Non-Performing Loans as a Driver of Banking Distress: A Systematic Literature Review

1

Doctoral School of Regional and Business Administration Sciences, Széchenyi István University, 9026 Győr, Hungary

2

Faculty of Economics, University of Tuzla, 75000 Tuzla, Bosnia and Herzegovina

3

V.P.N.C Laboratory, Faculty of Law, Economics and Management, University of Jendouba, Jendouba 8100, Tunisia

*

Author to whom correspondence should be addressed.

Commodities 2023, 2(2), 111-130; https://doi.org/10.3390/commodities2020007

Submission received: 2 February 2023

/

Revised: 18 March 2023

/

Accepted: 29 March 2023

/

Published: 7 April 2023

Abstract

:The main purpose of this paper is to present a systematic literature review of studies on the determinants of non-performing loans (NPLs) published over the period 1987–2022. This paper reviewed 76 studies in 58 peer-reviewed journals. The provocation for this analysis is that the issue of NPLs is attributed to close attention from policymakers and is currently addressed with various measures. The authors synthesize the literature according to the following main boards: macroeconomic factors, bank-specific factors, and industry factors. This study tries to construct the main findings from the numerous studies that are performed concerning NPLs and their determinants. The authors’ motivation is to provide a detailed perspective on NPLs. Hence, this study provides a complete and coherent framework for the researchers to examine the varied NPL literature.

1. Introduction

Banking institutions play a vital role in the financial system. There are many experiences of financial crises associated with deteriorating asset quality in the banking sector, especially the building-up of non-performing loans (henceforth NPLs). One of the primary sources of banking activities is lending; the significant credit expansion by financial institutions during the two decades before the global financial crisis of 2007–2009 was a defining feature of those years [1]. NPLs are the most commonly used metric for assessing credit risk. This indicator reflects the risk that underlying cash flows from loans held by financial institutions may not be fully repaid and is related to the quality of bank assets [2]. Numerous earlier empirical investigations demonstrate that bank failure is typically caused by a high amount of NPLs [3].

The primary source of growing concerns in the banking industry for both developing and developed countries has been the degradation of the quality of the loan portfolio of banks. The world has occasionally experienced a variety of financial crises. For example, in the 1980s and 1990s, the savings and loan crisis in the United States failed 747 out of 3234 savings and loans due to non-repayment. Further, the Finnish banking crisis in 1991–1993 because by economic distortion resulting in the government takeover of the banks and providing monetary assistance. Furthermore, the Venezuelan banking crisis of 1994 failed 17 out of 49 commercial banks [4]. The Asian crisis of 1997 is also an example of a financial crisis that happened because of excessive foreign debt, in addition to currency devaluation brought on by excessive credit expansion in the real-estate sector. The global financial crisis of 2007–2009, which led to the collapse of numerous significant financial institutions and slowed down global economic growth, is the most important in banking history [5]. The underlying lesson from past crises is that financial distress and economic unrest are deeply linked [6]. Moreover, it has been demonstrated that excessive lending by banks to various industries can prevent banks from accessing their funds, leading to bank failure and a negative impact on economic growth [7].

The objective of this paper is to provide a systematic literature review on the determinants of NPLs. To adapt the continuing dispute literature reviews in an effective way of arranging many parts of research concerns to give a conceptual framework for developing and comprehending the subject matter [8]. In this regard, [9] contribute a first qualitative review of the literature on NPLs. To achieve this, we selected articles listed in at least one of the following indices: Web of Science Journal Citation Index and Scopus. After a careful reading and synthesizing of the articles, 76 papers from 58 peer-reviewed journals were considered for the final review.

Following the work of [10], our paper tries to contribute to the existing literature by providing a systematic literature review on the determinants of NPLs. First, aside from the main determinants of NPLs (bank specifics, industry specifics, and financial and macroeconomic factors), we expand the period by including the COVID-19 pandemic in our review. To the best of our knowledge, no previous review paper has approached the issue of COVID-19 on bad loans. Second, we collected, summarized, and synthesized a wide range of research articles, and we discussed the findings of these studies based on several criteria that cover the temporal dimension (period of studies), the geographic dimension (region of studies), the dimension of research quality (ranking of journal of publication), and the dimension of empirical methodology (empirical method). Third, the readers of this paper will be more informed about the period that attracts researchers to investigate NPLs, the regions which are considered appropriate case studies, the main empirical method used, and the journals that publish those articles.

The remainder of this article is organized as follows. An overview of the regulatory history of NPLs is provided in Section 2. The methodology approach used for the literature gathering is illustrated in Section 3. The literature is summarized in Section 4 using a framework based on macroeconomics, bank-specific factors, and industry-specific factors. The implications of this article are highlighted in Section 5, along with potential directions for further research and a conclusion reflection.

2. Definition and Regulatory Landscape of NPLs

A first glance at the review of the literature reveals that there is no globally valid definition for the term non-performing loans (NPLs). This means that characterizations of NPLs vary across different jurisdictions. In the narrow sense, there are three commonly used institutional approaches to define NPLs as follows:

The Institute of International Finance 1999 working group on loan quality divided the loans into five groups: standard, watch, substandard, doubtful, and loss. The last three categories were identified as NPLs, which means that payment of principal and/or interest is overdue more than 90 days, 180 days, and 365 days [11].

The International Monetary Fund defines loans as NPLs when (a) payments of principal and interest are past due by 90 days or more; (b) interest payments equal to 90 days interest or more have been capitalized (reinvested into the principal amount), refinanced, or rolled over (payment delayed by agreement); or (c) evidence exists to reclassify them as NPLs even in the absence of a 90-day past due payment. For instance, when the debtor files for bankruptcy after classifying the loan as NPLs [12].

The Basel Committee on Banking Supervision defines NPLs as when “a default is considered to have occurred concerning a particular obligor when either or both of the two following events have taken place. The obligor is past due more than 90 days on any material credit obligation to the banking group. Overdrafts will be considered as being past due once the customer has breached an advised limit or been advised of a limit smaller than current outstanding” [13].

In the wider sense, NPLs consist of sub-performing loans; such loans are not fully defaulted but are in arrears between 60–90 days. In addition, there is a watchlist loan, and those loans are not expected to default directly. Lastly, non-strategic loans, which are not considered a bank’s core activities for strategic reasons, can be part of NPLs. However, we will focus on the narrow sense when we synthesize the literature. Following the work of [14], these are the most agreed-upon definitions of bad loans in the literature. However, the definition of NPLs may vary across countries, but the concept is relatively similar the world over.

The bank classifies the loan as NPLs and, depending on domestic accounting regulations, it becomes “bad debt.” There are significant differences in the treatment of NPLs, which might not correctly depict the problem’s scope. The reported NPLs can be overstated or understated by regions, countries, and individual banks. The following factors influence various NPL interpretations:

- Whether or not restructured loans need to be recognized as NPLs,

- Whether collateral is considered when granting a loan,

- Whether NPLs are listed as fully or partially overdue in terms of outstanding value,

- Whether banks must downgrade every loan.

Analyzing NPLs is crucial from a regulatory perspective. The International Monetary Fund (IMF), the Basel Committee on Banking Supervision (BCBS), the Financial Stability Board (FSB), and the Bank for International Settlements (BIS) have all raised concerns about the lack of international comparability when it comes to evaluating NPLs held by banks and how they affect their balance sheets. Moreover, international norms or standard governing bodies for NPLs are missing due to (1) different prudential agendas, (2) policy agenda and its priorities, (3) technology terminology, and (4) the associated problem of regulatory forbearance. In short, the banking and financial industry lacks a standard definition of NPLs [15].

3. Research Methodology

The main goal of this paper is to gain a thorough understanding of the subject of NPLs by following [16]. A rigorous literature review was conducted, starting from the identification of the subject, the scientific need, and the primary goal of the reviews. Then, the criteria used to choose which studies to conduct are covered in detail for data abstraction and extraction. This research resulted in the inclusion of 140 studies that tackled the issue of NPLs. For quality standards, only peer-reviewed articles published by publishers were included in the final review. In this vein, the selected articles are listed in at least one of the following indices: the Web of Science Journal Citation Index and/or Scopus. After a careful reading and synthesizing of the articles, 76 papers from 58 peer-reviewed journals were considered for the final review. The final review includes articles that empirically and theoretically examine the determinants of NPLs worldwide.

Inclusion Criteria

We only included studies that provide evidence of the determinants of NPLs, and we included studies written in English. We started the literature search by using the keywords of “bad loans AND determinants” and “non AND performing AND loans AND determinants.” For each manuscript, preliminary relevance was conducted by title. From the title of the paper, if the content seemed to discuss the determinants of credit risk, especially NPLs, we obtained its full reference, including author, year, abstract, and results for further evaluation. We searched the Web of Science and Scopus, which are frequently used by scholars and researchers across various disciplines. A search on the Web of Science using the keywords “bad loans AND determinants” and “non AND performing AND loans AND determinants” yielded a total of 495 studies. A search on Scoups using keywords “Bad loans AND determinants” and “non AND performing AND loans AND determinants” returned 311 studies. After initial title screening, we found 140 studies related to the determinants of NPLs. Altogether we included a total of 76 potential studies in this research. We read the abstracts of the 76 studies to further decide the relevance to the research topic. We skimmed through the full-text articles to evaluate the quality and eligibility of the studies. We consider journal articles published by reputable publishers as high-quality research. In this context, most duplicated and conference papers were excluded from the review due to a lack of a peer-review process. We included a few high-quality papers with well-cited references. However, due to technological changes in archiving information, we limit the publication date from 1987 to 2022. Thus, we can build our review on the recent literature considering information retrieval.

4. Literature Search and Evaluation

After synthesizing and identifying the relevant literature, the following subsections review the literature on the determinants of NPLs. Respectively: bank-specific factors, macroeconomic factors, industry factors, and the COVID-19 pandemic.

4.1. Determinants of NPLs: Theoretical Perspectives and Review from the Literature

The literature addressing the determinants of credit risk highlights various important types of determinants, ranging from macroeconomic and institutional issues to bank-specific and industry factors. The fundamental tenet of these studies is that credit standards gradually deteriorate during economic expansions [17]. Only peer-reviewed articles that provide specific guidelines on determinants of NPLs are included in Appendix A.

