Theory-Guided Analytics Process: Using Theories to Underpin an Analytics Process for New Banking Product Development Using Segmentation-Based Marketing Analytics Leveraging on Marketing Intelligence

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

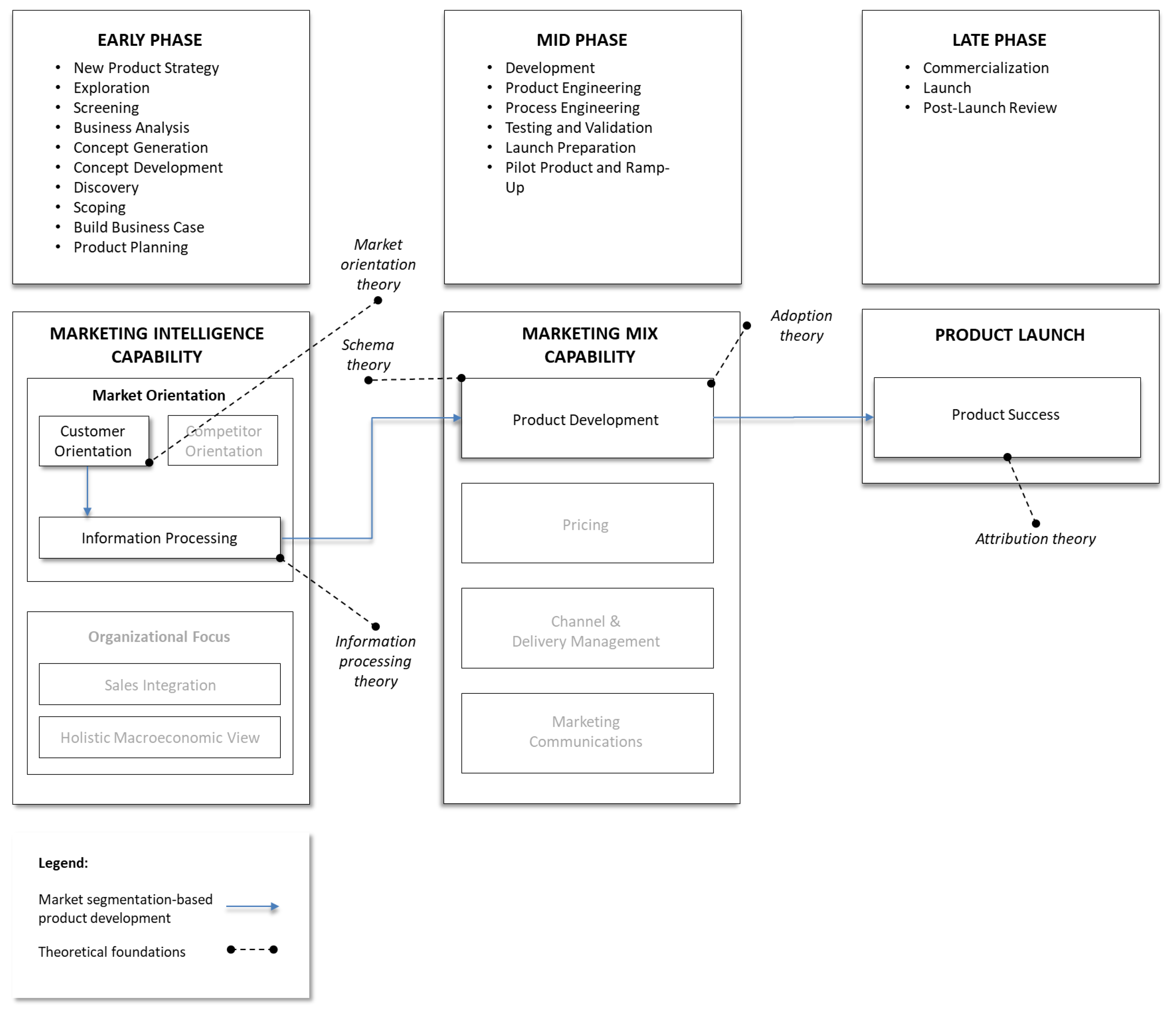

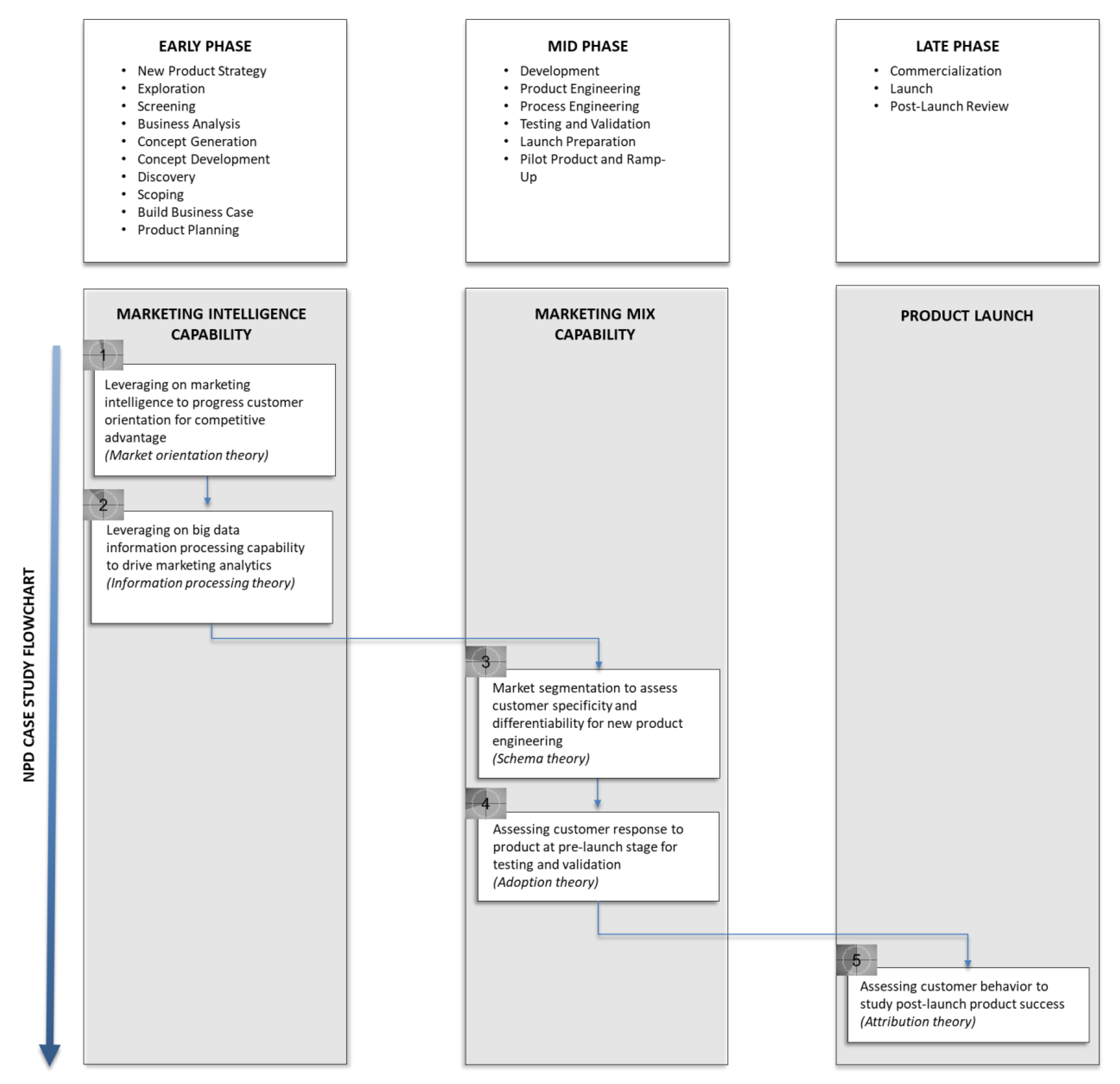

:1. Introduction

2. Theoretical Foundation and Conceptual Framework

2.1. Theoretical Foundation: Marketing Intelligence Underlying Market Segmentation-Based New Product Development

2.2. Conceptual Framework

2.2.1. Early Phase: Leveraging on Marketing Intelligence to Progress Customer Orientation for Competitive Advantage

Theoretical Underpinning: Market Orientation Theory

Empirical Literature

2.2.2. Early Phase: Leveraging on Big Data Information Processing Capability to Drive Marketing Analytics

