1. Introduction

In various circumstances, investors display irrational behaviors due to different situations, feelings, emotions, and perceptions. They may include the wrong judgments in their investments and perceive them as the perfect rational choices in the stock market (

Babajide and Adetiloye 2012). Some emotions and sentiments of the investors are caused by the disposition effect or other psychological reasons, and, in turn, the psychological factors can significantly influence their investment decisions (

Summers and Duxbury 2012;

Ahmad et al. 2017b;

Barberis and Thaler 2003). In addition, most of the investors use various kinds of tools, techniques, and models, such as CAPM, capital budgeting techniques, arbitrage, etc., to process the available information and to make investment decisions, while these models ignore the investor’s emotions, feelings, and conflicts during the investment decisions (

Sanfey et al. 2003).

Some factors have little impact on investors’ behaviors, whereas some others may have a major influence on investors’ behaviors (

Iqbal et al. 2014). These factors heavily contribute to the irrational behaviors of investors when the investments from investors are based on personal experience and characteristics (

Kudryavtsev et al. 2013). Some behavioral biases, such as herd bias, anchoring, mental accounting, and overconfidence bias, have a significant impact on the investors’ investment decision making (

Ullah 2019). For example, overconfidence bias most likely occurs in active investors, while passive investors follow herding in financial markets (

Abdin et al. 2018). As the financial market consists of investors, the aggregate behavior of the investors in the market represents the behavior of the overall financial market. If a large number of investors in the market have biases in their investment decision making, certain market anomalies may occur. Stock market anomalies are usually linked with the specific kinds of financial securities, causing the securities to overperform or underperform (

Giles et al. 2014;

Thaler 2005). These anomalies explain the events (e.g., certain stock price movements) that cannot be explained by the efficient market hypothesis (

Silver 2011).

The occurrence of stock market anomalies, in turn, can influence the investors’ behaviors and overall stock market performance (

Barber and Odean 2008;

Brealey et al. 2012;

Daniel et al. 1998). Specifically, three types of anomalies, such as the fundamental, technical, and calendar anomalies, have been well known to exist in the stock market for a long time (

Lam et al. 2008). Many investors have a lack of the essential technical skills and knowledge regarding the stock market (

Frydman and Rangel 2014). These investors always follow other investors or brokers to make their investment decisions, which occur due to information generalizations and the failure of investors to conduct extra trading (

Shefrin 2002). Thus, it is important to construct the most effective financial advisory services and policies for a strong and secure financial system.

Most developed countries, such as the United States of America, have more sophisticated financial markets. In contrast, countries in emerging markets, such as Pakistan, have experienced fast economic growth but have less sophisticated financial markets. As most of the extant literature focuses on examining the investment decision making in developed countries, examining the investment decision making in an emerging market can help us better understand the behaviors of the investors and the financial market. Specifically, the Pakistan Stock Exchange has faced many ups and downs in recent times. Many investors blame this scenario on behavioral factors and the manipulation of large investors in the market. These factors have been created by prominent investors who are biased regarding investment decisions (

Hayat and Anwar 2016). Numerous studies have formed a direct relationship between behavioral biases and decisions of investment amongst individual investors. Investors may follow the other investors’ portfolios for investment decision making and ignore their own perception because of greediness or anxiety of loss (

Landberg 2003). In certain scenarios, investors may overestimate their calculations and think that their perceptions are accurate and ignore the suggestions of other investors (

Dar et al. 2021;

Larrick et al. 2007). It is also worth noting that studies show that financial knowledge has an important impression in minimizing the unreasonable conduct of behavioral biases in investment decisions (

Hsiao and Tsai 2018;

Al-Tamimi and Kalli 2009).

As Pakistan is a developing country, the individual investors in the country may not receive sufficient financial education. Thus, the majorities of individual investors in Pakistan do not know or fully understand the concept of rationality, and this scenario can highly influence their investment decisions (

Akbar et al. 2016). They are behaviorally biased, causing them to be less risk averse in certain scenarios while more risk averse in others (

Kim and Nofsinger 2008). Most studies have been implemented to examine the direct impact of behavioral biases on individual and institutional investors’ investment decisions (

Hayat and Anwar 2016). Few studies have been conducted in Pakistan to explore the multimediation mechanism between behavioral biases and the investment decision making. Thus, one primary purpose of the study is to address this gap, with a focus to inspect the multimediation mechanism that further explains the relationship between behavioral biases and investment decisions. By inspecting the alternative mediation mechanisms, we can gain a better understanding of the decision making process (

Abdin et al. 2018), potentially address some problems in the analytic process that are identified by the extant literature (

Peloza 2009), and clarify the nature of the relationship between behavioral biases and investment decisions. According to our best knowledge,

Abdin et al. (

2018) is the only study that uses the multimediation mechanism between prospect factors and investment performance, but no other studies have been conducted to check the role of financial literacy along with the multimediation mechanism between behavioral biases and investment decisions.

