‘Safe Assets’ during COVID-19: A Portfolio Management Perspective

1

IPAG Lab, IPAG Business School, 184 Boulevard Saint-Germain, 75006 Paris, France

2

Economics Department, Université Paris 8 (LED), 2 Rue de la Liberté, 93526 Saint-Denis, France

Commodities 2023, 2(1), 13-51; https://doi.org/10.3390/commodities2010002

Submission received: 3 January 2023

/

Revised: 19 January 2023

/

Accepted: 21 January 2023

/

Published: 31 January 2023

Abstract

:The pandemic crisis of COVID-19 hit the financial markets like a shockwave on 16 March 2020. This paper attempts to capture which ‘safe assets’ asset managers could have fled during the first wave of the pandemic. From an investment manager’s perspective, candidate assets are stocks, bonds, exchange rates, commodities, gold, and (gold-backed) cryptocurrencies. Empirical tests of the ‘Safe-Haven’ hypothesis are conducted, upon which the selection of assets is performed. The methodological framework hinges on the Global Minimum Variance Portfolio with Monte Carlo simulations, and the routine is performed under Python. Other optimization techniques, such as risk parity and equal weighting, are added for robustness checks. The benchmark portfolio hits a yearly profitability of 7.2% during such a stressful event (with 3.6% downside risk). The profitability can be enhanced to 8.4% (even 14.4% during sub-periods) with a careful selection of ‘Safe assets’. Besides short- to long-term U.S. bonds, we document that investors’ exposure to Chinese, Argentinian, and Mexican stocks during COVID-19 could have been complemented with Swiss and Japanese currencies, grains, physical gold mine ETFs, or gold-backed tokens for defensive purposes.

1. Introduction

Stock markets worldwide have experienced a sudden turnaround due to the impact of COVID-19 on the global economy. On 29 June 2020, observe the Financial Times conversation, entitled ‘The safe-asset shortage after COVID-19’, here: https://www.ft.com/content/b98078c0-6acc-43e6-929b-13883c211288 accessed on 19 January 2023. The Dow Jones Industrial Average lost over 2997 points on March 16, 2020, marking the most significant drop since the crash of 1987; the CAC 40 was not spared and experienced a 9% drop of its index in 24 h. A far worse situation was observed for the S&P 500 (−32%). This was also felt in other equity and commodity markets, which led to global uncertainty. Investors, therefore, typically concentrate their investments toward safe-haven assets to protect their investment in such cases. To achieve this goal, gold, bonds, and some currencies constitute assets, towards which asset managers retreat in these troubled times because they are considered a store of value and, therefore, as value refuge in times of crisis or recession on the markets.

In a nutshell, this paper is essentially composed of two parts. In the first part, we run regressions à la [1], a fairly well-established definition of a safe haven in the literature. We also introduce the newest contribution by [2] with DCC correlations. In the second part, we run the workhorse asset management model, i.e., the minimum variance portfolio optimization, and conclude in terms of safe havens during the pandemic. We also consider well-known alternative strategies, such as risk-parity and equal weighting.

In macroeconomics, safe havens are usually studied utilizing rolling-window correlations. Gold, for instance, could be tracked against the variation of U.S. Treasuries and the S&P 500. Market analysts agree that gold tends to outperform in left-tail events (such as during VIX spikes). In time series econometrics, Ref. [1] have famously defined the concept of the safe haven, as follows:

- Hedge: An asset that is uncorrelated or negatively correlated with another asset or portfolio on average. A strict hedge is (strictly) negatively correlated with another asset or a portfolio on average.

- Diversifier: An asset that is positively (but not perfectly correlated) with another asset or portfolio on average.

- Safe haven: An asset that is uncorrelated or negatively correlated with another asset or portfolio in times of market stress or turmoil.

Usually, the following series can be considered as possessing the intrinsic characteristics of being a ‘Safe asset’:

- Gold,

- U.S. government bonds,

- German government bonds,

- The Swiss franc,

- The Japanese yen.

Since these financial assets have been studied exhaustively, in this paper, we investigate further the inclusion of commodities and (gold-backed) cryptocurrencies within the ‘Safe assets’ list. Indeed, besides the usual suspects exhibiting safe-haven properties, it is fascinating to add the following research questions: Can cryptocurrencies backed by gold be considered a safe haven during the COVID-19 pandemic? Do gold-backed cryptocurrencies and commodities improve the performance of the minimum variance portfolio? To do so, the paper employs daily return data and focuses on the COVID-19 Phase I period between 1 November 2019 and 31 October 2020. This investigation looks particularly interesting for private investors.

As the main original contribution compared to the extant literature, we develop a keen interest in gold-backed cryptocurrencies being considered candidates for Safe-Assets. Stablecoins having commodities as collateral, such as gold or other precious metals, point out that the issuer of the stablecoin concerned has an amount of gold equal to the asset’s market value. Here, the issuer has no obligation to provide several precious metals to the stablecoin holder in exchange, but rather, provides a token. In an ARMA-GARCH framework, Ref. [3] document that the PAX Gold token experiences increased volatility during the COVID-19 crisis. Based on tail dependence copula and quantile unit roots analyses, Ref. [4] conclude that gold-backed cryptocurrencies (namely, the Digix gold token (DGX), Perth Mint Gold Token (PMGT), Tether Gold (XAUT), PAX Gold (PAXG) and the Midas Touch Gold (TMTG)) did not exhibit safe-haven potential comparable to their underlying precious metal, gold.

This article distinguishes itself from the previous research works by focusing on the extra interest of portfolio managers for gold-based cryptocurrencies. This paper’s econometrics spans the main phase of COVID-19, i.e., from November 2019 to October 2020. Subsequent pandemic waves until March 2022 are analyzed for sensitivity purposes. To preview our results, the safe-haven regressions confirm the potential of gold and the short- to long-term U.S. Treasuries to be part of that list. In addition, our research reveals the interest in investing in gold-backed tokens, Bitcoin, and Ethereum (the two most mature cryptocurrency markets) during that particular period. Regarding the portfolio application, the gold-backed cryptocurrencies considered (e.g., Digix gold, PAXG, Perth Mint Token, Tether Gold) constitute a new means of diversification that makes it possible to reduce the risk of a portfolio during the COVID-19 crisis. The yearly risk-return trade-off amounts to 7.2% return (and 3.6% risk) for the benchmark portfolio. A more careful selection of ‘Safe assets’ during COVID-19 yields to an increased profitability of 8.4% (even 14.4% during sub-periods) against the same risk level. In addition to grains (e.g., Soybean), the addition of gold-backed cryptocurrencies such as the Perth Mint Gold Token could enhance the performance of a portfolio that was predominantly oriented towards Chinese, Argentinian and Mexican stocks during COVID-19. Near the end of our study period, the profitability drops to 4.56% yearly (guided by fixed-income earnings), whilst investors renew interest in defensive currencies (Swiss Franc; Yen) and commodities (grains; gold mine ETFs).

2. Literature Review

This paper seeks to test the findings of the recent literature on distinguishing which cryptocurrencies can be used as diversification tools in asset management. The paper seeks to explore, in particular, the usefulness of gold-backed cryptocurrencies during the COVID-19 pandemic.

2.1. On the Safe-Haven Regression Framework

Ref. [1]’s approach has been deepened in a recently researched paper [5]. In a significant contribution, Ref. [6] developed a full-fledged Hedging and safe-haven model, complemented with the safe-haven Index computation, for the top-five cryptocurrencies and gold as a Hedge and safe haven against the economic policy uncertainty (EPU) before and during the COVID-19 crisis. According to [6], all considered cryptocurrencies, as well as gold, cannot act as a hedge against EPU during the whole sample period and the recent COVID-19 health crisis. Moreover, the Tether, Ethereum, and gold exhibit weak safe-haven properties during the whole sample period under study; however, all assets lose this property during the onset of the COVID-19 pandemic.

2.2. First Contributions on Safe Havens during COVID-19

Ref. [7] is the first research paper scrutinizing safe-haven assets during the COVID-19 pandemic. Based on a sequential monitoring procedure to detect left-quantile changes, gold and Soybean futures are found to have a robust safe-haven role. However, the safe-haven property is found to be changing over time and is sensitive to the choice of markets. Another central contribution to this literature can be found in [2], who attempted to find the best safe haven for stock investors in the American market since the COVID-19 pandemic outbreak during March 2020–May 2022. Among the possible alternatives, Ref. [2] considers U.S. bonds, gold and silver, as well as stable DeFi and CeFi coins, Bitcoin and Ether. Ref. [2] documents that the safe-haven properties of the assets varied over time and that centralized stablecoins could have been used as a safe haven against American stocks during the pandemic.

Based on feasible quasi-GLS estimates, Ref. [8] support the use of gold as a defensive asset during the COVID-19 pandemic. According to [9], only gold is a weak safe haven against the S&P 500 in the long run with an ARDL model. Based on the Wavelet Quantile Correlation, Ref. [10] establish that gold consistently exhibits safe-haven properties for all the markets except NSE in the long and short run, while Bitcoin provided mixed results. Ref. [11] documents the better safe-haven properties of the Swiss Franc over gold, inciting asset allocation strategies, which give relatively more weight to the Swiss currency in global stock portfolios.

2.3. On the Classic Role of Gold as Safe Haven

For [12], gold acts as a hedge and safe-haven asset on average and in extreme market conditions for U.S., U.K. and German stock and bond returns. Ref. [7] conclude that gold remains a safe-haven asset during the COVID-19 pandemic. Ref. [13] assess that gold served as a safe-haven asset during the pandemic for stock markets from 31 December 2019 to 16 March 2020. However, gold lost its safe-haven role from 17 March to 24 April 2020. The optimal portfolio weights were recorded for gold, the S&P 500, the Euro Stoxx 50, the Nikkei 225 and the WT crude oil.

2.4. On the Role of Alternative Assets as Safe Haven, Such as Bitcoin

Contemporary research in the field of cryptocurrencies has gained considerable importance in the economic literature. Bitcoin, in particular, has been the subject of much questioning in this literature. The tumultuous evolution of its market value exemplifies a general trend in cryptocurrency: Bitcoin has the highest financial valuation. Its price has risen sharply in recent years, mainly due to the quantitative easing measures adopted by major central banks to address the consequences of the COVID-19 crisis. The unpredictable and consequent volatility of cryptocurrencies is attracting more and more short-term investors. Nevertheless, the fact that no central bank is issuing modern cryptocurrencies reduces their long-term attractiveness, making them uncompetitive with assets such as gold or silver as a safe haven.

The most recent empirical studies present cryptocurrencies as a financial diversification and hedging tool. In what follows, we review some of the determinants of cryptocurrency prices to shed light on their potential financial use and to explore asymmetries between financial and commodity markets.

Is Bitcoin the new ‘digital’ gold with diversifying properties for asset diversification? Ref. [14] argue against this view. Their portfolio analyses reveal that Bitcoin is no safe haven and offers no hedging capabilities for developed markets. This perspective is also shared by [15], who conclude that gold is a safe haven for oil and stock markets during the COVID-19 pandemic. However, unlike gold, Bitcoin’s response is the opposite, rejecting the safe haven property. Nevertheless, given its growing popularity with the opening of regulated Exchange-Traded funds in North America, we consider Bitcoin in our set of candidates as a ‘safe asset’ to turn to during the COVID-19. Based on DCC-GARCH correlation analyses, Ref. [16] assess that Bitcoin and Ethereum exhibit short-term safe-haven properties. Moreover, Ethereum is potentially a better safe haven than Bitcoin, given its crucial characteristic as a base of exchange for smart contracts.

Ref. [17] analyzes the impact of the COVID-19 crisis on the use of cryptocurrencies as a portfolio diversification tool. While the COVID-19 crisis shock does not appear to have increased correlations between cryptocurrency returns (Bitcoin and Ethereum are taken as examples), it does seem to have increased correlations between cryptocurrency returns on the one hand and the S&P 500 on the other. Overall, this variation suggests that cryptocurrencies do not have the characteristics of an effective portfolio diversification tool, at least not in the context of the COVID-19 crisis. This result is consistent with the findings of other studies [18,19,20,21,22].

Ref. [23] examine the correlations between 10 cryptocurrencies (Bitcoin, Ethereum, Tether, Ripple, Litecoin, Bitcoin Cash, Stellar, Monero, EOS and NEO.) and investment strategies over the period 2017–2022 using a GARCH model. From the pre-COVID-19 period to the COVID-19 period, the correlations between Bitcoin and other cryptocurrencies have particularly increased. Ref. [23] conclude that Tether can be used as a safe-haven cryptocurrency. This result is shared by [24], but it is refuted by [25], who argue that no secure haven cryptocurrency would exist. Based on the Wavelet coherence and connectedness methodology, Ref. [26] also believe that gold, oil and Bitcoin do not exhibit safe-haven characteristics.

Having reviewed the extant literature, we now produce our original analysis of the gold-backed cryptocurrencies’ performance as an investment class during COVID-19.

3. Data and Methods

3.1. Data Sample

The COVID-19 period under scrutiny ranges from 1 November 2019 to 31 October 2020. Daily data were extracted from Datastream and FRED. Descriptive statistics are given in Appendix A.

Regarding the selection of assets, as exchange rates and gold are essential safe-haven assets, we select them because they have specific characteristics distinct from other financial assets, such as their returns being much less volatile than those of cryptocurrencies and traditional stock markets.

Why should the results be different for gold-based tokens? Gold-backed cryptocurrencies represent an exciting mixture between gold (an ancient store of value) and cryptocurrency that potentially represent new-age money. While many investors like cryptocurrencies backed by gold for their more tangible characters, gold cryptocurrencies have counterparty risks and are more centralized than actual cryptocurrencies. The market value of the gold tokens is now around $950 million combined.

Since a cryptocurrency backed by gold is ultimately tracking the price of gold, exciting research questions arise: What is the degree of correlation between the returns of gold and gold-based tokens? Why would they be superior to gold in the context of portfolio diversification?

That is why we study the returns of four gold-backed cryptocurrencies, namely the Digix gold token, the Perth Mint Token, the Tether Gold and PAX Gold, during the pandemic period, in order to compare them to the value of gold, Bitcoin and Ethereum.

3.1.1. A Focus on Gold-Based Cryptocurrencies

What does a gold-backed cryptocurrency look like? Cryptocurrencies backed by gold take the form of fungible and divisible tokens in some cases. Funds of buyers of this type of cryptocurrency are transferred by users to an equivalent in gold and are converted into the corresponding amount of tokens. The tokens, therefore, represent a precise quantity of gold. The system depends on the fact that a custodian retains user funds and that an issuer of those tokens maintains a ‘clever contract’ such as ERC20 on the Ethereum blockchain. The ‘smart contract’ determines the allocation of cryptocurrencies and is recorded on a distributed register, such as a blockchain. This makes it possible to automate the exchanges or reduce intermediary costs.

Several criteria must be fulfilled to satisfy the definition of a gold-backed cryptocurrency. The first is being an ‘anchor’ to the price of certain assets, for example, that of the dollar or even gold. This represents the primary aspect of a gold-backed currency, consisting of taking an asset as a point of reference and holding this asset as collateral, either totally or in part. In the case of a gold-backed cryptocurrency, the collateral is not backed by any other cryptocurrency and is therefore not held on the blockchain but instead deposited outside the blockchain and therefore kept by a custodian, for example, in traditional institutions such as banks.

The second is the level of collateralization, i.e., the issuer of coins is held to hold reserves of an amount equal to or greater than the market capitalization of the gold-backed cryptocurrency. In other words, the value of the guarantees must cover the value of all tokens available in the market. It is more expensive and less divisible for the issuer than partial collateralization. Conversely, in the event of the partial collateralization, there is a risk that the issuer of stablecoins may only be able to redeem some gold-backed tokens should investors want to sell. This decreases the confidence of coin holders, which harms the stability of the gold-backed cryptocurrency.

Let us provide more detail about the functioning of some gold-backed cryptocurrencies. The PAXG or ‘PAX Gold’ token (PAXG is a variation over the original PAXOS (PAX) token that is pegged to the US dollar) is collateralized, of course, against gold, where a token is worth one OZ of gold (i.e., 28 g). Each PAXG token is backed by a fraction of a piece of a London Good Delivery gold bar, stored in Brink’s gold vaults, which is the approved storage company by the London Bullion Market Association. Launched in 2019, it was priced at USD 1547.88 on 16 March 2020 with a 24 h volume of USD 1.20 million. PAXG had accumulated a market capitalization of USD 61.96 million by September 2020. In April 2022, the PAX Gold Token price traded at USD 1959.38 with a daily volume of USD 28.8 million, resulting in a market capitalization of over USD 631 million. Today, it is traded on all major exchanges, such as Binance, Kraken, Kucoin, UniSwap, Gemini, etc. (A complete list can be found at https://coinmarketcap.com/currencies/pax-gold/markets/ accessed on 19 January 2023).