Theoretical Underpinning: Information Processing Theory

Empirical Literature

2.2.3. Mid Phase: Market Segmentation to Assess Customer Specificity and Differentiability for New Product Engineering

Theoretical Underpinning: Schema Theory

The Empirical Literature

2.2.4. Mid Phase: Assessing Customer Response to Product at Pre-Launch Stage for Testing and Validation

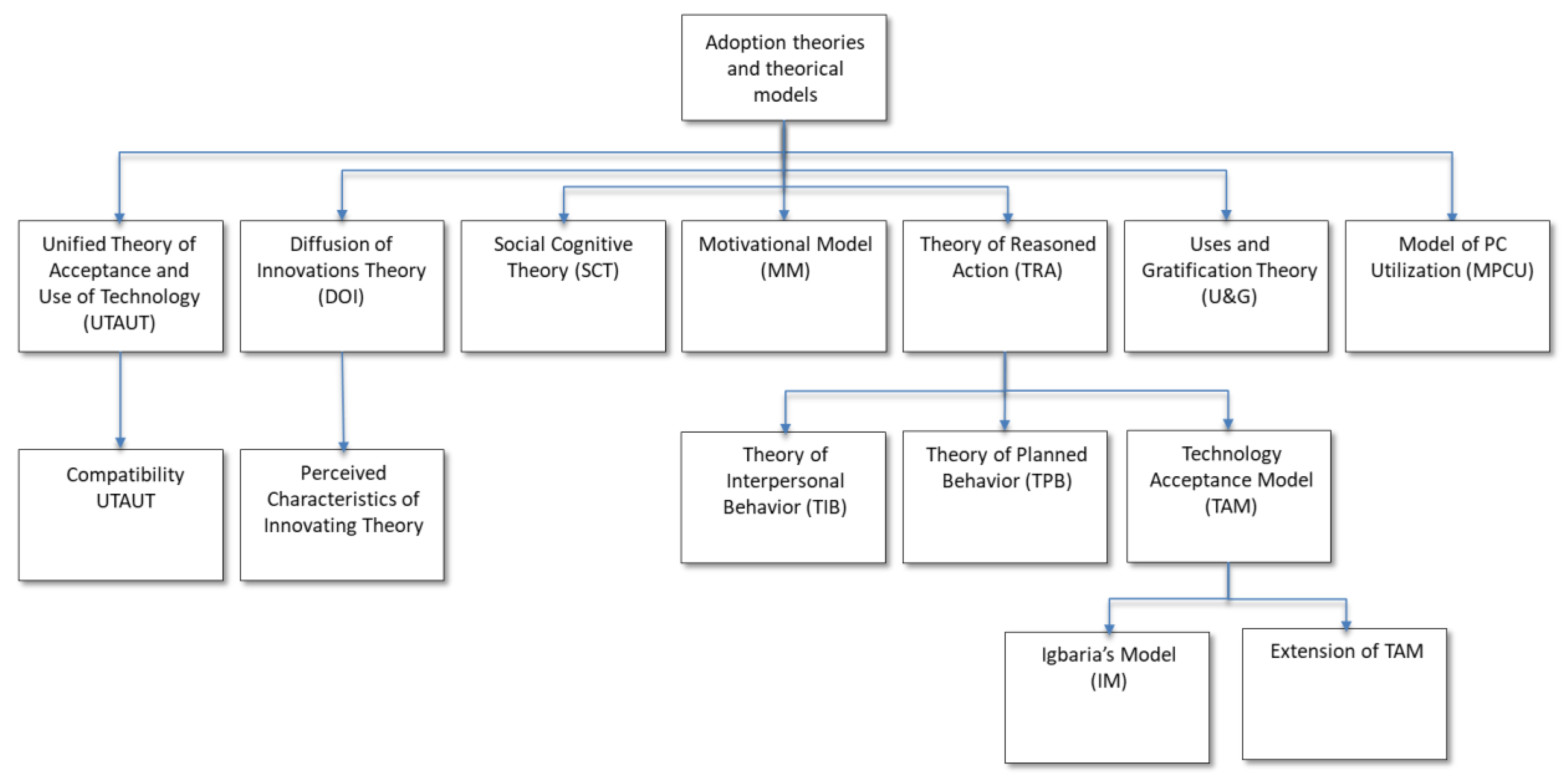

Theoretical Underpinning: Adoption Theory

Empirical Literature

2.2.5. Late Phase: Assessing Customer Behavior to Study Post-Launch Product Success

Theoretical Underpinning: Attribution Theory

Empirical Literature

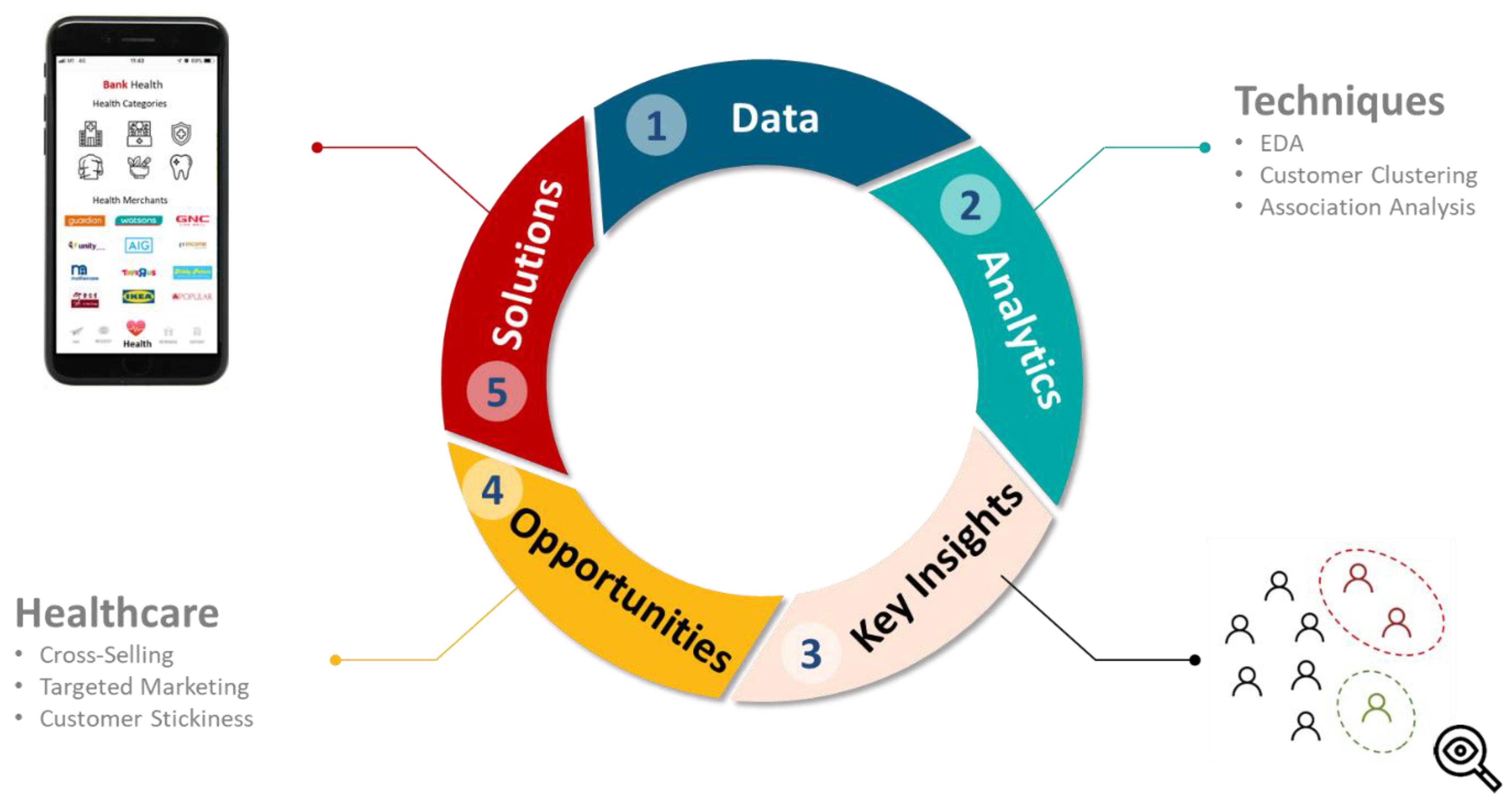

3. Methodology

3.1. Case Study Approach

3.2. Banking Case Event

“Banking industry is highly competitive … we have different customer segments, and these customers have different expectations from the bank.”

