Big Data Analytics to Support Open Innovation Strategies in Banks

Abstract

:1. Introduction

- What are the essential strategic resources required to create effective OIS for banks?

- What is the role of BDA in creating and managing OIS for banks?

2. Literature Review

2.1. Background of OI

2.2. Operationalizing BDA in Banks

2.3. Operationalizing BDA in Banks

2.4. Theoretical Background and Hypotheses Development

3. Materials and Methods

3.1. Construct Operationalization

3.2. Data Collection Process

3.3. Data Analysis Procedures

4. Results and Discussion

4.1. Model Estimation

4.2. Common Method Bias (CMB)

4.3. Endogeneity Test

4.4. Hypotheses Testing

5. Discussion and Conclusions

5.1. Research Contribution

5.2. Theoretical Implications

5.3. Implications for Practice

5.4. Limitations and Future Research

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Ahn, Joon Mo, Tim Minshall, and Letizia Mortara. 2017. Understanding the Human Side of Openness: The Fit between Open Innovation Modes and CEO Characteristics. R&D Management 47: 727–40. [Google Scholar] [CrossRef] [Green Version]

- Ahn, Joon Mo, Nadine Roijakkers, Riccardo Fini, and Letizia Mortara. 2019. Leveraging Open Innovation to Improve Society: Past Achievements and Future Trajectories. R&D Management 49: 267–78. [Google Scholar] [CrossRef]

- Akter, Shahriar, Samuel Fosso Wamba, Angappa Gunasekaran, Rameshwar Dubey, and Stephen J. Childe. 2016. How to Improve Firm Performance Using Big Data Analytics Capability and Business Strategy Alignment? International Journal of Production Economics 182: 113–31. [Google Scholar] [CrossRef] [Green Version]

- Alam, Nafis. 2021. Digital Banking Is Key to Financial Inclusion in Malaysia. Available online: https://www.eastasiaforum.org/2021/09/10/digital-banking-is-key-to-financial-inclusion-in-malaysia/ (accessed on 11 April 2023).

- Alassaf, Deemah, Marina Dabić, Dara Shifrer, and Tugrul Daim. 2020. The Impact of Open-Border Organization Culture and Employees’ Knowledge, Attitudes, and Rewards with Regards to Open Innovation: An Empirical Study. Journal of Knowledge Management 24: 2273–97. [Google Scholar] [CrossRef]

- Alberti-Alhtaybat, Larissa V., Khaldoon Al-Htaybat, and Khalid Hutaibat. 2019. A Knowledge Management and Sharing Business Model for Dealing with Disruption: The Case of Aramex. Journal of Business Research 94: 400–7. [Google Scholar] [CrossRef]

- Ali, Qaisar. 2018. Service quality from customer perception: Comparative analysis between Islamic and conventional bank. Journal of Marketing and Consumer Research 43: 70–82. [Google Scholar]

- Ali, Qaisar, Hakimah Yaacob, Shazia Parveen, and Zaki Zaini. 2021. Big Data and Predictive Analytics to Optimise Social and Environmental Performance of Islamic Banks. Environment Systems and Decisions 41: 616–32. [Google Scholar] [CrossRef]

- Antons, David, Robin Kleer, and Torsten Oliver Salge. 2016. Mapping the Topic Landscape of JPIM, 1984–2013: In Search of Hidden Structures and Development Trajectories. Journal of Product Innovation Management 33: 726–49. [Google Scholar] [CrossRef]

- Armstrong, J. Scott, and Terry Overton. 1977. Estimating Non Response Bias Mail Surveys. Journal of Marketing Research 14: 396–402. [Google Scholar] [CrossRef] [Green Version]

- Bagherzadeh, Mehdi, Stefan Markovic, and Marcel Bogers. 2021. Managing Open Innovation: A Project-Level Perspective. IEEE Transactions on Engineering Management 68: 301–16. [Google Scholar] [CrossRef]

- Barlatier, Pierre-Jean, Anne-Laure Mention, and Avni Misra. 2020. The Interplay of Digital Technologies and the Open Innovation Process: Benefits and Challenges. In Open Innovation: Bridging Theory and Practice—Managing Digital Open Innovation. Singapore: World Scientific Publishing Co Pte Ltd., pp. 1–34. [Google Scholar]

- Barney, Jay. 1991. Firm resources and sustained competitive advantage. Journal of Management 17: 99–120. [Google Scholar] [CrossRef]

- Bayraktar, Nihal, and Yan Wang. 2006. Banking Sector Openness and Economic Growth. Policy Research Working Paper No. 4019. Washington, DC: World Bank. Available online: https://openknowledge.worldbank.org/handle/10986/9273 (accessed on 13 March 2022).

- Bekaert, Geert, Campbell R. Harvey, and Christian Lundblad. 2011. Financial Openness and Productivity. World Development 39: 1–19. [Google Scholar] [CrossRef] [Green Version]

- Bertello, Alberto, Alberto Ferraris, Stefano Bresciani, and Paola De Bernardi. 2021. Big Data Analytics (BDA) and Degree of Internationalization: The Interplay between Governance of BDA Infrastructure and BDA Capabilities. Journal of Management and Governance 25: 1035–55. [Google Scholar] [CrossRef]

- Bertello, Alberto, Paola De Bernardi, Alberto Ferraris, and Stefano Bresciani. 2022. Shedding Lights on Organizational Decoupling in Publicly Funded R&D Consortia: An Institutional Perspective on Open Innovation. Technological Forecasting and Social Change 176: 121433. [Google Scholar] [CrossRef]

- Bigliardi, Barbara, Giovanna Ferraro, Serena Filippelli, and Francesco Galati. 2021. The Past, Present and Future of Open Innovation. European Journal of Innovation Management 24: 1130–61. [Google Scholar] [CrossRef]

- Bogers, Marcel, Ann-Kristin Zobel, Allan Afuah, Esteve Almirall, Sabine Brunswicker, Linus Dahlander, Lars Frederiksen, Annabelle Gawer, Marc Gruber, Stefan Haefliger, and et al. 2017. The Open Innovation Research Landscape: Established Perspectives and Emerging Themes across Different Levels of Analysis. Industry and Innovation 24: 8–40. [Google Scholar] [CrossRef]

- Bogers, Marcel, Henry Chesbrough, and Carlos Moedas. 2018a. Open Innovation: Research, Practices, and Policies. California Management Review 60: 5–16. [Google Scholar] [CrossRef]

- Bogers, Marcel, Nicolai J. Foss, and Jacob Lyngsie. 2018b. The ‘Human Side’ of Open Innovation: The Role of Employee Diversity in Firm-Level Openness. Research Policy 47: 218–31. [Google Scholar] [CrossRef]

