1. Introduction

Indonesia can be a country that builds infrastructure and manages its environment by utilizing the power of nature as its resource. In 2021, Indonesia had a cultivation fishery production target of around 19.47 million tons, consisting of 7.92 million tons of fish and 11.55 million tons of seaweed; this was an increase of 1.03 million tons from the 2020 production target of 18.44 million tons [

1]. Indonesia has an estimated potential for fish resources, the number of allowable catches (JTB), and the level of utilization of fish resources, in its 11 regions, with a total estimated value of fish resource potential of 12.01 million tons per year with a JTB of 8.6 million tons per year [

2].

Indonesia is only one of the maritime countries in the world. Complete data and information about marine ecosystems in the world can be obtained from [

3]:

Marine Spatial Planning by assessing ecosystem resilience, the roles of various stakeholders, policies, and institutions.

Blue Natural Capital Accounting and Economic Analysis that identifies the value of blue natural resource capital or assets, and the other potentials for increasing income and employment, by calculating the distribution of current and potential benefits to people associated with the blue economy.

The marine ecosystem approach is the key to ocean sustainability and resilience. Information that describes the current state of ecosystems and seascape economies, as well as the specific policies, roles of stakeholders, and institutions that determine the use and design of the policies/institutional reforms needed to manage the transition to a Blue Economy. In addition, innovative financing is needed to implement these reforms.

The development of the marine aquaculture sector frequently relies on well-known opportunity discourses that highlight unrealized economic growth possibilities. This discourse also serves as the foundation for the more expansive idea of the Blue Economy, which places the ocean at the forefront of economic growth. Aquaculture is seen as a crucial component of the Blue Economy [

4].

This information must show the value of the economic benefits from better blue natural asset management; how much revenue/rent potential is lost due to poor management; how much income could be increased through better management, including adaptation measures for climate change; could the fiscal costs of natural disasters be reduced by managing nature-based infrastructure for resilience; how many jobs and incomes increase with better management of the fishery; and who is affected by the policy changes.

The conceptual framework of accounting must provide the following useful information to blue economy stakeholders.

2. Methods

This research aims to account for the value of assets and natural resource capital in the blue economy in Indonesia, by collecting written data from various research paper sources, and utilizing fisheries’ statistics. This research reviewed the literature to identify available evidence and data. Then, the data were reviewed and analyzed to propose a conceptual framework of accounting to measure the value of blue economy in Indonesia.

This research includes all articles about the blue economy and ocean, or blue accounting articles, published between 2010 and 2022, without geographical limitations.

3. Result

There are different terms used in several articles which focus on accounting in marine or sea contexts. Some articles use the term ocean accounting, and others use the term blue accounting. Blue accounting focuses on the life of marine ecosystems, which cover 72% of the entire planet Earth. Blue accounting has highlighted sustainability, which means meeting the needs of the present generation without forgetting the future generations [

5].

The Ocean Accounts Framework adapted international statistical standards to perform measures of ocean accounting; these included the System of National Accounts (SNA), the System of Environmental Economic Accounting (SEEA), National Spatial Data Infrastructure (NSDI), and The Framework for the Development of Environment Statistics (FDES). The SNA provides various recommendations on how to compile monetary measures of economic activity, including a coherent, consistent, and integrated set of macroeconomic accounts. It summarizes economic processes, how production is distributed among consumers, businesses, governments, and foreign countries. The SNA account is one of the fundamental building blocks of macroeconomic statistics that forms the basis for economic analysis, and policy formulation for Ocean Accounts [

6].

The reporting of ocean accounting cannot be separated from international commitments; seventeen Sustainable Development Goals (SDG) are aimed to be met by 2030, especially SDG 14 (life below water), SDG 15 (life on land which calls for the integration of ecosystem and biodiversity values into national and local planning, development processes, poverty reduction strategies, and accounts by 2020), and SDG 17 (partnership for the goals, which calls for efforts building on existing initiatives to develop measurements of progress on sustainable development that complement gross domestic product, and support statistical capacity building in developing countries by 2030) [

7].

Ocean accounting or blue accounting reporting must also refer to the financial reporting conceptual framework. The basic conceptual framework, in accounting of financial reporting, includes definitions of an asset, a liability, equity, income and expenses, and guidance supporting these definitions: criteria for including assets and liabilities in financial statements (recognition), and guidance on when to remove them (derecognition); measurement bases and guidance on when to use them; concepts and guidance on presentation and disclosure; and concepts relating to capital, and capital maintenance [

