Agricultural Commodities in the Context of the Russia-Ukraine War: Evidence from Corn, Wheat, Barley, and Sunflower Oil

Abstract

:1. Introduction

2. Literature Review

3. Methodology

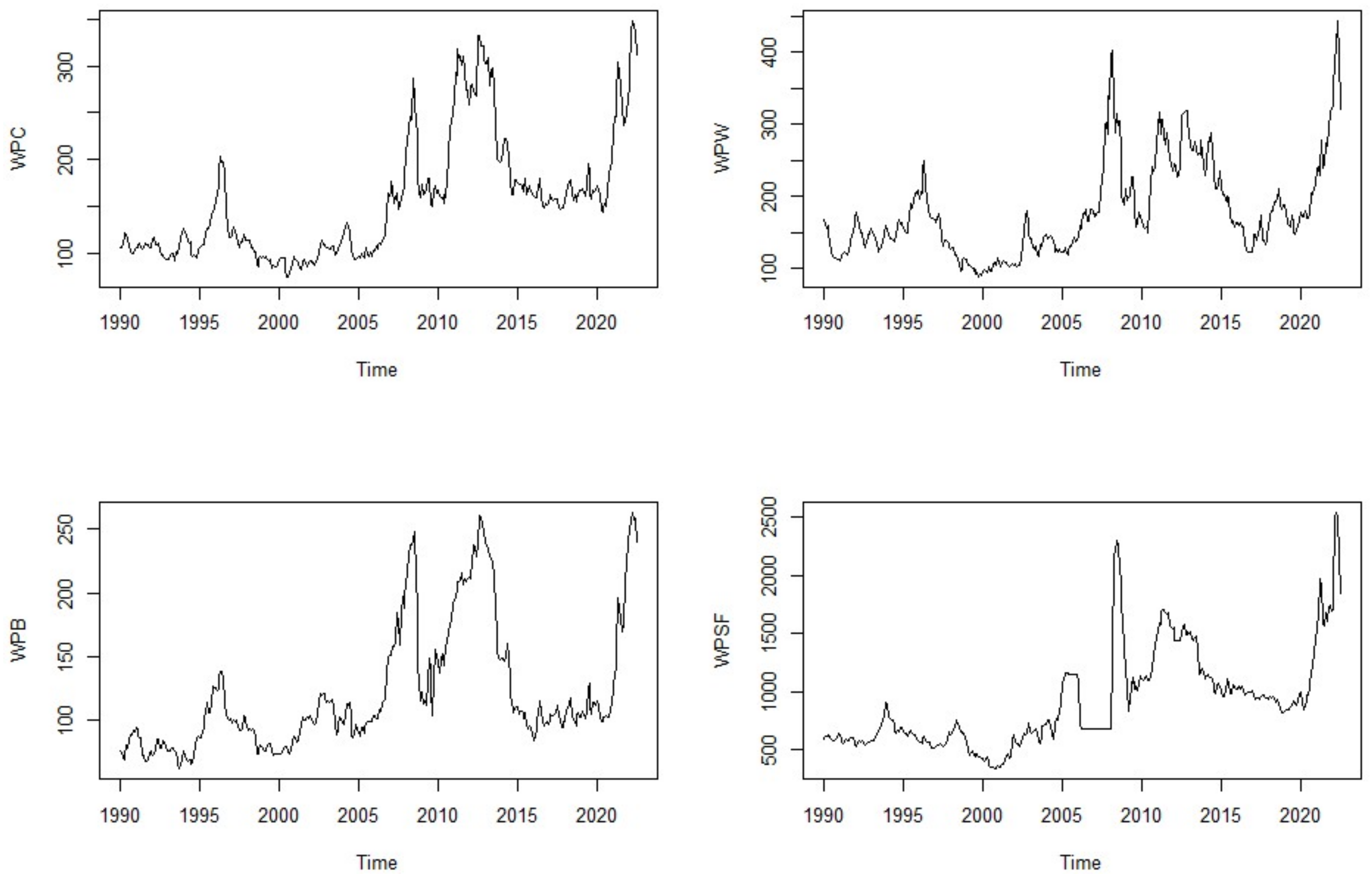

3.1. Data

- Note: plots are constructed based on 391 observations and stand on monthly observations. The R studio program was used for data processing and visualization. The monthly series were obtained from St. Louis FED [59], indicating raw data. The figures were constructed using R studio’s “tidyverse” and “ggplot2” packages. WPW stands for the World Price of Wheat, WPB stands for the World Price of Barley, WPC stands for the World Price of Corn, and the World Price of Sunflower Oil holds the acronym WPSF.