The DGX or ‘Digix Gold’ token is correlated to the price of one gram of gold. The company reportedly procures its gold from LBMA-approved refiners. For security, Digix includes third-party auditing from Bureau Veritas. Launched in 2018, it was priced at USD 49.53 on 16 March 2020 with a 24h volume of USD 116,256. The DGX market capitalization rose to USD 8 million in September 2020. DGX is mainly traded on Indodax (formerly known as bitcoin.co.id) registered with the Indonesian Commodity Futures Trading Regulatory Agency (BAPPEBTI). The live Digix gold token price today is USD 44.03.

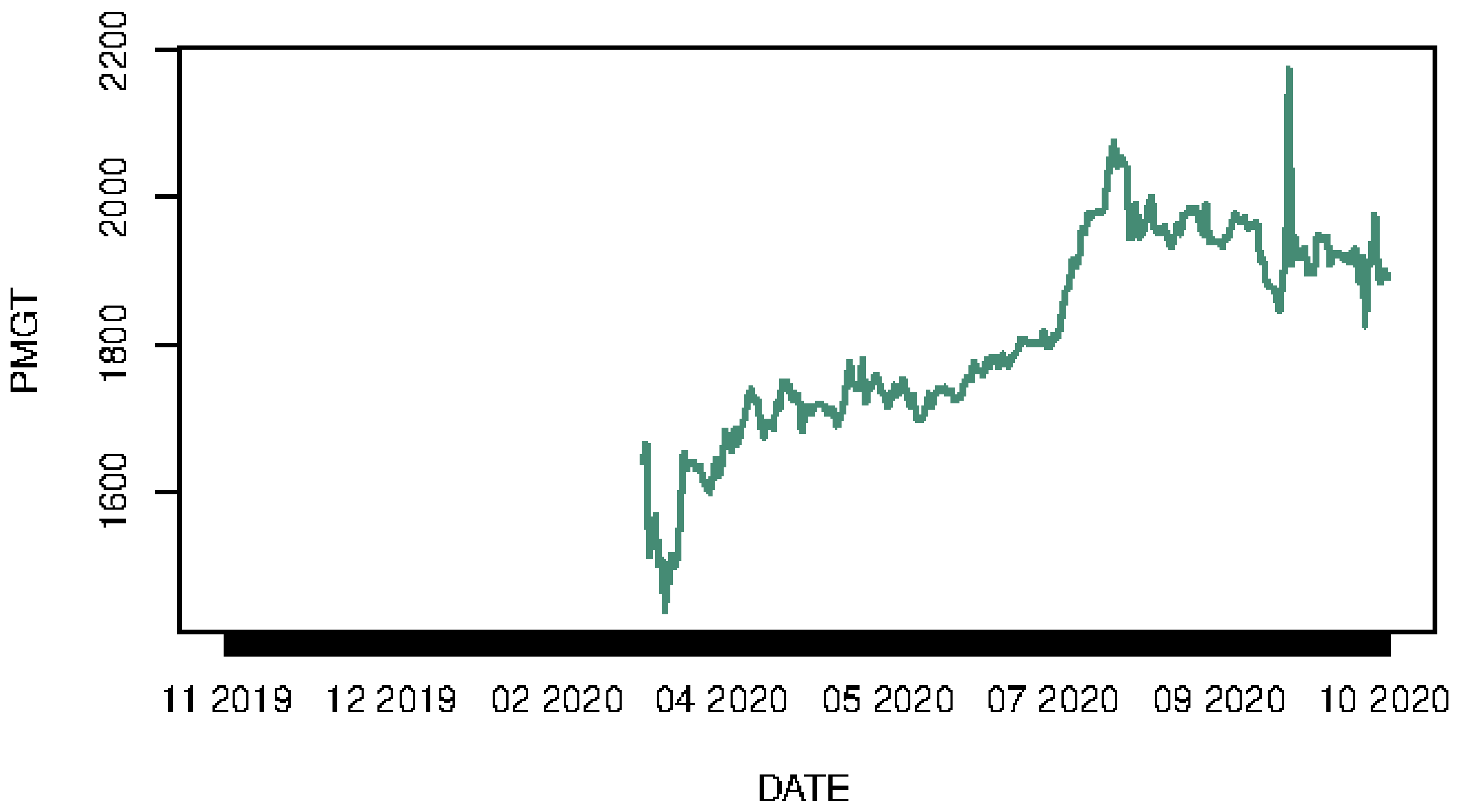

The Perth Mint Gold Token is issued by the Perth Mint company, which guarantees the conversion of tokens into physical gold. Each unit represents 1 fine troy ounce of physical gold. PMGT claims to be 100% backed by gold securely stored in The Perth Mint’s central bank grade vaults, where the Government of Western Australia guarantees the weight and purity of every ounce. This makes PMGT the first gold-backed token on a public blockchain, whereby the physical gold is government guaranteed. Created in 2018, PMGT may be bought and sold on the exchange Independent Reserve for AUD, USD and NZD. It was priced at USD 1498 on 17 March 2020. The live Perth Mint Gold Token price today is USD 1782.52. The market capitalization has slowly risen to USD 2.25 million. See the graph here: https://coinmarketcap.com/currencies/perth-mint-gold-token/ accessed on 19 January 2023.

Tether Gold is a stablecoin created by TG Commodities Limited; here, a XAUt token represents one troy fine ounce (or 31.10 g) of gold on a London Good Delivery gold bar. XAUt tokens are a proxy for physical gold, and can be redeemed for physical gold bars in Switzerland. According to the company website (accessible here: https://gold.tether.to/ accessed on 19 January 2023), 611 gold bars (equivalent to 7643.71 gold kilograms) are currently held in reserve. Tether Gold is presented as a safe portfolio diversification asset (to cite the company, Tether Gold: ‘Properly diversified investors combine Gold with stocks and bonds and crypto in a portfolio to reduce the overall volatility and risk’), a hedge against inflation, and as a store of value. It was priced at USD 1590.17 on 15 March 2020 with a 24 h volume of USD 4.32 million. In April 2022, Tether Gold was traded at USD 1953.88 with a daily volume of USD 4.85 million, resulting in a market capitalization of over USD 481 million. Today, it is traded on Bitfinex, Gate.io, OKX or UniSwap, among others.

For these gold stablecoins, the collateral is physical gold, and their market share is small compared to a 3.5 trillion dollar total market (with ETFs). Unlike fiat-backed stablecoins, gold-backed cryptocurrency shares do not show as steep a rise in volatility over the COVID-19 period from October 2019 to September 2020. This supports the idea that gold-backed cryptocurrencies can act as safe-haven investments during times of crisis. Unlike Bitcoin, which has experienced more visible increases in volatility during the transition period into the crisis of COVID-19, gold-backed currencies exhibit less volatility for the pre and post-COVID periods. Thus, cryptocurrencies backed by gold can also function as a safe haven, even in times of economic slowdown, just like gold. However, the volatility of these two cryptocurrencies is higher than those backed by the dollar (USDT and USDC).

Among other working hypotheses, we can highlight a fundamental difference in the value refuge of a cryptocurrency, in the sense that we can observe that those not backed by gold, such as Tether, have been playing the role of a safe haven for longer, while those backed by gold, such as the DGX, become safe havens, but only when events were leading to downtrends, such as COVID-19. This study, therefore, reinforces the idea that stablecoins, such as those backed by gold, can be a store of value; however, this result is nuanced depending on the period.

3.1.2. Series’ Plots

Below, we display the time-series used in the paper. The sharp downturn of COVID-19 is immediately visible in the S&P 500 price plunge (Figure 1).

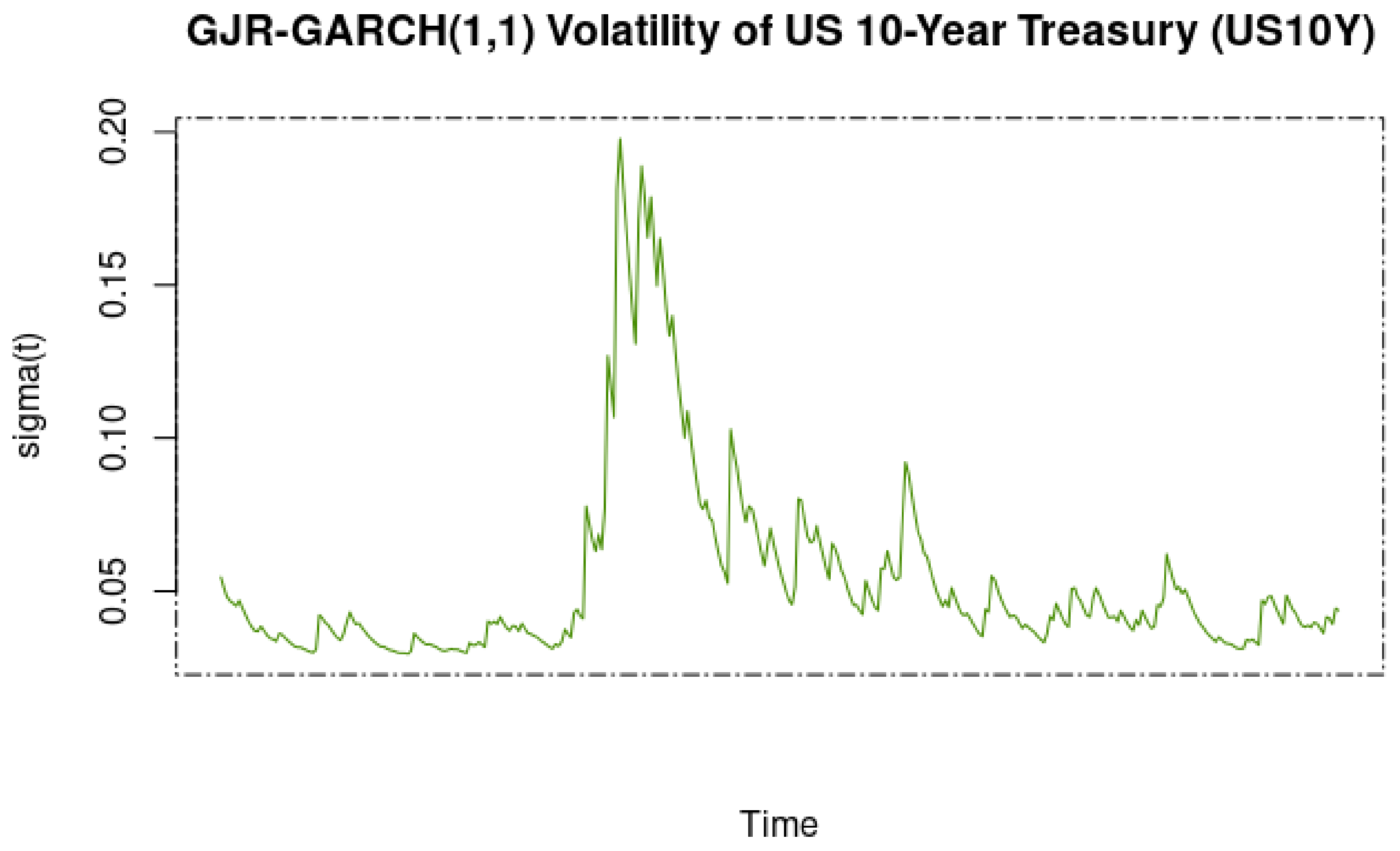

The pandemic shock was transmitted to the US bond markets as well, whose returns remained low in a quantitative-easing era from the Fed (Figure 2).

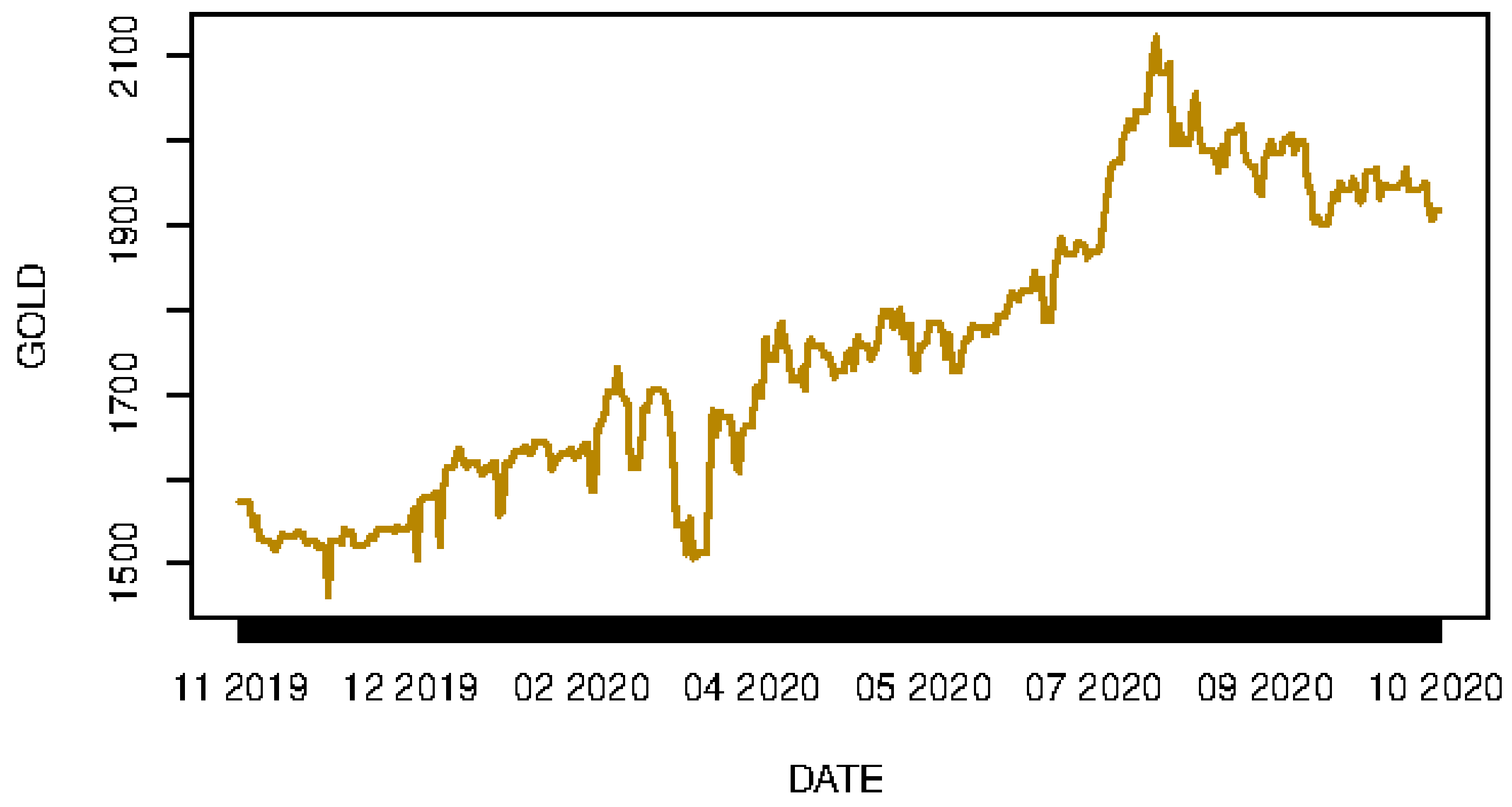

Is gold a refuge for value? The raw series plot seems to indicate that this is indeed the case (Figure 3).

