Investigation of COVID-19 Impact on the Food and Beverages Industry: China and India Perspective

,

,

Abstract

:

1. Introduction

Problem Statement and Research Objectives

- RO1: What is the scenario of the ongoing pandemic in China and India?

- RO2: What is the scale of research in different fields concerning COVID-19 carried out during the pandemic and ongoing in both nations?

- RO3: What is the scale of research on food and beverage commodities concerning COVID-19 in both nations?

- RO4: What is the impact of COVID-19 on the food and beverage industry in both nations concerning the following factors: loss of enterprises, growth in revenue (%), total profit (%), gross value added and growth value of exports (%)?

- RO5: Did COVID-19 bring a sudden change in consumer food behavior, digitalization, and technology advancement in both nations?

- RO6: Which strategies, policies, and responses were undertaken against COVID-19 for smooth operations of food supply chains by China and India?

- RO7: What is the future of China and India’s food and beverage industries post-pandemic?

2. Materials and Methods

3. Results

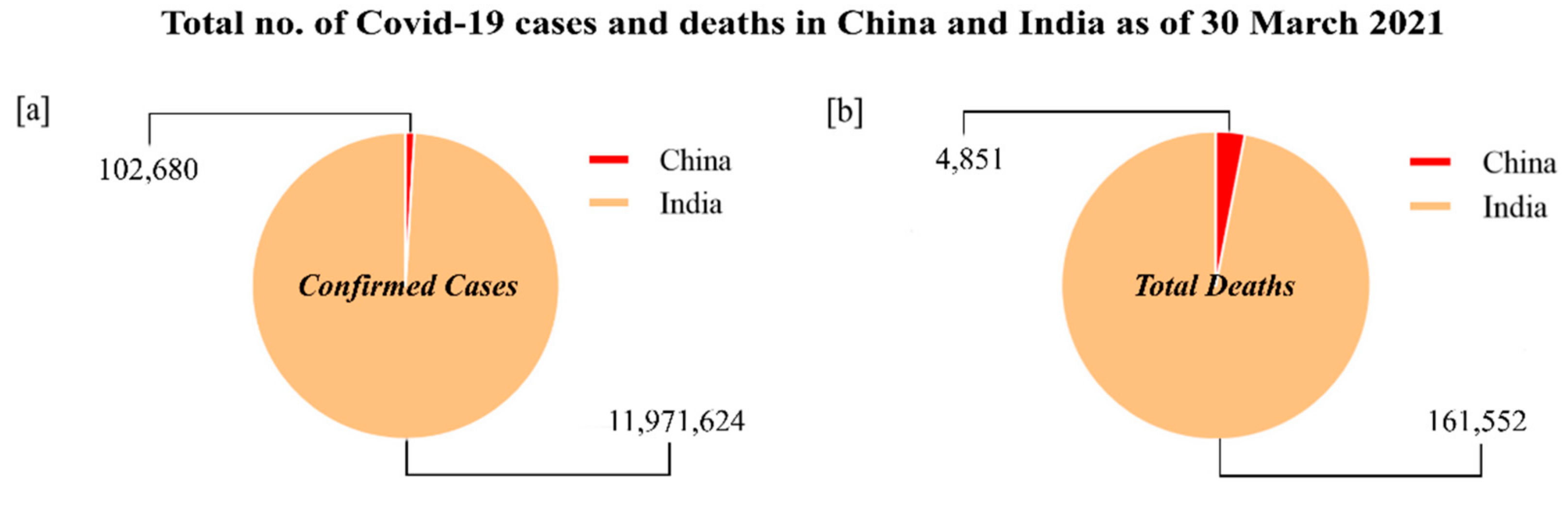

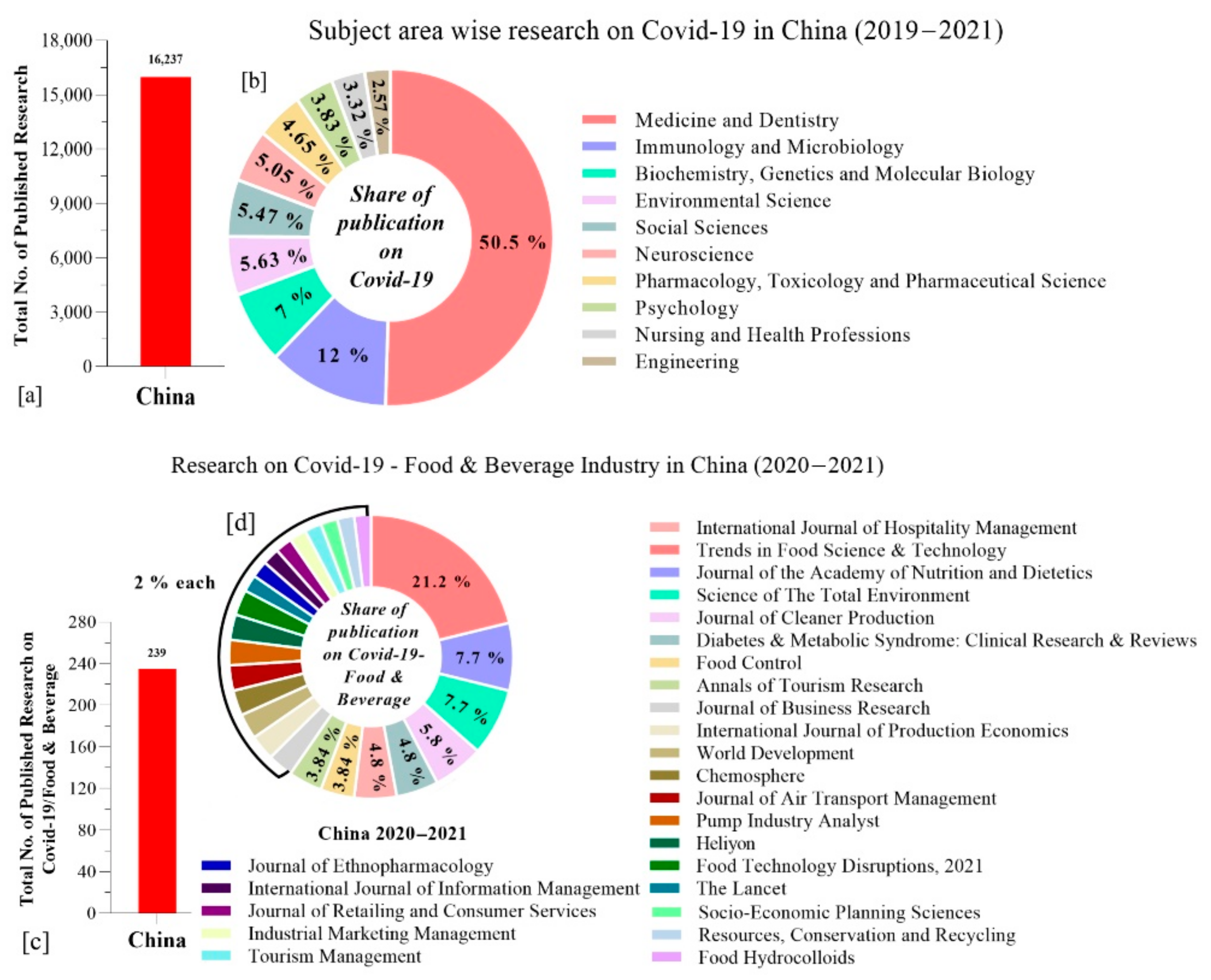

3.1. Research on COVID-19 in China

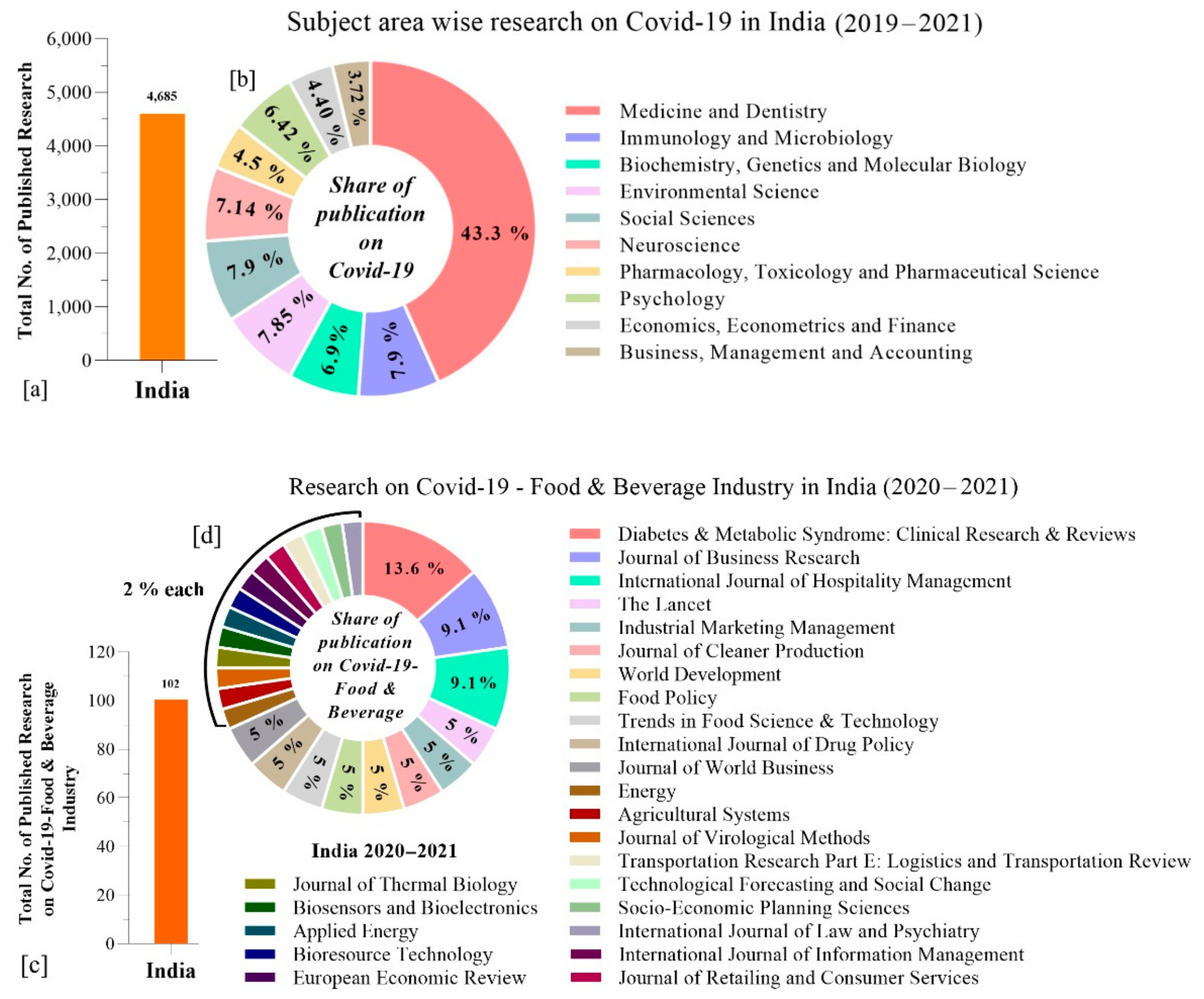

3.2. Research on COVID-19 in India

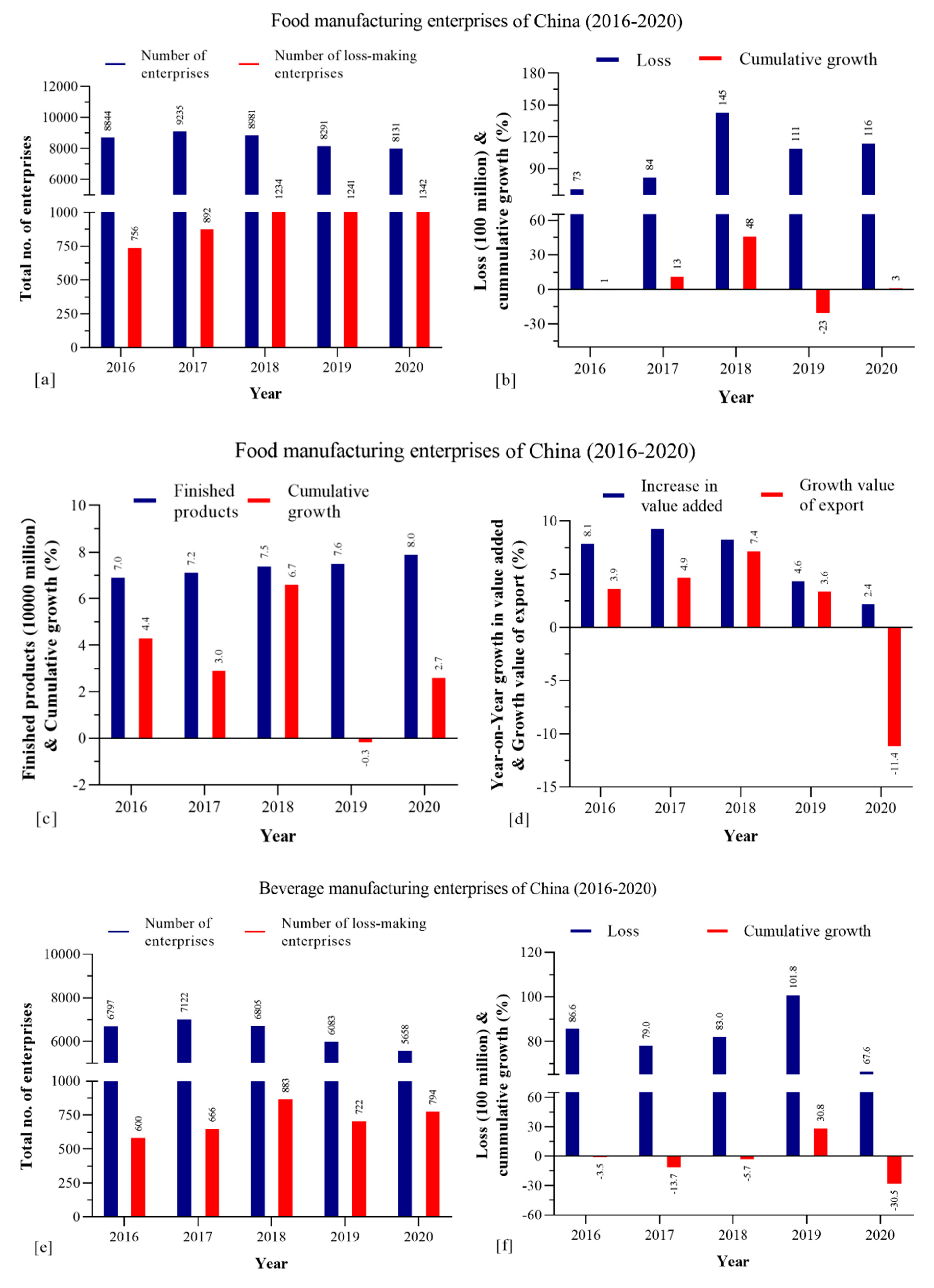

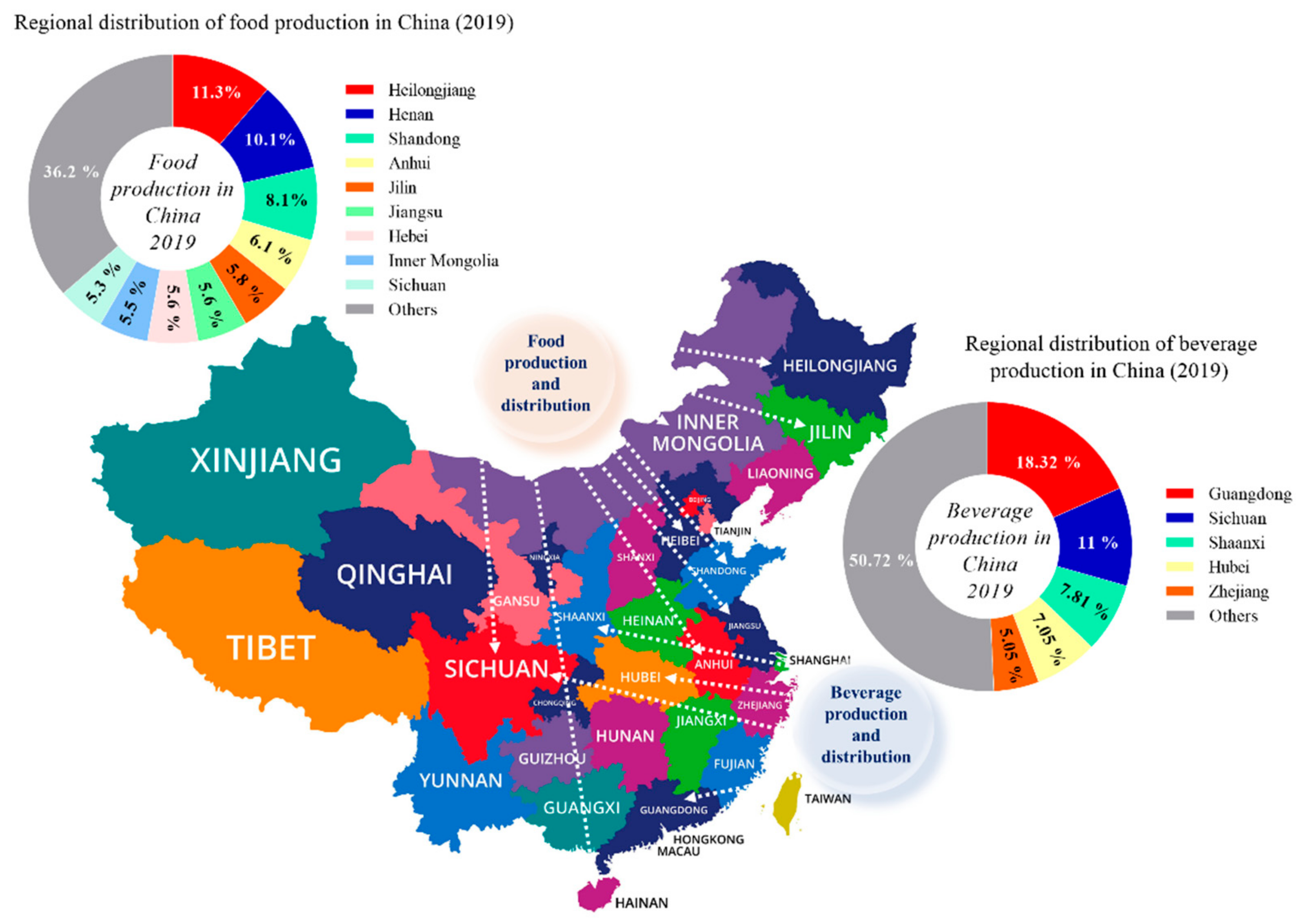

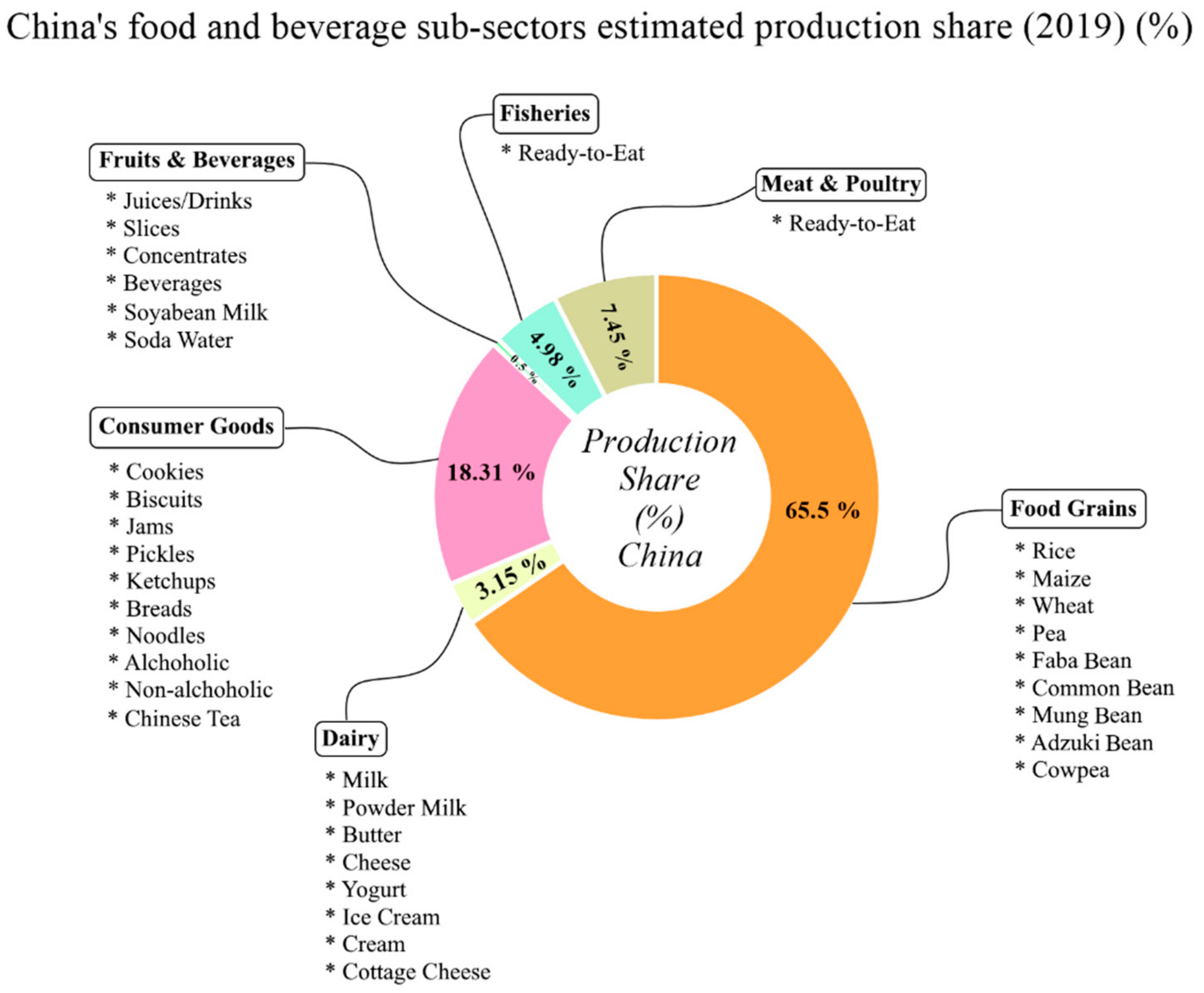

3.3. Food and Beverage Industry in China

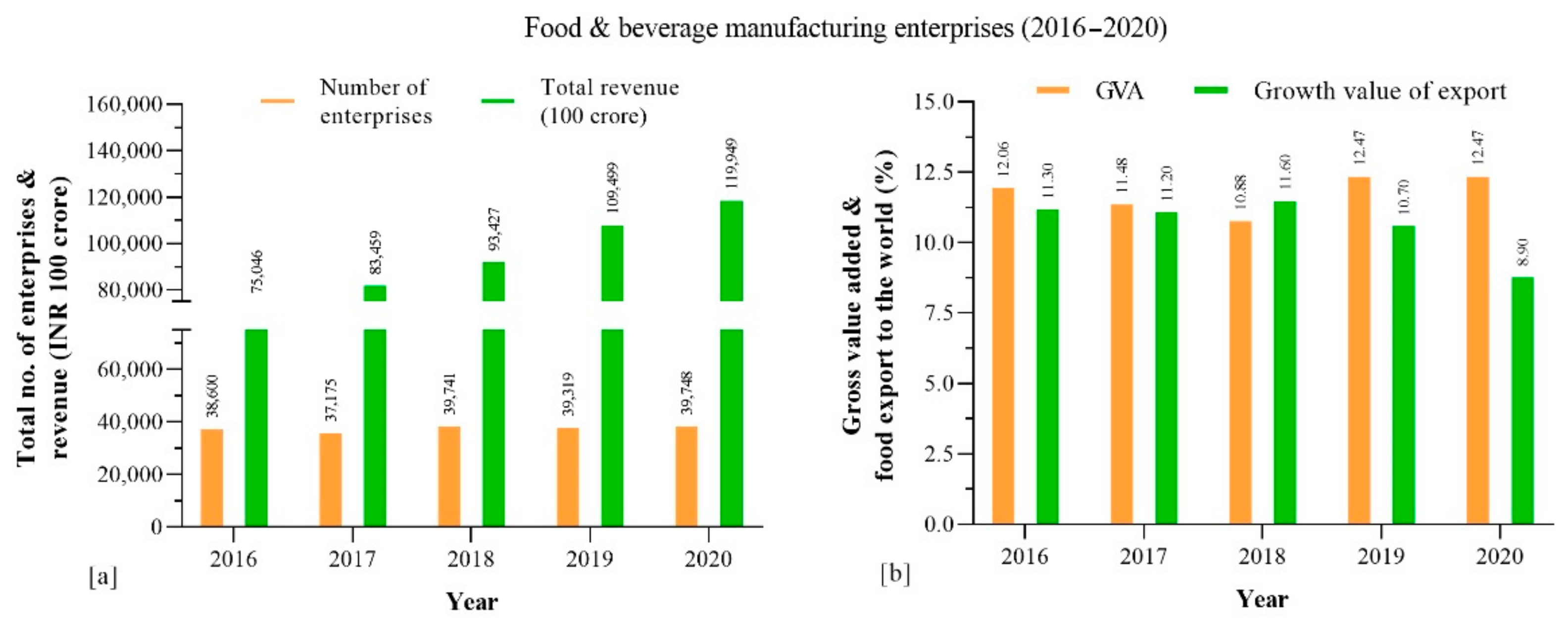

3.4. Food and Beverage Industry in India

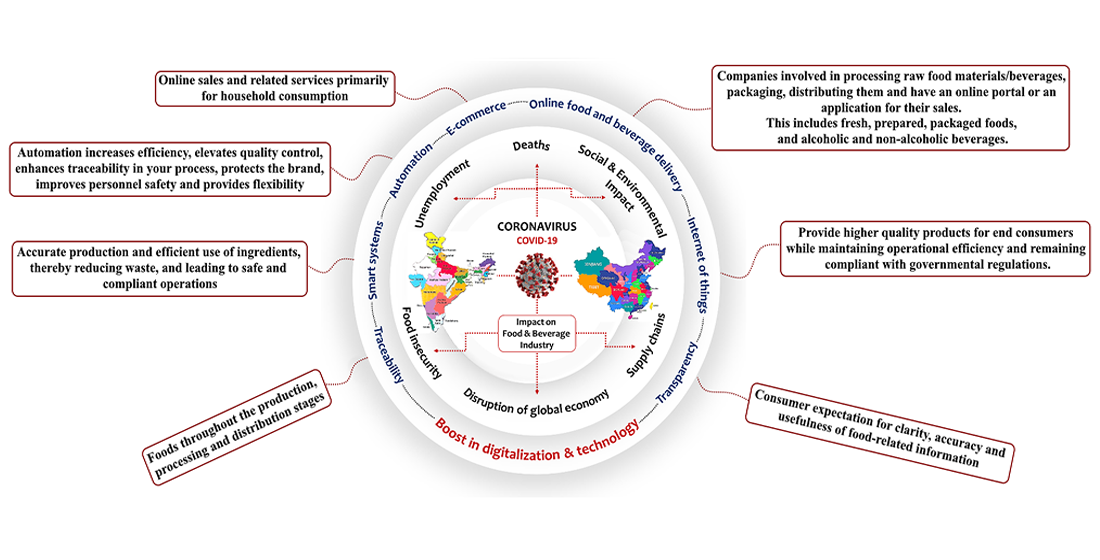

4. Discussion

4.1. Impacts of COVID-19 on Food and Beverage Industry in China and India

4.2. Food and Beverage Monitoring Safety Authority Organizations of China and India

4.3. Digitalization and Technological Advances in Food and Beverage Industries in China and India

