How Do Financial Development and Renewable Energy Affect Consumption-Based Carbon Emissions?

,

,  ,

,  and

and

Abstract

:1. Introduction

2. Literature Review

2.1. Renewable Energy and Environmental Degradation

2.2. International Trade and Consumption-Based Carbon Emission

2.3. Financial Development and Environmental Degradation

3. Theoretical Framework, Data, and Methods

3.1. Theoretical Framework

3.2. Data

3.3. Methodology

3.3.1. Quantile Cointegration Test

3.3.2. Quantile-on-Quantile (QQ) Approach

3.3.3. Robustness Test for the QQ Method

3.3.4. Quantile Causality Approach

4. Empirical Results

4.1. Preliminary Test Outcomes

4.2. Non-Linearity Test Outcomes

4.3. Quantile Cointegration Outcomes

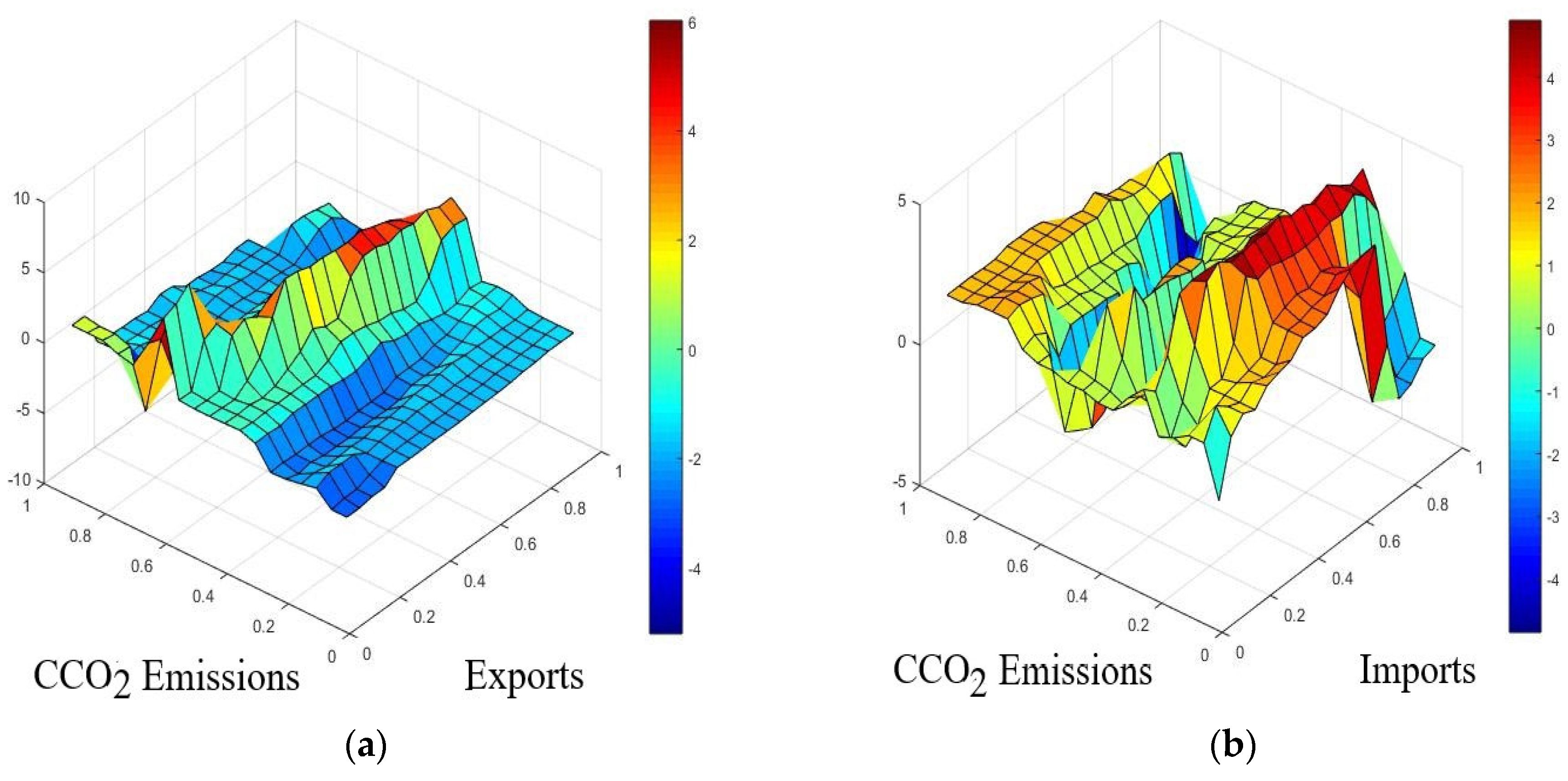

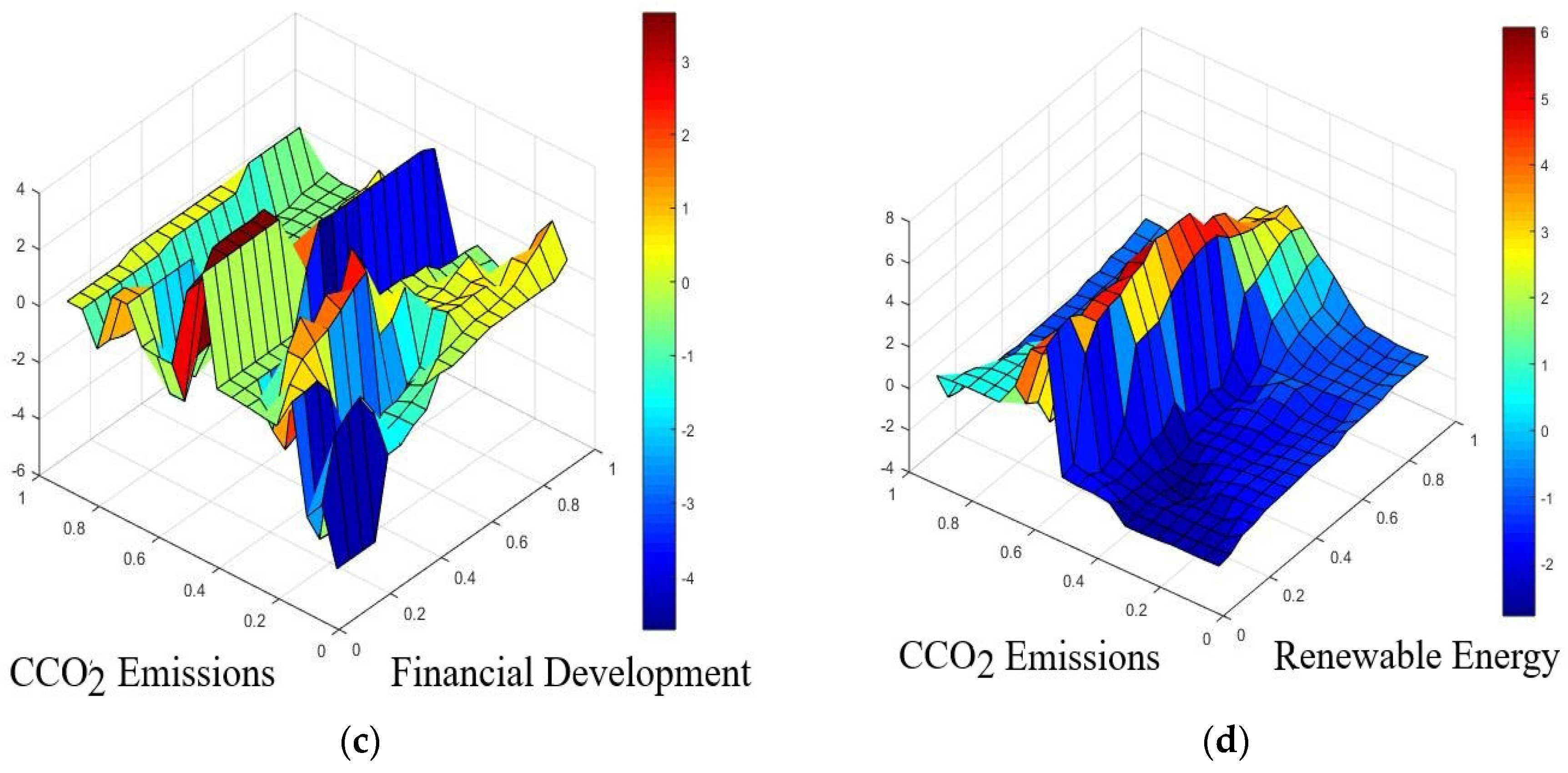

4.4. QQ Empirical Results

4.5. Robustness Check

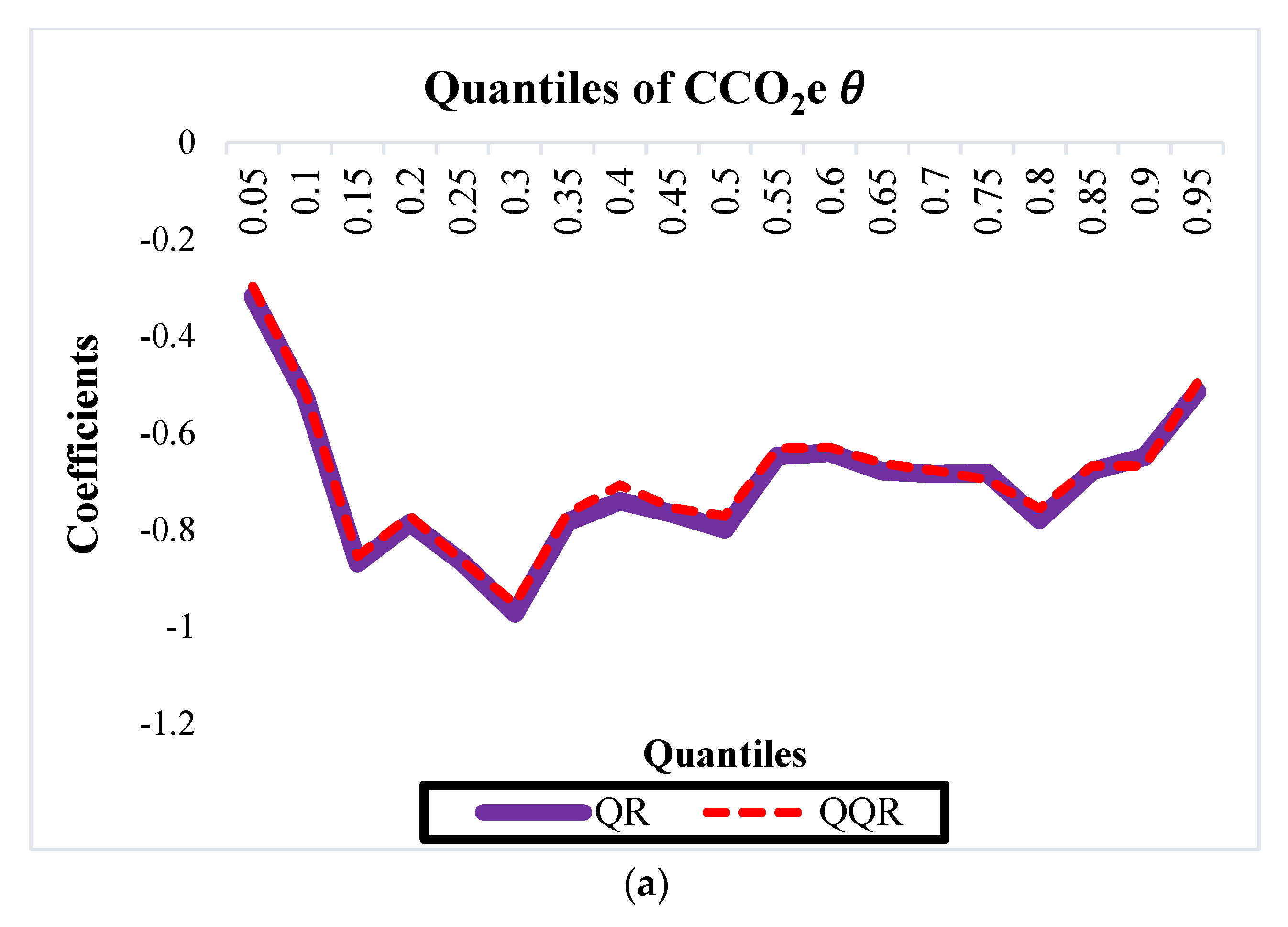

