Do We Need Trust Transfer Mechanisms? An M-Commerce Adoption Perspective

Abstract

:1. Introduction

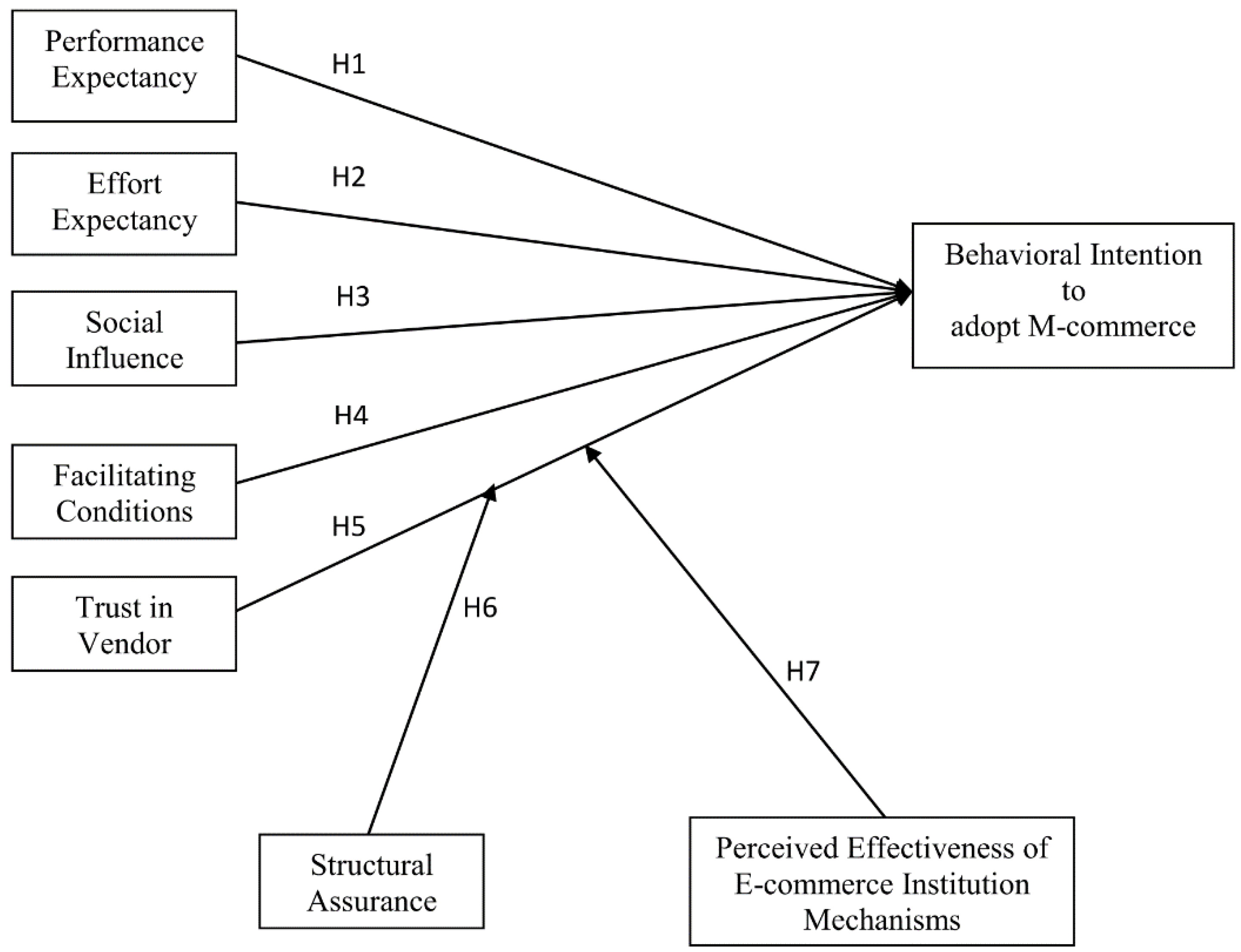

2. Literature Review and Hypotheses Development

2.1. UTAUT

2.2. Trust Transfer Theory

2.3. Institutional-Based Mechanism

2.4. Performance Expectancy

2.5. Effort Expectancy

2.6. Social Influence

2.7. Facilitating Conditions

2.8. Trust in Vendor

2.9. Perceived Effectiveness of E-Commerce Institutional Mechanisms (PEEIM) and Structural Assurance (SA)

3. Research Methodology

3.1. Data Collection and Sampling Procedure

3.2. Instrument Development

3.3. Demographic Characteristic of Respondents

4. Analysis of Data

4.1. Analysis of Measurement Model

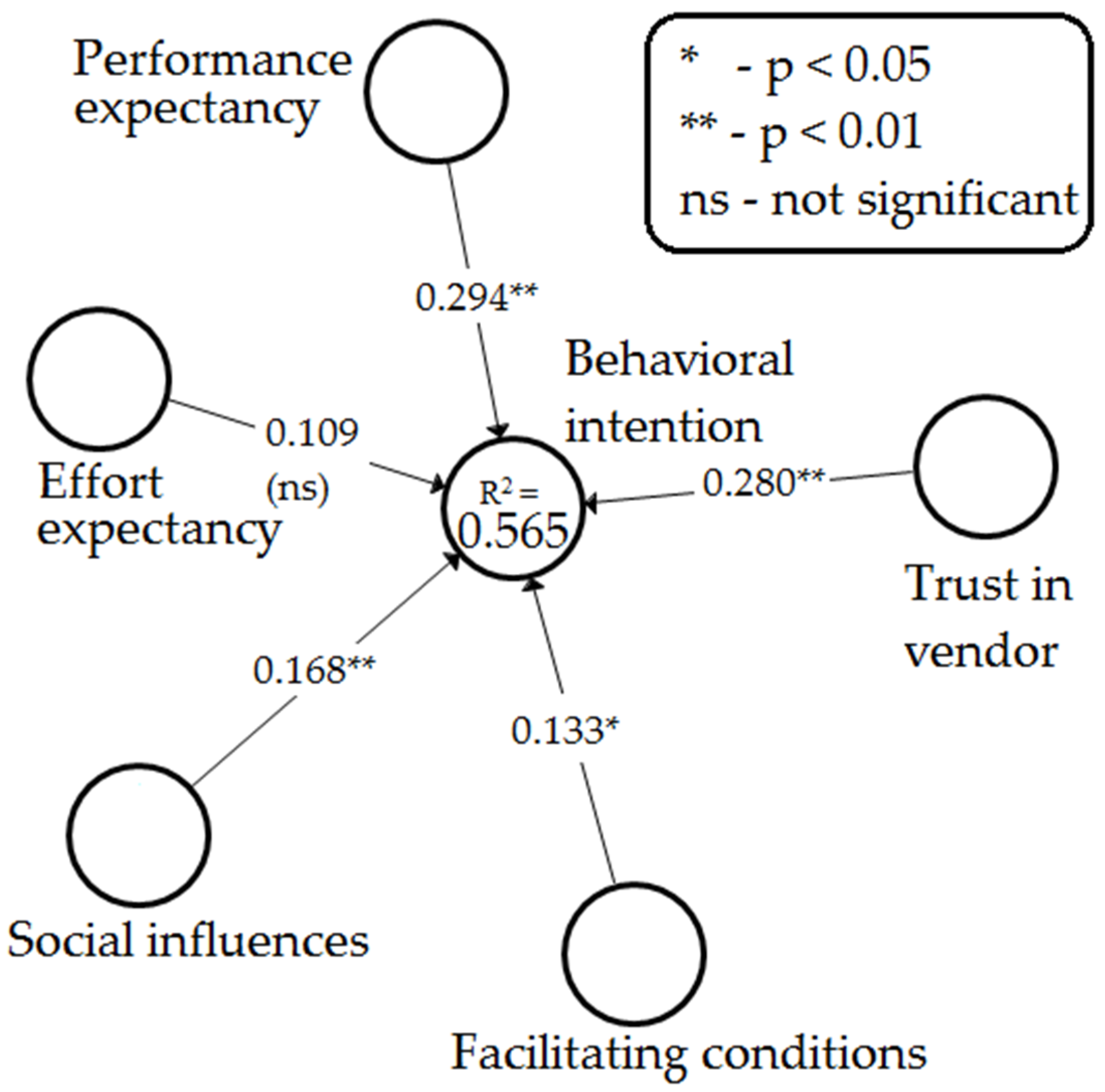

4.2. Analysis of Structural Model

4.3. Moderating Analysis

4.3.1. SA as the Moderator

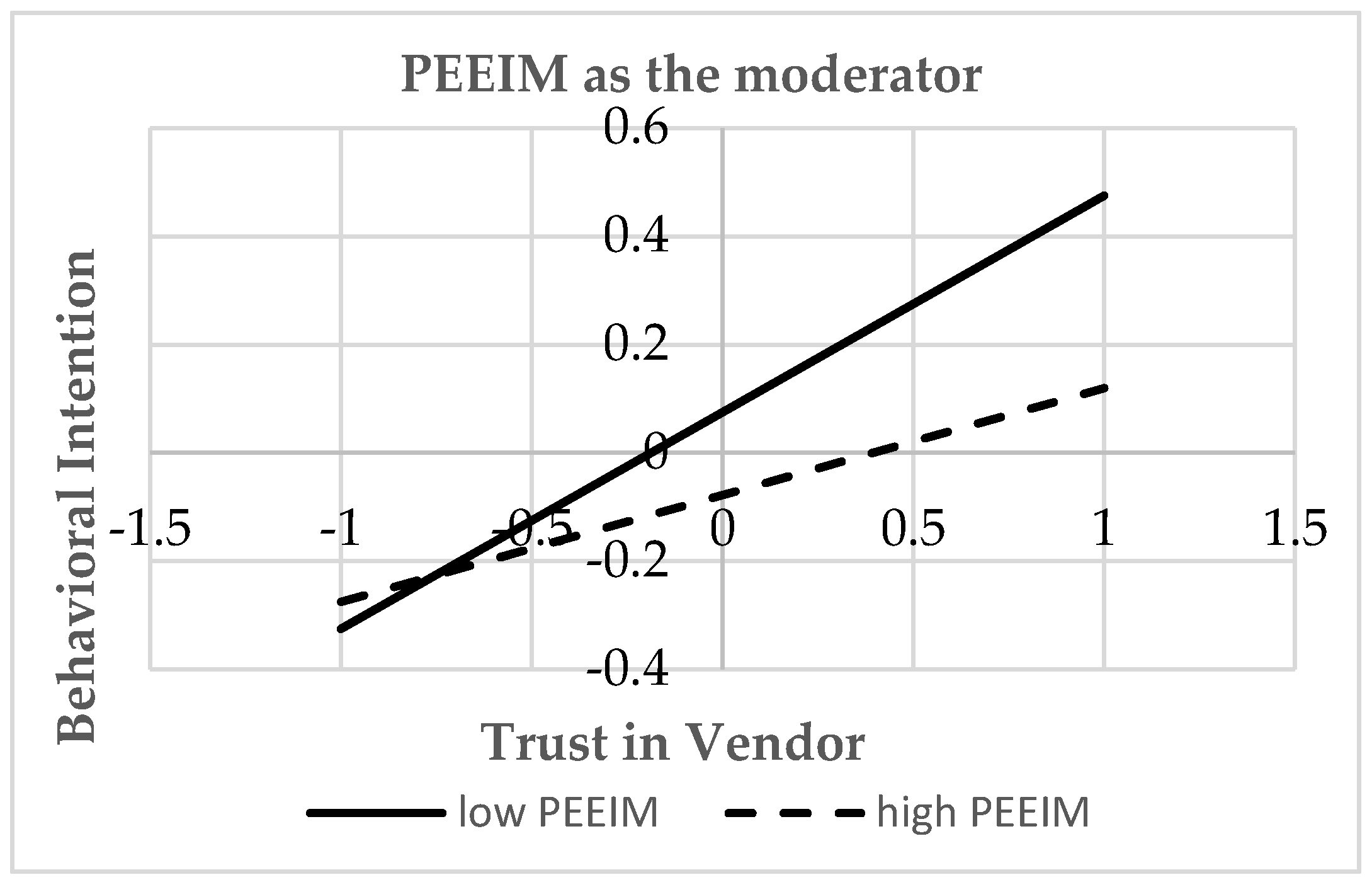

4.3.2. PEEIM as the Moderator

5. Discussion

6. Conclusions

6.1. Theoretical Implications

6.2. Managerial Implications

6.3. Limitations and Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

| Constructs | Items |

|---|---|

| Performance expectancy adapted from Venkatesh et al. (2012) | |

| PE1 | I find mobile commerce useful in my daily life. |

| PE2 | Using mobile commerce increases my chances of achieving things that are important to me. |

| PE3 | Using mobile commerce helps me accomplish things more quickly. |

| PE4 | Using mobile commerce increases my productivity. |

| Effort expectancy adapted from Venkatesh et al. (2012) | |

| EE1 | Learning how to use mobile commerce is easy for me. |

| EE2 | My interaction with mobile commerce is clear and understandable. |

| EE3 | I find mobile commerce easy to use. |

| EE4 | It is easy for me to become skillful at using mobile commerce. |

| Social influences adapted from Venkatesh et al. (2012) | |

| SI1 | People who are important to me think that I should use mobile commerce. |

| SI2 | People who influence my behavior think that I should use mobile commerce. |

