On Forecasting Cryptocurrency Prices: A Comparison of Machine Learning, Deep Learning, and Ensembles

Abstract

:1. Introduction

2. Materials and Methods

2.1. Predictive Models

- Auto Regressive Integrated Moving Average (ARIMA). This is a generalisation of the simpler ARMA model (auto regressive moving average). The traditional three-step process of constructing ARIMA models by [13], includes model identification, parameter estimation, and finally, the diagnosis of the simulation and its verification. Essentially, a prediction for a value is the linear combination of the values up to the timestamp and the prediction errors made for the same values. Examples of ARIMA usage include forecasting for air transport demand [23,24], long-term earning prediction [25], and next-day electricity price prediction [26]. ARIMA has effectively predicted BTC prices in [6,14,27].

- k-Nearest Neighbor (kNN). Originally suited for classification tasks, kNN is a non-parametric model that has been successfully extended and employed for regression tasks in time series analysis. To predict , the kNN calculates the k most-similar values to . Then, prediction of is the weighted average of the k values. The kNN model has been used in financial forecasting [28], electric market price prediction [29], and in the prediction of Bitcoin [30].

- Support Vector Regression (SVR). Built on support vector machines for classification, SVR enables both linear and non-linear regression. Similarly to kNN, SVR is a non-parametric methodology introduced by [31]. SVR aims to maximise generalisation performance when designing regression functions [32]. SVR was applied to a variety of time series tasks such as forecasting warranty claims [32], predicting blood glucose levels [33], and for stock predictions in the financial market [34]. Examples of SVR usage in forecasting crypto prices can be found in [20,21].

- Random Forest (RF) Regressor. This is essentially an ensemble of decision trees, each of which is built on a random subset of the training set. RF’s predictions are performed by averaging the predictions of individual trees. The key benefits of RF are its generalisation capability, and minimal sensitivity to hyperparameters [35]. RF has been used in time series tasks for forecasting cyber security incidents [36], for the prediction of methane outbreaks in coal mines usage [37], and for projecting monthly temperature variations [35]. In the prediction of cryptos, RF has been used for BTC forecasting in [20] and BTC, ETH, and XRP in [19].

- Long Short Term Memory (LSTM). This is a type of RNN capable of learning long-term dependencies and, therefore, is suitable for time series analysis [38]. Although LSTMs follow a chain-like structure similar to ordinary RNNs, in an LSTM’s repeating module, four neural layers interact, i.e., two in the input gate, one in the forget gate, and one in the output gate. The input gate adds or updates new information, and the forget gate removes irrelevant information. The output gate ultimately passes updated information to the following LSTM cell. Examples of LSTM usage can be found in short-term travel speed prediction [39], predicting healthcare trajectories from medical records [40], and forecasting aquifer levels [41]. The model has also been successful for crypto price prediction [7,8,9].

- Gated Recurrent Unit (GRU). Although the GRU model is similar to LSTM, the former improves upon the computational efficiency of the latter because it has fewer external gating signals in the interpolation. Consequently, the related parameters are reduced. GRU has been used in the short-term prediction for a bike-sharing service [42], network traffic predictions [43], and forecasting airborne particle pollution [44]. GRU was found in [10] to forecast the prices of BTC, ETH, and LTC successfully.

- LSTM-GRU (HYBRID). This method was proposed by Patel et al. [11] to avail of the advantages of both LSTM and GRU. Their study indicated that this hybrid approach effectively predicted Litecoin and Monero daily prices, for this reason we include it herein. Combinations of LSTM and GRU have been successfully applied to predict water prices [45].

- Temporal Convolution Network (TCN). Presented by Bai, Kolter, and Koltun [46], TCN is a variant of the convolutional neural network architecture, and uses dilated, causal, one-dimensional convolutional layers. TCN’s causal convolutions prevent future data from leaking into the input. TCNs have been widely adopted in time series forecasting. For example, TCNs can produce a short-term prediction of wind power [47], predict just-in-time design smells [48], and forecast in stock volatility [49]. In addition, TCN was effective at forecasting weekly Ethereum prices [50].