4. Case Study

4.1. Early Phase: Leveraging on Marketing Intelligence to Progress Customer Orientation for Competitive Advantage

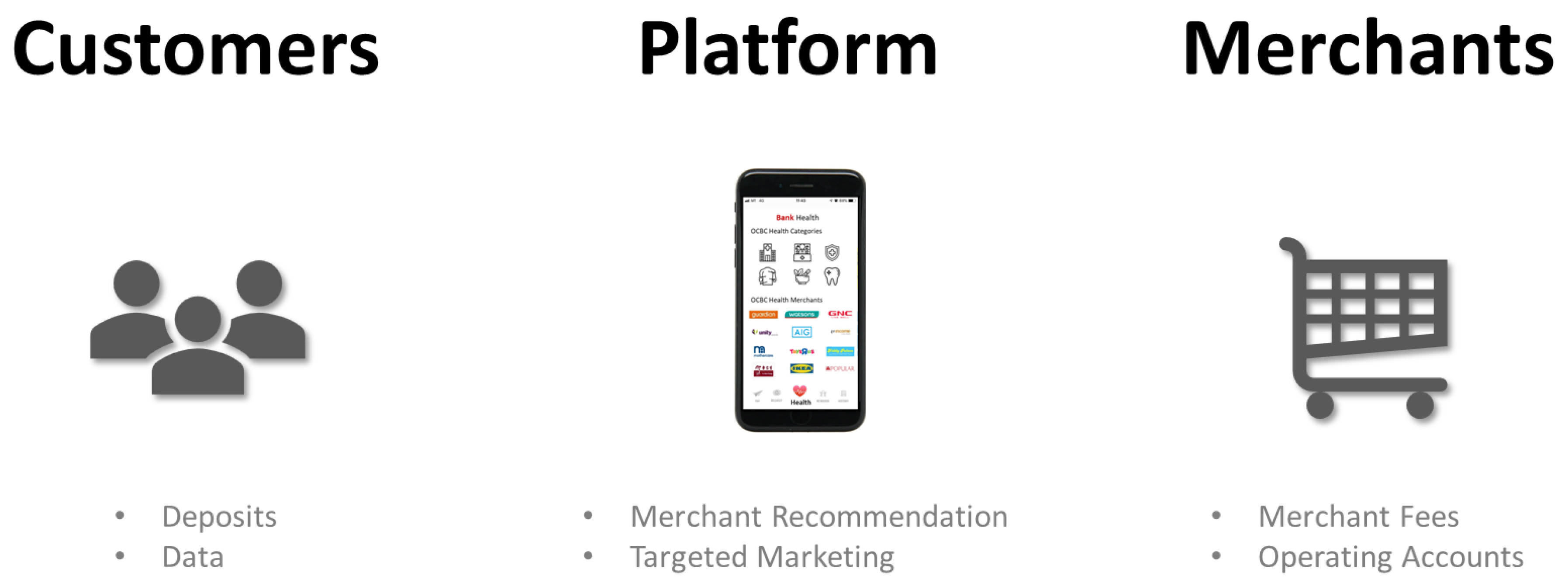

4.1.1. Case Study Bank’s Product Development Stage

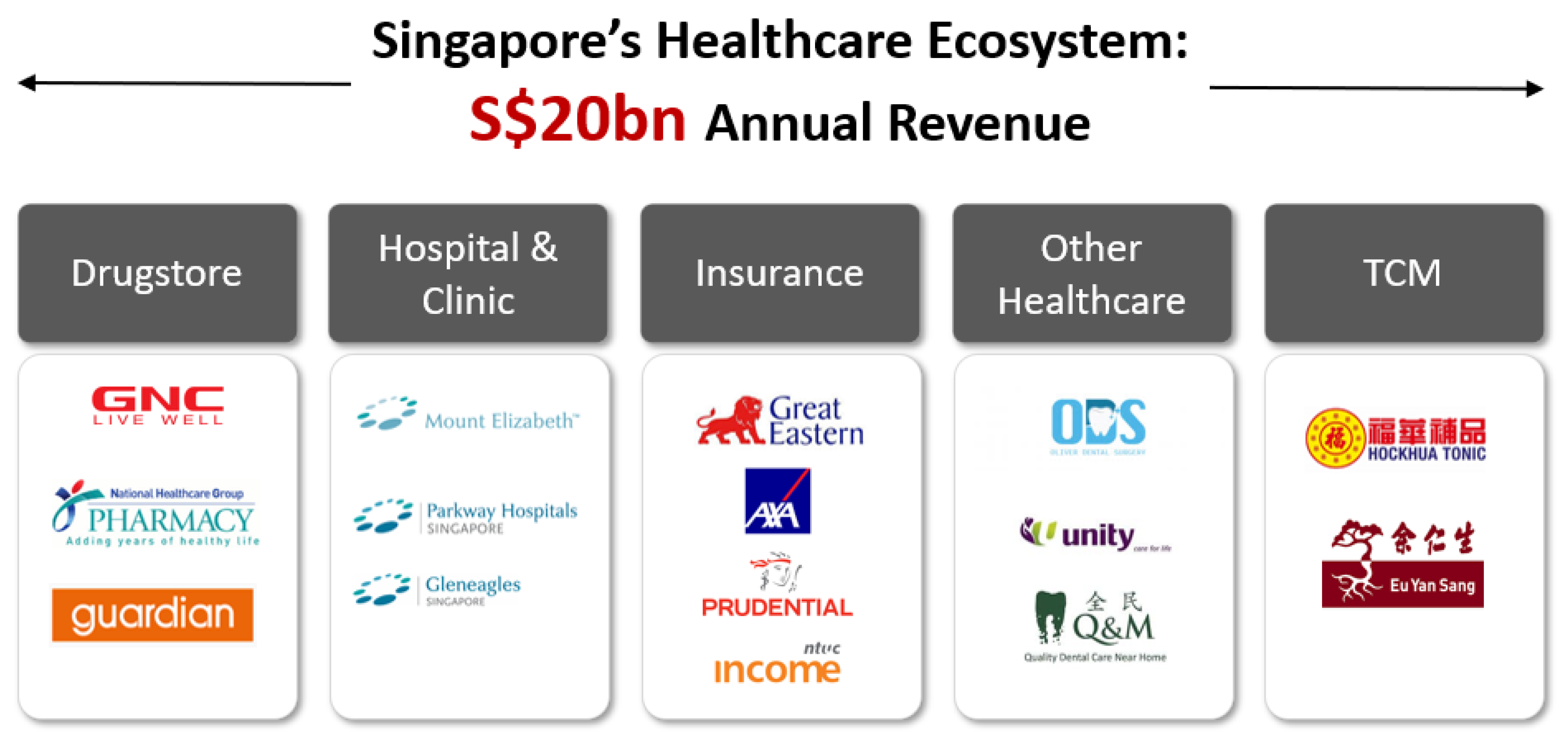

4.1.2. Data Background

4.1.3. Summary of NPD Strategy