| SI3 | People whose opinions that I value prefer that I use mobile commerce. |

| Facilitating conditions adapted from Venkatesh et al. (2012) | |

| FC1 | I have resource necessary to use mobile commerce. |

| FC2 | I have the knowledge necessary to use mobile commerce. |

| FC3 | Mobile commerce is compatible with other technologies I use. |

| FC4 | I can get help from others when I have difficulties using mobile commerce. |

| Perceived effectiveness of e-commerce institutional mechanisms adapted from Fang et al. (2014) | |

| PEEIM1 | When buying through smartphone, I am confident that there are mechanisms in place to protect me against any potential risks (eg. leaking of information, credit card fraud, goods not received, etc.) of online shopping if something goes wrong with my online mobile purchase. |

| PEEIM2 | I have confidence in third parties (eg. SafeTraders, TRUSTe) to protect me against any potential risks (eg. leaking of information, credit card fraud, goods not received, etc.) of online shopping if something goes wrong with my online mobile purchase. |

| PEEIM3 | I am sure that I cannot be taken advantage of (eg. leaking of information, credit card fraud, goods not received, etc.) of online shopping if something goes wrong with my online mobile purchase. |

| Trust in vendor adapted from Fang et al. (2014) | |

| TV1 | I believe that the online vendor is consistent in quality and service. |

| TV2 | I believe that the online vendor is keen on fulfilling my needs and wants. |

| TV3 | I believe that the online vendor is honest. |

| TV4 | I believe that the online vendor wants to be known as one that keeps promises and commitments. |

| TV5 | I believe that the online vendor has my best interests in mind. |

| TV6 | I believe that the online vendor is trustworthy. |

| TV7 | I believe that the online vendor has high integrity. |

| TV8 | I believe that the online vendor is dependable. |

| Structural assurance adapted from Gefen et al. (2003) | |