- Temporal Fusion Transformer (TFT). Introduced by [51], the architecture of TFT is built on the vanilla transformer architecture. TFT is one of the most recent deep learning approaches for time series forecasting. Its design incorporates novel components such as gating mechanisms, variable section networks, static covariates, prediction intervals, and temporal processing. TFT has been applied in other time series tasks such as the prediction of pH levels in bodies of water [52], flight demand forecasting [53], and projecting future precipitation levels [54]. To the best of our knowledge, we are the first to employ it for the crypto price prediction.

2.2. Data Collection

- —the timestamp of the day;

- —the opening price of the cryptocurrency at ;

- —the highest price of the cryptocurrency at ;

- —the lowest price of the cryptocurrency at ;

- —the target variable, i.e., the closing price of the cryptocurrency at (which corresponds to the opening price of the following day, i.e., ).

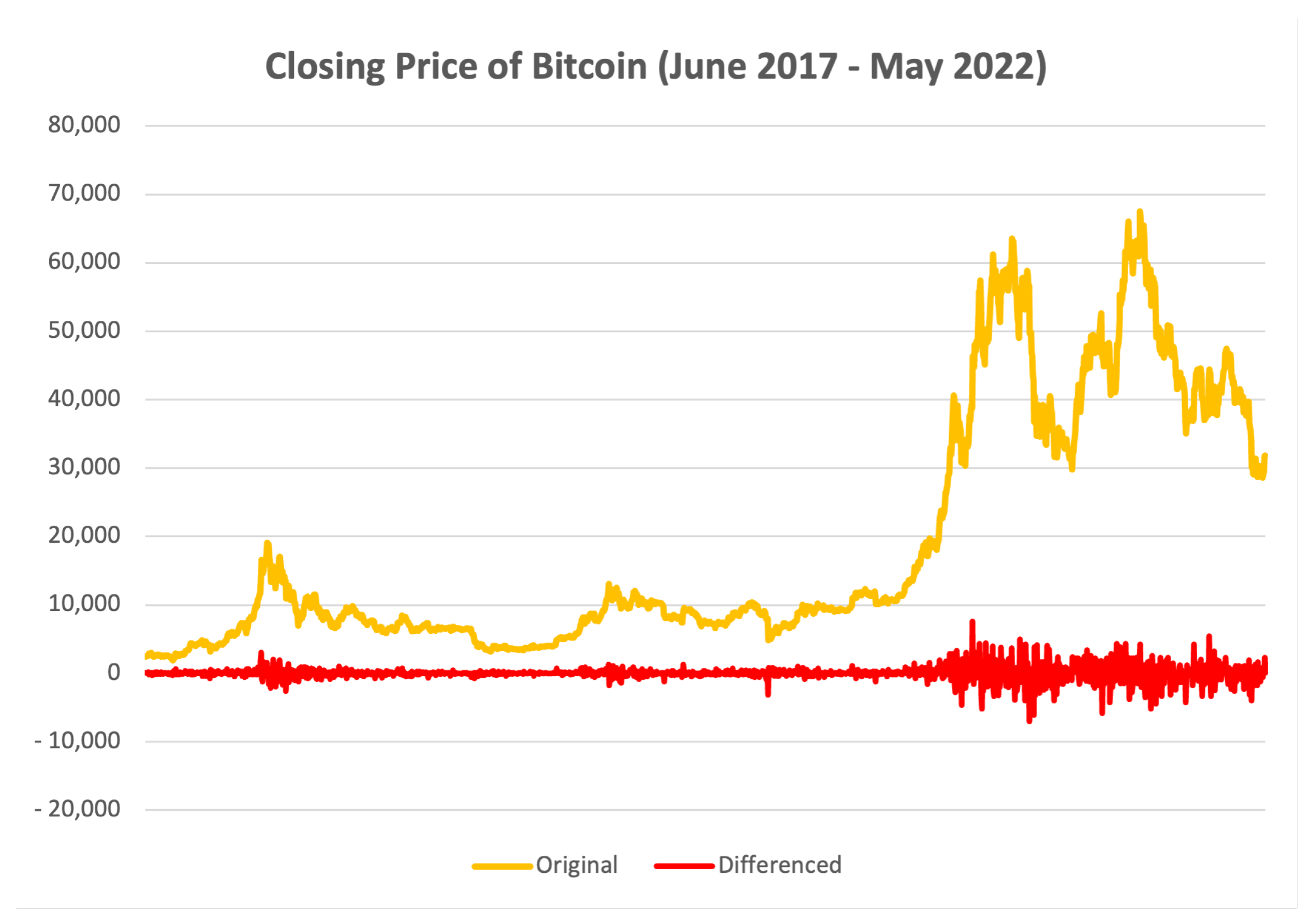

2.3. Data Pre-Processing

2.4. Experimental Methodology

2.5. Evaluation Metrics

3. Results

3.1. Individual Models

3.2. Ensembles

4. Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A. The Hyperparameter Values of the Predictive Models

{kind=link}

| Model | Python Library | Architecture | Hyperparameters Used |

|---|---|---|---|

| LSTM | TensorFlow | Single Convolutional Layer and a LSTM Layer. |

|

| GRU | TensorFlow | Single GRU Layer and Dense Layer. |

|

| LSTM-GRU Hybrid | TensorFlow | Two LSTM Layers and a GRU Layer. |

|

| TCN | TensorFlow | Four Convolutional Layers |

|

| TFT | DARTS |

| |

| RF | Scikit-Learn |

| |

| SVR | Scikit-Learn |

| |

| kNN | Scikit-Learn |

| |

| ARIMA | StatsModel |

|

References

- Cryptocurrency Prices, Charts and Market Capitalizations. Available online: https://coinmarketcap.com/ (accessed on 25 November 2022).

- Bouri, E.; Shahzad, S.J.H.; Roubaud, D. Co-explosivity in the cryptocurrency market. Financ. Res. Lett. 2019, 29, 178–183. [Google Scholar] [CrossRef]

