1. Introduction

Understanding the relationships among cryptocurrencies is important for policymakers whose role is to maintain the stability of financial markets as well as for investors whose investment portfolios contain a portion of cryptocurrencies. Cryptocurrency is a non-centralized digital currency that is exchanged between peers without the need of a central government. Bitcoin [

1,

2], which was the first cryptocurrency, operates with block chain technology with a system of recording information in a way that makes it difficult or impossible to change, hack, or cheat the system. Because the prices of cryptocurrencies have been increased such as speculative investment purposes and/or a digital asset for real use, they have received growing attention from the media, academics, and the finance industry. Since the inception of Bitcoin in 2009, over several thousand alternative digital currencies have been developed, and there have been a number of studies on the analysis of the exchange rates of cryptocurrency [

3]. The degree of the return volatility has been regarded as a crucial characteristic of cryptocurrencies for investors including them in their portfolio. The prices of Bitcoin and Ethereum have been rapidly increased so that the last one-year price of Bitcoin was an almost 400 percent increase to USD 40,406 on 15 June 2021 from USD 9451 on 15 June 2020. Since [

4,

5], empirical investigations of Bitcoin showed that Bitcoin is more characteristic of an asset rather than a currency, and Bitcoin also possesses risk management and hedging capabilities [

6]. In order to predict the exchange rates of the Bitcoin electronic currency against the US Dollar, ref. [

7] proposed a non-causal autoregressive process with Cauchy errors. The volatility of Bitcoin using monthly return series is higher than that of gold or some foreign currencies in dollars [

8].

A number of academic studies have investigated the factors influencing the price and volatility of cryptocurrencies ([

9,

10,

11,

12]). Especially, GARCH family models are employed to estimate the time-varying volatility of cryptocurrencies. Ref. [

13] proposed the AR-CGARCH model to estimate the volatility of Bitcoin by comparing GARCH models. Ref. [

14] looked at the tail behavior of returns of the five major cryptocurrencies (Bitcoin, Ethereum, Ripple, Bitcoin Cash, and Litecoin), using extreme value analysis and estimating VaR and ES as tail risk measures. They found that Bitcoin Cash is the riskiest, while Bitcoin and Litecoin are the least risky cryptocurrencies. Ref. [

15] examined more than 1000 GARCH models and suggest the best fitted GARCH model chosen by back-testing VaR and ES as well as an MCS procedure. They claim that standard GARCH models may result in incorrect predictions and could be improved by allowing asymmetries and regime switching. Ref. [

16] employs the BEKK GARCH model to estimate time-varying conditional correlations between gold and Bitcoin.

For the volatility, previous studies have employed a variation of GARCH models, while little attention has been paid to methods outside the GARCH family. Refs. [

17,

18], examples of a few papers in this area, examine the volatility of cryptocurrencies by hiring the stochastic volatility model and finding out that the use of fast-moving autocorrelation function captures the volatility of cryptocurrencies better than smoothly decaying functions. This study sheds light on other statistical methods for better out-of-sample forecasting power, in particular, the SV model. Instead of using traditional approaches to interpret the association and/or causality among the cryptocurrencies, we use the approaches (SV method) described above because of several advantages. First, financial asset returns are generally fat-tailed and have negative skewness, and the residuals obtained from traditional time series analysis such as GARCH and/or VAR may be contaminated by other explainable portions of the volatility of the return series. Second, it is common that financial time series volatility is correlated in a non-Gaussian way. Lastly, because of the occurrence of extreme observations and the complex structure of the dependence among asset returns, traditional approaches often fail to incorporate the influences of asymmetries in individual distributions and in dependence. A copula function introduces a function linking univariate marginal to their multivariate distribution ([

19]).

This study contributes to the literature by highlighting the SV model, which shows superior forecasting accuracy compared with GARCH family models studied in prior studies. The SV considers two error processes, but the GARCH model considers a single error term so that the SV model makes a better in-sample fit. The adoption of cryptocurrencies as an alternative investment asset by institutional investors, such as hedge fund investors, has increased significantly in recent years. The cryptocurrency market, which has shown higher volatility than any other assets in the financial market, requires a significant level of risk management from institutional investors and individuals that incorporate them into their investment portfolios. The excellence of forecasting power in our SV model provides implications that it can be used as a better risk management tool than other GARCH family models. Moreover, the forecasting errors of the SV model, compared with the GARCH models, tend to be more accurate as forecast time horizons are longer. Another contribution of our paper to the literature is, rather, to pay attention to the forecasting power of volatility models using cryptocurrency data than measure volatility itself. Finally, by hiring principal component analysis (PCA), this study examines whether a smaller number of factors are able to explain the variation of a large set of cryptocurrencies. This approach may shed light on which group of cryptocurrencies mainly drives the variation of the daily log-return of cryptocurrencies used in the paper. As the crypto market has been gradually accepted into the mainstream of financial markets, the accurate prediction of cryptocurrency return volatility is in more demand by market participants, financial institutions, and government agencies. The approach used in this study sheds light on what models are examined for a more accurate estimate of cryptocurrency volatility.