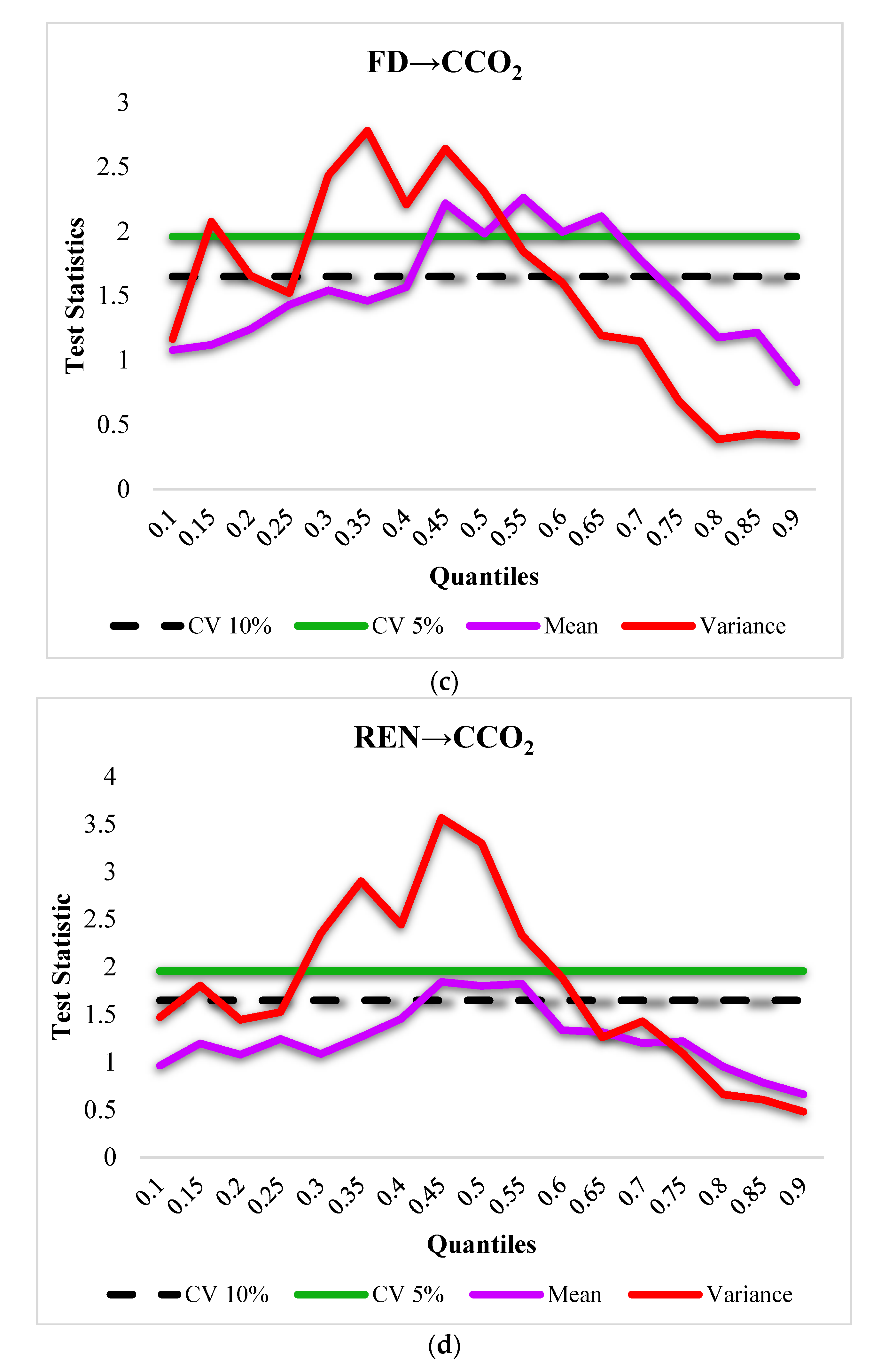

4.6. Granger Causality in Quantiles

4.7. Discussion

5. Conclusions and Policy Recommendations

5.1. Conclusions

5.2. Policy Recommendations

5.3. Limitations of Study and Extensions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Wang, Q.; Wang, L. Renewable energy consumption and economic growth in OECD countries: A nonlinear panel data analysis. Energy 2020, 207, 118200. [Google Scholar] [CrossRef]