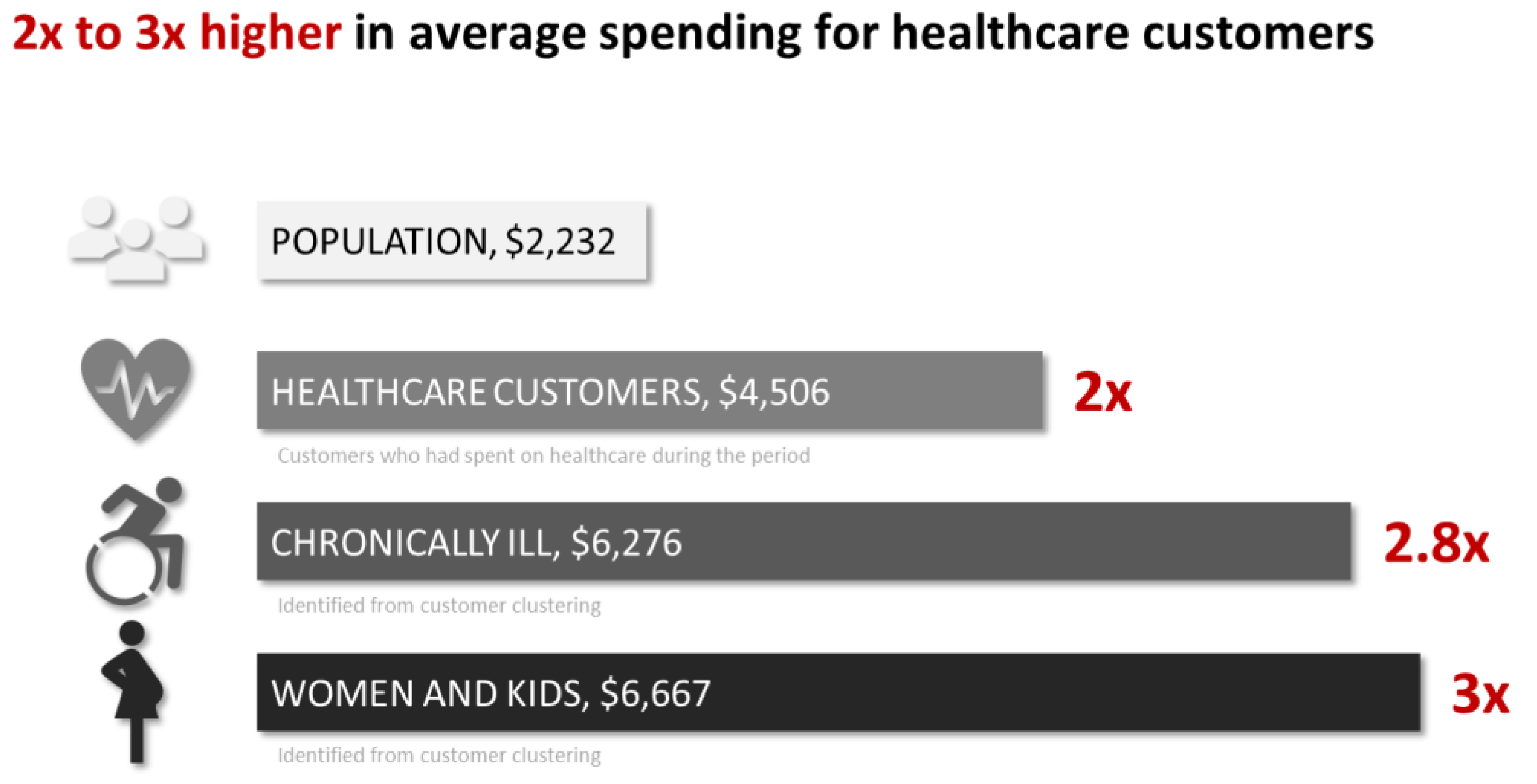

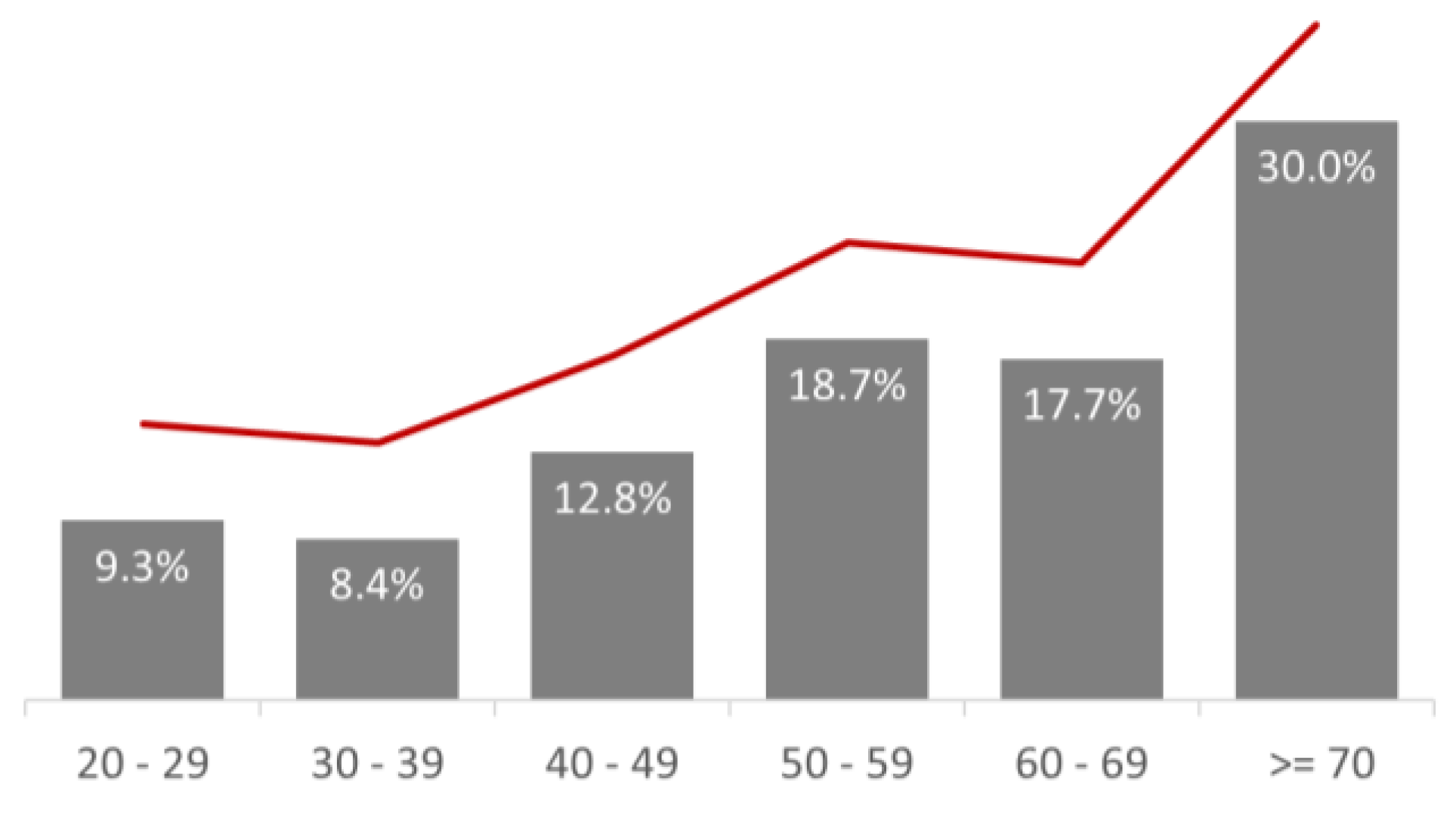

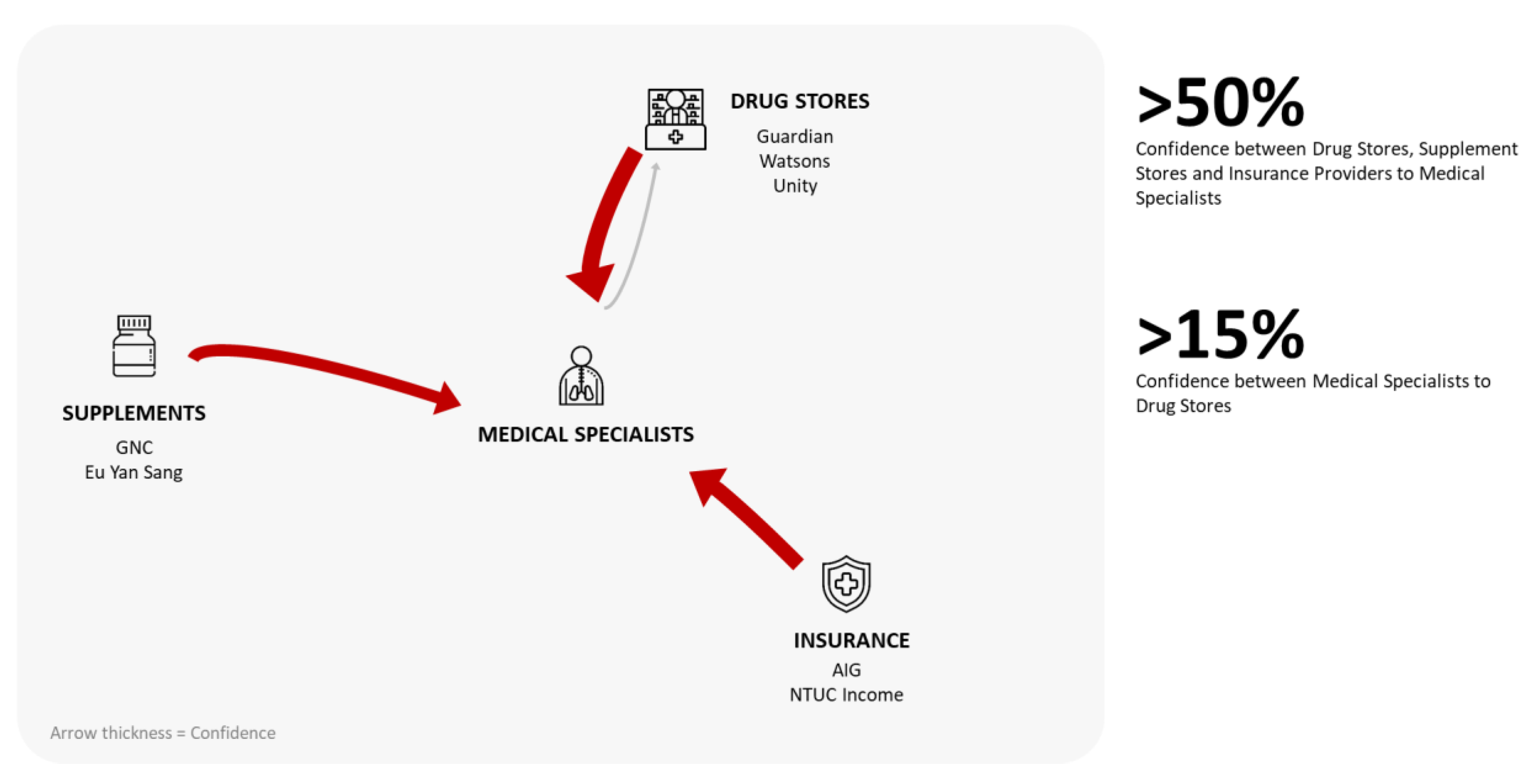

“In fact, customers who had spent in the healthcare sector had spent disproportionately more. This group of customers represented 15% of the sample population, but accounted for 30% of the total transacted amount.”