| SA1 | I feel safe conducting business with the online vendor because the authority will protect me. |

| SA2 | I feel safe conducting business with the online vendor because of it provides a 1-800 number. |

| SA3 | I feel safe conducting business with the online vendor because of its statements of guarantees. |

| SA4 | I feel safe conducting business with the online vendor because I accessed its site through a well-known, reputable portal. |

| Behavioral intention adapted from Venkatesh et al. (2012) | |

| BI1 | I intend to continue using mobile commerce in the future. |

| BI2 | I will always try to use mobile commerce in my daily life. |

| BI3 | I plan to continue to use mobile commerce frequently. |

References

- Xu, T. Development Analysis of O2O Model Based on Mobile Electronic Business. In Proceedings of the Fourth International Forum on Decision Sciences; Li, X., Xu, X., Eds.; Uncertainty and Operations Research; Springer: Singapore, 2017; pp. 507–516. ISBN 978-981-10-2919-6. [Google Scholar]

- Dabija, D.-C.; Lung, L. Millennials Versus Gen Z: Online Shopping Behaviour in an Emerging Market. In Applied Ethics for Entrepreneurial Success: Recommendations for the Developing World; Văduva, S., Fotea, I., Văduva, L.P., Wilt, R., Eds.; Springer Proceedings in Business and Economics; Springer International Publishing: Cham, Switzerland, 2019; pp. 1–18. ISBN 978-3-030-17214-5. [Google Scholar]

- Moorthy, K.; Johanthan, S.; Tham, C.; Xuan, K.X.; Yan, L.L.; Xunda, T.; Sim, T.C. Behavioural Intention to Use Mobile Apps by Gen Y in Malaysia. J. Inf. 2019, 5, 1–15. [Google Scholar] [CrossRef]

- Moorthy, K.; Chun T’ing, L.; Chea Yee, K.; Wen Huey, A.; Joe In, L.; Chyi Feng, P.; Jia Yi, T. What Drives the Adoption of Mobile Payment? A Malaysian Perspective. Int. J. Fin. Econ. 2020, 25, 349–364. [Google Scholar] [CrossRef]

- Global Mobile eCommerce Statistics, Trends & Forecasts (2020). Available online: https://www.merchantsavvy.co.uk/mobile-ecommerce-statistics/ (accessed on 3 September 2021).