- Fang, F.; Ventre, C.; Basios, M.; Kanthan, L.; Martinez-Rego, D.; Wu, F.; Li, L. Cryptocurrency trading: A comprehensive survey. Financ. Innov. 2022, 8, 13. [Google Scholar] [CrossRef]

- Ariyo, A.A.; Adewumi, A.O.; Ayo, C.K. Stock Price Prediction Using the ARIMA Model. In Proceedings of the 2014 UKSim-AMSS 16th International Conference on Computer Modelling and Simulation, Cambridge, UK, 26–28 March 2014; pp. 106–112. [Google Scholar] [CrossRef] [Green Version]

- Livieris, I.E.; Kiriakidou, N.; Stavroyiannis, S.; Pintelas, P. An Advanced CNN-LSTM Model for Cryptocurrency Forecasting. Electronics 2021, 10, 287. [Google Scholar] [CrossRef]

- Wirawan, I.M.; Widiyaningtyas, T.; Hasan, M.M. Short Term Prediction on Bitcoin Price Using ARIMA Method. In Proceedings of the 2019 International Seminar on Application for Technology of Information and Communication (iSemantic), Semarang, Indonesia, 21–22 September 2019; pp. 260–265. [Google Scholar] [CrossRef]

- Lahmiri, S.; Bekiros, S. Cryptocurrency forecasting with deep learning chaotic neural networks. Chaos Solitons Fractals 2019, 118, 35–40. [Google Scholar] [CrossRef]

- Adegboruwa, T.I.; Adeshina, S.A.; Boukar, M.M. Time Series Analysis and prediction of bitcoin using Long Short Term Memory Neural Network. In Proceedings of the 2019 15th International Conference on Electronics, Computer and Computation (ICECCO), Abuja, Nigeria, 10–12 December 2019; pp. 1–5. [Google Scholar] [CrossRef]

- Tandon, S.; Tripathi, S.; Saraswat, P.; Dabas, C. Bitcoin Price Forecasting using LSTM and 10-Fold Cross validation. In Proceedings of the 2019 International Conference on Signal Processing and Communication (ICSC), Noida, India, 7–9 March 2019; pp. 323–328. [Google Scholar] [CrossRef]

- Hamayel, M.J.; Owda, A.Y. A Novel Cryptocurrency Price Prediction Model Using GRU, LSTM and bi-LSTM Machine Learning Algorithms. AI 2021, 2, 477–496. [Google Scholar] [CrossRef]