- Bogers, Marcel, Henry Chesbrough, Sohvi Heaton, and David J. Teece. 2019. Strategic Management of Open Innovation: A Dynamic Capabilities Perspective. California Management Review 62: 77–94. [Google Scholar] [CrossRef]

- Bresciani, Stefano, Alberto Ferraris, and Manlio Del Giudice. 2018. The Management of Organizational Ambidexterity through Alliances in a New Context of Analysis: Internet of Things (IoT) Smart City Projects. Technological Forecasting and Social Change 136: 331–38. [Google Scholar] [CrossRef]

- Brown, P., C. Von Daniels, N. M. P. Bocken, and A. R. Balkenende. 2021. A Process Model for Collaboration in Circular Oriented Innovation. Journal of Cleaner Production 286: 125499. [Google Scholar] [CrossRef]

- Capurro, Rosita, Raffaele Fiorentino, Stefano Garzella, and Alessandro Giudici. 2022. Big Data Analytics in Innovation Processes: Which Forms of Dynamic Capabilities Should Be Developed and How to Embrace Digitization? European Journal of Innovation Management 25: 273–94. [Google Scholar] [CrossRef]

- Caputo, Andrea, Raffaele Fiorentino, and Stefano Garzella. 2019. From the Boundaries of Management to the Management of Boundaries. Business Process Management Journal 25: 391–413. [Google Scholar] [CrossRef] [Green Version]

- Chen, C. L. Philip, and Chun-Yang Zhang. 2014. Data-Intensive Applications, Challenges, Techniques and Technologies: A Survey on Big Data. Information Sciences 275: 314–47. [Google Scholar] [CrossRef]

- Chesbrough, Henry. 2003. Open Innovation: The New Imperative for Creating and Profiting from Technology. Brighton: Harvard Bus. Press. [Google Scholar]

- Chesbrough, Henry. 2004. Managing Open Innovation. Research-Technology Management 47: 23–26. [Google Scholar] [CrossRef]

- Chesbrough, Henry. 2006. New puzzles and new findings. In Open Innovation: Researching a New Paradigm. Edited by Chesbrough Henry, Wim Vanhaverbeke and West Joel. Oxford: Oxford University Press, pp. 1–12. [Google Scholar]

- Chesbrough, Henry, and Marcel Bogers. 2014. Explicating open innovation: Clarifying an emerging paradigm for understanding innovation. In New Frontiers in Open Innovation. Edited by Henry Chesbrough, Wim Vanhaverbeke and West Joel. Oxford: Oxford University Press, pp. 3–28. [Google Scholar]

- Chin, Wynne W. 1998. The partial least squares approach to structural equation modeling. Modern Methods for Business Research 295: 295–336. [Google Scholar]

- Cohen, J. 1988. Statistical Power Analysis for the Behavioral Sciences, 2nd ed. Hillsdale: Erlbaum. [Google Scholar]

- Damanpour, Fariborz, Richard M. Walker, and Claudia N. Avellaneda. 2009. Combinative Effects of Innovation Types and Organizational Performance: A Longitudinal Study of Service Organizations. Journal of Management Studies 46: 650–75. [Google Scholar] [CrossRef]

- Davidson, Russell, and James G. MacKinnon. 1993. Estimation and Inference in Econometrics. New York: Oxford University Press. [Google Scholar]

- De Mauro, Andrea, Marco Greco, and Michele Grimaldi. 2016. A Formal Definition of Big Data Based on Its Essential Features. Library Review 65: 122–35. [Google Scholar] [CrossRef]

- Del Vecchio, Pasquale, Alberto Di Minin, Antonio Messeni Petruzzelli, Umberto Panniello, and Salvatore Pirri. 2018. Big Data for Open Innovation in SMEs and Large Corporations: Trends, Opportunities, and Challenges. Creativity and Innovation Management 27: 6–22. [Google Scholar] [CrossRef]

- Diebold, Francis X., Ghysels Eric, Mykland Per, and Zhang Lan. 2019. Big data in dynamic predictive econometric modeling. Journal of Econometrics 212: 1–3. [Google Scholar] [CrossRef]

- Du, Jingshu, Bart Leten, and Wim Vanhaverbeke. 2014. Managing Open Innovation Projects with Science-Based and Market-Based Partners. Research Policy 43: 828–40. [Google Scholar] [CrossRef]

- Duan, Lian, and Ye Xiong. 2015. Big data analytics and business analytics. Journal of Management Analytics 2: 1–21. [Google Scholar] [CrossRef]

- Dubey, Rameshwar, Angappa Gunasekaran, and Stephen J. Childe. 2019. Big Data Analytics Capability in Supply Chain Agility. Management Decision 57: 2092–112. [Google Scholar] [CrossRef] [Green Version]

- Elia, Gianluca, Antonio Messeni Petruzzelli, and Andrea Urbinati. 2020. Implementing Open Innovation through Virtual Brand Communities: A Case Study Analysis in the Semiconductor Industry. Technological Forecasting and Social Change 155: 119994. [Google Scholar] [CrossRef]

- Enkel, Ellen, Gassmann Oliver, and Henry Chesbrough. 2009. Open R&D and open innovation: Exploring the phenomenon. R&D Management 39: 311–16. [Google Scholar] [CrossRef]

- Erevelles, Sunil, Nobuyuki Fukawa, and Linda Swayne. 2016. Big Data Consumer Analytics and the Transformation of Marketing. Journal of Business Research 69: 897–904. [Google Scholar] [CrossRef]

- Eriksson, Kent, and Jan Mattsson. 1996. Organising for Market Segmentation in Banking: The Impact from Production Technology and Coherent Bank Norms. The Service Industries Journal 16: 35–45. [Google Scholar] [CrossRef]

- Fasnacht, Daniel. 2018. Open Innovation in the Financial Services—the Magic Bullet. In Open Innovation Ecosystems: Creating New Value Constellations in the Financial Services. Edited by Daniel Fasnacht. Cham: Springer Management for Professionals. [Google Scholar] [CrossRef]

- Gandomi, Amir, and Murtaza Haider. 2015. Beyond the Hype: Big Data Concepts, Methods, and Analytics. International Journal of Information Management 35: 137–44. [Google Scholar] [CrossRef] [Green Version]

- Garzella, Stefano, Raffaele Fiorentino, Andrea Caputo, and Alessandra Lardo. 2021. Business Model Innovation in SMEs: The Role of Boundaries in the Digital Era. Technology Analysis & Strategic Management 33: 31–43. [Google Scholar] [CrossRef]

- Gatzweiler, Alexandra, Vera Blazevic, and Frank Thomas Piller. 2017. Dark Side or Bright Light: Destructive and Constructive Deviant Content in Consumer Ideation Contests. Journal of Product Innovation Management 34: 772–89. [Google Scholar] [CrossRef] [Green Version]