4.1.4. Application of Underpinning Theory in Banking Case Scenario

4.2. Early Phase: Leveraging on Big Data Information Processing Capability to Drive Marketing Analytics

4.2.1. Case Study Bank’s Product Development Stage

“The positive effect of this dominant and increasing spending pattern on healthcare improved the appetency of exploration on this client segment.”

4.2.2. Application of Underpinning Theory in Banking Case Scenario

4.3. Mid Phase: Market Segmentation to Assess Customer Specificity and Differentiability for New Product Engineering

4.3.1. Case Study Bank’s Product Development Stage

- Age band of the customer

- Credit limit band of the customer

- Gender of the customer

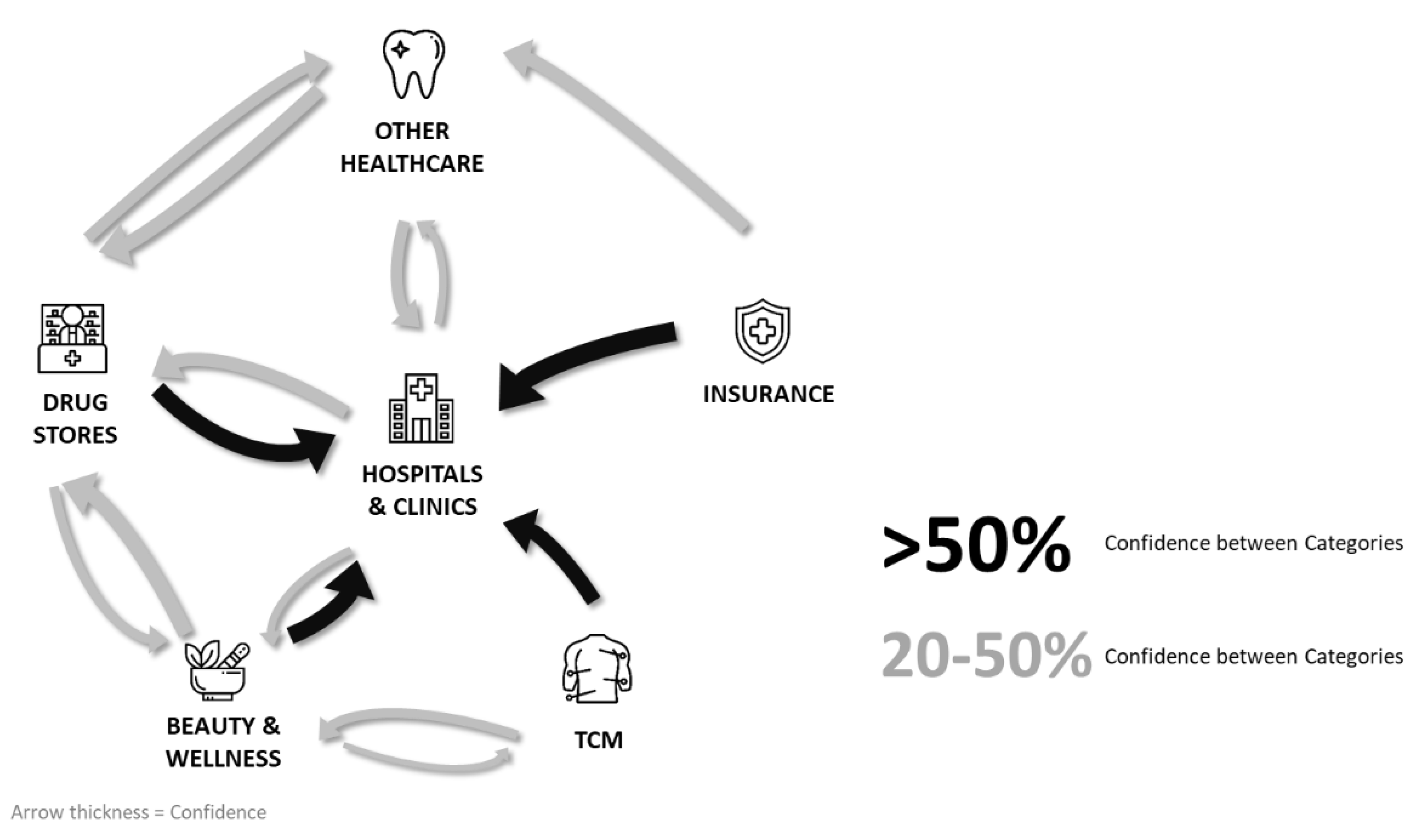

- Frequency of healthcare-related spending by the customer (‘Once’, ‘Infrequent’, ‘Frequent’, where ‘Infrequent’ was defined as two to three times of visit and ‘Frequent’ was defined as more than three times of visit during the quarter under observation)

- Monetary value of healthcare-related spending by the customer (‘Low’, ‘Medium’, ‘High’, where the categorization was based on percentiles)

- Whether the customer had visited medical specialists during the period (‘Yes’, ‘No’)

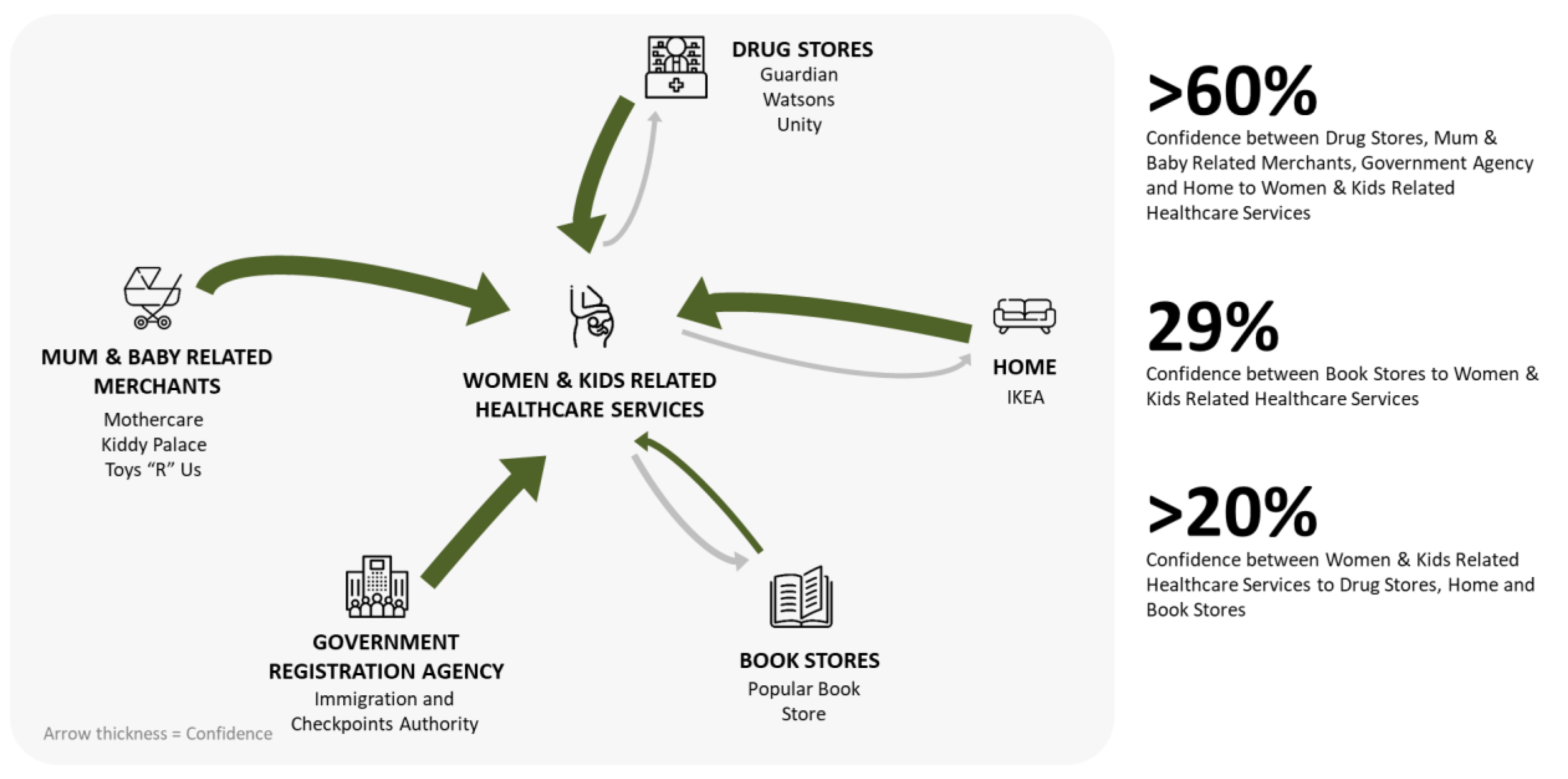

- Whether the customer had visited women and kids-related healthcare services during the period (‘Yes’, ‘No’)

- Whether the customer had spent on insurance during the period (‘Yes’, ‘No’)