- Digital 2020. Available online: https://wearesocial.com/digital-2020 (accessed on 5 July 2021).

- Hooi, R.T.S. E-Wallets to Carve up More Market. Available online: https://www.thestar.com.my/news/nation/2020/01/02/e-wallets-to-carve-up-more-market (accessed on 5 July 2021).

- Ecommerce in Malaysia in 2019. Available online: https://datareportal.com/reports/digital-2019-ecommerce-in-malaysia (accessed on 5 July 2021).

- Fang, Y.; Qureshi, I.; Sun, H.; McCole, P.; Ramsey, E.; Lim, K.H. Trust, Satisfaction, and Online Repurchase Intention: The Moderating Role of Perceived Effectiveness of E-Commerce Institutional Mechanisms. MIS Q. 2014, 38, 407–427. [Google Scholar] [CrossRef] [Green Version]

- Gao, L.; Waechter, K.A. Examining the Role of Initial Trust in User Adoption of Mobile Payment Services: An Empirical Investigation. Inf. Syst. Front. 2017, 19, 525–548. [Google Scholar] [CrossRef]

- Liu, Y.; Tang, X. The Effects of Online Trust-Building Mechanisms on Trust and Repurchase Intentions: An Empirical Study on EBay. Inf. Technol. People 2018, 31, 666–687. [Google Scholar] [CrossRef]

- Stouthuysen, K.; Teunis, I.; Reusen, E.; Slabbinck, H. Initial Trust and Intentions to Buy: The Effect of Vendor-Specific Guarantees, Customer Reviews and the Role of Online Shopping Experience☆. Electron. Commer. Res. Appl. 2018, 27, 23–38. [Google Scholar] [CrossRef]

- McKnight, D.H.; Chervany, N.L. What Trust Means in E-Commerce Customer Relationships: An Interdisciplinary Conceptual Typology. Int. J. Electron. Commer. 2001, 6, 35–59. [Google Scholar] [CrossRef]

- Huang, P.-C.; Hou, C.-C.; Chen, J.-S. Analyzing the Trust Mechanism of the Sharing Economy Based on Innovation Diffusion Theory and Innovation Resistance Theory. Manag. Rev. 2017, 36, 123–137. [Google Scholar] [CrossRef]

- E-Commerce Consumers Survey 2018. Available online: https://www.mcmc.gov.my/skmmgovmy/files/2c/2c7d733b-e086-43f1-9254-97cf0740c733/files/assets/basic-html/page-1.html# (accessed on 5 July 2021).

- Wei, K.; Li, Y.; Zha, Y.; Ma, J. Trust, Risk and Transaction Intention in Consumer-to-Consumer e-Marketplaces: An Empirical Comparison between Buyers’ and Sellers’ Perspectives. IMDS 2019, 119, 331–350. [Google Scholar] [CrossRef]

- Özpolat, K.; Gao, G.; Jank, W.; Viswanathan, S. Research Note—The Value of Third-Party Assurance Seals in Online Retailing: An Empirical Investigation. Inf. Syst. Res. 2013, 24, 1100–1111. [Google Scholar] [CrossRef]

- Chen, X.; Huang, Q.; Davison, R.M.; Hua, Z. What Drives Trust Transfer? The Moderating Roles of Seller-Specific and General Institutional Mechanisms. Int. J. Electron. Commer. 2015, 20, 261–289. [Google Scholar] [CrossRef]

- Chong, A.Y.L.; Lacka, E.; Boying, L.; Chan, H.K. The Role of Social Media in Enhancing Guanxi and Perceived Effectiveness of E-Commerce Institutional Mechanisms in Online Marketplace. Inf. Manag. 2018, 55, 621–632. [Google Scholar] [CrossRef] [Green Version]

- McCole, P.; Ramsey, E.; Kincaid, A.; Fang, Y.; Li, H. The Role of Structural Assurance on Previous Satisfaction, Trust and Continuance Intention: The Case of Online Betting. ITP 2019, 32, 781–801. [Google Scholar] [CrossRef] [Green Version]

- Huang, Q.; Chen, X.; Ou, C.X.; Davison, R.M.; Hua, Z. Understanding Buyers’ Loyalty to a C2C Platform: The Roles of Social Capital, Satisfaction and Perceived Effectiveness of e-Commerce Institutional Mechanisms: The Impact of Social Capital on Buyer Satisfaction. Inf. Syst. J. 2017, 27, 91–119. [Google Scholar] [CrossRef]

- Venkatesh, V.; Morris, M.G.; Davis, G.B.; Davis, F.D. User Acceptance of Information Technology: Toward a Unified View. MIS Q. 2003, 27, 425–478. [Google Scholar] [CrossRef] [Green Version]

- Kim, D.J. A Study of the Multilevel and Dynamic Nature of Trust in E-Commerce from a Cross-Stage Perspective. Int. J. Electron. Commer. 2014, 19, 11–64. [Google Scholar] [CrossRef]

- Mcknight, D.H.; Kacmar, C.J.; Choudhury, V. Shifting Factors and the Ineffectiveness of Third Party Assurance Seals: A Two-Stage Model of Initial Trust in a Web Business. Electron. Mark. 2004, 14, 252–266. [Google Scholar] [CrossRef]