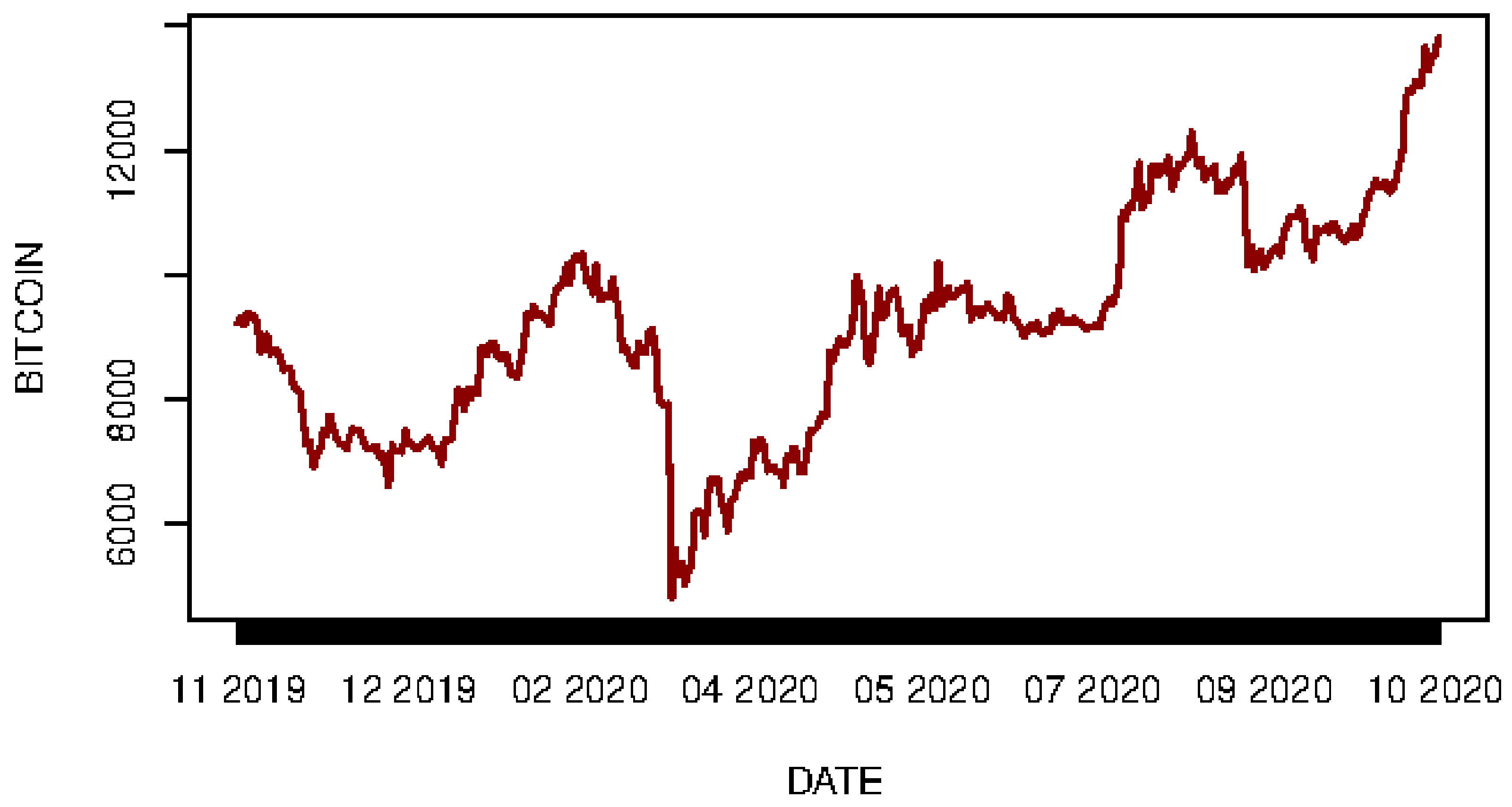

The previous literature features mixed results on the enigmatic role of Bitcoin during stock market crashes. In Figure 4, the Bitcoin price seems to mimic the S&P (thereby invalidating the refuge for value hypothesis).

Ethereum is often proposed as an alternative investment vehicle, whose capabilities of creating an eco-system of smart contracts seem limitless. Since the financial underlying product is still at an early stage, it can also be proposed to risk-lover investors. It follows the same pattern as Bitcoin, as can be seen in Figure 5.

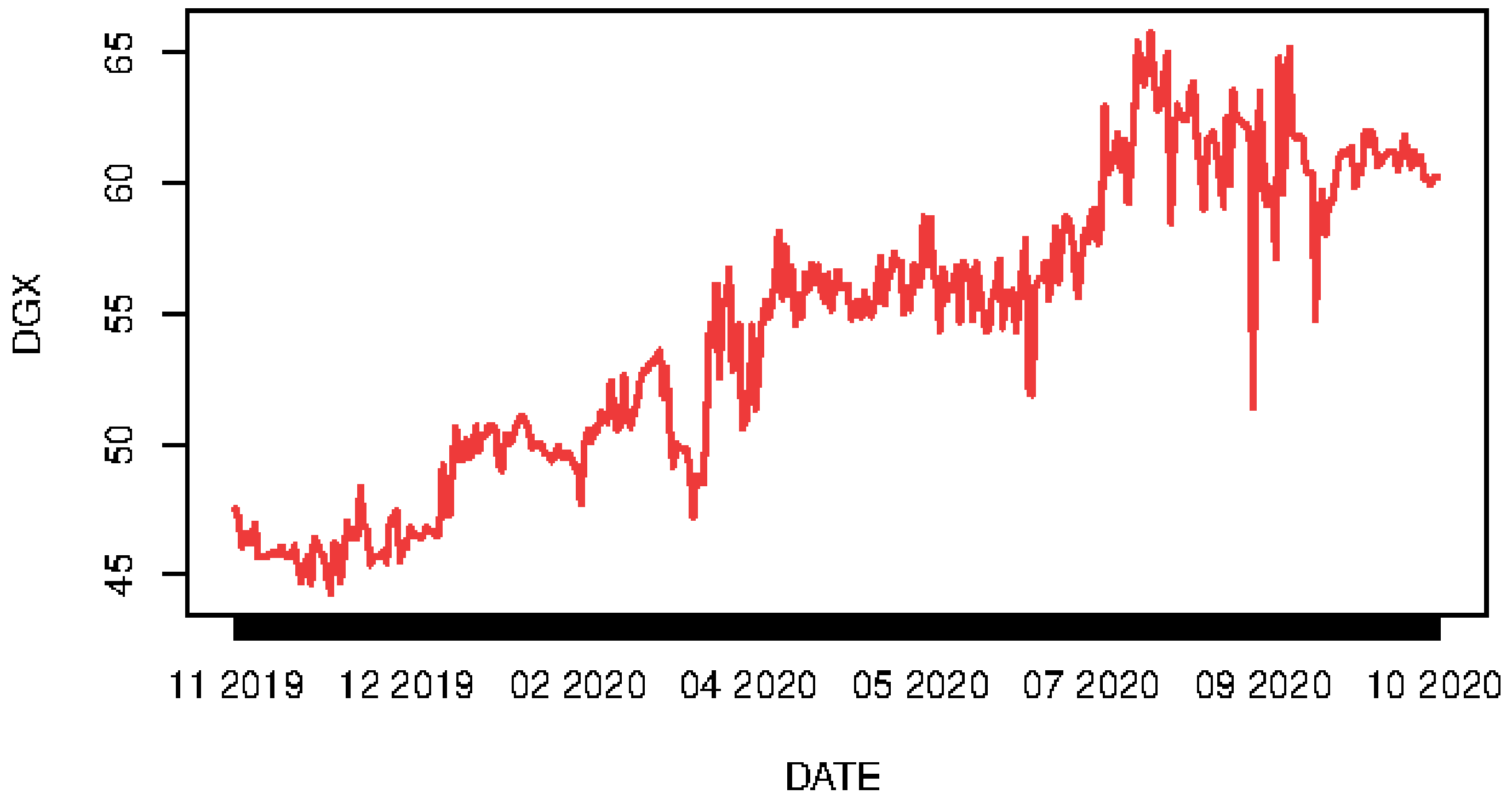

Regarding gold-backed tokens, we will include them in our candidate list of safe assets during COVID-19. Hence, the first one displayed is Digix in Figure 6. Interestingly, its ever-increasing price pattern stands in sharp contrast to that of stock markets, hence warranting its potential as a refuge for value.

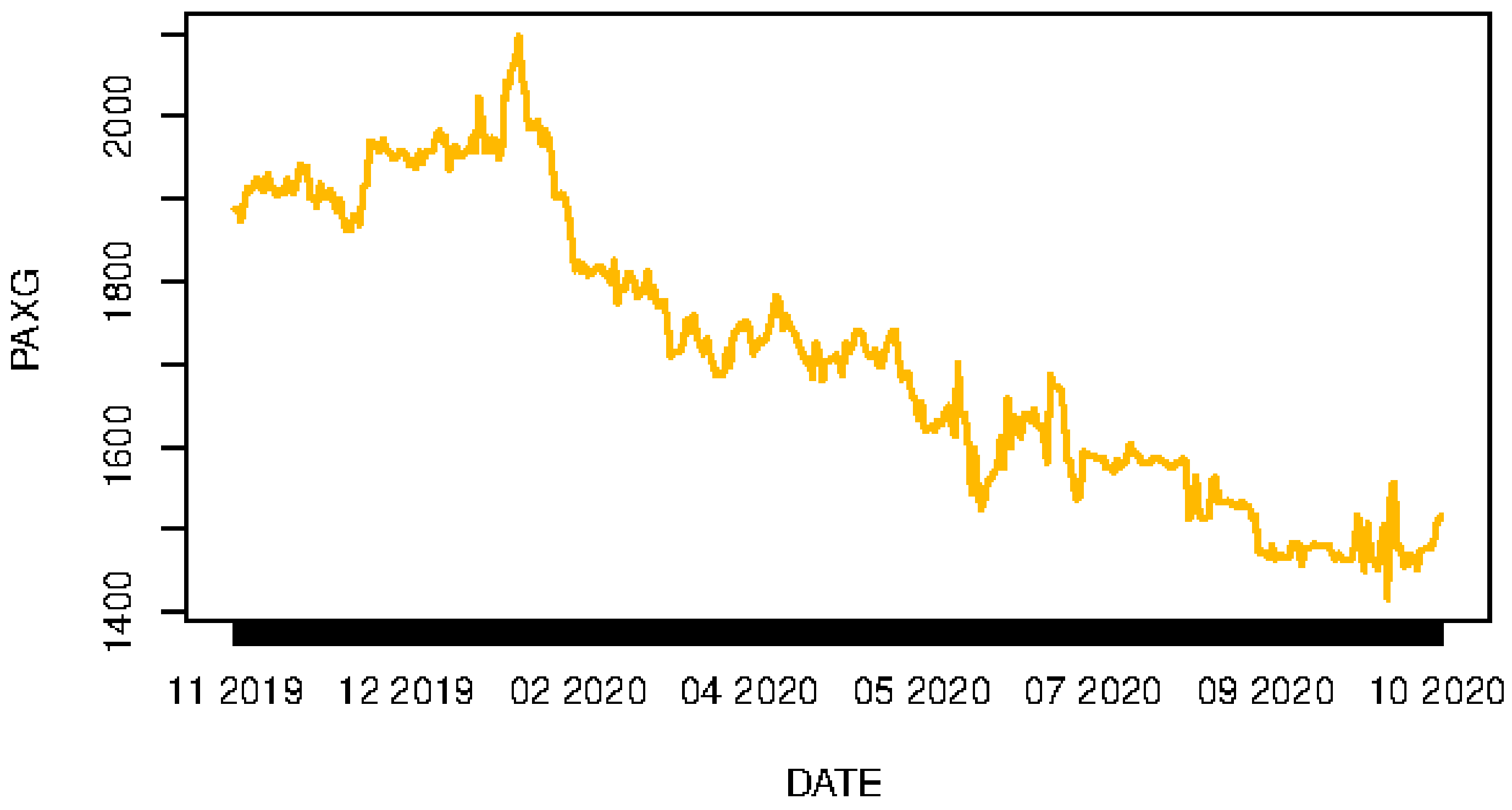

Next is the PAX Gold token in Figure 7. It is decreasing all the time. Therefore, one might wonder whether this is a savvy investment opportunity.

3.2. Models

To assess whether the studied cryptocurrencies are simply ways to diversify a portfolio or really safe havens, we follow the model of [1], where an asset with a positive correlation would not be a safe haven, against the alternative that having a zero or negative correlation during the COVID-19 period would translate as being a safe haven.

To counter the volatile nature of cryptocurrencies, gold-backed cryptocurrencies appear opposite to traditional cryptocurrencies. They are designed to be a cryptocurrency whose price is stable thanks to their gold mechanism trustees. They stand on the following postulate: gold-backed cryptocurrencies are suitable means of diversification and safe havens when not linked to cryptocurrencies’ traditional markets, and this under normal or extreme market conditions.

3.2.1. Volatility

Underlying the models are GJR-GARCH dynamics [27]:

with for , and zero otherwise. captures the effect of good news, while bad news manifest their impact by . Moreover, if the coefficients and , the impact of the news is asymmetric, and leverage exists, respectively. The meaning of the leverage is that the bad news exacerbates volatility. In order to satisfy the non-negativity condition, the coefficients should be .

Presently, these models are routinely estimated in R using the BHHH algorithm; hence, we do not need to reproduce the results’ tables: the ARCH and GARCH coefficients have been checked to be statistically significant and positive, whilst the sum of the coefficients is strictly inferior to one.

Instead, we prefer to provide insights on the volatility graphs produced below.

In Figure 10, the S&P500 conditional volatility exhibits the effects of the COVID-19 crisis, with a pronounced volatility spike during the lock-down period.

The same comment applies for the US 10-year bond market in Figure 11.

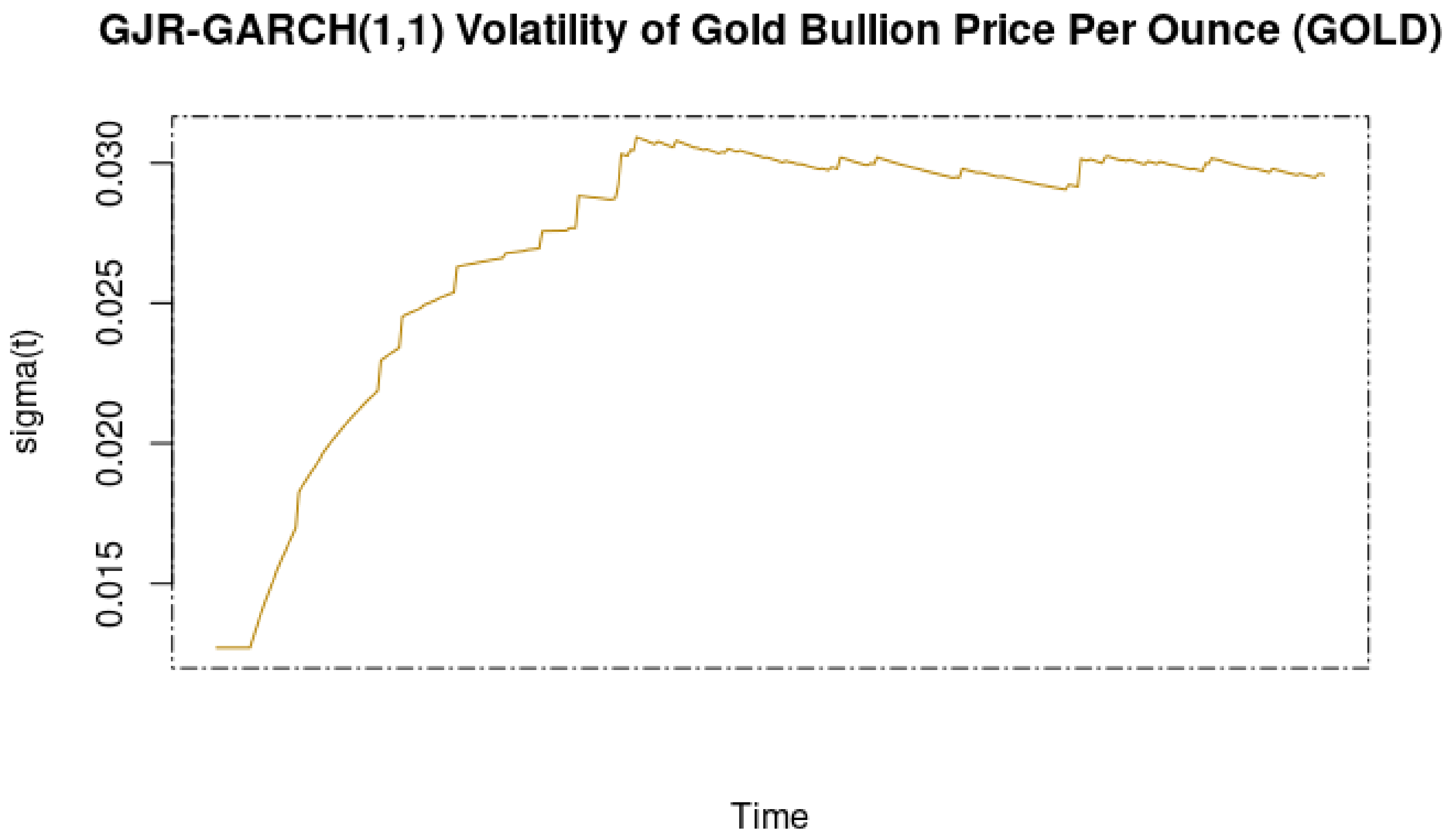

On the Y-axis of Figure 12, the reader can verify that the shock transmitted to the gold market is very small. Hence, the picture obtained is of a staggering shock.