4.1.1. Bank-Specific Factors

In their seminal work, [14] examined the link between loan quality, cost efficiency, and bank capital by using a sample of US commercial banks by testing four hypotheses concerning the direction of causality. These include bad luck, bad management, skimping, and moral hazards. Under the bad luck hypothesis, [14] propose that cost efficiency negatively correlates with NPLs. For example, external events may incur additional bank costs because of dealing with these loans. Thus, weakening cost efficiency. However, in their study, [18] found no evidence that NPLs had a significant, negative impact on cost efficiency, while [19] concluded that the bad luck hypothesis has a favorable impact in their sample of transition countries. The bad management hypothesis suggests that low-cost efficiency will develop before or because of rising NPLs [14]. This is justified by the relationship between management quality and awareness of credit scoring, collateral valuation, and borrower monitoring. Previous studies have based their criteria for the selection of the bad management hypothesis [18,19,20,21,22]. The initial inspiration for the skimping hypothesis came from a suggestion made by [23] and was later developed by [24]. According to the skimping theory, high efficiency is associated with higher NPLs [13]. Notably, [25] noticed that inefficient banks are more likely to take more risks. Later, [26] confirm these findings. Lastly, under the moral hazard hypothesis, which is proposed by [27]. Banks with lower capitalization have more NPLs because their managers may be more inclined to take risks with their loan portfolios [25,26,27,28]. Regarding bank capitalization, an abundance of research has been conducted to determine the effect of the capital adequacy ratio on NPLs. In this vein, [29] find that a higher CAR implies reducing NPLs. While the study of [26] supposes a negative link between CAR and NPLs. Based on that, many scholars agree with this argument [13,14,15,16,17,18,19,20,21,22,23,24,25,26,27,28,29,30]. Bank size has been considered a crucial factor that affects NPLs. An extensive strand of the literature finds that bank size has a negative impact on NPLs [19,20,21,22,23,24,25,26,27,28,29,30,31,32]. However, bank size is positively correlated with NPLs, as supported by [33,34,35]. Profitability is a significant factor in determining NPLs. Many scholars study the relationship between banks’ profitability and NPLs. However, there is no consensus in the literature on the relationship between banks’ profitability and NPLs. [36] demonstrated that low profitability would boost banks’ managers to be more risk aggressive, which in turn increases the number of NPLs. On the contrary, [37] by studying the Spanish banks, concluded that increased profitability causes clients to take more risks, which results in larger NPLs.

4.1.2. Industry Factors

Theoretical and empirical research on the connection between bank rivalry and stability generated contentious findings. The theoretical parts have been developed on this matter. Firstly, [38] suggests the competition-fragility view. According to this viewpoint, increased competition among banks motivates banks to take on more risk. According to [39], greater market power lowers a bank’s risk of default. Furthermore, [40] contend that competition may have a negative effect on banks’ prudent behavior. Similarly, [41] claim that less concentrated banking systems are more likely to experience an economic decline. Secondly, the competition-stability view was proposed by [42] which argues that less competition results in higher interest rates for loans, raising the likelihood of default. However, the empirical findings on the relationship between competition and bank stability have shown conflicting findings. [43] provide empirical evidence between bank competition and banks’ risk-taking; according to their findings, banks with higher capital buffers in more competitive markets are less likely to undergo a protracted crisis. Moreover, [44] investigated how regulations, competition, and risk-taking are related. They claim that market power has a negative association with risk-taking. On the contrary, [45] examined the trade-off between bank competition and financial stability, suggesting that greater concentration fosters financial fragility. Thus, inducing bank risk exposure. The effects of competition and concentration on bank stability in the Turkish banking industry were examined by [46]. The key results imply that NPLs and bank competition are inversely connected. However, the results regarding bank concentration indicate that greater concentration has a positive impact on NPLs. Finally, [47] investigate the determinants of NPLs in the MENA region by considering both bank competition and bank concentration as industry factors that might affect NPLs, among other factors. According to their research, less concentrated banks have greater levels of NPLs, while more concentrated banks have lower levels of NPLs.

4.1.3. Macroeconomic Factors

Earlier studies investigated the assessment of the link between credit risk and macroeconomic factors [26,27,28,29,30,31,32,33,34,35,36,37,38,39,40,41,42,43,44,45,46,47,48]. Their findings demonstrate that macroeconomic factors have a negative effect on NPLs. The results suggest that borrowers’ income increases and their ability to repay loans occur during times of economic growth. However, NPLs rise as unemployment and income fall, causing borrowers to struggle to repay their loans [25,26,27,28,29,30,31,32,33,34,35,36,37,38,39,40,41,42,43,44,45,46,47,48,49,50]. A theoretical framework for identifying GDP, unemployment, and interest rates as major contributors to NPLs is provided by the life cycle strand. According to several scholars, macroeconomic variables have the strongest single capacity to explain NPL determinants [51,52,53,54]. Interestingly, [30] found through studying the impact of the global financial crisis on NPLs in the Turkish banking sector that the crisis affected NPL dynamics across banks. [25] used the vector autoregressive model (VAR) to validate this finding for a large sample of 2470 commercial banks in the USA between 1979 and 1985. However, they found that the literature does not agree on a single factor and that NPLs can be influenced by several different factors, including real GDP, unemployment, interest rates, exchange rate depreciation, public debt, and inflation. Real GDP and the state of the business cycle are related to economic growth [25,26,27,28,29,30,31,32,33,34,35,36,37,38,39,40,41,42,43,44,45,46,47,48,49,50,51,52,53,54,55,56,57]. Unemployment is also found by many scholars to be a significant variable claiming that higher unemployment corresponds to lower income. As a result, borrowers may have difficulty repaying their debt [19,20,21,22,23,24,25,26,27,28]. Interest rates play a significant role as a monetary variable in determining NPLs. The literature agrees that raising interest rates will affect the ability of borrowers to repay their loans [30,31,32,33,34,35,36,37,38,39,40,41,42,43,44,45,46,47,48,49,50,51,52,53,54,55,56,57,58]. From a monetary perspective, exchange rate depreciation has been less abundantly examined in the literature. However, the IMF working papers tried to explore this variable [5,6,7,8,9,10,11,12,13,14,15,16,17,18,19,20,21,22,23,24,25,26,27,28,29,30,31,32,33,34,35,36,37,38,39,40,41,42,43,44,45,46,47,48,49,50,51,52,53,54,55,56,57,58]. Several studies tried to investigate the sovereign debt crisis variables, such as public debt and public debt as a percentage of GDP. [19] presumed that the “sovereign debt hypothesis” claims that the raising of sovereign debt relates to higher NPLs. Following that, many scholars confirmed the sovereign debt hypothesis [21,22,23,24,25,26,27,28,29,30,31,32,33,34,35,36,37,38,39,40,41,42,43,44,45,46,47,48,49,50,51,52,53,54]. In the literature, inflation appears to be an ambiguous stream [25,26,27,28,29,30,31,32,33,34,35,36,37,38,39,40,41,42,43,44,45,46,47,48,49,50,51,52,53,54,55,56,57,58,59]. Lower inflation is positively associated with borrowers’ financial situation and ability to repay debt [28,29,30,31,32,33,34,35,36,37,38,39,40,41,42,43,44,45,46,47,48,49,50,51,52,53,54,55] showing that higher inflation may improve borrowers’ ability to repay their loans by lowering the real value of outstanding loans.