- Patel, M.M.; Tanwar, S.; Gupta, R.; Kumar, N. A Deep Learning-based Cryptocurrency Price Prediction Scheme for Financial Institutions. J. Inf. Secur. Appl. 2020, 55, 102583. [Google Scholar] [CrossRef]

- De Gooijer, J.G.; Hyndman, R.J. 25 years of time series forecasting. Int. J. Forecast. 2006, 22, 443–473. [Google Scholar] [CrossRef] [Green Version]

- Box, G.E.P.; Jenkins, G.M. Time Series Analysis: Forecasting and Control; Holden-Day: San Francisco, CA, USA, 1976. [Google Scholar]

- Yamak, P.T.; Yujian, L.; Gadosey, P.K. A Comparison between ARIMA, LSTM, and GRU for Time Series Forecasting. In Proceedings of the 2019 2nd International Conference on Algorithms, Computing and Artificial Intelligence, Sanya, China, 20–22 December 2019; Association for Computing Machinery: New York, NY, USA, 2020; pp. 49–55. [Google Scholar] [CrossRef]

- Roy, S.; Nanjiba, S.; Chakrabarty, A. Bitcoin Price Forecasting Using Time Series Analysis. In Proceedings of the 2018 21st International Conference of Computer and Information Technology (ICCIT), Dhaka, Bangladesh, 21–23 December 2018; pp. 1–5. [Google Scholar] [CrossRef]

- Walther, T.; Klein, T.; Bouri, E. Exogenous drivers of Bitcoin and Cryptocurrency volatility – A mixed data sampling approach to forecasting. J. Int. Financ. Mark. Inst. Money 2019, 63, 101133. [Google Scholar] [CrossRef]

- Maciel, L. Cryptocurrencies value-at-risk and expected shortfall: Do regime-switching volatility models improve forecasting? Int. J. Financ. Econ. 2021, 26, 4840–4855. [Google Scholar] [CrossRef]

- Mba, J.C.; Mwambi, S.M.; Pindza, E. A Monte Carlo Approach to Bitcoin Price Prediction with Fractional Ornstein–Uhlenbeck Lévy Process. Forecasting 2022, 4, 409–419. [Google Scholar] [CrossRef]

- Derbentsev, V.; Babenko, V.; Khrustalev, K.; Obruch, H.; Khrustalova, S. Comparative performance of machine learning ensemble algorithms for forecasting cryptocurrency prices. Int. J. Eng. 2021, 34, 140–148. [Google Scholar]

- Chevallier, J.; Guégan, D.; Goutte, S. Is It Possible to Forecast the Price of Bitcoin? Forecasting 2021, 3, 377–420. [Google Scholar] [CrossRef]

- Khedr, A.M.; Arif, I.; El-Bannany, M.; Alhashmi, S.M.; Sreedharan, M. Cryptocurrency price prediction using traditional statistical and machine-learning techniques: A survey. Intell. Syst. Account. Financ. Manag. 2021, 28, 3–34. [Google Scholar] [CrossRef]

- Brownlee, J. Deep Learning for Time Series Forecasting: Predict the Future with MLPs, CNNs and LSTMs in Python; Machine Learning Mastery: San Juan, PR, USA, 2018. [Google Scholar]

- Andreoni, A.; Postorino, M.N. Time Series Models to Forecast Air Transport Demand: A Study about a Regional Airport. IFAC Proc. Vol. 2006, 39, 101–106. [Google Scholar] [CrossRef]

- Lim, C.; McAleer, M. Time series forecasts of international travel demand for Australia. Tour. Manag. 2002, 23, 389–396. [Google Scholar] [CrossRef]

- Lorek, K.S.; Lee Willinger, G. An analysis of the accuracy of long-term earnings predictions. Adv. Account. 2002, 19, 161–175. [Google Scholar] [CrossRef]

- Contreras, J.; Espínola, R.; Nogales, F.; Conejo, A. ARIMA models to predict next-day electricity prices. IEEE Trans. Power Syst. 2003, 18, 1014–1020. [Google Scholar] [CrossRef]

- Iqbal, M.; Iqbal, M.; Jaskani, F.; Iqbal, K.; Hassan, A. Time-Series Prediction of Cryptocurrency Market using Machine Learning Techniques. EAI Endorsed Trans. Creat. Technol. 2021, 8, e4. [Google Scholar] [CrossRef]