- Whether the customer had spent on mum and baby-related merchants, e.g., Mothercare or Kiddy Palace during the period (‘Yes’, ‘No’)

4.3.2. Cluster 1—‘Young Occasional Healthcare Spenders’

4.3.3. Cluster 2—‘Senior Occasional Healthcare Spenders’

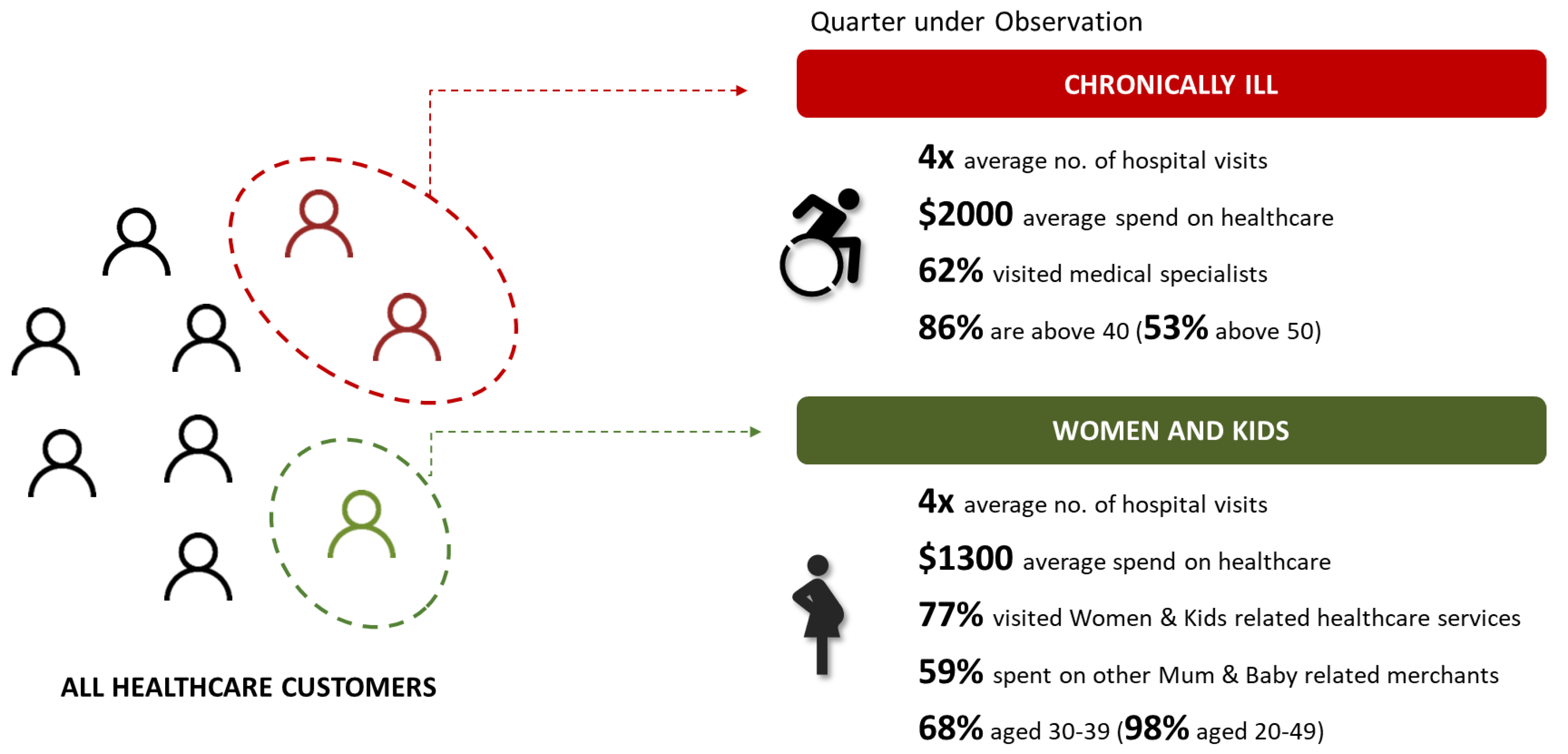

4.3.4. Cluster 3—‘Chronically Ill’

4.3.5. Cluster 4—‘Women and Kids’

4.3.6. Application of Underpinning Theory in Banking Case Scenario

4.4. Mid Phase: Assessing Customer Response to Product at Pre-Launch Stage for Testing and Validation

4.4.1. Case Study Bank’s Product Development Stage

“Data analysis findings suggested that there is a high growth opportunity in the healthcare sector, given its strong associations with customers’ spending and importance to customers’ life goals.”

4.4.2. Application of Underpinning Theory in Banking Case Scenario

4.5. Late Phase: Assessing Customer Behavior to Study Post-Launch Product Success

4.5.1. Case Study Bank’s Product Development

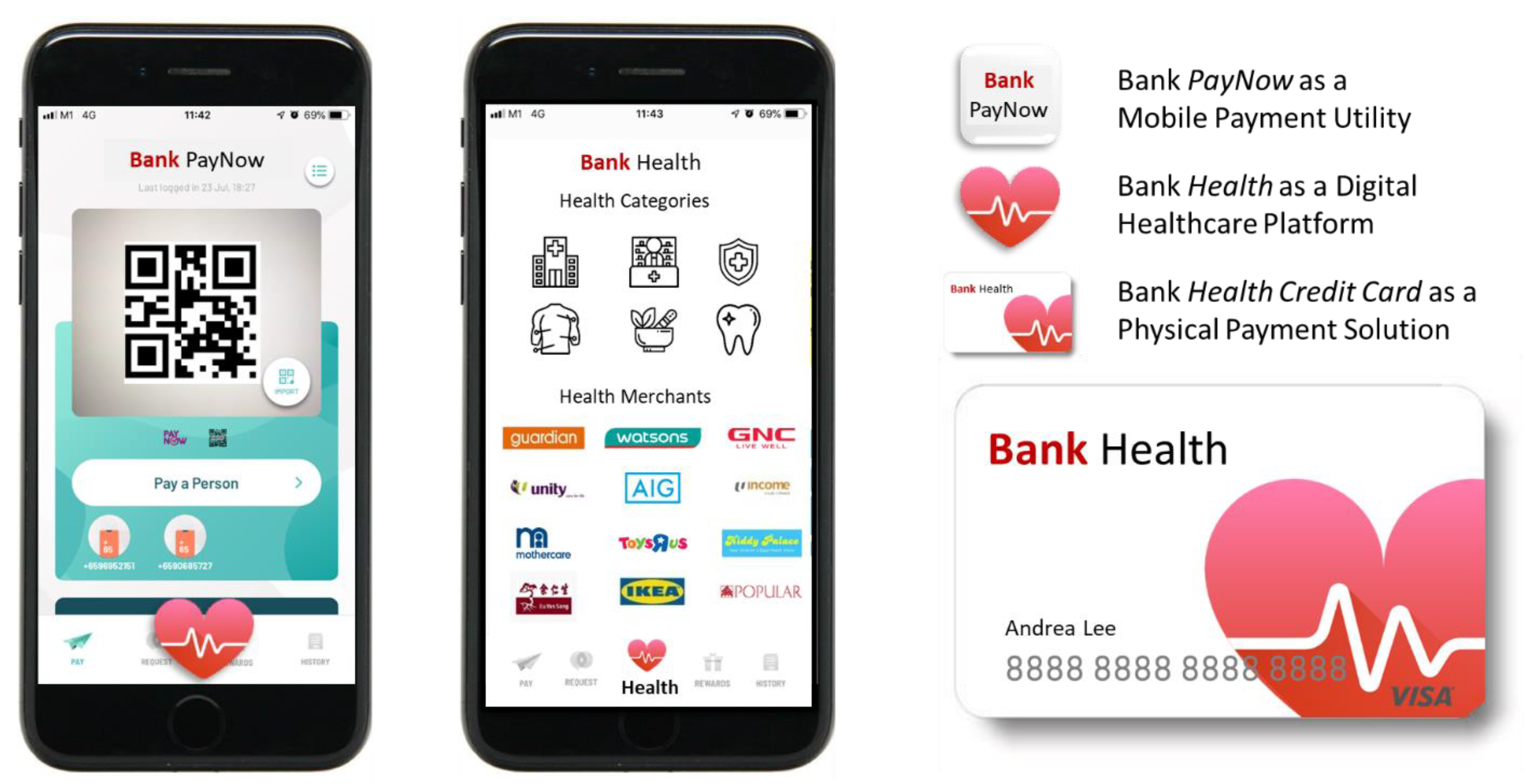

“Health is wealth. We hope the solution can help provide a boost to manage Singapore’s healthcare needs.”

4.5.2. Application of Underpinning Theory in Banking Case Scenario

5. Implications and Limitations

5.1. Theoretical and Practical Implications

5.2. Limitations

- The card transaction data only covered a three-month period and presented a stratified subset of the bank’s total customer base. It might not give a full picture of the bank’s overall business, and might not allow the study of any seasonal patterns, making it difficult to estimate the impact of the proposed solution or project potential revenue growth. For future NPD product strategy analysis, a more comprehensive dataset covering a larger time frame could be utilized.

