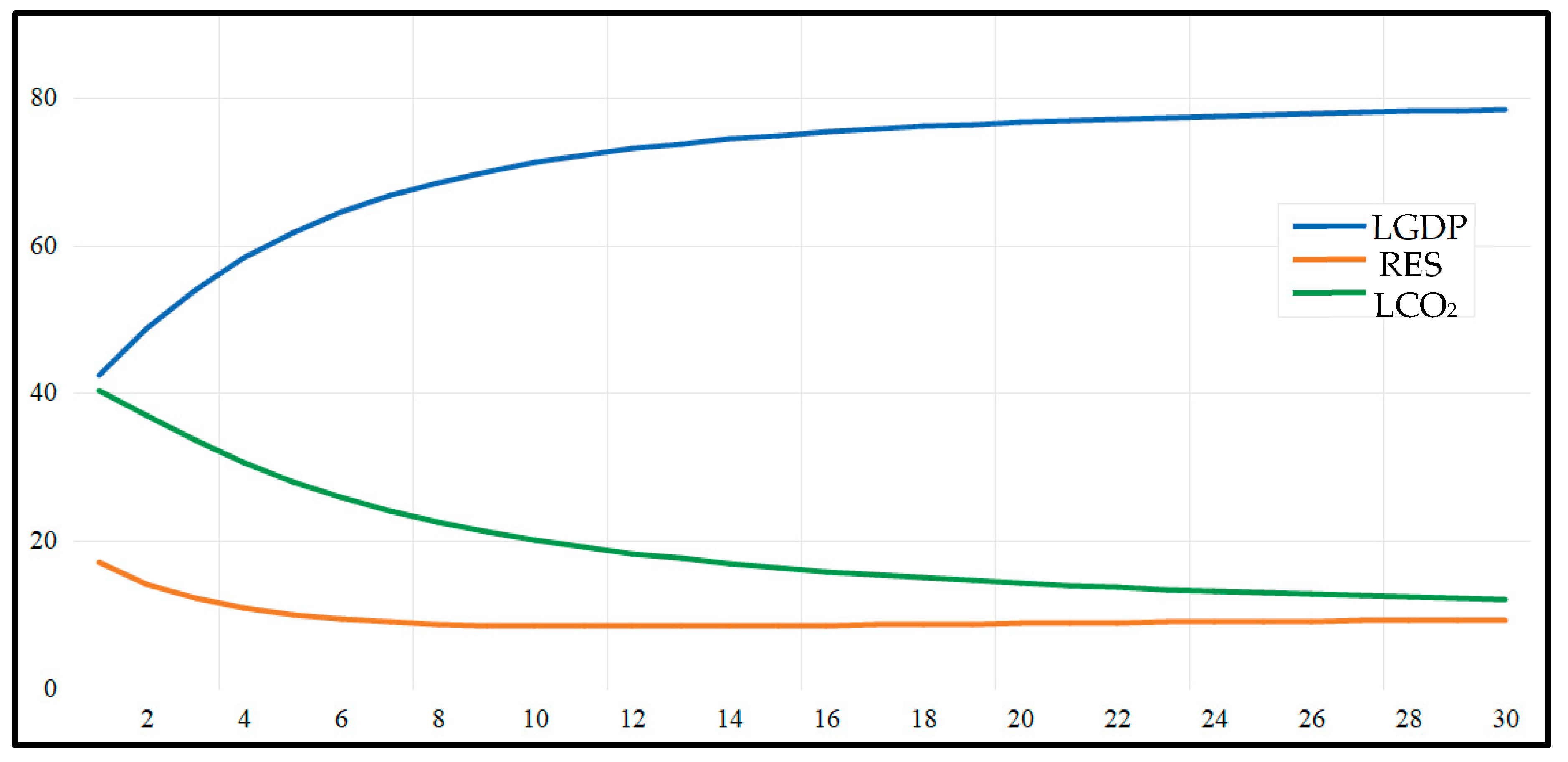

3. Data and Empirical Finding

3.1. Data

3.2. Empirical Findings

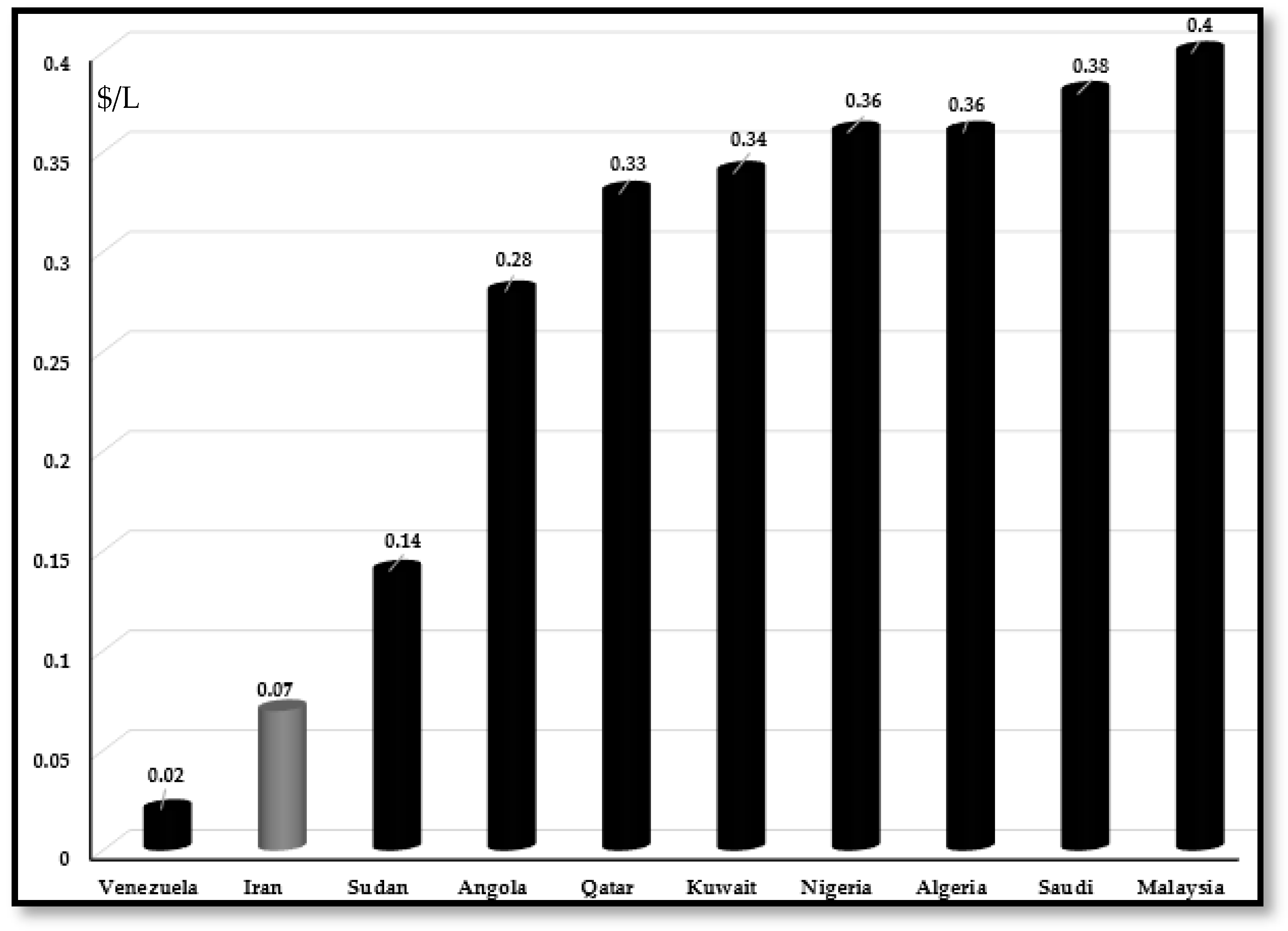

- Low gasoline and diesel prices (Figure 6 and Figure 7) caused by widespread supply of combustible fuels and allocating significant subsidies to them. Based on the report of IEA entitled “World Energy Outlook 2018”, allocating $69 billion for fossil fuels ($26.6 billion, $26 billion, and $16.6 billion for oil, natural gas, and electricity, respectively), Iran ranks as the world’s largest country in terms of allocating fossil fuel consumption subsidies. This amount accounts for 15 percent of total GDP [39].