- Bekun, F.V.; Awosusi, A.A.; Altuntaş, M. Another look at the nexus between economic growth trajectory and emission within the context of developing country: Fresh insights from a nonparametric causality-in-quantiles test. Renew. Energy 2021, 175, 1012–1024. [Google Scholar] [CrossRef]

- Awosusi, A.A.; Adebayo, T.S.; Altuntaş, M.; Agyekum, E.B.; Zawbaa, H.M.; Kamel, S. The dynamic impact of biomass and natural resources on ecological footprint in BRICS economies: A quantile regression evidence. Energy Rep. 2022, 8, 1979–1994. [Google Scholar] [CrossRef]

- Wang, Q.; Li, S.; Li, R.; Jiang, F. Underestimated impact of the COVID-19 on carbon emission reduction in developing countries—A novel assessment based on scenario analysis. Environ. Res. 2022, 204, 111990. [Google Scholar] [CrossRef] [PubMed]

- Adebayo, T.S.; Awosusi, A.A.; Rjoub, H.; Agyekum, E.B.; Kirikkaleli, D. The influence of renewable energy usage on consumption-based carbon emissions in MINT economies. Heliyon 2022, 8, e08941. [Google Scholar] [CrossRef] [PubMed]

- Kirikkaleli, D.; Altuntaş, M.; Awosusi, A.A.; Adebayo, T.S. Role of technological innovation and globalization in BRICS economies: Policy towards environmental sustainability. Int. J. Sustain. Dev. World Ecol. 2022, 1–18. [Google Scholar] [CrossRef]

- Wang, Q.; Wang, S.; Jiang, X. Preventing a rebound in carbon intensity post-COVID-19—Lessons learned from the change in carbon intensity before and after the 2008 financial crisis. Sustain. Prod. Consum. 2021, 27, 1841–1856. [Google Scholar] [CrossRef]

- Li, R.; Wang, Q.; Wang, X.; Zhou, Y.; Han, X.; Liu, Y. Germany’s contribution to global carbon reduction might be underestimated—A new assessment based on scenario analysis with and without trade. Technol. Forecast. Soc. Chang. 2022, 176, 121465. [Google Scholar] [CrossRef]

- Wang, Q.; Zhang, F. The effects of trade openness on decoupling carbon emissions from economic growth—Evidence from 182 countries. J. Clean. Prod. 2021, 279, 123838. [Google Scholar] [CrossRef]

- Awosusi, A.A.; Kirikkaleli, D.; Akinsola, G.D.; Mwamba, M.N. Can CO2 emissions and energy consumption determine the economic performance of South Korea? A time series analysis. Environ. Sci. Pollut. Res. 2021, 28, 38969–38984. [Google Scholar] [CrossRef]

- Awosusi, A.A.; Kutlay, K.; Altuntaş, M.; Khodjiev, B.; Agyekum, E.B.; Shouran, M.; Elgbaily, M.; Kamel, S. A Roadmap toward Achieving Sustainable Environment: Evaluating the Impact of Technological Innovation and Globalization on Load Capacity Factor. Int. J. Environ. Res. Public Health 2022, 19, 3288. [Google Scholar] [CrossRef]

- He, K.; Ramzan, M.; Awosusi, A.A.; Ahmed, Z.; Ahmad, M.; Altuntaş, M. Does Globalization Moderate the Effect of Economic Complexity on CO2 Emissions? Evidence From the Top 10 Energy Transition Economies. Front. Environ. Sci. 2021, 9, 555. [Google Scholar] [CrossRef]

- Alola, A.A.; Adebayo, T.S.; Onifade, S.T. Examining the dynamics of ecological footprint in China with spectral Granger causality and quantile-on-quantile approaches. Int. J. Sustain. Dev. World Ecol. 2021, 29, 263–276. [Google Scholar] [CrossRef]

- Awosusi, A.A.; Xulu, N.G.; Ahmadi, M.; Rjoub, H.; Altuntaş, M.; Uhunamure, S.E.; Akadiri, S.S.; Kirikkaleli, D. The Sustainable Environment in Uruguay: The Roles of Financial Development, Natural Resources, and Trade Globalization. Front. Environ. Sci. 2022, 10. Available online: https://www.frontiersin.org/article/10.3389/fenvs.2022.875577 (accessed on 1 June 2022). [CrossRef]

- Ojekemi, O.S.; Rjoub, H.; Awosusi, A.A.; Agyekum, E.B. Toward a sustainable environment and economic growth in BRICS economies: Do innovation and globalization matter? Environ. Sci. Pollut. Res. 2022. [Google Scholar] [CrossRef] [PubMed]

- Awosusi, A.A.; Mata, M.N.; Ahmed, Z.; Coelho, M.F.; Altuntaş, M.; Martins, J.M.; Martins, J.N.; Onifade, S.T. How Do Renewable Energy, Economic Growth and Natural Resources Rent Affect Environmental Sustainability in a Globalized Economy? Evidence From Colombia Based on the Gradual Shift Causality Approach. Front. Energy Res. 2022, 9. Available online: https://www.frontiersin.org/article/10.3389/fenrg.2021.739721 (accessed on 11 February 2022). [CrossRef]

- Yuping, L.; Ramzan, M.; Xincheng, L.; Murshed, M.; Awosusi, A.A.; Bah, S.I.; Adebayo, T.S. Determinants of carbon emissions in Argentina: The roles of renewable energy consumption and globalization. Energy Rep. 2021, 7, 4747–4760. [Google Scholar] [CrossRef]

- Xu, D.; Salem, S.; Awosusi, A.A.; Abdurakhmanova, G.; Altuntaş, M.; Oluwajana, D.; Kirikkaleli, D.; Ojekemi, O. Load Capacity Factor and Financial Globalization in Brazil: The Role of Renewable Energy and Urbanization. Front. Environ. Sci. 2022, 9. Available online: https://www.frontiersin.org/article/10.3389/fenvs.2021.823185 (accessed on 11 February 2022). [CrossRef]

