Factors Affecting Fintech Adoption: A Systematic Literature Review

Abstract

:1. Introduction

2. Literature Review

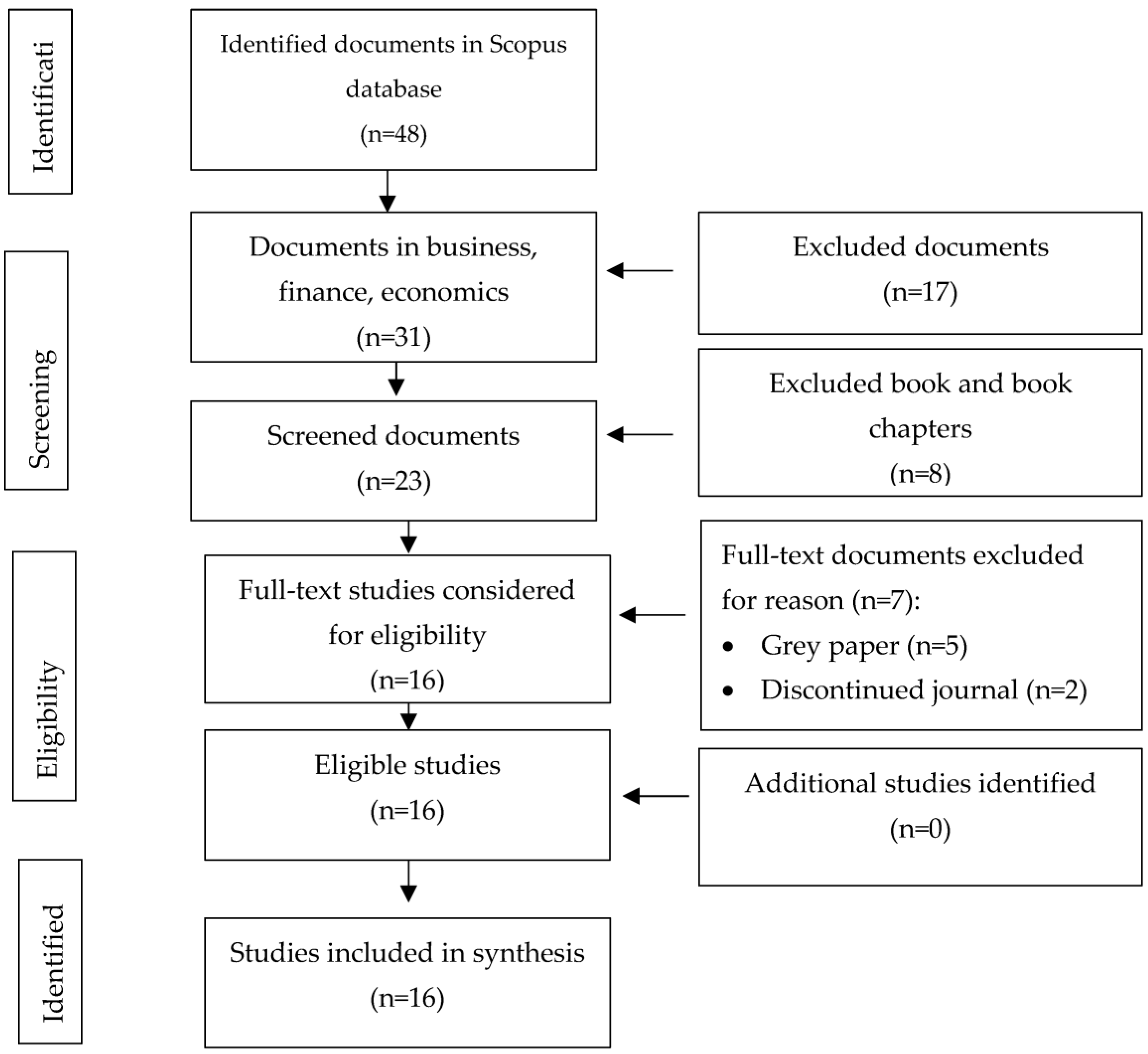

3. Materials and Methods

4. Results and Discussion

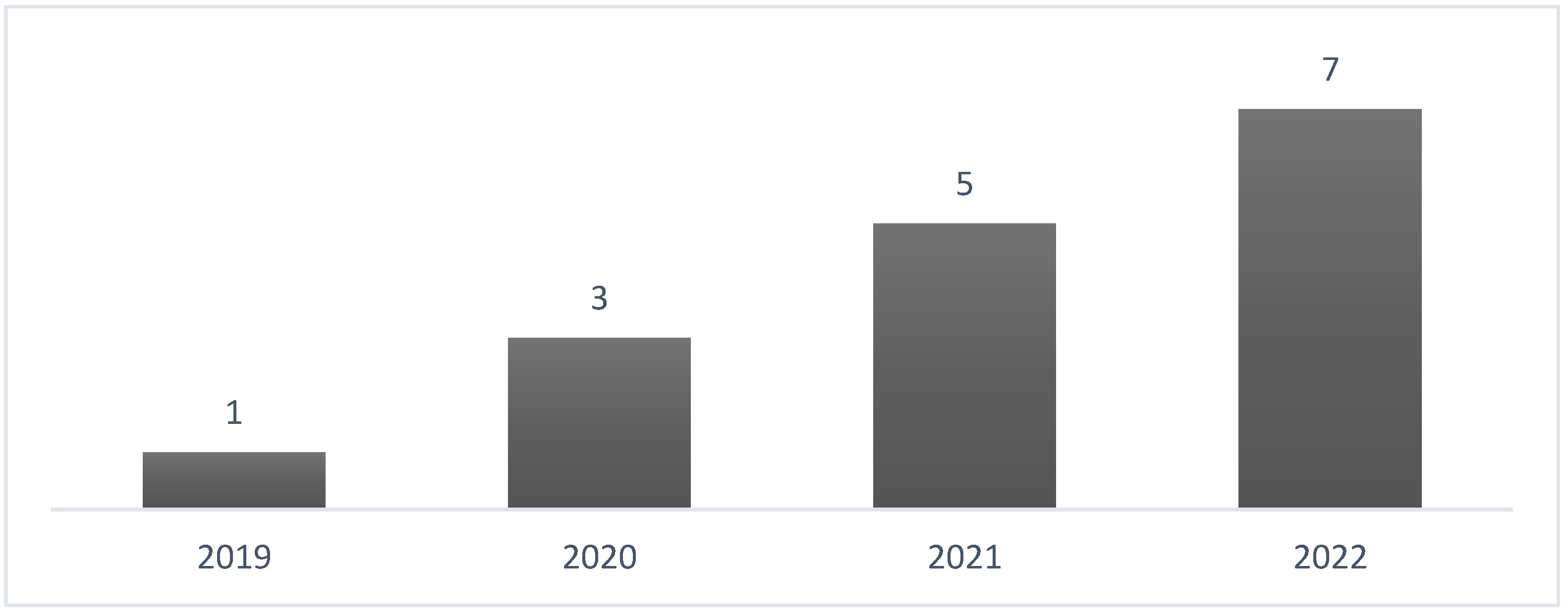

4.1. Publication Year

4.2. Journal and Publisher

4.3. Selected Paper

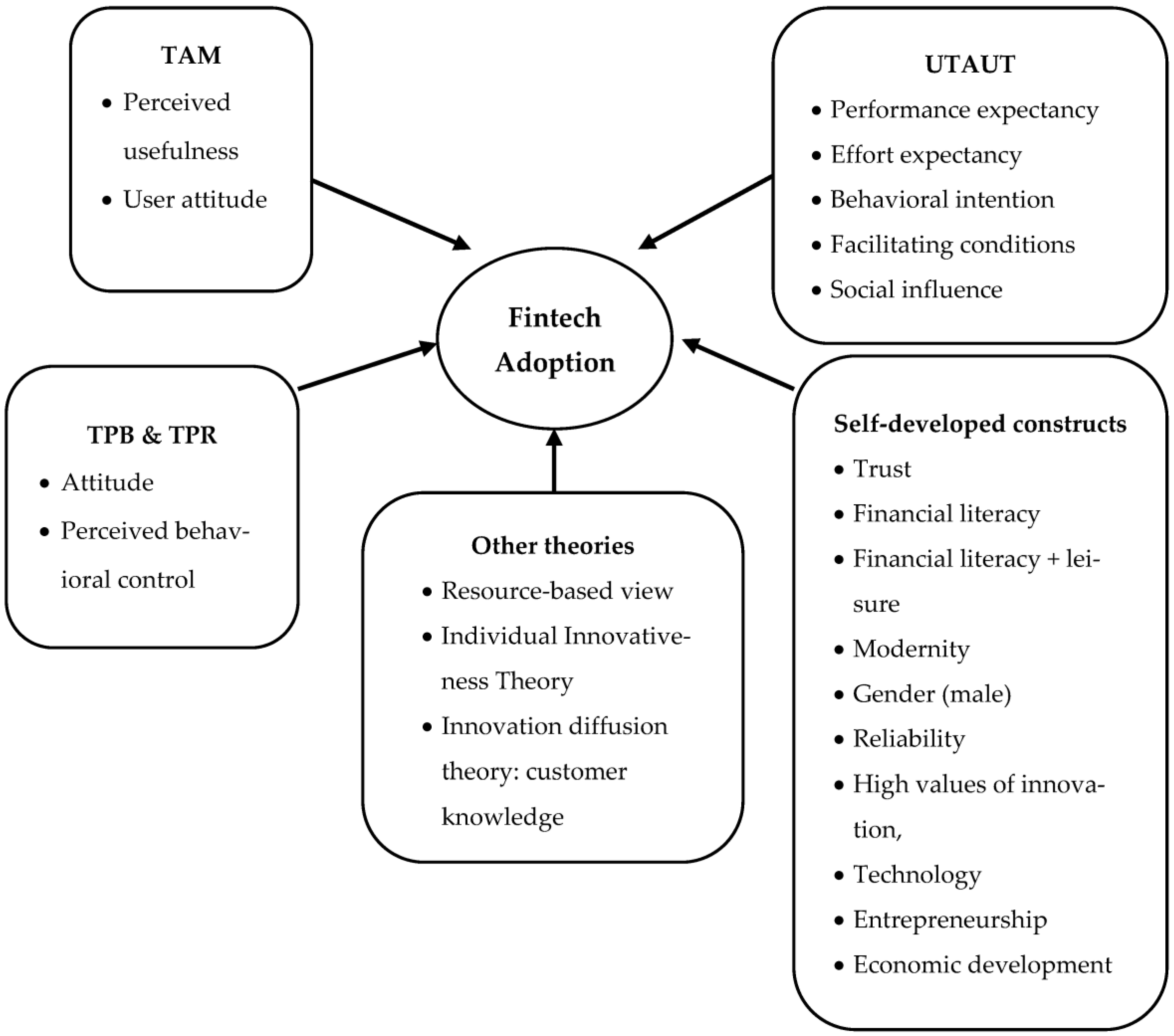

4.4. Determinants of Fintech Adoption

4.4.1. TAM-Related Determinants

{kind=link}

{kind=link}

{kind=link}

| No | Authors | Title | Year | Method & Research Type | Theory | Country | Significant Independent Variables (Including Sign) |

|---|---|---|---|---|---|---|---|