In Figure 13, the Bitcoin market registers a volatility shock of a higher amplitude than the stock market.

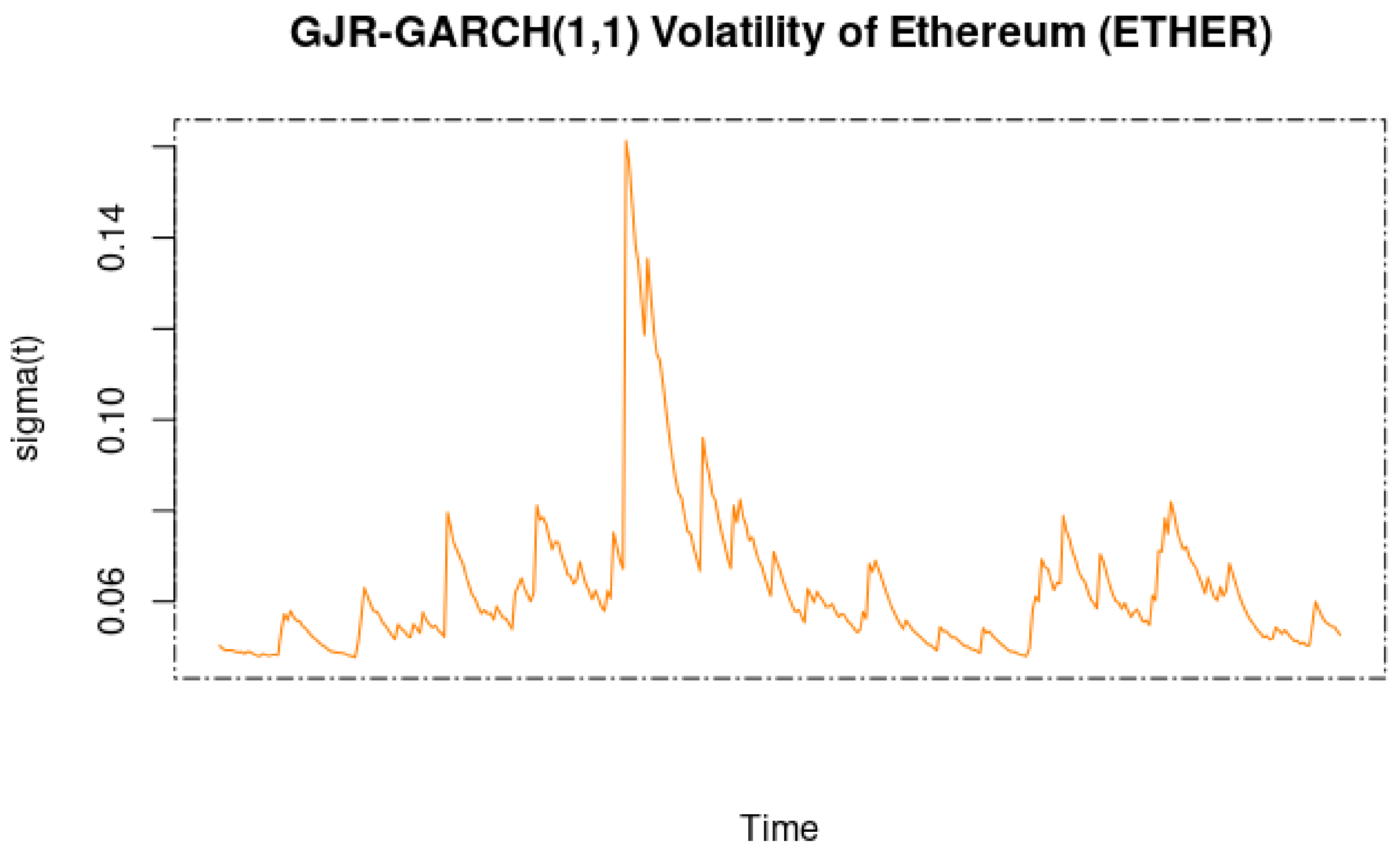

In Figure 14, Ethereum has also witnessed a contemporaneous agitated market turmoil.

For the gold-backed Digix token in Figure 15, the interpretation is different. Indeed, we do not record a volatility spike at the time of the COVID-19 period. (The volatility spike recorded near the end of the study period might be due to the low liquidity.).

In Figure 16, the PAX Gold token features the same interesting characteristics as DGX.

As is visible from the small scale of the Y-axis in Figure 17, the COVID-19 shock has also been little transmitted to the Perth Mint Gold Token.

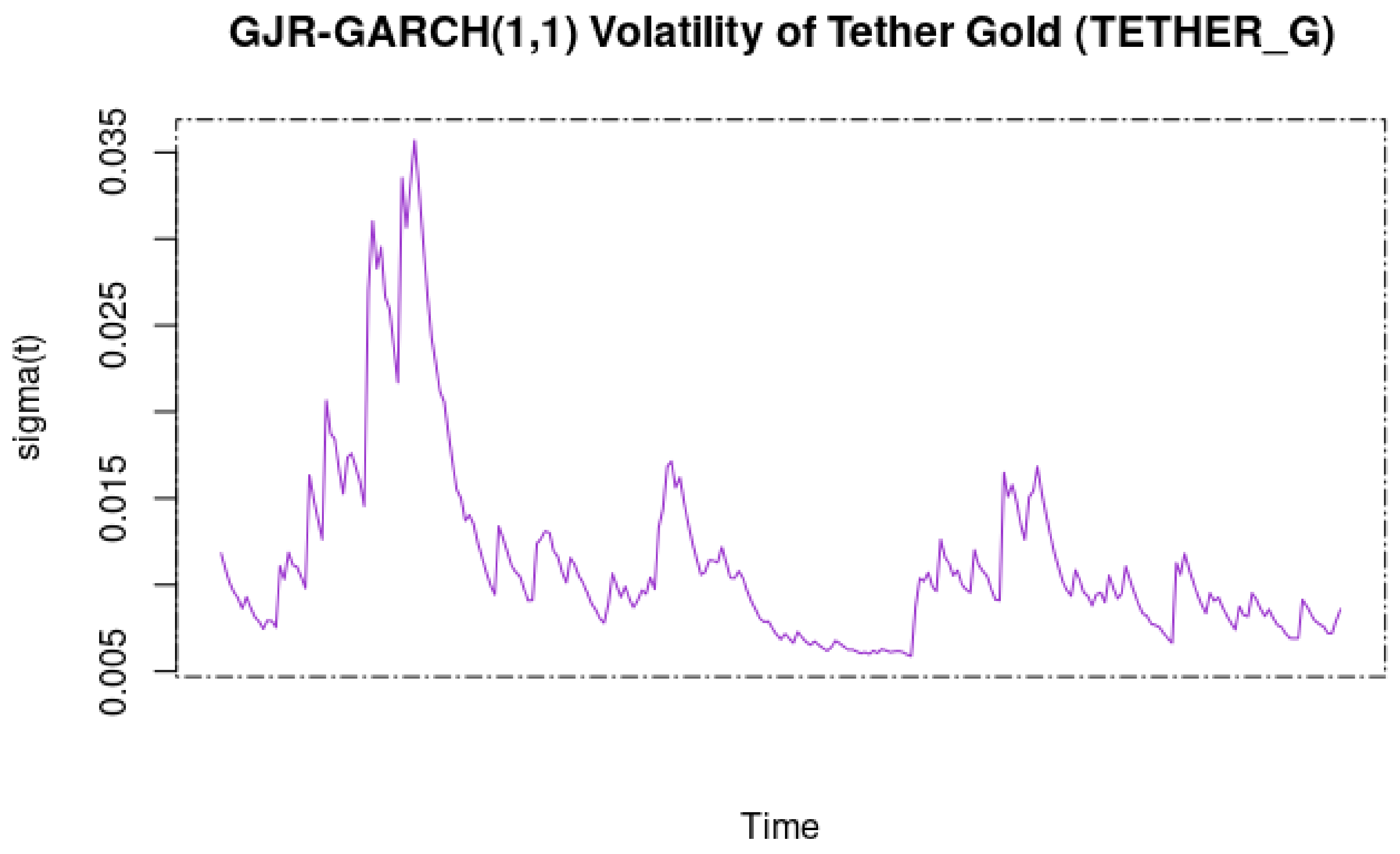

Regarding the last token in Figure 18, the shock transmission to Tether Gold appears minimal, although one could argue that it is contemporaneous to that of the stock market.

This preview of the volatility dynamics informs us that the stock and bond markets have suffered from a large negative shock during the COVID-19 period, which is the premise of this paper. We have visualized that both the gold asset and gold-backed cryptocurrencies exhibit interesting asynchronous characteristics with regard to the stock and bond market fluctuations.

3.2.2. Safe-Haven Regressions

- Hedge: A strong (weak) hedge is defined as an asset that is negatively correlated (uncorrelated) with another asset or portfolio, on average.

- Safe haven: A strong (weak) safe haven is defined as an asset that is negatively correlated (uncorrelated) with another asset or portfolio in certain periods only, e.g., in times of falling stock markets.

In a nested form, the model writes:

with being the log-returns of the candidate for the safe haven (SH), being the coefficient for regressing the SH against the stock market index (S&P 500) and being the error term. is a dummy variable capturing the extreme stock market declines. It is equal to one if the stock market exceeds a threshold given by the 5% quantile of the stock market return distribution. (The reader can verify in the Appendix the correspondence with the ‘classic’ version of [1]’s safe-haven regressions.)

Presently, following [2], it is possible to extend this classic framework to regressions with Dynamic Conditional Correlations (DCC):

It is essentially the same framework, except that the LHS equation has been replaced with the DCC(1,1) conditional correlations between the candidate safe haven and the stock market. The reader can find this in Appendix A as well as in the formal writing of the DCC model). Note that we resort to DCC in its corrected form of [28].

- Hedge: An instrument can be considered a hedge if it is, on average, negatively correlated with the S&P ().

- Safe haven: It can be treated as a safe haven if its correlation diminishes or becomes negative in the moments of extreme declines in the base asset ().

- Diversifier: It can be called a diversifier if its correlation with the base asset is, on average, positive ().

4. Safe-Haven Results

From the review of the previous literature in the introduction, we can hypothesize that gold is generally considered a safe haven in the short and long term. By contrast, Bitcoin seems to exhibit no safe-haven characteristics against the S&P 500, or is only effective as a short-term safe haven, whose role is more about long-term diversification. Thus, we can assume that gold is more efficient than Bitcoin in times of crisis, such as COVID-19. Therefore, it is not without interest to favor cryptocurrencies backed by gold over those not backed by this asset, which is considered a refuge for value.

In Figure 19, we provide the plots of the stationary log-returns on which the [1]’s regressions are run. All the calculations have been performed using the R package rmgarch [29].

4.1. Equation (3) Estimates

According to [1]’s methodological framework, the decision rules are as follows:

- Hedge: The instrument can be considered a hedge if the intercept is negative.

- Safe haven: The instrument can be considered a strong safe haven when is significantly lower than 0.

Recalling that:

- In the ‘Hedge’ column, negative coefficients indicate that the asset is a hedge against stocks.

- In the ‘Safe Haven’ column, zero (negative) coefficients during extreme market conditions (5% quantile) indicate that the asset is a weak (strong) safe haven.

Table 1 uncovers the following insights:

- We detect no ‘Hedge’ during the COVID-19 period.

- We detect potentially five ‘Safe Havens’:

- US 10-Year Bond,

- Gold,

- Perth Mint Gold Token (PMGT),

- PAX Gold (PAXG),

- Tether Gold.

Only Tether Gold exhibits statistical significance (at 10%).

Regarding the potential role of a safe haven for three gold-backed cryptocurrencies, during this period of uncertainty, investors are looking for an asset class in which to invest with low risk, low volatility, and a positive return, which is typically found in gold-backed cryptocurrencies. The variation in profitability and volatility during the COVID-19 period transforms this asset class into a potential refuge for value against risk in times of crisis. Thus, adding PMGT, PAXG, and Tether Gold to a portfolio composed of stocks, bonds, exchange rates, and commodities could be a promising strategy during the epidemic crisis.

Regarding Pax Gold, it was approved at that time by the New York State Department of Financial Services for its reserves and listing. (We can also notice that in the middle of the crisis, the asset demonstrated an increase in returns of around 134% from March 2020 until August, while the price of gold only increased by 35% during the year 2020.) The attraction for such gold-backed cryptocurrencies since the start of the COVID-19 pandemic is driven by the increase in access to cryptocurrencies in general but also by the fact that a token allows access to gold at a lower cost and without storage.

Regarding Tether Gold, one of the explanations is that during periods of crisis or economic downturn, investors prefer to convert their traditional cryptocurrencies against stablecoins, thus inducing an appreciation of the latter. In addition, investors can convert their cryptocurrencies into assets representing a safe haven, such as, for example, bonds and gold, in order to reduce portfolio risks. This economic logic also leads to the increase in the price of the dollar and of gold, which in turn leads to increased prices of stablecoins backed by gold or the dollar.

4.2. Equation (4) Estimates

After visualizing the cDCC(1,1) correlations of each candidate asset with the S&P500 in Figure 20 and inspecting the safe-haven regressions in Table 2, we understand the usefulness of pursuing our investigation besides the classic [1]’s framework. Indeed, in a dynamic correlations setting, the approach by [2] allows us to uncover these additional characteristics:

- We detect potentially one ‘Hedge’ during the COVID-19 period, i.e., Tether Gold (although not statistically significant). Other assets could be called ‘Diversifiers’ (although not significant either).

- We confirm the possibility to have five ‘Safe Havens’ (although not exactly the same as in Equation (3)):

- Gold,

- Perth Mint Gold Token (PMGT),

- Bitcoin,

- Ethereum,

- Digix gold (DGX).

- What is striking is the high significance (between 1% and 5%) recorded for each candidate as a safe haven in this context.

In contrast, the safe-haven property of the US 10-year bond and PAXG are not visible in the DCC correlation regressions framework anymore. Tether Gold still exhibits a statistical significance, but records the wrong sign (also known as positive).

To summarize our findings in this section, the [1]’s regressions have revealed no hedge assets during the COVID-19 period, and potentially five safe havens (US 10-year bond, Gold, PMGT, PAX Gold and Tether Gold). The [2]’s Dynamic Conditional Correlations have highlighted one hedge (Tether Gold), and potentially five safe havens (Gold, PMGT, Bitcoin, Ethereum and Digix gold). In the next section, we will bring these insights about additional safe-haven candidates in the realm of gold-backed cryptocurrencies into a portfolio management exercise.

5. Portfolio Optimization

For the sake of further empirical application, we constitute a global portfolio composed of stocks, bonds and bilateral foreign exchange rates (an alternative could be to gather the Trade-weighted US dollar index with various expositions to emerging market economies, goods and services), commodity prices and (gold-backed) cryptocurrencies. The list (other candidate assets could have been included, such as the Euro Stoxx 50 or the China FTSE A50. Moreover, AAA-grade corporate bonds could also be included in the list of potential safe-haven assets) of 56 assets is given in Table 3.

5.1. Global Minimum Variance Portfolio with Monte Carlo Simulations

This Python routine is based on many theoretical contributions in portfolio theory (to name a few: [30,31,32,33]).

Given an estimated covariance matrix S, the global portfolio variance minimization problem when portfolio weights are constrained to satisfy both a lower bound of zero and an upper bound of is given by:

The Kuhn-Tucker conditions (necessary and sufficient) are:

Here:

Ref. [32] derive the solution to the constrained portfolio variance minimization problem in Equations (5)–(8) as . Given the quantitative easing era (historically, the US 10-year government bond interest rate stood at 1.81% in November 2019 and 0.78% in October 2020), the risk-free rate is set to 0.021. The number of trading days per year is set to 252. The number of MC simulations of portfolios is set to 1000. Notice that any portfolio manager can reduce, at a bare minimum, the transaction costs of rebalancing the portfolio, thanks to a high degree of fidelity to his/her prime broker.

5.1.1. Benchmark Portfolio Results

In the following graphs:

- × symbols are the dominated assets;

- ⋆ symbols are the tangent risk-free assets (short- to long-term U.S. bonds);

- ○ symbols are the optimal investments on the portfolio frontier.