4.1.4. Health Crisis (COVID-19)

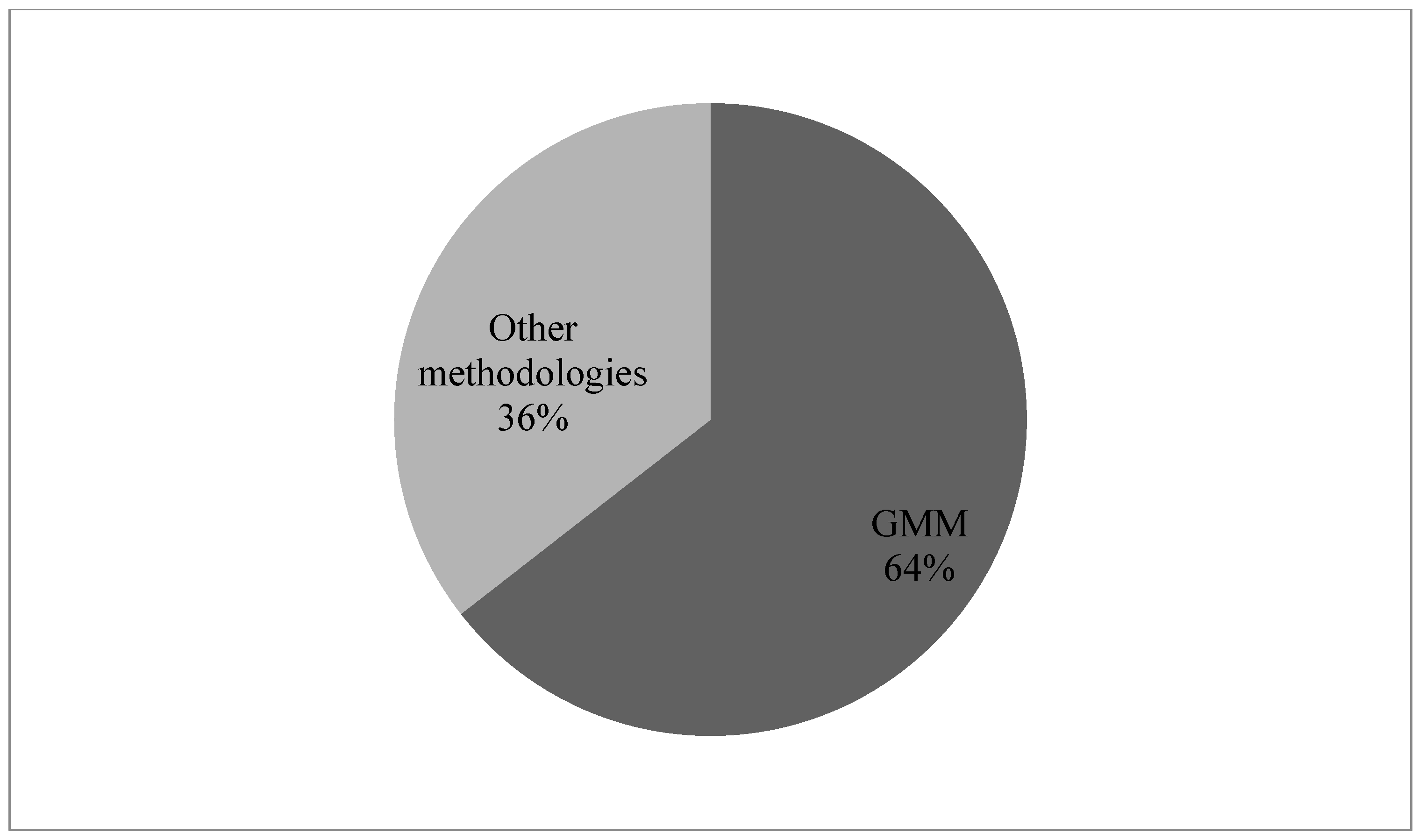

In the aftermath of the COVID-19 pandemic, one of the challenges is whether the health crisis will affect NPLs; financial institutions worldwide will be facing a rise in NPLs [60]. The higher volume of NPLs has adverse effects on banks’ profits while requiring high provisions [61]. Additionally, NPLs have a negative impact on bank lending, thus disturbing the smooth processes of the real economy. [62]. During COVID-19, NPL recognition has been lengthened through banks to cover the loss of capital. [63] investigate the determinants of NPLs in the banking sector of Bosnia and Herzegovina from 2012–2020. The results found that the impact of COVID-19 on NPLs is not yet adequately observable due to introduce the moratorium on loans. [64] documented a new dataset of NPLs during 92 banking crises; they found that most banking crises are followed by elevated NPLs. Moreover, the findings suggest that there is a considerable variation in predicated NPLs vulnerabilities. [65] studied the quarterly data of the largest 144 banks in the EU spanning the period 2016–2021. The results confirm the diverse picture over the pandemic period with various variables, such as economic growth, bank profitability, and banking risks. [66] explored the impact of COVID-19 and lockdown policies on the banking system in the US.; their results demonstrate that banks that are exposed to lockdown measures experience an increase in loan loss provisions and NPLs. In addition, the findings confirm the negative impact of the pandemic on the supply side of finance. [67] researched how European banks adjusted their lending during COVID-19 by using bank-level COVID-19 exposure; their findings are consistent with the zombie lending literature that shows banks with low capital have the incentive to grant more loans during bad times. Appendix A lists the existing literature of studies related to the determinants of NPLs. Firstly, by exploring the research methodology used in each paper. Secondly, the main determinants were carried out by the authors. Thirdly, the coverage country and the period of the study. Lastly, we elaborate on the key findings of the study. However, after reviewing the relevant literature, we found that the Generalized method of moments (GMM) technique, which is a generic method to estimate parameters in a statistical model, is quite dominant, with 64.47% representative of the sample because it avoids endogeneity issues and is considered one of the most powerful econometric techniques.

5. Analysis and Discussion

The topic of NPLs has received special attention from scholars over the last decade. The relevant literature classified the factors that drive NPLs into three classifications: macroeconomic, bank-specific, and industry factors. The macroeconomic factors are the most common factors related to NPLs [25,26,27,28,29,30,31,32,33,34,35,36,37,38,39,40,41,42,43,44,45,46,47,48,49,50,51,52,53,54,55,56,57,58,59,60,61,62,63,64,65,66,67,68]. These studies support the idea that the country’s business cycles impact the ability of debtors to pay back their loans. Other studies use bank-specific factors to define the emergence of NPLs. The fundamental idea of using bank-specific factors is the possibility of a relationship between ownership structure, bank profitability, bank efficiency, and NPLs [13,14,15,16,17,18,19,20,21,22,23,24,25,26,27,28,29,30,31,32,33,34,35,36,37,38,39,40,41,42,43,44,45,46,47,48,49,50,51,52,53,54,55,56,57,58,59,60,61,62,63,64,65]. In addition, industry factors can negatively impact banks’ NPLs, such as bank competition and bank concentration [43,44,45,46,47,48,49,50,51,52,53,54,55,56,57,58,59,60,61,62,63,64,65,66,67,68,69,70]. In the following subsections, we will discuss the results of our review.

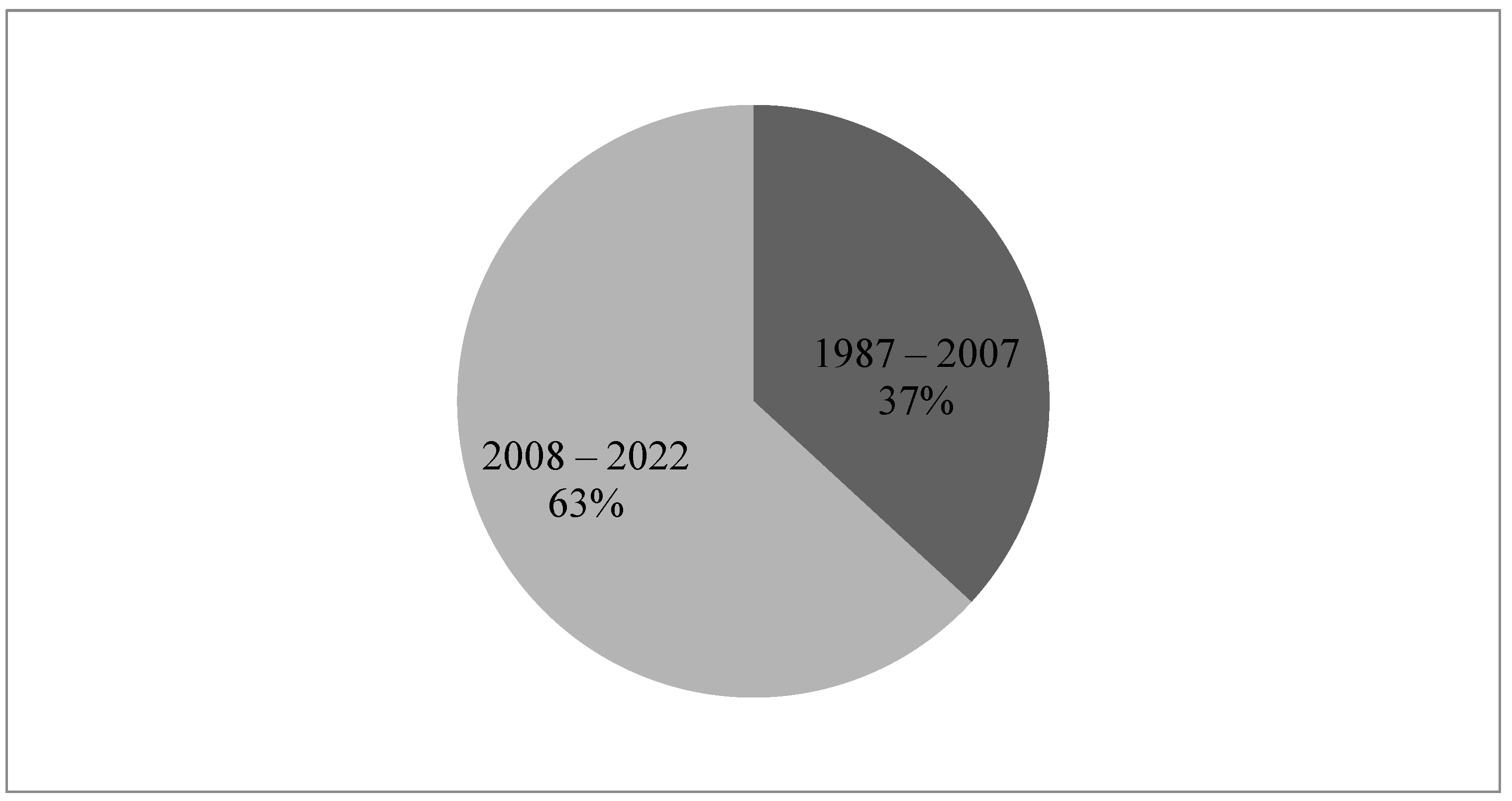

According to the distribution of the sample research articles in Appendix A, and Figure 1, 36.85% of studies related to the determinants of NPLs were conducted during the period 1987–2007. However, 63.15% of the studies were conducted between the period 2008–2022. This increased number of publications can be justified by the global financial crisis, which encouraged scholars to analyze the determinants of NPLs, in addition to the European Sovereign Debt crisis between 2009 and the mid-to-late 2010s. The accessibility of both macroeconomic and bank-specific data can be explained by the increase in the number of publications in this current period.

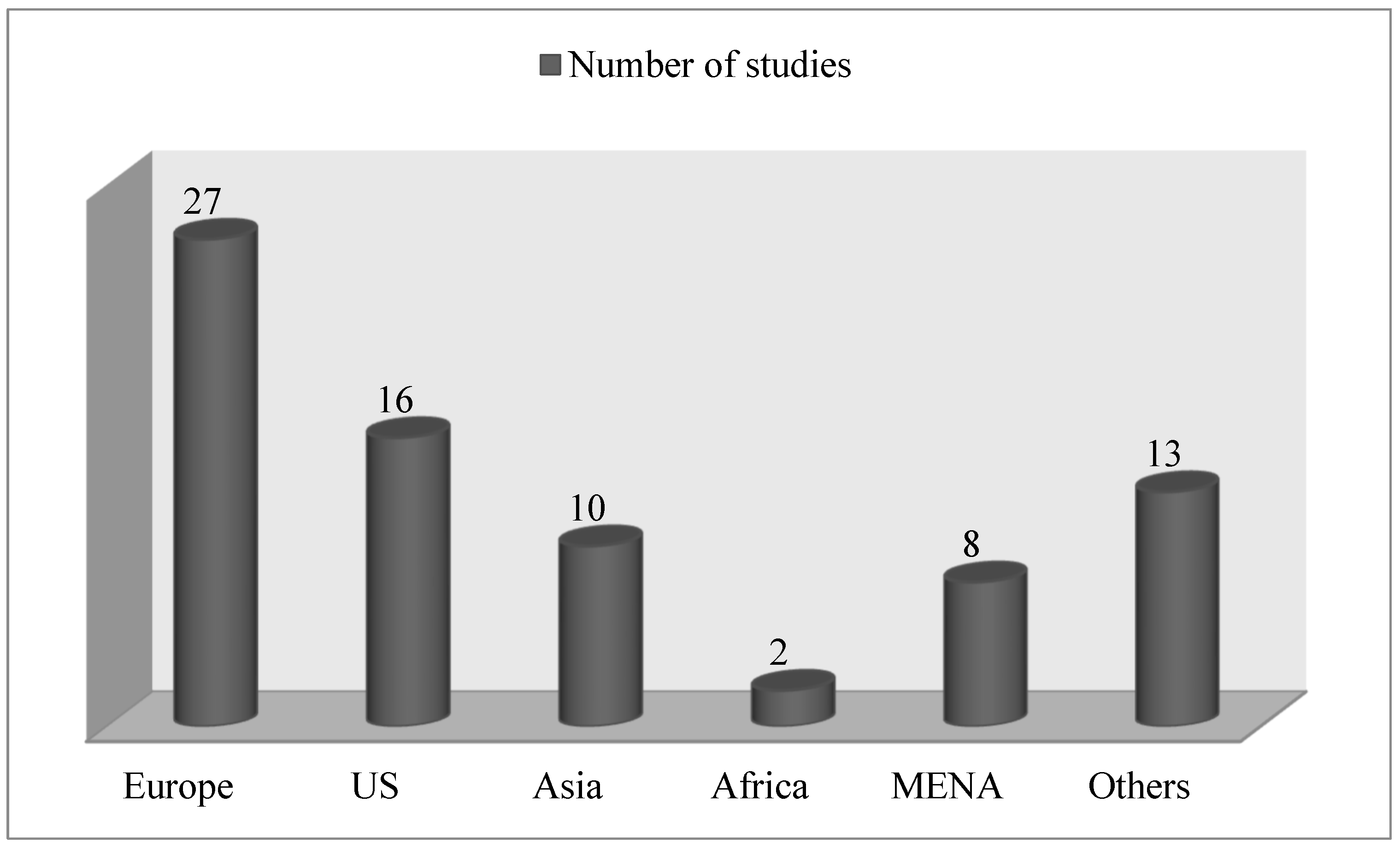

Figure 2 represents statistics of the covered sample, indicating that most of the research was conducted in the USA and European countries while little attention was addressed to the Middle East and North African regions. In this regard, 35.52% of the studies were conducted in Europe, 21.05% in the United States, 13.15% in Asia, 10.52% in the Middle East and North Africa, and only 2.63% in African countries. This indicates the absence of research in emerging countries like the Middle East and North Africa.