- The low share of renewable energy in the energy mix and electricity generation [21] despite its high potential.

- The lack of access to advanced renewable technologies, which is caused by imposing sanctions.

- Failure to invest in energy savings and reduce energy intensity due to financial difficulties, which are partially caused by the sanctions.

4. Conclusions and Policy Implication

Author Contributions

Funding

Conflicts of Interest

Abbreviations

| AIC | Akaike Information Criterion |

| ARDL | Autoregressive Distributed Lag |

| CCR | Canonical Co-integration Regression |

| CD | Cholesky Decomposition |

| CO2 | Carbon Dioxide |

| CR | Croux and Reusens test |

| DH PC | Dumitrescu–Hurlin Panel Causality test |

| DOLS | Dynamic Least Square |

| EKC | Environmental Kuznets Curve |

| FMOLS | Fully Modified Least Square |

| FPE | Final Prediction Error |

| GDP | Gross Domestic Production |

| HQ | Hannan–Quinn Information Criterion |

| IRF | Impulse Response Function |

| LRT | Likelihood-Ratio test |

| LR | Long-run |

| PMG-ARDL | Panel Pooled Mean Group-Autoregressive Autoregressive Distributive Lag Model |

| SC | Schwartz Information Criterion |

| SR | Short run |

| SVAR | Structural Vector Autoregressive model |

| VAR | Vector Autoregressive |

| VD | Variance Decomposition |

| VECM | Vector Error Correction Model |

References

- Lin, B.; Zhu, J. The role of renewable energy technological innovation on climate change: Empirical evidence from China. Sci. Total. Environ. 2019, 659, 1505–1512. [Google Scholar] [CrossRef] [PubMed]

- Sadeghi, A.; Larimian, T. Sustainable electricity generation mix for Iran: A fuzzy analytic network process approach. Sustain. Energy Technol. Assess. 2018, 28, 30–42. [Google Scholar] [CrossRef]

- Zhixin, Z.; Xin, R. Causal Relationships between Energy Consumption and Economic Growth. Energy Procedia 2011, 5, 2065–2071. [Google Scholar] [CrossRef] [Green Version]

- Bowden, N.; Payne, J.E. Sectoral Analysis of the Causal Relationship Between Renewable and Non-Renewable Energy Consumption and Real Output in the US. Energy Sources Part B Econ. Plan. Policy 2010, 5, 400–408. [Google Scholar] [CrossRef]

- Kuznets, S. Economic growth and income inequality. Am. Econ. Rev. 1955, 45, 1–28. [Google Scholar]

- Grossman, G.; Krueger, A. Environmental Impacts of a North American Free Trade Agreement. Env. Impacts N. Am. Free Trade Agreem. 1991. [Google Scholar] [CrossRef]

- Shafik, N.; Bandyopadhyay, S. Economic Growth and Environmental Quality: Time-Series and Cross-Country Evidence; World Bank Publications: Washington, DC, USA, 1992; Volume 904. [Google Scholar]

- Panayotou, T. Empirical Tests and Policy Analysis of Environmental Degradation at Different Stages of Economic Development; International Labour Organization: Geneva, Switzerland, 1993. [Google Scholar]

- Selden, T.M.; Song, D. Environmental Quality and Development: Is There a Kuznets Curve for Air Pollution Emissions? J. Environ. Econ. Manag. 1994, 27, 147–162. [Google Scholar]

- Nourry, M. Measuring sustainable development: Some empirical evidence for France from eight alternative indicators. Ecol. Econ. 2008, 67, 441–456. [Google Scholar] [CrossRef]

- Tiwari, A.K. A structural VAR analysis of renewable energy consumption, real GDP and CO2 emissions: Evidence from India. Econ. Bull. 2011, 31, 1793–1806. [Google Scholar]