3.2. Methods Used

4. Results

4.1. VAR Estimated Results

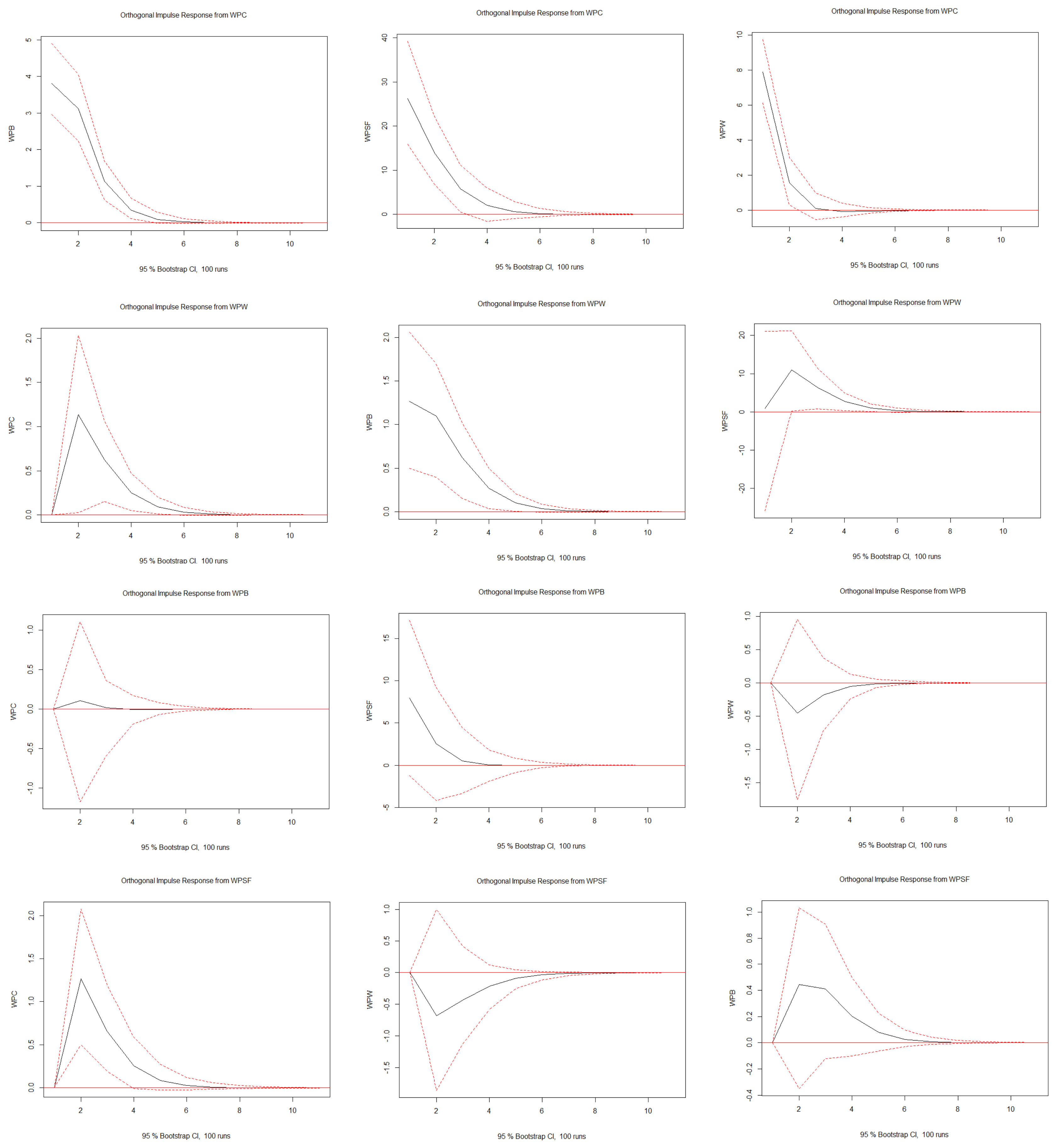

- Note: Plots indicate the VAR (1) impulse response function with twelve combinations of WPC, WPB, WPW and WPSF. IRF results stand within a 95% confidence interval (CI) and are constrained to ten periods ahead. Red lines represent error margins, and simulations were performed with 100 trials. Because our differenced series are monthly, the IRF effects were measured for the next ten months. The variables display the period from 1 January 1990 to 1 August 2022. The figure was generated in R studio using the package “vars” and the function “irf”.

- Note: This figure highlights FEVD results based on four variables in the system for 10 months ahead. The series were differenced indicating the full period from 1 January 1990 to 1 August 2022. Plots were generated in R studio through the “vars” package and implemented with the “fevd” function. Results in a numerical format are available upon request.