The descriptive statistics of Table 1 list the number of publications by an ABS-ranked journal. A wide range of journals has published research on the NPL determinants. Most of the publications were conducted in the Journal of Banking and Finance, including nine articles. Not surprisingly, 55.55% of those articles are among the most widely cited articles in the research field.

Figure 3 represents the research methodology used, the authors adopt different econometric estimates, beginning from simple regressions to vector autoregression models. For instance, most authors used dynamic panel data models, such as the two-step general method of moments. In this regard, 64.47% of the reviewed sample used panel models. The reason is that GMM estimates have the advantage of avoiding biases through p-values and the generation of correct standard errors. We strongly suggest the application of more advanced econometric models. In this vein, [71] developed a new method for testing Granger non-causality in panel data models with both large cross-sectional and time-series dimensions. Additionally, [72] used structural break analysis to explore changes in the relationship between COVID-19 cases and deaths in the US. Employing these methods leads to detecting an additional break that is not detected when using the time series data set.

The results of this paper differ from previous studies. While prior works show how NPLs affect bank profitability and bank stability, the current research treats this subject differently. The findings of this paper show the classification of the results of previous studies based on several criteria. These criteria cover the temporal dimension (period of studies), the geographic dimension (region of studies), the dimension of research quality (ranking of journal of publication), and the dimension of empirical methodology (empirical method).

6. Conclusions

This paper examines the expansive literature by focusing on the issue of NPLs and incorporating macroeconomic factors, bank-specific factors, and industry factors. The review reveals that macroeconomic and bank-specific factors, not industry factors, can hinder borrowers’ ability to repay loans. As NPLs cause concerns and are a major cause of financial distress, this research focuses on these factors and contributes to a more comprehensive understanding of the factors that influence NPLs. The review has attempted to summarize and highlight the central aspects of NPLs. In this regard, the motivation of this paper is to provide a comprehensive review of the literature on NPL determinants, which would contribute to the existing literature. Furthermore, the literature on banking and finance related to NPLs will benefit more from this review. We were able to recognize the main challenges impeding the development of this field through critical analysis and propose solutions for potential future paths.

The threat of bank failure arises in many countries because of NPLs. As such, many academics, researchers, and decision-makers are examining NPLs and potential management techniques in several areas. Firstly, this review provides a detailed and in-depth analysis of the relevant studies on NPLs, supporting researchers not only in defining important findings but also deciding on the appropriate research methodology. Secondly, this review assists policymakers and regulators by providing them with a holistic approach to the main determinants of NPLs. Additionally, this review assists them in using appropriate strategies for controlling NPLs. Finally, this review presents remedies based on prior literature, providing dimension to the topic and substantially improving the realms of banking and risk management.

One of the issues that need to be addressed is the scarcity of research in emerging markets. Not surprisingly, this review affirms a focus on European countries and the United States. However, countries may differ in terms of risk management and legal and institutional environment, which will impact the determinants of NPLs. Considering all studies in Appendix A. Most research stems from the USA and Europe, while Asia and other regions like MENA are less represented. Few studies have addressed the credit risk in the MENA region, making this a promising area for research. Consequently, enlarging the scope of studies would help to identify new factors that may form credit risk. In addition, this review demonstrates that a vast amount of research is focused on macroeconomic and bank-specific determinants in various regions, while little attention was paid to industry factors on the escalation of NPLs. However, given that market conditions impact banks’ risk behavior, we believe that more analysis should be performed on the competition/concentration characteristics that would empower bank managers to prevent bad loans.

Despite the literature review that is presented, we identify areas for future research that academics should pursue to gain a thorough understanding of the factors that influence NPLs, globally. Firstly, perform a direct study toward an interdisciplinary and broken-down analysis of borrowers and collateral. Such a disaggregated inquiry might produce illuminating findings and uncover fresh information. Secondly, few empirical studies have been performed on NPLs by applying current ideas to various regions, country clusters, and political systems. For example, why do certain countries perform better than others? Policymakers and regulators should carefully consider the consequences of this query. Thirdly, focus research on sensible stress testing and pro-cyclical applications. Moreover, in the context of the recent discussion about potential interest rate increases, this would be practically interesting. Finally, direct research on prudent stress testing and pro-cyclical applications. This would be intriguing, practically speaking, considering the ongoing debate about interest rate increases that are expected to dictate how loans perform in the future.

Author Contributions

Conceptualization, K.A.; methodology, K.A. and E.K.; software, A.H.; validation, E.K.; formal analysis, K.A. and E.K.; investigation, K.A.; resources, K.A.; data curation, A.H.; writing—original draft preparation, K.A.; writing—review and editing, E.K.; visualization, A.H.; supervision, E.K.; project administration, E.K.; All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The data used in this study is available from the corresponding author upon request.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

{kind=link}

{kind=link}

{kind=link}

Table A1.

Synthesis of Empirical Studies Related to NPLs.

| Author (s) | Method | Macroeconomic Factors | Industry-Specific | Bank-Specific Factors | Country and Period of Study | Key Findings |

|---|---|---|---|---|---|---|

| Keeton and Morris (1987) [27] | Dynamic panel data | X | X | USA (1979–1985) | The results suggest that local economic conditions and bad sector performance are reasons for higher NPLs. | |

| Sinkey and Greenawalt (1989) [30] | Log-linear regression model | X | X | USA (1984–1987) | The findings reveal that loan-loss rates are positively associated with loan rates. However, banks with adequate capital tend to have lower loss rates. | |

| Berger and DeYoung (1997) [14] | Granger causality approach | X | USA (1985–1994) | Cost efficiency plays a key role in future bad loans. | ||

| Kwan and Eisenbeis (1997) [25] | Simultaneous equations model | X | USA (1986–1995) | A U-shaped relationship is detected between inefficiency and loan growth. | ||

| Keeton (1999) [17] | Surveys and reports | X | USA (1982–1996) | The results suggest that business loan growth and business credit change in loan growth are not always due to shifts in supply. | ||

| Fernández et al. (2000) [73] | Government and bank reports | X | X | Spain (1963–1999) | During a boom period, credit disbursement is high; loans are given without considering the quality of loans. Thus, in a downturn period, NPLs will increase. | |

| Salas and Saurina (2002) [26] | Panel data approach | X | X | Spain (1985–1997) | GDP, firms and family indebtedness, rapid past credit, inefficiency, size, net interest margin, and market power are major variables that explain NPLs. | |

| Kalirai and Scheicher (2002) [74] | Dynamic panel data analysis (OLS) | X | Austria (1990–2001) | A rise in the short rate, a fall in business confidence, and a decline in the stock market have effects on loan loss provision, which in turn affect NPLs. | ||

| Jiménez and Saurina (2002) [75] | Dynamic model | X | Spain (1984–2003) | During a boom period, bank managers tend to lend excessively despite herd behavior and agency problems. | ||

| Nishimura and Kawamoto (2003) [76] | Government reports | X | Japan (1990–2000) | The study suggests that a major fragment that is given during the economic boom becomes bad loans as the economy shows a receding trend. | ||

| Rajan and Dhal (2003) [32] | Panel regression model | X | X | Indian banks in 2003 | The empirical results suggest that NPLs are influenced by terms of credit, bank size, and macroeconomic factors. | |

| Shih (2004) [77] | Interviews, policies, internal data | X | X | China (2004) | The findings strongly suggest that political considerations play a significant role in shaping financial policies in China. | |

| Hu et al. (2004) [33] | Dynamic panel data GMM/OLS estimates | X | Taiwan (1996–1999) | The results show that NPLs decrease the ratio of government shareholding, and bank size is negatively related to NPLs. In addition, banks established after deregulation have a lower rate of NPLs. | ||

| Girardone et al. (2004) [78] | Fourier-flexible stochastic | X | Italy (1993–1996) | Inefficiencies appear to be inversely associated with capital strength and positively correlated with NPLs. | ||

| Babouček and Jančar (2005) [79] | Impulsive response and unrestricted VAR | X | Czech Republic (1993–2004) | The results reveal that both external stability and price stability are compatible with banking sector stability. Due increase NPLs will cause a rising trade deficit. In addition to that, a rise in NPLs will mitigate the growth of the unemployment rate. | ||

| Lu et al. (2005) [80] | Logit regression | X | China (1994–1999) | The empirical findings suggest that Chinese banks have a systematic lending bias in favor of state-owned enterprises. | ||

| Ghosh (2005) [81] | Fixed effects and dynamic GMM estimations | X | X | India (1993–2004) | The findings suggest that lagged leverage is an important indicator of bad loans of banks. | |

| Fofack (2005) [7] | Econometric and causality analysis | X | X | Sub-Saharan Africa (1990) | The findings suggest that there is a dramatic and significant difference between Central African countries and Non-Central African countries. In addition to that, there is a strong causality between bad loans and macroeconomic factors. | |

| Jimenez and Saurina (2006) [49] | GMM estimations | X | Spain (1984–2002) | The empirical results find dedicated support for a positive relationship between rapid credit growth and loan loss. Moreover, three is robust evidence that during the boom period, risker borrowers get bank loans while collateralized loans decrease. | ||