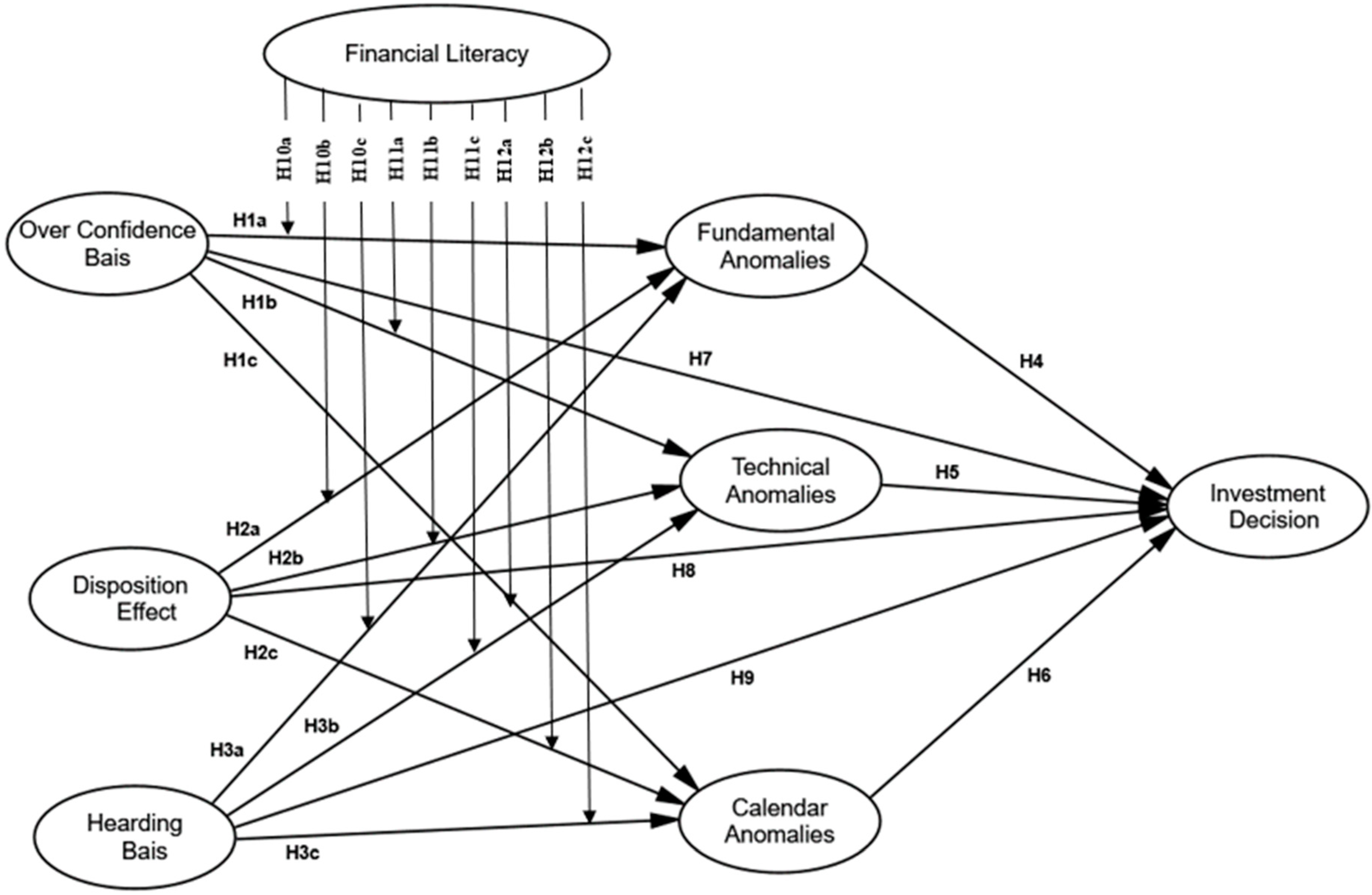

This study inspects the role of behavioral biases in investors’ investment decision making. For this purpose, we developed and distributed a questionnaire amongst the investors in the stock market in 2021. Thereafter, we collected the responses to the questionnaire from various respondents and used the data to conduct the analysis for the associations between behavioral biases, anomalies, financial literacy, and investment decisions. Specifically, this study is characterized by examining the mediating role of three modules of stock market anomalies (fundamental, technical, and calendar anomalies) between behavioral biases and investment decisions, especially the behavioral biases that integrate in their speculation choices escorting to illogical investment. Moreover, the study investigates the moderating role of financial literacy between the biases and the stock market anomalies.

The current analysis contributes to accessible writings by the accumulation of novel suggestions from an emergent economy such as that of Pakistan. Few research studies have been conducted on the perspective of behavioral finance in Pakistan. The study contributes to the existing literature in different ways, for instance, how behavioral biases affect investors’ investment decision making, how stock market anomalies mediate the association between behavioral biases and investors’ investment decision making, how financial literateness moderates the association between investors’ behavioral biases and market anomalies, and the joint effects amongst all three factors on the investors’ overall investment decision making. Furthermore, this study contributes to the literature by establishing an integrated model to identify the mediated and moderated relationship between biases of behavioral finance and decisions of investment. Moreover, the study has some important practical implications. As the evidence from the study highlights the importance of financial literacy in terms of optimal investment decision making of individuals and the stability of the overall stock market, all the relevant parties, including policymakers, financial advisers, or even individual investors, should pay special attention to financial literacy. For example, policymakers need to think about how to appropriately develop policy to improve financial literacy among market participants and to build a strong and secure financial system; financial advisers should provide proper financial education when working with clients; investors, particularly the individual investors, should pay attention to seeking proper financial training to mitigate behavioral biases in their personal investment.

The remainder of the paper is organized as follows:

Section 2 discusses the existing literature and develops hypotheses;

Section 3 presents the sample construction and research design;

Section 4 reports the main empirical results;

Section 5 provides a further discussion on the empirical results;

Section 6 concludes the paper.

2. Literature Review

Standard finance makes judgements within a defined set of outcomes, knowing all the possible consequences and alternatives for an optimum solution to wealth maximization. The individual behavior in practice differs from theory and classical financial models (

Raiffa 1968;

Kahneman and Tversky 1979). People tend to forget the general principles in investment theory and follow the intuitions and others, which contradicts rational theory (

De Bondt 1998). In such a situation, the efficient market hypothesis and rational behavior theory become incapable of predicting the market. The efficient market ideas and investment rationality conflict with behavioral biases and investors’ psychology.

