Climate Change and Grain Price Volatility: Empirical Evidence for Corn and Wheat 1971–2019

Abstract

:1. Introduction

2. Climate Change, Food Production and Prices

3. Data and Descriptive Statistics

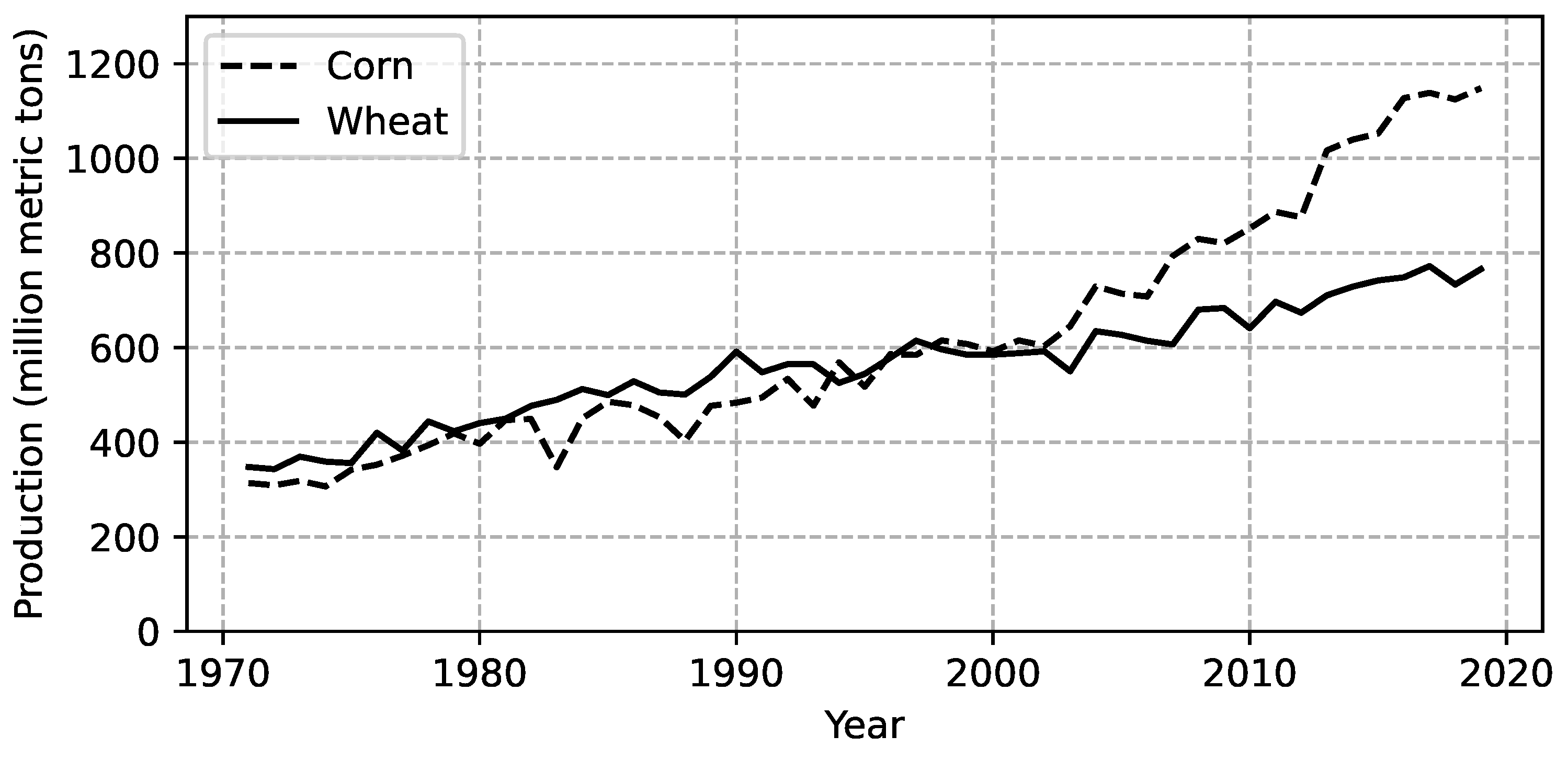

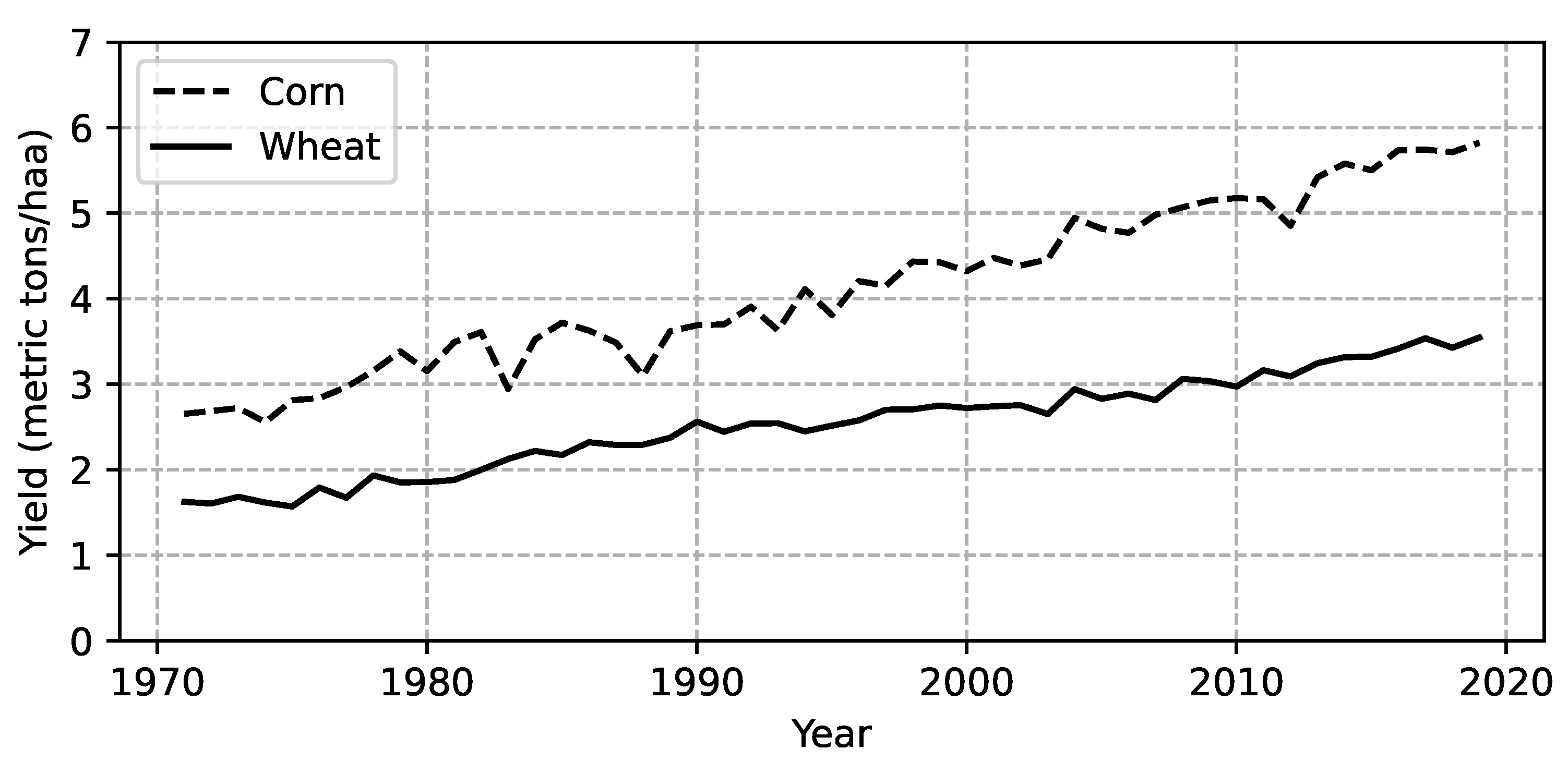

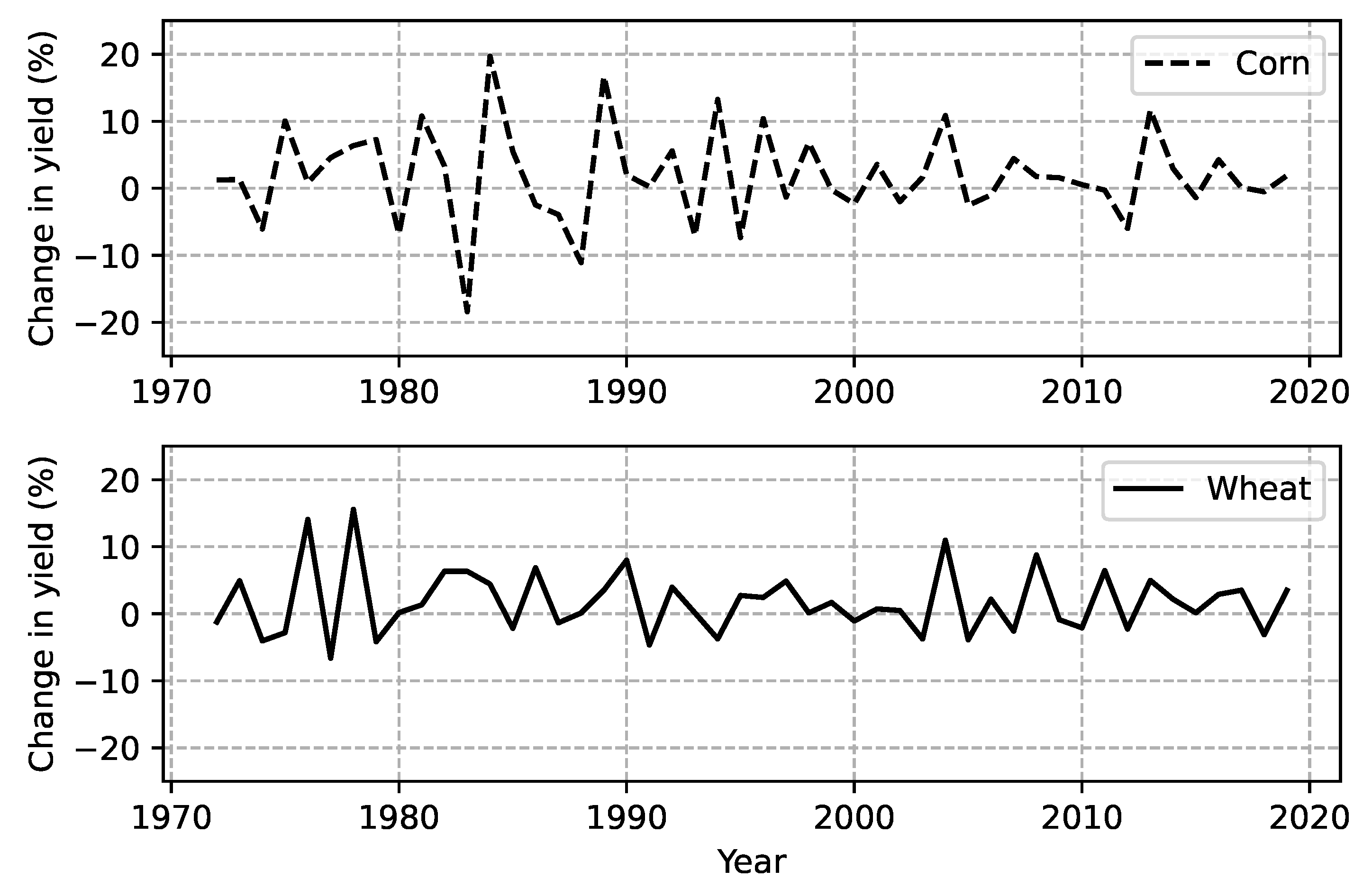

