Recent Trends in Accounting and Information System Research: A Literature Review Using Textual Analysis Tools

Abstract

:1. Introduction

2. Literature Analysis

2.1. Materials and Methods

- (i)

- The identification of the most frequent terms, which includes the presentation of illustrative word clouds;

- (ii)

- The main set of topics and subtopics from the papers gathered, which includes a complementary diagram of a cluster analysis.

2.2. Results

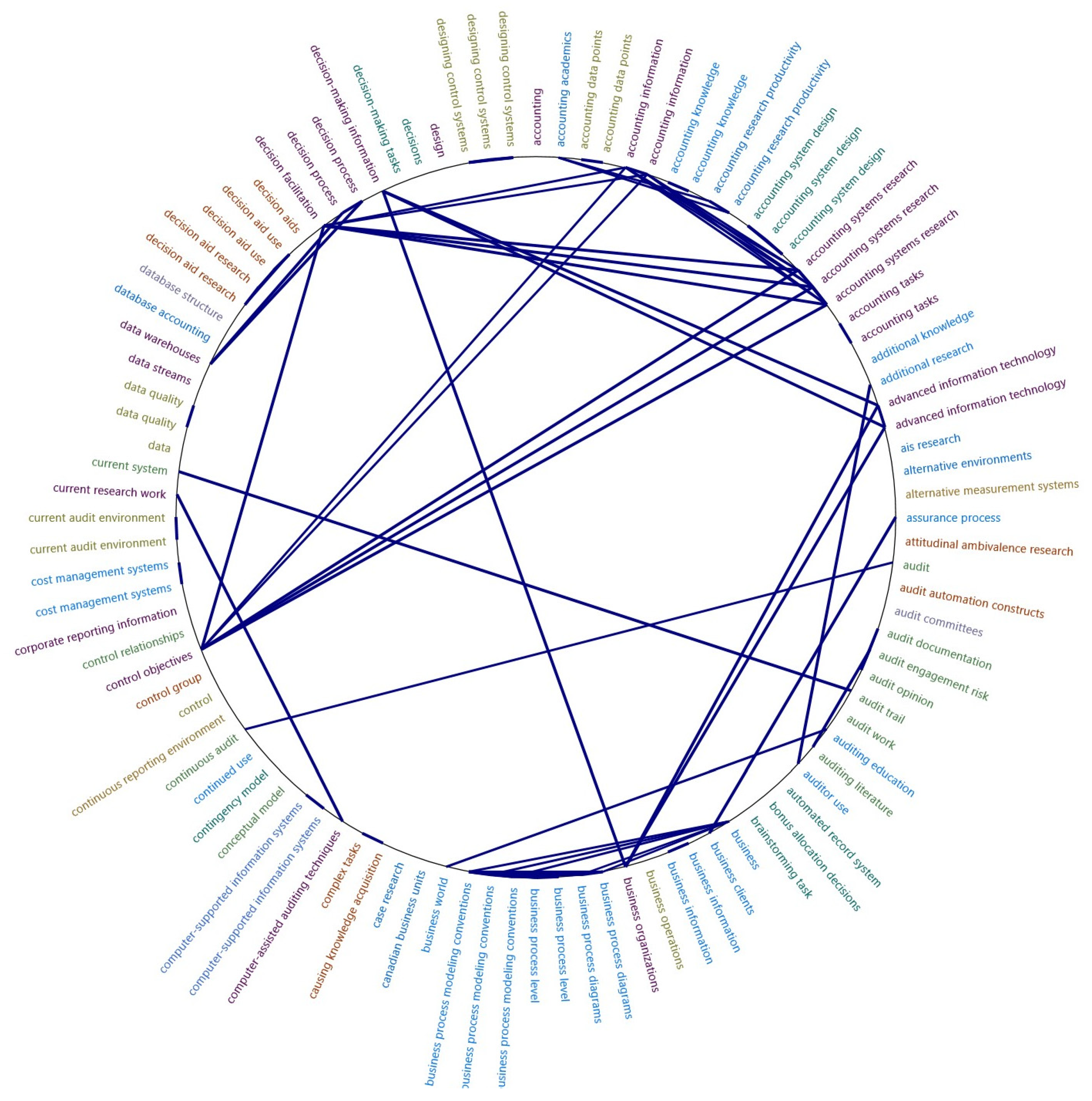

2.2.1. Results for the First Period (2000 to 2009)

- The implementation of internal control system models in the IT area, such as control objectives for information and related technology (COBIT), the relevance of IT certification, such as WebTrust, and also the topics from the Information Systems Audit and Control Association (ISACA) curricula (for instance, [54,55,56]);

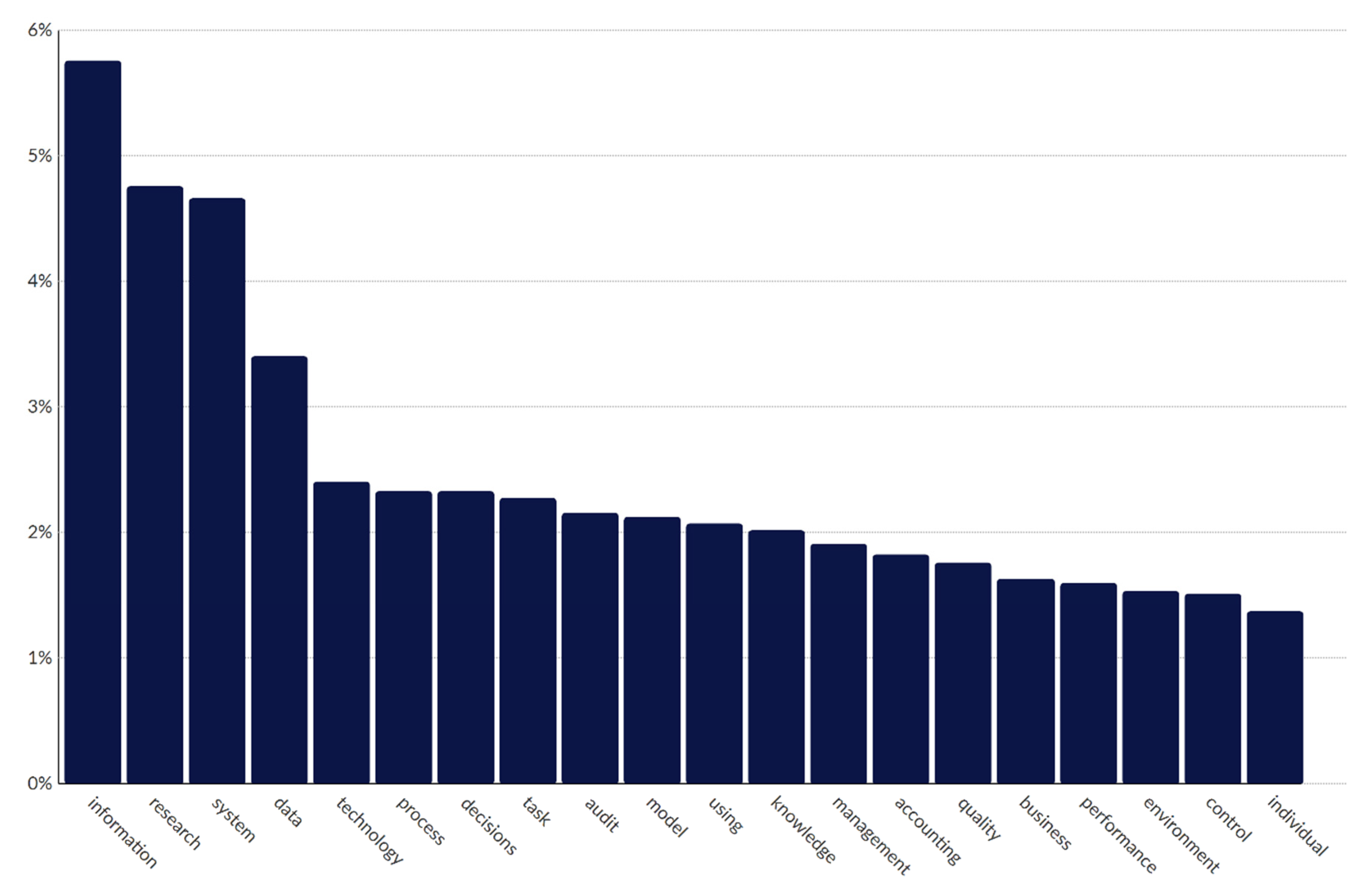

- Accounting: accounting academics, accounting data points, accounting information, accounting knowledge, accounting research productivity, accounting system design, accounting systems research, accounting tasks, database accounting, differentiating accounting systems, financial accounting literature, leading accounting, managerial accounting perspective, quality accounting publication;

- Audit: audit automation constructs, audit committees, audit documentation, audit engagement risk, audit opinion, audit trail, audit work, auditing education, auditing literature, computer-assisted auditing techniques, continuous audit, current audit environment, specific auditing concerns, various audit domains;

- Business: business clients, business information, business operations, business organizations, business process diagrams, business process level, business process modelling conventions, business world, Canadian business units, everyday business communications, extensible business, strategic business planning, web-based business;