- Ban, T.; Zhang, R.; Pang, S.; Sarrafzadeh, A.; Inoue, D. Referential kNN regression for financial time series forecasting. Lect. Notes Comput. Sci. (Incl. Subser. Lect. Notes Artif. Intell. Lect. Notes Bioinform.) 2013, 8226, 601–608. [Google Scholar] [CrossRef]

- Troncoso Lora, A.; Santos, J.; Santos, J.; Ramos, J.; Expósito, A. Electricity market price forecasting: Neural networks versus weighted-distance k Nearest Neighbours. Lect. Notes Comput. Sci. (Incl. Subser. Lect. Notes Artif. Intell. Lect. Notes Bioinform.) 2002, 2453, 321–330. [Google Scholar]

- Huang, W. KNN Virtual Currency Price Prediction Model Based on Price Trend Characteristics. In Proceedings of the 2022 IEEE 2nd International Conference on Power, Electronics and Computer Applications (ICPECA), Shenyang, China, 21–23 January 2022; pp. 537–542. [Google Scholar] [CrossRef]

- Vapnik, V. The Nature of Statistical Learning Theory; Springer Science & Business Media: Berlin, Germany, 1995. [Google Scholar]

- Wu, S.; Akbarov, A. Support vector regression for warranty claim forecasting. Eur. J. Oper. Res. 2011, 213, 196–204. [Google Scholar] [CrossRef] [Green Version]

- Bunescu, R.; Struble, N.; Marling, C.; Shubrook, J.; Schwartz, F. Blood glucose level prediction using physiological models and support vector regression. In Proceedings of the 2013 12th International Conference on Machine Learning and Applications, Miami, FL, USA, 4–7 December 2013; Volume 1, pp. 135–140. [Google Scholar] [CrossRef]

- Xia, Y.; Liu, Y.; Chen, Z. Support Vector Regression for prediction of stock trend. In Proceedings of the 2013 6th International Conference on Information Management, Innovation Management and Industrial Engineering, Xi’an, China, 23–24 November 2013; Volume 2, pp. 123–126. [Google Scholar] [CrossRef]

- Naing, W.; Htike, Z. Forecasting of monthly temperature variations using random forests. ARPN J. Eng. Appl. Sci. 2015, 10, 10109–10112. [Google Scholar]

- Liu, Y.; Sarabi, A.; Zhang, J.; Naghizadeh, P.; Karir, M.; Bailey, M.; Liu, M. Cloudy with a chance of breach: Forecasting cyber security incidents. In Proceedings of the 24th USENIX Security Symposium, Washington, DC, USA, 12–14 August 2015; pp. 1009–1024. [Google Scholar]

- Zagorecki, A. Prediction of methane outbreaks in coal mines from multivariate time series using random forest. Lect. Notes Comput. Sci. (Incl. Subser. Lect. Notes Artif. Intell. Lect. Notes Bioinform.) 2015, 9437, 494–500. [Google Scholar] [CrossRef]

- Hochreiter, S.; Schmidhuber, J. Long Short-Term Memory. Neural Comput. 1997, 9, 1735–1780. [Google Scholar] [CrossRef] [PubMed]

- Ma, X.; Tao, Z.; Wang, Y.; Yu, H.; Wang, Y. Long short-term memory neural network for traffic speed prediction using remote microwave sensor data. Transp. Res. Part C Emerg. Technol. 2015, 54, 187–197. [Google Scholar] [CrossRef]

- Pham, T.; Tran, T.; Phung, D.; Venkatesh, S. Predicting healthcare trajectories from medical records: A deep learning approach. J. Biomed. Inform. 2017, 69, 218–229. [Google Scholar] [CrossRef]

- Solgi, R.; Loáiciga, H.A.; Kram, M. Long short-term memory neural network (LSTM-NN) for aquifer level time series forecasting using in-situ piezometric observations. J. Hydrol. 2021, 601, 126800. [Google Scholar] [CrossRef]

- Wang, B.; Kim, I. Short-term prediction for bike-sharing service using machine learning. Transp. Res. Procedia 2018, 34, 171–178. [Google Scholar] [CrossRef]