| 1 | Ali et al. [38] | How perceived risk, benefit and trust determine user Fintech adoption: a new dimension for Islamic finance | 2021 | Quantitative & empirical | Theory of perceived risk (TPR), perceived benefit and trust | Pakistan | (+) User trust |

| 2 | Belanche et al. [33] | Artificial Intelligence in FinTech: understanding robo-advisors adoption among customers | 2019 | Quantitative & empirical | Technology acceptance model (TAM) | North America, Britain, Portugal | (+) Consumers’ attitudes toward robo-advisors (+) Mass media (+) Interpersonal subjective norms |

| 3 | Chan et al. [39] | Towards an understanding of consumers’ FinTech adoption: the case of Open Banking | 2022 | Quantitative & empirical | Unified theory of acceptance and use of technology (UTAUT) | Australia | (+) Performance expectancy (+) Effort expectancy (+) Social influence (-) Perceived risk |

| 4 | Frederiks et al. [40] | The early bird catches the worm: The role of regulatory uncertainty in early adoption of blockchain’s cryptocurrency by fintech ventures | 2022 | Quantitative & empirical | Resource-based view | Cross-countries | (+) Regulatory uncertainty has a positive effect on NTBFs’ adoption of fintech (crypto) |

| 5 | Fu & Mishra [41] | Fintech in the time of COVID-19: Technological adoption during crises | 2022 | Quantitative & empirical | Not available | Cross-countries | (+) COVID-19 pandemic spread and lockdowns affect download finance app |