| Rinaldi and Sanchis-Arellano (2006) [59] | Unbalanced and balanced estimation | X | EU countries (1989–2004) | The findings suggest that the financial conditions of households might become more vulnerable to adverse shocks in their income. | ||

| Berge and Boye (2007) [4] | Panel regression | X | Nordic banking sector (1993–2005) | The results reveal that the decline of NPLs is primarily attributed to the development in the real interest rate and unemployment. | ||

| Quagliarello (2007) [82] | Static and dynamic model | X | X | Italy (1985–2002) | The findings confirm the business cycle affects banks’ loan loss provision and new bad debt. | |

| Podpiera and Weill (2008) [18] | GMM dynamic panel | X | X | Czech Republic (1994–2005) | The findings support the bad management hypothesis in which the deterioration of cost efficiency led to increasing in NPLs. | |

| Rossi et al. (2009) [19] | Granger causality approach | X | X | Austria (1997–2003) | The empirical results find that, although diversification is negatively correlated with cost efficiency, it increases profit efficiency and reduces banks’ credit risk. | |

| Boudriga et al. (2010) [83] | Pooled regression approach | X | X | MENA (2002–2006) | The results find that among bank-specific factors, higher credit growth and foreign participation reduce NPLs. Additionally, the role of the institutional environment in enhancing bank credit quality. Better control of corruption, sound regulatory quality, better enforcement of the rule of law, and accountability play a significant role in reducing NPLs in the MENA region. | |

| Barseghyan (2010) [84] | Two-period overlapping generations (OLG) | X | X | Japan (1990–2003) | The existence of NPLs, combined with a delay in the bailout, leads to a persistent decline in economic activity. | |

| Espinoza et al. (2010) [6] | System GMM, panel vector autoregressive | X | X | MENA—GCC countries (1995–2008 | The study supports the view that both macro- and bank-specific factors play a key role in determining NPLs. | |

| Reinhart and Rogoff (2011) [68] | Vector autoregression | X | Global (1800–2009) | The study examines a sample of 290 banking crises and 209 sovereign episodes. Banking crises are importantly preceded by increasing private indebtedness. | ||

| Nkusu (2011) [56] | Panel regression and panel vector autoregressive | X | X | Global (1998–2009) | The findings confirm that adverse macroeconomic development is associated with rising of NPLs. | |

| Agoraki et al. (2011) [44] | Dynamic model | X | X | X | Central and Eastern European countries (1998–2005) | The empirical results reveal that banks with market power tend to take on lower credit risk and have a lower probability of default. |

| De Bock and Demyanets (2012) [52] | Dynamic panel regression | X | X | Emerging countries (1996–2010) | The results find a significant link between banks’ asset quality, credit, and macroeconomic aggregates. Economic activity slows down when NPLs increase. | |

| Louzis et al. (2012) [20] | Dynamic panel regression | X | X | Greece (2003–2009) | NPLs in Greece can be explained mainly by macroeconomic and management quality. | |

| Messai and Jouini (2013) [85] | Panel data regression | X | X | EU (2004–2008) | The findings suggest that GDP growth and ROA have a negative impact on NPLs. The unemployment rate and the real interest rate have a positive effect on NPLs. | |

| Klein (2013) [29] | Dynamic panel regression | X | X | EU (1998–2011) | The results find that NPLs can be attributed to both macroeconomic and bank-specific factors. Interestingly, the bank-level effects were significant during pre-crisis and post-crisis. | |

| Castro (2013) [86] | Dynamic panel regression | X | EU—GIPSI countries (1997q1–2011q3) | The banking credit risk is significantly affected by the macroeconomic environment. In addition to the global financial crisis, several robustness tests confirmed the results. | ||

| Makri et al. (2014) [55] | Dynamic panel regression | X | X | EU (2000–2008) | The results confirm a strong relation between NPLs and macroeconomic factors (public debt, unemployment, growth rate of GDP) and bank-specific factors (CAR, ROE, rate of NPLs of the previous year). | |

| Ghosh (2015) [34] | Fixed effect and dynamic GMM | X | X | USA (1984–2013) | Greater capitalization, liquidity risks, poor credit quality, greater cost inefficiency, and bank size significantly increase NPLs. On the contrary, higher GDP and changes in state housing prices lower NPLs. | |

| Fu et al. (2014) [45] | Panel data model | X | X | X | Asian pacific economies (2003–2010) | The results suggest that greater concentration fosters financial fragility and that lower pricing levels will induce bank exposure. |

| Beck et al. (2015) [50] | Dynamic panel regression | X | Global (2000–2010) | Real GDP growth, share prices, exchange rates, and lending interest rates significantly affected NPLs. | ||

| Baselga-Pascual et al. (2015) [87] | System GMM estimator | X | X | Euro area (2001–2012) | Capitalization, profitability, efficiency, and liquidity are inversely related to bank risk. Less -concentrated markets, lower interest rates, higher inflation, and falling GDP increase bank risk | |

| Touny and Shehab (2015) [88] | Dynamic panel regression | X | Arab countries (2000–2012) | The findings suggest that the inflation rate, improvement in macroeconomic and financial conditions, and the global financial crisis have a significant negative relation with NPLs. While household consumption found a negative impact in non-petroleum countries, petroleum countries had a positive effect. | ||

| Chaibi and Ftiti (2015) [89] | GMM estimations | X | X | France and Germany (2005–2011) | The results indicate that expectations for inflation rates in both counties are influenced by a set of macroeconomic factors used in the paper. Additionally, the findings reveal that France is more susceptible to bank-specific than Germany. | |

| Rajha (2016) [35] | Panel data regression | X | X | Jordan (2008–2012) | Among other bank-specific factors, the lagged NPLs and the ratio of loans to total assets are the most crucial factors that affect NPLs. Regarding macroeconomic factors, economic growth and inflation have negative influences on NPLs. Along with this, the global financial crisis is positively correlated with NPLs. | |

| Agarwal et al. (2016) [90] | Logistic model | X | USA (2003–2007) | Condominium loan defaults grow at a faster rate. The greater default level and growth rate are consistent with investor expectations. | ||

| González (2017) [91] | Panel data estimates. OLS, fixed effect, and random effect | X | X | X | MENA (2005–2012) | The findings suggest the U-shaped relation between banks’ competition and banks’ risk-taking. Both competition-stability and competition-fragility can be applied at the same time in the MENA region. |

| Amuakwa-Mensah et al. (2017) [92] | Dynamic, state, and impulse response analysis | X | X | Ghana (1997–2011) | NPLs are significantly affected by both bank-specific factors and macroeconomic factors. The role of the global financial crisis was observed to be conditional on NPLS. | |

| Ghosh (2017) [58] | Static and dynamic estimation | X | USA (1992q4–2016q1) | Total NPLs have the most effect on US housing prices and real GDP growth. At disaggregate levels, non-performing construction, land development, and C&I loans have the most persistent impact on sector-specific growth. | ||

| Bashir et al. (2017) [69] | Two-step system GMM dynamic panel | X | X | X | China (2000–2014) | The high transparency in the Chinese banking sector reduces poor-quality assets, but not in the case of state-owned banks, while an increase in competition increases NPLs. |

| Kjosevski and Petkovski (2017) [93] | Panel data analysis | X | X | Baltic states (2005–2014) | The main determinants that influence NPLs were, among others, macroeconomic and bank-specific factors. | |

| Ghosh (2018) [70] | 3SLS method | X | MENA (2001–2012) | The findings confirm the bad luck hypothesis and the gamble for resurrection hypothesis to be equally relevant. Hoverer, this behavior is different between oil-exporters and oil-importers countries. | ||

| Ghosh (2018) [94] | Panel data fixed effects estimation | X | X | USA (1999Q1–2016Q3) | Greater regulatory capital, more diversification, higher profits, and cost efficiency reduce the charge-off rate. On the contrary, a higher share of loans and a higher share of real estate loans have a significant impact on loan performance. Strong macroeconomics reduces loan charge-offs. | |

| Vo (2018) [95] | Dynamic estimation technique | X | X | X | Vietnam (2006–2015) | The findings suggest that bank lending behavior is significantly influenced by both bank-specific factors and macroeconomic factors. |

| Cui et al. (2018) [96] | Panel regression techniques | X | China (2009–2015) | The results find that green loans to total loans do reduce banks’ NPLs. | ||

| Koju et al. (2018) [97] | Static and dynamic panel estimation | X | X | Nepal (2003–2015) | NPLs have a significant positive relation with bank size, inefficiency, and export-to-import ratio while a negative relation with GDP, CAR, and inflation. | |

| Bapat (2018) [98] | Dynamic panel data analysis | X | X | India (2006/2007–2012/2013) | Among others, NPLs and the cost-to-income ratio negatively affect bank profitability. | |

| Jabbouri and Naili (2019) [99] | Panel data analysis | X | X | MENA (2003–2016) | The results show that bank size, capital adequacy ratio, bank operation efficiency profitability, GDP growth, unemployment, inflation, and public debt represent the main determinants of NPLs. | |

| Bayar (2019) [100] | GMM dynamic panel | X | X | Emerging countries (2000–2013) | The findings reveal that economic growth, inflation, institutional quality, ROA, ROE, CAR, and non-interest income affect NPLs negatively, while unemployment, public debt, credit growth, lagged value of NPLs, cost-to-income ratio, and global financial crisis affect NPLs positively. | |

| Rachid (2019) [101] | Panel data analysis | X | X | MENA and CEE countries (1997–2016) | The empirical results find that rule of law increases NPLs in MENA while decreasing NPLs in CEE. Moreover, the global financial crisis has a significant role in the accumulation of NPLs in MENA countries. | |

| Gulati et al. (2019) [102] | System GMM approach | X | X | X | India (1998/99–2014/15) | Lower profitability, more diversification, large size, and higher concentration increase the probability of default in the Indian banking system. |

| Kuzucu and Kuzucu (2019) [103] | Dynamic panel estimations | X | X | Emerging and Advanced economies (2001–2015) | Real GDP growth is the main determinant that affects NPLs, and NPLs exhibit high persistence for both emerging and advanced economies in pre-crisis and post-crisis | |

| Farooq et al. (2019) [104] | Two-step GMM | X | X | GCC countries (2009–2015) | The empirical findings generated from the bad management hypothesis, bad luck, asset size, and combined theories are statistically significant. | |

| Ghosh (2019) [105] | Regression analysis | X | X | X | MENA (2000–2012) | The results suggest credit reporting system reforms lead to a decline NPLs. Among others, the efficiency of credit reporting systems is much less compelling during the crisis. |