- Control: control group, control objectives, control relationships, designing control systems, external controls, hierarchical control structures, informal controls, internal control, international control guideline, proper control procedures, using control charts;

- Data: accounting data points, data quality, data streams, data warehouses, electronic data interchange, financial data, including data flow diagrams, normal form data structure, numerical data increases, secondary data analysis, site data, specific data, spending data, underlying data trends, unnormalized data structure, using data;

- Decisions: bonus allocation decisions, decision aid research, decision aid use, decision aids, decision facilitation, decision process, investment decisions, management decision models, multiple decision, novice decision makers, operational decisions, repetitive choice decisions, repetitive valuation decisions, user decisions;

- Environment: alternative environments, continuous reporting environment, current audit environment, external environment, manufacturing environments, traditional reporting environment, virtual team environment;

- Individual: individual characteristics, individual decision-makers, individual determinants, individual faculty members, individual faculty productivity, individual level, individual provider attributes, individual units, judging individuals, perceiving individuals;

- Information: accounting information, advanced information technology, business information, computer-supported information systems, corporate reporting information, decision-making information, emerging information needs, emerging information technologies, financial reporting information, financial statement information, future-oriented information, human information processing, important information processing mechanism, information age, information content, information integrity attributes, information load, information location, information requests, information security, information system designs, information systems research, informationally equivalent, inter-organizational information sharing, low information quality seal, management information systems, management information value chain, nonfinancial information, online information, open information sharing, output information, preliminary information, specific information technology, supporting information technology, varied information, vast information source;

- Knowledge: accounting knowledge, additional knowledge, causing knowledge acquisition, expert-like knowledge structures, feedback impacts knowledge acquisition, filtering knowledge, improving knowledge workers, knowledge management focus, knowledge management practices, knowledge management system, procedural knowledge;

- Management: cost management systems, effective management, hybrid manager profile, impression management, knowledge management focus, knowledge management practices, knowledge management system, management decision models, management information systems, management information value chain, senior managers, top management support;

- Model: business process modelling conventions, conceptual model, contingency model, enterprise modelling, er model, management decision models, mathematical model, research model, residual income valuation model, task circumplex model, theoretical model;

- Performance: firm performance, managerial end-user performance, organisational performance, organizational performance, performance evaluation, performance outcomes, subsequent decision-making performance, superior performance, task performance, traditional performance measures;

- Process: assurance process, business process diagrams, business process level, business process modeling conventions, decision process, event process chains, extensive sample selection process, human information processing, important information processing mechanism, little processing, process level risk assessment, processing view, production processes, stable processes, standard development process;

- Quality: data quality, disseminating quality, low information quality seal, quality accounting publication, quality measurement component, quality outlets, quality perspective, service quality, system quality;

- Research: accounting research productivity, accounting systems research, additional research, ais research, attitudinal ambivalence research, case research, current research work, decision aid research, development research, empirical research, field research, future research, information systems research, little research, past research, previous research, prior research, recent research, research community, research domain, research findings, research hypotheses, research instrument, research issues, research method opportunities, research model, research propositions, research prototype system, research questions, research survey, rich research opportunities, various research methods;

- System: accounting system design, accounting systems research, alternative measurement systems, automated record system, computer-supported information systems, cost management systems, current system, designing control systems, differentiating accounting systems, electronic audit-work paper system, enterprise systems implementation, expert system groups, expert system types, expert system users, information system designs, information systems research, key system components, knowledge management system, management information systems, medical record system, research prototype system, successful system, system acceptance, system acquisition, system design alternatives, system effectiveness, system implementation changes, system integration, system outputs, system quality, system transformation, system usage, systems design scenarios, tertiary assurance system, work systems;

- Task: accounting tasks, brainstorming tasks, complex tasks, decision-making tasks, financial tasks, optimisation tasks, querying tasks, simple tasks, specific design tasks, task accuracy, task characteristics, task circumplex model, task completion, task force, task performance, task requirements, task routineness;

- Technology: advanced information technology, emerging information technologies, emerging technologies, learning technology, specific information technology, supporting information technology, technological advances, technological determinism, technological discourse, technology complexities, technology features, technology fit, technology medium;

- Use: auditor use, continued use, decision aid use, expert system users, user acceptance, user decisions, user requests, user satisfaction, using activity, using control charts, using data, using eighty-nine, using paper methods.

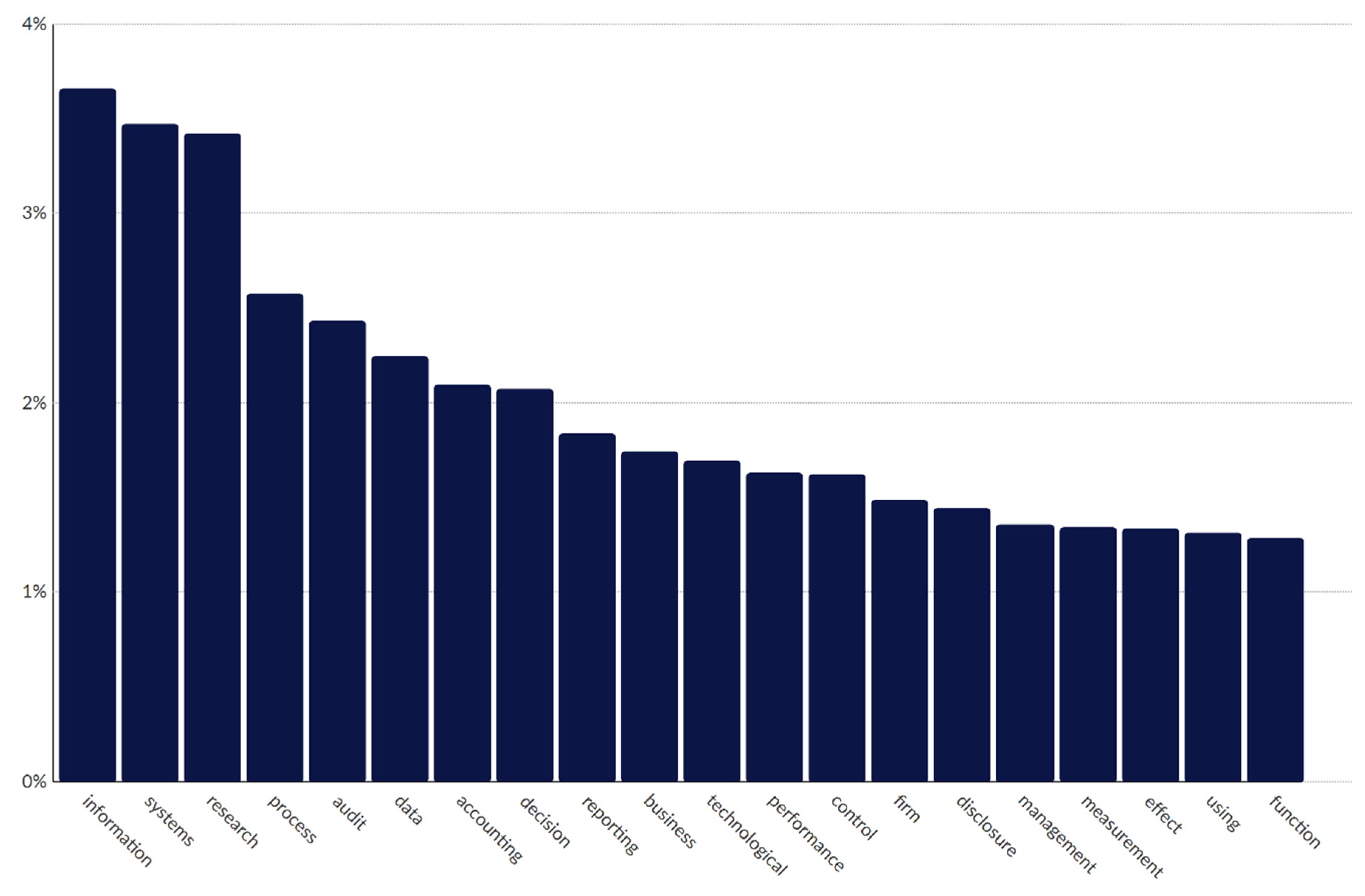

2.2.2. Results for the Second Period (2010 to 2019)

- Artificial intelligence, data analytics, big data treatment, and the use of machine learning and data mining techniques (mostly), which are sometimes associated with previous themes and, in many cases, dedicated to the definition of processes related to the detection of fraud, misreporting or tax evasion (e.g., [84,85,86,87,88,89,90,91,92]);

- Accounting: 129 accounting students, accounting benefits, accounting domains, accounting information systems academics, accounting information systems field, accounting journals, accounting literature, accounting processes, accounting publications, accounting researchers, accounting standards, annual bank account balances, especially management accounting, firm accounting performance, outsourcing accounting functions;

- Audit: audit analytics, audit arena, audit fraud brainstorming, audit process, audit standards, audit support systems, audit team, auditing literature, budgeted audit hours, chief audit executives, computer audit specialist, continuous auditing methodology, current audit practice, financial audits, internal audit function, internal auditing department, prior year audit, reduced audit fee increases, small audit firms, traditional audit paradigm;