4.2. Granger Causality Tests

4.3. Estimated VECM Results

4.4. Estimated Forecasts with VAR and VECM Fanchart

- Note: Plots indicate predictions with raw data through the VAR fanchart package. The estimated forecasts were conducted individually for each variable with a 95% confidence band for ten months ahead. The results cover the entire period from 1 January 1990 to 1 June 2022, based on 391 observations. The estimated forecasts start on 1 July 2022, and end on 1 April 2023. The black line represents the predictions, and the gray-shaded area indicates the error margin.

- Note: This figure presents the forecasts for the next ten months based on 391 observations of each variable in the model. The forecast starts on 1 July 2022 and ends on 1 April 2023 using raw data. Estimations were conducted through the VECM fanchart on a 95% confidence band. The black line represents estimated forecasts, and the shaded part in gray is the error margin. The figure was generated in R studio using the “forecast” package and the “fanchart” function.

5. Discussion: Price Forecasts—Presumption and Limits

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

- Note: The figure indicates the correlation matrix based on the raw data of individual variables. The series represents the full-time period from 1 January 1990 to 1 August 2022. However, the boxplots were also based on raw data, and the plots were generated using the package “tidyverse” in R studio.

- Note: The plot was completed in R studio using the “vars” package and was generated through the “stability” function. The monthly series cover the entire period from 1 January 1990 to 1 August 2022. The red lines show each variable’s 95% confidence band within the system. The series is within the 95% confidence band, indicating a stable system.

- Note: Plots were built in R studio using the functions “acf” and “pacf” through the “vars” package. The series represents the full time period from 1 January 1990 to 1 August 2022, using the first difference. The first differencing was used because the data did not pass the stationarity tests in their raw form. The blue line stands for the 95% confidence band, and the black bars highlight the number of autoregressive lags in the system.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Time | fcst (WPC) | fcst (WPW) | fcst (WPB) | fcst (WPSF) |

|---|---|---|---|---|

| 1 July 2022 | 297.32 | 302.31 | 223.73 | 1666.86 |

| 1 August 2022 | 288.83 | 297.71 | 214.47 | 1587.24 |

| 1 September 2022 | 283.95 | 295.76 | 209.53 | 1555.62 |

| 1 October 2022 | 280.65 | 293.64 | 206.52 | 1545.06 |

| 1 November 2022 | 278.01 | 291.11 | 204.26 | 1542.13 |

| 1 December 2022 | 275.60 | 288.38 | 202.27 | 1540.85 |

| 1 January 2023 | 273.31 | 285.62 | 200.39 | 1538.83 |

| 1 February 2023 | 271.07 | 282.93 | 198.56 | 1535.34 |

| 1 March 2023 | 268.87 | 280.33 | 196.76 | 1530.28 |

| 1 April 2023 | 266.68 | 277.82 | 194.98 | 1523.82 |

| Horizon | fcst (WPC) | fcst (WPW) | fcst (WPB) | fcst (WPSF) |

|---|---|---|---|---|

| 1 July 2022 | 295.36 | 297.31 | 218.98 | 1693.19 |

| 1 August 2022 | 285.69 | 290.54 | 206.28 | 1637.49 |

| 1 September 2022 | 279.14 | 287.66 | 202.09 | 1600.58 |

| 1 October 2022 | 275.18 | 285.65 | 200.88 | 1569.88 |

| 1 November 2022 | 272.97 | 283.52 | 200.08 | 1546.78 |

| 1 December 2022 | 271.46 | 281.53 | 199.32 | 1530.63 |

| 1 January 2023 | 270.25 | 279.98 | 198.69 | 1519.40 |

| 1 February 2023 | 269.27 | 278.81 | 198.25 | 1510.98 |

| 1 March 2023 | 268.47 | 277.91 | 197.99 | 1504.00 |

| 1 April 2023 | 267.78 | 277.16 | 197.84 | 1497.89 |

References

- Algieri, B.; Kalkuhl, M.; Koch, N. A tale of two tails: Explaining extreme events in financialized agricultural markets. Food Policy 2017, 69, 256–269. [Google Scholar] [CrossRef]

- Cheng, I.H.; Xiong, W. Financialization of commodity markets. Ann. Rev. Financ. Econ. 2014, 6, 419–441. [Google Scholar] [CrossRef] [Green Version]

- Algieri, B.; Leccadito, A. Price volatility and speculative activities in futures commodity markets: A combination of combinations of p-values test. J. Commod. Mark. 2019, 13, 40–54. [Google Scholar] [CrossRef]

- International Grains Council IGC. Grain Market Report 2022/23. Available online: https://www.igc.int/en/default.aspx (accessed on 11 May 2022).