- Transaction-level data provided merchant-level data, but not any information on the actual products and services purchased. This implied that assumptions had to be made, which might affect the accuracy of customer clustering analysis and profiling. This could potentially be mitigated by collecting more detailed product level data from merchant-level data sharing or new banking product launches that collects granular product level data.

- Segmentation based on historical data might not persist in the future. The most frequent merchants and some association rules could change. For future NPD post-launch analysis, it would be useful to undertake periodic analysis to update changes in customer behavioral patterns.

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Garg, A.; Goldshtein, D.; Kaura, U.; Varadarajan, R. Reinventing Credit Cards: Responses to New Lending Models in the US. McKinsey & Company. 2022. Available online: https://www.mckinsey.com/industries/financial-services/our-insights/reinventing-credit-cards-responses-to-new-lending-models-in-the-us (accessed on 30 November 2022).

- Coyle, K.; Kim, L.; O’Brien, S. 2021 Findings from the Diary of Consumer Payment Choice. U.S. Federal Reserve Cash Product Office. 2021. Available online: https://www.frbsf.org/cash/publications/fed-notes/2021/may/2021-findings-from-the-diary-of-consumer-payment-choice/ (accessed on 30 November 2022).

- Mazanec, J.A. Hidden theorizing in big data analytics: With a reference to tourism design research. Ann. Tour. Res. 2020, 83, 102931. [Google Scholar] [CrossRef]

- Krishnan, V.; Ulrich, K.T. Product development decisions: A review of the literature. Manag. Sci. 2001, 47, 1–12. [Google Scholar] [CrossRef]

- Tan, T.T.W.; Ahmed, Z.U. Managing market intelligence: An Asian marketing research perspective. Mark. Intell. Plan. 1999, 17, 298–306. [Google Scholar] [CrossRef]

- Mkhomazi, S.S.; Iyamu, T. A guide to selecting theory to underpin information systems studies. In International Working Conference on Transfer and Diffusion of IT; Springer: Berlin/Heidelberg, Germany, 2013; pp. 525–537. [Google Scholar]

- Glanz, K. Social and Behavioral Theories. Office of Behavioral and Social Sciences Research (OBSSR), U.S. National Institutes of Health. Available online: https://obssr.od.nih.gov/sites/obssr/files/Social-and-Behavioral-Theories.pdf (accessed on 7 December 2022).

- Frishammar, J. Towards a Theory of Managing Information in New Product Development. Doctoral Dissertation, Luleå University of Technology. 2005. Available online: https://www.diva-portal.org/smash/get/diva2:999487/FULLTEXT01.pdf (accessed on 7 December 2022).

- Helm, R.; Krinner, S.; Endres, H. Exploring the role of product development capability for transforming marketing intelligence into firm performance. J. Bus. Bus. Mark. 2020, 27, 19–40. [Google Scholar] [CrossRef]

- Morgan, N.; Katsikeas, C.; Vorhies, D. Export marketing strategy implementation, export marketing capabilities, and export venture performance. J. Acad. Mark. Sci. 2012, 40, 271–289. [Google Scholar] [CrossRef]

- Sarta, A.; Durand, R.; Vergne, J.P. Organizational adaptation. J. Manag. 2021, 47, 43–75. [Google Scholar] [CrossRef]

- Kohli, A.K.; Jaworski, B.J. Market orientation: The construct, research propositions, and managerial implications. J. Mark. 1990, 54, 1–18. [Google Scholar] [CrossRef]

- Ketchen, D.J.; Hult, G.T.M.; Slater, S.F. Toward greater understanding of market orientation and the resource-based view. Strateg. Manag. J. 2007, 28, 961–964. [Google Scholar] [CrossRef]

- Slater, S.F.; Narver, J.C. Market-oriented is more than being customer-led. Strateg. Manag. J. 1999, 20, 1165–1168. [Google Scholar] [CrossRef]

- Fleisher, C.S.; Blenkhorn, D.L. Controversies in Competitive Intelligence: The Enduring Issues; Praeger: Westport, CT, USA, 2003. [Google Scholar]

- Hunt, S.D.; Morgan, R.M. The comparative advantage theory of competition. J. Mark. 1995, 59, 1–15. [Google Scholar] [CrossRef]

- Kunle AL, P.; Akanbi, A.M.; Ismail, T.A. The influence of marketing intelligence on business competitive advantage (A study of Diamond Bank PLC). J. Compet. 2017, 9, 51–71. [Google Scholar] [CrossRef]

- Taherdoost, H. A review of technology acceptance and adoption models and theories. Procedia Manuf. 2018, 22, 960–967. [Google Scholar] [CrossRef]

- Snead, K.C.; Magal, S.R.; Christensen, L.F.; Ndede-Amadi, A.A. Attribution theory: A theoretical framework for understanding information systems success. Syst. Pract. Action Res. 2015, 28, 273–288. [Google Scholar] [CrossRef]

- McNamara, C.P. The present status of the marketing concept. J. Mark. 1972, 36, 50–57. [Google Scholar] [CrossRef]

- Narver, J.C.; Slater, S.F. The effect of a market orientation on business profitability. J. Mark. 1990, 54, 20–35. [Google Scholar] [CrossRef]

- Walter, J.; Lechner, C.; Kellermanns, F.W. Learning activities, exploration, and the performance of strategic initiatives. J. Manag. 2016, 42, 769–802. [Google Scholar] [CrossRef]

- Li, Q.; Maggitti, P.G.; Smith, K.G.; Tesluk, P.E.; Katila, R. Top management attention to innovation: The role of search selection and intensity in new product introductions. Acad. Manag. J. 2013, 56, 893–916. [Google Scholar] [CrossRef]

- Helfat, C.E.; Peteraf, M.A. Managerial cognitive capabilities and the microfoundations of dynamic capabilities. Strateg. Manag. J. 2015, 36, 831–850. [Google Scholar] [CrossRef]

- Yu, H.; Jin, Y.; Wang, X. Exploratory research on the model of creating market orientation in China’s banks. In Proceedings of the 2010 7th International Conference on Service Systems and Service Management, Tokyo, Japan, 28–30 June 2010; pp. 1–6. [Google Scholar]

- Monferrer Tirado, D.; Moliner Tena, M.Á.; Estrada Guillén, M. Ambidexterity as a key factor in banks’ performance: A marketing approach. J. Mark. Theory Pract. 2019, 27, 227–250. [Google Scholar] [CrossRef]

- Iyer, P.; Davari, A.; Zolfagharian, M.; Paswan, A. Market orientation, positioning strategy and brand performance. Ind. Mark. Manag. 2019, 81, 16–29. [Google Scholar] [CrossRef]

- Galbraith, J.R. Organization design: An information processing view. Interfaces 1974, 4, 28–36. [Google Scholar] [CrossRef]

- Song, M.; Zhang, H.; Heng, J. Creating sustainable innovativeness through big data and big data analytics capability: From the perspective of the information processing theory. Sustainability 2020, 12, 1984. [Google Scholar] [CrossRef]

- Helm, R.; Krinner, S.; Schmalfuß, M. Conceptualization and Integration of Marketing Intelligence: The Case of an Industrial Manufacturer. J. Bus. Bus. Mark. 2014, 21, 237–255. [Google Scholar] [CrossRef]

- Egelhoff, W.G. Information-processing theory and the multinational enterprise. J. Int. Bus. Stud. 1991, 22, 341–368. [Google Scholar] [CrossRef]

- Rogers, P.R.; Miller, A.; Judge, W.Q. Using information-processing theory to understand planning/performance relationships in the context of strategy. Strateg. Manag. J. 1999, 20, 567–577. [Google Scholar] [CrossRef]

- Isik, Ö. Big data capabilities: An organizational information processing perspective. In Analytics and Data Science; Springer: Cham, Switzerland, 2018; pp. 29–40. [Google Scholar]

- Arbib, M.A. Schema theory. Encycl. Artif. Intell. 1992, 2, 1427–1443. [Google Scholar]

- Corbacho, F.J.; Arbib, M.A. Schema-based learning: Biologically inspired principles of dynamic organization. In International Work-Conference on Artificial Neural Networks; Springer: Berlin/Heidelberg, Germany, 1997; pp. 678–687. [Google Scholar]

- Tsoukas, H.; Vladimirou, E. What is organizational knowledge? J. Manag. Stud. 2001, 38, 973–993. [Google Scholar] [CrossRef]

- Yoseph, F.; Malim, N.H.A.H.; AlMalaily, M. New behavioral segmentation methods to understand consumers in retail industry. Int. J. Comput. Sci. Inf. Technol. 2019, 11, 43–61. [Google Scholar] [CrossRef]

- France, S.L.; Ghose, S. Marketing analytics: Methods, practice, implementation, and links to other fields. Expert Syst. Appl. 2019, 119, 456–475. [Google Scholar] [CrossRef]

- Kotler, P.T.; Keller, K.L. Marketing Management, 15th ed.; Pearson: Hoboken, NJ, USA, 2015. [Google Scholar]

- Häfner, N.; Burkhard, B.; Bettis, R.A.; Piezunka, H.; Posen, H.E.; Puranam, P.; Raisch, S.; Teodoridis, F. The Nexus Between Artificial Intelligence and the Behavioral Theory of the Firm. Panel Symposium. 2020. Available online: https://www.alexandria.unisg.ch/260216/1/AI%20and%20BTF%202020%20AOM%20Panel%20Symposium.pdf (accessed on 7 December 2022).