- Wang, N.; Shen, X.-L.; Sun, Y. Transition of Electronic Word-of-Mouth Services from Web to Mobile Context: A Trust Transfer Perspective. Decis. Support. Syst. 2013, 54, 1394–1403. [Google Scholar] [CrossRef]

- Pop, R.-A.; Săplăcan, Z.; Dabija, D.-C.; Alt, M.-A. The Impact of Social Media Influencers on Travel Decisions: The Role of Trust in Consumer Decision Journey. Curr. Issues Tour. 2021, 1–21. [Google Scholar] [CrossRef]

- Stewart, K.J. Trust Transfer on the World Wide Web. Organ. Sci. 2003, 14, 5–17. [Google Scholar] [CrossRef]

- Pavlou, P.A.; Gefen, D. Building Effective Online Marketplaces with Institution-Based Trust. Inf. Syst. Res. 2004, 15, 37–59. [Google Scholar] [CrossRef] [Green Version]

- Zucker, L.G. Production of Trust: Institutional Sources of Economic Structure, 1840–1920. Res. Organ. Behav. 1986, 8, 53–111. [Google Scholar]

- Venkatesh, V.; Thong, J.Y.L.; Xu, X. Consumer Acceptance and Use of Information Technology: Extending the Unified Theory of Acceptance and Use of Technology. MIS Q. 2012, 36, 157. [Google Scholar] [CrossRef] [Green Version]

- Wang, H.; Tao, D.; Yu, N.; Qu, X. Understanding Consumer Acceptance of Healthcare Wearable Devices: An Integrated Model of UTAUT and TTF. Int. J. Med. Inform. 2020, 139, 104156. [Google Scholar] [CrossRef] [PubMed]

- Shiferaw, K.B.; Mehari, E.A. Modeling Predictors of Acceptance and Use of Electronic Medical Record System in a Resource Limited Setting: Using Modified UTAUT Model. Inform. Med. Unlocked 2019, 17, 100182. [Google Scholar] [CrossRef]

- Mousa Jaradat, M.-I.R.; Al Rababaa, M.S. Assessing Key Factor That Influence on the Acceptance of Mobile Commerce Based on Modified UTAUT. IJBM 2013, 8, 102. [Google Scholar] [CrossRef] [Green Version]

- Khalilzadeh, J.; Ozturk, A.B.; Bilgihan, A. Security-Related Factors in Extended UTAUT Model for NFC Based Mobile Payment in the Restaurant Industry. Comput. Hum. Behav. 2017, 70, 460–474. [Google Scholar] [CrossRef]

- Zhou, T. Examining Users’ Switch from Online Banking to Mobile Banking. Int. J. Netw. Virtual Organ. 2018, 18, 51–66. [Google Scholar] [CrossRef]

- Yeh, Y.-S.; Li, Y.-M. Design-to-Lure in the e-Shopping Environment: A Landscape Preference Approach. Inf. Manag. 2014, 51, 995–1004. [Google Scholar] [CrossRef]

- Li, W. The Role of Trust and Risk in Citizens’ E-Government Services Adoption: A Perspective of the Extended UTAUT Model. Sustainability 2021, 13, 7671. [Google Scholar] [CrossRef]

- Dwivedi, Y.K.; Rana, N.P.; Chen, H.; Williams, M.D. A Meta-analysis of the Unified Theory of Acceptance and Use of Technology (UTAUT). In Governance and Sustainability in Information Systems. Managing the Transfer and Diffusion of IT; Nüttgens, M., Gadatsch, A., Kautz, K., Schirmer, I., Blinn, N., Eds.; IFIP Advances in Information and Communication Technology; Springer: Berlin/Heidelberg, Germany, 2011; Volume 366, pp. 155–170. ISBN 978-3-642-24147-5. [Google Scholar]

- Lallmahomed, M.Z.I.; Lallmahomed, N.; Lallmahomed, G.M. Factors Influencing the Adoption of E-Government Services in Mauritius. Telemat. Inform. 2017, 34, 57–72. [Google Scholar] [CrossRef]

- Herrero, Á.; San Martín, H.; del Mar Garcia-De los Salmones, M. Explaining the Adoption of Social Networks Sites for Sharing User-Generated Content: A Revision of the UTAUT2. Comput. Hum. Behav. 2017, 71, 209–217. [Google Scholar] [CrossRef] [Green Version]

- Slade, E.L.; Dwivedi, Y.K.; Piercy, N.C.; Williams, M.D. Modeling Consumers’ Adoption Intentions of Remote Mobile Payments in the United Kingdom: Extending UTAUT with Innovativeness, Risk, and Trust: CONSUMERS’ ADOPTION INTENTIONS OF REMOTE MOBILE PAYMENTS. Psychol. Mark. 2015, 32, 860–873. [Google Scholar] [CrossRef]

- Oliveira, T.; Thomas, M.; Baptista, G.; Campos, F. Mobile Payment: Understanding the Determinants of Customer Adoption and Intention to Recommend the Technology. Comput. Hum. Behav. 2016, 61, 404–414. [Google Scholar] [CrossRef]

- Musa, A.; Khan, H.U.; AlShare, K.A. Factors Influence Consumers’ Adoption of Mobile Payment Devices in Qatar. IJMC 2015, 13, 670. [Google Scholar] [CrossRef]

- Tsou, H.-T.; Chen, J.-S.; Chou, Y.; Chen, T.-W. Sharing Economy Service Experience and Its Effects on Behavioral Intention. Sustainability 2019, 11, 5050. [Google Scholar] [CrossRef] [Green Version]

- Venkatesh, V.; Davis, F.D. A Theoretical Extension of the Technology Acceptance Model: Four Longitudinal Field Studies. Manag. Sci. 2000, 46, 186–204. [Google Scholar] [CrossRef] [Green Version]