- United Nations Human Rights Office of the High Commissioner–UNHCR. Ukraine: Civilian Causality Updates August 2022. Available online: https://www.ohchr.org/en/news/2022/08/ukraine-civilian-casualty-update-22-august-2022 (accessed on 11 May 2022).

- Aliu, F.; Hašková, S.; Bajra, U.Q. Consequences of Russian invasion on Ukraine: Evidence from foreign exchange rates. J. Risk Financ. 2022; ahead-of-print. [Google Scholar] [CrossRef]

- Sun, M.; Zhang, C. Comprehensive analysis of global stock market reactions to the Russia-Ukraine war. Appl. Econ. Lett. 2022, 1–8. [Google Scholar] [CrossRef]

- Ihle, R.; Bar-Nahum, Z.; Nivievskyi, O.; Rubin, O.D. Russia’s invasion of Ukraine increased the synchronisation of global commodity prices. Aust. J. Agric. Resour. Econ. 2022, 66, 775–796. [Google Scholar] [CrossRef]

- Svanidze, M.; Götz, L.; Serebrennikov, D. The influence of Russia’s 2010/2011 wheat export ban on spatial market integration and transaction costs of grain markets. Appl. Econ. Perspect. Policy 2022, 44, 1083–1099. [Google Scholar] [CrossRef]

- FAO. Impact of the Ukraine-Russia Conflict on Global Food Security and Related Matters under the Mandate of the Food and Agriculture Organization of the United Nations (FAO). Available online: https://www.fao.org/3/ni734en/ni734en.pdf (accessed on 11 May 2022).

- United Nations Children’s Fund–UNICEF. The Impact of the War in Ukraine and Subsequent Economic Downturn on Child Poverty in Eastern Europe and Central Asia. Available online: https://reliefweb.int/report/ukraine/impact-war-ukraine-and-subsequent-economic-downturn-child-poverty-eastern-europe-and-central-asia (accessed on 30 October 2022).

- Hassan, M.K.; Muneeza, A.; Sarea, A.M. The impact of the COVID-19 pandemic on Islamic finance: The lessons learned and the way forward. In Towards a Post-Covid Global Financial System; Emerald Publishing Limited: Bingley, UK, 2022. [Google Scholar]

- Batten, J.A.; Choudhury, T.; Kinateder, H.; Wagner, N.F. Volatility impacts on the European banking sector: GFC and COVID-19. Ann. Oper. Res. 2022, 1–26. [Google Scholar]

- Kinateder, H.; Campbell, R.; Choudhury, T. Safe haven in GFC versus COVID-19: 100 turbulent days in the financial markets. Financ. Res. Lett. 2021, 43, 101951. [Google Scholar] [CrossRef]

- International Monetary Fund. World Economic Outlook, July 2022: Gloomy and Uncertain. Available online: https://www.imf.org/en/Publications/WEO#:~:text=Global%20growth%20is%20projected%20to,percent%20over%20the%20medium%20term (accessed on 30 October 2022).

- Ben Hassen, T.; El Bilali, H. Impacts of the Russia-Ukraine war on global food security: Towards more sustainable and resilient food systems? Foods 2022, 11, 2301. [Google Scholar] [CrossRef]

- Furceri, D.; Loungani, P.; Simon, J.; Wachter, S.M. Global food prices and domestic inflation: Some cross-country evidence. Oxf. Econ. Pap. 2016, 68, 665–687. [Google Scholar] [CrossRef]

- Ferrucci, G.; Jiménez-Rodríguez, R.; Onorantea, L. Food price pass-through in the euro area: Non-linearities and the role of the common agricultural policy. Int. J. Cent. Bank. 2018, 8, 179–217. [Google Scholar]

- Pedersen, M. Propagation of Shocks to Food and Energy Prices: An International Comparison; Central Bank of Chile: Santiago, Chile, 2011. [Google Scholar]

- Bajra, U.Q.; Aliu, F.; Aver, B.; Čadež, S. COVID-19 pandemic–related policy stringency and economic decline: Was it really inevitable? Econ. Res.—Ekon. Istraž. 2022, 36, 1–17. [Google Scholar] [CrossRef]

- Peersman, G. International food commodity prices and missing (dis) inflation in the euro area. Rev. Econ. Stat. 2022, 104, 85–100. [Google Scholar] [CrossRef]

- Mester, L.J. The Role of Inflation Expectations in Monetary Policymaking: A Practitioner’s Perspective. Available online: https://www.ecb.europa.eu/pub/conferences/ecbforum/shared/pdf/2022/Mester_speech.pdf (accessed on 30 October 2022).