- Piaggio, M.; Padilla, E.; Román, C. The long-term relationship between CO2 emissions and economic activity in a small open economy: Uruguay 1882–2010. Energy Econ. 2017, 65, 271–282. [Google Scholar] [CrossRef]

- Adebayo, T.S.; AbdulKareem, H.K.K.; Bilal; Kirikkaleli, D.; Shah, M.I.; Abbas, S. CO2 behavior amidst the COVID-19 pandemic in the United Kingdom: The role of renewable and non-renewable energy development. Renew. Energy 2022, 189, 492–501. [Google Scholar] [CrossRef]

- Piaggio, M.; Alcántara, V.; Padilla, E. Greenhouse Gas Emissions and Economic Structure in Uruguay. Econ. Syst. Res. 2014, 26, 155–176. [Google Scholar] [CrossRef]

- Liddle, B. Consumption-based accounting and the trade-carbon emissions nexus. Energy Econ. 2018, 69, 71–78. [Google Scholar] [CrossRef]

- Hasanov, F.J.; Liddle, B.; Mikayilov, J.I. The impact of international trade on CO2 emissions in oil exporting countries: Territory vs consumption emissions accounting. Energy Econ. 2018, 74, 343–350. [Google Scholar] [CrossRef]

- Adebayo, T.S.; Acheampong, A.O. Modelling the globalization-CO2 emission nexus in Australia: Evidence from quantile-on-quantile approach. Environ. Sci. Pollut. Res. 2021, 29, 9867–9882. [Google Scholar] [CrossRef]

- Ding, Q.; Khattak, S.I.; Ahmad, M. Towards sustainable production and consumption: Assessing the impact of energy productivity and eco-innovation on consumption-based carbon dioxide emissions (CCO2) in G-7 nations. Sustain. Prod. Consum. 2021, 27, 254–268. [Google Scholar] [CrossRef]

- Ali, M.; Kirikkaleli, D. The asymmetric effect of renewable energy and trade on consumption-based CO2 emissions: The case of Italy. Integr. Environ. Assess. Manag. 2021, 18, 784–795. [Google Scholar] [CrossRef]

- Kirikkaleli, D.; Güngör, H.; Adebayo, T.S. Consumption-based carbon emissions, renewable energy consumption, financial development and economic growth in Chile. Bus. Strategy Environ. 2021, 31, 1123–1137. [Google Scholar] [CrossRef]

- Kirikkaleli, D.; Adebayo, T.S. Do public-private partnerships in energy and renewable energy consumption matter for consumption-based carbon dioxide emissions in India? Environ. Sci. Pollut. Res. 2021, 28, 30139–30152. [Google Scholar] [CrossRef]

- Khan, Z.; Ali, M.; Kirikkaleli, D.; Wahab, S.; Jiao, Z. The impact of technological innovation and public-private partnership investment on sustainable environment in China: Consumption-based carbon emissions analysis. Sustain. Dev. 2020, 28, 1317–1330. [Google Scholar] [CrossRef]

- Udemba, E.N.; Adebayo, T.S.; Ahmed, Z.; Kirikkaleli, D. Determinants of consumption-based carbon emissions in Chile: An application of nonlinear ARDL. Environ. Sci. Pollut. Res. 2021, 28, 43908–43922. [Google Scholar] [CrossRef]

- Hassan, T.; Song, H.; Kirikkaleli, D. International trade and consumption-based carbon emissions: Evaluating the role of composite risk for RCEP economies. Environ. Sci. Pollut. Res. 2021, 29, 3417–3437. [Google Scholar] [CrossRef] [PubMed]

- Miao, Y.; Razzaq, A.; Awosusi, A.A. Do renewable energy consumption and financial globalisation contribute to ecological sustainability in newly industrialized countries? Renew. Energy 2022, 187, 688–697. [Google Scholar] [CrossRef]

- Panait, M.; Awosusi, A.A.; Rjoub, H.; Popescu, C. Asymmetric Impact of International Trade on Consumption-Based Carbon Emissions in MINT Nations. Energies 2021, 14, 6581. [Google Scholar] [CrossRef]

- Khan, Z.; Ali, M.; Jinyu, L.; Shahbaz, M.; Siqun, Y. Consumption-based carbon emissions and trade nexus: Evidence from nine oil exporting countries. Energy Econ. 2020, 89, 104806. [Google Scholar] [CrossRef]

- Kirikkaleli, D.; Oyebanji, M.O. Consumption-based carbon emissions, trade, and globalization: An empirical study of Bolivia. Environ. Sci. Pollut. Res. 2022, 29, 29927–29937. [Google Scholar] [CrossRef] [PubMed]

- Abid, A.; Mehmood, U.; Tariq, S.; Haq, Z.U. The effect of technological innovation, FDI, and financial development on CO2 emission: Evidence from the G8 countries. Environ. Sci. Pollut. Res. 2021, 29, 11654–11662. [Google Scholar] [CrossRef]

- Szymczyk, K.; Şahin, D.; Bağcı, H.; Kaygın, C.Y. The Effect of Energy Usage, Economic Growth, and Financial Development on CO2 Emission Management: An Analysis of OECD Countries with a High Environmental Performance Index. Energies 2021, 14, 4671. [Google Scholar] [CrossRef]

- Saleem, H.; Khan, M.B.; Shabbir, M.S. The role of financial development, energy demand, and technological change in environmental sustainability agenda: Evidence from selected Asian countries. Environ. Sci. Pollut. Res. 2020, 27, 5266–5280. [Google Scholar] [CrossRef]