Prospect theory is an assessment or review of expected utility theory that provides an eloquent representation of hesitation, and the value function evaluates only a single outcome (

Kahneman and Tversky 1979). The multiple outcomes in individual decision making interpret the value functions through prospect factors, explaining that individuals demonstrate different behavior in different situations. This happens due to the uncertain and unreliable predictions that delay the investment decisions of investors. Investors develop more risk to circumvent the shortfalls, but the same investor takes less risk when confronted with a slight increase in turnover and profits regarding future prospects. This altered risk behavior is the fundamental part of prospect theory. Investors present themselves with the possibility to upsurge or decline in shortfalls and the likelihood of declining the deficits (

Zunino et al. 2008). Moreover, investors divide their portfolios into various mental accounts, which are commonly referred to as mental buckets. There might be downside mental account protection due to fear of poverty or upside mental account protection for the chance of richness. Investors might behave as risk averse in downside mental account protection and risk seekers in upside mental account protection.

The adaptive expectation theory (

Tinbergen 1939), bounded rational theory (

Simon 1955), regret theory (

Loomes and Sugden 1982), and prospect theory (

Kahneman and Tversky 1979) collectively explain the role of heterogeneity in investors’ preferences and decisions. However, prospect theory is more appropriate when dealing with behavioral biases, anomalies, and investment in the stock market (

Barberis 2013;

Barberis et al. 2001;

Shiller 1999). They formulate their decisions based on bounded rationality, as described by the decision theory (

Barberis and Thaler 2003). The decision theory has incorrect assumptions because an investor’s judgements are not clearly defined in relation to a problem, but it is due to limited knowledge about possible outcomes. The cognitive and emotional factors influence the investor risk perception while making investment choices. They use those factors in their judgement process for various investment instruments, such as overconfidence, loss aversion, herding, and disposition effect. Moreover, the heuristic biases directly explain the investment decisions in Pakistan (

Mumtaz et al. 2018;

Malik et al. 2022;

Farooq and Sajid 2015). However, heuristic biases have markedly decreased the investment decisions of Pakistani investors due to perceived market efficiency (

Shah et al. 2018).

The aggregate effects of emotional and cognitive biases in the investors’ investment decision making lead to the stock market anomalies (

Thanki et al. 2022), whereas stock market anomalies, in turn, affect the performance of the stock market and decision making of individual investors. These anomalies are usually associated with certain kinds of securities, causing them to under- or over perform (

Thaler 2005). Such anomalies describe the events or movements of stock price that are not defined by the efficient market hypothesis (

Silver 2011). Three types of anomalies existing in the inefficient markets are fundamental anomalies, calendar anomalies, and technical anomalies. Fundamental anomalies are associated with elements of fundamental analysis (

Thushara and Perera 2013). Technical anomalies are related to technical analysis, which predicts the expected stock returns based on stock prices movement and trading volume (

Mizrach and Weerts 2009;

Bako and Sechel 2013). This refers particularly to price patterns and volume spikes (

Turner 2017) and predictive charts (

Achelis 2001). Investors attempt to make logical conjectures to navigate between stock prices and signals due to asymptotic behavior of stock prices (

Brown and Jennings 1989). Finally, the stock prices are different at different times in calendar anomalies, which is the seasonal variation in stock prices (

Thushara and Perera 2013;

Thaler 2005). These stock market anomalies occur due to irrational investor behavior and play a critical role in measuring the investment decisions of Pakistani investors (

Abdin et al. 2017). All three classes of anomalies apply under prospect theory, which helps to understand the market conditions under which individual investors behave.

2.1. Behavioral Biases and Stock Market Anomalies

2.1.1. Overconfidence and Fundamental Anomalies

Overconfidence is the risk propensity and thinking behavior of investors to be superior and better as compared to others (

De Bondt et al. 2013). They undervalue the observations and predictions of other investors but overvalue their own skills (

Forbes et al. 2016). Overconfident investors overestimate their own abilities as they ponder performing well as compared to others but in fact are not (

Lin 2012). These investors misprice the securities and overrate their observations due to overconfidence bias (

Elizabeth et al. 2020;

Parikh 2009). Overconfident investors invest in value stocks to gain profit and avoid future loss, thus indicating the value effect of fundamental anomalies (

Kudryavtsev et al. 2013;

Abdin et al. 2017). Overconfidence is the most prominent bias that adversely affects the investment decisions of individual investors and makes the market inefficient (

Waweru et al. 2008). It is most influential factor of change in stock prices and trading volume. The changes in the preferences show that changes in the price of stocks affect the perception of investors (

Doyle et al. 2021).

H1a: Degree of overconfidence bias has a significant positive affiliation with fundamental anomalies.

2.1.2. Overconfidence and Technical Anomalies

The most organized psychological attribute or bias in behavioral finance is overconfidence (

Baker et al. 2017). It is the self-attribution that addresses the earnings announcement anomaly in the stock market (

Chou et al. 2021). Technical anomalies are the bullish and bearish trend in respect of stock prices and trading volume. Overconfident investors have astonishing behavior towards the stock market in the creation of bullish market trends and high trading volume (

Ahmad et al. 2017a). Trading volume is expectedly high due to overconfidence and the depth of market increases and decreases due to overconfident traders’ expected utility. The overconfident behavior of investors affects the volatility and price quality of stocks (

Kinoshita et al. 2012). They make their decisions on the basis of available information about the market and the previous performance of stocks (

Mitroi and Stancu 2014). A decrease in stock prices from the support level (technical analysis) creates a fear of loss in the market, which induces investors to sell their stock in equilibrium. In this case, the investment decisions of the investors completely rely on technical analysis, which is the key reason for creation of technical anomalies in the stock market (

Kamoto 2014). On the other hand, the perception about the decline in stock’s worth lowers the substance level (technical analysis), and any additional forfeiture would encourage the investors to trade the security at equilibrium. They seriously depend upon the technical anomalies under such situations, which outline the technical anomalies in the securities market (

Chen et al. 2020). Different technical analyses are used to predict the future price of stock on the basis of historical stock prices by overconfident investors for making their investment decision (

Hoffmann and Shefrin 2014;

Mizrach and Weerts 2009). The historical price pattern deviates the investors from the efficient market hypothesis and generates technical anomalies in the Pakistani market (

Abdin et al. 2018).