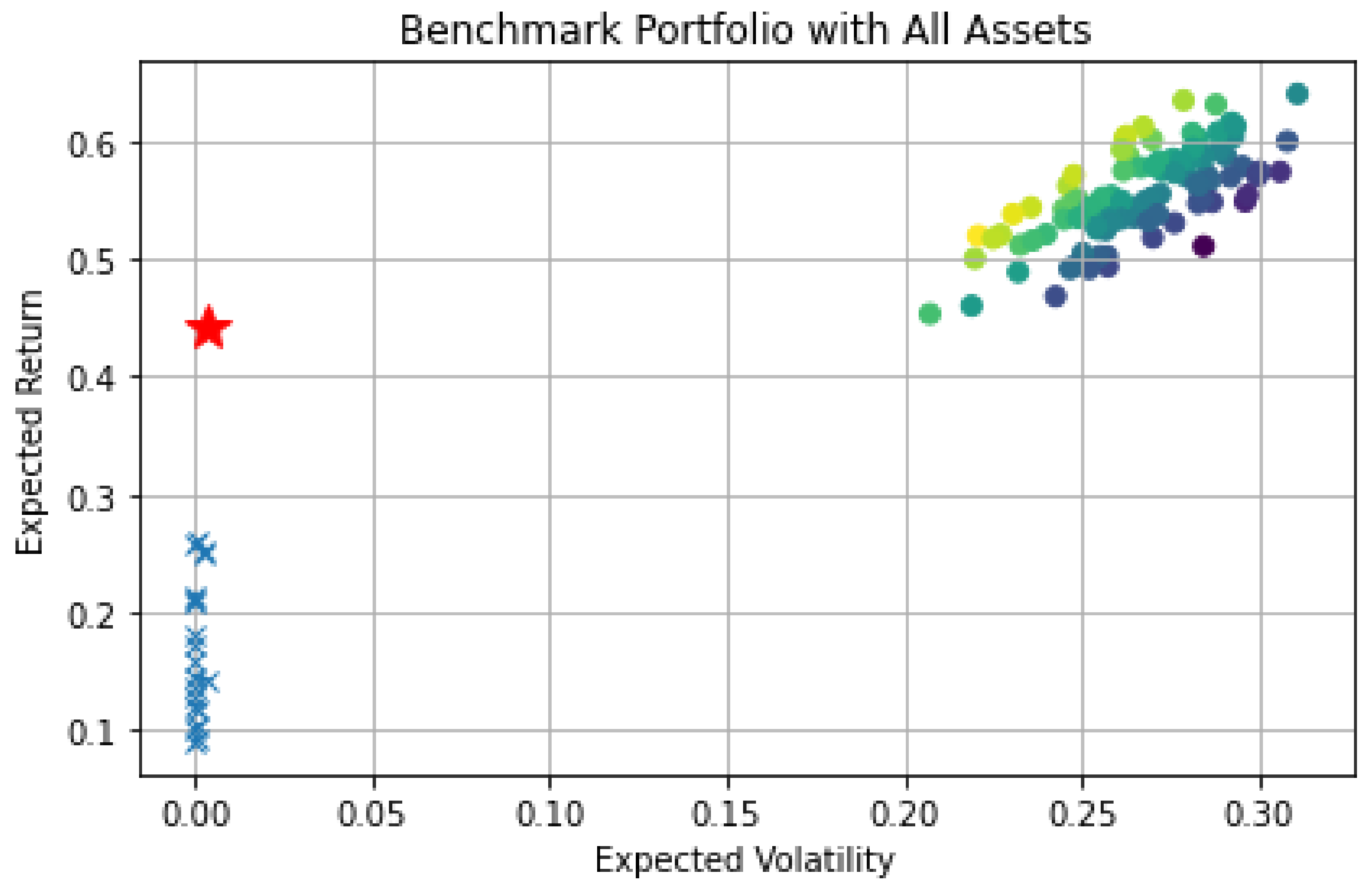

As can be observed from Figure 21 in the benchmark setting, with minimum variance optimization, we achieved during the COVID-19 period a monthly mean return of 0.6% and a monthly standard deviation of 0.3%. To illustrate the meaning of this result, consider a notional amount of USD 10,000,000 invested. On 14 February 2020, the S&P dropped from 3380 points to 2304 on 20 March 2020. Therefore, such a 32% backdrop on the S&P constitutes a potential loss of USD 3,200,000 if the investor monetizes the loss by exiting his/her position. In contrast, the benchmark portfolio is a buy-and-hold strategy, which delivered a yearly gain of 7.2% (12 × 0.6%) = USD 720,000 during the COVID-19 period (and a corresponding potential loss of 3.6% (12 × 0.3%) = USD 360,000). The results are based on historical returns. The expected return is the annualized monthly arithmetic mean return. Hence, the risks of capital loss are much smaller in the benchmark portfolio. The earning performance during COVID-19 shall also be judged against the quantitative easing background, with low profitability coming from zero to negative bond rates.

Regarding benchmark portfolio weights, the assets with the highest weights are the following:

- SSE Composite Index and ALL ORDINARIES;

- IPC MEXICO and MERVAL;

- S&P-GSCI Commodity Index Future and Bitcoin Futures;

- Bitcoin Cash and Litecoin USD;

- XRP USD and DOGE USD;

- Digix gold token USD and Tether Gold USD.

It is, therefore, a mix of stock markets (China, Australia, Mexico and Argentina) and a basket of commodities and cryptocurrencies. We notice the presence of two variants of Bitcoin (the futures and cash) and the ‘silver’ crypto, Litecoin. One crypto is for swift banking transactions (Ripple), whereas another is purely an internet meme (Dogecoin). Last but not least, we identify the presence of two gold-backed cryptos: Digix and Tether Gold. Regarding the Digix gold token, the statistical analysis informs us that this token is almost negatively correlated to the S&P 500, thereby demonstrating some leeway for this gold-backed cryptocurrency to be a better hedge against risk on the stock market.

Benchmark portfolio Sharpe ratios are reproduced in Figure 22. Three groups record the highest Sharpe ratios:

- Soybean Futures;

- IPC MEXICO;

- Shenzhen Component.

Hence, a well-advised portfolio manager would have invested into grains and the emerging economies’ stocks from China and Mexico in order to save his/her performance during the COVID-19 turmoil.

5.1.2. Alternative Portfolio Results

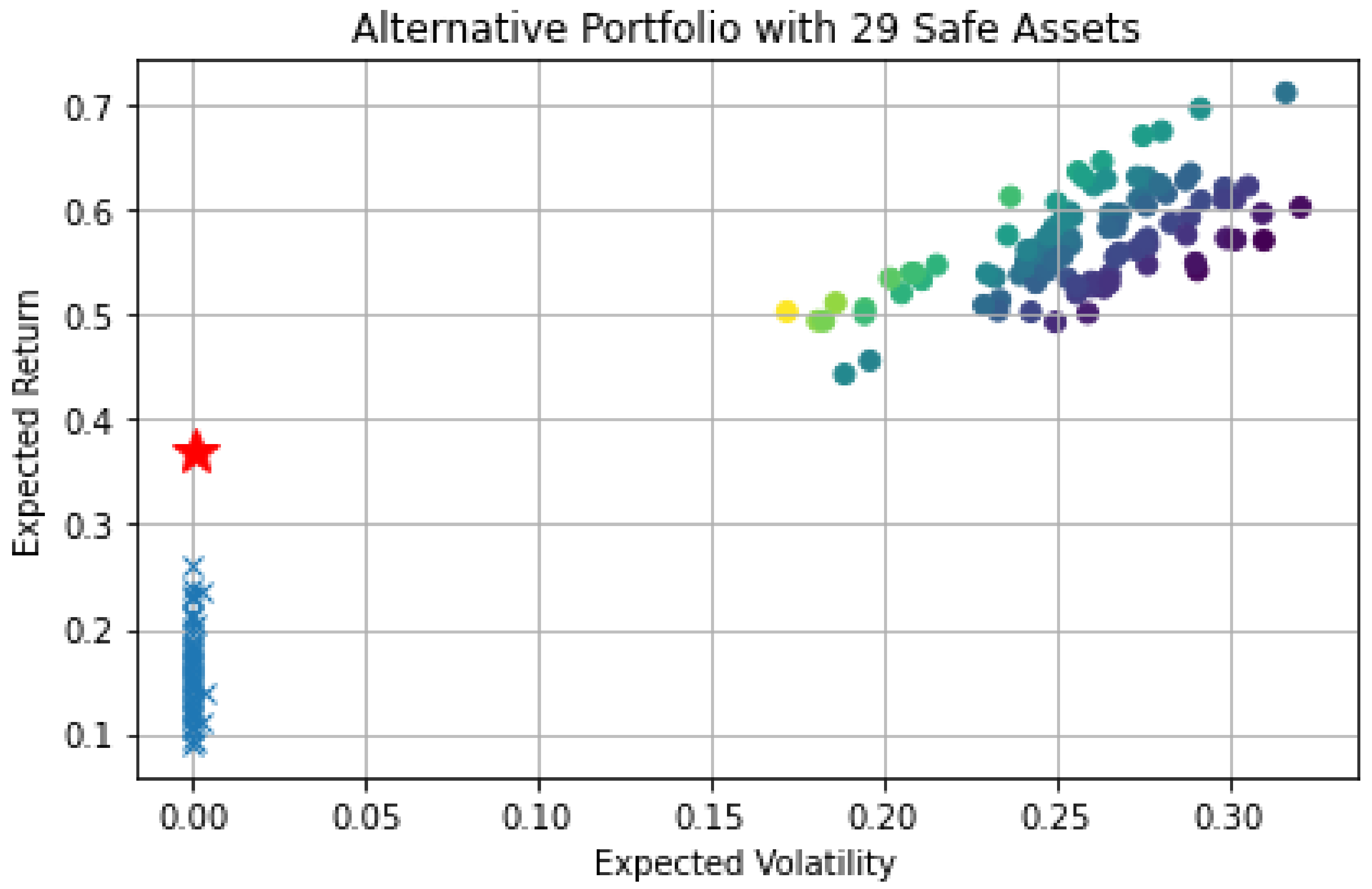

Given the results from the safe-haven regressions in Section 3, we now proceed to a more careful selection of the ‘Safe assets’ during COVID-19. In particular, this selection yields to a sub-set of 29 ‘Safe’ assets, listed in Table 4 as the Alternative Portfolio.

As can be observed from Figure 23, this careful selection yields to a slightly enhanced return profile (12 × 0.7% monthly = 8.4% yearly) for the same risk levels.

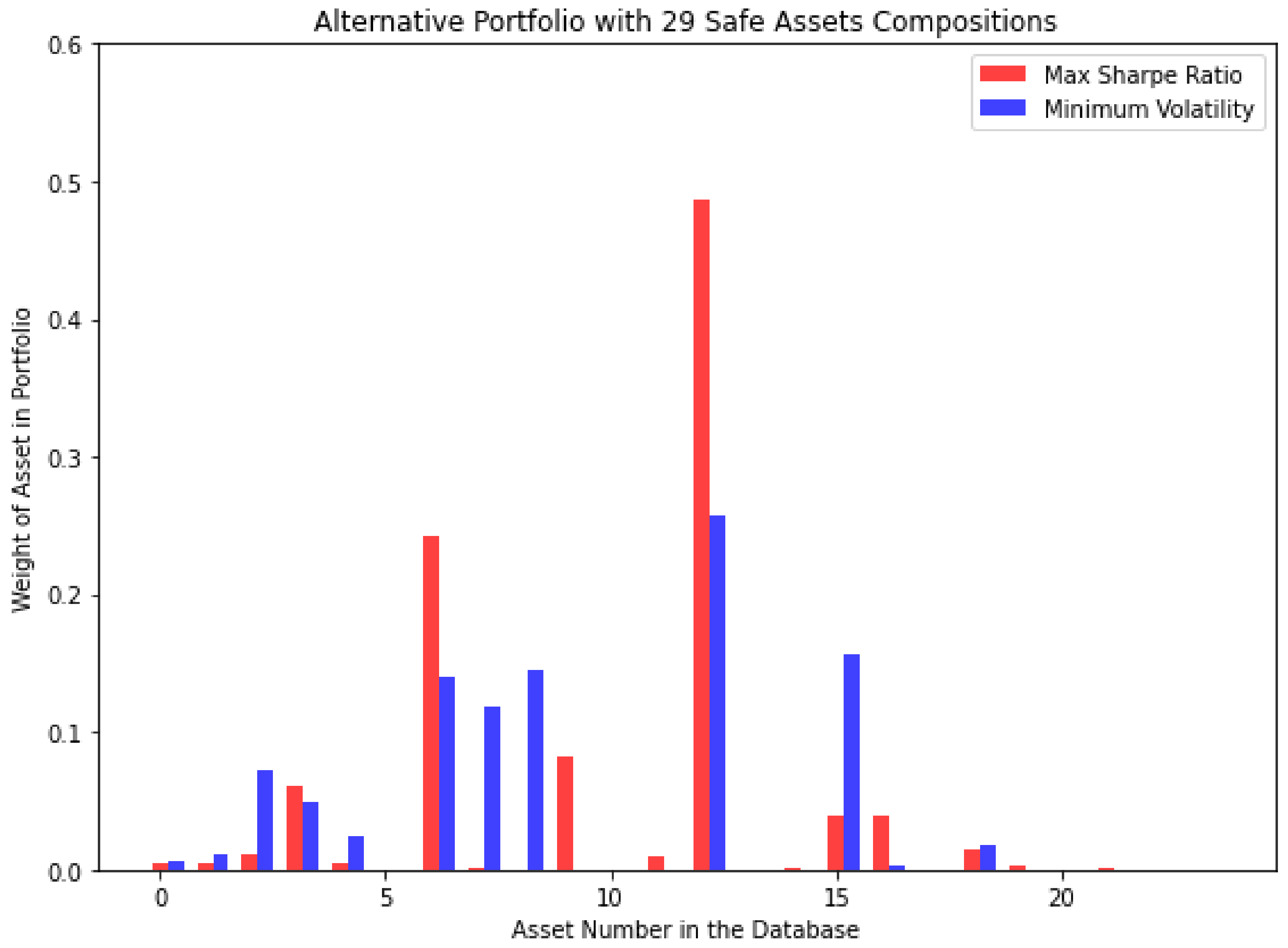

Regarding alternative portfolio weights reproduced in Figure 24, we notice the following changes among the highest weights:

- Soybean Futures CBOT;

- XRP-USD;

- Perth Mint Gold Token USD.

Whilst the position in grains remains intact, the alternative portfolio confirms the need to hold in priority two kinds of cryptocurrencies. Ripple (XRP) is a closed (not open-source) blockchain funded by a consortium of private companies in order to potentially replace the SWIFT (SEPA) routing numbers for international (European) banking transactions. Its advantage lies in its small fee for immediate money transfer, compared to 5 to 7 days for international bank transfers and high fees from multiple brokering partners. The Perth Mint is a gold-backed token (equal to 31.10 g of pure gold) that was identified as a potential safe haven in the regressions. Although it was lacking statistical significance, it exhibited the corrected negative sign. In a portfolio optimization setting, this is a new finding originating from our research effort. It also corroborates the previous work by [4].

Regarding Sharpe ratios, Figure 24 also recalls the importance of holding:

- IPC MEXICO;

- Bitcoin Cash USD.

Compared to the benchmark portfolio, we highlight the importance of the continuous ownership of Mexican stocks for diversification during COVID-19. In addition to Ripple, the portfolio manager could also leave Bitcoin Cash in his/her safe selection of holdings. This particular version of the Bitcoin blockchain is dedicated to the speed of executing transactions as if it were instant cashless payments in a supermarket or other store using one’s smartphone. Bitcoin Cash is mainly used in South America (alongside Dash) in countries where the State’s money is either unreliable or subject to frequent devaluation/inflation spikes.

5.2. Robustness Checks

The announced performance (between 7.2% and 8.4%) could be applicable only during phase I when the COVID-19 pandemic broke the news, and caused lockdowns worldwide.