- George, Gerad, Ernst C. Osinga, Dovev Lavie, and Brent A. Scott. 2016. Big data and data science methods for management research. Academy of Management Journal 59: 1493–507. [Google Scholar] [CrossRef] [Green Version]

- Germann, Frank, Gary L. Lilien, Lars Fiedler, and Matthias Kraus. 2014. Do Retailers Benefit from Deploying Customer Analytics? Journal of Retailing 90: 587–93. [Google Scholar] [CrossRef]

- Gianiodis, Peter T., John E. Ettlie, and Jose J. Urbina. 2014. Open Service Innovation in the Global Banking Industry: Inside-Out Versus Outside-In Strategies. Academy of Management Perspectives 28: 76–91. [Google Scholar] [CrossRef]

- Greco, Marco, Michele Grimaldi, and Livio Cricelli. 2019. Benefits and Costs of Open Innovation: The BeCO Framework. Technology Analysis & Strategic Management 31: 53–66. [Google Scholar] [CrossRef]

- Greco, Marco, Michele Grimaldi, Giorgio Locatelli, and Mattia Serafini. 2021. How Does Open Innovation Enhance Productivity? An Exploration in the Construction Ecosystem. Technological Forecasting and Social Change 168: 120740. [Google Scholar] [CrossRef]

- Hair, Joe, Carole L. Hollingsworth, Adriane B. Randolph, and Alain Yee Loong Chong. 2017. An Updated and Expanded Assessment of PLS-SEM in Information Systems Research. Industrial Management & Data Systems 117: 442–58. [Google Scholar] [CrossRef]

- Hale, Galina, and Jose Angel Lopez. 2019. Monitoring Banking System Connectedness with Big Data. Journal of Econometrics 212: 203–20. [Google Scholar] [CrossRef]

- Hartmann, Philipp Max, Mohamed Zaki, Niels Feldmann, and Andy Neely. 2016. Capturing Value from Big Data—A Taxonomy of Data-Driven Business Models Used by Start-up Firms. International Journal of Operations & Production Management 36: 1382–406. [Google Scholar] [CrossRef]

- Hasan, Md. Morshadul, József Popp, and Judit Oláh. 2020. Current Landscape and Influence of Big Data on Finance. Journal of Big Data 7: 21. [Google Scholar] [CrossRef]

- Henseler, Jörg, Theo K. Dijkstra, Marko Sarstedt, Christian M. Ringle, Adamantios Diamantopoulos, Detmar W. Straub, David J. Ketchen, Joseph F. Hair, G. Tomas M. Hult, and Roger J. Calantone. 2014. Common Beliefs and Reality About PLS: Comments on Rönkkö and Evermann (2013). Organizational Research Methods 17: 182–209. [Google Scholar] [CrossRef] [Green Version]

- Hitt, Michael A., Kai Xu, and Christina Matz Carnes. 2016. Resource Based Theory in Operations Management Research. Journal of Operations Management 41: 77–94. [Google Scholar] [CrossRef]

- James, Ewen. 2019. How Big Data Is Changing the Finance Industry. Available online: https://www.tamoco.com/blog/big-data-financeindustry-analytics/ (accessed on 13 February 2022).

- Kim, Namkuk, Dong-Jae Kim, and Sungjoo Lee. 2015. Antecedents of Open Innovation at the Project Level: Empirical Analysis of Korean Firms. R&D Management 45: 411–39. [Google Scholar] [CrossRef]

- Kiron, David, Renee Boucher Ferguson, and Pamela Kirk Prentice. 2013. From value to vision: Reimagining the possible with data analytics. MIT Sloan Management Review 54: 1. [Google Scholar]

- Kline, Rex B. 2016. Principles and Practice of Structural Equation Modeling, 4th ed. New York: Guilford Press. [Google Scholar]

- Kock, Ned. 2015. Common method bias in PLS-SEM: A full collinearity assessment approach. International Journal of e-Collaboration 11: 1–10. [Google Scholar] [CrossRef] [Green Version]

- Koty, Alexander Chipman. 2021. Digital Banking in Malaysia: New Opportunities for Fintech. Available online: https://www.aseanbriefing.com/news/digital-banking-in-malaysia-new-opportunities-for-fintech/ (accessed on 10 April 2022).

- Lakemond, Nicolette, Lars Bengtsson, Keld Laursen, and Fredrik Tell. 2016. Match and Manage: The Use of Knowledge Matching and Project Management to Integrate Knowledge in Collaborative Inbound Open Innovation. Industrial and Corporate Change 25: 333–52. [Google Scholar] [CrossRef]

- Lanzolla, Gianvito, and Alessandro Giudici. 2017. Pioneering Strategies in the Digital World. Insights from the Axel Springer Case. Business History 59: 744–77. [Google Scholar] [CrossRef]

- Lassen, Astrid Heidemann, and Bjørge Timenes Laugen. 2017. Open Innovation: On the Influence of Internal and External Collaboration on Degree of Newness. Business Process Management Journal 23: 1129–43. [Google Scholar] [CrossRef]

- Laursen, Keld, and Ammon Salter. 2006. Open for Innovation: The Role of Openness in Explaining Innovation Performance among U.K. Manufacturing Firms. Strategic Management Journal 27: 131–50. [Google Scholar] [CrossRef]

- Leckel, Anja, Sophie Veilleux, and Leo Paul Dana. 2020. Local Open Innovation: A Means for Public Policy to Increase Collaboration for Innovation in SMEs. Technological Forecasting and Social Change 153: 119891. [Google Scholar] [CrossRef]

- León, G., A. Tejero, and José N. Franco-Riquelme. 2020. New Methodology for Profiling and Comparison of Open Innovation Models to Conduct R&D Activities. IEEE Access 8: 48491–502. [Google Scholar] [CrossRef]

- Levine, Sheen S., Mark Bernard, and Rosemarie Nagel. 2017. Strategic Intelligence: The Cognitive Capability to Anticipate Competitor Behavior. Strategic Management Journal 38: 2390–423. [Google Scholar] [CrossRef] [Green Version]

- Lu, Qinli, and Henry Chesbrough. 2022. Measuring Open Innovation Practices through Topic Modelling: Revisiting Their Impact on Firm Financial Performance. Technovation 114: 102434. [Google Scholar] [CrossRef]

- Luo, Yun, Sailesh Tanna, and Glauco De Vita. 2016. Financial Openness, Risk and Bank Efficiency: Cross-Country Evidence. Journal of Financial Stability 24: 132–48. [Google Scholar] [CrossRef] [Green Version]

- Ma, Yong, and Chi Yao. 2022. Openness, Financial Structure, and Bank Risk: International Evidence. International Review of Financial Analysis 81: 102065. [Google Scholar] [CrossRef]

- Mahmoud, Mahmoud Abdulai, Robert E. Hinson, and Patrick Amfo Anim. 2018. Service Innovation and Customer Satisfaction: The Role of Customer Value Creation. European Journal of Innovation Management 21: 402–22. [Google Scholar] [CrossRef]