H1b: Degree of overconfidence bias has a significant positive affiliation with technical anomalies.

2.1.3. Overconfidence and Calendar Anomalies

Overconfident investors overestimate their own abilities and personal knowledge against the information that is publicly available (

Musciotto et al. 2018). They believe that they possess more knowledge, self-achievement, superior abilities, and experience regarding the stock market, which makes them more overconfident investors (

Mitroi and Stancu 2014;

Pompian 2011). Calendar anomalies are in different categories, such as day anomaly, moon anomaly, and holiday anomaly (

Barak 2008). The poorly performed stocks in December are more probably retrieved in January, which is the driving force for discrete investors to trade in those stocks and receive tax benefits (

Branch and Chang 1990). Most overconfident investors prefer to sell their stock at the end of the year to reap tax benefits. This suggests that they are overconfident in terms of calendar anomalies (

Lee et al. 2013).

Ahn et al. (

2014) investigated that overconfident investors seem very active during the year end and weekend, which creates the calendar anomalies in the stock market.

H1c: Degree of overconfidence bias has a significant positive affiliation with calendar anomalies.

2.1.4. Disposition Effect and Fundamental Anomalies

Disposition effect narrates the inclination or propensity of investors to sell the winning stocks immediately with the increase in stock prices and hold the stocks that have dropped in value (

Singh 2016). This happens due to loss aversion behavior in connection with loss and a rapid increase in wealth transformation (

Niehaus and Shrider 2014;

Pompian 2011). Disposition effects seem to occur more in male investors rather than female investors. These are emotions that cause the occurrence of disposition effect, causing the investors to trade stocks without regret after knowing the monetary turnover on them (

Summers and Duxbury 2012). Prospect theory derives the disposition effect in connection with intrinsic value and equilibrium price of stocks (

Hasler and Lusardi 2019). It all depends upon news in stocks that divert the investment decisions of investors (

Pelster and Hofmann 2018). A news announcement creates a fundamental anomaly in the stock market because stock prices go up or down accordingly with the announcement (

Ahmed and Doukas 2021).

H2a: Degree of disposition effect has a significant positive affiliation with fundamental anomalies.

2.1.5. Disposition Effect and Technical Anomalies

Regarding the phenomenon to avoid loss, retail investors sell or quit winning stock speedily and keep loser stocks for an extended period in disposition effect (

Taffler et al. 2017).

Shefrin and Statman (

1985) revealed that the investors who kept their losing investment for a long time and sell winning stock too early may cause disposition for different asset classes. This kind of forecasting about stock returns is grounded in preceding risk and uncertainty (

Azzopardi 2010). Investors make financial decisions with some prospects in mind (

Thaler 2005). Investors use technical analysis to predict future stock prices with the help of past stock prices (

Konstantinidis et al. 2012). This entire phenomenon about disposition effect and technical analysis is based upon prospect theory (

Grinblatt and Han 2005). This theory suggests that the investor cannot act rationally all the time (

Kumar and Goyal 2015). Since investors in disposition effect do not involve reasonable conclusions while handling each element of an investment discretely (

Bekiros et al. 2017), they might depend upon technical analysis to make investment decisions that generate the technical anomalies in stock market.

H2b: Degree of disposition bias has a significant positive affiliation with technical anomalies.

2.1.6. Disposition Effect and Calendar Anomalies

Investors consider the gains and losses before making any investment decision. The prospect-theory-based disposition effect identifies that every single investor frames their prospects in accordance with the value function relative to a reference point (

Thaler 2005;

Kahneman and Tversky 1979). Investors evaluate the gains and losses separately and treat the assets accordingly (

Lewis 2017). It is observed that losses have a very strong emotional effect on investors (

Azzopardi 2010). The loss aversion theory explained that individual investors are more concerned with losses and gains. However, rational investors do this oppositely for tax benefits (

Singh 2016). Investors minimize the taxes at the end of the year and less disposition effect is observed at the end of the year (

Taffler et al. 2017). They are reluctant to incur any loss but choose to sell losing stocks in December for tax reasons and start to invest in smaller firms’ stocks that are likely to provide huge returns in January (

Haug and Hirschey 2006). The convinced improvement in January indicates the investors as risk averse in calendar anomalies.

H2c: Degree of disposition effect has a significant positive affiliation with calendar anomalies.

2.1.7. Herding Bias and Fundamental Anomalies

Every single investor in the stock market without any proper direction creates the herding bias (

Braha 2012). It is observed that uncertainty and fear of loss might influence the investors in selling their stocks. They armed themselves with inferior information and others have superior information (

Shukla et al. 2020). This happens due to fear of loss and greed (

Landberg 2003). The occurrence of herding bias in the stock market is due to the enormity of risk perception with returns of stock (

Shah et al. 2017). The herding bias of the investor is created due to the investors’ intent to avoid or reduce the level of risk they take (

Ullah and Elahi 2015). Individuals behave irrationally during herding behavior in response to a change in stock price. For instance, they see the large investors are selling their stocks and start following them in selling their stocks quickly (

Dodonova and Khoroshilov 2005). It all depends upon an announcement effect in the stock market that describes the tendency of fluctuations in stock prices to continue even after the very first declarations. Simply, investors follow the positive and negative news announcements and react accordingly (

Joo and Durri 2017).