- Puranam, P. Human–AI collaborative decision-making as an organization design problem. J. Organ. Des. 2021, 10, 75–80. [Google Scholar]

- Raisch, S.; Krakowski, S. Artificial intelligence and management: The automation–augmentation paradox. Acad. Manag. Rev. 2021, 46, 192–210. [Google Scholar] [CrossRef]

- Umuhoza, E.; Ntirushwamaboko, D.; Awuah, J.; Birir, B. Using unsupervised machine learning techniques for behavioral-based credit card users segmentation in Africa. SAIEE Afr. Res. J. 2020, 111, 95–101. [Google Scholar] [CrossRef]

- Hung, P.D.; Lien, N.T.T.; Ngoc, N.D. Customer segmentation using hierarchical agglomerative clustering. In Proceedings of the 2019 2nd International Conference on Information Science and Systems; Association for Computing Machinery: New York, NY, USA, 2019; pp. 33–37. [Google Scholar]

- Wang, J.J.; Qian, T.Y.; Li, B.; Mastromartino, B. Reversing equity transfer in sponsorship for competitive advantage of emerging local events: Quantitative evidence from an experimental study. Int. J. Sport. Mark. Spons. 2022, 23, 748–766. [Google Scholar] [CrossRef]

- Gong, X.; Zhang, K.Z.; Zhao, S.J. Halo Effect on the Adoption of Mobile Payment: A Schema Theory Perspective. In International Conference on E-Technologies; Springer: Cham, Switzerland, 2015; pp. 153–165. [Google Scholar]

- Simon, B. Wissensmedien im Bildungssektor. Eine Akzeptanzuntersuchung an Hochschulen (Knowledge Media in the Education System: Acceptance Research in Universities); WU Vienna University of Economics and Business: Wien, Austria, 2001; p. 179. [Google Scholar]

- Motiwalla, L.; Albashrawi, M.; Kartal, H. Understanding Mobile Banking Success through User Segmentation. In Proceedings of the 51st Hawaii International Conference on System Sciences, Hilton Waikoloa Village, HI, USA, 3–6 January 2018; pp. 882–891. [Google Scholar] [CrossRef]

- Shaikh, A.A.; Karjaluoto, H. Mobile banking adoption: A literature review. Telemat. Inform. 2015, 32, 129–142. [Google Scholar] [CrossRef]

- Martins, C.; Oliveira, T.; Popovič, A. Understanding the Internet banking adoption: A unified theory of acceptance and use of technology and perceived risk application. Int. J. Inf. Manag. 2014, 34, 1–13. [Google Scholar] [CrossRef]

- Jamshidi, D.; Hussin, N. An integrated adoption model for Islamic credit card: PLS-SEM based approach. J. Islam. Account. Bus. Res. 2018, 9, 308–335. [Google Scholar] [CrossRef]

- Hsieh, S.T. From attribution theory and IS success aspects, examining how and why nostalgia affects the introduction of a new IT system. J. Internet Technol. 2019, 20, 1961–1971. [Google Scholar]

- Heinemann, K.; Zwergel, B.; Gold, S.; Seuring, S.; Klein, C. Exploring the Supply-Demand-Discrepancy of Sustainable Financial Products in Germany from a Financial Advisor’s Point of View. Sustainability 2018, 10, 944. [Google Scholar] [CrossRef]

- Srivastava, M.; Gosain, A. Impact of service failure attributions on dissatisfaction: Revisiting attribution theory. J. Manag. Res. 2020, 20, 99–112. [Google Scholar]

- Puspitasari, C.; Jayanto, P.Y. The influence of selling price pricing, margin level, product quality, shariah marketing, collateral, product knowledge and risk on member’s interest in using murabahah financing. Account. Anal. J. 2016, 5, 229–237. [Google Scholar]

- Crowe, S.; Cresswell, K.; Robertson, A.; Huby, G.; Avery, A.; Sheikh, A. The case study approach. BMC Med. Res. Methodol. 2011, 11, 100. [Google Scholar] [CrossRef]

- Levy, J.S. Case studies: Types, designs, and logics of inference. Confl. Manag. Peace Sci. 2008, 25, 1–18. [Google Scholar] [CrossRef]

- George, A.L.; Bennett, A. Case Studies and Theory Development in the Social Sciences; MIT Press: Cambridge, MA, USA, 2005. [Google Scholar]

- Levy, J.S. Explaining events and testing theories: History, political science, and the analysis of international relations. In Bridges and Boundaries; Elman, C., Elman, M.F., Eds.; MIT Press: Cambridge, MA, USA, 2001; pp. 39–83. [Google Scholar]

- Porter, M.E. Competitive Strategy: Techniques for Analyzing Industries and Competitors; Free Press: New York, NY, USA, 1980. [Google Scholar]

- Department of Statistics Singapore. Key Indicators of the Household Expenditure Survey, 2002/3–2012/3, Singapore. 2019. Available online: https://www.singstat.gov.sg/-/media/files/find_data/population/statistical_tables/hes-key-indicators.pdf (accessed on 30 November 2022).

- Business Times. Singapore Budget 2018 Addresses Healthcare Needs but Costs Remain a Challenge. 2018. Available online: https://www.businesstimes.com.sg/opinion/singapore-budget-addresses-healthcare-needs-but-costs-remain-a-challenge (accessed on 30 November 2022).

- Yahoo News Singapore. Singaporeans Unprepared on Rising Medical Costs of Living to 100: Healthcare Survey. 2019. Available online: https://sg.news.yahoo.com/singaporeans-unprepared-on-rising-medical-costs-of-living-to-100-healthcare-survey-072434720.html (accessed on 7 December 2022).

- Delen, D.; Zolbanin, H.M. The analytics paradigm in business research. J. Bus. Res. 2018, 90, 186–195. [Google Scholar] [CrossRef]

- Immigration and Checkpoints Authority (ICA). Registration and Collection of Birth Certificate. 2022. Available online: https://www.ica.gov.sg/citizen/birth/citizen_birth_register (accessed on 7 December 2022).

- Gharaibeh, M.K.; Arshad, M.R.M.; Gharaibh, N.K. Using the UTAUT2 model to determine factors affecting adoption of mobile banking services: A qualitative approach. Int. J. Interact. Mob. Technol. 2018, 12, 123–134. [Google Scholar] [CrossRef] [Green Version]

- Tobbin, P. Towards a model of adoption in mobile banking by the unbanked: A qualitative study. Info 2012, 14, 74–88. [Google Scholar] [CrossRef]

- Souiden, N.; Ladhari, R.; Chaouali, W. Mobile banking adoption: A systematic review. Int. J. Bank Mark. 2021, 39, 214–241. [Google Scholar] [CrossRef]

- Kolodner, J.L. An introduction to case-based reasoning. Artif. Intell. Rev. 1992, 6, 3–34. [Google Scholar] [CrossRef]

- Felcman, M. Reflections on the market-oriented theory in the behaviour of real organization. Atl. Mark. J. 2012, 1, 4. [Google Scholar]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lim, T.; Pan, T.; Ong, C.S.; Chen, S.; Chia, J.J.J. Theory-Guided Analytics Process: Using Theories to Underpin an Analytics Process for New Banking Product Development Using Segmentation-Based Marketing Analytics Leveraging on Marketing Intelligence. Analytics 2023, 2, 105-131. https://doi.org/10.3390/analytics2010007

Lim T, Pan T, Ong CS, Chen S, Chia JJJ. Theory-Guided Analytics Process: Using Theories to Underpin an Analytics Process for New Banking Product Development Using Segmentation-Based Marketing Analytics Leveraging on Marketing Intelligence. Analytics. 2023; 2(1):105-131. https://doi.org/10.3390/analytics2010007

Chicago/Turabian StyleLim, Tristan, Tao Pan, Chin Sin Ong, Shuaiwei Chen, and Jie Jun Jeremy Chia. 2023. "Theory-Guided Analytics Process: Using Theories to Underpin an Analytics Process for New Banking Product Development Using Segmentation-Based Marketing Analytics Leveraging on Marketing Intelligence" Analytics 2, no. 1: 105-131. https://doi.org/10.3390/analytics2010007