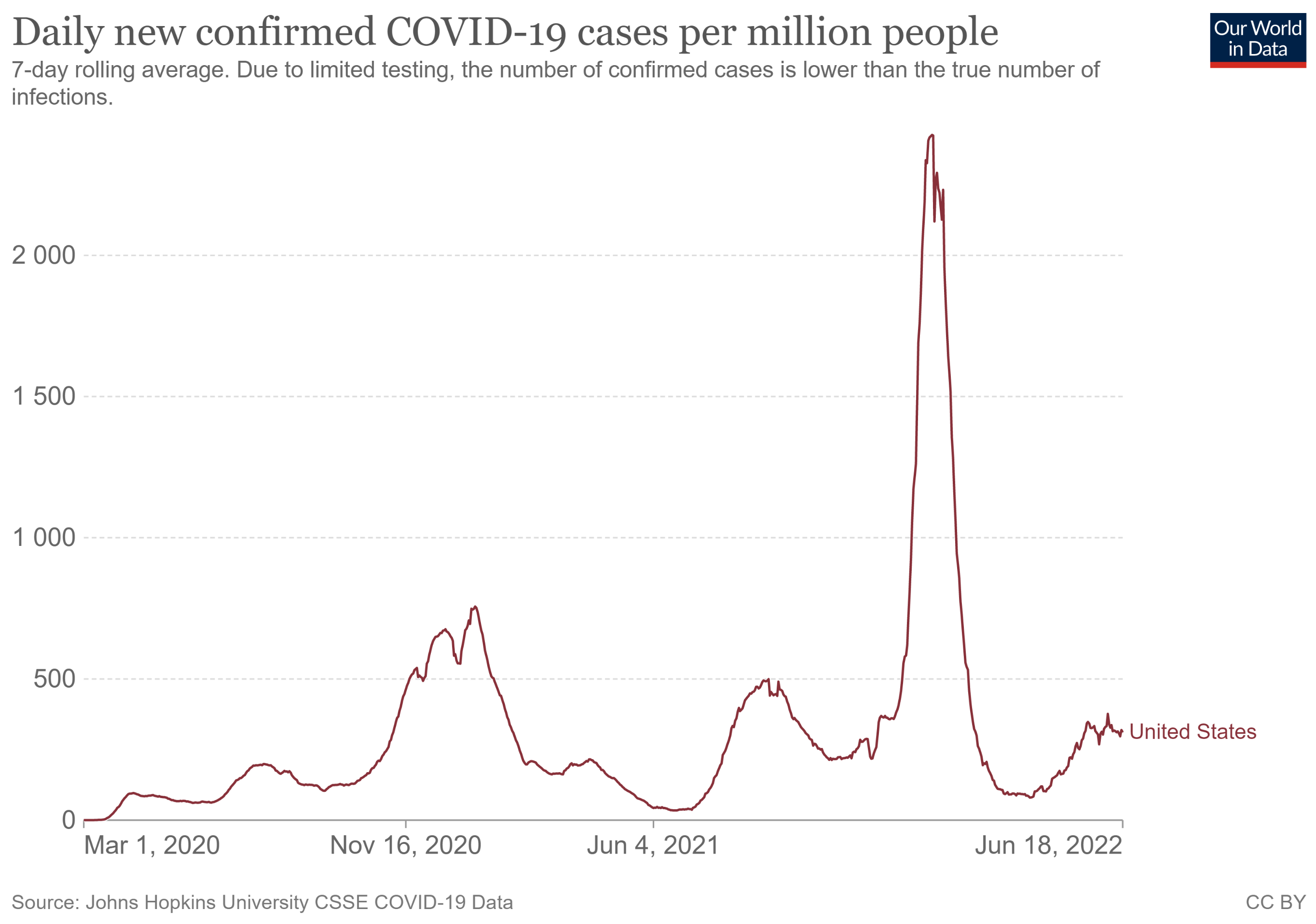

Figure 25 displays the U.S. recorded cases of COVID-19 according to John’s Hopkins university database. The few cases recorded in March 2020 can be misleading, since, at the beginning of the pandemic, there were no available self-test kits for the COVID-19 virus, little availability of face masks, and long lines in pharmacies to get tested. Nevertheless, Figure 25 is useful for detecting COVID-19 waves:

- From 2019-11-01 to 2020-10-31;

- From 2020-11-01 to 2021-05-31;

- From 2021-07-31 to 2022-03-31.

Approximately, we could therefore identify phase I before/after the lockdown period of March 2020, then phase II from November 2020 to May 2021 with another climb of epidemic cases (and public campaigns of renewed vaccines for the whole population), and finally, phase III from August 2021 (with a considerable peak visible in U.S. COVID cases) to March 2022, which coincides with another era for portfolio managers in terms of market fundamentals (namely, geopolitical concerns around oil and gas investments, as well as new monetary policy linked to two-digit inflation levels in OECD countries).

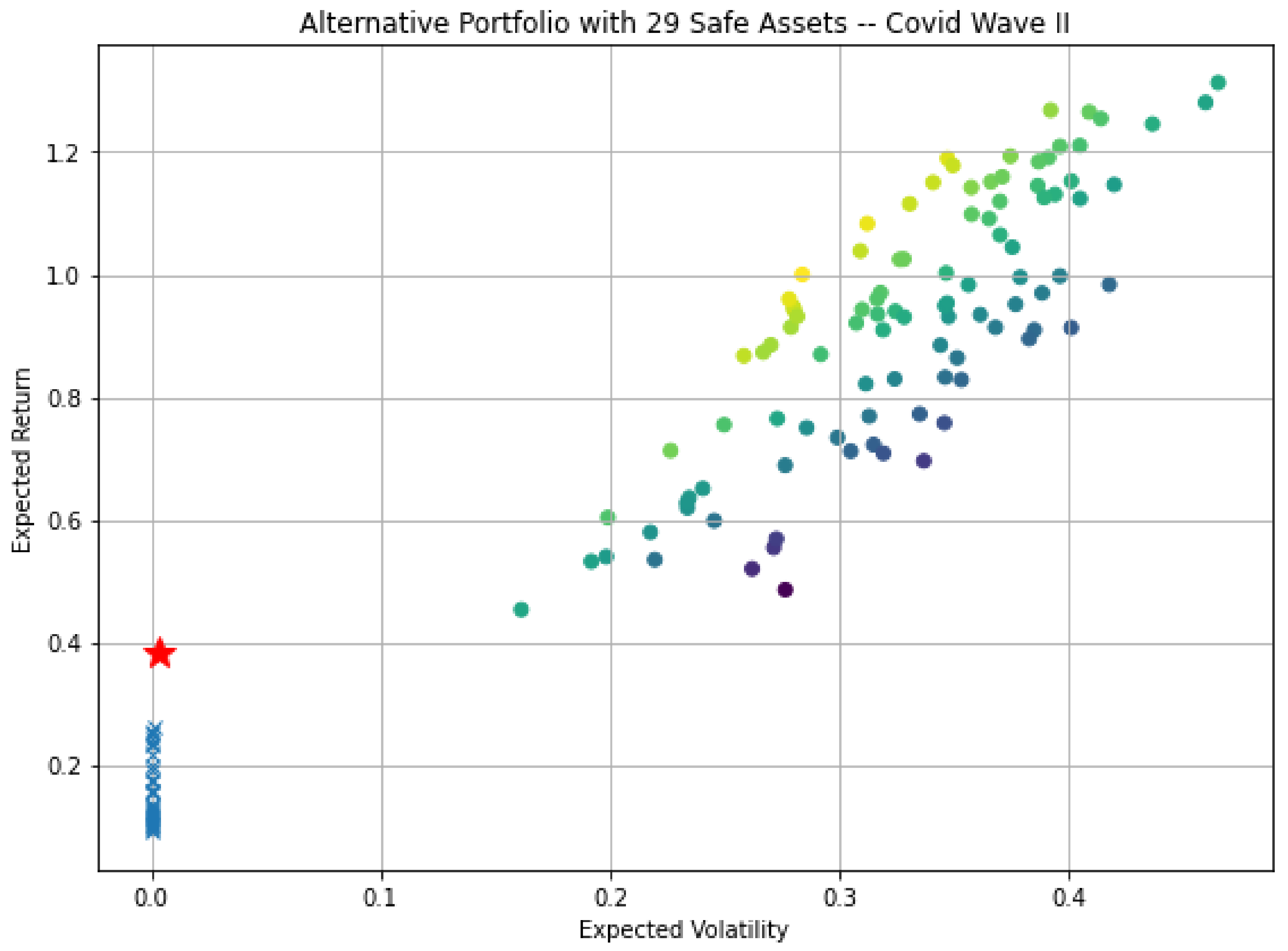

5.2.1. COVID-19 Wave II

During phase II, we re-evaluate the 29 ‘Safe-Assets’ performance selected by the portfolio manager based on his/her insights and the information drawn from the various safe-haven regressions. In Figure 26, we notice that the profitability is higher from November 2020 to March 2021. Financial markets regained trust that the health crisis is over, thanks to the scientific advances brought by the revolutionary DNA messenger technique of the COVID-19 vaccine. Therefore, the proposed selection improves regarding its performance and the uptake in stock markets worldwide. On the contrary, our strategy cannot achieve a maximum performance, since it is composed of many protective assets (e.g., our whole quest of the so-called ‘Safe’ assets comprising U.S. bonds, Swiss Francs and precious metals). On average, we record 1.2% monthly returns × 12, equal to 14.4% yearly returns (for risk levels stable around 3.30% yearly). Considering a USD 10,000,000 portfolio, the portfolio manager could have delivered a solid gain of USD 1,440,000 and a downside scenario of losing USD 330,000. Compared to phase I, this better performance is explained by the comeback of stock markets compared to the pre-COVID-19 period.

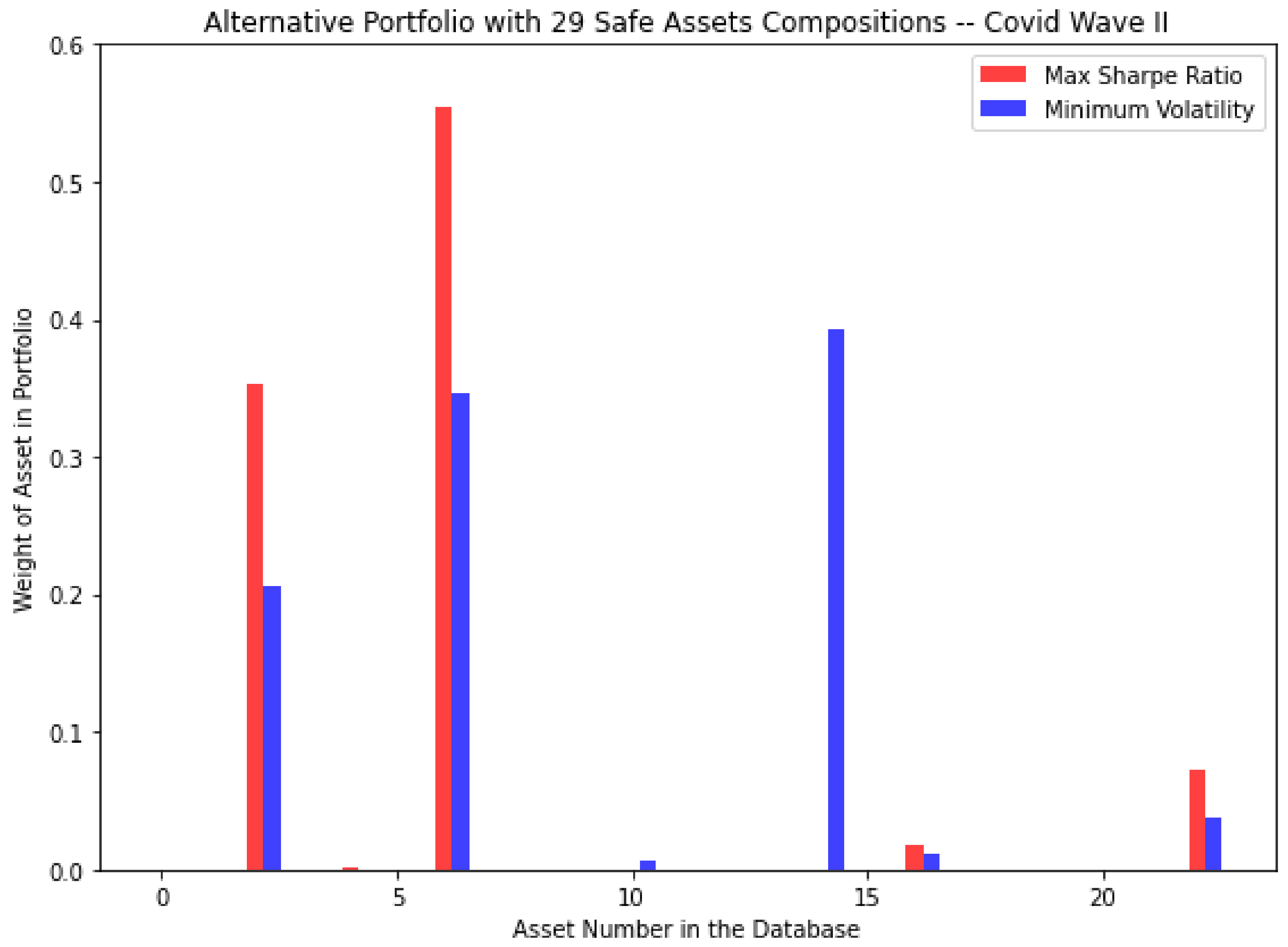

As can be observed in Figure 27, the highest weights are the following:

- S&P 500;

- PAXG-USD;

- Perth Mint Gold Token USD.

In terms of asset re-allocation, the portfolio manager would resume his/her holdings in the S&P 500 (characterized by a sudden boost) and purchase the gold-backed tokens PAXG and PMGT (which do not require the physical storage of the gold bars). We also have a look at the highest Sharpe ratios recorded:

- SSE Composite Index;

- CHF–USD.

Hence, assets that stand out in asset selection are the Swiss Franc (as a refuge for value) and Chinese stocks (similar to phase I). Mexican and Argentinian stocks can be re-sold to buy U.S. stocks. The geographical re-location of the portfolio implies moving from South America to North America whilst maintaining the allocation towards China. Short- to long-term U.S. bonds are maintained in all portfolios for a safe haven.

5.2.2. COVID-19 Wave III

During phase III, from August 2021 to March 2022, striking changes in the portfolio exposition appear. Following the epidemic peak (it has been hypothesized above that this peak of COVID-19 cases might be connected to the widespread availability of self-test kits, given that the weather is neither cold nor humid in August) in the U.S. during the summer of 2021, the optimization routine highlights the necessity to shift the portfolio massively towards U.S bonds, whatever the maturity that can be found by brokers (13 weeks to 30 years). We notice indeed the presence of two star symbols, i.e., U.S. bonds of different maturities.

In Figure 28, it is not possible anymore to draw an efficient frontier tangent to the risk-free rate. In such a bear territory (potentially returns of −0.1% in the basket of risky assets), a strategic retreat towards safe assets such as bonds constitutes the only logical investment vehicle available (holding cash itself presents purchasing parity challenges in 2022) in order to achieve a near-zero risk (0.13 × 12, equal 1.56%) and whatever the profitability that fixed income offers at that time (0.38% monthly × 12, equal 4.56% yearly).

Against the background of the worldwide demand for U.S. bonds, Figure 29 informs us when to allocate the portfolio towards the following highest weights:

- Shenzhen Component;

- JPY-USD;

- U.S. Global GO GOLD and Precious Metal Miners ETF.

Besides his/her continued investment in China, the portfolio manager would purchase the Yen currency and physical gold mine ETFs (since the cryptocurrencies’ winter mood impacts the gold-backed tokens with frequent crashes) as safe havens. The highest Sharpe ratios are achieved for the following assets:

- MERVAL;

- Soybean Futures;

- USDT-USD.

Compared to phase I, the portfolio manager resumes his/her purchase of grains (e.g., Soybean) and Argentinian stocks in phase III. Tether (in its original version, not gold-backed) is used here as a gateway to convert cryptocurrencies into fiat money. The profitability is lower than during phase I; therefore, the priority lies in cutting losses.

Thanks to the defensive strategy implemented, a notional investment of USD 10,000,000 USD would have brought a gain of USD 456,000 (associated with a potential loss of USD 156,000) during a period of turmoil characterized by doubts regarding the opportunity to detain cryptocurrencies and, in conjunction, their replacement with the emerging countries’ stocks and physical commodity holdings.

5.2.3. Risk Parity versus Equal Weighting

Last but not least, we provide an additional sensitivity analysis of the results regarding the choice of the Global Minimum Variance optimization. In what follows, we also consider the risk parity and equal weighting methodological frameworks. This section borrows notations from [34].

Risk Parity

According to [35], a standard approach, such as the mean-variance optimization, has two drawbacks in practice. First, optimal portfolios seem to be concentrated in a few assets. Second, small changes in the estimated parameters give rise to relevant modifications in the optimal portfolio composition, as remarked in Merton (1980). Form the following quantities:

where MRC stands for marginal risk contribution, and TRC for total risk contribution.

Risk parity, as in other portfolio optimization rules, identifies portfolio weights (or exposures) that satisfy specific criteria. Maillard et al. (2010) propose to perform the following minimization:

The risk parity (RP) portfolio, in the case of long-only positions, is characterized by the requirement of having equal total risk contributions from each asset:

This approach essentially constitutes a particular form of risk budgeting, where the asset allocator is distributing the same risk budget to each component, so that none dominates on an ex ante basis.