- Silva, S.; Soares, I.; Pinho, C. The Impact of Renewable Energy Sources on Economic Growth and CO2 Emissions: A SVAR approach. Eur. Res. Stud. J. 2012, 15, 133–144. [Google Scholar] [CrossRef] [Green Version]

- Onafowora, O.A.; Owoye, O. Structural vector auto regression analysis of the dynamic effects of shocks in renewable electricity generation on economic output and carbon dioxide emissions: China, India and Japan. Int. J. Energy Econ. Policy 2015, 5, 1022–1032. [Google Scholar]

- Al-Mulali, U.; Saboori, B.; Ozturk, I. Investigating the environmental Kuznets curve hypothesis in Vietnam. Energy Policy 2015, 76, 123–131. [Google Scholar] [CrossRef]

- Al-Mulali, U.; Tang, C.F.; Ozturk, I. Estimating the Environment Kuznets Curve hypothesis: Evidence from Latin America and the Caribbean countries. Renew. Sustain. Energy Rev. 2015, 50, 918–924. [Google Scholar] [CrossRef]

- Ahmed, K.; Mahalik, M.K.; Shahbaz, M. Dynamics between economic growth, labor, capital and natural resource abundance in Iran: An application of the combined cointegration approach. Resour. Policy 2016, 49, 213–221. [Google Scholar] [CrossRef]

- Ito, K. CO2 emissions, renewable and non-renewable energy consumption, and economic growth: Evidence from panel data for developing countries. Int. Econ. 2017, 151, 1–6. [Google Scholar] [CrossRef]

- Pata, U.K. Renewable energy consumption, urbanization, financial development, income and CO2 emissions in Turkey: Testing EKC hypothesis with structural breaks. J. Clean. Prod. 2018, 187, 770–779. [Google Scholar] [CrossRef]

- Hdom, H.A.D. Examining carbon dioxide emissions, fossil & renewable electricity generation and economic growth: Evidence from a panel of South American countries. Renew. Energy 2019, 139, 186–197. [Google Scholar]

- Bekun, F.V.; Alola, A.A.; Sarkodie, S.A. Toward a sustainable environment: Nexus between CO2 emissions, resource rent, renewable and nonrenewable energy in 16-EU countries. Sci. Total. Environ. 2019, 657, 1023–1029. [Google Scholar] [CrossRef]

- Dudley, B. BP Statistical Review of World Energy; BP p.l.c.: London, UK, 2018; Volume 6, Available online: https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/energy-economics/statistical-review/bp-stats-review-2018-full-report.pdf (accessed on 8 June 2020).

- Fadai, D.; Esfandabadi, Z.S.; Abbasi, A. Analyzing the causes of non-development of renewable energy-related industries in Iran. Renew. Sustain. Energy Rev. 2011, 15, 2690–2695. [Google Scholar] [CrossRef]

- Sims, C.A. Macroeconomics and Reality. Econometrica 1980, 48, 1. [Google Scholar] [CrossRef] [Green Version]

- Elbourne, A. The UK housing market and the monetary policy transmission mechanism: An SVAR approach. J. Hous. Econ. 2008, 17, 65–87. [Google Scholar] [CrossRef]

- Bernanke, B.S. Alternative Explanations of the Money-Income Correlation; National Bureau of Economic Research: Cambridge, MA, USA, 1986. [Google Scholar]

- Blanchard, O.; Watson, M. Are business cycles all alike? In The American Business Cycle: Continuity and Change; University of Chicago Press: Chicago, IL, USA, 1986; pp. 123–180. [Google Scholar]

- Sims, C.A. Are Forecasting Models Usable for Policy Analysis? Q. Rev. 1986, 10, 2–16. [Google Scholar] [CrossRef]

- Clarida, R.; Galí, J. Sources of real exchange-rate fluctuations: How important are nominal shocks. In Carnegie-Rochester Conference Series on Public Policy; Elsevier: Amsterdam, The Netherlands, 1994; Volume 41, pp. 1–56. [Google Scholar]

- Kwiatkowski, D.; Phillips, P.C.; Schmidt, P.; Shin, Y. Testing the null hypothesis of stationarity against the alternative of a unit root. J. Econ. 1992, 54, 159–178. [Google Scholar] [CrossRef]