| Anastasiou et al. (2019) [106] | OLS and Bayesian panel-cointegration vector autoregression | X | X | Euro area (2003q1–2016q1) | NPLs in the Euro area have performed an upward shift after 2008 and are mostly related to worsening macroeconomic conditions. | |

| Mahrous et al. (2020) [107] | Dynamic panel GMM and threshold | X | MENA (1997–2017) | The findings indicate the relationship between monetary policy and credit risk is positive and significant to a certain threshold 6.3. | ||

| Betz et al. (2020) [108] | Survival analysis | X | Sample of defaulted bank loans in USA, Great Britain, and Canada | Frailties have a huge impact on the resolution time of NPLs. Moreover, the findings suggest that the resolution of NPLs is a key determinant of bank credit default losses. | ||

| Gupta et al. (2020) [109] | Fixed effect and GMM | X | X | X | India (1999–2016) | The main findings suggest that private banks are more capitalized and operate more efficiently than public banks. |

| Boussaada et al. (2020) [110] | PSTR model | X | X | MENA (2004–2017) | The results suggest that there is a threshold effect on liquidity risk and NPLs. | |

| Ahmed et al. (2021) [111] | System GMM estimation | X | X | Pakistan (2008–2018) | Credit growth, net interest margin, loan loss provision, and bank diversification increase NPLs while operating efficiency, bank size, and ROA reduce NPLs. Regarding macroeconomic factors, GDP decreases NPLs while interest rate, exchange rate, and political risk increase NPLs. | |

| Katusiime (2021) [112] | ARDL approach | X | X | Uganda (2000q1–2021q1) | The findings suggest that COVID-19 has a significant negative effect only in the long run. In the short-run bank, profitability negatively affects NPLs, liquidity ratio, and market sensitivity. | |

| Kılıç Depren and Kartal (2021) [113] | Predictive analysis, multivariate adaptive regression splines | X | X | Turkey (2005–2019) | The results find that credits, the US dollar to Turkish lira exchange rate, and unemployment are the most significant factors in defining NPLs. | |

| Alnabulsi and Kozarevic (2021) [114] | Multiple linear regression model | X | Jordan (2006–2019) | The findings suggest that for economic growth factors such as GDP growth and unemployment, there is a negative relation with NPLs. While for financial stability indicators such as lending interest rate and capital adequacy ratio, there is a positive relation with NPLs. | ||

| Syed and Aidyngul (2022) [115] | Dynamic GMM technique | X | X | Developing and developed countries (1995–2019) | The common macroeconomic and bank-specific affect NPLs among both developed and developing countries. | |

| Taghizadeh-Hesary et al. (2022) [116] | Vector autoregressive approach | X | X | ASEAN member states (pre-COVID and post-COVID) | The empirical results prove that the loan default ratio is the optimal credit guarantee ratio’s main indicator. In addition, in the ASEAN region, the credit guarantee needs to be increased to help SMEs in the wake of COVID-19. | |

| Abusharbeh (2022) [117] | Fixed and random effect estimates | X | X | Palestine (2007–2018) | The results of the fixed effect prove that interest and credit supply are positively correlated with NPLs, while profitability has significant negative relation with NPLs. | |

| Naili and Lahrichi (2022) [118] | Dynamic GMM technique | X | X | MENA (2000–2019) | The results suggest that GDP growth, unemployment, bank capitalization, bank performance, bank operating inefficiency, bank concentration, inflation, sovereign debt, and bank size are the main factors that affect NPLs. | |

| Alnabulsi et al. (2022) [47] | System generalized method of moment | X | X | X | MENA (2005–2020) | The empirical findings suggest that NPLs are more sensitive to bank-specific factors than macroeconomic factors. In addition, the financial environment and institutional quality significantly affect NPLs. |

Source: The Authors based on studies related to NPLs.

References

- Cingolani, M. Finance capitalism: A look at the European financial accounts. Panoeconomicus 2013, 60, 249–290. [Google Scholar] [CrossRef]

- Saunders, A.; Corner, M. Financial Institutions Management: A Risk Management Approach, 8th ed.; McGraw-Hill Education: New York, NY, USA, 2008. [Google Scholar]

- Samad, A. Credit risk determinants of bank failure: Evidence from US bank failure. Int. Bus. Res. 2012, 5, 10–15. [Google Scholar] [CrossRef]

- Berge, O.; Boye, G. An analysis of banks’ problem loans. Econ. Bull. 2007, 2, 65–76. [Google Scholar]

- Umar, M.; Sun, G. Determinants of non-performing loans in Chinese banks. J. Asia Bus. Stud. 2018, 12, 273–289. [Google Scholar] [CrossRef]

- Espinoza, R.; Prasad, A. Nonperforming Loans in the GCC Banking Systems and Their Macroeconomic Effects; IMF Working Paper 10/224; International Monetary Fund: Washington, DC, USA, 2010. [Google Scholar]

- Fofack, H. Nonperforming Loans in Sub-Saharan Africa: Causal Analysis and Macroeconomic Implications; Working Paper No. 3769; World Bank Policy Research: Washington, DC, USA, 2005. [Google Scholar]

- Vom Brocke, J.; Simons, A.; Niehaves, B.; Niehaves, B.; Reimer, K.; Plattfaut, R.; Cleven, A. Reconstructing the giant: On the importance of rigour in documenting the literature search process. In Proceedings of the ECIS 2009, Verona, Italy, 8–10 June 2009. [Google Scholar]

- Nikolopoulos, K.I.; Tsalas, A.I. Non-performing Loans: A Review of the Literature and the International Experience. In Non-Performing Loans and Resolving Private Sector Insolvency: Experiences from the EU Periphery and the Case of Greece; Monokroussos, P., Gortsos, C., Eds.; Springer: Cham, Stwitzerland, 2017; pp. 47–68. [Google Scholar] [CrossRef]

- Manz, F. Determinants of non-performing loans: What do we know? A systematic review and avenues for future research. Manag. Rev. Q. 2019, 69, 351–389. [Google Scholar] [CrossRef]

- Krueger, R. International Standards for Impairment and Provisions and Their Implications for Financial Soundness Indicators (FSIs); International Monetary Fund: Washington, DC, USA, 2002. [Google Scholar]

- International Monetary Fund. Financial Soundness Indicators: Compilation Guide; International Monetary Fund: Washington, DC, USA, 2006; ISBN 978-1-58906-385-3. [Google Scholar]

- BCBS International Convergence of Capital Measurement and Capital Standards: A Revised Framework Comprehensive Version; Bank for International Settlements: Basel, Switzerland, 2006; Available online: https://www.bis.org/publ/bcbs128.htm (accessed on 19 January 2023).

- Berger, A.; DeYoung, R. Problem loans and cost efficiency in commercial banks. J. Bank. Financ. 1997, 21, 849–870. [Google Scholar] [CrossRef] [Green Version]

- Angklomkliew, S.; George, J.; Packer, F. Issues and Developments in Loan Loss Provisioning: The Case of Asia. BIS Q. Rev. 2009, 69–83. Available online: https://ssrn.com/abstract=1519809 (accessed on 19 January 2023).

- Bown, M.; Sutton, A. Quality control in systematic reviews and meta-analyses. Eur. J. Vasc. Endovasc. Surg. 2010, 40, 669–677. [Google Scholar] [CrossRef] [Green Version]

- Keeton, W. Does faster loan growth lead to higher loan losses? Econ. Rev. Fed. Reserve Bank Kans. City 1999, 84, 57–75. [Google Scholar]

- Podpiera, J.; Weill, L. Bad luck or bad management? Emerging banking market experience. J. Financ. Stab. 2008, 4, 135–148. [Google Scholar] [CrossRef] [Green Version]

- Rossi, S.; Schwaiger, M.; Winkler, G. How loan portfolio diversification affects risk, efficiency and capitalization: A managerial behavior model for Austrian banks. J. Bank. Financ. 2009, 33, 2218–2226. [Google Scholar] [CrossRef]

- Louzis, D.; Vouldis, A.; Metaxas, V. Macroeconomic and bank-specific determinants of non-performing loans in Greece: A comparative study of mortgage, business and consumer loan portfolios. J. Bank. Financ. 2012, 36, 1012–1027. [Google Scholar] [CrossRef]

- Dimitrios, A.; Helen, L.; Mike, T. Determinants of non-performing loans: Evidence from Euro-area countries. Financ. Res. Lett. 2016, 18, 116–119. [Google Scholar] [CrossRef]

- Konstantakis, K.; Michaelides, P.; Vouldis, A. Non performing loans (NPLs) in a crisis economy: Long-run equilibrium analysis with a real time VEC model for Greece (2001–2015). Phys. A Stat. Mech. Its Appl. 2016, 451, 149–161. [Google Scholar] [CrossRef]

- Berg, S.; Førsund, F.; Jansen, E. Malmquist indices of productivity growth during the deregulation of Norwegian banking, 1980–89. Scand. J. Econ. 1992, 94, S211–S228. [Google Scholar] [CrossRef]

- Hughes, J.; Mester, L. A quality and risk-adjusted cost function for banks: Evidence on the “too-big-to-fail” doctrine. J. Product. Anal. 1993, 4, 293–315. [Google Scholar] [CrossRef]

- Kwan, S.; Eisenbeis, R. Bank risk, capitalization, and operating efficiency. J. Financ. Serv. Res. 1997, 12, 117–131. [Google Scholar] [CrossRef]

- Salas, V.; Saurina, J. Credit risk in two institutional regimes: Spanish commercial and savings banks. J. Financ. Serv. Res. 2002, 22, 203–224. [Google Scholar] [CrossRef]

- Keeton, R.; Morris, S. Why do banks’ loan losses differ. Econ. Rev. 1987, 72, 3–21. [Google Scholar]

- Goczek, Ł.; Malyarenko, N. Loan loss provisions during the financial crisis in Ukraine. Post-Communist Econ. 2015, 27, 472–496. [Google Scholar] [CrossRef]

- Klein, N. Non-Performing Loans in CESEE: Determinants and Impact on Macroeconomic Performance; IMF Working Paper WP/13/72; International Monetary Fund: Washington, DC, USA, 2013. [Google Scholar]

- Sinkey, J.; Greenawalt, M. Loan-loss experience and risk-taking behavior at large commercial banks. J. Financ. Serv. Res. 1991, 5, 43–59. [Google Scholar] [CrossRef]

- Us, V. Dynamics of non-performing loans in the Turkish banking sector by an ownership breakdown: The impact of the global crisis. Financ. Res. Lett. 2017, 20, 109–117. [Google Scholar] [CrossRef]