- Coibion, O.; Gorodnichenko, Y. Is the Phillips curve alive and well after all? Inflation expectations and the missing disinflation. Am. Econ. J. Macroecon. 2015, 7, 197–232. [Google Scholar] [CrossRef] [Green Version]

- De Winne, J.; Peersman, G. Macroeconomic Effects of Disruptions in Global Food Commodity Markets: Evidence for the United States. Brookings Papers on Economic Activity; Brookings Institution Press: Washington, DC, USA, 2016; pp. 183–286. [Google Scholar]

- Astrov, V.; Ghodsi, M.; Grieveson, R.; Holzner, M.; Kochnev, A.; Landesmann, M.; Bykova, A. Russia’s invasion of Ukraine: Assessment of the humanitarian, economic, and financial impact in the short and medium term. Int. Econ. Econ. Policy 2022, 19, 331–381. [Google Scholar] [CrossRef]

- Just, M.; Echaust, K. Dynamic spillover transmission in agricultural commodity markets: What has changed after the COVID-19 threat? Econ. Lett. 2022, 217, 110671. [Google Scholar] [CrossRef]

- Mišečka, T.; Ciaian, P.; Rajčániová, M.; Pokrivčák, J. In search of attention in agricultural commodity markets. Econ. Lett. 2019, 184, 108668. [Google Scholar] [CrossRef]

- Gardebroek, C.; Hernandez, M.A.; Robles, M. Market interdependence and volatility transmission among major crops. Agric. Econ. 2016, 47, 141–155. [Google Scholar] [CrossRef] [Green Version]

- Jagtap, S.; Trollman, H.; Trollman, F.; Garcia-Garcia, G.; Parra-López, C.; Duong, L.; Martindale, W.; Munekata, P.E.S.; Lorenzo, J.M.; Hdaifeh, A.; et al. The Russia-Ukraine conflict: Its implications for the global food supply chains. Foods 2022, 11, 2098. [Google Scholar] [CrossRef]

- Prohorovs, A. Russia’s war in Ukraine: Consequences for European countries’ businesses and economies. J. Risk Financ. Manag. 2022, 15, 295. [Google Scholar] [CrossRef]

- Mendez, A.; Forcadell, F.J.; Horiachko, K. Russia–Ukraine crisis: China’s Belt Road Initiative at the crossroads. Asian Bus. Manag. 2022, 21, 488–496. [Google Scholar] [CrossRef]

- Dodd, O.; Fernandez-Perez, A.; Sosvilla-Rivero, S. Currency and commodity return relationship under extreme geopolitical risks: Evidence from the invasion of Ukraine. Appl. Econ. Lett. 2022. Early Access. [Google Scholar] [CrossRef]

- Siqueira, E.L., Jr.; Stošić, T.; Bejan, L.; Stošić, B. Correlations and cross-correlations in the Brazilian agrarian commodities and stocks. Phys. A Stat. Mech. Appl. 2010, 389, 2739–2743. [Google Scholar] [CrossRef]

- Lundberg, C.; Abman, R. Maize price volatility and deforestation. Am. J. Agric. Econ. 2022, 104, 693–716. [Google Scholar] [CrossRef]

- Carriquiry, M.; Dumortier, J.; Elobeid, A. Trade scenarios compensating for halted wheat and maize exports from Russia and Ukraine increase carbon emissions without easing food insecurity. Nat. Food 2022, 3, 847–850. [Google Scholar] [CrossRef]

- Eurostat. The Food Price Monitoring Tool. 2022. Available online: https://ec.europa.eu/eurostat/cache/metadata/en/prc_fsc_idx_esms.htm (accessed on 30 October 2022).

- Ahn, S.; Kim, D.; Steinbach, S. The impact of the Russian invasion of Ukraine on grain and oilseed trade. Agribusiness 2023, 39, 291–299. [Google Scholar] [CrossRef]

- Gordeev, R.V.; Pyzhev, A.I.; Zander, E.V. Does Climate Change Influence Russian Agriculture? Evidence from Panel Data Analysis. Sustainability 2022, 14, 718. [Google Scholar] [CrossRef]

- World Data Center. Ukraine: Agricultural Overview. 2022. Available online: http://wdc.org.ua/en/node/29 (accessed on 15 October 2022).

- Svanidze, M.; Đurić, I. Global wheat market dynamics: What is the role of the EU and the Black Sea wheat exporters? Agriculture 2021, 11, 799. [Google Scholar] [CrossRef]

- Zyukin, D.A.; Zhilyakov, D.I.; Bolokhontseva, Y.I.; Petrushina, O.V. Export of Russian grain: Prospects and the role of the state in its development. Amazon. Investig. 2020, 9, 320–329. [Google Scholar] [CrossRef]

- Observatory of Economic Complexity OEC. Export of Corn of Russia. Available online: https://oec.world/en/profile/bilateral-product/corn/reporter/rus (accessed on 15 October 2022).