H3a: Degree of herding bias has a significant positive affiliation with fundamental anomalies.

2.1.8. Herding Bias and Technical Anomalies

The factors of herding behavior greatly influence the financial choice and trading behavior of individual investors (

Baddeley et al. 2010). Moreover, demographic traits determine the risk-taking behavior and financial behavior in the stock market (

Bashir et al. 2013). Investors with herding behavior concentrate to follow the directions and information of other investors in lieu of their own (

Elizabeth et al. 2020). They act irrationally and set forth the others’ judgment with the increase in herding behavior in the stock market (

Kumar and Goyal 2015). These investors do not have an idea about how and where to invest due to low-risk propensity, which causes them to follow the opinion or direction of other investors (

Islam 2012).

Huang et al. (

2016) investigated that institutional investors have a positive strong relationship with herding behavior with respect to risk and return since herding behavior does not always entail rational decisions and investors may rely on technical analysis to make investment decisions, thereby creating technical anomalies in the stock market (

Pompian 2011).

H3b: Degree of herding bias has a significant positive affiliation with technical anomalies.

2.1.9. Herding Bias and Calendar Anomalies

In financial markets, herding is the inclination of the market investors to observe the stock, ignoring their own private information (

Braha 2012). They follow the choice of majority investors instead of anticipating their personal information due to return fluctuations (

Lin 2012). The herding behavior of investors can also be influenced by information unavailability (

Ben Mabrouk 2018). It is a common likelihood in human nature to follow, imitate, and notice the behavior of other investors during irregular market conditions (

Yu et al. 2018). Investors and managers prefer to follow others’ beliefs and opinions that affect the investment (

Filiz et al. 2018). Herding behavior is more profound in unstable market conditions, such as misrepresentation, price bubbles, and rumors (

Mertzanis and Allam 2018). Investors are reluctant to incur any losses and choose to sell their losing stocks in December for tax reasons and then invest in smaller firms that are likely to provide a high return in January (

Haug and Hirschey 2006). This tendency to follow most likely occurs at diverse times of the month that create the calendar anomalies in the stock market.

H3c: Degree of herding bias has a significant positive affiliation with calendar anomalies.

2.2. Stock Market Anomalies and Investment Decisions

2.2.1. Fundamental Anomalies and Investment Decisions

The stock price does not show the intrinsic or fundamental value in fundamental anomalies that increase the price in the stock market (

Foorthuis 2021). There are many factors that influence stock prices (

Graham et al. 2009). According to those factors, investors follow the growing stocks in the stock market rather than overvalued stocks. This concentrating behavior about stocks affects the investment trading behavior of investors. Value stocks are abandoned with the reason of risk and inaccurate investors’ decisions (

Abdin et al. 2018). This component is categorized as a fundamental anomaly that impacts the investment decisions. The irregularities that are linked with a stock’s value are referred to as the fundamental anomalies (

Pompian 2011). These anomalies are the reasons to create fundamental analysis while trading the stocks. They change the stock prices, which has a huge impact on investment behavior and investment performance (

Waweru et al. 2008). Investors tend to select stocks attracting their attention whatever their fundamentals are in Pakistan, thus influencing the investment performance (

Abdin et al. 2018). As a result, fundamental anomalies positively impact the investment performance in Pakistan (

Malik et al. 2022). However, fundamental anomalies restrained them from investments in Pakistan due to inability in obtaining abnormal returns (

Zafar and Siddiqui 2020).

H4: There is a significant positive affiliation between fundamental anomalies and individuals’ investment decisions.

2.2.2. Technical Anomalies and Investment Decisions

The affiliation between technical anomalies and efficient market hypothesis is not consistent (

Pompian 2011). The anomalies determine the trends in the stock market, which are based on past stock prices and volume. This trend in stock prices and anomalies has a huge influence on investors’ investment decisions (

Latif et al. 2011). Therefore, technical analysis is performed to predict the future price behavior based on previous stock prices and trading volume in the stock market (

Bako and Sechel 2013). The behavioral pattern gives rise to technical analysis to opt for prompt investment choices. The past prices and volumes of stock are being used to perform technical analysis to predict stock returns (

Mizrach and Weerts 2009). An investor’s investment decisions heavily rely on technical anomalies to gain abnormal returns from the market (

Taylor 2011). The technical anomalies influence the investors to use technical analysis for ease of interpretation and to highlight future prices for making investment decisions, affecting the investment performance (

Abdin et al. 2018). The technical anomalies increase the investment performance in Pakistan (

Malik et al. 2022). Another study in Pakistan indicates that technical analysis is useless in semi-strong and strong forms of market efficiency because investors cannot obtain abnormal returns that restrain them from investments (

Zafar and Siddiqui 2020).

H5: There is a significant positive affiliation between technical anomalies and individuals’ investment decisions.

2.2.3. Calendar Anomalies and Investment Decisions

Calendar anomalies are comprised of the January effect or weekend effect (

Taylor 2011;

Singal 2014), which imitate the value of stocks (

Joo and Durri 2017). It is difficult to regulate the stock prices in these circumstances. The seasonal outcome endangers the stock prices, which makes the market unproductive and forces the investors to cross the market in a definite way. Investors sell losing stocks at the end of year with the goal of avoiding taxes. This induces them to capitalize on small companies that propose advance returns (

Schultz 1985). A contradictory and weak January effect is testified to in relation to utmost stock returns (

Tonchev and Kim 2004). During the last 15 min of a day, the stock prices and trading volumes tend to increase (

Guin 2005). For instance, investors seem to be very active at the end of the year (

Abdin et al. 2018).