- Business: business networks, business operations, business process agility, business process standards, business value research, computing-related business objectives, existing business processes, extensible business, hindering business efforts, intermediate business processes, overall business performance, reporting business information;

- Control: control compliance, control issues, corrective controls, effective controls, ineffective controls, informal management control systems, internal control deficiencies, internal control environment, internal control overrides, internal control reporting requirements, internal control weakness, internal control weaknesses, it-related controls;

- Data: applying data mining techniques, corporate data, data analysis tool, data patterns, descriptive data mining approach, descriptive data mining strategy, financial data, global data ecosystem, journal entry data sets, out-of-sample data, panel data, perceptive field survey data, precise data values, prediction data mining techniques, process-level data, procurement data, proprietary data, quantitative data, researching journal entry data mining, semi-monthly data, soft copy data, tagged data, using data;

- Decisions: compared decisions, deception detection decision aid, decision aid reliability, decision aid reliance behavior, decision aids, decision problems, decision processes, decision trees, experimental decision aid research spans, governance decision making, optimal decision, outsourcing decision, reliance decision;

- Disclosure: cybersecurity disclosure guidance, cybersecurity risk disclosure, disclosure credibility, disclosure role, environmental disclosures, extensive disclosure, financial statement disclosures, improving disclosure timeliness, issuing video disclosures, unauthorized disclosure;

- Effective: brainstorming effectiveness, compromising regulation effectiveness, detrimental effect, differential effect, effective controls, halo effect, information environment effects, interactive effect, mean effects, positive effect, profound effect;

- Firm: aggregate firm level, appointing firms, durable goods industry firms, firm accounting performance, firm productivity, firm profitability, firm value, firm years, registered firms, small audit firms, superior firm performance, threatened firms;

- Function: bi-planning functionality, bi-reporting functionality, incompatible functions, internal audit function, outsourcing accounting functions;

- Information: accounting information systems academics, accounting information systems field, bank trading information systems, capturing context information, chief information officer, deceptive information, detail-tagged footnote information, financial reporting information, health information technology expenses, information asymmetry, information environment effects, information quality, information release, information security risk management, information systems professionals, information systems researchers, information technology literature, information technology outsourcing, integrating information, performance measurement information, qualitative information, recent high-profile information security breach incidents, reporting business information, risk information increases, supplemental information displays, ™ information processing costs, user satisfaction measure information system success, using information;

- Management: bank management, cloud management committee, entail managers, environmental management approach, especially management accounting, informal management control systems, information security risk management, management assertions, management support, managing expectations, resource management;

- Measures: measuring spreadsheet infusion, perceptual measures, performance measurement capabilities, performance measurement information, quality measures, quantitative measure, strategic performance measurement system, subjective measures, user satisfaction measure information system success;

- Performance: average performance, firm accounting performance, firm-level performance, future performance goals, internal process-level performance, organizational performance, overall business performance, performance measurement capabilities, performance measurement information, strategic performance measurement system, superior firm performance, supply chain performance;

- Process: accounting processes, assurance process, audit process, business process agility, business process standards, close process, decision processes, estimation process, existing business processes, implementation processes, intermediate business processes, labor process, manual process, natural language processing, order fulfilment processes, process efficiency, process level, strategic erm processes, ™ information processing costs, work processes;

- Reporting: annual reports, digital reporting, discretionary reporting, financial reporting information, financial reporting systems, internal control reporting requirements, internet reporting, reporting business information, reporting language, reporting timeliness, required reporting deadlines, standard reports, traditional business-to-government reporting;

- Research: artificial intelligence research, broad research streams, business value research, collaborative design research, experimental decision aid research spans, expert systems research, future research, multi-method research, potential research, prior research, research discipline, research environments, research methodology, research perspectives, research program, research quality, research settings, researching journal entry data mining, right research, traditional research classification;

- System: 43 expert systems, accounting information systems academics, accounting information systems field, accounting-related expert systems papers, audit support systems, automated systems, bank trading information systems, computer-mediated communication system, decision-aid system, enterprise resource planning systems adoption, enterprise systems results, expert system publications, expert systems research, financial reporting systems, incentive systems, informal management control systems, information systems professionals, information systems researchers, manual systems, restrictive systems, strategic performance measurement system, system quality, transparent system, user satisfaction measure information system success;

- Technological: health information technology expenses, information technology literature, information technology outsourcing, supporting technologies, technological competence, technological domain, technological solutions, technology dominance;

- Using: emergent use, managerial use, media use, practice use, spreadsheet use, user satisfaction measure information system success, using activity theory, using data, using a hospital, using information, using responses.