| 6 | Hasan et al. [34] | Evaluating Drivers of Fintech Adoption in The Netherlands | 2021 | Quantitative & empirical | TAM & VAM (value-based adoption model) | Netherland | (+) Perceived ease of use (+) Perceived usefulness (+) Safety (+) Trust |

| 7 | Huarng & Yu [42] | Causal complexity analysis for fintech adoption at the country level | 2022 | Quantitative & empirical | Not available | Cross-countries | Combination of the followings: (+) High values of innovation, (+) Technology (+) Entrepreneurship (+) Economic development |

| 8 | Jünger & Mietzner [43] | Banking goes digital: The adoption of FinTech services by German households | 2020 | Quantitative & empirical | Not available (self-developed) | Germany | (+) Perceived trust (+) Reliability (+) Transparency requirement (+) Financial literacy |

| 9 | Kakinuma [44] | Financial literacy and quality of life: a moderated mediation approach of fintech adoption and leisure | 2022 | Quantitative & empirical | Not available (self-developed) | Thailand | (+) Leisure (+) Financial literacy + leisure |

| 10 | Mazambani & Mutambara [45] | Predicting FinTech innovation adoption in South Africa: the case of cryptocurrency | 2020 | Quantitative & empirical | Theory of Planned Behavior (TPB) | South Africa | (+) Attitude (+) Perceived behavioral control |

| 11 | Ngo & Nguyen [37] | Consumer adoption intention toward FinTech services in a bank-based financial system in Vietnam | 2022 | Quantitative & empirical | TAM & innovation diffusion theory | Vietnam | (+) Customer latent needs for fintech service (+) Customer knowledge |

| 12 | Rahim et al. [46] | Measurement and structural modelling on factors of Islamic Fintech adoption among millennials in Malaysia | 2022 | Quantitative & empirical | UTAUT | Malaysia | (+) Behavioral intention (+) Facilitating conditions |

| 13 | Setiawan et al. [36] | User innovativeness and fintech adoption in Indonesia | 2021 | Quantitative & empirical | TAM, Institutional Theory (IT), and Individual Innovativeness Theory (IIT) | Indonesia | (+) Brand image (+) Fintech perceived usefulness (+) User attitude (+) Financial literacy (+) User innovativeness |

| 14 | Shubbangi Singh et al. [35] | What drives FinTech adoption? A multi-method evaluation using an adapted technology acceptance model | 2020 | Quantitative & empirical | TAM, UTAUT, ServPerfand & WebQual 4.0 | (+) Perceived usefulness (-) social influence | |

| 15 | Solarz & Swacha-Lech [47] | Determinants of the adoption of innovative fintech services by millennials | 2021 | Quantitative & empirical | Not available (self-developed) | Poland | (+) H2: making decisions about choosing a financial institution based on the opinions about a financial institution in social media (+) H4: Modernity applied solutions (+) H7: Using a smartwatch is important (-) H10: age (+) H11: male, than female |

| 16 | Xie et al. [48] | Understanding fintech platform adoption: Impacts of perceived value and perceived risk | 2021 | Quantitative & empirical | UTAUT | China | (+) perceived value (-) perceived risk (+) social influence |

4.4.2. UTAUT-Related Determinants

4.4.3. TPB and TPR-Related Determinants

4.4.4. Other Theories

4.4.5. Self-Developed Constructs

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Baber, H. FinTech, Crowdfunding and Customer Retention in Islamic Banks. Vision 2020, 24, 260–268. [Google Scholar] [CrossRef]

- Zhang, B.Z.; Ashta, A.; Barton, M.E. Do FinTech and financial incumbents have different experiences and perspectives on the adoption of artificial intelligence? Strateg. Chang. 2021, 30, 223–234. [Google Scholar] [CrossRef]

- Hornuf, C.; Hornuf, L. The emergence of the global fintech market: Economic and technological determinants. Small Bus. Econ. 2019, 53, 81–105. [Google Scholar]

- Mackenzie, A. The Fintech Revolution. Lond. Bus. Sch. Rev. 2015, 26, 50–53. [Google Scholar] [CrossRef]

- Buchak, G.; Matvos, G.; Piskorski, T.; Seru, A. Fintech, regulatory arbitrage, and the rise of shadow banks. J. Financ. Econ. 2018, 130, 453–483. [Google Scholar] [CrossRef]