- Manyika, James, Michael Chui, Brad Brown, Jacques Bughin, Richard Dobbs, Charles Roxburgh, and Angela Hung Byers. 2011. Big Data: The Next Frontier for Innovation, Competition, and Productivity. San Francisco: McKinsey Global Institute. [Google Scholar]

- Marina, Solesvik, and Magnus Gulbrandsen. 2013. Partner Selection for Open Innovation. Technology Innovation Management Review 8: 11–16. [Google Scholar] [CrossRef]

- Martovoy, Andrey, Anne-Laure Mention, and Marko Torkkeli. 2015. Inbound Open Innovation in Financial Services. Journal of Technology Management and Innovation 10: 117–31. [Google Scholar] [CrossRef]

- Mazzei, Matthew J., and David Noble. 2017. Big Data Dreams: A Framework for Corporate Strategy. Business Horizons 60: 405–14. [Google Scholar] [CrossRef]

- McAfee, Andrew, Erik Brynjolfsson, Thomas Davenport, D. J. Patil, and Barton Dominic. 2012. Big Data: The management revolution. Harvard Business Review 90: 61–68. [Google Scholar]

- Mikalef, Patrick, Maria Boura, George Lekakos, and John Krogstie. 2019. Big Data Analytics Capabilities and Innovation: The Mediating Role of Dynamic Capabilities and Moderating Effect of the Environment. British Journal of Management 30: 272–98. [Google Scholar] [CrossRef]

- Mishra, Deepa, Zongwei Luo, Shan Jiang, Thanos Papadopoulos, and Rameshwar Dubey. 2017. A Bibliographic Study on Big Data: Concepts, Trends and Challenges. Business Process Management Journal 23: 555–73. [Google Scholar] [CrossRef]

- Mora Cortez, Roberto, and Wesley J. Johnston. 2017. The Future of B2B Marketing Theory: A Historical and Prospective Analysis. Industrial Marketing Management 66: 90–102. [Google Scholar] [CrossRef]

- Moshtari, Mohammad. 2016. Inter-Organizational Fit, Relationship Management Capability, and Collaborative Performance within a Humanitarian Setting. Production and Operations Management 25: 1542–57. [Google Scholar] [CrossRef]

- Naqshbandi, M. Muzamil, and Sajjad M. Jasimuddin. 2022. The Linkage between Open Innovation, Absorptive Capacity and Managerial Ties: A Cross-Country Perspective. Journal of Innovation & Knowledge 7: 100167. [Google Scholar] [CrossRef]

- Naseer, Saima, Kausar Fiaz Khawaja, Shadab Qazi, Fauzia Syed, and Fatima Shamim. 2021. How and When Information Proactiveness Leads to Operational Firm Performance in the Banking Sector of Pakistan? The Roles of Open Innovation, Creative Cognitive Style, and Climate for Innovation. International Journal of Information Management 56: 102260. [Google Scholar] [CrossRef]

- Nestle, Volker, Florian A. Täube, Sven Heidenreich, and Marcel Bogers. 2019. Establishing Open Innovation Culture in Cluster Initiatives: The Role of Trust and Information Asymmetry. Technological Forecasting and Social Change 146: 563–72. [Google Scholar] [CrossRef]

- Obradović, Tena, Božidar Vlačić, and Marina Dabić. 2021. Open Innovation in the Manufacturing Industry: A Review and Research Agenda. Technovation 102: 102221. [Google Scholar] [CrossRef]

- OECD, Organisation for Economic Co-operation and Development. 2014. Data-Driven Innovation for Growth and Well-Being. Available online: https://www.oecd.org/sti/data-driven-innovation-9789264229358-en.htm (accessed on 14 February 2022).

- Oztaysi, Basar, Sezi Cevik Onar, and Cengiz Kahraman. 2017. Selection among innovative project proposals using a hesitant fuzzy multiple criteria decision making method. Journal of Economics Finance and Accounting 4: 194–202. [Google Scholar] [CrossRef]

- Peng, David Xiaosong, and Fujun Lai. 2012. Using Partial Least Squares in Operations Management Research: A Practical Guideline and Summary of Past Research. Journal of Operations Management 30: 467–80. [Google Scholar] [CrossRef]

- Priem, Richard L., Sali Li, and Jon C. Carr. 2011. Insights and New Directions from Demand-Side Approaches to Technology Innovation, Entrepreneurship, and Strategic Management Research. Journal of Management 38: 346–74. [Google Scholar] [CrossRef]

- PricewaterhouseCoopers PWC. 2020. Digital Banking: Malaysian Banks at a Crossroads. Available online: https://www.pwc.com/my/en/publications/2020/malaysian-banks-at-a-cross-roads.html (accessed on 13 April 2022).

- Radziwon, Agnieszka, and Marcel Bogers. 2019. Open Innovation in SMEs: Exploring Inter-Organizational Relationships in an Ecosystem. Technological Forecasting and Social Change 146: 573–87. [Google Scholar] [CrossRef]

- Rochet, Jean-Charles, and Jean Tirole. 2006. Two-Sided Markets: A Progress Report. The RAND Journal of Economics 37: 645–67. [Google Scholar] [CrossRef] [Green Version]

- Saura, Jose Ramon. 2021. Using Data Sciences in Digital Marketing: Framework, Methods, and Performance Metrics. Journal of Innovation & Knowledge 6: 92–102. [Google Scholar] [CrossRef]

- Schmidthuber, Lisa, Frank Piller, Marcel Bogers, and Dennis Hilgers. 2019. Citizen Participation in Public Administration: Investigating Open Government for Social Innovation. R&D Management 49: 343–55. [Google Scholar] [CrossRef]

- Seddon, Jonathan J. J. M., and Wendy L. Currie. 2017. A Model for Unpacking Big Data Analytics in High-Frequency Trading. Journal of Business Research 70: 300–307. [Google Scholar] [CrossRef]

- Sengupta, Abhijit, and Vania Sena. 2020. Impact of Open Innovation on Industries and Firms—A Dynamic Complex Systems View. Technological Forecasting and Social Change 159: 120199. [Google Scholar] [CrossRef]

- Shaikh, Ibrahim, and Krithika Randhawa. 2022. Managing the Risks and Motivations of Technology Managers in Open Innovation: Bringing Stakeholder-Centric Corporate Governance into Focus. Technovation 114: 102437. [Google Scholar] [CrossRef]

- Shen, Dehua, and Shu-heng Chen. 2018. Big Data Finance and Financial Markets. In Big Data in Computational Social Science and Humanities. Computational Social Sciences. Cham: Springer, pp. 235–48. [Google Scholar] [CrossRef]