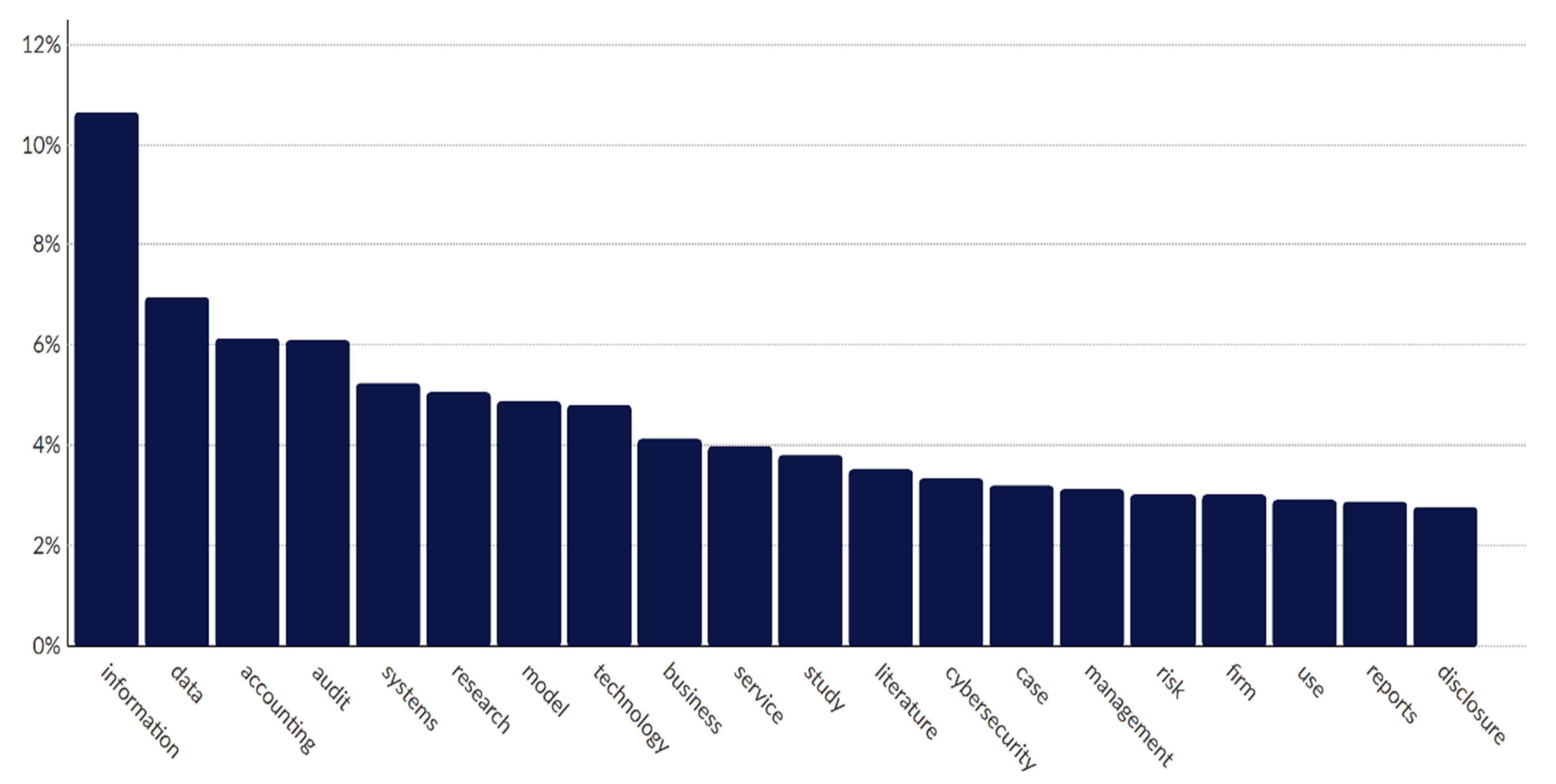

2.2.3. Results for the Latest Period (2020 to 2022)

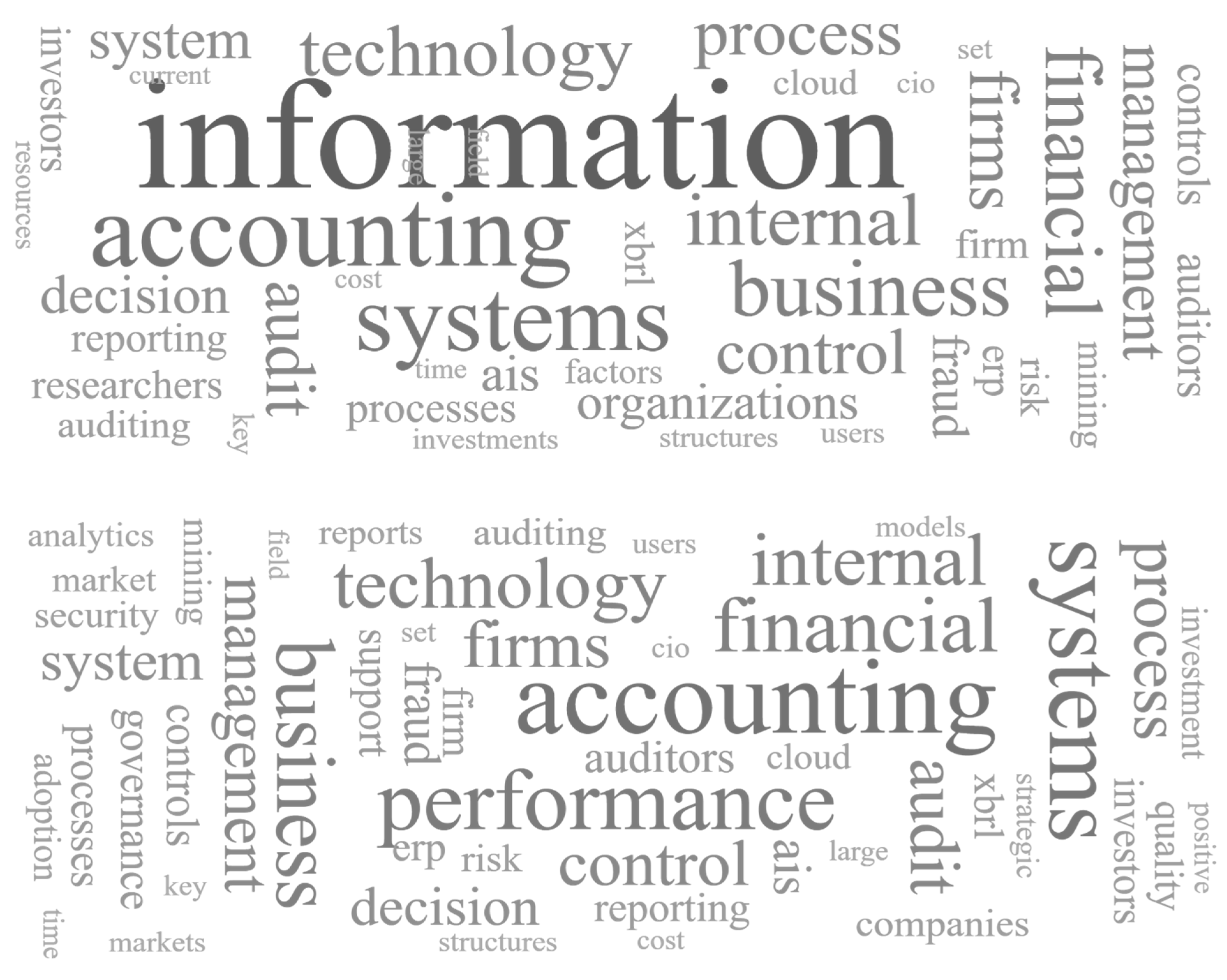

- Accounting: 136 accounting professionals, accounting context, accounting data, accounting fraud data mining literature, accounting fraud detection models, accounting information systems case study, accounting information systems scholars, accounting literature, aggregated accounting numbers, cloud-based client accounting, developing accounting information systems, different accounting standards, highest-ranked accounting journals, laggard accounting systems, management accounting, professional accounting bodies, recent accounting fraud theory, robust account;

- Audit: 4 audit firms, asset-related audits, audit conclusions, audit fee premiums, audit framework, audit hours, audit personnel, audit practice, audited entity, auditing parties, auditing profession, computer-assisted audit tools, contemporary audit standards, continuous audit procedures, cybersecurity audit effectiveness, digital audit evidence, financial statement audits, improving audit quality, increasing audit productivity, internal control audit work, manual audit procedures, recurring audit deficiencies, relevant audit standards, reliable audit evidence;

- Business: business digitization, business information technology intensity, business model transformation indices, business operations, business processes, business professionals, business rules, general business descriptions, increasing business competition, strategic business partner role;

- Case: accounting information systems case study, compelling use case, in-depth case study, participatory case study, specific case, various use cases;

- Cybersecurity: 52 cybersecurity comment letters, cybersecurity audit effectiveness, cybersecurity breach incidents, cybersecurity incidents, cybersecurity risk disclosure practices, cybersecurity risk disclosure trends, organizational cybersecurity risk exposure, overall cybersecurity risks, proprietary cybersecurity information, regarding cybersecurity;

- Data: accounting data, accounting fraud data mining literature, available data, big data capabilities, big data technologies, climate data, collected data, data analytics, data breach, data processing integrity, data quality research, data standards, data visualization software, financial data, general ledger data, interactive data visualization, interview data, legal-entity data segmentation, novel data analysis technique, novel data mining technique, real-life data, social media data, textual data, unstructured data, using data;

- Disclosures: corporate disclosures, cryptocurrency disclosures, cybersecurity risk disclosure practices, cybersecurity risk disclosure trends, disclosure location, firm disclosures, remediation disclosures;

- Firms: 4 audit firms, adopting firm, firm disclosures, firm resource, firm samples, firm size, firm tenure, incentivizing client firms, Korean-listed firms;

- Information: accounting information systems, accounting information systems case study, accounting information systems scholars, agricultural information systems, budget information, business information technology intensity, clarifying information, developing accounting information systems, existing information systems, information content, information dissemination, information overload, information processing capabilities, information quality, information systems discipline, information systems theories, information technology experts, integrated information systems, personal information management capabilities, private information, proprietary cybersecurity information, qualitative information, quantitative information, social responsibility information, specific value information, text information;

- Literature: accounting fraud data mining literature, accounting literature, current literature, existing literature, extensive literature review, natural language processing literature, prior literature, research literature, systematic literature review;

- Management: cyber risk management effectiveness, cyber risk management maturity, knowledge management research, management accountants, management accounting, management reporting, personal information management capabilities, supply chain management, top management commitment, top management support, workflow management;

- Model: accounting fraud detection models, business model transformation indices, developed models, digital maturity model, filed model, force field model, model performance, predictive models, proposed model, research model, theoretical model, wave theory life cycle model;

- Reporting: financial reporting, management reporting, report length, social responsibility reports, unique reporting requirements;

- Research: answering research questions, data quality research, design science research contribution, empirical research, extending research, future research, knowledge management research, prior research, recent research, research initiative, research literature, research model, research studies;

- Risk: cyber risk management effectiveness, cyber risk management maturity, cybersecurity risk disclosure practices, cybersecurity risk disclosure trends, organizational cybersecurity risk exposure, overall cybersecurity risks, regulation risks, risk assessment;

- Service: assurance services, consumer services, payment services, service components, service quality, shared service mode;

- Study: accounting information systems case study, cross-sectional field study, existing studies, in-depth case study, longitudinal study, multi-case study approach, participatory case study, research studies;

- System: accounting information systems, accounting information systems case study, accounting information systems scholars, agricultural information systems, developing accounting information systems, enterprise resource planning system design agenda, existing information systems, information systems discipline, information systems theories, integrated information systems, intelligent systems, laggard accounting systems, system quality, system usage;

- Technology: above-mentioned technologies, big data technologies, blockchain technology applications, blockchain technology solutions, business information technology intensity, computer technology, emerging technology adoption, information technology experts, learning technologies, ledger technology, past technology experience, technological advancements, technological developments, trending technology;

- Use: compelling use case, cost-effective use, decision-making use, effective use, organizational use, user satisfaction, using data, using DevOps, using propensity score, various use cases.

- A more diversified set of subtopics within the topics found;

- The increasing relevance of matters regarding social responsibility, climate, and budgetary information;

- A more evident link, from the subtopics, identified, between accounting and other social sciences through the consideration or inclusion of a wide-ranging of explanatory factors, such as “individual factors”, “environmental factors”, “organizational complexity factors”, “psychological factors”, and “social-psychological factors”;

- A diverse set of underlying theories and research methods used, particularly those focusing on case and experimental studies, as well as literature reviews (for this reason, “case”, “study”, and “literature” appears as novelties within the most relevant topics, besides those previously found, such as “research” and “model”);

- Besides general references to “emergent technologies” or “trending technologies”, the most significant number of indications on specific uses of those tools as precise topics or subtopics, for instance, “blockchain”, “crypto assets” or “cryptocurrencies”, “intelligent systems”, “cloud-based accounting”, “big data”, “data analytics”, “data mining, “learning technologies”, and “natural language”;

- “Risk”, “cybersecurity” and “tax” are included in the set of main topics, which demonstrates the growing relevance of those topics (the latter as a particular novelty for this period).

3. Discussion

3.1. Research Limitations

3.2. Future Avenues in Accounting and Information System Research

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Islam, M.A. Future of Accounting Profession: Three Major Changes and Implications for Teaching and Research. Business Reporting, International Federation of Accountants (IFAC). 2017. Available online: https://eprints.qut.edu.au/104070/ (accessed on 4 December 2022).