- Verkijika, S.F. Factors Influencing the Adoption of Mobile Commerce Applications in Cameroon. Telemat. Inform. 2018, 35, 1665–1674. [Google Scholar] [CrossRef]

- Prayoonphan, F.; Xu, X. Factors Influencing the Intention to Use the Common Ticketing System (Spider Card) in Thailand. Behav. Sci. 2019, 9, 46. [Google Scholar] [CrossRef] [Green Version]

- Mensah, I.K. Factors Influencing the Intention of University Students to Adopt and Use E-Government Services: An Empirical Evidence in China. SAGE Open 2019, 9, 1–19. [Google Scholar] [CrossRef] [Green Version]

- Chen, K.; Chan, A.H.S. Gerontechnology Acceptance by Elderly Hong Kong Chinese: A Senior Technology Acceptance Model (STAM). Ergonomics 2014, 57, 635–652. [Google Scholar] [CrossRef]

- Morosan, C.; DeFranco, A. It’s about Time: Revisiting UTAUT2 to Examine Consumers’ Intentions to Use NFC Mobile Payments in Hotels. Int. J. Hosp. Manag. 2016, 53, 17–29. [Google Scholar] [CrossRef]

- Jarvenpaa, S.L.; Tractinsky, N.; Saarinen, L. Consumer Trust in an Internet Store: A Cross-Cultural Validation. J. Comput.-Mediat. Commun. 2006, 5. [Google Scholar] [CrossRef]

- Liébana-Cabanillas, F.; Marinković, V.; Kalinić, Z. A SEM-Neural Network Approach for Predicting Antecedents of m-Commerce Acceptance. Int. J. Inf. Manag. 2017, 37, 14–24. [Google Scholar] [CrossRef]

- Zhang, L.; Zhu, J.; Liu, Q. A Meta-Analysis of Mobile Commerce Adoption and the Moderating Effect of Culture. Comput. Hum. Behav. 2012, 28, 1902–1911. [Google Scholar] [CrossRef]

- Chong, A.Y.-L.; Chan, F.T.S.; Ooi, K.-B. Predicting Consumer Decisions to Adopt Mobile Commerce: Cross Country Empirical Examination between China and Malaysia. Decis. Support. Syst. 2012, 53, 34–43. [Google Scholar] [CrossRef]

- Giovanis, A.; Assimakopoulos, C.; Sarmaniotis, C. Adoption of Mobile Self-Service Retail Banking Technologies: The Role of Technology, Social, Channel and Personal Factors. IJRDM 2019, 47, 894–914. [Google Scholar] [CrossRef]

- Chang, M.K.; Cheung, W.; Tang, M. Building Trust Online: Interactions among Trust Building Mechanisms. Inf. Manag. 2013, 50, 439–445. [Google Scholar] [CrossRef]

- Shao, Z.; Yin, H. Building Customers’ Trust in the Ridesharing Platform with Institutional Mechanisms: An Empirical Study in China. Internet Res. 2019, 29, 1040–1063. [Google Scholar] [CrossRef]

- Chiu, C.-M.; Hsu, M.-H.; Lai, H.; Chang, C.-M. Re-Examining the Influence of Trust on Online Repeat Purchase Intention: The Moderating Role of Habit and Its Antecedents. Decis. Support. Syst. 2012, 53, 835–845. [Google Scholar] [CrossRef]

- Luhmann, N. Trust and Power; English edition; Polity: Malden, MA, USA, 2017; ISBN 978-1-5095-1945-3. [Google Scholar]

- Steele, J.; Bourke, L.; Luloff, A.E.; Liao, P.-S.; Theodori, G.L.; Krannich, R.S. The Drop-Off/Pick-Up Method For Household Survey Research. Community Dev. Soc. J. 2001, 32, 238–250. [Google Scholar] [CrossRef]

- Gefen; Karahanna; Straub Trust and TAM in Online Shopping: An Integrated Model. MIS Q. 2003, 27, 51. [CrossRef]

- Hair, J.F. (Ed.) A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM), 2nd ed.; Sage: Los Angeles, CA, USA, 2017; ISBN 978-1-4833-7744-5. [Google Scholar]

- Bagozzi, R.P.; Yi, Y. On the Evaluation of Structural Equation Models. J. Acad. Mark. Sci. 1988, 16, 74–94. [Google Scholar] [CrossRef]

- Hair, J.F. (Ed.) Multivariate Data Analysis: Pearson New International Edition, 7th ed.; Pearson: Harlow, UK, 2014; ISBN 978-1-292-02190-4. [Google Scholar]

- Fornell, C.; Larcker, D.F. Evaluating Structural Equation Models with Unobservable Variables and Measurement Error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Henseler, J.; Ringle, C.M.; Sarstedt, M. A New Criterion for Assessing Discriminant Validity in Variance-Based Structural Equation Modeling. J. Acad. Mark. Sci. 2015, 43, 115–135. [Google Scholar] [CrossRef] [Green Version]

- Kline, R.B. Principles and Practice of Structural Equation Modeling, 4th ed.; Methodology in the social sciences; The Guilford Press: New York, NY, USA, 2016; ISBN 978-1-4625-2335-1. [Google Scholar]

- Gold, A.H.; Malhotra, A.; Segars, A.H. Knowledge Management: An Organizational Capabilities Perspective. J. Manag. Inf. Syst. 2001, 18, 185–214. [Google Scholar] [CrossRef]

- Diamantopoulos, A.; Siguaw, J.A. Formative Versus Reflective Indicators in Organizational Measure Development: A Comparison and Empirical Illustration. Br. J. Manag. 2006, 17, 263–282. [Google Scholar] [CrossRef]

- Lohmöller, J.-B. Latent Variable Path Modeling with Partial Least Squares; Springer: Berlin/Heidelberg, Germany, 1989; ISBN 978-3-642-52512-4. [Google Scholar]