- Baber, H. Relevance of e-SERVQUAL for determining the quality of FinTech services. Int. J. Electron. Financ. 2019, 9, 257–267. [Google Scholar] [CrossRef]

- Lee, I.; Shin, Y.J. Fintech: Ecosystem, business models, investment decisions, and challenges. Bus. Horiz. 2018, 61, 35–46. [Google Scholar] [CrossRef]

- Takeda, A.; Ito, Y. A review of FinTech research. Int. J. Technol. Manag. 2021, 86, 67–88. [Google Scholar] [CrossRef]

- Hasan, R.; Hassan, M.K.; Aliyu, S. Fintech and Islamic Finance: Literature Review and Research Agenda. Int. J. Islam. Econ. Financ. 2020, 3, 75–94. [Google Scholar] [CrossRef] [Green Version]

- Alshater, M.M.; Saba, I.; Supriani, I.; Rabbani, M.R. Fintech in islamic finance literature: A review. Heliyon 2022, 8, e10385. [Google Scholar] [CrossRef]

- Okfalisa, O.; Mahyarni, M.; Anggraini, W.; Saeed, F.; Moshood, T.D.; Saktioto, S. Quadruple Helix Engagement: Reviews on Syariah Fintech Based SMEs Digitalization Readiness. Indones. J. Electr. Eng. Inform. 2022, 10, 112–122. [Google Scholar] [CrossRef]

- Utami, A.F.; Ekaputra, I.A.; Japutra, A. Adoption of FinTech Products: A Systematic Literature Review. J. Creat. Commun. 2021, 16, 233–248. [Google Scholar] [CrossRef]

- Oladapo, I.A.; Hamoudah, M.M.; Alam, M.M.; Olaopa, O.R.; Muda, R. Customers’ perceptions of FinTech adaptability in the Islamic banking sector: Comparative study on Malaysia and Saudi Arabia. J. Model. Manag. 2021, 17, 1241–1261. [Google Scholar] [CrossRef]

- Najib, M.; Ermawati, W.J.; Fahma, F.; Endri, E.; Suhartanto, D. Fintech in the small food business and its relation with open innovation. J. Open Innov. Technol. Mark. Complex. 2021, 7, 88. [Google Scholar] [CrossRef]

- Milian, E.Z.; Spinola, M.d.M.; de Carvalho, M.M. Fintechs: A literature review and research agenda. Electron. Commer. Res. Appl. 2019, 34, 100833. [Google Scholar] [CrossRef]

- Page, M.J.; McKenzie, J.E.; Bossuyt, P.M.; Boutron, I.; Hoffmann, T.C.; Mulrow, C.D.; Shamseer, L.; Tetzlaff, J.M.; Akl, E.A.; Brennan, S.E.; et al. The PRISMA 2020 statement: An updated guideline for reporting systematic reviews. BMJ 2021, 372, n71. [Google Scholar] [CrossRef]

- Bellucci, M.; Bianchi, D.C.; Manetti, G. Blockchain in accounting practice and research: Systematic literature review. Meditari Account. Res. 2022, 30, 121–146. [Google Scholar] [CrossRef]

- Singh, H.P.; Kumar, S. Working capital management: A literature review and research agenda. Qual. Res. Financ. Mark. 2014, 6, 173–197. [Google Scholar] [CrossRef]

- Aravindaraj, K.; Chinna, P.R. A systematic literature review of integration of industry 4.0 and warehouse management to achieve Sustainable Development Goals (SDGs). Clean. Logist. Supply Chain 2022, 5, 100072. [Google Scholar] [CrossRef]

- Singh, S.; Paul, J.; Dhir, S. Innovation implementation in Asia-Pacific countries: A review and research agenda. Asia Pac. Bus. Rev. 2021, 27, 180–208. [Google Scholar] [CrossRef]

- Sikandar, H.; Kohar, U.H.A. A systematic literature review of open innovation in small and medium enterprises in the past decade. Foresight 2022, 24, 742–756. [Google Scholar] [CrossRef]

- Khaw, T.Y.; Teoh, A.P.; Khalid, S.N.A.; Letchmunan, S. The impact of digital leadership on sustainable performance: A systematic literature review. J. Manag. Dev. 2022, 41, 514–534. [Google Scholar] [CrossRef]