- Christensen, J. Accounting in 2036: A Learned Profession. Account. Rev. 2018, 93, 387–390. [Google Scholar] [CrossRef]

- Kaplan, R.S.; Robert, S.; Dzuranin, A.C.; Mălăescu, I.; Janvrin, D.J.; Wood, D.A.; Malsch, B.; Salterio, S.E.; Power, M.K.; Gendron, Y.; et al. Accounting Scholarship that Advances Professional Knowledge and Practice. Account. Rev. 2011, 86, 367–383. [Google Scholar] [CrossRef]

- Al-Adeem, K.R. Who decides what is publishable? Empirical Study on the Influence of a Journal’s Editorial Board on the Observed Paradigm Shift in US Academic Accounting Research. North Am. Account. Stud. 2019, 2, 1–21. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4127109 (accessed on 13 December 2022).

- Carnegie, G.; Parker, L.; Tsahuridu, E. It’s 2020: What is Accounting Today? Aust. Account. Rev. 2021, 31, 65–73. [Google Scholar] [CrossRef]

- Moll, J.; Yigitbasioglu, O. The role of internet-related technologies in shaping the work of accountants: New directions for accounting research. Br. Account. Rev. 2019, 51, 100833. [Google Scholar] [CrossRef]

- Silva, R.; Inácio, H.; Marques, R.P. Blockchain implications for auditing: A systematic literature review and bibliometric analysis. Int. J. Digit. Account. Res. 2022, 22, 163–192. [Google Scholar] [CrossRef]

- Bellucci, M.; Bianchi, D.C.; Manetti, G. Blockchain in accounting practice and research: Systematic literature review. Meditari Account. Res. 2022, 30, 121–146. [Google Scholar] [CrossRef]

- Secinaro, S.; Mas, F.D.; Brescia, V.; Calandra, D. Blockchain in the accounting, auditing and accountability fields: A bibliometric and coding analysis. Account. Audit. Account. J. 2022, 35, 168–203. [Google Scholar] [CrossRef]

- Lardo, A.; Corsi, K.; Varma, A.; Mancini, D. Exploring blockchain in the accounting domain: A bibliometric analysis. Account. Audit. Account. J. 2022, 35, 204–233. [Google Scholar] [CrossRef]

- Mugwira, T. Internet Related Technologies in the auditing profession: A WOS bibliometric review of the past three decades and conceptual structure mapping. Rev. Contab. 2022, 25, 201–216. [Google Scholar] [CrossRef]

- Tank, A.K.; Farrell, A.M. Is Neuroaccounting Taking a Place on the Stage? A Review of the Influence of Neuroscience on Accounting Research. Eur. Account. Rev. 2022, 31, 173–207. [Google Scholar] [CrossRef]

- Kumar, S.; Marrone, M.; Liu, Q.; Pandey, N. Twenty years of the International Journal of Accounting Information Systems: A bibliometric analysis. Int. J. Account. Inf. Syst. 2020, 39, 100488. [Google Scholar] [CrossRef]

- Kroon, N.; Alves, M.; Martins, I. The Impacts of Emerging Technologies on Accountants’ Role and Skills: Connecting to Open Innovation—A Systematic Literature Review. J. Open Innov. Technol. Mark. Complex. 2021, 7, 163. [Google Scholar] [CrossRef]

- Chiu, V.; Liu, Q.; Muehlmann, B.; Baldwin, A.A. A bibliometric analysis of accounting information systems journals and their emerging technologies contributions. Int. J. Account. Inf. Syst. 2019, 32, 24–43. [Google Scholar] [CrossRef]

- Yigitbasioglu, O.M.; Velcu, O. A review of dashboards in performance management: Implications for design and research. Int. J. Account. Inf. Syst. 2012, 13, 41–59. [Google Scholar] [CrossRef]

- Lee, L.; Petter, S.; Fayard, D.; Robinson, S. On the use of partial least squares path modeling in accounting research. Int. J. Account. Inf. Syst. 2011, 12, 305–328. [Google Scholar] [CrossRef]

- Appelbaum, D.; Kogan, A.; Vasarhelyi, M.; Yan, Z. Impact of business analytics and enterprise systems on managerial accounting. Int. J. Account. Inf. Syst. 2017, 25, 29–44. [Google Scholar] [CrossRef]

- Bradford, M.; Florin, J. Examining the role of innovation diffusion factors on the implementation success of enterprise resource planning systems. Int. J. Account. Inf. Syst. 2003, 4, 205–225. [Google Scholar] [CrossRef]

- Poston, R.; Grabski, S. Financial impacts of enterprise resource planning implementations. Int. J. Account. Inf. Syst. 2001, 2, 271–294. [Google Scholar] [CrossRef]

- Elbashir, M.Z.; Collier, P.A.; Davern, M.J. Measuring the effects of business intelligence systems: The relationship between business process and organizational performance. Int. J. Account. Inf. Syst. 2008, 9, 135–153. [Google Scholar] [CrossRef]

- Baldwin, A.A.; Morris, B.W.; Scheiner, J.H. Where do AIS researchers publish? Int. J. Account. Inf. Syst. 2000, 1, 123–134. [Google Scholar] [CrossRef]

- Daigle, R.J.; Arnold, V. An analysis of the research productivity of AIS faculty. Int. J. Account. Inf. Syst. 2000, 1, 106–122. [Google Scholar] [CrossRef]

- Nicolaou, A.I. A contingency model of perceived effectiveness in accounting information systems: Organizational coordination and control effects. Int. J. Account. Inf. Syst. 2000, 1, 91–105. [Google Scholar] [CrossRef]

- Nicolaou, A.I. Quality of postimplementation review for enterprise resource planning systems. Int. J. Account. Inf. Syst. 2004, 5, 25–49. [Google Scholar] [CrossRef]

- Hunton, J.E.; Lippincott, B.; Reck, J.L. Enterprise resource planning systems: Comparing firm performance of adopters and nonadopters. Int. J. Account. Inf. Syst. 2003, 4, 165–184. [Google Scholar] [CrossRef]

- Ismail, N.A.; King, M. Firm performance and AIS alignment in Malaysian SMEs. Int. J. Account. Inf. Syst. 2005, 6, 241–259. [Google Scholar] [CrossRef]

- Nicolaou, A.I.; Bhattacharya, S. Organizational performance effects of ERP systems usage: The impact of post-implementation changes. Int. J. Account. Inf. Syst. 2006, 7, 18–35. [Google Scholar] [CrossRef]

- Boulianne, E. Revisiting fit between AIS design and performance with the analyzer strategic-type. Int. J. Account. Inf. Syst. 2007, 8, 1–16. [Google Scholar] [CrossRef]

- Grabski, S.V.; Leech, S.A. Complementary controls and ERP implementation success. Int. J. Account. Inf. Syst. 2007, 8, 17–39. [Google Scholar] [CrossRef]

- O’Leary, D. On the relationship between citations and appearances on “top 25” download lists in the International Journal of Accounting Information Systems. Int. J. Account. Inf. Syst. 2008, 9, 61–75. [Google Scholar] [CrossRef]

- Vasarhelyi, M.A.; Alles, M.G. The “now” economy and the traditional accounting reporting model: Opportunities and challenges for AIS research. Int. J. Account. Inf. Syst. 2008, 9, 227–239. [Google Scholar] [CrossRef]

- Geerts, G.L.; McCarthy, W.E. An ontological analysis of the economic primitives of the extended-REA enterprise information architecture. Int. J. Account. Inf. Syst. 2002, 3, 1–16. [Google Scholar] [CrossRef]

- Bowen, P.L.; Cheung, M.-Y.D.; Rohde, F.H. Enhancing IT governance practices: A model and case study of an organization’s efforts. Int. J. Account. Inf. Syst. 2007, 8, 191–221. [Google Scholar] [CrossRef]

- Dowling, C.; Leech, S. Audit support systems and decision aids: Current practice and opportunities for future research. Int. J. Account. Inf. Syst. 2007, 8, 92–116. [Google Scholar] [CrossRef]

- Kang, H.; Bradley, G. Measuring the performance of IT services: An assessment of SERVQUAL. Int. J. Account. Inf. Syst. 2002, 3, 151–164. [Google Scholar] [CrossRef]

- Bhattacharya, S.; Behara, R.S.; Gundersen, D.E. Business risk perspectives on information systems outsourcing. Int. J. Account. Inf. Syst. 2003, 4, 75–93. [Google Scholar] [CrossRef]

- Bedard, J.C.; Jackson, C.; Ettredge, M.L.; Johnstone, K.M. The effect of training on auditors’ acceptance of an electronic work system. Int. J. Account. Inf. Syst. 2003, 4, 227–250. [Google Scholar] [CrossRef]

- Boritz, J.E. IS practitioners’ views on core concepts of information integrity. Int. J. Account. Inf. Syst. 2005, 6, 260–279. [Google Scholar] [CrossRef]

- Bradley, J. Management based critical success factors in the implementation of Enterprise Resource Planning systems. Int. J. Account. Inf. Syst. 2008, 9, 175–200. [Google Scholar] [CrossRef]

- Curtis, M.B.; Payne, E.A. An examination of contextual factors and individual characteristics affecting technology implementation decisions in auditing. Int. J. Account. Inf. Syst. 2008, 9, 104–121. [Google Scholar] [CrossRef]