- Blanchard, O.J.; Quah, D. The Dynamic Effects of Aggregate Demand and Supply Disturbances; National Bureau of Economic Research: Cambridge, MA, USA, 1988. [Google Scholar]

- Lütkepohl, H. New Introduction to Multiple Time Series Analysis; Springer: Berlin/Heidelberg, Germany, 2005. [Google Scholar]

- Amisano, G.; Giannini, C. From var models to structural var models. In Topics in Structural VAR Econometrics; Springer: Berlin/Heidelberg, Germany, 1997; pp. 1–28. [Google Scholar]

- Lütkepohl, H. Estimation of structural vector autoregressive modelsCommun. Stat. Appl. Methods 2017, 24, 421–441. [Google Scholar]

- Kilian, L.; Lütkepohl, H. Structural Vector Autoregressive Analysis; Cambridge University Press: Cambridge, MA, USA, 2017. [Google Scholar]

- World Bank Open Data. Available online: http://data.worldbank.org/indicator (accessed on 8 June 2020).

- U.S. Energy Information Administration. Available online: https://www.eia.gov/beta/international/analysis (accessed on 8 June 2020).

- Tiwari, A.K. Globalization and wage inequality: A revisit of empirical evidences with new approach. J. Asian Bus. Manag. 2010, 2, 173–187. [Google Scholar]

- Maslyuk, S.; Dharmaratna, D. Renewable Electricity Generation, CO2 Emissions and Economic Growth: Evidence from Middle-Income Countries in Asia. Stud. Appl. Econ. 2020, 31, 217–244. [Google Scholar] [CrossRef]

- International Energy Agency. IEA World Energy Outlook; IEA OECD: Paris, France, 2018. [Google Scholar]

- Global Petrol Price. Available online: www.Globalpetrolprices.Com (accessed on 13 July 2020).

- Mirza, U.K.; Ahmad, N.; Harijan, K.; Majeed, T. Identifying and addressing barriers to renewable energy development in Pakistan. Renew. Sustain. Energy Rev. 2009, 13, 927–931. [Google Scholar] [CrossRef]

- Pegels, A. Renewable energy in South Africa: Potentials, barriers and options for support. Energy Policy 2010, 38, 4945–4954. [Google Scholar] [CrossRef]

- Rezaee, M.J.; Yousefi, S.; Hayati, J. Root barriers management in development of renewable energy resources in Iran: An interpretative structural modeling approach. Energy Policy 2019, 129, 292–306. [Google Scholar] [CrossRef]

- Bezir, N.Ç.; Murat, Ö.; Nuri, Ö. Renewable energy market conditions and barriers in Turkey. Renew. Sustain. Energy Rev. 2009, 13, 1428–1436. [Google Scholar]

- Ansari, F.; Kharb, R.K.; Luthra, S.; Shimmi, S.; Chatterji, S. Analysis of barriers to implement solar power installations in India using interpretive structural modeling technique. Renew. Sustain. Energy Rev. 2013, 27, 163–174. [Google Scholar] [CrossRef]

- Eleftheriadis, I.M.; Anagnostopoulou, E. Identifying barriers in the diffusion of renewable energy sources. Energy Policy 2015, 80, 153–164. [Google Scholar] [CrossRef]

- Luthra, S.; Kumar, S.; Garg, D.; Haleem, A. Barriers to renewable/sustainable energy technologies adoption: Indian perspective. Renew. Sustain. Energy Rev. 2015, 41, 762–776. [Google Scholar] [CrossRef]

- Ghimire, L.P.; Kim, Y.; Kim, Y. An analysis on barriers to renewable energy development in the context of Nepal using AHP. Renew. Energy 2018, 129, 446–456. [Google Scholar] [CrossRef]

- Shah, S.A.A.; Solangi, Y.A.; Ikram, M. Analysis of barriers to the adoption of cleaner energy technologies in Pakistan using Modified Delphi and Fuzzy Analytical Hierarchy Process. J. Clean. Prod. 2019, 235, 1037–1050. [Google Scholar] [CrossRef]