- Joshi, A. Comparison Between Scopus & ISI Web of Science. J. Glob. Values 2016, VII, 1–11. [Google Scholar]

- Thomas, A.; Gupta, V. Tacit knowledge in organizations: Bibliometrics and a framework-based systematic review of antecedents, outcomes, theories, methods and future directions. J. Knowl. Manag. 2021, 26, 1014–1041. [Google Scholar] [CrossRef]

- Coetzee, J. Risk aversion and the adoption of Fintech by South African banks. Afr. J. Bus. Econ. Res. 2019, 14, 133–153. [Google Scholar] [CrossRef]

- Singh, R.; Malik, G.; Jain, V. FinTech effect: Measuring impact of FinTech adoption on banks’ profitability. Int. J. Manag. Pract. 2021, 14, 411–427. [Google Scholar] [CrossRef]

- Tripathy, A.K.; Jain, A. FinTech adoption: Strategy for customer retention. Strateg. Dir. 2020, 36, 47–49. [Google Scholar] [CrossRef]

- Young, D.; Young, J. Technology adoption: Impact of FinTech on financial inclusion of low-income households. Int. J. Electron. Financ. 2022, 11, 202–218. [Google Scholar] [CrossRef]

- Katyayani, J.; Varalakshmi, C. Influence of Consumer Profile on Adoption of Fintech Products with Reference to Vijayawada City, Ap. Int. J. Recent Technol. Eng. 2019, 7, 455–457. [Google Scholar]

- Noreen, M.; Mia, M.S.; Ghazali, Z.; Ahmed, F. Role of Government Policies to Fintech Adoption and Financial Inclusion: A Study in Pakistan. Univers. J. Account. Financ. 2022, 10, 37–46. [Google Scholar] [CrossRef]

- Cortegiani, A.; Ippolito, M.; Ingoglia, G.; Manca, A.; Cugusi, L.; Severin, A.; Strinzel, M.; Panzarella, V.; Campisi, G.; Manoj, L.; et al. Citations and metrics of journals discontinued from Scopus for publication concerns: The GhoS(t)copus Project. F1000Research 2020, 9, 415. [Google Scholar] [CrossRef] [PubMed]

- Davis, F.D.; Bagozzi, R.P.; Warshaw, P.R. User Acceptance of Computer Technology: A Comparison of Two Theoretical Models. Manag. Sci. 1989, 35, 982–1003. [Google Scholar] [CrossRef] [Green Version]

- Belanche, D.; Casaló, L.V.; Flavián, C. Artificial Intelligence in FinTech: Understanding robo-advisors adoption among customers. Ind. Manag. Data Syst. 2019, 119, 1411–1430. [Google Scholar] [CrossRef]

- Hasan, R.; Ashfaq, M.; Shao, L. Evaluating Drivers of Fintech Adoption in the Netherlands. Glob. Bus. Rev. 2021, 1–14. [Google Scholar] [CrossRef]

- Singh, S.; Sahni, M.M.; Kovid, R.K. What drives FinTech adoption? A multi-method evaluation using an adapted technology acceptance model. Manag. Decis. 2020, 58, 1675–1697. [Google Scholar] [CrossRef]

- Setiawan, B.; Nugraha, D.P.; Irawan, A.; Nathan, R.J. User Innovativeness and Fintech Adoption in Indonesia. J. Open Innov. Technol. Mark. Complex. 2021, 7, 188. [Google Scholar] [CrossRef]

- Ngo, H.T.; Nguyen, L.T.H. Consumer adoption intention toward FinTech services in a bank-based financial system in Vietnam. J. Financ. Regul. Compliance 2022. [Google Scholar] [CrossRef]

- Ali, M.; Raza, S.A.; Khamis, B.; Puah, C.H.; Amin, H. How perceived risk, benefit and trust determine user Fintech adoption: A new dimension for Islamic finance. Foresight 2021, 23, 403–420. [Google Scholar] [CrossRef]

- Chan, R.; Troshani, I.; Hill, S.R.; Hoffmann, A. Towards an understanding of consumers’ FinTech adoption: The case of Open Banking. Int. J. Bank Mark. 2022, 40, 886–917. [Google Scholar] [CrossRef]