- Shipilov, Andrew, Frédéric C. Godart, and Julien Clement. 2017. Which Boundaries? How Mobility Networks across Countries and Status Groups Affect the Creative Performance of Organizations. Strategic Management Journal 38: 1232–52. [Google Scholar] [CrossRef]

- Sirmon, David G., Michael A. Hitt, and R. Duane Ireland. 2007. Managing Firm Resources in Dynamic Environments to Create Value: Looking Inside the Black Box. Academy of Management Review 32: 273–92. [Google Scholar] [CrossRef] [Green Version]

- Sofka, Wolfgang, and Christoph Grimpe. 2010. Specialized Search and Innovation Performance–Evidence across Europe. R&D Management 40: 310–23. [Google Scholar] [CrossRef] [Green Version]

- Sun, Yongbo, Jingyan Liu, and Yixin Ding. 2020. Analysis of the Relationship between Open Innovation, Knowledge Management Capability and Dual Innovation. Technology Analysis & Strategic Management 32: 15–28. [Google Scholar] [CrossRef]

- Tasya, Aspiranti, Qaisar Ali, Shazia Parveen, Ima Amaliah, Muna Abdul Jalil, and Farah Merican Isahak Merican. 2023. Bibliometric Review of Corporate Governance of Islamic Financial Institutions Through AI-Based Tools. International Journal of Professional Business Review 8: 1710. [Google Scholar] [CrossRef]

- Teece, David J., Gary Pisano, and Amy Shuen. 1997. Dynamic capabilities and strategic management. Strategic Management Journal 18: 509–33. [Google Scholar] [CrossRef]

- Teplov, Roman, Ekaterina Albats, and Daria Podmetina. 2018. What does open innovation mean? Business versus academic perceptions. International Journal of Innovation Management 23: 1950002. [Google Scholar] [CrossRef] [Green Version]

- Tian, Xuemei. 2017. Big Data and Knowledge Management: A Case of Déjà vu or Back to the Future? Journal of Knowledge Management 21: 113–31. [Google Scholar] [CrossRef]

- Usman, Muhammad, Nadine Roijakkers, Wim Vanhaverbeke, and Federico Frattini. 2018. A Systematic Review of the Literature on Open Innovation in SMEs. In Researching Open Innovation in SMEs. Singapore: World Scientific, pp. 3–35. [Google Scholar] [CrossRef]

- Vanhaverbeke, Wim, Nadine Roijakkers, Annika Lorenz, and Henry Chesbrough. 2017. The Importance of Connecting Open Innovation to Strategy. In Strategy and Communication for Innovation. Edited by N. Pfeffermann and J. Gould. Cham: Springer. [Google Scholar] [CrossRef]

- Veugelers, Reinhilde, and Bruno Cassiman. 1999. Make and Buy in Innovation Strategies: Evidence from Belgian Manufacturing Firms. Research Policy 28: 63–80. [Google Scholar] [CrossRef]

- Vlaar, Paul W. L., Frans A. J. Van Den Bosch, and Henk W. Volberda. 2007. Towards a Dialectic Perspective on Formalization in Interorganizational Relationships: How Alliance Managers Capitalize on the Duality Inherent in Contracts, Rules and Procedures. Organization Studies 28: 437–66. [Google Scholar] [CrossRef]

- Wamba, Samuel F., and Deepa Mishra. 2017. Big Data Integration with Business Processes: A Literature Review. Business Process Management Journal 23: 477–92. [Google Scholar] [CrossRef] [Green Version]

- Wamba, Samuel F., Shahriar Akter, Andrew Edwards, Geoffrey Chopin, and Denis Gnanzou. 2015. How ‘Big Data’ Can Make Big Impact: Findings from a Systematic Review and a Longitudinal Case Study. International Journal of Production Economics 165: 234–46. [Google Scholar] [CrossRef]

- Wamba, Samuel F., Angappa Gunasekaran, Shahriar Akter, Steven Ji-fan Ren, Rameshwar Dubey, and Stephen J. Childe. 2017. Big Data Analytics and Firm Performance: Effects of Dynamic Capabilities. Journal of Business Research 70: 356–65. [Google Scholar] [CrossRef] [Green Version]

- Watson, George F., Scott Weaven, Helen Perkins, Deepak Sardana, and Robert W. Palmatier. 2018. International Market Entry Strategies: Relational, Digital, and Hybrid Approaches. Journal of International Marketing 26: 30–60. [Google Scholar] [CrossRef] [Green Version]

- West, Joel, and Marcel Bogers. 2017. Open Innovation: Current Status and Research Opportunities. Innovation 19: 43–50. [Google Scholar] [CrossRef]

- Yang, Chaowei, Qunying Huang, Zhenlong Li, Kai Liu, and Fei Hu. 2017. Big Data and Cloud Computing: Innovation Opportunities and Challenges. International Journal of Digital Earth 10: 13–53. [Google Scholar] [CrossRef] [Green Version]

- Yildirim, Ercan, Ilker Murat AR, Marina Dabić, Birdogan Baki, and Iskender Peker. 2022. A Multi-Stage Decision Making Model for Determining a Suitable Innovation Structure Using an Open Innovation Approach. Journal of Business Research 147: 379–91. [Google Scholar] [CrossRef]

- Yoon, Byungun, and Bomi Song. 2014. A Systematic Approach of Partner Selection for Open Innovation. Industrial Management & Data Systems 114: 1068–93. [Google Scholar] [CrossRef]

- Zhu, Xiaoxuan, Zhenxin Xiao, Maggie Chuoyan Dong, and Jibao Gu. 2019. The Fit between Firms’ Open Innovation and Business Model for New Product Development Speed: A Contingent Perspective. Technovation 86–87: 75–85. [Google Scholar] [CrossRef]

- Zillner, Sonja, Tilman Becker, Ricard Munné, Kazim Hussain, Sebnem Rusitschka, Helen Lippell, Edward Curry, and Adegboyega Ojo. 2016. Big Data-Driven Innovation in Industrial Sectors. In New Horizons for a Data-Driven Economy. Edited by J. Cavanillas, E. Curry and W. Wahlster. Cham: Springer. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

| Event | Source | Explanation/Application |

|---|---|---|

| Introduction of BDA in research | (McAfee et al. 2012) | It was featured as a frontier of science, innovation, and the new-millennium industrial revolution. |

| Evolution of BDA as 3Vs | (Duan and Xiong 2015) | 3Vs (volume, velocity, and verity) described BDA as voluminous data originating from multiple sources at a high speed. |

| Extension of BDA as 5Vs | (Wamba et al. 2015) | 5Vs (volume, velocity, verity, veracity, and value) defined BDA as voluminous data originating from multiple sources from high-speed reliable networks, resulting in economic benefits. |

| Further extension of BDA as 7Vs | (Mishra et al. 2017; Seddon and Currie 2017; Wamba and Mishra 2017) | 7Vs added two additional dimensions (variability and visualization) to the previous 5Vs which essentialized the significance of the difference in data flow and experts to visualize BDA to extract actual value. |

| BDA creation through innovative financial services such as online peer-to-peer lending, crowdfunding, SME financing, assets, wealth, trading, and mobile payment managing platforms, cryptocurrencies, and remittance administration channels | (Hale and Lopez 2019) | These sources are used by financial analysts to make strategic investment decisions, analyze consumers’ spending patterns, and customize financial products and services. |

| BDA enhances understanding of financial markets | (Shen and Chen 2018) | This alternatively resulted in smart and careful investment decisions taken by the public. |

| Banks accessing trillions of data from various points | (James 2019) | Bankers use BDA to improve the quality and security of services. |

| Banks leveraging BDA to enhance their social and environmental performance | (Ali et al. 2021) | Bankers harness BDA to improve their environmental social and governance (ESG). |