- Hunt, E.; Femia, F.; Werrell, C.; Christian, J.I.; Otkin, J.A.; Basara, J.; McGaughey, K. Agricultural and food security impacts from the 2010 Russia flash drought. Weather Clim. Extremes 2021, 34, 100383. [Google Scholar] [CrossRef]

- Zyukin, D.A.; Pronskaya, O.N.; Golovin, A.A.; Belova, T.V. Prospects for increasing exports of Russian wheat to the world market. Amazon. Investig. 2020, 9, 346–355. [Google Scholar] [CrossRef]

- Vasylieva, N. Ukrainian Cereals in Global Food Security: Production and Export Components. Montenegrin J. Econ. 2020, 16, 143–153. [Google Scholar] [CrossRef]

- Chuprina, Y.Y.; Klymenko, I.V.; Belay, Y.M.; Golovan, L.V.; Buzina, I.M.; Nazarenko, V.V.; Laslo, O.O. The adaptability of soft spring wheat (Triticum aestivum L.) varieties. Ukr. J. Ecol. 2021, 11, 267–272. [Google Scholar]

- Ajanovic, A. Biofuels versus food production: Does biofuels production increase food prices? Energy 2011, 36, 2070–2076. [Google Scholar] [CrossRef]

- Kapustová, Z.; Kapusta, J.; Bielik, P. Food-biofuels interactions: The case of the US biofuels market. AGRIS Pap. Econ. Inform. 2018, 10, 27–38. [Google Scholar] [CrossRef]

- Persson, U.M. The impact of biofuel demand on agricultural commodity prices: A systematic review. Adv. Bioenergy Sustain. Chall. 2016, 4, 410–428. [Google Scholar]

- Khanna, M.; Rajagopal, D.; Zilberman, D. Lessons learned from US experience with biofuels: Comparing the hype with the evidence. Rev. Environ. Econ. Policy 2021, 15, 67–86. [Google Scholar] [CrossRef]

- Barichello, R. The COVID-19 pandemic: Anticipating its effects on Canada’s agricultural trade. Can. J. Agric. Econ./Rev. Can. D’agroecon. 2020, 68, 219–224. [Google Scholar] [CrossRef]

- Vercammen, J. Information-rich wheat markets in the early days of COVID-19. Can. J. Agric. Econ./Rev. Can. D’agroecon. 2020, 68, 177–184. [Google Scholar] [CrossRef]

- Espitia, A.; Rocha, N.; Ruta, M. COVID-19 and Food Protectionism: The Impact of the Pandemic and Export Restrictions on World Food Markets. World Bank Policy Research Working Paper; World Bank Group: Washington, DC, USA, 2020; p. 9253. [Google Scholar]

- Dietrich, S.; Giuffrida, V.; Martorano, B.; Schmerzeck, G. COVID-19 policy responses, mobility, and food prices. Am. J. Agric. Econ. 2022, 104, 569–588. [Google Scholar] [CrossRef]

- Nechaev, V.; Mikhailushkin, P.; Davydova, Y. Complex of economic measures for the production of corn hybrids in the Russia. IOP Conf. Ser. Earth Environ. Sci. 2020, 604, 012004. [Google Scholar] [CrossRef]

- Hamulczuk, M.; Makarchuk, O. Time-varying relationship between Ukrainian corn and world crude oil prices. Econ. Ann. XXI 2020, 184, 49–57. [Google Scholar] [CrossRef]

- Grabovskyi, M.; Lozinskyi, M.; Grabovska, T.; Roubík, H. Green mass to biogas in Ukraine—Bioenergy potential of corn and sweet sorghum. Biomass Convers. Biorefinery 2021, 13, 3309–3317. [Google Scholar] [CrossRef]

- Shyurova, N.A.; Dubrovin, V.V.; Narushev, V.B.; Kozhevnikov, A.A.; Milovanov, I.V. Biofuel as an Alternative Energy Source for the Automobile Industry: The Experience of the Lower Volga Region (Russia). J. Ecol. Eng. 2020, 21, 29–35. [Google Scholar] [CrossRef]

- St. Louis FRED (2022). Economic Data on Global Commodity Prices. Available online: https://fred.stlouisfed.org/series/PBARLUSDM (accessed on 15 October 2022).