3.1. Global Wheat and Corn Production 1971–2019

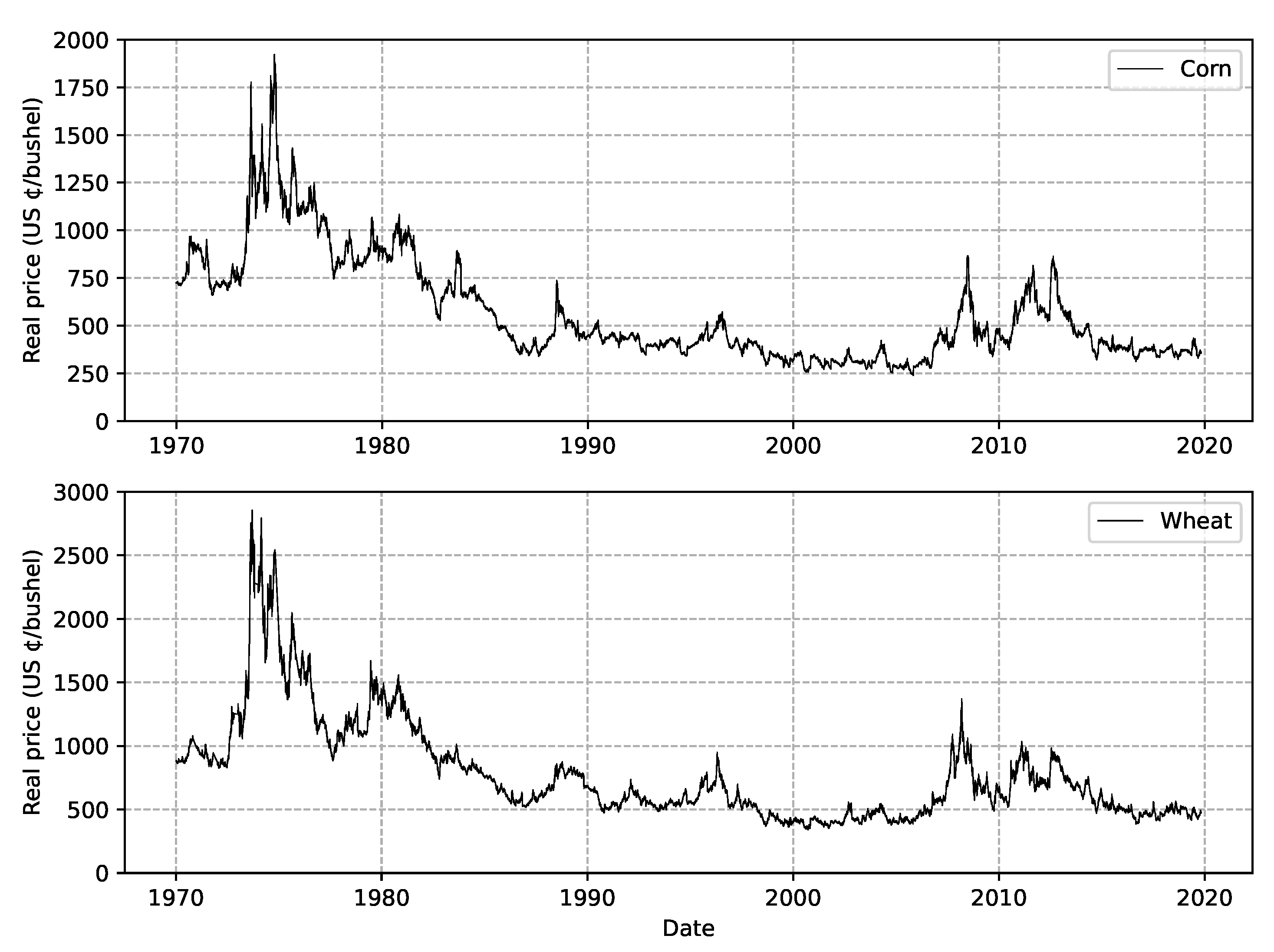

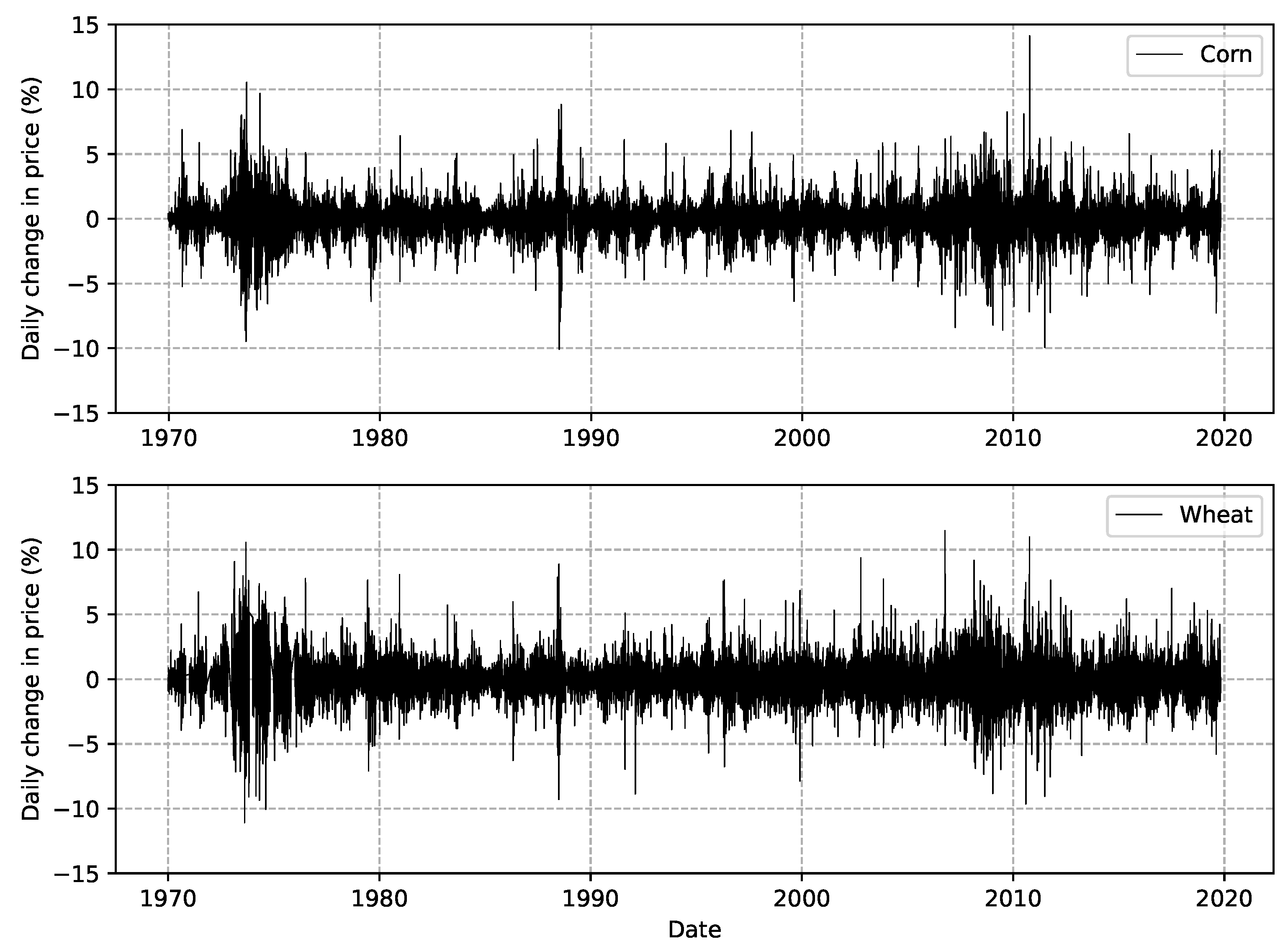

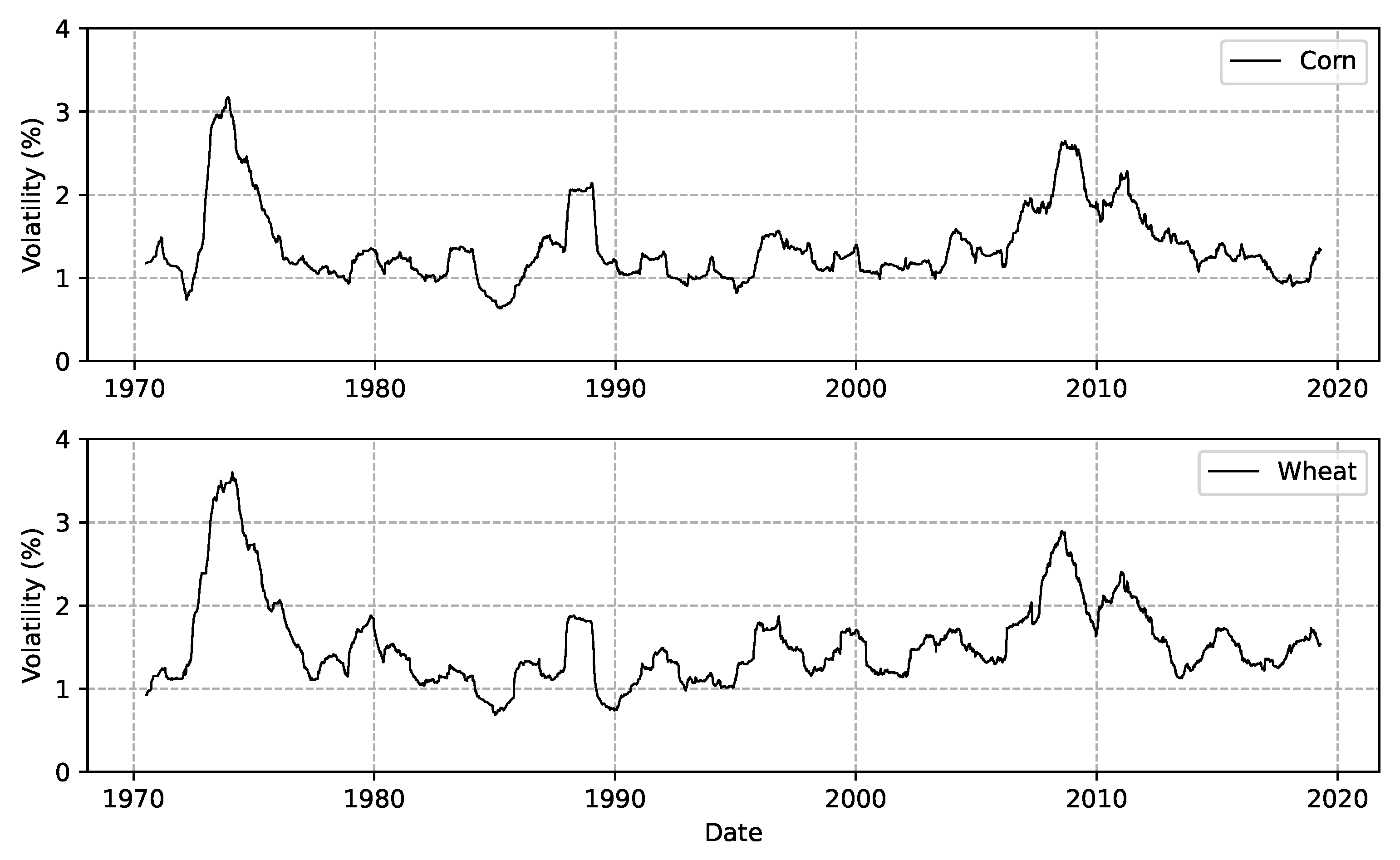

3.2. Prices and Volatility