Giovanis (

2016) test the month of year effect through the GARCH model and experience the uppermost return in December in twenty stock markets, February effect in nine markets, January effect in seven, while April effect in six stock markets. The same situation happens in Pakistan that stock returns are highest at the end of the calendar year but the return lowers afterwards (

Anjum 2020). The Pakistan equity market exhibits positive returns in the last day of the week and illustrates negative returns in the last day of the week (

Alvi et al. 2021). This trend of stock prices is due to the calendar effect that influences the investment decisions.

H6: There is a noteworthy optimistic affiliation amidst calendar anomalies and individuals’ investment decisions.

2.3. Behavioral Biases and Investment Decisions

2.3.1. Herding Bias and Investment Decisions

Herding is the psychological element that has an impact on an investor’s decisions (

Abul 2019). It is the mutual tendency of human nature to mention, witness, and replicate someone’s conduct in an asymmetrical disorder in stock markets (

Rompotis 2018). However, the existence of herding enforces them to act irrationally for investment decisions. They desire to follow the other investors with certainty and for accurate speculation. Herd behavior designates how a cluster of people performs and invests altogether (

Braha 2012). It is perceived that investors discard their own investment choices during panics and subsequently follow other investors with the vision that they possess additional information about market conduct (

Gao et al. 2021). They hesitate to invest because of greed and fear of loss (

Landberg 2003). Generally, investors perform a similar thing for investment in stocks under the shadow of other investors. This happens due to idle and less trained behavior of investors (

Persaud 2000). Some agents are equipped to follow the people possessing the richest information, a behavior called herding (

Mello et al. 2010). Herd investors are inclined to confine their choices and follow other investors. Herding overwhelms the stock market, such as market anomalies and bubbles in the market (

Mertzanis and Allam 2018). The positive feedback strategy influences every individual investor to follow the crowd (herd) for the purpose of buying and selling of stock during bullish market trends (

Kim and Ryu 2021). Herding behavior interacts negatively in a bullish market trend, but it positively interacts in a bearish market trend (

Shah et al. 2019). Investment decision making is significantly affected by herding behavior (

Raheja and Dhiman 2019;

Boda and Sunitha 2018;

Almansour and Arabyat 2017;

Dominic and Gupta 2020).

Shah et al. (

2017) stated that herding exists in the Pakistan stock market, which affects the investment. However, this herding behavior does not affect the investment decisions in some circumstances (

Ahmed et al. 2022). The herding behaviors do not change the investment policy and preference of investors that belong to stocks. Investors’ sentiments in such situations are aligned with the phenomenon “slow rise and sharp fall” (

Gong et al. 2022). In the case of a fall in prices, the herding is more obvious in the market. Herding behavior occurs more frequently in investment decisions of investors in Pakistan (

Aftab 2020;

Katper et al. 2019). However, herding bias is insignificantly related to investment decisions of investors in Pakistan (

Ahmed et al. 2022;

Quddoos et al. 2020).

H7: Herding bias has significant and positive influence on investment decision making.

2.3.2. Overconfidence Bias and Investment Decisions

H8: Overconfidence has a substantial and confident effect on investment decisions.

2.3.3. Disposition Effect and Investment Decisions

The disposition effect indicates to hold stocks when prices go down and sell immediately whenever prices go up (

Pelster and Hofmann 2018). This happens for the reason that they are losing indifferently and want to produce principal advances rapidly (

Lin 2011). The proposition of disposition effect depends upon investment styles and market cycles (

Bernard et al. 2018). The presence of the disposition effect helps the speculative investors in speculation activities (

Summers and Duxbury 2012). Likewise, disposition bias is more pronounced in broader situations as compared to precise situations (

Bekiros et al. 2017). Moreover, discrete investors are more susceptible to the disposition effect as compared to external and established investors (

Roger 2009). The amount of instruction of discrete investors has a confident affiliation with the disposition effect. The disposition effect fluctuates the cross-market situations and exhibits its role in mutual fund investments (

Lee et al. 2013). The disposition effect has a strong impact on investment decisions (

Ploner 2017). The impact of disposition effect on investment is strong in long position rather than short position (

Madaan and Singh 2019). The investors that are following the disposition effect would be likely to make more investment decisions (

Siraji et al. 2021;

Ahmed et al. 2022). However,

Adil et al. (

2022) found an insignificant influence of disposition effect on investment choices.

H9: Disposition Effect has substantial and optimistic influence on investment decision making.

2.4. Role of Financial Literacy among Behavioral Biases and Stock Market Anomalies

2.4.1. Financial Literacy Has Moderating Role Amidst Behavioral Biases and Fundamental Anomalies

The financial knowledge in relation to investment describes the sum of information about monetary benefits and is a key component of cognitive behavior (

Mirza et al. 2022). The financial literacy is the investor’s competence to understand the money market and the way to wealth maximization (

Giesler and Veresiu 2014). The financial literacy incredibly contributes to accurate speculation, investment choices, and reserves (

Idris et al. 2013). The financial monetary knowledge helps to perform the monetary decisions in an understandable way (

Hilgert et al. 2003;

Robb and Woodyard 2011). Well-educated investors in the stock market continuously use accurate methods and tools before making investment choices. They consider the value of firm and firm size for investment decisions, which lead to fundamental anomalies in the stock market. On the other hand, low-literacy investors always follow the instructions of other investors or follow the advice of family, friends, and stockbrokers. Due to the low literacy of investors in the financial market, different kinds of behavioral biases are raised in stock market (

Al-Tamimi and Kalli 2009).