- Asante, D.; He, Z.; Adjei, N.O.; Asante, B. Exploring the barriers to renewable energy adoption utilising MULTIMOORA- EDAS method. Energy Policy 2020, 142, 111479. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Reference | Country (ies) | Methodology (ies) | Impact of Renewable Energy/Electricity on | |

|---|---|---|---|---|

| Economic Growth | CO2 Emissions | |||

| [11] | India | SVAR | + | − |

| [12] | The US, Denmark, Portugal, Spain | SVAR | − except for the US | − |

| [13] | China, India, Japan | SVAR | China (SR): − LR: + | |

| [14] | Vietnam | ARDL | No effect | |

| [15] | Latin American and the Caribbean countries | FMOLS, VECM Granger Causality | Feedback hypothesis | No effect |

| [16] | Iran | ARDL, VECM, DOLS, FMOLS | + | |

| [17] | 42 developing (Iran) | Panel Data | + | |

| [18] | Turkey | ARDL, FMOLS, CCR | No effect | |

| [19] | 8 South American | ARDL | − | |

| [20] | 16 EU-countries | PMG-ARDL | − | |

| RES | LGDP | LCO2 | |

|---|---|---|---|

| Mean | 9.575796 | 5.726277 | 5.689736 |

| Median | 7.264000 | 5.680259 | 5.680323 |

| Maximum | 22.45900 | 6.214520 | 6.467844 |

| Minimum | 3.662000 | 5.168314 | 4.695737 |

| Std. Dev. | 4.910548 | 0.327201 | 0.530751 |

| Skewness | 1.124100 | 0.038299 | −0.090554 |

| Kurtosis | 3.008702 | 1.706429 | 1.851405 |

| Jarque–Bera | 7.581718 | 2.518792 | 2.028106 |

| Probability | 0.022576 | 0.283825 | 0.362746 |

| Sum | 344.7286 | 206.1460 | 204.8305 |

| Sum Sq. Dev. | 843.9720 | 3.747111 | 9.859376 |

| Variable | KPSS Test Statistic | Stationary Order | |

|---|---|---|---|

| At Level | At 1st Difference | ||

| 0.616 | 0.356 | I (1) | |

| 0.714 | 0.046 | I (1) | |

| 0.727 | 0.240 | I (1) | |

| Lag | LRT | FPE | AIC | SC | HQ |

|---|---|---|---|---|---|

| 0 | NA | 0.013111 | 4.179277 | 4.315323 | 4.225052 |

| 1 | 186.0963 * | 3.71 × 10−5 * | −1.692383 * | −1.148199 * | −1.509282 * |

| 2 | 13.91959 | 3.81 × 10−5 | −1.682298 | −0.729975 | −1.361870 |

| 3 | 11.81004 | 4.09 × 10−5 | −1.650323 | −0.289862 | −1.192569 |

| Lag | Lagrange Multiplier Statistic | p-Value |

|---|---|---|

| 1 | 8.672702 | 0.4689 |

| 2 | 7.617272 | 0.5740 |

| 3 | 4.974177 | 0.8369 |

| 4 | 7.148563 | 0.6224 |

| 5 | 5.737527 | 0.7664 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Oryani, B.; Koo, Y.; Rezania, S. Structural Vector Autoregressive Approach to Evaluate the Impact of Electricity Generation Mix on Economic Growth and CO2 Emissions in Iran. Energies 2020, 13, 4268. https://doi.org/10.3390/en13164268

Oryani B, Koo Y, Rezania S. Structural Vector Autoregressive Approach to Evaluate the Impact of Electricity Generation Mix on Economic Growth and CO2 Emissions in Iran. Energies. 2020; 13(16):4268. https://doi.org/10.3390/en13164268

Chicago/Turabian StyleOryani, Bahareh, Yoonmo Koo, and Shahabaldin Rezania. 2020. "Structural Vector Autoregressive Approach to Evaluate the Impact of Electricity Generation Mix on Economic Growth and CO2 Emissions in Iran" Energies 13, no. 16: 4268. https://doi.org/10.3390/en13164268