4.3.1. Robotics

4.3.2. Drones and AI in China’s and India’s Food and Beverage Industry: Ensuring Transparency for the Customer

4.4. National Strategies, Policies, and Responses in COVID-19 Crisis

5. Future of Chinese and Indian Food and Beverage Industry Post-Pandemic

5.1. Hygiene Standards

5.2. Contactless Solutions

5.3. At-Home Experiences

5.4. Vegan and Healthy Food Brands

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Dey, S.K.; Rahman, M.M.; Siddiqi, U.R.; Howlader, A. Analyzing the epidemiological outbreak of COVID-19: A visual exploratory data analysis approach. J. Med. Virol. 2020, 92, 632–638. [Google Scholar] [CrossRef]

- Yoo, J.-H. The fight against the 2019-nCoV outbreak: An arduous march has just begun. J. Korean Med. Sci. 2020, 35, e56. [Google Scholar] [CrossRef]

- Ibrahim, I.M.; Abdelmalek, D.H.; Elshahat, M.E.; Elfiky, A.A. COVID-19 spike-host cell receptor GRP78 binding site prediction. J. Infect. 2020, 80, 554–562. [Google Scholar] [CrossRef] [PubMed]

- Gorbalenya, A.E.; Baker, S.C.; Baric, R.; Groot, R.J.d.; Drosten, C.; Gulyaeva, A.A.; Haagmans, B.L.; Lauber, C.; Leontovich, A.M.; Neuman, B.W. The species severe acute respiratory syndrome-related coronavirus: Classifying 2019-nCoV and naming it SARS-CoV-2. Nat. Microbiol. 2020, 5, 536–544. [Google Scholar]

- Wu, J.; Xie, X.; Yang, L.; Xu, X.; Cai, Y.; Wang, T.; Xie, X. Mobile health technology combats COVID-19 in China. J. Infect. 2021, 82, 159–198. [Google Scholar] [CrossRef]

- Avittathur, B.; Jayaram, J. Supply chain management in emerging economies. Decision 2016, 43, 117–124. [Google Scholar] [CrossRef]

- Bajpai, P. The 5 Largest Economies in the World and Their Growth in 2020. Available online: https://www.nasdaq.com/articles/the-5-largest-economies-in-the-world-and-their-growth-in-2020-2020-01-22 (accessed on 11 March 2021).