- Gill, A.R.; Hassan, S.; Haseeb, M. Moderating role of financial development in environmental Kuznets: A case study of Malaysia. Environ. Sci. Pollut. Res. 2019, 26, 34468–34478. [Google Scholar] [CrossRef]

- Haldar, A.; Sethi, N. Environmental effects of Information and Communication Technology—Exploring the roles of renewable energy, innovation, trade and financial development. Renew. Sustain. Energy Rev. 2022, 153, 111754. [Google Scholar] [CrossRef]

- Anwar, A.; Sinha, A.; Sharif, A.; Siddique, M.; Irshad, S.; Anwar, W.; Malik, S. The nexus between urbanization, renewable energy consumption, financial development, and CO2 emissions: Evidence from selected Asian countries. Environ. Dev. Sustain. 2021, 24, 6556–6576. [Google Scholar] [CrossRef]

- Shahbaz, M.; Haouas, I.; Sohag, K.; Ozturk, I. The financial development-environmental degradation nexus in the United Arab Emirates: The importance of growth, globalization and structural breaks. Environ. Sci. Pollut. Res. 2020, 27, 10685–10699. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Zakaria, M.; Bibi, S. Financial development and environment in South Asia: The role of institutional quality. Environ. Sci. Pollut. Res. 2019, 26, 7926–7937. [Google Scholar] [CrossRef]

- Ramzan, M.; Iqbal, H.A.; Awosusi, A.A.; Akinsola, G.D. The environmental sustainability effects of financial development and urbanization in Latin American countries. Environ. Sci. Pollut. Res. 2021, 28, 57983–57996. [Google Scholar] [CrossRef]

- Khan, Z.; Ali, S.; Umar, M.; Kirikkaleli, D.; Jiao, Z. Consumption-based carbon emissions and International trade in G7 countries: The role of Environmental innovation and Renewable energy. Sci. Total Environ. 2020, 730, 138945. [Google Scholar] [CrossRef] [PubMed]

- Akinsola, G.D.; Awosusi, A.A.; Kirikkaleli, D.; Umarbeyli, S.; Adeshola, I.; Adebayo, T.S. Ecological footprint, public-private partnership investment in energy, and financial development in Brazil: A gradual shift causality approach. Environ. Sci. Pollut. Res. 2022, 29, 10077–10090. [Google Scholar] [CrossRef]

- Abbasi, K.R.; Hussain, K.; Haddad, A.M.; Salman, A.; Ozturk, I. The role of Financial Development and Technological Innovation towards Sustainable Development in Pakistan: Fresh insights from consumption and territory-based emissions. Technol. Forecast. Soc. Chang. 2022, 176, 121444. [Google Scholar] [CrossRef]

- Xiao, Z. Quantile cointegrating regression. J. Econom. 2009, 150, 248–260. [Google Scholar] [CrossRef] [Green Version]

- Saikkonen, P. Asymptotically Efficient Estimation of Cointegration Regressions. Econom. Theory 1991, 7, 1–21. [Google Scholar] [CrossRef]

- Engle, R.F.; Granger, C.W.J. Co-Integration and Error Correction: Representation, Estimation, and Testing. Econometrica 1987, 55, 251–276. [Google Scholar] [CrossRef]

- Sim, N.; Zhou, H. Oil prices, US stock return, and the dependence between their quantiles. J. Bank. Financ. 2015, 55, 1–8. [Google Scholar] [CrossRef]

- Koenker, R.; Bassett, G. Regression Quantiles. Econometrica 1978, 46, 33–50. [Google Scholar] [CrossRef]

- Cleveland, W.S. Robust Locally Weighted Regression and Smoothing Scatterplots. J. Am. Stat. Assoc. 1979, 74, 829–836. [Google Scholar] [CrossRef]

- Stone, C.J. Consistent Nonparametric Regression. Ann. Stat. 1977, 5, 595–620. [Google Scholar] [CrossRef]

- Balcilar, M.; Gupta, R.; Pierdzioch, C. Does uncertainty move the gold price? New evidence from a nonparametric causality-in-quantiles test. Resour. Policy 2016, 49, 74–80. [Google Scholar] [CrossRef] [Green Version]

- Balcilar, M.; Bonato, M.; Demirer, R.; Gupta, R. The effect of investor sentiment on gold market return dynamics: Evidence from a nonparametric causality-in-quantiles approach. Resour. Policy 2017, 51, 77–84. [Google Scholar] [CrossRef]

- Jeong, K.; Härdle, W.K.; Song, S. A Consistent Nonparametric Test for Causality in Quantile. Econom. Theory 2012, 28, 861–887. [Google Scholar] [CrossRef] [Green Version]

- Nishiyama, Y.; Hitomi, K.; Kawasaki, Y.; Jeong, K. A consistent nonparametric test for nonlinear causality—Specification in time series regression. J. Econom. 2011, 165, 112–127. [Google Scholar] [CrossRef] [Green Version]

- Broock, W.A.; Scheinkman, J.A.; Dechert, W.D.; LeBaron, B. A test for independence based on the correlation dimension. Econom. Rev. 1996, 15, 197–235. [Google Scholar] [CrossRef]

- Adebayo, T.S.; Rjoub, H. Assessment of the role of trade and renewable energy consumption on consumption-based carbon emissions: Evidence from the MINT economies. Environ. Sci. Pollut. Res. 2021, 28, 58271–58283. [Google Scholar] [CrossRef]

- Halicioglu, F. An econometric study of CO2 emissions, energy consumption, income and foreign trade in Turkey. Energy Policy 2009, 37, 1156–1164. [Google Scholar] [CrossRef] [Green Version]