This paper is organized as follows.

Section 2 gives an overview of the existing volatility models, that is, the GARCH and SV methods.

Section 3 presents the data analysis and the discussion and conclusion follow in

Section 4 and

Section 5, respectively.

3. Results

For volatility efficiency comparison, nine cryptocurrencies are applied to the models introduced in

Section 2. Considering the sensitivity of the time period in predicting the volatility of financial time-series return data such as cryptocurrencies, we examine two different time periods, short-term and long-term periods. The sample consists of the daily log-returns of the nine cryptocurrencies over period 1 (19 August 2018 to 27 November 2018) and period 2 (2 January 2018 to 27 November 2018). The log-returns of Bitcoin (BTC), XRP (XRP), Ethereum (ETH), Bitcoin Cash (BCH), Stellar (XLM), Litecoin (LTC), TRON (TRX), Cardano (ADA), and IOTA (IOTA) are denoted by LBTC, LXRP, LETH, LBCH, LXLM, LLTC, LTRX, LADA, and LMIOTA, respectively. We obtain our data from a financial website (

https://coinmarketcap.com/coins/) (accessed on 10 May 2020). Throughout the year of 2018, BTC’s price fluctuated from USD 17,527.00 (6 January 2018) to USD 3820.72 (27 November 2018). The cryptocurrency market had extremely high volatility during the period 2. However, during the second half of the year 2018 (period 1), BTC’s price did not fluctuate from USD 6308.53 (20 August 2018) to USD 3820.72 (27 November 2018) compared with period 2. We can say that the period 1 was low volatile time period and the period 2 was high volatile time period. It is good to perform the comparison of volatile forecasting with the GARCH models and SV model for two low and high volatile cryptocurrency data.

The data set consists of the daily historical prices and volumes of the nine cryptocurrencies.