- Troia, S.; Alvizu, R.; Zhou, Y.; Maier, G.; Pattavina, A. Deep Learning-Based Traffic Prediction for Network Optimization. In Proceedings of the 2018 International Conference on Transparent Optical Networks, Bucharest, Romania, 1–5 July 2018. [Google Scholar] [CrossRef] [Green Version]

- Becerra-Rico, J.; Aceves-Fernández, M.; Esquivel-Escalante, K.; Pedraza-Ortega, J. Airborne particle pollution predictive model using Gated Recurrent Unit (GRU) deep neural networks. Earth Sci. Inform. 2020, 13, 821–834. [Google Scholar] [CrossRef]

- Muhammad, A.U.; Yahaya, A.S.; Kamal, S.M.; Adam, J.M.; Muhammad, W.I.; Elsafi, A. A Hybrid Deep Stacked LSTM and GRU for Water Price Prediction. In Proceedings of the 2020 2nd International Conference on Computer and Information Sciences (ICCIS), Sakaka, Saudi Arabia, 13–15 October 2020; pp. 1–6. [Google Scholar] [CrossRef]

- Bai, S.; Kolter, J.Z.; Koltun, V. An Empirical Evaluation of Generic Convolutional and Recurrent Networks for Sequence Modeling. arXiv 2018, arXiv:1803.01271. [Google Scholar]

- Zhu, R.; Liao, W.; Wang, Y. Short-term prediction for wind power based on temporal convolutional network. Energy Rep. 2020, 6, 424–429. [Google Scholar] [CrossRef]

- Ardimento, P.; Aversano, L.; Bernardi, M.L.; Cimitile, M.; Iammarino, M. Temporal convolutional networks for just-in-time design smells prediction using fine-grained software metrics. Neurocomputing 2021, 463, 454–471. [Google Scholar] [CrossRef]

- Zhang, C.X.; Li, J.; Huang, X.F.; Zhang, J.S.; Huang, H.C. Forecasting stock volatility and value-at-risk based on temporal convolutional networks. Expert Syst. Appl. 2022, 207, 117951. [Google Scholar] [CrossRef]

- Politis, A.; Doka, K.; Koziris, N. Ether Price Prediction Using Advanced Deep Learning Models. In Proceedings of the 2021 IEEE International Conference on Blockchain and Cryptocurrency (ICBC), Sydney, Australia, 3–6 May 2021; pp. 1–3. [Google Scholar] [CrossRef]

- Lim, B.; Arık, S.O.; Loeff, N.; Pfister, T. Temporal Fusion Transformers for interpretable multi-horizon time series forecasting. Int. J. Forecast. 2021, 37, 1748–1764. [Google Scholar] [CrossRef]

- Srivastava, A.; Cano, A. Analysis and forecasting of rivers pH level using deep learning. Prog. Artif. Intell. 2022, 11, 181–191. [Google Scholar] [CrossRef]

- Wang, L.; Mykityshyn, A.; Johnson, C.; Cheng, J. Flight Demand Forecasting with Transformers. arXiv 2021, arXiv:2111.04471. [Google Scholar]

- Civitarese, D.S.; Szwarcman, D.; Zadrozny, B.; Watson, C. Extreme Precipitation Seasonal Forecast Using a Transformer Neural Network. arXiv 2021, arXiv:2107.06846. [Google Scholar]

- Shah, I.; Jan, F.; Ali, S. Functional data approach for short-term electricity demand forecasting. Math. Probl. Eng. 2022, 2022, 6709779. [Google Scholar] [CrossRef]

- Shah, I.; Iftikhar, H.; Ali, S. Modeling and forecasting electricity demand and prices: A comparison of alternative approaches. J. Math. 2022, 2022, 3581037. [Google Scholar] [CrossRef]

- Sopelsa Neto, N.F.; Stefenon, S.F.; Meyer, L.H.; Ovejero, R.G.; Leithardt, V.R.Q. Fault Prediction Based on Leakage Current in Contaminated Insulators Using Enhanced Time Series Forecasting Models. Sensors 2022, 22, 6121. [Google Scholar] [CrossRef]