3.3. Descriptive Statistics

4. Empirical Framework

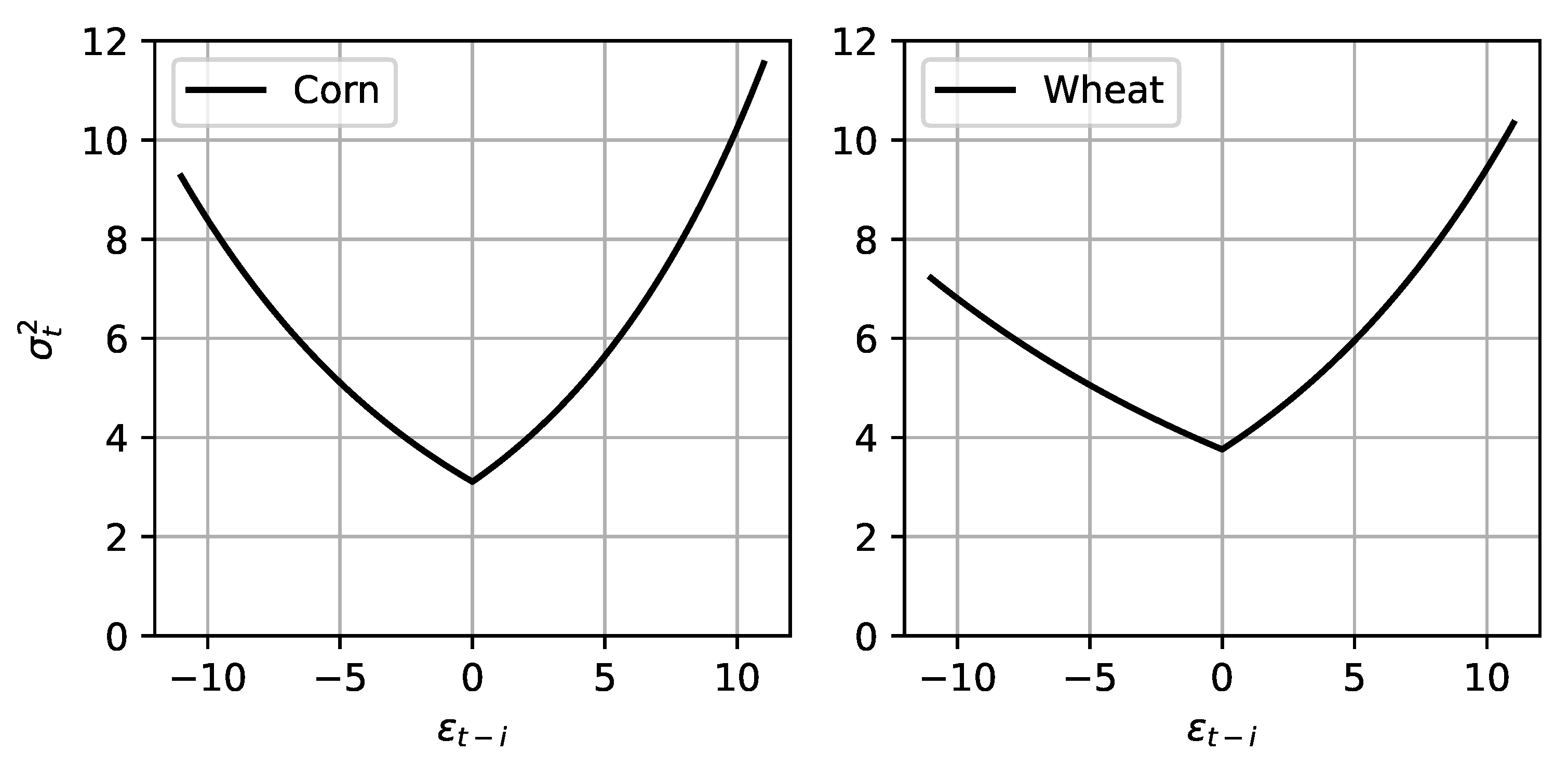

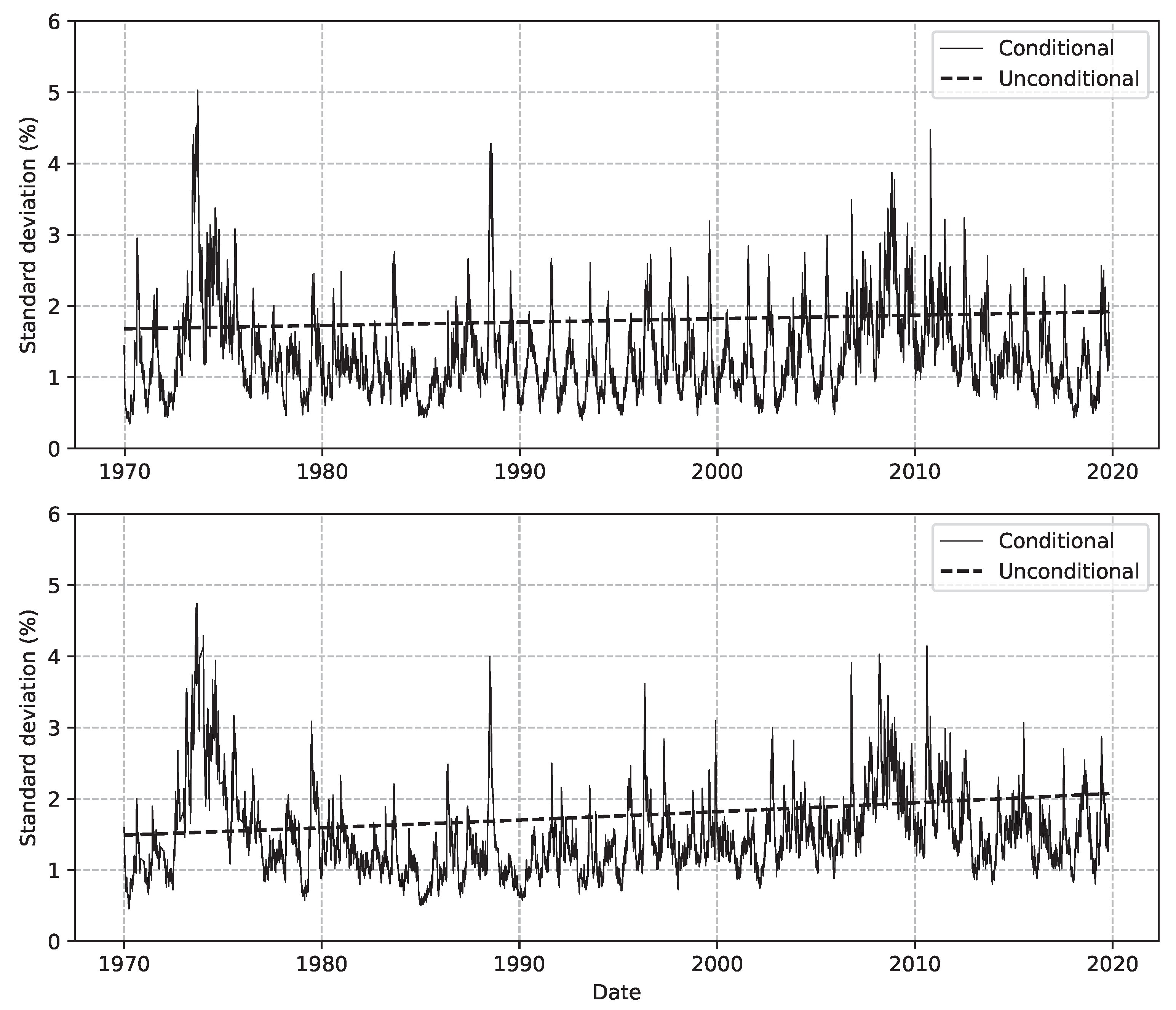

Heterogeneous EGARCH Model

5. Results and Discussion

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- IPCC. Climate Change 2014: Impacts, Adaptation, and Vulnerability. Part A: Global and Sectoral Aspects. Contribution of Working Group II to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change; Cambridge University Press: Cambridge, MA, USA, 2014. [Google Scholar]