- Rahman, M.M. Do population density, economic growth, energy use and exports adversely affect environmental quality in Asian populous countries? Renew. Sustain. Energy Rev. 2017, 77, 506–514. [Google Scholar] [CrossRef]

- Salman, M.; Long, X.; Dauda, L.; Mensah, C.N.; Muhammad, S. Different impacts of export and import on carbon emissions across 7 ASEAN countries: A panel quantile regression approach. Sci. Total Environ. 2019, 686, 1019–1029. [Google Scholar] [CrossRef] [PubMed]

- Al-mulali, U.; Sheau-Ting, L. Econometric analysis of trade, exports, imports, energy consumption and CO2 emission in six regions. Renew. Sustain. Energy Rev. 2014, 33, 484–498. [Google Scholar] [CrossRef]

- Du, L.; Jiang, H.; Awosusi, A.A.; Razzaq, A. Asymmetric effects of high-tech industry and renewable energy on consumption-based carbon emissions in MINT countries. Renew. Energy 2022, 33, 484–498. [Google Scholar] [CrossRef]

- Nguyen, T.T.H.; Moslehpour, M.; Vo, T.T.V.; Wong, W.-K. State Ownership and Risk-Taking Behavior: An Empirical Approach to Get Better Profitability, Investment, and Trading Strategies for Listed Corporates in Vietnam. Economies 2020, 8, 46. [Google Scholar] [CrossRef]

- Zada, H.; Hassan, A.; Wong, W.-K. Do Jumps Matter in Both Equity Market Returns and Integrated Volatility: A Comparison of Asian Developed and Emerging Markets. Economies 2021, 9, 92. [Google Scholar] [CrossRef]

- Guo, X.; Jiang, X.; Wong, W.-K. Stochastic Dominance and Omega Ratio: Measures to Examine Market Efficiency, Arbitrage Opportunity, and Anomaly. Economies 2017, 5, 38. [Google Scholar] [CrossRef] [Green Version]

- Rangata, M.; Das, S.; Ali, M. Analysing Maximum Monthly Temperatures in South Africa for 45 Years Using Functional Data Analysis. 2020. Available online: https://repository.up.ac.za/handle/2263/78993 (accessed on 29 June 2022).

- Gülerce, M.; Ünal, G. Forecasting of oil and agricultural commodity prices: Varma versus arma. Ann. Financ. Econ. 2017, 12, 1750012. [Google Scholar] [CrossRef]

- Ghazouani, T.; Drissi, R.; Boukhatem, J. Financial integration and macroeconomic volatility: New evidence from dsge modeling. Ann. Financ. Econ. 2019, 14, 1950007. [Google Scholar] [CrossRef]

- Wang, Q.; Wang, L.; Li, R. Renewable energy and economic growth revisited: The dual roles of resource dependence and anticorruption regulation. J. Clean. Prod. 2022, 337, 130514. [Google Scholar] [CrossRef]

- Aye, G.C.; Gupta, R. Macroeconomic uncertainty and the comovement in buying versus renting in the USA. Adv. Decis. Sci. 2019, 23, 93–121. [Google Scholar] [CrossRef]

- Ha, N.M.; Ngoc, B.H.; McAleer, M. Financial integration, energy consumption and economic growth in Vietnam. Ann. Financ. Econ. 2020, 15, 2050010. [Google Scholar] [CrossRef]

- Naghavi, N.; Mubarik, M.S.; Kaur, D. Financial liberalization and stock market efficiency: Measuring the threshold effects of governance. Ann. Financ. Econ. 2018, 13, 1850016. [Google Scholar] [CrossRef]

- Wong, W.-K. Editorial Statement and Research Ideas for Efficiency and Anomalies in Stock Markets. Economies 2020, 8, 10. [Google Scholar] [CrossRef] [Green Version]

- Woo, K.-Y.; Mai, C.; McAleer, M.; Wong, W.-K. Review on Efficiency and Anomalies in Stock Markets. Economies 2020, 8, 20. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variables | Metric | Sources |