Equal Weighting

In the case of equal weighting, the allocation weight is simply set to:

Therefore, the strategy is a ‘naive’ portfolio, in which a fraction, , of wealth is allocated to each of the N assets available for investment at each rebalancing date. According to [36], there are advantages to equal weighting. When sub-asset classes have similar expected returns, volatility and correlations, the most efficient portfolio will be generated by equal weighting. Equal weighting forces the asset manager to rebalance his/her portfolio. Rebalancing will decrease the overall risk level and modestly increase returns within an asset class.

For the COVID-19 phase I (2019-11-01 to 2020-10-31), we obtain the following results when the optimization goal is set to ‘Risk Parity versus Equal Weighting’ in Table 5:

Risk parity results (7.15% returns with 2.3% downside risk) conform to the Global Minimum Variance framework (8.4% return with 3.6% downside risk). This strategy would yield a net gain of USD 714,670 over the period. The equal weighting results stand in sharp contrast: a gain of 22.95% (i.e., USD 2,294,860) could be achieved, only at the expense of a whopping level of risk (24.63%). Regarding allocation, the strategy delivers no surprises. In the risk parity model, the portfolio is over-allocated in ‘Safe assets’, such as short-term U.S. Treasuries (62.86%), intermediate-term U.S. Treasuries (14.27%), 10-year U.S. Treasuries (8.96%) and long-term U.S. Treasuries (2.30%). The remaining twelve percent are scattered around gold ETF and futures (less than 2%), Pacific stocks (about 1%) and for less than 1% each: S&P 500, Russell 2000, European stocks (FTSE, DAX, CAC and Euronext), Emerging market stocks (China, Argentina and Mexico) are silver, palladium, platinum, crude oil, coffee and Ethereum.

During COVID-19 phase II (2020-11-01 to 2021-05-31), we obtain the following results in Table 6:

Compared to the Global Minimum Variance framework (potential gain of USD 1,440,000 with 14.4% yearly returns against a 3.30% risk level), the risk parity results are disappointing during that second sub-period. Indeed, a total of USD 178 590 could be gained in this setting against a risk level of 2.4%. The allocation is oriented again towards short-term U.S. Treasuries (56.38%), intermediate-term U.S. Treasuries (11.33%), 10-year U.S. Treasuries (8.70%) and long-term U.S. Treasuries (4.24%). Other allocation shares are found in U.S. and European stocks (up to 6.67%), Pacific stocks (3.26%), emerging stock market indexes (2.19%), gold (below 2%), other precious metals (silver, palladium and platinum, all below 1%), GSCI commodities and crude oil (below 2%), and cryptocurrencies such as Bitcoin, Bitcoin Cash, Ripple, Ethereum or Dogecoin (slightly above 1%). We will not further comment on the results, which could result in a USD 8,556,710 gain, only at the expense of a potential loss of 50.8%. Therefore, this strategy is not advisable for any asset manager.

Finally, during COVID-19 phase III (2021-07-31 to 2022-03-31), we obtained the following results in Table 7:

The risk parity strategy loses USD 58,000 during phase III of COVID-19. The investor is exposed to capital losses up to 9.27%, perhaps becausE the rebalancing needed to take the new inflation dynamics and geopolitical concerns during 2021–2022 more into account. Maybe the portfolio should have been more exposed to inflation-protected bonds and energy ETFs (e.g., oil and gas). Compared to phases I and II, the asset allocation is, this time, more diversified. The treasuries account for less than half of the portfolio. Typically, we obtain the following bond purchases: short-term U.S. Treasuries (27.02%), intermediate-term U.S. Treasuries (10.56%), 10-year U.S. Treasuries (7.40%) and long-term U.S. Treasuries (4.41%). Other assets include commodities such as gold (6.85%), coffee (6.20%), GSCI Index (5.22%), platinum (3.56%) or silver (2.39%). Next come European stocks (6,87%), followed by emerging markets and Pacific stocks (6.13%), the U.S. stock market (5.06%), and other developed markets’ stocks (2.37%). Cryptocurrencies (Bitcoin, Bitcoin Cash, Ethereum, Dogecoin, Ripple and Dash) amount to only 4.30% of the portfolio, given that rising electricity production concerns and peaks in electricity demand endanger their mining capability. In the equal weighting scheme, USD 2,194,170 can be gained, again at the expense of a too-wide risk margin of 41.82%.

Overall, the empirical results from the Minimum Variance Portfolio with Monte Carlo simulations underline that the assets with the highest weights in the optimal portfolio change each period:

- Phase I: A mix of stock markets (China, Australia, Mexico and Argentina), and a basket of commodities and cryptocurrencies;

- Phase II: S&P500 and the gold-backed tokens PAXG and PMGT;

- Phase III: Chinese stocks, Yen currency, and physical goldmine ETFs.

The robustness checks have confirmed the sound performance of the Global Minimum Variance portfolio optimization routine regarding risk/return metrics over the three COVID-19 phases.

5.3. Policy Implications

In the digital finance, the econometric study of the crypto-currency price series is experiencing an unprecedented boom. On the contrary, Central Bank presidents continue to declare that cryptocurrencies are worthless and that only a digital currency with the Central Bank as a guarantor would have a fundamental role in money creation. Therefore, this article’s object of study is both contemporary and original, which gives rise to economic implications on the usefulness of cryptocurrencies.

In particular, the scientific interest of this article consists in including gold-backed cryptocurrencies as a basket of financial assets to diversify the pandemic risks within the methodological framework of minimum variance portfolio optimization. The transversality of the scientific approach is at the crossroads of economics (study of price mechanisms), management (survey of financial markets), and computer science (programming of various recent models of the interaction of cryptocurrency prices with financial markets and commodities with open-source software such as R (Cran) and Python).

In terms of the commercial impact, this academic paper’s findings can be used by market practitioners on their Bloomberg terminal, in the PORT+AIM applications, for instance. Portfolio holdings have been precisely documented in the text, which makes it effortless to replicate and invest with clients’ assets under management.

6. Conclusions

The pandemic has significantly impacted all the sectors concerned by the financial markets, such as between 19 February and 23 March 2020, when the S&P 500 index fell by 32%. This prompted investors to seek safe havens such as bonds, foreign exchange, gold and potentially other assets such as cryptocurrencies. Comparatively to gold or Bitcoin, some gold-backed tokens are negatively correlated to the S&P, demonstrating some leeway for this asset class to be a better hedge against risk. In a portfolio management exercise, this paper assesses the performance of a selection of gold-backed cryptocurrencies, such as PAX Gold, Digix gold, Tether Gold, and Perth Mint Gold Token. This article is, therefore, one of the first research papers to analyze the potential of gold-based cryptocurrencies as safe havens and their impact on portfolio diversification.

During times of recession, stock markets’ volatility has a lesser impact on the volatility of gold-backed cryptocurrencies such as PAXG, DGX, XAUT and PMGT, thereby relying on the safe-haven property of such gold-backed cryptocurrencies. An asset is considered a safe haven if its value remains stable or increases during bearish market phases; its returns are not negatively correlated with other assets in times of crisis. Gold-backed cryptocurrencies can be considered an investment vehicle for asset managers during times of crisis.

In this paper, ‘Safe asset’ regressions à la [1,2] confirm the potential of five defensive assets, among which are short- to long-term U.S. bonds, physical gold, gold-backed tokens and other cryptocurrencies. A total of 56 assets are selected to compose a broad portfolio of stocks, bonds, exchange rates, commodities and cryptocurrencies. In the benchmark, the tangent portfolio to the efficient frontier is composed of U.S. bonds as risk-free assets. Several gold-backed tokens also fulfill the role of the safe haven, thereby verifying the hypothesis that gold-backed cryptocurrencies could generate profitability in times of crisis. Instead of monetizing losses on the S&P 500, the benchmark portfolio delivers a performance of 7.2% yearly (for 3.6% risk). Robustness checks confirm these results in the risk parity framework. For instance, we obtain 7.15% returns with 2.3% downside risk. Another alternative portfolio is composed of 29 ‘Safe’ assets, guided by the safe-haven regressions à la [1,2]. Regarding equities, the portfolio composition shifts back and forth from emerging countries (China, Argentina, Mexico) to the U.S. stock market, depending on whether the S&P 500 recovers from the pandemic lockdown or tanks again due to systematic risk. From November 2020 to March 2021, the uptake in the financial markets allows for delivering a yearly performance of 14.4% (for 3.30% risk) with the alternative portfolio. It is possible that during that particular phase II, the strategy was too protective about the stocks’ exposition. From August 2021 to March 2022, the profitability dropped like a stone to 4.56%, guided by the low earnings of quantitative easing. Protective assets take the form of the Yen currency, grains, and gold mine ETFs.

During the COVID-19 crisis, stock markets entered a bear market. Our analysis reveals that COVID-19 had a weaker impact on gold-backed cryptocurrencies in terms of returns and volatility. Therefore, gold-backed cryptocurrencies could be added to the asset managers’ toolkit as a hedge against the stock markets’ fluctuations.

The shortcoming of the present work is that it stops in March 2022 at the end of COVID-19 Phase III. Much has changed in the world since then for portfolio managers, the main topics being, of course, geopolitical concerns, the persistence of high inflation and the rise of interest rates in OECD countries. Consequently, areas for future research cover updated portfolio simulations, where the asset managers would rebalance their portfolios towards natural gas and crude oil ETFs and flee buyout debt in the bond markets.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Data were last downloaded in December 2022 from private and public repositories such as the Refinitiv Eikon Datastream https://www.refinitiv.com/en/products/datastream-macroeconomic-analysis accessed on 19 January 2023 and FRED https://fred.stlouisfed.org/ accessed on 19 January 2023. Tickers used from FRED and the Datastream can be transmitted per request to the author. The proprietary (licensed) data cannot be transmitted.

Acknowledgments

For comments and feedbacks, I wish to thank Aidas Malakauskas, Sofiane Aboura, Jose Manuel Carbo Martinez, Michael Froemmel and Efe Cotelioglu as well as conference participants at the 11th International Research Meeting in Business and Management (IRMBAM 2022, Nice, France), the 16th International Conference on Computational and Financial Econometrics (CFE 2022, London, UK), and the 8th Paris Financial Management Conference (PFMC 2022, Paris, France).

Conflicts of Interest

The author declares no conflict of interest.

Appendix A

Appendix A.1. Non-Nested Version of [1]’s Safe-Haven Regressions

The presentation here follows [37]:

with being the return on precious metals’ assets (gold, silver and platinum) or stock markets (VIX); being the error term; being a dummy variable capturing the sharp declines of stock markets with a value of 1 above a given threshold and 0 otherwise; and the quantiles of the distribution of the stock market’s returns. Equation (A3) features a GARCH . If the coefficients of Equation (A2) are statistically significant and negative, the asset is considered a refuge for value.

Appendix A.2. DCC Model

Let represents the price returns computed as the asset price logarithmic first difference . Let denote an vector of innovations at time t, which is assumed to be conditionally normal with the mean zero and covariance of matrix :

where represents the information set at time . The conditional covariance matrix can be decomposed, as follows [40]:

is the time-varying correlation matrix. diag is the diagonal matrix of time-varying standard deviations extracted from univariate GARCH models with on the ith diagonal. The dynamic conditional correlation structure in matrix form is given by:

An element of has the following form:

is a diagonal matrix composed of the square root of the diagonal elements of the covariance matrix, . The covariance matrix of the DCC model evolves according to:

where the unconditional covariance matrix is composed of the vector of standardized residuals computed from the first stage procedure, for which . A and B are diagonal matrices, where and . The scalar version of the DCC model can be written as:

Following [28], we estimate the corrected version of the DCC (cDCC).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table A1.

Descriptive statistics.