- Rothan, H.A.; Byrareddy, S.N. The epidemiology and pathogenesis of coronavirus disease (COVID-19) outbreak. J. Autoimmun. 2020, 109, 102433. [Google Scholar] [CrossRef] [PubMed]

- Amankwah-Amoah, J.; Khan, Z.; Wood, G. COVID-19 and business failures: The paradoxes of experience, scale, and scope for theory and practice. Eur. Manag. J. 2021, 39, 179–184. [Google Scholar] [CrossRef]

- Leite, H.; Hodgkinson, I.R.; Gruber, T. New development: ‘Healing at a distance’—Telemedicine and COVID-19. Public Money Manag. 2020, 40, 483–485. [Google Scholar] [CrossRef] [Green Version]

- Chowdhury, M.T.; Sarkar, A.; Paul, S.K.; Moktadir, M.A. A case study on strategies to deal with the impacts of COVID-19 pandemic in the food and beverage industry. Oper. Manag. Res. 2020, 1–13. [Google Scholar] [CrossRef]

- HLPE. Impacts of COVID-19 on Food Security and Nutrition: Developing Effective Policy Responses to Address the Hunger and Malnutrition Pandemic; Committee on World Food Security High Level Panel of Experts on Food Security and Nutrition: Rome, Italy, 2020. [Google Scholar] [CrossRef]

- CISA. Guidance on the Essential Critical Infrastructure Workforce. Available online: https://www.cisa.gov/publication/guidance-essential-critical-infrastructure-workforce (accessed on 12 March 2021).

- Mbow, C.; Rosenzweig, C.; Barioni, L.; Benton, T.; Herrero, M.; Krishnapillai, M.; Waha, K. Chapter 5: Food Security. IPCC Special Report on Climate Change and Land. 2019. Available online: https://www.ipcc.ch/site/assets/uploads (accessed on 11 March 2021).

- Arenas-Jal, M.; Suñé-Negre, J.; Pérez-Lozano, P.; García-Montoya, E. Trends in the food and sports nutrition industry: A review. Crit. Rev. Food Sci. Nutr. 2020, 60, 2405–2421. [Google Scholar] [CrossRef] [PubMed]

- Shafi, M.; Liu, J.; Ren, W. Impact of COVID-19 pandemic on micro, small, and medium-sized Enterprises operating in Pakistan. Res. Glob. 2020, 2, 100018. [Google Scholar] [CrossRef]

- Donthu, N.; Gustafsson, A. Effects of COVID-19 on business and research. J. Bus. Res. 2020, 117, 284. [Google Scholar] [CrossRef] [PubMed]

- Sánchez-Ramírez, C.; Ramos-Hernández, R.; Mendoza Fong, J.R.; Alor-Hernández, G.; García-Alcaraz, J.L. A system dynamics model to evaluate the impact of production process disruption on order shipping. Appl. Sci. 2020, 10, 208. [Google Scholar] [CrossRef] [Green Version]

- Zhu, G.; Chou, M.C.; Tsai, C.W. Lessons learned from the COVID-19 pandemic exposing the shortcomings of current supply chain operations: A long-term prescriptive offering. Sustainability 2020, 12, 5858. [Google Scholar] [CrossRef]

- ADB. Asian Development Outlook: What Drives Innovation in Asia? Special Topic: The Impact of the Coronavirus Outbreak—An Update; Asian Development Bank: Manila, Philippines, 2020. [Google Scholar]

- ICAO. Economic Impacts of COVID-19 on Civil Aviation. Available online: https://www.icao.int/sustainability/Documents/COVID-19/ICAO_Coronavirus_Econ_Impact.pdf (accessed on 12 March 2021).

- Xie, X.; Huang, L.; Li, J.J.; Zhu, H. Generational differences in perceptions of food health/risk and attitudes toward organic food and game meat: The case of the COVID-19 crisis in China. Int. J. Environ. Res. Public Health 2020, 17, 3148. [Google Scholar] [CrossRef]

- Khan, M.R.; Sikandar, M.; Kazi, R.; Sikandar, A. A Study of Changing Consumer Behaviour of Four Metro Cities in India during Covid-19 Pandemic. Wesley. J. Res. 2021, 13, 57. [Google Scholar]

- Berkman, S.J.; Roscoe, E.M.; Bourret, J.C. Comparing self-directed methods for training staff to create graphs using Graphpad Prism. J. Appl. Behav. Anal. 2019, 52, 188–204. [Google Scholar] [CrossRef]

- Swift, M.L. GraphPad prism, data analysis, and scientific graphing. J. Chem. Inf. Comput. Sci. 1997, 37, 411–412. [Google Scholar] [CrossRef]

- Pramod, K.; Aji Alex, M.; Singh, M.; Dang, S.; Ansari, S.H.; Ali, J. Eugenol nanocapsule for enhanced therapeutic activity against periodontal infections. J. Drug Target. 2016, 24, 24–33. [Google Scholar] [CrossRef]

- Hu, D.; Lou, X.; Meng, N.; Li, Z.; Teng, Y.; Zou, Y.; Wang, F. Influence of age and gender on the epidemic of COVID-19. Wien. Klin. Wochenschr. 2021, 133, 321–330. [Google Scholar] [CrossRef]

- Xu, L.; Tang, F.; Wang, Y.; Cai, Q.; Tang, S.; Xia, D.; Xu, X.; Lu, X. Research progress of pre-hospital emergency during 2000-2020: A bibliometric analysis. Am. J. Transl. Res. 2021, 13, 1109. [Google Scholar] [PubMed]

- Zhu, J.; Zhang, J.; Xia, H.; Ge, J.; Ye, X.; Guo, B.; Liu, M.; Dai, L.; Zhang, L.; Chen, L. Stillbirths in China: A nationwide survey. BJOG Int. J. Obstet. Gynaecol. 2021, 128, 67–76. [Google Scholar] [CrossRef]

- Ali, M.A.; Kamraju, M.; Wani, M.A. An analysis on impact of banning China goods to India. IJIRSET 2020, 9, 1111–1114. [Google Scholar]

- Jung, H.J.; Choi, Y.J.; Oh, K.W. Influencing factors of Chinese consumers’ purchase intention to sustainable apparel products: Exploring consumer “attitude–behavioral intention” gap. Sustainability 2020, 12, 1770. [Google Scholar] [CrossRef] [Green Version]

- Cai, F. The Second Demographic Dividend as a Driver of China’s Growth. China World Econ. 2020, 28, 26–44. [Google Scholar] [CrossRef]

- Crona, B.; Wassénius, E.; Troell, M.; Barclay, K.; Mallory, T.; Fabinyi, M.; Zhang, W.; Lam, V.W.; Cao, L.; Henriksson, P.J. China at a Crossroads: An Analysis of China’s Changing Seafood Production and Consumption. One Earth 2020, 3, 32–44. [Google Scholar] [CrossRef]

- Yu, J. 2020 White Paper on China’s Food & Beverage Industry. Kantar World Panel. 2020. Available online: https://www.kantarworldpanel.com/cn-en/news/2020-White-Paper-on-China-s-Food-Beverage-Industry (accessed on 15 March 2021).