|---|---|---|

| Consumption-based carbon emissions | Million tons | Global Carbon Atlas |

| Imports | Share of GDP in percentage | World Bank database |

| Exports | ||

| Renewable energy | Kilowatts/per hour | British Petroleum Database |

| Financial development | Index | International Monetary Fund database |

| CCO2e | EXP | IMP | REC | FD | |

|---|---|---|---|---|---|

| Mean | 2.1401 | 3.1320 | 3.1305 | 3.8056 | 3.3590 |

| Median | 2.1494 | 3.1557 | 3.0536 | 3.7722 | 3.2495 |

| Maximum | 2.6210 | 3.4811 | 3.5742 | 4.1070 | 4.2843 |

| Minimum | 1.5579 | 2.7073 | 2.8699 | 3.4935 | 2.9838 |

| Std. Dev. | 0.2911 | 0.2131 | 0.1909 | 0.16308 | 0.2977 |

| Skewness | −0.2492 | −0.2612 | 0.5439 | 0.5002 | 1.4911 |

| Kurtosis | 1.8907 | 1.9196 | 2.0495 | 2.3926 | 4.3987 |

| Jarque−Bera | 7.1480 | 6.9611 | 10.0872 | 6.6207 | 52.442 |

| Probability | 0.0280 | 0.0307 | 0.0064 | 0.0365 | 0.0000 |

| KPSS | PP | |||

|---|---|---|---|---|

| I(0) | I(1) | I(0) | I(1) | |

| CCO2e | 0.0724 | 0.2463 * | −2.3141 | −4.8119 * |

| EXP | 0.1237 | 1.5585 * | −2.1120 | −5.1189 * |

| IMP | 0.1957 | 0.7136 * | −0.7536 | −5.2604 * |

| REN | 0.2625 * | 0.1621 ** | −2.1371 | −5.5937 * |

| FD | 0.1266 | 0.2503 * | −2.1017 | −4.8810 * |

| Dimension | CCO2e | EXP | IMP | REN | FD |

|---|---|---|---|---|---|

| M2 | 44.7617 * | 44.4099 * | 38.1529 * | 28.2532 * | 18.5641 * |

| M3 | 47.1428 * | 46.6071 * | 40.1524 * | 29.2406 * | 19.3796 * |

| M4 | 50.1467 * | 49.3602 * | 42.3827 * | 30.6910 * | 20.3522 * |

| M5 | 54.6470 * | 53.3648 * | 45.6022 * | 33.1269 * | 21.8835 * |

| M6 | 60.8736 * | 59.1472 * | 50.0714 * | 36.6792 * | 24.0877 * |

| Coefficient | CV1 | CV5 | CV10 | ||

|---|---|---|---|---|---|

| β | 2211.36 | 1398.24 | 813.794 | 586.187 | |

| 284.409 | 192.786 | 120.875 | 76.4328 | ||

| β | 5628.83 | 3542.02 | 2333.68 | 1354.62 | |

| 782.396 | 511.830 | 358.278 | 233.824 | ||

| β | 7054.79 | 5512.85 | 3683.32 | 1948.55 | |

| 600.905 | 492.281 | 358.792 | 234.751 | ||

| β | 8471.78 | 6585.66 | 4661.35 | 2356.93 | |

| 794.193 | 594.904 | 382.531 | 202.847 |

| Exports | Imports | Financial Development | Renewable Energy | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| CV-5% | CV-10% | Mean | Variance | Mean | Variance | Mean | Variance | Mean | Variance | |

| 0.10 | 1.96 | 1.65 | 1.549 | 1.905 ** | 1.079 | 1.164 | 1.483 | 1.191 | 0.963 | 1.473 |

| 0.15 | 1.96 | 1.65 | 1.772 ** | 1.999 * | 1.119 | 2.076 * | 1.680 ** | 1.485 | 1.197 | 1.808 ** |

| 0.20 | 1.96 | 1.65 | 1.522 | 1.555 | 1.241 | 1.656 ** | 1.650 ** | 1.288 | 1.080 | 1.446 |

| 0.25 | 1.96 | 1.65 | 1.536 | 1.762 ** | 1.431 | 1.522 | 1.421 | 1.508 | 1.245 | 1.527 |

| 0.30 | 1.96 | 1.65 | 1.711 ** | 2.160 * | 1.542 | 2.436 * | 1.379 | 2.243 * | 1.086 | 2.352 * |

| 0.35 | 1.96 | 1.65 | 1.828 ** | 2.414 * | 1.461 | 2.782 * | 1.303 | 2.511 * | 1.266 | 2.901 * |

| 0.40 | 1.96 | 1.65 | 2.048 * | 1.618 | 1.568 | 2.207 * | 1.367 | 1.724 ** | 1.456 | 2.443 * |

| 0.45 | 1.96 | 1.65 | 2.198 * | 2.019 * | 2.219 * | 2.642 * | 1.528 | 2.367 * | 1.846 ** | 3.567 * |

| 0.50 | 1.96 | 1.65 | 1.915 ** | 1.901 ** | 1.982 * | 2.305 * | 1.485 | 2.275 * | 1.802 ** | 3.300 * |

| 0.55 | 1.96 | 1.65 | 2.193 * | 1.309 | 2.262 * | 1.843 ** | 1.654 ** | 1.956 ** | 1.825 ** | 2.334 * |

| 0.60 | 1.96 | 1.65 | 1.833 ** | 1.131 | 1.995 * | 1.602 | 1.620 | 1.583 | 1.337 | 1.890 ** |

| 0.65 | 1.96 | 1.65 | 1.536 | 1.014 | 2.118 * | 1.193 | 1.527 | 1.348 | 1.317 | 1.261 |

| 0.70 | 1.96 | 1.65 | 1.357 | 1.053 | 1.780 ** | 1.146 | 1.457 | 1.279 | 1.201 | 1.431 |

| 0.75 | 1.96 | 1.65 | 1.192 | 0.708 | 1.485 | 0.680 | 1.126 | 1.043 | 1.220 | 1.094 |

| 0.80 | 1.96 | 1.65 | 1.107 | 0.498 | 1.175 | 0.385 | 0.989 | 0.597 | 0.953 | 0.662 |

| 0.85 | 1.96 | 1.65 | 0.818 | 0.650 | 1.215 | 0.428 | 0.904 | 0.741 | 0.785 | 0.605 |

| 0.90 | 1.96 | 1.65 | 0.488 | 0.443 | 0.831 | 0.411 | 0.587 | 0.569 | 0.663 | 0.481 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Awosusi, A.A.; Adebayo, T.S.; Rjoub, H.; Wong, W.-K. How Do Financial Development and Renewable Energy Affect Consumption-Based Carbon Emissions? Math. Comput. Appl. 2022, 27, 73. https://doi.org/10.3390/mca27040073

Awosusi AA, Adebayo TS, Rjoub H, Wong W-K. How Do Financial Development and Renewable Energy Affect Consumption-Based Carbon Emissions? Mathematical and Computational Applications. 2022; 27(4):73. https://doi.org/10.3390/mca27040073

Chicago/Turabian StyleAwosusi, Abraham Ayobamiji, Tomiwa Sunday Adebayo, Husam Rjoub, and Wing-Keung Wong. 2022. "How Do Financial Development and Renewable Energy Affect Consumption-Based Carbon Emissions?" Mathematical and Computational Applications 27, no. 4: 73. https://doi.org/10.3390/mca27040073