- Rajan, R.; Dhal, S. Non-performing loans and terms of credit of public sector banks in India: An empirical assessment. Reserve Bank India Occas. Pap. 2003, 24, 81–121. [Google Scholar]

- Hu, J.; Li, Y.; Chiu, Y. Ownership and nonperforming loans: Evidence from Taiwan’s banks. Dev. Econ. 2004, 42, 405–420. [Google Scholar] [CrossRef]

- Ghosh, A. Banking-industry specific and regional economic determinants of non-performing loans: Evidence from US states. J. Financ. Stab. 2015, 20, 93–104. [Google Scholar] [CrossRef]

- Rajha, K.S. Determinants of non-performing loans: Evidence from the Jordanian banking sector. J. Financ. Bank Manag. 2016, 4, 125–136. [Google Scholar] [CrossRef] [Green Version]

- Swamy, V. Impact of macroeconomic and endogenous factors on nonperforming banks assets. Int. J. Bank. Financ. 2012, 9, 26–47. [Google Scholar] [CrossRef] [Green Version]

- García-Marco, T.; Robles-Fernández, M. Risk-taking behaviour and ownership in the banking industry: The Spanish evidence. J. Econ. Bus. 2008, 60, 332–354. [Google Scholar] [CrossRef]

- Keeley, M. Deposit insurance, risk, and market power in banking. Am. Econ. Rev. 1990, 80, 1183–1200. [Google Scholar]

- Matutes, C.; Vives, X. Imperfect competition, risk taking, and regulation in banking. Eur. Econ. Rev. 2000, 44, 1–34. [Google Scholar] [CrossRef]

- Hellmann, T.; Murdock, K.; Stiglitz, J. Liberalization, moral hazard in banking, and prudential regulation: Are capital requirements enough? Am. Econ. Rev. 2000, 90, 147–165. [Google Scholar] [CrossRef] [Green Version]

- Allen, F.; Gale, D. Competition and financial stability. J. Money Credit Bank. 2004, 36, 453–480. [Google Scholar] [CrossRef] [Green Version]

- Boyd, J.; De Nicolo, G. The theory of bank risk taking and competition revisited. J. Financ. 2005, 60, 1329–1343. [Google Scholar] [CrossRef]

- Schaeck, K.; Cihak, M.; Wolfe, S. Are competitive banking systems more stable? J. Money Credit Bank. 2009, 41, 711–734. [Google Scholar] [CrossRef] [Green Version]

- Agoraki, M.; Delis, M.; Pasiouras, F. Regulations, competition and bank risk-taking in transition countries. J. Financ. Stab. 2011, 7, 38–48. [Google Scholar] [CrossRef] [Green Version]

- Fu, X.; Lin, Y.; Molyneux, P. Bank competition and financial stability in Asia Pacific. J. Bank. Financ. 2014, 38, 64–77. [Google Scholar] [CrossRef]

- Kasman, S.; Kasman, A. Bank competition, concentration and financial stability in the Turkish banking industry. Econ. Syst. 2015, 39, 502–517. [Google Scholar] [CrossRef]

- Alnabulsi, K.; Kozarević, E.; Hakimi, A. Assessing the determinants of non-performing loans under financial crisis and health crisis: Evidence from the MENA banks. Cogent Econ. Financ. 2022, 10, 2124665. [Google Scholar] [CrossRef]

- Bernanke, B.; Gertler, M. Agency Costs, Net Worth, and Business Fluctuations. Am. Econ. Rev. 1989, 79, 14–31. [Google Scholar]

- Jimenez, G.; Saurina, J. Credit cycles, credit risk, and prudential regulation. Int. J. Cent. Bank. 2006, 2, 65–98. [Google Scholar]

- Beck, R.; Jakubik, P.; Piloiu, A. Key determinants of non-performing loans: New evidence from a global sample. Open Econ. Rev. 2015, 26, 525–550. [Google Scholar] [CrossRef]

- Carey, M. Credit risk in private debt portfolios. J. Financ. 1998, 53, 1363–1387. [Google Scholar] [CrossRef]

- De Bock, M.; Demyanets, M. Bank Asset Quality in Emerging Markets: Determinants and Spillovers; International Monetary Fund: Washington, DC, USA, 2012. [Google Scholar]

- Bofondi, M.; Ropele, T. Macroeconomic Determinants of Bad Loans: Evidence from Italian Banks’; Bank of Italy Occasional Paper; Bank of Italy: Rome, Italy, 2011. [Google Scholar]

- Moinescu, B.G. Determinants of nonperforming loans in Central and Eastern European Countries: Macroeconomic indicators and credit discipline. Rev. Econ. Bus. Stud. 2012, 10, 47–58. [Google Scholar]

- Makri, V.; Tsagkanos, A.; Bellas, A. Determinants of non-performing loans: The Case of Eurozone. Panoeconomicus 2014, 61, 193–206. [Google Scholar] [CrossRef] [Green Version]

- Nkusu, M. Non-Performing Loans and Macro-Financial Vulnerabilities in Advanced Economies; IMF Working Paper 11/161; International Monetary Fund: Washington, DC, USA, 2011. [Google Scholar]

- Zhang, D.; Cai, J.; Dickinson, D.; Kutan, A. Non-performing loans, moral hazard and regulation of the Chinese commercial banking system. J. Bank. Financ. 2016, 63, 48–60. [Google Scholar] [CrossRef]

- Ghosh, A. Sector-specific analysis of non-performing loans in the US banking system and their macroeconomic impact. J. Econ. Bus. 2017, 93, 29–45. [Google Scholar] [CrossRef]

- Rinaldi, L.; Sanchis-Arellano, A. Household Debt Sustainability: What Explains Household Nonperforming Loans? An Empirical Analysis; ECB Working Paper Series No. 570; European Central Bank: Frankfurt am Main, Germany, 2006. [Google Scholar]

- Reinhart, C. From health crisis to financial distress. IMF Econ. Rev. 2022, 70, 4–31. [Google Scholar] [CrossRef]

- Aiyar, S.; Bergthaler, W.; Garrido, J.M.; Ilyina, A.; Jobst, A.; Kang, K.; Kovtun, D.; Liu, Y.; Monaghan, D.; Moretti, M. A strategy for resolving Europe’s problem loans. Eur. Econ. 2017, 1, 87–95. [Google Scholar] [CrossRef]

- Accornero, M.; Alessandri, P.; Carpinelli, L.; Sorrentino, A.M. Non-Performing Loans and the Supply of Bank Credit: Evidence from Italy; Bank of Italy Occasional Paper; Bank of Italy: Rome, Italy, 2017. [Google Scholar] [CrossRef] [Green Version]

- Žunić, A.; Kozarić, K.; Dželihodžić, E.Ž. Non-performing loan determinants and impact of covid-19: Case of Bosnia and Herzegovina. J. Cent. Bank. Theory Pract. 2021, 10, 5–22. [Google Scholar] [CrossRef]

- Ari, A.; Chen, S.; Ratnovski, L. The dynamics of non-performing loans during banking crises: A new database with post-COVID-19 implications. J. Bank. Financ. 2021, 133, 106140. [Google Scholar] [CrossRef]

- Apergis, N. Convergence in non-performing loans across EU banks: The role of COVID-19. Cogent Econ. Financ. 2022, 10, 2024952. [Google Scholar] [CrossRef]

- Beck, T.; Keil, J. Have banks caught corona? Effects of COVID on lending in the US. J. Corp. Financ. 2022, 72, 102160. [Google Scholar] [CrossRef]

- Dursun-de Neef, H.Ö.; Schandlbauer, A. COVID-19 and lending responses of European banks. J. Bank. Financ. 2021, 133, 106236. [Google Scholar] [CrossRef] [PubMed]

- Reinhart, C.; Rogoff, K. From financial crash to debt crisis. Am. Econ. Rev. 2011, 101, 1676–1706. [Google Scholar] [CrossRef] [Green Version]

- Bashir, U.; Yu, Y.; Hussain, M.; Wang, X.; Ali, A. Do banking system transparency and competition affect nonperforming loans in the Chinese banking sector? Appl. Econ. Lett. 2017, 24, 1519–1525. [Google Scholar] [CrossRef]

- Ghosh, S. Bad luck, Bad policy or Bad banking? Understanding the financial management behavior of MENA banks. J. Multinatl. Financ. Manag. 2018, 47, 110–128. [Google Scholar] [CrossRef]

- Juodis, A.; Karavias, Y.; Sarafidis, V. A homogeneous approach to testing for Granger non-causality in heterogeneous panels. Empir. Econ. 2021, 60, 93–112. [Google Scholar] [CrossRef]

- Ditzen, J.; Karavias, Y.; Westerlund, J. Testing and estimating structural breaks in time series and panel data in stata. arXiv 2021, arXiv:2110.14550. [Google Scholar]

- Abusharbeh, M.T. Determinants of credit risk in Palestine: Panel data estimation. Int. J. Financ. Econ. 2022, 27, 3434–3443. [Google Scholar] [CrossRef]

- Agarwal, S.; Deng, Y.; Luo, C.; Qian, W. The hidden peril: The role of the condo loan market in the recent financial crisis. Rev. Financ. 2016, 20, 467–500. [Google Scholar] [CrossRef]

- Ahmed, S.; Majeed, M.E.; Thalassinos, E.; Thalassinos, Y. The impact of bank specific and macro-economic factors on non-performing loans in the banking sector: Evidence from an emerging economy. J. Risk Financ. Manag. 2021, 14, 217. [Google Scholar] [CrossRef]

- Alnabulsi, K.; Kozarević, E. Interdependence between non-performing loans, financial stability and economic growth. In Proceedings of the 10th International Scientific Symposium “Region, Entrepreneurship, Development” (RED 2021), Osijek, Croatia, 17 June 2021; Leko Šimić, M., Crnković, B., Eds.; 2021. Available online: http://www.efos.unios.hr/red/wp-content/uploads/sites/20/2021/07/RED_2021_Proceedings.pdf (accessed on 19 January 2023).