- Beasley, M.; Bradford, M.; Dehning, B. The value impact of strategic intent on firms engaged in information systems outsourcing. Int. J. Account. Inf. Syst. 2009, 10, 79–96. [Google Scholar] [CrossRef]

- Ettredge, M.; Richardson, V.J.; Scholz, S. The presentation of financial information at corporate Web sites. Int. J. Account. Inf. Syst. 2001, 2, 149–168. [Google Scholar] [CrossRef]

- Kaplan, S.E.; Nieschwietz, R.J. A Web assurance services model of trust for B2C e-commerce. Int. J. Account. Inf. Syst. 2003, 4, 95–114. [Google Scholar] [CrossRef]

- Marston, C.; Polei, A. Corporate reporting on the Internet by German companies. Int. J. Account. Inf. Syst. 2004, 5, 285–311. [Google Scholar] [CrossRef]

- Bonsón, E.; Escobar, T. Digital reporting in Eastern Europe: An empirical study. Int. J. Account. Inf. Syst. 2006, 7, 299–318. [Google Scholar] [CrossRef]

- Cormier, D.; Ledoux, M.-J.; Magnan, M. The use of Web sites as a disclosure platform for corporate performance. Int. J. Account. Inf. Syst. 2009, 10, 1–24. [Google Scholar] [CrossRef]

- Kim, H.-J.; Mannino, M.; Nieschwietz, R.J. Information technology acceptance in the internal audit profession: Impact of technology features and complexity. Int. J. Account. Inf. Syst. 2009, 10, 214–228. [Google Scholar] [CrossRef]

- Murthy, U.S.; Groomer, S. A continuous auditing web services model for XML-based accounting systems. Int. J. Account. Inf. Syst. 2004, 5, 139–163. [Google Scholar] [CrossRef]

- Alles, M.; Brennan, G.; Kogan, A.; Vasarhelyi, M.A. Continuous monitoring of business process controls: A pilot implementation of a continuous auditing system at Siemens. Int. J. Account. Inf. Syst. 2006, 7, 137–161. [Google Scholar] [CrossRef]

- Debreceny, R.; Gray, G.L. The production and use of semantically rich accounting reports on the Internet: XML and XBRL. Int. J. Account. Inf. Syst. 2001, 2, 47–74. [Google Scholar] [CrossRef]

- Premuroso, R.F.; Bhattacharya, S. Do early and voluntary filers of financial information in XBRL format signal superior corporate governance and operating performance? Int. J. Account. Inf. Syst. 2008, 9, 1–20. [Google Scholar] [CrossRef]

- Bonsón, E.; Cortijo, V.; Escobar, T. Towards the global adoption of XBRL using International Financial Reporting Standards (IFRS). Int. J. Account. Inf. Syst. 2009, 10, 46–60. [Google Scholar] [CrossRef]

- Lord, A.T. ISACA model curricula 2004. Int. J. Account. Inf. Syst. 2004, 5, 251–265. [Google Scholar] [CrossRef]

- Tuttle, B.; Vandervelde, S.D. An empirical examination of CobiT as an internal control framework for information technology. Int. J. Account. Inf. Syst. 2007, 8, 240–263. [Google Scholar] [CrossRef]

- Boulianne, E.; Cho, C.H. The rise and fall of WebTrust. Int. J. Account. Inf. Syst. 2009, 10, 229–244. [Google Scholar] [CrossRef]

- Calderon, T.G.; Cheh, J.J. A roadmap for future neural networks research in auditing and risk assessment. Int. J. Account. Inf. Syst. 2002, 3, 203–236. [Google Scholar] [CrossRef]

- Sutton, S.G. A research discipline with no boundaries: Reflections on 20years of defining AIS research. Int. J. Account. Inf. Syst. 2010, 11, 289–296. [Google Scholar] [CrossRef]

- Granlund, M. Extending AIS research to management accounting and control issues: A research note. Int. J. Account. Inf. Syst. 2011, 12, 3–19. [Google Scholar] [CrossRef]

- Kallunki, J.-P.; Laitinen, E.K.; Silvola, H. Impact of enterprise resource planning systems on management control systems and firm performance. Int. J. Account. Inf. Syst. 2011, 12, 20–39. [Google Scholar] [CrossRef]

- Guan, J.; Levitan, A.S.; Kuhn, J.R. How AIS can progress along with ontology research in IS. Int. J. Account. Inf. Syst. 2013, 14, 21–38. [Google Scholar] [CrossRef]

- Kanellou, A.; Spathis, C. Accounting benefits and satisfaction in an ERP environment. Int. J. Account. Inf. Syst. 2013, 14, 209–234. [Google Scholar] [CrossRef]

- Bradford, M.; Earp, J.B.; Grabski, S. Centralized end-to-end identity and access management and ERP systems: A multi-case analysis using the Technology Organization Environment framework. Int. J. Account. Inf. Syst. 2014, 15, 149–165. [Google Scholar] [CrossRef]

- Gray, G.L.; Chiu, V.; Liu, Q.; Li, P. The expert systems life cycle in AIS research: What does it mean for future AIS research? Int. J. Account. Inf. Syst. 2014, 15, 423–451. [Google Scholar] [CrossRef]

- Ruivo, P.; Oliveira, T.; Neto, M. Examine ERP post-implementation stages of use and value: Empirical evidence from Portuguese SMEs. Int. J. Account. Inf. Syst. 2014, 15, 166–184. [Google Scholar] [CrossRef]

- Hutchison, P.D.; Daigle, R.J.; George, B. Application of latent semantic analysis in AIS academic research. Int. J. Account. Inf. Syst. 2018, 31, 83–96. [Google Scholar] [CrossRef]

- Alles, M. Examining the role of the AIS research literature using the natural experiment of the 2018 JIS conference on cloud computing. Int. J. Account. Inf. Syst. 2018, 31, 58–74. [Google Scholar] [CrossRef]

- Hunton, J.E.; Mauldin, E.; Wheeler, P.; Libby, D.; Libby, J. RETRACTED: Continuous monitoring and the status quo effect. Int. J. Account. Inf. Syst. 2010, 11, 239–252. [Google Scholar] [CrossRef]

- Chan, D.Y.; Vasarhelyi, M. Innovation and practice of continuous auditing. Int. J. Account. Inf. Syst. 2011, 12, 152–160. [Google Scholar] [CrossRef]

- Vasarhelyi, M.; Alles, M.; Kuenkaikaew, S.; Littley, J. The acceptance and adoption of continuous auditing by internal auditors: A micro analysis. Int. J. Account. Inf. Syst. 2012, 13, 267–281. [Google Scholar] [CrossRef]

- Rikhardsson, P.; Dull, R. An exploratory study of the adoption, application and impacts of continuous auditing technologies in small businesses. Int. J. Account. Inf. Syst. 2016, 20, 26–37. [Google Scholar] [CrossRef]

- Jans, M.; Hosseinpour, M. How active learning and process mining can act as Continuous Auditing catalyst. Int. J. Account. Inf. Syst. 2019, 32, 44–58. [Google Scholar] [CrossRef]

- Srivastava, R.P.; Kogan, A. Assurance on XBRL instance document: A conceptual framework of assertions. Int. J. Account. Inf. Syst. 2010, 11, 261–273. [Google Scholar] [CrossRef] [Green Version]

- Henderson, D.; Sheetz, S.D.; Trinkle, B.S. The determinants of inter-organizational and internal in-house adoption of XBRL: A structural equation model. Int. J. Account. Inf. Syst. 2012, 13, 109–140. [Google Scholar] [CrossRef]

- O’Riain, S.; Curry, E.; Harth, A. XBRL and open data for global financial ecosystems: A linked data approach. Int. J. Account. Inf. Syst. 2012, 13, 141–162. [Google Scholar] [CrossRef]

- Heravi, B.R.; Lycett, M.; de Cesare, S. Ontology-based standards development: Application of OntoStanD to ebXML business process specification schema. Int. J. Account. Inf. Syst. 2014, 15, 275–297. [Google Scholar] [CrossRef] [Green Version]

- Dhole, S.; Lobo, G.J.; Mishra, S.; Pal, A.M. Effects of the SEC’s XBRL mandate on financial reporting comparability. Int. J. Account. Inf. Syst. 2015, 19, 29–44. [Google Scholar] [CrossRef]

- Chou, C.-C.; Chang, C.; Peng, J. Integrating XBRL data with textual information in Chinese: A semantic web approach. Int. J. Account. Inf. Syst. 2016, 21, 32–46. [Google Scholar] [CrossRef]

- Chou, C.-C.; Hwang, N.-C.R.; Wang, T.; Debreceny, R. The topical link model-integrating topic-centric information in XBRL-formatted reports. Int. J. Account. Inf. Syst. 2018, 29, 16–36. [Google Scholar] [CrossRef]

- Abdolmohammadi, M.J.; DeSimone, S.M.; Hsieh, T.-S.; Wang, Z. Factors associated with internal audit function involvement with XBRL implementation in public companies: An international study. Int. J. Account. Inf. Syst. 2017, 25, 45–56. [Google Scholar] [CrossRef]