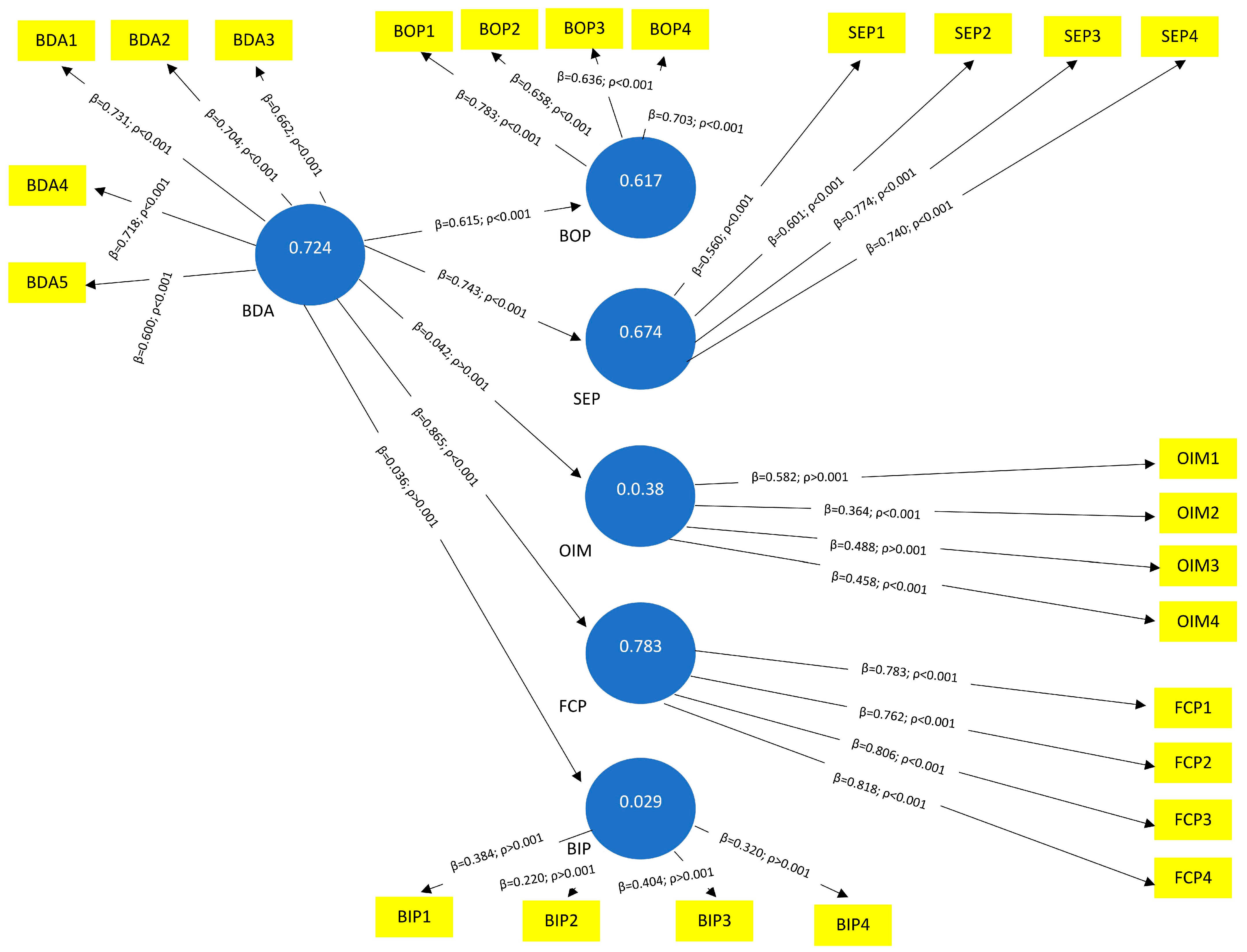

| Construct | Construct Label | Measures | Source |

|---|---|---|---|

| Banks openness | BOP | (BOP1) Our bank uses BDA to share information with collaborating partners of innovation projects. (BOP2) Our bank uses BDA to share financial portfolio data with external partners. (BOP3) Our bank uses BDA for sharing our products and services information with external partners. (BOP4) Our bank uses BDA to share corporate information with customers. | (Enkel et al. 2009; Yoon and Song 2014) |

| Selection of external partners | SEP | (SEP1) Our bank uses BDA for external partner screening to create open innovation strategies. (SEP2) Our bank uses BDA to match the selection of external partners with project needs. (SEP3) Our bank uses BDA to evaluate the performance of external partners. (SEP4) Our bank uses BDA to strengthen the mutual networks to ensure the success of open innovation projects. | (Yildirim et al. 2022) |

| Open innovation methods | OIM | (OIP1) Our bank uses BDA to identify the internal innovation practices relevant to the project. (OIP2) Our bank uses BDA to select and engage the key internal resources for an open innovation project. (OIP3) Our bank uses BDA to evaluate internal capabilities and identify project-specific capabilities. (OIP4) Our bank uses BDA to adjust internal capabilities and resources essential for an open innovation project. | (Brown et al. 2021) |

| Formalizing collaboration process | FCP | (FCP1) Our bank uses BDA to formalize the open innovation collaboration process. (FCP2) Our bank uses BDA to understand the legal requirements for collaboration. (FCP3) Our bank uses BDA to verify internal sources required to formalize the collaboration process. (FCP4) Our bank legal team uses BDA to ensure that formal collaboration requirements are fulfilled and are in line with the regulatory guidelines of the central bank. | (Bogers et al. 2018b) |

| Banks internal practices | BIP | (BIP1) Our bank uses BDA to identify the internal resources relevant for creating open innovation strategies. (BIP2) Our bank uses BDA to assess the existing knowledge and skill relevant to creating open innovation strategies. (BIP3) Our bank uses BDA to evaluate the governance practices relevant to creating open innovation strategies. (BIP4) Our bank uses BDA to assess and develop open innovation-related skills and competencies. | (Lu and Chesbrough 2022) |