- Xi, S.; Zhang, X.; Yang, G.; Liu, M. China Catering Industry Annual Report 2019; China Hospitality Association: Beijing, China, 2019. [Google Scholar]

- ITA. China Growth in Food and Beverage Franchises. Available online: https://www.trade.gov/market-intelligence/growth-food-and-beverage-franchises-china#:~:text=Most%20F%26B%20revenue%20in%20China,7.8%20percent%20increase%20over%202018 (accessed on 18 March 2021).

- Statista. Food & Beverages. Available online: https://www.statista.com/outlook/dmo/ecommerce/food-personal-care/food-beverages/china (accessed on 15 March 2021).

- Industry Data. Available online: https://www.askci.com/reports/ (accessed on 17 March 2021).

- MedTrend. Seven Trends to Interpret China’s Healthcare Big Data in 2019. Available online: https://medtrend.com.cn/ (accessed on 17 March 2021).

- Thornton, G. CII Social Impact Report 2019. Confedertaion of Indian Industry. Available online: https://www.grantthornton.in/globalassets/1.-member-firms/india/assets/pdfs/cii_csr_social_impact_report_2019.pdf (accessed on 17 March 2021).

- Adlakha, A. Population Trends: India. US Department of Commerce, Economics and Statistics Administration, Bureau, 1996; Volume 3, 4. Available online: http://www.census.gov/ipc/prod/ib-9701.pdf (accessed on 18 March 2021).

- Das, S.; Chatterjee, A.; Pal, T.K. Organic farming in India: A vision towards a healthy nation. Food Qual. Saf. 2020, 4, 69–76. [Google Scholar] [CrossRef]

- Greer, G. Win in India: An Analysis of Market Entry Strategy into India’s Food and Beverage Industry. Undergraduate Thesis, The University of Arkansas, Fayetteville, AR, USA, 2018. Available online: https://scholarworks.uark.edu/finnuht/39/ (accessed on 18 March 2021).

- Jernigan, D.; Ross, C.S. The alcohol marketing landscape: Alcohol industry size, structure, strategies, and public health responses. J. Stud. Alcohol Drugs Suppl. 2020, 2020, 13–25. [Google Scholar] [CrossRef]

- Barichello, R. The COVID-19 pandemic: Anticipating its effects on Canada’s agricultural trade. Can. J. Agric. Econ./Rev. Can. D’agroeconomie 2020, 68, 219–224. [Google Scholar] [CrossRef]

- Brewin, D.G. The impact of COVID-19 on the grains and oilseeds sector. Can. J. Agric. Econ./Rev. Can. D’agroeconomie 2020, 68, 185–188. [Google Scholar] [CrossRef] [Green Version]

- Dryhurst, S.; Schneider, C.R.; Kerr, J.; Freeman, A.L.; Recchia, G.; Van Der Bles, A.M.; Spiegelhalter, D.; van der Linden, S. Risk perceptions of COVID-19 around the world. J. Risk Res. 2020, 23, 994–1006. [Google Scholar] [CrossRef]

- Morton, J. On the susceptibility and vulnerability of agricultural value chains to COVID-19. World Dev. 2020, 136, 105132. [Google Scholar] [CrossRef]

- Pulighe, G.; Lupia, F. Food first: COVID-19 outbreak and cities lockdown a booster for a wider vision on urban agriculture. Sustainability 2020, 12, 5012. [Google Scholar] [CrossRef]

- Siche, R. What is the impact of COVID-19 disease on agriculture? Sci. Agropecu. 2020, 11, 3–6. [Google Scholar] [CrossRef] [Green Version]

- Timilsina, B.; Adhikari, N.; Kafle, S.; Paudel, S.; Poudel, S.; Gautam, D. Addressing impact of COVID-19 post pandemic on farming and agricultural deeds. Asian J. Adv. Res. Rep. 2020, 28–35. [Google Scholar] [CrossRef]

- Zhang, S.; Wang, S.; Yuan, L.; Liu, X.; Gong, B. The impact of epidemics on agricultural production and forecast of COVID-19. China Agric. Econ. Rev. 2020, 12, 409–425. [Google Scholar] [CrossRef]

- Ramakumar, R. Agriculture and the Covid-19 Pandemic: An Analysis with special reference to India. Rev. Agrar. Stud. 2020, 10, 72–110. [Google Scholar]

- Pu, M.; Zhong, Y. Rising concerns over agricultural production as COVID-19 spreads: Lessons from China. Global Food Secur. 2020, 26, 100409. [Google Scholar] [CrossRef]

- FAO; IFAD; UNICEF; WFP; WHO. The State of Food Security and Nutrition in the World 2019. Safeguarding against Economic Slowdowns and Downturns; FAO: Rome, Italy, 2019. [Google Scholar]

- Anthem, P. Risk of Hunger Pandemic as Coronavirus Set to almost Double Acute Hunger by End of 2020. WFP. 2020. Available online: https://www.wfp.org/stories/risk-hunger-pandemic-coronavirus-set-almost-double-acute-hunger-end-2020 (accessed on 19 March 2021).

- FAO. COVID-19 Global Economic Recession: Avoiding Hunger Must Be at the Centre of the Economic Stimulus; FAO: Rome, Italy, 2020. [Google Scholar] [CrossRef]

- FSIN. Global Report on Food Crises—Joint Analysis for Better Decisions. 2020. Available online: http://ebrary.ifpri.org/utils/getfile/collection/p15738coll2/id/133693/filename/133904.pdf (accessed on 18 March 2021).

- Zurayk, R. Pandemic and food security. J. Agric. Food Syst. Community Dev. 2020, 9, 1–5. [Google Scholar] [CrossRef]

- Galanakis, C.M. The food systems in the era of the coronavirus (COVID-19) pandemic crisis. Foods 2020, 9, 523. [Google Scholar] [CrossRef] [PubMed]

- Niles, M.T.; Bertmann, F.; Belarmino, E.H.; Wentworth, T.; Biehl, E.; Neff, R. The early food insecurity impacts of COVID-19. Nutrients 2020, 12, 2096. [Google Scholar] [CrossRef]

- Liverpool-Tasie, L.S.O.; Reardon, T.; Belton, B. “Essential non-essentials”: COVID-19 policy missteps in N igeria rooted in persistent myths about a frican food supply chains. Appl. Econ. Perspect. Policy 2021, 43, 205–224. [Google Scholar] [CrossRef]

- Sina Finance. Global Supply Chain Restructuring under the Impact of the Epidemic: Supply Chain Disruption has Surpassed China. Available online: https://baijiahao.baidu.com/s?id=1661185532506136363&wfr=spider&for=pc (accessed on 15 March 2021).