H10a: Financial literacy moderates amidst overconfidence bias and fundamental anomalies.

H10b: Financial literacy moderates amidst disposition effect and fundamental anomalies.

H10c: Financial literacy moderates amidst herding bias and fundamental anomalies.

2.4.2. Financial Literacy Has Moderating Role Amidst Behavioral Biases and Technical Anomalies

The financially literate investors overvalue their skills, talent, and occupation, which is depicted as overoptimism, which is injurious for speculations (

Mandell and Klein 2009). The financial literacy is quite an extensive expression that recognizes the financial literateness of investors and helps them in changing their financial decisions. Investors who have financial knowledge can make different calculations and analysis before making an investment decision, and this creates the technical anomaly in the stock market (

Hayat and Anwar 2016). However, lower financial knowledge leads them to yield to the guidance of acquaintances, family associates, or stock agents. These investors typically demonstrate themselves as overoptimistic, displaying herding behavior and disposition effect for the reason that they were uneducated. Thus, they are incapable of making decisions and make incorrect investment choices (

Al-Tamimi and Kalli 2009).

H11a: Financial literacy moderates amidst overconfidence bias and technical anomalies.

H11b: Financial literacy moderates amidst disposition effect and technical anomalies.

H11c: Financial literacy moderates amidst herding bias and technical anomalies.

2.4.3. Financial Literacy Has Moderating Role Amidst Behavioral Biases and Calendar Anomalies

The level of financial knowledge and calendar anomalies determine that investors who are financially more literate are more active at the end of the year or beginning of the month. It is observed that financially literate investors are active during the start of the week and end of the week due to calendar anomalies in these days. Nevertheless, some investors follow others because of low financial knowledge, leading to the creation of different kinds of behavioral biases in the stock market. Investors widely integrate these behavioral biases in their investment choices (

Kahneman and Tversky 1979;

Odean 1998;

Dhar and Zhu 2002;

Weber and Camerer 1998). These biases and the announcement effect are subject to biased results (

Idris et al. 2013;

Hilgert et al. 2003;

Robb and Woodyard 2011).

H12a: Financial literacy moderates amidst overconfidence bias and calendar anomalies.

H12b: Financial literacy moderates amidst disposition effect and calendar anomalies.

H12c: Financial literacy moderates amidst herding bias and calendar anomalies.

5. Discussion

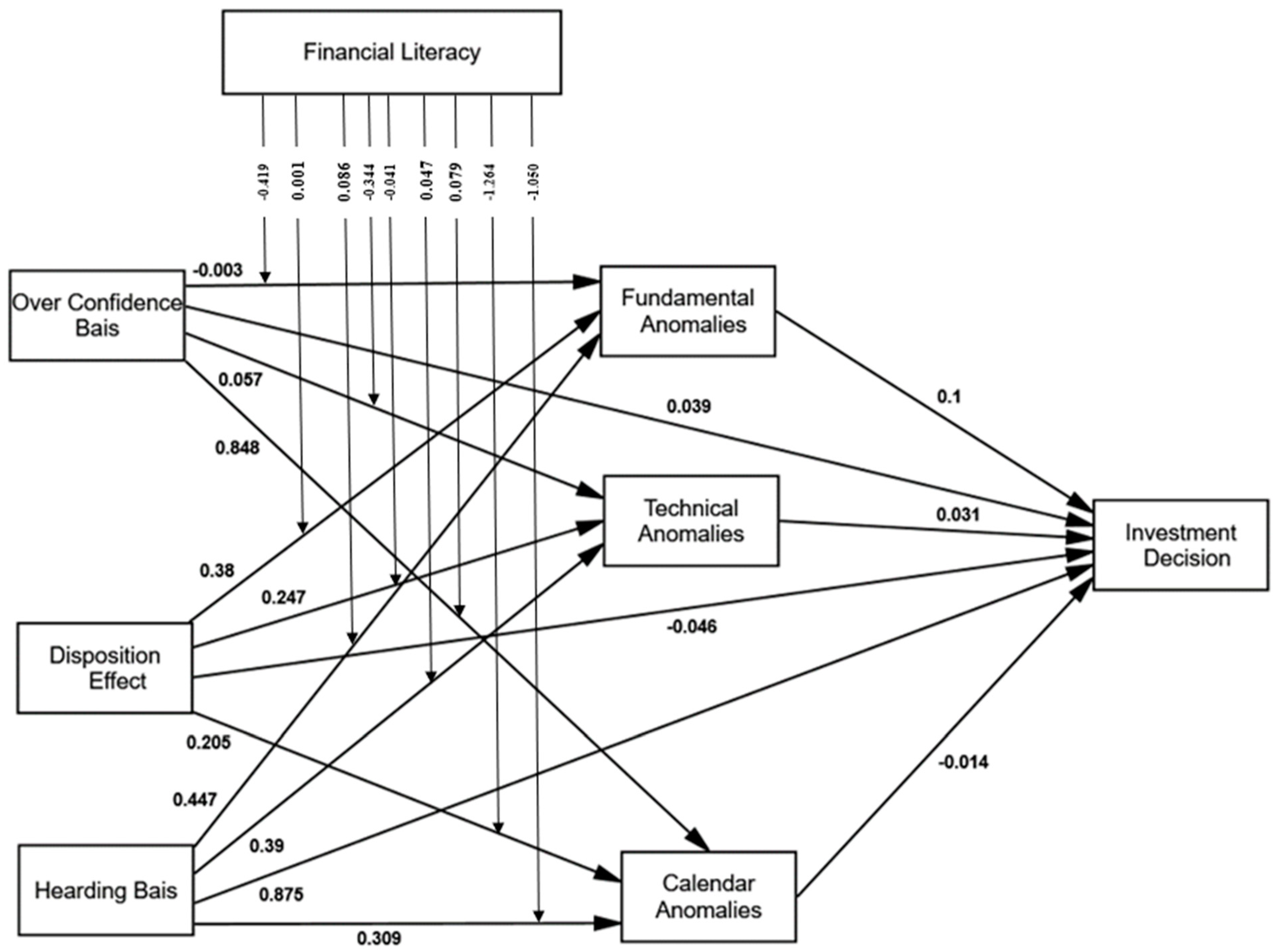

This section provides a summary and further discussion on the empirical results. The results from