| Variable | Mean | Median | Minimum | Maximum |

|---|---|---|---|---|

| GSPC | 3117.7 | 3193.9 | 2237.4 | 3580.8 |

| DJI | 25,843 | 26,379 | 18,592 | 29,101 |

| IXIC | 10,008 | 10,402 | 6860.7 | 12,056 |

| RUT | 1417.2 | 1452.1 | 991.16 | 1649.1 |

| GDAXI | 11,921 | 12,495 | 8441.7 | 13,255 |

| FCHI | 4758.4 | 4875.9 | 3754.8 | 5197.8 |

| N100 | 943.18 | 972.5 | 733.93 | 1017.8 |

| N225 | 21,758 | 22,549 | 16,553 | 23,671 |

| HSI | 24,378 | 24,458 | 21,696 | 26,339 |

| SS | 3098.5 | 3214.1 | 2660.2 | 3451.1 |

| SZ | 12,159 | 12,817 | 9691.5 | 14,149 |

| AXJO | 5773.6 | 5927.6 | 4735.7 | 6210.3 |

| AORD | 5898.3 | 6069.2 | 4753.3 | 6414.2 |

| JKSE | 4892.4 | 4958.8 | 3937.6 | 5371.5 |

| KS11 | 2137.3 | 2184.3 | 1457.6 | 2443.6 |

| GSPTSE | 15,408 | 15,671 | 11,229 | 16,790 |

| BVSP | 91804 | 95983 | 63570 | 1.06 × 10 |

| MXX | 36,821 | 36,981 | 32,964 | 39,954 |

| MERV | 40,799 | 42,748 | 22,087 | 52,513 |

| CHFUSDX | 1.0654 | 1.0612 | 1.0114 | 1.1077 |

| JPYUSDX | 0.0093679 | 0.00936 | 0.0089855 | 0.0095863 |

| EURUSDX | 1.1387 | 1.1339 | 1.0657 | 1.1948 |

| GBPUSDX | 1.2667 | 1.2609 | 1.1494 | 1.3399 |

| GOAU | 19.983 | 20.643 | 10.635 | 25.583 |

| GCF | 1807.6 | 1799.2 | 1477.3 | 2051.5 |

| SIF | 20.553 | 18.983 | 11.735 | 29.249 |

| PAF | 2097.3 | 2154.1 | 1449.9 | 2454 |

| PLF | 849.27 | 858.1 | 595.9 | 1009.6 |

| GDF | 316.88 | 334.6 | 245.9 | 360.1 |

| CLF | 34.371 | 39.22 | −37.63 | 43.39 |

| ZSF | 912.05 | 884.25 | 821.75 | 1087.8 |

| KCF | 109.94 | 109.15 | 93.65 | 134.8 |

| BTCF | 9751.5 | 9655 | 4930 | 13685 |

| BTGUSD | 8.9524 | 9.0663 | 5.9208 | 11.628 |

| BCHUSD | 244.95 | 238.15 | 170.74 | 317.3 |

| LTCUSD | 47.343 | 45.924 | 32.876 | 67.028 |

| ETHUSD | 278.39 | 244.14 | 110.61 | 477.05 |

| USDTUSD | 1.0015 | 1.0011 | 0.97425 | 1.0202 |

| XRPUSD | 0.22113 | 0.20518 | 0.14106 | 0.31477 |

| XLMUSD | 0.075237 | 0.07354 | 0.035161 | 0.11365 |

| DOGEUSD | 0.0026639 | 0.002596 | 0.001566 | 0.00475 |

| XMRUSD | 77.576 | 67.922 | 33.816 | 133.73 |

| ZECUSD | 56.183 | 55.515 | 24.504 | 96.03 |

| DASHUSD | 74.994 | 73.189 | 42.945 | 100.56 |

| DGXUSD | 58.306 | 57.899 | 47.26 | 68.394 |

| PAXGUSD | 1819.9 | 1801.6 | 1513.5 | 2083.3 |

| PMGTUSD | 1818.3 | 1798.6 | 1438.8 | 2173.4 |

| XAUTUSD | 1805 | 1795 | 1466.9 | 2014 |

| VIX | 32.733 | 28.51 | 21.35 | 82.69 |

| FTSE | 5951.9 | 6000 | 4993.9 | 6484.3 |

| EUROBOND | 22.951 | 23.06 | 21.79 | 23.6 |

| US30Y | 1.3948 | 1.372 | 0.937 | 1.918 |

| US10Y | 0.72545 | 0.676 | 0.499 | 1.471 |

| US5Y | 0.40394 | 0.335 | 0.195 | 1.318 |

| US13WK | 0.19722 | 0.11 | −0.105 | 1.518 |

| GSPC | 302.8 | 0.097122 | −0.81474 | −0.06963 |

| DJI | 2291.3 | 0.088662 | −0.93106 | 0.29012 |

| IXIC | 1335 | 0.13339 | −0.63954 | −0.59918 |

| RUT | 163.72 | 0.11553 | −0.77733 | −0.3176 |

| GDAXI | 1231.9 | 0.10334 | −0.97326 | −0.14441 |

| FCHI | 301 | 0.063257 | −1.0631 | 0.55411 |

| N100 | 62.133 | 0.065876 | −1.1804 | 0.77202 |

| N225 | 1875.6 | 0.086201 | −1.0678 | 0.034426 |

| HSI | 793.67 | 0.032556 | −0.49475 | 0.86656 |

| SS | 240.06 | 0.077474 | −0.1275 | −1.6337 |

| SZ | 1376.2 | 0.11318 | −0.22476 | −1.5779 |

| AXJO | 374.67 | 0.064894 | −1.0154 | −0.052617 |

| AORD | 420.36 | 0.071267 | −0.98265 | −0.1473 |

| JKSE | 298.4 | 0.060992 | −0.81914 | 0.39934 |

| KS11 | 236.87 | 0.11082 | −0.73733 | −0.35043 |

| GSPTSE | 1189.6 | 0.077205 | −1.3052 | 1.248 |

| BVSP | 10,827 | 0.11793 | −0.75801 | −0.78076 |

| MXX | 1429.3 | 0.038818 | −0.61974 | −0.14357 |

| MERV | 7872.8 | 0.19297 | −0.78904 | −0.37632 |

| CHFUSDX | 0.029413 | 0.027608 | −0.069166 | −1.562 |

| JPYUSDX | 0.0001176 | 0.012553 | −0.6437 | 0.81207 |

| EURUSDX | 0.040198 | 0.035303 | −0.18048 | −1.5264 |

| GBPUSDX | 0.037276 | 0.029428 | −0.43277 | 0.21355 |

| GOAU | 3.6367 | 0.18199 | −0.85314 | −0.024357 |

| GCF | 125.62 | 0.069499 | −0.35429 | −0.48181 |

| SIF | 4.8286 | 0.23494 | 0.09444 | −1.4002 |

| PAF | 211.42 | 0.1008 | −0.57303 | −0.13504 |

| PLF | 82.21 | 0.096801 | −0.60296 | 0.3686 |

| GDF | 38.71 | 0.12216 | −0.61853 | −1.1208 |

| CLF | 10.239 | 0.29789 | −2.7282 | 13.67 |

| ZSF | 76.078 | 0.083415 | 0.9121 | −0.53116 |

| KCF | 9.9735 | 0.090715 | 0.43049 | −0.45326 |

| BTCF | 1858 | 0.19053 | −0.36163 | −0.30078 |

| BTGUSD | 1.084 | 0.12109 | −0.15058 | −0.34292 |

| BCHUSD | 25.953 | 0.10595 | 0.56283 | 0.44416 |

| LTCUSD | 6.5943 | 0.13929 | 0.79179 | 0.20097 |

| ETHUSD | 94.811 | 0.34057 | 0.095365 | −1.3247 |

| USDTUSD | 0.0046009 | 0.004594 | −1.2207 | 14.747 |

| XRPUSD | 0.039326 | 0.17784 | 0.46479 | −0.53483 |

| XLMUSD | 0.01851 | 0.24602 | −0.20333 | −0.39884 |

| DOGEUSD | 0.0005364 | 0.20138 | 0.50818 | 0.89287 |

| XMRUSD | 22.987 | 0.29631 | 0.67723 | −0.18783 |

| ZECUSD | 15.341 | 0.27306 | 0.30926 | −0.24892 |

| DASHUSD | 8.5303 | 0.11375 | 0.28582 | 1.9477 |

| DGXUSD | 3.5698 | 0.061226 | −0.29486 | 0.62835 |

| PAXGUSD | 121.36 | 0.066685 | −0.14414 | −0.67559 |

| PMGTUSD | 134.5 | 0.073972 | −0.20357 | −0.40763 |

| XAUTUSD | 123.04 | 0.068164 | −0.3203 | −0.49998 |

| VIX | 11.645 | 0.35577 | 2.1719 | 4.7363 |

| FTSE | 270.06 | 0.045374 | −1.1288 | 1.7434 |

| EUROBOND | 0.43657 | 0.019022 | −0.5369 | −0.71108 |

| US30Y | 0.16006 | 0.11476 | 0.98626 | 1.5418 |

| US10Y | 0.17981 | 0.24786 | 2.2695 | 5.3534 |

| US5Y | 0.20918 | 0.51784 | 2.5682 | 6.8095 |

| US13WK | 0.31325 | 1.5883 | 3.2977 | 10.057 |

| GSPC | 2476.9 | 3484.5 | 465.18 | 0 |

| DJI | 21067 | 28512 | 3501.9 | 0 |

| IXIC | 7374.2 | 11693 | 2089 | 0 |

| RUT | 1086.9 | 1627.9 | 241.75 | 0 |

| GDAXI | 9547.4 | 13,193 | 2029.6 | 0 |

| FCHI | 4208.6 | 5080.8 | 471.89 | 0 |

| N100 | 828 | 1007.4 | 96.42 | 0 |

| N225 | 17,845 | 23,559 | 3048.6 | 0 |

| HSI | 23,066 | 25,546 | 972.85 | 0 |

| SS | 2751.7 | 3404.7 | 464.98 | 0 |

| SZ | 10110 | 13851 | 2676.8 | 0 |

| AXJO | 5005 | 6173.2 | 586.75 | 0 |

| AORD | 5016.3 | 6382.7 | 652.35 | 0 |

| JKSE | 4418.7 | 5280.4 | 485.38 | 0 |

| KS11 | 1688.1 | 2407.5 | 407.23 | 0 |

| GSPTSE | 12,707 | 16,625 | 1444.5 | 0 |

| BVSP | 71,277 | 1.04 × 10 | 20,040 | 0 |

| MXX | 33,923 | 38,708 | 1772.2 | 0 |

| MERV | 24,478 | 50,998 | 8672 | 0 |

| CHFUSDX | 1.0244 | 1.1028 | 0.060738 | 0 |

| JPYUSDX | 0.0091647 | 0.009552 | 0.0001665 | 0 |

| EURUSDX | 1.0804 | 1.1874 | 0.08307 | 0 |

| GBPUSDX | 1.22 | 1.322 | 0.057138 | 0 |

| GOAU | 12.31 | 24.295 | 4.6113 | 0 |

| GCF | 1587.3 | 1968.1 | 206.25 | 0 |

| SIF | 14.076 | 27.602 | 8.709 | 0 |

| PAF | 1756.8 | 2391.1 | 335.65 | 0 |

| PLF | 712.48 | 970.65 | 109.15 | 0 |

| GDF | 249.86 | 360.02 | 72.61 | 0 |

| CLF | 17.073 | 42.751 | 13.6 | 0 |

| ZSF | 830.85 | 1061.8 | 114.88 | 0 |

| KCF | 95.95 | 129.93 | 14.25 | 0 |

| BTCF | 6389.5 | 12728 | 2108.8 | 0 |

| BTGUSD | 7.3048 | 10.655 | 1.6849 | 0 |

| BCHUSD | 216.09 | 296.36 | 30.77 | 0 |

| LTCUSD | 39.14 | 59.358 | 6.5723 | 0 |

| ETHUSD | 134.98 | 416.17 | 170.38 | 0 |

| USDTUSD | 0.99706 | 1.0079 | 0.002584 | 0 |

| XRPUSD | 0.16575 | 0.2976 | 0.05463 | 0 |

| XLMUSD | 0.040603 | 0.10505 | 0.019332 | 0 |

| DOGEUSD | 0.001813 | 0.003517 | 0.000634 | 0 |

| XMRUSD | 47.062 | 127 | 29.484 | 0 |

| ZECUSD | 31.875 | 84.1 | 18.816 | 0 |

| DASHUSD | 65.982 | 92.32 | 9.5895 | 0 |

| DGXUSD | 52.921 | 63.905 | 4.5996 | 0 |

| PAXGUSD | 1630.3 | 1986.7 | 199.32 | 0 |

| PMGTUSD | 1608.9 | 1991 | 221.91 | 0 |

| XAUTUSD | 1634.5 | 1982.6 | 200.05 | 0 |

| VIX | 22.289 | 61.662 | 8.22 | 0 |

| FTSE | 5371 | 6292.6 | 290.76 | 0 |

| EUROBOND | 22.22 | 23.539 | 0.715 | 0 |

| US30Y | 1.1983 | 1.7338 | 0.1695 | 0 |

| US10Y | 0.562 | 1.127 | 0.1145 | 0 |

| US5Y | 0.2291 | 0.9082 | 0.1185 | 0 |

| US13WK | −0.0325 | 1.2205 | 0.0525 | 0 |

References

- Baur, D.G.; McDermott, T.K. Is gold a safe haven? International evidence. J. Bank. Financ. 2010, 34, 1886–1898. [Google Scholar] [CrossRef]

- Kliber, A. Looking for a safe haven against American stocks during COVID-19 pandemic. N. Am. J. Econ. Financ. 2022, 63, 101825. [Google Scholar] [CrossRef]

- Wasiuzzaman, S.; Rahman, H.S.W.H.A. Performance of gold-backed cryptocurrencies during the COVID-19 crisis. Financ. Res. Lett. 2021, 43, 101958. [Google Scholar] [CrossRef] [PubMed]

- Jalan, A.; Matkovskyy, R.; Yarovaya, L. “Shiny” crypto assets: A systemic look at gold-backed cryptocurrencies during the COVID-19 pandemic. Int. Rev. Financ. Anal. 2021, 78, 101958. [Google Scholar] [CrossRef] [PubMed]

- Baur, D.G.; Dimpfl, T. A Safe Haven Index. 2021. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3641589 (accessed on 19 January 2023).

- Mokni, K.; Youssef, M.; Ajmi, A.N. COVID-19 pandemic and economic policy uncertainty: The first test on the hedging and safe haven properties of cryptocurrencies. Res. Int. Bus. Financ. 2022, 60, 101573. [Google Scholar] [CrossRef]

- Ji, Q.; Zhang, D.; Zhao, Y. Searching for safe-haven assets during the COVID-19 pandemic. Int. Rev. Financ. Anal. 2020, 71, 101526. [Google Scholar] [CrossRef]

- Salisu, A.A.; Raheem, I.D.; Vo, X.V. Assessing the safe haven property of the gold market during COVID-19 pandemic. Int. Rev. Financ. Anal. 2021, 74, 101666. [Google Scholar] [CrossRef]

- Lahiani, A.; Mefteh-Wali, S.; Vasbieva, D.G. The safe-haven property of precious metal commodities in the COVID-19 era. Resour. Policy 2021, 74, 102340. [Google Scholar] [CrossRef]

- Kumar, A.S.; Padakandla, S.R. Testing the safe-haven properties of gold and bitcoin in the backdrop of COVID-19: A wavelet quantile correlation approach. Financ. Res. Lett. 2022, 47, 102707. [Google Scholar] [CrossRef]

- Tronzano, M. Optimal Portfolio Allocation between Global Stock Indexes and Safe Haven Assets: Gold versus the Swiss Franc (1999–2021). J. Risk Financ. Manag. 2022, 15, 241. [Google Scholar] [CrossRef]

- Baur, D.G.; Lucey, B.M. Is gold a hedge or a safe haven? An analysis of stocks, bonds and gold. Financ. Rev. 2010, 45, 217–229. [Google Scholar] [CrossRef]

- Akhtaruzzaman, M.; Boubaker, S.; Lucey, B.M.; Sensoy, A. Is gold a hedge or a safe-haven asset in the COVID–19 crisis? Econ. Model. 2021, 102, 105588. [Google Scholar] [CrossRef]

- Klein, T.; Thu, H.P.; Walther, T. Bitcoin is not the New Gold—A comparison of volatility, correlation, and portfolio performance. Int. Rev. Financ. Anal. 2018, 59, 105–116. [Google Scholar] [CrossRef]

- Wen, F.; Tong, X.; Ren, X. Gold or Bitcoin, which is the safe haven during the COVID-19 pandemic? Int. Rev. Financ. Anal. 2022, 81, 102121. [Google Scholar] [CrossRef]

- Mariana, C.D.; Ekaputra, I.A.; Husodo, Z.A. Are Bitcoin and Ethereum safe-havens for stocks during the COVID-19 pandemic? Financ. Res. Lett. 2021, 38, 101798. [Google Scholar] [CrossRef]

- Allen, D.E. Cryptocurrencies, Diversification and the COVID-19 Pandemic. J. Risk Financ. Manag. 2022, 15, 103. [Google Scholar] [CrossRef]

- Maasoumi, E.; Wu, X. Contrasting cryptocurrencies with other assets: Full distributions and the COVID Impact. J. Risk Financ. Manag. 2021, 14, 440. [Google Scholar] [CrossRef]

- Kristoufek, L. Grandpa, grandpa, tell me the one about Bitcoin being a safe haven: New evidence from the COVID-19 pandemic. Front. Phys. 2020, 8, 296. [Google Scholar] [CrossRef]

- Conlon, T.; Corbet, S.; McGee, R.J. Are cryptocurrencies a safe haven for equity markets? An international perspective from the COVID-19 pandemic. Res. Int. Bus. Financ. 2020, 54, 101248. [Google Scholar] [CrossRef]

- Lahmiri, S.; Bekiros, S. The impact of COVID-19 pandemic upon stability and sequential irregularity of equity and cryptocurrency markets. Chaos Solitons Fractals 2020, 138, 109936. [Google Scholar] [CrossRef]

- Grobys, K. When Bitcoin has the flu: On Bitcoin’s performance to hedge equity risk in the early wake of the COVID-19 outbreak. Appl. Econ. Lett. 2021, 28, 860–865. [Google Scholar] [CrossRef]

- Yan, K.; Yan, H.; Gupta, R. Are GARCH and DCC values of 10 cryptocurrencies affected by COVID-19? J. Risk Financ. Manag. 2022, 15, 113. [Google Scholar] [CrossRef]

- Hasan, M.B.; Hassan, M.K.; Rashid, M.M.; Alhenawi, Y. Are safe haven assets really safe during the 2008 global financial crisis and COVID-19 pandemic? Glob. Financ. J. 2021, 50, 100668. [Google Scholar] [CrossRef]

- Kyriazis, N.A.; Daskalou, K.; Arampatzis, M.; Prassa, P.; Papaioannou, E. Estimating the volatility of cryptocurrencies during bearish markets by employing GARCH models. Heliyon 2019, 5, e02239. [Google Scholar] [CrossRef] [PubMed]

- Disli, M.; Nagayev, R.; Salim, K.; Rizkiah, S.K.; Aysan, A.F. In search of safe haven assets during COVID-19 pandemic: An empirical analysis of different investor types. Res. Int. Bus. Financ. 2021, 58, 101461. [Google Scholar] [CrossRef]

- Glosten, L.R.; Jagannathan, R.; Runkle, D.E. On the relation between the expected value and the volatility of the nominal excess return on stocks. J. Financ. 1993, 48, 1779–1801. [Google Scholar] [CrossRef]

- Aielli, G.P. Dynamic conditional correlation: On properties and estimation. J. Bus. Econ. Stat. 2013, 31, 282–299. [Google Scholar] [CrossRef]

- Ghalanos, A. rmgarch: Multivariate GARCH models, CRAN. R Package Version 2019, 1, 1–3. [Google Scholar]

- Haugen, R.A.; Baker, N.L. The efficient market inefficiency of capitalization–weighted stock portfolios. J. Portf. Manag. 1991, 17, 35–40. [Google Scholar] [CrossRef]

- Chan, L.K.; Karceski, J.; Lakonishok, J. On portfolio optimization: Forecasting covariances and choosing the risk model. Rev. Financ. Stud. 1999, 12, 937–974. [Google Scholar] [CrossRef] [Green Version]

- Jagannathan, R.; Ma, T. Risk reduction in large portfolios: Why imposing the wrong constraints helps. J. Financ. 2003, 58, 1651–1683. [Google Scholar] [CrossRef]

- Clarke, R.G.; De Silva, H.; Thorley, S. Minimum-variance portfolios in the US equity market. J. Portf. Manag. 2006, 33, 10–24. [Google Scholar] [CrossRef]

- Chevallier, J.; Vo, D.T. Portfolio allocation across variance risk premia. J. Risk Financ. 2019, 20, 556–593. [Google Scholar] [CrossRef]

- Maillard, S.; Roncalli, T.; Teïletche, J. The properties of equally weighted risk contribution portfolios. J. Portf. Manag. 2010, 36, 60–70. [Google Scholar] [CrossRef]

- Chow, T.m.; Hsu, J.; Kalesnik, V.; Little, B. A survey of alternative equity index strategies. Financ. Anal. J. 2011, 67, 37–57. [Google Scholar] [CrossRef]