- You, S.; Wang, H.; Zhang, M.; Song, H.; Xu, X.; Lai, Y. Assessment of monthly economic losses in Wuhan under the lockdown against COVID-19. Humanit. Soc. Sci. Commun. 2020, 7, 1–12. [Google Scholar] [CrossRef]

- Torero, M. Without Food, there Can Be no Exit from the Pandemic. Nature Publishing Group. 2020, 580, 588–589. [Google Scholar] [CrossRef] [Green Version]

- Miwil, O. Sabah Hawker Gives away 2 Tonnes of Fresh Vegetables. Available online: https://www.nst.com.my/news/nation/2020/04/581407/sabah-hawker-gives-away-2-tonnes-fresh-vegetables (accessed on 10 March 2021).

- Singh, S.; Kumar, R.; Panchal, R.; Tiwari, M.K. Impact of COVID-19 on logistics systems and disruptions in food supply chain. Int. J. Prod. Res. 2020, 59, 1993–2008. [Google Scholar] [CrossRef]

- Savary, S.; Akter, S.; Almekinders, C.; Harris, J.; Korsten, L.; Rötter, R.; Waddington, S.; Watson, D. Mapping disruption and resilience mechanisms in food systems. Food Secur. 2020, 12, 695–717. [Google Scholar] [CrossRef] [PubMed]

- Devaiah, D. Coronavirus Lockdown: After Karnataka Farmers Dump Produce; Govt Decides to Direct It towards Needy. Available online: https://in.style.yahoo.com/coronavirus-lockdown-karnataka-farmers-dump-170836772.html (accessed on 10 March 2021).

- Bailey, S. Broken supply chains: COVID-19 Lockdown is having a Devastating Effect on Livelihoods in Rural India. Available online: https://tigr2ess.globalfood.cam.ac.uk/news/broken-supply-chains-Covid-19-lockdown-having-devastating-effect-livelihoods-rural-india (accessed on 10 March 2021).

- The World Bank. Could the Coronavirus Pandemic Threaten Food Supplies for the Most Vulnerable? 2020. Available online: https://www.worldbank.org/en/news/video/2020/04/27/coronavirus-threaten-foodsupplies-for-most-vulnerable (accessed on 12 March 2021).

- Mollenkopf, D.A.; Ozanne, L.K.; Stolze, H.J. A transformative supply chain response to COVID-19. J. Serv. Manag. 2020, 32, 190–202. [Google Scholar] [CrossRef]

- Reardon, T.; Bellemare, M.F.; Zilberman, D. How COVID-19 may disrupt food supply chains in developing countries. In IFPRI Book Chapters; International Food Policy Research Institute (IFPRI): Washington, DC, USA, 2020; Volume 17, pp. 78–80. [Google Scholar]

- Tongia, R. India’s Biggest Challenge: The Future of Farming. 2019. Available online: https://www.theindiaforum.in/article/india-s-biggest-challenge-future-farming (accessed on 12 March 2021).

- Fei, S.; Ni, J. Local Food Systems and COVID-19: An insight from China. Resour Conserv Recycl. 2020, 162, 105022. [Google Scholar] [CrossRef]

- Jia, C.; Jukes, D. The national food safety control system of China–a systematic review. Food Control 2013, 32, 236–245. [Google Scholar] [CrossRef]

- Shukla, S.; Shankar, R.; Singh, S.P. Food safety regulatory model in India. Food Control 2014, 37, 401–413. [Google Scholar] [CrossRef]

- Shingh, S.; Kamalvanshi, V.; Ghimire, S.; Basyal, S. Dairy supply chain system based on blockchain technology. Asian J. Econ. Bus. Account. 2020, 13–19. [Google Scholar] [CrossRef]

- Olayanju, J.B. Top Trends Driving Change in the Food Industry. Available online: https://www.forbes.com/sites/juliabolayanju/2019/02/16/top-trends-driving-change-in-the-food-industry/?sh=4f86b1386063 (accessed on 12 March 2021).

- Walaszczyk, A.; Galińska, B. Food Origin Traceability from a Consumer’s Perspective. Sustainability 2020, 12, 1872. [Google Scholar] [CrossRef] [Green Version]

- Astill, J.; Dara, R.A.; Campbell, M.; Farber, J.M.; Fraser, E.D.; Sharif, S.; Yada, R.Y. Transparency in food supply chains: A review of enabling technology solutions. Trends Food Sci. Technol. 2019, 91, 240–247. [Google Scholar] [CrossRef]

- Telukdarie, A.; Munsamy, M.; Mohlala, P. Analysis of the Impact of COVID-19 on the Food and Beverages Manufacturing Sector. Sustainability 2020, 12, 9331. [Google Scholar] [CrossRef]

- Hua, J.; Wang, X.; Kang, M.; Wang, H.; Wang, F.-Y. Blockchain based provenance for agricultural products: A distributed platform with duplicated and shared bookkeeping. In Proceedings of the 2018 IEEE Intelligent Vehicles Symposium (IV), Changshu, China, 26–30 June 2018; pp. 97–101. [Google Scholar]

- Tian, F. A supply chain traceability system for food safety based on HACCP, blockchain & Internet of things. In Proceedings of the 2017 International Conference on Service Systems and Service Management, Dalian, China, 16–18 June 2017; pp. 1–6. [Google Scholar]

- Sunny, J.; Undralla, N.; Pillai, V.M. Supply chain transparency through blockchain-based traceability: An overview with demonstration. Comput. Ind. Eng. 2020, 150, 106895. [Google Scholar] [CrossRef]

- Ben-Daya, M.; Hassini, E.; Bahroun, Z.; Banimfreg, B.H. The role of internet of things in food supply chain quality management: A review. Qual. Manag. J. 2020, 17–40. [Google Scholar] [CrossRef]

- Iqbal, R.; Butt, T.A. Safe farming as a service of blockchain-based supply chain management for improved transparency. Clust. Comput. 2020, 23, 12139–12150. [Google Scholar] [CrossRef]

- Al-Rakhami, M.S.; Al-Mashari, M. A Blockchain-Based Trust Model for the Internet of Things Supply Chain Management. Sensors 2021, 21, 1759. [Google Scholar] [CrossRef]

- Jiang, X. Digital economy in the post-pandemic era. J. Chin. Econ. Bus. Stud. 2020, 18, 333–339. [Google Scholar] [CrossRef]

- Eklahare, J. Food & Beverage Industry in India—Heading Towards Advanced Automation...? Available online: https://www.industr.com/en/food-beverage-industry-in-india-heading-towards-advanced-automation-2392853 (accessed on 13 March 2021).

- Davis, K. Welcome to China’s Latest ‘Robot Restaurant’. Available online: https://www.weforum.org/agenda/2020/07/china-robots-ai-restaurant-hospitality (accessed on 15 March 2021).

- Wang, X.V.; Wang, L. A literature survey of the robotic technologies during the COVID-19 pandemic. J. Manuf. Syst. 2021. [Google Scholar] [CrossRef]

- Arya, R.; Delmas, A. Business Plan Annapurna: A Food Service Availability in Housing Complexes in India. Master’s Thesis, Geneva Business School, Geneva, Switzerland, 2021. Available online: https://gbsge.com/media/wzlh0305/arya-rajani-2020-annapurna-a-food-service-availability-in-the-housing-complexes-in-india-mba-thesis-geneva-business.pdf (accessed on 13 March 2021).

- IANS. Covid impact: Restaurants innovate new, creative ways to bring back diners. Bus. Stand. 2020. Available online: https://www.business-standard.com/article/current-affairs/covid-impact-restaurants-innovate-new-creative-ways-to-bring-back-diners-120101700573_1.html (accessed on 27 March 2021).