| Big data analytics | BDA | (BDA1) Our bank continuously examines the open innovation opportunities through the strategic use of BDA. (BDA2) Our bank implements effective strategies to introduce and utilize BDA for open innovation. (BDA2) Our bank formally initiates the BDA planning process on how to implement it during open innovation projects. (BDA3) Our bank frequently adjusts open innovation strategies using BDA to better adapt to changing market conditions. (BDA5) Our bank has access to BDA sources essential to designing open innovation strategies. | (Akter et al. 2016) |

| Demographic Character | N | Percentage |

|---|---|---|

| Gender | ||

| Male | 186 | 43.76 |

| Female | 232 | 54.58 |

| Other | 7 | 1.64 |

| Age (years) | ||

| Below 30 | 12 | 2.82 |

| Between 30 and 35 | 56 | 13.17 |

| Between 36 and 40 | 123 | 28.94 |

| Between 41 and 45 | 163 | 38.35 |

| Between 46 and 50 | 43 | 10.11 |

| Above 50 | 28 | 6.58 |

| Education level | ||

| Diploma/certificate | 48 | 11.29 |

| Bachelor | 246 | 57.88 |

| Master | 126 | 29.64 |

| PHD | 5 | 1.17 |

| Job position | ||

| Marketing manager | 114 | 26.82 |

| Customer relationship manager | 109 | 25.64 |

| Business manager | 154 | 36.23 |

| Branch manager | 48 | 11.29 |

| Job experience (years) | ||

| Below 5 | 53 | 12.47 |

| Between 5 and 10 | 92 | 21.64 |

| Between 11 and 15 | 209 | 49.17 |

| Between 16 and 20 | 47 | 11.05 |

| Above 20 | 24 | 5.64 |

| Variables | Measurements | Factor Loadings | Variance | Error | SCR | AVE |

|---|---|---|---|---|---|---|

| BDA | BDA1 | 0.73 | 0.53 | 0.57 | 0.85 | 0.48 |

| BDA2 | 0.22 | 0.06 | 0.94 | |||

| BDA3 | 0.37 | 0.08 | 0.92 | |||

| BDA4 | 0.82 | 0.64 | 0.36 | |||

| BDA5 | 0.85 | 0.67 | 0.37 | |||

| BOP | BOP1 | 0.77 | 0.62 | 0.38 | 0.88 | 0.73 |

| BOP2 | 0.66 | 0.57 | 0.53 | |||

| BOP3 | 0.62 | 0.58 | 0.58 | |||

| BOP4 | 0.88 | 0.38 | 0.62 | |||

| SEP | SEP1 | 0.67 | 0.58 | 0.42 | 0.80 | 0.74 |

| SEP2 | 0.70 | 0.62 | 0.38 | |||

| SEP3 | 0.78 | 0.67 | 0.37 | |||

| SEP4 | 0.58 | 0.55 | 0.45 | |||

| OIM | OIM1 | 0.75 | 0.68 | 0.32 | 0.83 | 0.77 |

| OIM2 | 0.69 | 0.53 | 0.47 | |||

| OIM3 | 0.66 | 0.55 | 0.45 | |||

| OIM4 | 0.80 | 0.71 | 0.29 | |||

| FCP | FCP1 | 0.56 | 0.52 | 0.48 | 0.92 | 0.72 |

| FCP2 | 0.64 | 0.55 | 0.45 | |||

| FCP3 | 0.53 | 0.51 | 0.49 | |||

| FCP4 | 0.72 | 0.68 | 0.32 | |||

| BIP | BIP1 | 0.75 | 0.72 | 0.28 | 0.95 | 0.81 |

| BIP2 | 0.72 | 0.53 | 0.47 | |||

| BIP3 | 0.79 | 0.69 | 0.31 | |||

| BIP4 | 0.69 | 0.51 | 0.49 |

| Variables | Measurements | Factor Loadings | Variance | Error | SCR | AVE |

|---|---|---|---|---|---|---|

| BDA | BDA1 | 0.73 | 0.53 | 0.57 | 0.88 | 0.57 |

| BDA4 | 0.82 | 0.64 | 0.36 | |||

| BDA5 | 0.85 | 0.67 | 0.37 | |||

| BOP | BOP1 | 0.77 | 0.62 | 0.38 | 0.90 | 0.78 |

| BOP2 | 0.66 | 0.57 | 0.53 | |||

| BOP3 | 0.62 | 0.58 | 0.58 | |||

| BOP4 | 0.88 | 0.38 | 0.62 | |||

| SEP | SEP1 | 0.67 | 0.58 | 0.42 | 0.82 | 0.77 |

| SEP2 | 0.70 | 0.62 | 0.38 | |||

| SEP3 | 0.78 | 0.67 | 0.37 | |||

| SEP4 | 0.58 | 0.55 | 0.45 | |||