- Amuakwa-Mensah, F.; Marbuah, G.; Ani-Asamoah Marbuah, D. Re-examining the determinants of non-performing loans in Ghana’s banking industry: Role of the 2007–2009 financial crisis. J. Afr. Bus. 2017, 18, 357–379. [Google Scholar] [CrossRef]

- Anastasiou, D.; Louri, H.; Tsionas, M. Nonperforming loans in the euro area: A re core–periphery banking markets fragmented? Int. J. Financ. Econ. 2019, 24, 97–112. [Google Scholar] [CrossRef] [Green Version]

- Babouček, I.; Jančar, M. Effects of Macroeconomic Shocks to the Quality of the Aggregate Loan Portfolio (Vol. 22); Czech National Bank Working Paper Series 1; Czech National Bank: Praha, Czech, 2005. [Google Scholar]

- Bapat, D. Profitability drivers for Indian banks: A dynamic panel data analysis. Eurasian Bus. Rev. 2018, 8, 437–451. [Google Scholar] [CrossRef]

- Barseghyan, L. Non-performing loans, prospective bailouts, and Japan’s slowdown. J. Monet. Econ. 2010, 57, 873–890. [Google Scholar] [CrossRef]

- Baselga-Pascual, L.; Trujillo-Ponce, A.; Cardone-Riportella, C. Factors influencing bank risk in Europe: Evidence from the financial crisis. N. Am. J. Econ. Financ. 2015, 34, 138–166. [Google Scholar] [CrossRef]

- Bayar, Y. Macroeconomic, institutional and bank-specific determinants of non-performing loans in emerging market economies: A dynamic panel regression analysis. J. Cent. Bank. Theory Pract. 2019, 8, 95–110. [Google Scholar] [CrossRef] [Green Version]

- Betz, J.; Krüger, S.; Kellner, R.; Rösch, D. Macroeconomic effects and frailties in the resolution of non-performing loans. J. Bank. Financ. 2020, 112, 105212. [Google Scholar] [CrossRef]

- Boudriga, A.; Taktak, N.; Jellouli, S. Bank Specific, Business and Institutional Environment Determinants of Banks Nonperforming Loans: Evidence from Mena Countries; Working Paper 547; Economic Research Forum: Cario, Egypt, 2010; pp. 1–28. [Google Scholar]

- Boussaada, R.; Hakimi, A.; Karmani, M. Is there a threshold effect in the liquidity risk–non-performing loans relationship? A PSTR approach for MENA banks. Int. J. Financ. Econ. 2020, 27, 1886–1898. [Google Scholar] [CrossRef]

- Castro, V. Macroeconomic determinants of the credit risk in the banking system: The case of the GIPSI. Econ. Model. 2013, 31, 672–683. [Google Scholar] [CrossRef] [Green Version]

- Chaibi, H.; Ftiti, Z. Credit risk determinants: Evidence from a cross-country study. Res. Int. Bus. Financ. 2015, 33, 1–16. [Google Scholar] [CrossRef]

- Cui, Y.; Geobey, S.; Weber, O.; Lin, H. The impact of green lending on credit risk in China. Sustainability 2018, 10, 2008. [Google Scholar] [CrossRef] [Green Version]

- Farooq, M.O.; Elseoud, M.; Turen, S.; Abdulla, M. Causes of non-performing loans: The experience of gulf cooperation council countries. Entrep. Sustain. Issues 2019, 6, 1955–1974. [Google Scholar] [CrossRef]

- Fernández de Lis, S.; Martínez, J.; Saurina, J. Credit Growth, Problem Loans and Credit Risk Provisioning in Spain; Working Paper 18; Servicio de Estudios; Banco de España: Valencia, Spain, 2000. [Google Scholar]

- Ghosh, A. Determinants of bank loan charge-off rates: Evidence from the USA. J. Financ. Regul. Compliance 2018, 26, 526–542. [Google Scholar] [CrossRef]

- Ghosh, S. Does leverage influence banks’ non-performing loans? Evidence from India. Appl. Econ. Lett. 2005, 12, 913–918. [Google Scholar] [CrossRef]

- Ghosh, S. Loan delinquency in banking systems: How effective are credit reporting systems? Res. Int. Bus. Financ. 2019, 47, 220–236. [Google Scholar] [CrossRef]

- Girardone, C.; Molyneux, P.; Gardener, E. Analysing the determinants of bank efficiency: The case of Italian banks. Appl. Econ. 2004, 36, 215–227. [Google Scholar] [CrossRef] [Green Version]

- González, L.; Razia, A.; Búa, M.; Sestayo, R. Competition, concentration and risk taking in Banking sector of MENA countries. Res. Int. Bus. Financ. 2017, 42, 591–604. [Google Scholar] [CrossRef]

- Gulati, R.; Goswami, A.; Kumar, S. What drives credit risk in the Indian banking industry? An empirical investigation. Econ. Syst. 2019, 43, 42–62. [Google Scholar] [CrossRef]

- Gupta, N.; Mahakud, J. Ownership, bank size, capitalization and bank performance: Evidence from India. Cogent Econ. Financ. 2020, 8, 1808282. [Google Scholar] [CrossRef]

- Jabbouri, I.; Naili, M. Determinants of nonperforming loans in emerging markets: Evidence from the MENA region. Rev. Pac. Basin Financ. Mark. Policies 2019, 22, 1950026. [Google Scholar] [CrossRef]

- Jiménez, G.; Saurina, J. Loan Characteristics and Credit Risk; Bank of Spain: Valencia, Spain, 2002; pp. 1–34. [Google Scholar]

- Kalirai, H.; Scheicher, M. Macroeconomic stress testing: Preliminary evidence for Austria. Financ. Stab. Rep. 2002, 3, 58–74. [Google Scholar]

- Katusiime, L. COVID 19 and bank profitability in low income countries: The case of Uganda. J. Risk Financ. Manag. 2021, 14, 588. [Google Scholar] [CrossRef]

- Kılıç Depren, S.; Kartal, T. Prediction on the volume of non-performing loans in Turkey using multivariate adaptive regression splines approach. Int. J. Financ. Econ. 2021, 26, 6395–6405. [Google Scholar] [CrossRef]

- Kjosevski, J.; Petkovski, M. Non-performing loans in Baltic States: Determinants and macroeconomic effects. Balt. J. Econ. 2017, 17, 25–44. [Google Scholar] [CrossRef] [Green Version]

- Koju, L.; Koju, R.; Wang, S. Macroeconomic and bank-specific determinants of non-performing loans: Evidence from Nepalese banking system. J. Cent. Bank. Theory Pract. 2018, 7, 111–138. [Google Scholar] [CrossRef] [Green Version]

- Kuzucu, N.; Kuzucu, S. What drives non-performing loans? Evidence from emerging and advanced economies during pre-and post-global financial crisis. Emerg. Mark. Financ. Trade 2019, 55, 1694–1708. [Google Scholar] [CrossRef]

- Lu, D.; Thangavelu, S.; Hu, Q. Biased lending and non-performing loans in China’s banking sector. J. Dev. Stud. 2005, 41, 1071–1091. [Google Scholar] [CrossRef]

- Mahrous, S.; Samak, N.; Abdelsalam, M. The effect of monetary policy on credit risk: Evidence from the MENA region countries. Rev. Econ. Political Sci. 2020, 5, 289–304. [Google Scholar] [CrossRef]

- Messai, A.; Jouini, F. Micro and macro determinants of non-performing loan. Int. J. Econ. Financ. Issues Econ J. 2013, 3, 852–860. [Google Scholar]

- Naili, M.; Lahrichi, Y. Banks’ credit risk, systematic determinants and specific factors: Recent evidence from emerging markets. Heliyon 2022, 8, e08960. [Google Scholar] [CrossRef] [PubMed]

- Nishimura, K.; Kawamoto, Y. Why does the problem persist? ‘Rational rigidity’ and the plight of Japanese banks. World Econ. 2003, 26, 301–324. [Google Scholar] [CrossRef]

- Quagliarello, M. Banks’ Riskiness over the Business Cycle: A Panel Analysis on Italian intermediaries. Appl. Financ. Econ. 2007, 17, 119–138. [Google Scholar] [CrossRef]

- Syed, A.A.; Aidyngul, Y. Macro economical and bank-specific vulnerabilities of nonperforming loans: A comparative analysis of developed and developing countries. J. Public Aff. 2022, 22, e2414. [Google Scholar] [CrossRef]

- Rachid, S. The determinants of non-performing loans: Do institutions matter? A comparative analysis of the Middle East and North Africa (MENA) and Central and Eastern European (CEE) countries. J. Adv. Stud. Financ. 2019, 10, 96–108. [Google Scholar]

- Shih, V. Dealing with non-performing loans: Political constraints and financial policies in China. China Q. 2004, 180, 922–944. [Google Scholar] [CrossRef]

- Taghizadeh-Hesary, F.; Phoumin, H.; Rasoulinezhad, E. COVID-19 and regional solutions for mitigating the risk of SME finance in selected ASEAN member states. Econ. Anal. Policy 2022, 74, 506–525. [Google Scholar] [CrossRef]

- Touny, M.; Shehab, M. Macroeconomic determinants of non-performing loans: An empirical study of some Arab countries. Am. J. Econ. Bus. Adm. 2015, 7, 11–22. [Google Scholar] [CrossRef] [Green Version]

- Vo, X.V. Bank lending behavior in emerging markets. Financ. Res. Lett. 2018, 27, 129–134. [Google Scholar] [CrossRef]

Figure 1.

Evolution of the percentage number of studies on NPLs per period. Source: The author’s calculation is based on prior studies.

Figure 1.

Evolution of the percentage number of studies on NPLs per period. Source: The author’s calculation is based on prior studies.

Figure 2.

Representation of the number of studies on NPLs per region. Source: The author’s calculation is based on prior studies.

Figure 2.

Representation of the number of studies on NPLs per region. Source: The author’s calculation is based on prior studies.

Figure 3.

Classification of Studies based on the used empirical method. Source: The author’s calculation is based on prior studies.

Figure 3.

Classification of Studies based on the used empirical method. Source: The author’s calculation is based on prior studies.

Table 1.

Publications count by ABS-rated journal.

| Journal Title | ABS-Rating | No. of Publications |

|---|---|---|

| The Journal of Finance | 4 | 2 |

| Review of Finance | 4 | 1 |

| Journal of Money, Credit, and Banking | 4 | 2 |

| American Economic Review | 4 | 4 |

| Economic Review | 3 | 1 |

| Journal of Financial Services Research | 3 | 3 |

| Journal of Banking And Finance | 3 | 9 |

| Journal of Financial Stability | 3 | 3 |

| Open Economies Review | 2 | 1 |

| Economic Modelling | 2 | 1 |

| Research in International Business and Finance | 2 | 3 |

| Finance Research Letters | 2 | 3 |

| Economic Systems | 2 | 2 |

| Review of Pacific Basin Financial Markets and Policies | 2 | 1 |

| International Journal of Central Banking | 2 | 1 |

| Emerging Markets Finance and Trade | 2 | 1 |

| Applied Financial Economics | 2 | 1 |

| Journal of African Business | 1 | 1 |

| Journal of Economics and Business | 1 | 3 |

Source: The author’s based on studies related to NPLs.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style