- Ringle, C.M.; Wende, S.; Becker, J.-M. SmartPLS 3 2015; SmartPLS GmbH: Boenningstedt, Germany, 2015. [Google Scholar]

- Ramayah, T.; Cheah, J.; Chuah, F.; Ting, H.; Memon, M.A. Partial Least Squares Structural Equation Modeling (PLS-SEM) Using SmartPLS 3.0: An. Updated Guide and Practical Guide to Statistical Analysis, 2nd ed.; Pearson Malaysia Sdn Bhd: Kuala Lumpur, Malaysia, 2018; ISBN 978-967-349-750-8. [Google Scholar]

- Cohen, J. Statistical Power Analysis for the Behavioral Sciences, 2nd ed.; L. Erlbaum Associates: Hillsdale, NJ, USA, 1988; ISBN 978-0-8058-0283-2. [Google Scholar]

- Chin, W.W. The partial least squares approach for structural equation modeling. In Modern Methods for Business Research; Quantitative Methodology Series; Lawrence Erlbaum: Mahwah, NJ, USA, 1988; pp. 295–336. [Google Scholar]

- Fornell, C.; Cha, J. Partial Least Squares. In Advanced Methods of Marketing Research; Blackwell Business: Cambridge, UK, 1994; pp. 52–78. ISBN 978-1-55786-549-6. [Google Scholar]

- Bawack, R.E.; Kala Kamdjoug, J.R. Adequacy of UTAUT in Clinician Adoption of Health Information Systems in Developing Countries: The Case of Cameroon. Int. J. Med. Inform. 2018, 109, 15–22. [Google Scholar] [CrossRef]

- Shaw, N.; Sergueeva, K. The Non-Monetary Benefits of Mobile Commerce: Extending UTAUT2 with Perceived Value. Int. J. Inf. Manag. 2019, 45, 44–55. [Google Scholar] [CrossRef]

- Hong, I.B.; Cho, H. The Impact of Consumer Trust on Attitudinal Loyalty and Purchase Intentions in B2C E-Marketplaces: Intermediary Trust vs. Seller Trust. Int. J. Inf. Manag. 2011, 31, 469–479. [Google Scholar] [CrossRef]

- Oh, J.-C.; Yoon, S.-J. Predicting the Use of Online Information Services Based on a Modified UTAUT Model. Behav. Inf. Technol. 2014, 33, 716–729. [Google Scholar] [CrossRef]

- Rodrigues, G.; Sarabdeen, J.; Balasubramanian, S. Factors That Influence Consumer Adoption of E-Government Services in the UAE: A UTAUT Model Perspective. J. Internet Commer. 2016, 15, 18–39. [Google Scholar] [CrossRef]

- Manrai, R.; Gupta, K.P. Integrating UTAUT with Trust and Perceived Benefits to Explain User Adoption of Mobile Payments. In Strategic System Assurance and Business Analytics; Kapur, P.K., Singh, O., Khatri, S.K., Verma, A.K., Eds.; Asset Analytics; Springer: Singapore, 2020; pp. 109–121. ISBN 9789811536465. [Google Scholar]

- He, K.; Zhang, J.; Zeng, Y. Households’ Willingness to Pay for Energy Utilization of Crop Straw in Rural China: Based on an Improved UTAUT Model. Energy Policy 2020, 140, 111373. [Google Scholar] [CrossRef]

| Demographic | Frequency (n = 232) | Percentage (%) |

|---|---|---|

| Gender | ||

| Male | 99 | 42.7 |

| Female | 133 | 57.3 |

| Age | ||

| Below 20 | 39 | 16.8 |

| 21–25 | 70 | 30.2 |

| 26–30 | 37 | 15.9 |

| 31–35 | 25 | 10.8 |

| 36–40 | 15 | 6.5 |

| Above 40 | 46 | 19.8 |

| Highest level of academic qualification | ||

| No College Degree | 58 | 25.0 |

| Diploma/Advanced Diploma | 70 | 30.2 |

| Bachelor’s degree | 97 | 41.8 |

| Master’s degree | 5 | 2.2 |

| Ph.D. Degree | 2 | 0.9 |

| Occupation | ||

| Manager | 17 | 7.3 |

| Executive | 63 | 27.2 |

| Administrative/Clerical | 23 | 9.9 |

| Technician | 5 | 2.2 |

| Self-employed | 21 | 9.1 |

| Student | 71 | 30.6 |

| Other | 32 | 13.8 |

| Constructs | Items | Loadings | Composite Reliability (CR) | Average Variance Extracted (AVE) |