| OIM | OIM1 | 0.75 | 0.68 | 0.32 | 0.87 | 0.78 |

| OIM2 | 0.69 | 0.53 | 0.47 | |||

| OIM3 | 0.66 | 0.55 | 0.45 | |||

| OIM4 | 0.80 | 0.71 | 0.29 | |||

| FCP | FCP1 | 0.56 | 0.52 | 0.48 | 0.92 | 0.76 |

| FCP2 | 0.64 | 0.55 | 0.45 | |||

| FCP3 | 0.53 | 0.51 | 0.49 | |||

| FCP4 | 0.72 | 0.68 | 0.32 | |||

| BIP | BIP1 | 0.75 | 0.72 | 0.28 | 0.95 | 0.81 |

| BIP2 | 0.72 | 0.53 | 0.47 | |||

| BIP3 | 0.79 | 0.69 | 0.31 | |||

| BIP4 | 0.69 | 0.51 | 0.49 |

| Constructs | BDA | BOP | SEP | OIM | FCP | BIP |

|---|---|---|---|---|---|---|

| BDA | 0.76 | |||||

| BOP | 0.04 | 0.85 | ||||

| SEP | 0.27 | 0.37 | 0.83 | |||

| OIM | −0.07 | −0.02 | −0.09 | 0.84 | ||

| FCP | 0.22 | 0.31 | 0.19 | 0.36 | 0.79 | |

| BIP | −0.18 | −0.10 | −0.07 | −0.23 | −0.34 | 0.97 |

| Components | Initial Eigenvalues | Extraction Sums of Squared Loadings | ||||

|---|---|---|---|---|---|---|

| Total | Variance % | Cumulative % | Total | Variance % | Cumulative % | |

| 1 | 10.563 | 37.754 | 35.754 | 10.563 | 10.563 | 35.754 |

| 2 | 4.432 | 4.456 | 68.792 | |||

| 3 | 4.072 | 4.342 | 66.578 | |||

| 4 | 3.458 | 3.073 | 64.518 | |||

| 5 | 3.486 | 3.525 | 70.621 | |||

| 6 | 3.464 | 3.514 | 68.563 | |||

| 7 | 2.568 | 2.424 | 72.618 | |||

| 8 | 2.382 | 2.603 | 73.673 | |||

| 9 | 1.283 | 1.613 | 74.513 | |||

| 10 | 0.881 | 1.357 | 76.667 | |||

| 11 | 0.851 | 1.258 | 77.628 | |||

| 12 | 0.743 | 2.415 | 81.736 | |||

| 13 | 0.737 | 2.476 | 81.734 | |||

| 14 | 0.626 | 1.723 | 80.539 | |||

| 15 | 0.823 | 1.486 | 81.537 | |||

| 16 | 0.856 | 1.658 | 77.854 | |||

| 17 | 0.843 | 2.759 | 82.541 | |||

| 18 | 0.844 | 3.619 | 78.624 | |||

| 19 | 0.532 | 3.476 | 71.581 | |||

| 20 | 0.634 | 5.638 | 83.673 | |||

| 21 | 0.548 | 2.615 | 85.627 | |||

| 22 | 0.664 | 2.584 | 78.636 | |||

| 23 | 0.679 | 3.773 | 72.752 | |||

| 24 | 0.534 | 3.361 | 76.736 | |||

| 25 | 0.645 | 3.784 | 77.753 | |||

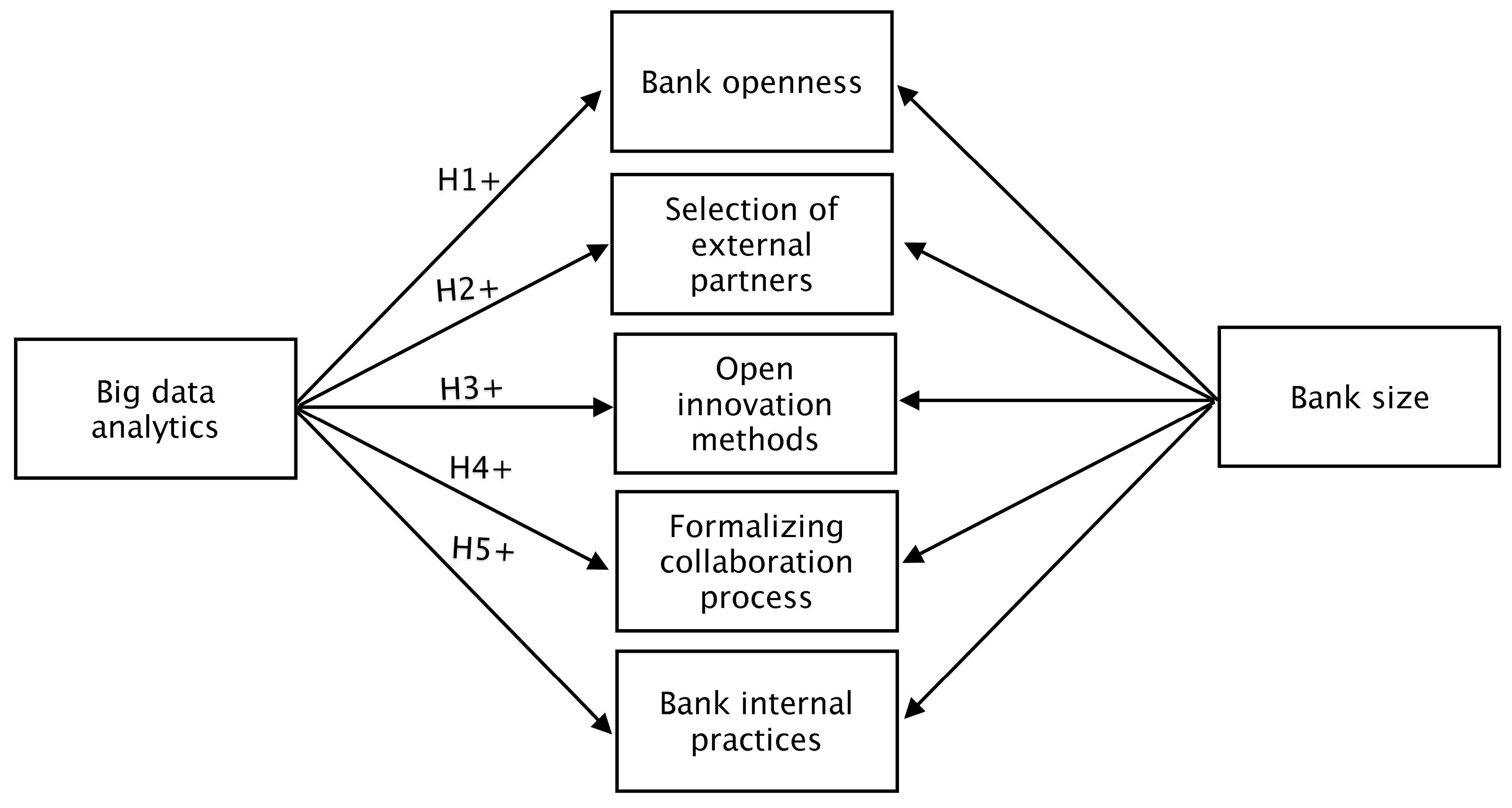

| Hypothesis | Impact of | On | β | ρ | Supported/Not Supported |

|---|---|---|---|---|---|

| H1 | BDA | BOP | 0.615 | <0.001 | Yes |

| H2 | BDA | SEP | 0.743 | <0.001 | Yes |

| H3 | BDA | OIM | 0.042 | >0.001 | No |

| H4 | BDA | FCP | 0.865 | <0.001 | Yes |

| H5 | BDA | BIP | 0.036 | >0.001 | No |

| Constructs | R2 | f2 | Q2 |

|---|---|---|---|

| BOP | 0.617 | 0.628 | 0.635 |

| SEP | 0.674 | 0.697 | 0.712 |

| IOM | 0.038 | 0.049 | 0.055 |

| FCP | 0.783 | 0.791 | 0.808 |

| BIP | 0.029 | 0.032 | 0.038 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Aspiranti, T.; Ali, Q.; Amaliah, I. Big Data Analytics to Support Open Innovation Strategies in Banks. Risks 2023, 11, 106. https://doi.org/10.3390/risks11060106

Aspiranti T, Ali Q, Amaliah I. Big Data Analytics to Support Open Innovation Strategies in Banks. Risks. 2023; 11(6):106. https://doi.org/10.3390/risks11060106

Chicago/Turabian StyleAspiranti, Tasya, Qaisar Ali, and Ima Amaliah. 2023. "Big Data Analytics to Support Open Innovation Strategies in Banks" Risks 11, no. 6: 106. https://doi.org/10.3390/risks11060106