- Frederiks, A.J.; Costa, S.; Hulst, B.; Groen, A.J.; Costa, S.; Hulst, B.; Groen, A.J. The early bird catches the worm: The role of regulatory uncertainty in early adoption of blockchain’ s cryptocurrency by fintech ventures. J. Small Bus. Manag. 2022, 11, 1–34. [Google Scholar] [CrossRef]

- Fu, J.; Mishra, M. Fintech in the time of COVID−19: Technological adoption during crises. J. Financ. Intermediation 2022, 50, 100945. [Google Scholar] [CrossRef]

- Huarng, K.; Yu, T.H. Causal complexity analysis for fintech adoption at the country level. J. Bus. Res. 2022, 153, 228–234. [Google Scholar] [CrossRef]

- Jünger, M.; Mietzner, M. Banking goes digital: The adoption of FinTech services by German households. Financ. Res. Lett. 2020, 34, 101260. [Google Scholar] [CrossRef]

- Kakinuma, Y. Financial literacy and quality of life: A moderated mediation approach of fintech adoption and leisure. Int. J. Soc. Econ. 2022, 49, 1713–1726. [Google Scholar] [CrossRef]

- Mazambani, L.; Mutambara, E. Predicting FinTech innovation adoption in South Africa: The case of cryptocurrency. Afr. J. Econ. Manag. Stud. 2020, 11, 30–50. [Google Scholar] [CrossRef]

- Rahim, N.F.; Bakri, M.H.; Fianto, B.A.; Zainal, N.; Al Shami, S.A.H. Measurement and structural modelling on factors of Islamic Fintech adoption among millennials in Malaysia. J. Islam. Mark. 2022. [Google Scholar] [CrossRef]

- Solarz, M.; Swacha-Lech, M. Determinants of the Adoption of Innovative Fintech Services by Determinants of the Adoption of Innovative Fintech Services by Millennials. E&M Ekon. Manag. 2021, 24, 149–166. [Google Scholar] [CrossRef]

- Xie, J.; Ye, L.; Huang, W.; Ye, M. Understanding FinTech Platform Adoption: Impacts of Perceived Value and Perceived Risk. J. Theor. Appl. Electron. Commer. Res. 2021, 16, 1893–1911. [Google Scholar] [CrossRef]

- Venkatesh, V.; Morris, M.G.; Davis, G.B.; Davis, F.D. User Acceptance of Information Technology: Toward a Unified View. MIS Q. 2003, 27, 425–478. [Google Scholar] [CrossRef]

| Journal Name | Best Scopus Quartile | Publisher |

|---|---|---|

| Journal of Financial Intermediation | Q1 | Academic Press Inc. |

| Journal of Business Research | Q1 | Elsevier Inc. |

| Finance Research Letters | Q1 | |

| African Journal of Economic and Management Studies | Q1 | Emerald Group Holdings Ltd. |

| Foresight | Q2 | |

| Industrial Management and Data Systems | Q1 | |

| International Journal of Bank Marketing | Q1 | |

| International Journal of Social Economics | Q2 | |

| Journal of Financial Regulation and Compliance | Q3 | |

| Journal of Islamic Marketing | Q2 | |

| Management Decision | Q1 | |

| Journal of Open Innovation: Technology, Market, and Complexity | Q1 | MDPI AG |

| Journal of Theoretical and Applied Electronic Commerce Research | Q2 | |

| Global Business Review | Q2 | Sage Publications India Pvt. Ltd. |

| Journal of Small Business Management | Q1 | Taylor and Francis Ltd. |

| E a M: Ekonomie a Management | Q1 | Technical University of Liberec |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Firmansyah, E.A.; Masri, M.; Anshari, M.; Besar, M.H.A. Factors Affecting Fintech Adoption: A Systematic Literature Review. FinTech 2023, 2, 21-33. https://doi.org/10.3390/fintech2010002

Firmansyah EA, Masri M, Anshari M, Besar MHA. Factors Affecting Fintech Adoption: A Systematic Literature Review. FinTech. 2023; 2(1):21-33. https://doi.org/10.3390/fintech2010002

Chicago/Turabian StyleFirmansyah, Egi Arvian, Masairol Masri, Muhammad Anshari, and Mohd Hairul Azrin Besar. 2023. "Factors Affecting Fintech Adoption: A Systematic Literature Review" FinTech 2, no. 1: 21-33. https://doi.org/10.3390/fintech2010002