- Cheng, D.; Yang, F.; Xiang, S.; Liu, J. Financial time series forecasting with multi-modality graph neural network. Pattern Recognit. 2022, 121, 108218. [Google Scholar] [CrossRef]

- Hyndman, R.J.; Athanasopoulos, G. Forecasting: Principles and Practice, 2nd ed.; Springer: Berlin, Germany, 2018. [Google Scholar]

- Dixit, A.; Jain, S. Effect of stationarity on traditional machine learning models: Time series analysis. In Proceedings of the 2021 Thirteenth International Conference on Contemporary Computing (IC3-2021), Noida, India, 5–7 August 2021; Association for Computing Machinery: New York, NY, USA, 2021; pp. 303–308. [Google Scholar] [CrossRef]

- Dickey, D.A.; Fuller, W.A. Likelihood Ratio Statistics for Autoregressive Time Series with a Unit Root. Econometrica 1981, 49, 1057–1072. [Google Scholar] [CrossRef]

- Guo, T.; Bifet, A.; Antulov-Fantulin, N. Bitcoin Volatility Forecasting with a Glimpse into Buy and Sell Orders. In Proceedings of the 2018 IEEE International Conference on Data Mining (ICDM), Singapore, 17–20 November 2018; pp. 989–994. [Google Scholar] [CrossRef]

- Chokor, A.; Alfieri, E. Long and short-term impacts of regulation in the cryptocurrency market. Q. Rev. Econ. Financ. 2021, 81, 157–173. [Google Scholar] [CrossRef]

- Tanwar, S.; Patel, N.P.; Patel, S.N.; Patel, J.R.; Sharma, G.; Davidson, I.E. Deep Learning-Based Cryptocurrency Price Prediction Scheme With Inter-Dependent Relations. IEEE Access 2021, 9, 138633–138646. [Google Scholar] [CrossRef]

- Song, J.Y.; Chang, W.; Song, J.W. Cluster analysis on the structure of the cryptocurrency market via Bitcoin–Ethereum filtering. Phys. A Stat. Mech. Its Appl. 2019, 527, 121339. [Google Scholar] [CrossRef]

| Name | Release Year | Market Cap 1 | 24 h Volume 1 | Min Price 2 | Max Price 2 | Mean Price 2 | Price SD 2 |

|---|---|---|---|---|---|---|---|

| Bitcoin (BTC) | 2009 | 393.41 | 45.67 | 1914.10 | 67,525.83 | 18,621.99 | 17,623.38 |