|---|---|---|---|---|

| PE | PE1 PE2 PE3 PE4 | 0.8197 0.8486 0.8624 0.7928 | 0.899 | 0.691 |

| EE | EE1 EE2 EE3 EE4 | 0.8403 0.8229 0.9031 0.8745 | 0.920 | 0.741 |

| SI | SI1 SI2 SI3 | 0.8791 0.9221 0.9166 | 0.932 | 0.821 |

| FC | FC1 FC2 FC3 FC4 | 0.8319 0.8505 0.7379 0.6850 | 0.860 | 0.607 |

| TV | TV1 TV2 TV3 TV4 TV5 TV6 TV7 TV8 | 0.7784 0.7659 0.8089 0.6720 0.7896 0.8282 0.8506 0.8413 | 0.931 | 0.630 |

| SA | SA1 SA2 SA3 SA4 | 0.8489 0.8220 0.8555 0.7764 | 0.896 | 0.683 |

| PEEIM | PEEIM1 PEEIM2 PEEIM3 | 0.8777 0.8786 0.7973 | 0.888 | 0.726 |

| BI | BI1 BI2 BI3 | 0.8897 0.9334 0.9149 | 0.937 | 0.833 |

| BI | EE | FC | PE | PEEIM | SA | SI | TV | |

|---|---|---|---|---|---|---|---|---|

| BI | 0.913 | |||||||

| EE | 0.533 | 0.816 | ||||||

| FC | 0.578 | 0.624 | 0.779 | |||||

| PE | 0.624 | 0.581 | 0.585 | 0.831 | ||||

| PEEIM | 0.460 | 0.348 | 0.449 | 0.409 | 0.852 | |||

| SA | 0.570 | 0.372 | 0.365 | 0.409 | 0.580 | 0.826 | ||

| SI | 0.505 | 0.337 | 0.481 | 0.423 | 0.443 | 0.405 | 0.906 | |

| TV | 0.574 | 0.404 | 0.442 | 0.418 | 0.663 | 0.753 | 0.400 | 0.794 |

| BI | EE | FC | PE | PEEIM | SA | SI | TV | |

|---|---|---|---|---|---|---|---|---|

| BI | ||||||||

| EE | 0.589 (0.457, 0.699) | |||||||

| FC | 0.671 (0.555, 0.763) | 0.729 (0.628, 0.812) | ||||||

| PE | 0.708 (0.609, 0.787) | 0.661 (0.551, 0.749) | 0.711 (0.599, 0.806) | |||||

| PEEIM | 0.523 (0.404, 0.624) | 0.390 (0.267, 0.506) | 0.546 (0.431, 0.655) | 0.485 (0.357, 0.596) | ||||

| SA | 0.647 (0.547, 0.732) | 0.422 (0.282, 0.546) | 0.439 (0.301, 0.555) | 0.478 (0.353, 0.588) | 0.690 (0.578, 0.781) | |||

| SI | 0.561 (0.439, 0.661) | 0.369 (0.240, 0.490) | 0.584 (0.477, 0.674) | 0.485 (0.352, 0.600) | 0.517 (0.385, 0.626) | 0.461 (0.323, 0.586) | ||

| TV | 0.623 (0.533, 0.702) | 0.442 (0.314, 0.554) | 0.518 (0.403, 0.621) | 0.471 (0.359, 0.573) | 0.769 (0.675, 0.840) | 0.846 (0.780, 0.894) | 0.436 (0.321, 0.542) |

| Hypotheses | Path | Path Coefficient (β) | Standard Deviation (STDEV) | t Statistics (|β/STDEV|) | Supported |

|---|---|---|---|---|---|

| H1 | PE → BI | 0.294 | 0.061 | 4.824 ** | Yes |

| H2 | EE → BI | 0.109 | 0.075 | 1.445 | No |

| H3 | SI → BI | 0.168 | 0.056 | 3.021 ** | Yes |

| H4 | FC → BI | 0.133 | 0.068 | 1.962 * | Yes |

| H5 | TV → BI | 0.280 | 0.072 | 3.877 ** | Yes |

| Construct | BI (Effect Size, f 2) |

|---|---|

| PE | 0.109 |

| EE | 0.014 |

| SI | 0.046 |

| FC | 0.020 |

| TV | 0.131 |

| Construct | Sum Square of Observations (SSO) | Sum Square of Errors (SSE) | Q² = (1 − SSE/SSO) |

|---|---|---|---|

| BI | 696.000 | 375.931 | 0.460 |

| EE | 928.000 | 928.000 | |

| FC | 928.000 | 928.000 | |

| PE | 928.000 | 928.000 | |

| SI | 696.000 | 696.000 | |

| TV | 1856.000 | 1856.000 |

| Path | Path Coefficient (β) | Standard Deviation (STDEV) | t Statistics (|β/STDEV|) |

|---|---|---|---|

| PE → BI | 0.276 | 0.060 | 4.586 ** |

| EE → BI | 0.087 | 0.075 | 1.160 |

| SI → BI | 0.154 | 0.056 | 2.769 ** |

| FC → BI | 0.152 | 0.068 | 2.237 * |

| TV → BI SA → BI (TV × SA) → BI | 0.143 0.164 −0.080 | 0.072 0.076 0.044 | 1.993 * 2.144 * 1.832 * |

| Path | Path Coefficient (β) | Standard Deviation (STDEV) | t Statistics (|β/STDEV|) |

|---|---|---|---|

| PE → BI | 0.290 | 0.061 | 4.710 ** |

| EE → BI | 0.110 | 0.073 | 1.520 |

| SI → BI | 0.182 | 0.057 | 3.214 ** |

| FC → BI | 0.150 | 0.069 | 2.178 * |

| TV → BI PEEIM → BI (TV × PEEIM) → BI | 0.297 −0.076 −0.106 | 0.068 0.067 0.050 | 4.361 ** 1.129 2.142 * |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sim, J.J.; Loh, S.H.; Wong, K.L.; Choong, C.K. Do We Need Trust Transfer Mechanisms? An M-Commerce Adoption Perspective. J. Theor. Appl. Electron. Commer. Res. 2021, 16, 2241-2262. https://doi.org/10.3390/jtaer16060124

Sim JJ, Loh SH, Wong KL, Choong CK. Do We Need Trust Transfer Mechanisms? An M-Commerce Adoption Perspective. Journal of Theoretical and Applied Electronic Commerce Research. 2021; 16(6):2241-2262. https://doi.org/10.3390/jtaer16060124

Chicago/Turabian StyleSim, Jia Jia, Siu Hong Loh, Kee Luen Wong, and Chee Keong Choong. 2021. "Do We Need Trust Transfer Mechanisms? An M-Commerce Adoption Perspective" Journal of Theoretical and Applied Electronic Commerce Research 16, no. 6: 2241-2262. https://doi.org/10.3390/jtaer16060124