- Peters, M.D.; Wieder, B.; Sutton, S.G.; Wakefield, J. Business intelligence systems use in performance measurement capabilities: Implications for enhanced competitive advantage. Int. J. Account. Inf. Syst. 2016, 21, 1–17. [Google Scholar] [CrossRef]

- Sutton, S.G.; Holt, M.; Arnold, V. “The reports of my death are greatly exaggerated”—Artificial intelligence research in accounting. Int. J. Account. Inf. Syst. 2016, 22, 60–73. [Google Scholar] [CrossRef]

- Rikhardsson, P.; Yigitbasioglu, O. Business intelligence & analytics in management accounting research: Status and future focus. Int. J. Account. Inf. Syst. 2018, 29, 37–58. [Google Scholar] [CrossRef] [Green Version]

- Debreceny, R.S.; Gray, G.L. Data mining journal entries for fraud detection: An exploratory study. Int. J. Account. Inf. Syst. 2010, 11, 157–181. [Google Scholar] [CrossRef]

- Jans, M.; Lybaert, N.; Vanhoof, K. Internal fraud risk reduction: Results of a data mining case study. Int. J. Account. Inf. Syst. 2010, 11, 17–41. [Google Scholar] [CrossRef] [Green Version]

- Gray, G.L.; Debreceny, R.S. A taxonomy to guide research on the application of data mining to fraud detection in financial statement audits. Int. J. Account. Inf. Syst. 2014, 15, 357–380. [Google Scholar] [CrossRef]

- Alles, M.; Gray, G.L. Incorporating big data in audits: Identifying inhibitors and a research agenda to address those inhibitors. Int. J. Account. Inf. Syst. 2016, 22, 44–59. [Google Scholar] [CrossRef]

- Amani, F.A.; Fadlalla, A.M. Data mining applications in accounting: A review of the literature and organizing framework. Int. J. Account. Inf. Syst. 2017, 24, 32–58. [Google Scholar] [CrossRef]

- Chen, Y.-J.; Wu, C.-H.; Li, H.-Y.; Chen, H.-K. Enhancement of fraud detection for narratives in annual reports. Int. J. Account. Inf. Syst. 2017, 26, 32–45. [Google Scholar] [CrossRef]

- Rahimikia, E.; Mohammadi, S.; Rahmani, T.; Ghazanfari, M. Detecting corporate tax evasion using a hybrid intelligent system: A case study of Iran. Int. J. Account. Inf. Syst. 2017, 25, 1–17. [Google Scholar] [CrossRef]

- Werner, M. Financial process mining—Accounting data structure dependent control flow inference. Int. J. Account. Inf. Syst. 2017, 25, 57–80. [Google Scholar] [CrossRef]

- Baader, G.; Krcmar, H. Reducing false positives in fraud detection: Combining the red flag approach with process mining. Int. J. Account. Inf. Syst. 2018, 31, 1–16. [Google Scholar] [CrossRef]

- Prasad, A.; Green, P.; Heales, J. On governance structures for the cloud computing services and assessing their effectiveness. Int. J. Account. Inf. Syst. 2014, 15, 335–356. [Google Scholar] [CrossRef] [Green Version]

- Prasad, A.; Green, P. Governing cloud computing services: Reconsideration of IT governance structures. Int. J. Account. Inf. Syst. 2015, 19, 45–58. [Google Scholar] [CrossRef] [Green Version]

- Yigitbasioglu, O.M. External auditors’ perceptions of cloud computing adoption in Australia. Int. J. Account. Inf. Syst. 2015, 18, 46–62. [Google Scholar] [CrossRef] [Green Version]

- Wang, Y.; Kogan, A. Designing confidentiality-preserving Blockchain-based transaction processing systems. Int. J. Account. Inf. Syst. 2018, 30, 1–18. [Google Scholar] [CrossRef]

- McCallig, J.; Robb, A.; Rohde, F. Establishing the representational faithfulness of financial accounting information using multiparty security, network analysis and a blockchain. Int. J. Account. Inf. Syst. 2019, 33, 47–58. [Google Scholar] [CrossRef]

- Yao, L.J.; Liu, C.; Chan, S.H. The influence of firm specific context on realizing information technology business value in manufacturing industry. Int. J. Account. Inf. Syst. 2010, 11, 353–362. [Google Scholar] [CrossRef]

- Prasad, A.; Heales, J. On IT and business value in developing countries: A complementarities-based approach. Int. J. Account. Inf. Syst. 2010, 11, 314–335. [Google Scholar] [CrossRef] [Green Version]

- Heidari, F.; Loucopoulos, P. Quality evaluation framework (QEF): Modeling and evaluating quality of business processes. Int. J. Account. Inf. Syst. 2014, 15, 193–223. [Google Scholar] [CrossRef]

- Lunardi, G.L.; Becker, J.L.; Maçada, A.C.G.; Dolci, P.C. The impact of adopting IT governance on financial performance: An empirical analysis among Brazilian firms. Int. J. Account. Inf. Syst. 2014, 15, 66–81. [Google Scholar] [CrossRef]

- Brocke, J.V.; Braccini, A.M.; Sonnenberg, C.; Spagnoletti, P. Living IT infrastructures—An ontology-based approach to aligning IT infrastructure capacity and business needs. Int. J. Account. Inf. Syst. 2014, 15, 246–274. [Google Scholar] [CrossRef]

- Cullinan, C.P.; Zheng, X. Outsourcing accounting information systems: Evidence from closed-end mutual fund families. Int. J. Account. Inf. Syst. 2015, 17, 65–83. [Google Scholar] [CrossRef]

- Li, H.; No, W.G.; Wang, T. SEC’s cybersecurity disclosure guidance and disclosed cybersecurity risk factors. Int. J. Account. Inf. Syst. 2018, 30, 40–55. [Google Scholar] [CrossRef]

- Asatiani, A.; Apte, U.; Penttinen, E.; Rönkkö, M.; Saarinen, T. Impact of accounting process characteristics on accounting outsourcing—Comparison of users and non-users of cloud-based accounting information systems. Int. J. Account. Inf. Syst. 2019, 34, 100419. [Google Scholar] [CrossRef]

- Chen, Y.-J.; Liou, W.-C.; Wu, J.-H. Fraud detection for financial statements of business groups. Int. J. Account. Inf. Syst. 2019, 32, 1–23. [Google Scholar] [CrossRef]

- Cho, C.H.; Roberts, R.W. Environmental reporting on the internet by America’s Toxic 100: Legitimacy and self-presentation. Int. J. Account. Inf. Syst. 2010, 11, 1–16. [Google Scholar] [CrossRef] [Green Version]

- Demek, K.C.; Raschke, R.L.; Janvrin, D.J.; Dilla, W.N. Do organizations use a formalized risk management process to address social media risk? Int. J. Account. Inf. Syst. 2018, 28, 31–44. [Google Scholar] [CrossRef]

- Wilkin, C.L.; Campbell, J.; Moore, S.; Simpson, J. Creating value in online communities through governance and stakeholder engagement. Int. J. Account. Inf. Syst. 2018, 30, 56–68. [Google Scholar] [CrossRef]

- Blackburn, N.; Brown, J.; Dillard, J.; Hooper, V. A dialogical framing of AIS–SEA design. Int. J. Account. Inf. Syst. 2014, 15, 83–101. [Google Scholar] [CrossRef]

- Robalo, R.C.; Moreira, J.A. The influence of power strategies in AIS implementation processes. Int. J. Account. Inf. Syst. 2020, 39, 100487. [Google Scholar] [CrossRef]

- Weber, R. Taking the ontological and materialist turns: Agential realism, representation theory, and accounting information systems. Int. J. Account. Inf. Syst. 2020, 39, 100485. [Google Scholar] [CrossRef]

- Huh, B.G.; Lee, S.; Kim, W. The impact of the input level of information system audit on the audit quality: Korean evidence. Int. J. Account. Inf. Syst. 2021, 43, 100533. [Google Scholar] [CrossRef]

- Zhen, J.; Xie, Z.; Dong, K. Impact of IT governance mechanisms on organizational agility and the role of top management support and IT ambidexterity. Int. J. Account. Inf. Syst. 2021, 40, 100501. [Google Scholar] [CrossRef]

- Plant, O.H.; van Hillegersberg, J.; Aldea, A. Rethinking IT governance: Designing a framework for mitigating risk and fostering internal control in a DevOps environment. Int. J. Account. Inf. Syst. 2022, 45, 100560. [Google Scholar] [CrossRef]

- Alles, M.; Gray, G.L. “The first mile problem”: Deriving an endogenous demand for auditing in blockchain-based business processes. Int. J. Account. Inf. Syst. 2020, 38, 100465. [Google Scholar] [CrossRef]

- Vincent, N.E.; Skjellum, A.; Medury, S. Blockchain architecture: A design that helps CPA firms leverage the technology. Int. J. Account. Inf. Syst. 2020, 38, 100466. [Google Scholar] [CrossRef]

- Søgaard, J.S. A blockchain-enabled platform for VAT settlement. Int. J. Account. Inf. Syst. 2021, 40, 100502. [Google Scholar] [CrossRef]