- IPCC. Climate Change 2022: Impacts, Adaptation, and Vulnerability. Contribution of Working Group II to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change; Cambridge University Press: Cambridge, MA, USA, 2022. [Google Scholar]

- Kopp, R.E.; Hayhoe, K.; Easterling, D.R.; Hall, T.; Horton, R.; Kunkel, K.E.; LeGrande, A.N. Potential Surprises — Compound Extremes and Tipping Elements. In Climate Science Special Report: Fourth National Climate Assessment; Wuebbles, D.J., Fahey, D.W., Hibbard, K.A., Dokken, D.J., Stewart, B.C., Maycock, T.K., Eds.; U.S. Global Change Research Program: Washington, DC, USA, 2017; Volume I, pp. 411–429. [Google Scholar]

- Tigchelaar, M.; Battisti, D.S.; Naylor, R.L.; Ray, D.K. Future Warming Increases Probability of Globally Synchronized Maize Production Shocks. Proc. Natl. Acad. Sci. USA 2018, 115, 6644–6649. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Ortiz-Bobea, A.; Ault, T.R.; Carrillo, C.M.; Chambers, R.G.; Lobell, D.B. Anthropogenic Climate Change has Slowed Global Agricultural Productivity Growth. Nat. Clim. Chang. 2021, 11, 306–312. [Google Scholar] [CrossRef]

- Hatfield, J.L.; Dold, C. Agroclimatology and Wheat Production: Coping with Climate Change. Front. Plant Sci. 2018, 9, 00224. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Huchet-Bourdon, M. Agricultural Commodity Price Volatility: An Overview; OECD Food, Agriculture and Fisheries Paper 52; OECD: Paris, France, 2011. [Google Scholar]

- Ray, D.K.; Gerber, J.S.; MacDonald, G.K.; West, P.C. Climate Variation Explains a Third of Global Crop Yield Variability. Nat. Commun. 2014, 6, 5989. [Google Scholar] [CrossRef] [Green Version]

- Musunuru, N. Examining Volatility Persistence and News Asymmetry in Soybeans Futures Returns. Atl. Econ. J. 2016, 44, 487–500. [Google Scholar] [CrossRef]

- Gilbert, C.L.; Morgan, C.W. Food Price Volatility. Philos. Trans. R. Soc. B 2010, 365, 3023–3034. [Google Scholar] [CrossRef]

- Balcombe, K. The Nature and Determinants of Volatility in Agricultural Prices. In The Evolving Structure of World Agricultural Trade: Implications for Trade Policy and Trade Agreements; Sarris, A., Morrison, J., Eds.; FAO: Rome, Italy, 2009; pp. 109–136. [Google Scholar]

- Gilbert, C.L.; Mugera, H.K. Food Commodity Prices Volatility: The Role of Biofuels. Nat. Resour. 2014, 5, 200–212. [Google Scholar] [CrossRef] [Green Version]

- Dawson, P.J. Measuring the Volatility of Wheat Futures Prices on the LIFFE. J. Agric. Econ. 2015, 66, 20–35. [Google Scholar] [CrossRef]

- Pindyck, R.S. Volatility in Natural Gas and Oil Markets. J. Energy Dev. 2004, 30, 1–19. [Google Scholar]

- Roll, R. Orange Juice and Weather. Am. Econ. Rev. 1984, 74, 861–880. [Google Scholar]

- Deschênes, O.; Greenstone, M. The Economic Impacts of Climate Change: Evidence from Agricultural Output and Random Fluctuations in Weather. Am. Econ. Rev. 2007, 97, 354–385. [Google Scholar] [CrossRef] [Green Version]

- Fisher, A.C.; Hanemann, W.M.; Roberts, M.J.; Schlenker, W. The Economic Impacts of Climate Change: Evidence from Agricultural Output and Random Fluctuations in Weather: Comment. Am. Econ. Rev. 2012, 102, 3749–3760. [Google Scholar] [CrossRef]

- Schlenker, W.; Roberts, M.J. Nonlinear Temperature Indicates Severe Damages to US Crop Yields Under Climate Change. Proc. Natl. Acad. Sci. USA 2009, 106, 15594–15598. [Google Scholar] [CrossRef] [Green Version]

- Kucharik, C.J.; Serbin, S. Impact of Recent Climate Change on Wisconsin Corn and Soybean Trends. Environ. Res. Lett. 2008, 3, 034003. [Google Scholar] [CrossRef]