- Light, J.; Shevlin, T. The 1996 grain price shock: How did it affect food inflation. Mon. Lab. Rev. 1998, 121, 3. [Google Scholar]

- Stock, J.H.; Watson, M.W. Vector Autoregressions. J. Econ. Perspect. 2001, 15, 101–115. [Google Scholar] [CrossRef] [Green Version]

- Sims, C.A. Macroeconomics and reality. Econ. J. Econ. Soc. 1980, 48, 1–48. [Google Scholar] [CrossRef] [Green Version]

- Dickey, D.A.; Fuller, W.A. Likelihood ratio statistics for autoregressive time series with a unit root. Econometrica 1981, 49, 1057–1072. [Google Scholar] [CrossRef]

- Phillips, P.C.; Perron, P. Testing for a unit root in time series regression. Biometrika 1988, 75, 335–346. [Google Scholar] [CrossRef]

- Kwiatkowski, D.; Phillips, P.C.; Schmidt, P.; Shin, Y. Testing the null hypothesis of stationarity against the alternative of a unit root: How sure are we that economic time series have a unit root? J. Econ. 1992, 54, 159–178. [Google Scholar] [CrossRef]

- Engle, R.F.; Granger, C.W. Cointegration and error correction: Representation, estimation, and testing. Econ. J. Econ. Soc. 1987, 55, 251–276. [Google Scholar]

- Wu, H.; Wu, H.; Zhu, M.; Chen, W.; Chen, W. A new method of large-scale short-term forecasting of agricultural commodity prices: Illustrated by the case of agricultural markets in Beijing. J. Big Data 2017, 4, 1–22. [Google Scholar] [CrossRef] [Green Version]

- Gelos, G.; Ustyugova, Y. Inflation responses to commodity price shocks–How and why do countries differ? J. Int. Money Financ. 2017, 72, 28–47. [Google Scholar] [CrossRef] [Green Version]

- De Gregorio, J. Commodity prices, monetary policy, and inflation. IMF Econ. Rev. 2012, 60, 600–633. [Google Scholar] [CrossRef] [Green Version]

- Myers, R.J.; Johnson, S.R.; Helmar, M.; Baumes, H. Long-run and Short-run Co-movements in Energy Prices and the Prices of Agricultural Feedstocks for Biofuel. Am. J. Agric. Econ. 2014, 96, 991–1008. [Google Scholar] [CrossRef]

- Jacks, D.S.; O’rourke, K.H.; Williamson, J.G. Commodity price volatility and world market integration since 1700. Rev. Econ. Stat. 2011, 93, 800–813. [Google Scholar] [CrossRef]

- Vochozka, M.; Janek, S.; Rowland, Z. Coffee as an Identifier of Inflation in Selected US Agglomerations. Forecasting 2023, 5, 153–169. [Google Scholar] [CrossRef]

| n | Mean | Median | Std | Skew | Kurtosis | Min | Max | |

|---|---|---|---|---|---|---|---|---|

| WPC | 391 | 155.1 | 147.2 | 64.9 | 1.15 | 0.47 | 75.1 | 348 |

| WPW | 391 | 178.5 | 161.2 | 65.8 | 1.18 | 1.17 | 88.5 | 444 |

| WPB | 391 | 120.9 | 102.8 | 49.5 | 1.32 | 0.73 | 60.8 | 262 |

| WPSF | 391 | 909.3 | 756.9 | 420.5 | 1.28 | 1.55 | 332.5 | 2204 |

| Variables | Model (1) | Model (2) | Model (3) | Model (4) |

|---|---|---|---|---|

| WPC | WPW | WPB | WPSF | |

| WPC (L1) | 0.172 *** (0.067) | 0.018 (0.094) | 0.180 *** (0.047) | −0.270 (0.527) |

| WPW (L1) | 0.091 ** (0.044) | 0.232 *** (0.062) | 0.074 ** (0.031) | 0.862 ** (0.345) |

| WPB (L1) | −0.004 (0.081) | −0.062 (0.114) | 0.132 ** (0.057) | −0.096 (0.640) |

| WPSF (L1) | 0.016 ** (0.006) | −0.009 (0.009) | 0.006 (0.005) | 0.396 *** (0.051) |

| Const | 0.312 (0.530) | 0.331 (0.749) | 0.192 (0.375) | 1.267 (4.200) |

| Observations | 390 | 390 | 390 | 390 |

| R2 | 0.102 | 0.048 | 0.197 | 0.170 |

| Adjusted R2 | 0.093 | 0.038 | 0.188 | 0.162 |

| Residual Std. Error (df = 384) | 10.438 | 14.741 | 7.372 | 82.645 |

| F Statistic (df = 10; 384) | 10.438 *** | 4.875 *** | 23.498 *** | 19.685 *** |

| Hypothesis Testing | p-Value | H0 |

|---|---|---|

| Granger causality H0: WPC does not Granger-cause WPW, WPB and WPSF | 0.0002 | Rejected |

| Granger causality H0: WPW does not Granger-cause WPC, WPB and WPSF | 0.0190 | Rejected |

| Granger causality H0: WPB does not Granger-cause WPC, WPW and WPSF | 0.9402 | Accepted |