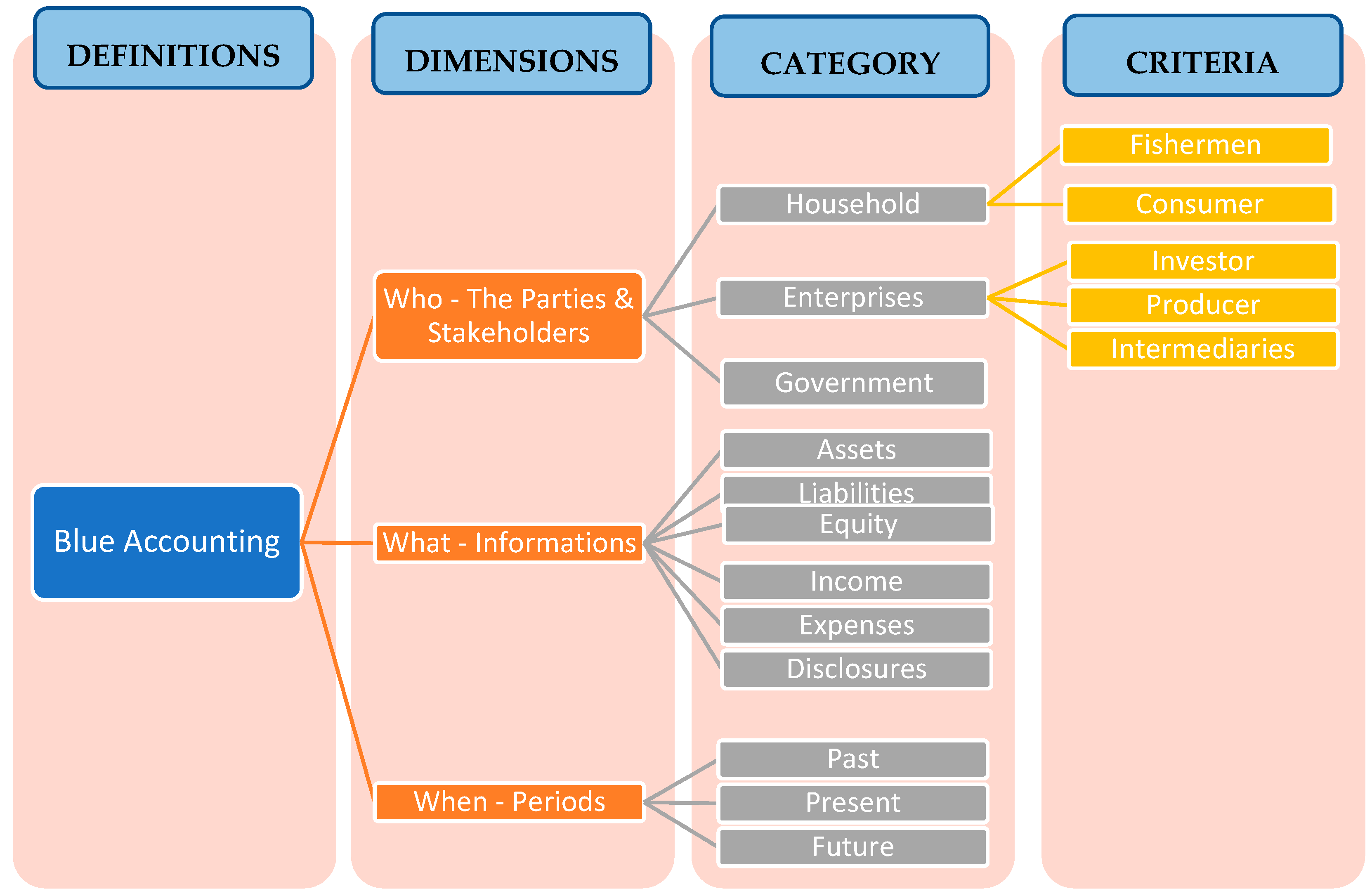

8]. Researchers compile the conceptual of blue accounting in

Figure 1.

This figure should be explained in more detail regarding how blue accounting can be interpreted into an accounting report. The key strength of blue accounting is data management, where the digital revolution is needed to change the way people interact with data. Blue accounting must use ‘big data’ and detailed business statistical data from various sources, so that research on blue accounting can be continued. However, the national blue accounting reporting must change the paradigm by using a revolutionary online digital dashboard, so that the data can be integrated in real time and be up to date. The other challenge of blue accounting focuses on how to disclose the three types of sustainability (SDGs) by providing a transparent and useful reporting framework for all stakeholders involved [

9].

4. Discussions

The ocean must be fully measured in the digital system or ‘big data’ to enable decision-makers around the world to use the ocean’s present day information to conserve, restore, or enhance it for the global future The complexity of the blue economy cannot be managed by one indicator alone. Complete information obtained by blue accounting includes three high-level key indicators, first is ocean products, changes in ocean balance, and ocean revenues in a period [

10].