Table 6 indicate that overconfidence bias (OB) has no significant relationship with fundamental anomalies, lending support to the rejection of H1a. This result suggests that fundamental anomalies (FA) are not explained by the overconfidence behavior of investors, although the extant literature suggests that investors’ behavior can cause fundamental anomalies in the market (

Abdin et al. 2018). However, the results from

Table 6 also suggest that overconfidence bias (OB) has a direct relationship with technical anomalies (TA), leading to the acceptance of H1b. The evidence does support findings from the extant literature that investors’ behavior in the stock market can lead to the creation of technical anomalies (TA), such as earnings announcement anomalies, the creation of an unusually bullish or bearish market, and high trading volume in the market (

Baker et al. 2007;

Chou et al. 2021;

Ahmad et al. 2017a). Furthermore, the results from

Table 6 reveal that overconfidence bias (OB) also has a direct positive relationship with calendar anomalies, ensuring the acceptance of hypothesis H1c. The results suggest that the overconfidence behavior in the market would create calendar anomalies, such as a January effect, as documented in the extant literature (e.g.,

Khan et al. 2017;

Mitroi and Stancu 2014;

Lee et al. 2013).

The results from

Table 6 also demonstrate that the disposition effect (DE) has a direct relationship with stock market anomalies (i.e., fundamental, technical and calendar anomalies), accepting hypotheses H2a, H2b, and H2c. The extant literature has documented multiple pieces of evidence that the presence of a disposition effect in the stock market resultantly strengthens the stock market anomalies (

Taffler et al. 2017;

Singh 2016). For example, investors are inclined to sell winning stocks and hold losing stocks. Investors who kept their losing investment for a long time and sold winning stock too early may cause disposition for different asset classes (

Shefrin and Statman 1985). This happens due to risk aversion behavior and perceived risk, which is in support of prospect theory (

Grinblatt and Han 2005). Overall, the study accepts H2a, H2b, and H2c.

Similarly, the results from

Table 6 confirm the direct link between herding behaviors (HB) and stock market anomalies, supporting H3a, H3b, and H3c. The results imply that the herding behaviors of the investors in the stock market is also the reason for stock market anomalies. Investors provided themselves with inferior information and others have superior information (

Shukla et al. 2020). Herding behavior in the stock market is because of loss and risk avoidance (

Ullah and Elahi 2015). It depends upon market fundamentals and stock price fluctuations. Investors act irrationally in their judgments, which most likely causes anomalies in the market (

Pompian 2011). Overall, the study accepts H3a, H3b, and H3c.

Furthermore, the results from

Table 6 suggest that the fundamental anomalies (FA) have a positive and significant association with the investment decisions (ID), lending support to H4. The result implies that investors do rely on the existing fundamental anomalies in the market, such as the deviation of stock price from its intrinsic value, to make further investment decisions, which is consistent with some empirical findings in the extant literature (

Pompian 2011;

Abdin et al. 2018;

Singh 2016). For instance, investors may follow growing stocks and abandon value stocks for their investment decisions. However, the results from

Table 6 do not support H5 or H6, indicating that technical and calendar anomalies are less attractive in terms of investors’ investment decision making.

Moreover, the results from

Table 6 indicate that the herding bias (HB) has a direct positive relationship on the investment decisions of investors, accepting hypothesis H7. The findings reveal that the investors in the stock market follow the moves of other investors during their stock trading because of risk averse and loss averse attitudes; the herding behavior of the investors, in turn, influences the investors’ further investment decision making (

Daniel et al. 2002;

Krugman 2009;

Ullah and Elahi 2015). Inversely, overconfidence bias (OB) and disposition effect (DE) are far less attractive in terms of investors’ investment decision making, and the result does reject H8 and H9. It is worth noting that the results from

Table 7 confirm the mediating role of certain stock market anomalies for the association between certain behavioral biases and investment decisions.

Table 8,

Table 9 and

Table 10 report the results related to the moderation role of financial literacy (FL) between various behavioral biases and stock market anomalies, representing hypotheses 10, 11, and 12. As can be seen from the tables, financial literacy (FL) plays a significant role between certain behavioral biases and stock market anomalies. The overall results from the tables thereby lend support to H10a, H11a, H12b, and H12c, but not H10b, H10c, H11b, H11c, and H12a. Our findings are consistent with some empirical evidence from the extant literature; for instance, financial literacy lessens the level of behavioral biases of the investors as investors with better financial literacy can continuously use the appropriate tools and methods to estimate equity value more accurately and thus make more rational investment decisions (

Mirza et al. 2022;

Thanki et al. 2022;

Giesler and Veresiu 2014).

Interestingly, most of our findings, as well as some investors’ irrational behaviors, can be explained by the behavioral finance theories, such as prospect theory. For example, the investors in the stock market are psychologically biased and are more sensitive to loss rather than gain. Psychologically biased investors create biases in the market, due to which the investor deviates from the actual returns. The existence of behavioral biases in the market can create anomalies in the stock market, which effects the investment decisions of the investor.

Male

Male

{kind=link}

{kind=link}

{kind=link}