| Granger causality H0: WPSF does not Granger-cause WPC, WPW and WPB | 0.0031 | Rejected |

| Test type: trace statistic, without a linear trend and constant cointegration | |||||

| Eigenvalues (lambda): | [1] 0.305 | [2] 0.278 | [3] 0.252 | [4] 0.174 | [5] 0.000 |

| Values of the test statistic and critical values of the test: | |||||

| Test | 10% | 5% | 1% | ||

| r ≤ 3 | 74.25 | 7.52 | 9.24 | 12.97 | |

| r ≤ 2 | 186.83 | 17.85 | 19.96 | 24.60 | |

| r ≤ 1 | 318.08 | 32.00 | 34.91 | 41.07 | |

| r = 0 | 459.28 | 49.65 | 53.12 | 60.16 | |

| Test type: maximal eigenvalue statistic (lambda max), without a linear trend and constant cointegration | |||||

| Eigenvalues (lambda): | [1] 0.591 | [2] 0.406 | [3] 0.366 | [4] 0.323 | [5] 0.216 |

| Values of the test statistic and critical values of the test: | |||||

| Test | 10% | 5% | 1% | ||

| r ≤ 3 | 74.25 | 7.52 | 9.24 | 12.97 | |

| r ≤ 2 | 112.59 | 13.75 | 15.67 | 20.21 | |

| r ≤ 1 | 131.24 | 19.77 | 22.00 | 26.81 | |

| r = 0 | 141.21 | 25.56 | 28.14 | 33.24 | |

| WPC | WPW | WPB | WPSF | |

| r1 | 1.000 | 0.000 | (0.000) | (0.195) |

| r2 | (0.000) | 1.000 | (0.000) | (0.179) |

| r3 | (0.000) | 0.000 | 1.000 | (0.144) |

| Equation | ECT1 | ECT2 | ECT3 | Intercept |

| WPC | −0.7340(0.0254) ** | 0.0376(0.0205) | 0.0217(0.0274) | −1.2992(0.8968) |

| WPW | 0.0230(0.0358) | −0.0913(0.0289) *** | −0.1096(0.0386) ** | 3.2415(1.2652) * |

| WPB | −0.0393(0.0181) ** | 0.0002(0.0146) | −0.0305(0.0195) | 0.7638(0.6398) |

| WPSF | 0.0488(0.1990) | 0.0107(0.1606) ** | 0.0584(0.2308) | −2.8155(7.0244) |

| Equation | WPW.L1 | WPB.L1 | WPSF.L1 | WPC(L1) |

| WPC | 0.1057(0.0455) * | −0.0258(0.0859) | 0.0062(0.0068) | 0.1729(0.0668) ** |

| WPW | 0.3208(0.0643) *** | −0.1583(0.1212) | −0.0121(0.0096) | 0.0039(0.0942) * |

| WPB | 0.0844(0.1972) ** | 0.1786(0.0476) ** | 0.0034(0.0048) | 0.1552(0.0476) ** |

| WPSF | 0.6014(0.3567) | −0.7129(0.6728) | 0.4268(0.0532) *** | −0.2482(0.5229) |

| Equation | WPB.L2 | WPSF.L2 | WPW.L2 | WPC.L2 |

| WPC | 0.1366(0.0823) | 0.0229(0.0074) ** | −0.0719(0.0462) | −0.0518(0.0680) |

| WPW | −0.0506(0.1161) | 0.0282(0.0104) ** | −0.0792(0.0652) | 0.0839(0.0595) |

| WPB | −0.0921(0.0587) | 0.0171(0.0053)** | 0.0207(0.0330) | −0.0739(0.0485) |

| WPSF | 0.6022(0.6447) | −0.0339(0.0578) | −0.4243(0.3621) | 0.8614(0.5234) *** |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Aliu, F.; Kučera, J.; Hašková, S. Agricultural Commodities in the Context of the Russia-Ukraine War: Evidence from Corn, Wheat, Barley, and Sunflower Oil. Forecasting 2023, 5, 351-373. https://doi.org/10.3390/forecast5010019

Aliu F, Kučera J, Hašková S. Agricultural Commodities in the Context of the Russia-Ukraine War: Evidence from Corn, Wheat, Barley, and Sunflower Oil. Forecasting. 2023; 5(1):351-373. https://doi.org/10.3390/forecast5010019

Chicago/Turabian StyleAliu, Florin, Jiří Kučera, and Simona Hašková. 2023. "Agricultural Commodities in the Context of the Russia-Ukraine War: Evidence from Corn, Wheat, Barley, and Sunflower Oil" Forecasting 5, no. 1: 351-373. https://doi.org/10.3390/forecast5010019