| Etherium (ETH) | 2015 | 192.46 | 19.31 | 83.76 | 4807.98 | 1021.77 | 1220.11 |

| Litecoin (LTC) | 2011 | 3.93 | 0.53 | 23.08 | 387.80 | 101.41 | 64.33 |

| Monero (XMR) | 2014 | 2.71 | 0.09 | 29.20 | 484.00 | 142.39 | 90.43 |

| XRP (XRP) | 2012 | 22.96 | 0.96 | 0.14 | 2.78 | 0.51 | 0.36 |

| Model | RMSE | MAE | MAPE | R2 | Train (s) | Inference (ms) |

|---|---|---|---|---|---|---|

| LSTM | 0.02224 | 0.0173 | 3.862% | 0.735 | 173.765 | 1.862 |

| GRU | 0.02285 | 0.0176 | 3.939% | 0.720 | 254.520 | 1.550 |

| HYBRID | 0.02295 | 0.0177 | 3.959% | 0.717 | 461.967 | 2.383 |

| KNN | 0.02332 | 0.0179 | 4.003% | 0.711 | <0.01 | 0.074 |

| TCN | 0.02334 | 0.0180 | 4.021% | 0.711 | 40.475 | 1.219 |

| ARIMA | 0.02343 | 0.0180 | 4.010% | 0.708 | 4.035 | 0.109 |

| TFT | 0.02353 | 0.0181 | 4.062% | 0.707 | 105.913 | 8.842 |

| RF | 0.02402 | 0.0184 | 4.095% | 0.697 | 2.121 | 0.586 |

| SVR | 0.02452 | 0.0189 | 4.240% | 0.681 | <0.01 | 0.008 |

| BTC | ETH | LTC | XMR | XRP | Average | |

|---|---|---|---|---|---|---|

| LSTM | 0.0239 (1) | 0.030 (1) | 0.0189 (1) | 0.0236 (1) | 0.0148 (1) | 0.0222 (1) |

| GRU | 0.0245 (2) | 0.0309 (2) | 0.0193 (2) | 0.0243 (2) | 0.0153 (2) | 0.0229 (2) |

| HYBRID | 0.0246 (3) | 0.0309 (3) | 0.0195 (3) | 0.0244 (3) | 0.0154 (3) | 0.0230 (3) |

| KNN | 0.0249 (6) | 0.0319 (5) | 0.0197(4) | 0.0245 (5) | 0.0155 (4) | 0.0233 (4) |

| TCN | 0.0250 (7) | 0.0319 (4) | 0.0198 (5) | 0.0245 (6) | 0.0156 (5) | 0.0233 (5) |

| ARIMA | 0.0251 (8) | 0.0320 (7) | 0.0198 (6) | 0.0244 (4) | 0.0158 (7) | 0.0234 (6) |

| TFT | 0.0249 (5) | 0.0319 (6) | 0.0199 (7) | 0.0250 (7) | 0.0159 (8) | 0.0235 (7) |

| RF | 0.0266 (9) | 0.0332 (8) | 0.0199 (8) | 0.0251 (8) | 0.0157 (6) | 0.0240 (8) |

| SVR | 0.0248 (4) | 0.0342 (9) | 0.0207 (9) | 0.0268 (9) | 0.0160 (9) | 0.0245 (9) |

| Ensemble | RMSE | MAE | MAPE | R2 |

|---|---|---|---|---|

| LSTM | 0.0222 | 0.0173 | 3.86% | 0.73 |

| GRU, LSTM | 0.0225 | 0.0174 | 3.89% | 0.73 |

| HYBRID, LSTM | 0.0225 | 0.0174 | 3.89% | 0.73 |

| HYBRID, GRU, LSTM | 0.0226 | 0.0175 | 3.90% | 0.73 |

| LSTM, KNN | 0.0227 | 0.0175 | 3.92% | 0.73 |

| GRU, LSTM, KNN | 0.0227 | 0.0176 | 3.91% | 0.72 |

| GRU, LSTM, TCN | 0.0227 | 0.0176 | 3.92% | 0.72 |

| LSTM, TCN | 0.0227 | 0.0176 | 3.93% | 0.72 |

| HYBRID, LSTM, KNN | 0.0227 | 0.0175 | 3.92% | 0.72 |

| HYBRID, GRU, LSTM, KNN | 0.0227 | 0.0175 | 3.91% | 0.72 |

| Model | RMSE with Model | RMSE without Model | Difference (%) 1 |

|---|---|---|---|

| LSTM | 0.023 | 0.0233 | 1.26% |

| GRU | 0.0231 | 0.0232 | 0.57% |

| HYBRID | 0.0231 | 0.0232 | 0.48% |

| KNN | 0.0232 | 0.0232 | −0.03% |

| TCN | 0.0232 | 0.0232 | −0.06% |

| ARIMA | 0.0232 | 0.0231 | −0.2% |

| TFT | 0.0232 | 0.0231 | −0.21% |

| RF | 0.0232 | 0.0231 | −0.41% |

| SVR | 0.0233 | 0.0231 | −0.87% |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Murray, K.; Rossi, A.; Carraro, D.; Visentin, A. On Forecasting Cryptocurrency Prices: A Comparison of Machine Learning, Deep Learning, and Ensembles. Forecasting 2023, 5, 196-209. https://doi.org/10.3390/forecast5010010

Murray K, Rossi A, Carraro D, Visentin A. On Forecasting Cryptocurrency Prices: A Comparison of Machine Learning, Deep Learning, and Ensembles. Forecasting. 2023; 5(1):196-209. https://doi.org/10.3390/forecast5010010

Chicago/Turabian StyleMurray, Kate, Andrea Rossi, Diego Carraro, and Andrea Visentin. 2023. "On Forecasting Cryptocurrency Prices: A Comparison of Machine Learning, Deep Learning, and Ensembles" Forecasting 5, no. 1: 196-209. https://doi.org/10.3390/forecast5010010