- Yen, J.-C.; Wang, T. Stock price relevance of voluntary disclosures about blockchain technology and cryptocurrencies. Int. J. Account. Inf. Syst. 2021, 40, 100499. [Google Scholar] [CrossRef]

- Gao, L.; Calderon, T.G.; Tang, F. Public companies’ cybersecurity risk disclosures. Int. J. Account. Inf. Syst. 2020, 38, 100468. [Google Scholar] [CrossRef]

- Chandra, A.; Snowe, M.J. A taxonomy of cybercrime: Theory and design. Int. J. Account. Inf. Syst. 2020, 38, 100467. [Google Scholar] [CrossRef]

- Slapničar, S.; Vuko, T.; Čular, M.; Drašček, M. Effectiveness of cybersecurity audit. Int. J. Account. Inf. Syst. 2022, 44, 100548. [Google Scholar] [CrossRef]

- Blakely, B.; Kurtenbach, J.; Nowak, L. Exploring the information content of cyber breach reports and the relationship to internal controls. Int. J. Account. Inf. Syst. 2022, 46, 100568. [Google Scholar] [CrossRef]

- Hsieh, S.-F.; Brennan, G. Issues, risks, and challenges for auditing crypto asset transactions. Int. J. Account. Inf. Syst. 2022, 46, 100569. [Google Scholar] [CrossRef]

- Wang, T.; Yen, J.-C.; Yoon, K. Responses to SEC comment letters on cybersecurity disclosures: An exploratory study. Int. J. Account. Inf. Syst. 2022, 46, 100567. [Google Scholar] [CrossRef]

- Saxton, G.D.; Guo, C.; Saxton, G.D.; Guo, C. Social media capital: Conceptualizing the nature, acquisition, and expenditure of social media-based organizational resources. Int. J. Account. Inf. Syst. 2020, 36, 100443. [Google Scholar] [CrossRef]

- Amin, M.H.; Mohamed, E.K.; Elragal, A. CSR disclosure on Twitter: Evidence from the UK. Int. J. Account. Inf. Syst. 2021, 40, 100500. [Google Scholar] [CrossRef]

- Wilkin, C.; Ferreira, A.; Rotaru, K.; Gaerlan, L.R. Big data prioritization in SCM decision-making: Its role and performance implications. Int. J. Account. Inf. Syst. 2020, 38, 100470. [Google Scholar] [CrossRef]

- Pei, D.; Vasarhelyi, M.A. Big data and algorithmic trading against periodic and tangible asset reporting: The need for U-XBRL. Int. J. Account. Inf. Syst. 2020, 37, 100453. [Google Scholar] [CrossRef]

- Bonsón, E.; Lavorato, D.; Lamboglia, R.; Mancini, D. Artificial intelligence activities and ethical approaches in leading listed companies in the European Union. Int. J. Account. Inf. Syst. 2021, 43, 100535. [Google Scholar] [CrossRef]

- Ma, D.; Fisher, R.; Nesbit, T. Cloud-based client accounting and small and medium accounting practices: Adoption and impact. Int. J. Account. Inf. Syst. 2021, 41, 100513. [Google Scholar] [CrossRef]

- Yoon, K.; Liu, Y.; Chiu, T.; Vasarhelyi, M.A. Design and evaluation of an advanced continuous data level auditing system: A three-layer structure. Int. J. Account. Inf. Syst. 2021, 42, 100524. [Google Scholar] [CrossRef]

- Geerts, G.L.; O’Leary, D.E. V-Matrix: A wave theory of value creation for big data. Int. J. Account. Inf. Syst. 2022, 47, 100575. [Google Scholar] [CrossRef]

- Jun, S.Y.; Kim, D.S.; Jung, S.Y.; Jun, S.G.; Kim, J.W. Stock investment strategy combining earnings power index and machine learning. Int. J. Account. Inf. Syst. 2022, 47, 100576. [Google Scholar] [CrossRef]

- Perdana, A.; Lee, H.H.; Koh, S.; Arisandi, D. Data analytics in small and mid-size enterprises: Enablers and inhibitors for business value and firm performance. Int. J. Account. Inf. Syst. 2021, 44, 100547. [Google Scholar] [CrossRef]

- Zhang, C.; Cho, S.; Vasarhelyi, M. Explainable Artificial Intelligence (XAI) in auditing. Int. J. Account. Inf. Syst. 2022, 46, 100572. [Google Scholar] [CrossRef]

- Zhang, G.; Atasoy, H.; Vasarhelyi, M.A. Continuous monitoring with machine learning and interactive data visualization: An application to a healthcare payroll process. Int. J. Account. Inf. Syst. 2022, 46, 100570. [Google Scholar] [CrossRef]

- Alzamil, Z.; Appelbaum, D.; Nehmer, R. An ontological artifact for classifying social media: Text mining analysis for financial data. Int. J. Account. Inf. Syst. 2020, 38, 100469. [Google Scholar] [CrossRef]

- Lin, H.; Hwang, Y. The effects of personal information management capabilities and social-psychological factors on accounting professionals’ knowledge-sharing intentions: Pre and post COVID-19. Int. J. Account. Inf. Syst. 2021, 42, 100522. [Google Scholar] [CrossRef]

- Monteiro, A.P.; Vale, J.; Leite, E.; Lis, M.; Kurowska-Pysz, J. The impact of information systems and non-financial information on company success. Int. J. Account. Inf. Syst. 2022, 45, 100557. [Google Scholar] [CrossRef]

- Manetti, G.; Bellucci, M.; Oliva, S. Unpacking dialogic accounting: A systematic literature review and research agenda. Account. Audit. Account. J. 2021, 34, 250–283. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

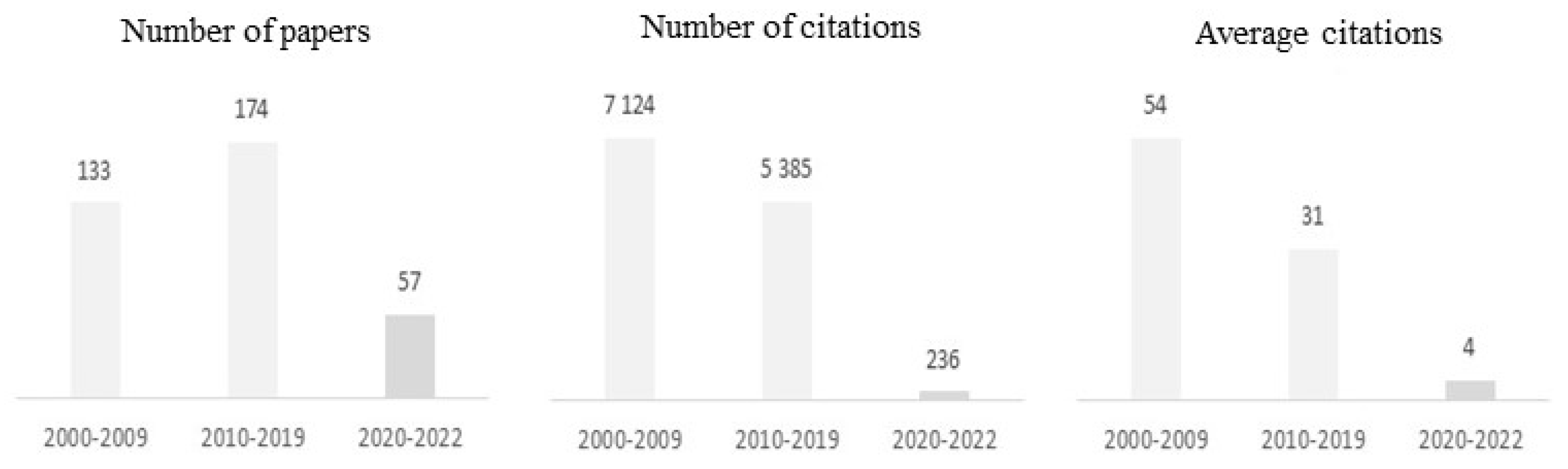

| Journal | Period | Number of Papers | Number of Terms Occurring Once | Total Number of Terms | Distinct Number of Terms | Vocabulary Density |

|---|---|---|---|---|---|---|

| IJAIS (N = 364) | 2000–2009 | 133 | 1477 | 10,870 | 3045 | 0.28 |

| 2010–2019 | 174 | 1643 | 13,969 | 3512 | 0.251 | |

| 2020–2022 | 57 | 1059 | 5161 | 1935 | 0.375 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Albuquerque, F.; Dos Santos, P.G. Recent Trends in Accounting and Information System Research: A Literature Review Using Textual Analysis Tools. FinTech 2023, 2, 248-274. https://doi.org/10.3390/fintech2020015

Albuquerque F, Dos Santos PG. Recent Trends in Accounting and Information System Research: A Literature Review Using Textual Analysis Tools. FinTech. 2023; 2(2):248-274. https://doi.org/10.3390/fintech2020015

Chicago/Turabian StyleAlbuquerque, Fábio, and Paula Gomes Dos Santos. 2023. "Recent Trends in Accounting and Information System Research: A Literature Review Using Textual Analysis Tools" FinTech 2, no. 2: 248-274. https://doi.org/10.3390/fintech2020015