- Lobell, D.B.; Field, C.B. Global Scale Climate-Crop Yield Relationships and the Impact of Recent Warming. Environ. Res. Lett. 2007, 2, 011002. [Google Scholar] [CrossRef]

- Schlenker, W.; Hanemann, W.M.; Fisher, A.C. The Impact of Global Warming on U.S. Agriculture: An Econometric Analysis of Optimal Growing Conditions. Rev. Econ. Stat. 2006, 88, 113–125. [Google Scholar] [CrossRef] [Green Version]

- Lobell, D.B.; Hammer, G.L.; McLean, G.; Roberts, M.J.; Schlenker, W. The Critical Role of Extreme Heat for Maize Production in the United States. Nat. Clim. Chang. 2013, 3, 497–501. [Google Scholar] [CrossRef]

- Carter, C.A.; Rausser, G.C.; Smith, A. Commodity Booms and Busts. Annu. Rev. Resour. Econ. 2011, 3, 87–118. [Google Scholar] [CrossRef]

- Engle, R.F. Autoregressive Conditional Heteroscedasticity with Estimates of the Variance of United Kingdom Inflation. Econometrica 1982, 36, 394–419. [Google Scholar] [CrossRef]

- Bollerslev, T. Generalized Autoregressive Conditional Heteroskedasticity. J. Econom. 1986, 31, 307–327. [Google Scholar] [CrossRef] [Green Version]

- Nelson, D.B. Conditional Heteroskedasticity in Asset Returns: A New Approach. Econometrica 1991, 59, 347–370. [Google Scholar] [CrossRef]

- Bollerslev, T. A Conditional Heteroskedastic Time Series Model for Speculative Prices and Rates of Return. Rev. Econ. Stat. 1987, 69, 542–547. [Google Scholar] [CrossRef]

- Engle, R.F.; Ng, V.K. Measuring and Testing the Impact of News on Volatility. J. Financ. 1993, 48, 1749–1778. [Google Scholar] [CrossRef]

- Lybbert, T.; Smith, J.A.; Sumner, D.A. Weather Shocks and Inter-Hemispheric Supply Responses: Implications for Climate Change Effects on Global Food Markets. Clim. Chang. Econ. 2014, 5, 1450010. [Google Scholar] [CrossRef] [Green Version]

- Lange, T.; Rahbek, A. An Introduction to Regime Switching Time Series Models. In Handbook of Financial Time Series; Mikosch, T., Kreiss, J.P., Davis, R.A., Andersen, T.G., Eds.; Springer: New York, NY, USA, 2009; pp. 871–887. [Google Scholar]

- Wright, B.D. The Economics of Grain Price Volatility. Appl. Econ. Perspect. Policy 2011, 33, 32–58. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Corn | Wheat | |||

|---|---|---|---|---|

| Real Price | Change in Price (%) | Real Price | Change in Price (%) | |

| Mean | 301.28 | −0.010 | 416.74 | −0.003 |

| Standard deviation | 115.66 | 1.442 | 159.11 | 1.598 |

| Minimum | 112.63 | −10.069 | 141.37 | −11.081 |

| Median | 267.50 | 0.000 | 373.50 | 0.000 |

| Maximum | 837.50 | 14.122 | 1245.00 | 11.463 |

| Skewness | 0.110 | 0.135 | ||

| Kurtosis (Fisher) | 5.129 | 4.028 | ||

| KPSS-test | 0.14 | 0.25 | ||

| Ljung-Box Q(5) | 23.61 | 82.10 | ||

| ARCH(1) test | 397.99 | 531.23 | ||

| Observations | 12936 | 12658 | ||

| Parameter | Corn | Wheat |

|---|---|---|

| −0.01166 | −0.01127 | |

| (0.00787) | (0.00938) | |

| −0.03164 | −0.06195 | |

| (0.00704) | (0.00863) | |

| −0.03008 | −0.02510 | |

| (0.00956) | (0.00997) | |

| 0.01380 | 0.01011 | |

| (0.00313) | (0.00258) | |

| 0.71 × 10 | 1.71 × 10 | |

| (0.99 × 10) | (0.81 × 10) | |

| 0.98666 | 0.98713 | |

| (0.00181) | (0.00189) | |

| 0.01917 | 0.03370 | |

| (0.00585) | (0.00544) | |

| 0.20943 | 0.15598 | |

| (0.01811) | (0.00979) | |

| f | 6.2966 | 7.4571 |

| (0.3491) | (0.4752) | |

| N | 12,936 | 12,658 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Steen, M.; Bergland, O.; Gjølberg, O. Climate Change and Grain Price Volatility: Empirical Evidence for Corn and Wheat 1971–2019. Commodities 2023, 2, 1-12. https://doi.org/10.3390/commodities2010001

Steen M, Bergland O, Gjølberg O. Climate Change and Grain Price Volatility: Empirical Evidence for Corn and Wheat 1971–2019. Commodities. 2023; 2(1):1-12. https://doi.org/10.3390/commodities2010001

Chicago/Turabian StyleSteen, Marie, Olvar Bergland, and Ole Gjølberg. 2023. "Climate Change and Grain Price Volatility: Empirical Evidence for Corn and Wheat 1971–2019" Commodities 2, no. 1: 1-12. https://doi.org/10.3390/commodities2010001