- Wu, F.; Lu, C.; Zhu, M.; Chen, H.; Zhu, J.; Yu, K.; Li, L.; Li, M.; Chen, Q.; Li, X. Towards a new generation of artificial intelligence in China. Nat. Mach. Intell. 2020, 2, 312–316. [Google Scholar] [CrossRef]

- Consulting, D. AI in the Food and Beverage Industry in China: The Future of Dining Starts Today. Available online: https://daxueconsulting.com/ai-food-and-beverage-industry-china/ (accessed on 15 March 2021).

- China’s Food Delivery Market Dynamics. 2020. Available online: https://daxueconsulting.com/o2o-food-delivery-market-in-china/ (accessed on 27 March 2021).

- Zhang, Z. How COVID-19 Will Transform the Fresh Food Industry in China. Available online: https://www.china-briefing.com/news/how-Covid-19-will-transform-china-fresh-food-industry-investment-opportunities/ (accessed on 16 March 2021).

- Preethika, T.; Vaishnavi, P.; Agnishwar, J.; Padmanathan, K.; Umashankar, S.; Annapoorani, S.; Subash, M.; Aruloli, K. Artificial Intelligence and Drones to Combat COVID-19. Preprints. 2020, 2020060027. [Google Scholar] [CrossRef]

- Padmanathan, K.; Govindarajan, U.; Ramachandaramurthy, V.K.; Rajagopalan, A.; Pachaivannan, N.; Sowmmiya, U.; Padmanaban, S.; Holm-Nielsen, J.B.; Xavier, S.; Periasamy, S.K. A sociocultural study on solar photovoltaic energy system in India: Stratification and policy implication. J. Clean. Prod. 2019, 216, 461–481. [Google Scholar] [CrossRef]

- Kumar, S. Amalgamation of AI & ML in India’s Food Tech Industry. Startup Talky. 2020. Available online: https://startuptalky.com/amalgamation-of-ai-ml-in-indias-food-tech-domain/ (accessed on 28 March 2021).

- Reardon, T.; Swinnen, J. COVID-19 and resilience innovations in food supply chains. In COVID-19 and Global food Security; Part Eight: Preparing food systems for future pandemics, Chapter 30; Johan, S., John, M., Eds.; International Food Policy Research Institute (IFPRI): Washington, DC, USA, 2020; pp. 132–136. [Google Scholar] [CrossRef]

- Gray, R.S. Agriculture, transportation, and the COVID-19 crisis. Can. J. Agric. Econ. /Rev. Can. D’agroeconomie 2020, 68, 239–243. [Google Scholar] [CrossRef] [Green Version]

- IBEF. Future of Indian Food and Beverage Industry Post-Pandemic. Knowl. Cent. 2020. Available online: https://www.ibef.org/blogs/future-of-indian-food-and-beverage-industry-post-pandemic (accessed on 28 March 2021).

- SCMP, C.M.P. New biometric products flood out to tackle Covid-19. Biom. Technol. Today 2020. [Google Scholar] [CrossRef]

- Li, J.; Hallsworth, A.G.; Coca-Stefaniak, J.A. Changing grocery shopping behaviours among Chinese consumers at the outset of the COVID-19 outbreak. Tijdschr. Econ. Soc. Geogr. 2020, 111, 574–583. [Google Scholar] [CrossRef]

- Van Ewijk, B.J.; Steenkamp, J.-B.E.; Gijsbrechts, E. The Rise of Online Grocery Shopping in China: Which Brands Will Benefit? J. Int. Mark. 2020, 28, 20–39. [Google Scholar] [CrossRef] [Green Version]

- Mehrolia, S.; Alagarsamy, S.; Solaikutty, V.M. Customers response to online food delivery services during COVID-19 outbreak using binary logistic regression. Int. J. Consum. Stud. 2020. [Google Scholar] [CrossRef]

- You, Y. Shift towards Vegan in China during COVID-19: An Online Behavioral Survey Study. In Proceedings of the 2020 2nd International Conference on Economic Management and Cultural Industry (ICEMCI2020), Chengdu, China, 30 November 2020; Atlantis Press: Paris, France, 2020; pp. 298–303. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Date | Entities | Strategies | Response |

|---|---|---|---|

| 19 January | MARA | Urgent notice on ensuring vegetable production and supply during COVID-19 epidemic |

|

| 1 February | MC | Notice on further ensuring supply of life necessities (inc. grain and edible oil, meat, vegetables etc.) |

|

| 4 February | MARA | Urgent notice on maintaining livestock and poultry industry in operation and ensuring supply of meat, eggs, and milk |

|

| 6 February | MC | Notice on ensuring delivery and distribution of life necessities during COVID-19 epidemic |

|

| 11 February | MC | Notice on further supply of life necessities in major cities |

|

| 11 February | MARA | Notice of ensuring agriculture products sales in poor stricken regions during COVID-19 epidemic |

|

| 14 February | MC | Notice on further strengthening linkages between agriculture demand and supply during COVID-19 epidemic |

|

| 14 February | MC, MF | Urgent notice on enhancing collaboration and coordination between agriculture and commercial sectors to improve the food supply chain during COVID-19 epidemic |

|

| 14 February | MF, MARA | Notice on ensuring stable production and adequate supply of agricultural products during COVID-19 epidemic |

|

| 16 February | MARA, NDRC, MT | Urgent notice on alleviating current practical difficulties and speeding up the resumption of breeding industry |

|

| 21 February | MC | Notice on overall planning and management of life necessities supply |

|

| 25 February | MC | Notice on popularizing the best practices of ensuring life necessities supply during the COVID-19 epidemic |

|

| 2 March | LGCC COVID-19 | Guidelines for agricultural production in spring planting season |

|

| 13 March | MARA | Notice on further simplifying certification and approval process to speeding up the resumption of agricultural enterprises |

|

| 19 March | MARA, MF, CBIRC | Notice on further strengthening supports to ensuring stable production and supply of pork |

|

| Date | Entities | Strategies | Response |

|---|---|---|---|

| 24 March | MAFW |

Launched new features of the electronic National Agriculture Market (e-NAM) platform |

|

| 25 March | MOHA | Issued a notice information to states and UTs |

|

| 25 March | NDDB | Urged all milk co-operatives |

|

| 26 March | APMC | Took proactive measures |

|

| 26 March | C&SG | Made efforts to maintain the operation of distribution channels |

|

| 31 March | MOS | Issued specific guidelines to main ports |

|

| 27 March | CG | Extend the current Foreign Trade Policy |

|

| 16 April | GOI | Govt allowed e-commerce, agri industry to resume from April 20 |

|

| 15 May | FM | Unveiled third set of economic stimulus |

|

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Memon, S.U.R.; Pawase, V.R.; Pavase, T.R.; Soomro, M.A. Investigation of COVID-19 Impact on the Food and Beverages Industry: China and India Perspective. Foods 2021, 10, 1069. https://doi.org/10.3390/foods10051069

Memon SUR, Pawase VR, Pavase TR, Soomro MA. Investigation of COVID-19 Impact on the Food and Beverages Industry: China and India Perspective. Foods. 2021; 10(5):1069. https://doi.org/10.3390/foods10051069

Chicago/Turabian StyleMemon, Shafique Ul Rehman, Vijayanta Ramesh Pawase, Tushar Ramesh Pavase, and Maqsood Ahmed Soomro. 2021. "Investigation of COVID-19 Impact on the Food and Beverages Industry: China and India Perspective" Foods 10, no. 5: 1069. https://doi.org/10.3390/foods10051069