First, we discuss who the related parties or the stakeholders are in blue accounting. We divide them into three categories of parties related to blue accounting, namely households, government, and enterprises. Households consist of fishermen and consumers. The government is divided into two parties: the first party are those who make blue accounting reports, and the second party are those who make the policies and regulations for the blue economy. The enterprises is divided into three, the first is a company that acts as an investor, the second is a company that acts as a producer, and the third is a company that acts as an intermediary.

Marine ecosystems, as “integrated assets”, recognize the ocean product, which is the ocean, as more than a source of fish; they recognize the importance of coastal protection, carbon sequestration, and climate regulation and recreation, including mangrove forests and coral reefs. The ocean product is a part of the blue accounting assets. The funding from investors and creditors will change in the ocean balance sheet, while ocean income is generated from ocean productivity. The expenditure of blue accounting includes expenses for research and development, education, environmental protection, and expenses and maintenance for resource management. Stakeholders need other information that must be disclosed, especially about the SDGs (SDG 14, SDG 15 and SDG 17). Disclosure of information in blue accounting is very important. The components of the blue accounting form can be seen in

Table 1.

Blue accounting reports are needed throughout the year, regardless of whether they are needed regarding current data, past data, or even future data. Therefore, a revolution in providing digital data is needed, so it can create big data in blue accounting.

5. Conclusions

Blue accounting is a new challenge for accountants around the world. Blue economy accountants are expected can compile ocean ecosystem data into financial reports, they also need to identify and reporting all blue economy calculations. As the ocean environment has significant changes, the accountants need to be a strategic role in an organizational, can quantify ocean big data in a blue economy. Blue accounting can be measured by the digital revolution of data.

Author Contributions

Conceptualization, A.Y.R. and D.K.S.; methodology, A.Y.R.; software, A.Y.R.; validation, A.Y.R.; formal analysis, A.Y.R. and D.K.S.; investigation, A.Y.R.; resources, A.Y.R.; data curation, A.Y.R.; writing—original draft preparation, A.Y.R.; writing—review and editing, A.Y.R.; visualization, A.Y.R. All authors have read and agreed to the published version of the manuscript.

Funding

This Research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Marine and Fisheries Ministry, Republik Indonesia. Aquaculture Fisheries Priority Targets and Programs in 2021. 28 December 2021. Available online: https://kkp.go.id/artikel/25859-target-dan-progam-prioritas-perikanan-budidaya-tahun-2021 (accessed on 5 March 2022).

- Marine and Fisheries Ministry, Directorate General of Capture Fisheries. KKP Updates Fish Potential Estimation Data 2022. 6 April 2022. Available online: https://kkp.go.id/djpt/artikel/39646-kkp-perbarui-data-estimasi-potensi-ikan-totalnya-12-01-juta-ton-per-tahun (accessed on 5 March 2022).

- Lange, G.-M. Ocean Natural Capital Accounts and the Blue Economy; Global Dialogue on Ocean Accounting; The World Bank Group: Sydney, Australia, 2019. [Google Scholar]

- Campbell, L.M.; Fairbanks, L.; Murray, G.; Stoll, J.S.; D’Anna, L.; Bingham, J. From Blue Economy to Blue Communities: Reorienting aquaculture expansion for community wellbeing. Mar. Policy 2020, 124, 104361. [Google Scholar] [CrossRef]

- Syah, S.; Saraswati, E.; Sukoharsono, E.G.; Roekhudin. Blue Accounting and Sustainability. In Proceedings of the 23rd Asian Forum of Business Education (AFBE 2019), Bali, Indonesia, 12–13 December 2019. [Google Scholar]

- Technical Guidance on Ocean Accounting for Sustainable Development Preliminary Consultation Draft United Nations Economic and Social Commission for Asia and the Pacific in Collaboration with Institutional Members of the Global Ocean Accounts Partnership. 2019. Available online: https://www.oceanaccounts.org/technical-guidance-on-ocean-accounting-2/ (accessed on 5 March 2022).

- Fenichel, E.P.; Milligan, B.; Porras, I. National Accounting for the Ocean and Ocean Economy; Oceanpanel: Wahsington, DC, USA, 2020. [Google Scholar]

- Conceptual Framework for Financial Reporting. 2018. Available online: https://www.ifrs.org/issued-standards/list-of-standards/conceptual-framework/ (accessed on 5 March 2022).

- Shiiba, N.; Wu, H.H.; Huang, M.C.; Tanaka, H. How blue financing can sustain ocean conservation and development: A proposed conceptual framework for blue financing mechanism. Mar. Policy 2022, 139, 104575. [Google Scholar] [CrossRef]

- Fenichel, E.P. National Accounting for the Ocean and Ocean Economy Lead Authors about the High Level Panel for a Sustainable Ocean Economy; Oceanpanel: Wahsington, DC, USA, 2020. [Google Scholar]

| Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

{kind=link}