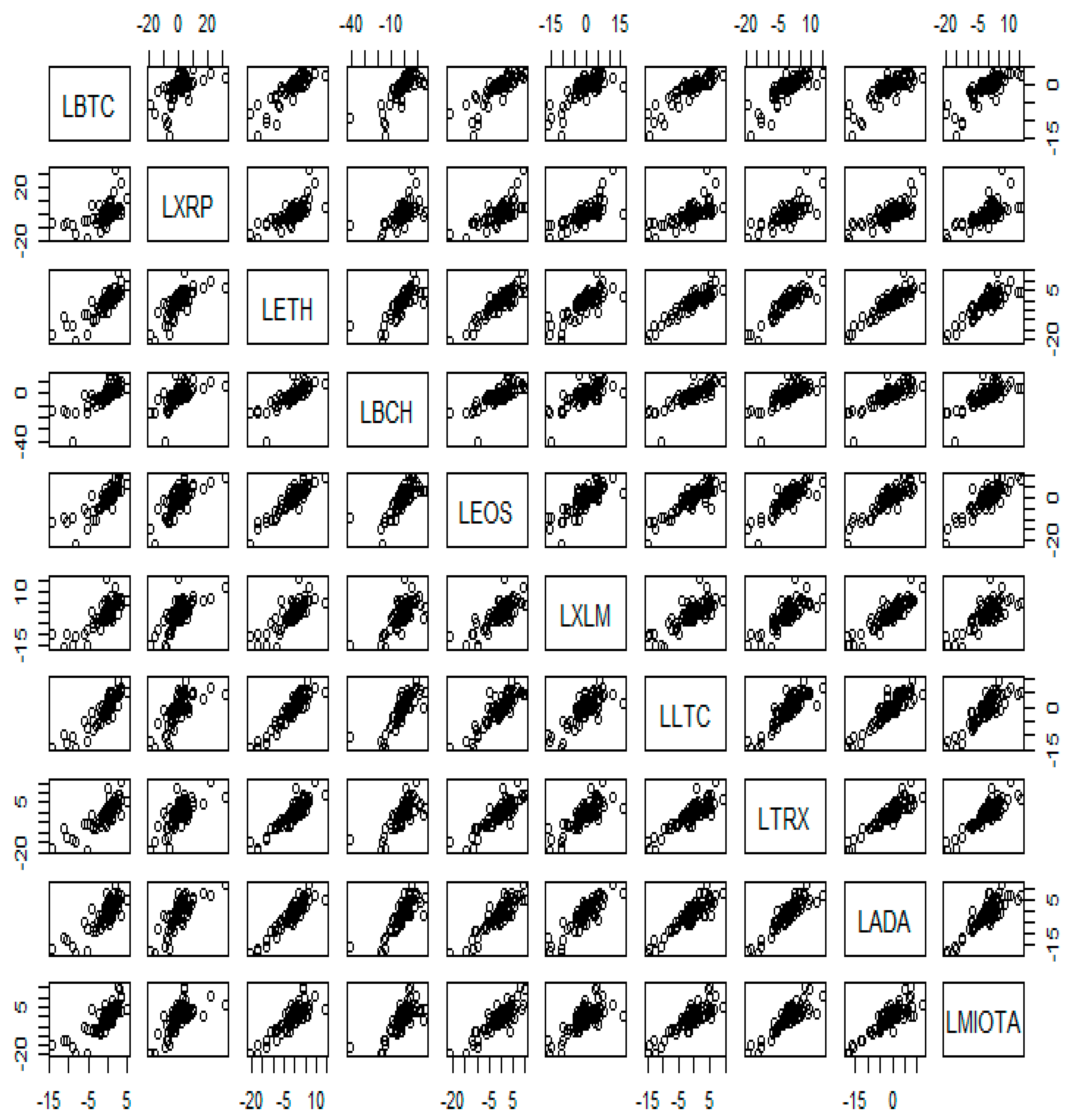

Figure 1 and

Figure 2 present the plot of the daily prices of the nine cryptocurrencies.

Figure 1 shows the scatterplots among the nine cryptocurrencies from August 2018 to November 2018 (period 1) and

Figure 2 from January 2018 to November 2018 (period 2). According to the figures, each pair of cryptocurrencies studied addresses similar results, positive and relatively high correlation regardless of period. For the nine time series data analyses in this section, daily log-returns in percentage are defined as

.

Table 1 shows the summary statistics of the log returns of the nine cryptocurrencies. In general, they share the fat-tail distribution, one of the common characteristics found in the return series of financial assets. Based on the kurtosis statistics, the fat-tailed distribution is observed in all nine cryptocurrencies, though the degree of the fat-tail is quite different among them. One of the interesting observations is the change in kurtosis values between periods 1 and 2. In period 1, the values of the kurtosis of major cryptocurrencies, BTC, XRP, ETH, and BCH (the top 4 based on market capitalization), are higher than the other relatively small market-cap cryptocurrencies (XLM, LTC, TRX, ADA, and MIOTA). This phenomenon is reversed in period 2 where the small-cap cryptocurrencies generally have higher kurtosis values than the large-cap ones. It suggests that over the period of 2018 (period 1), small-cap cryptocurrencies tend to have more extreme daily returns on both directions which can be identified by the magnitude of their minimum and maximum returns in each period. When we focus on the recent data of period 1, however, this trend is reversed. The large-cap cryptocurrencies show higher kurtosis. As for the skewness, all the cryptocurrencies except XRP show lower skewness in the more recent period (period 1) while XRP displays even higher positive skewness. This is an interesting observation because most financial asset returns show a negative skewness. Only XRP has tended to the positively-skewed return series from the negatively-skewed ones while other cryptocurrencies have enhanced the magnitude of skewness in a negative direction. This might be explained by the fact that the most recent bull market period in the crypto market, late 2017 to early 2018, is covered in the data period, and the positive returns during the period dominate the negative returns before and after the bull market in terms of the magnitude. XRP, however, is off this trend. It has been observed that in the more recent period (period 2), a bear market, XRP is the only one which tends to have more extreme positive returns. This implies that the co- movement of XRP with the cryptocurrency market is lower than any other cryptocurrencies and thus its systematic risk in the cryptocurrency market would be low. It might, therefore, attract more attention from potential investors looking to build a market-portfolio in the cryptocurrency market.

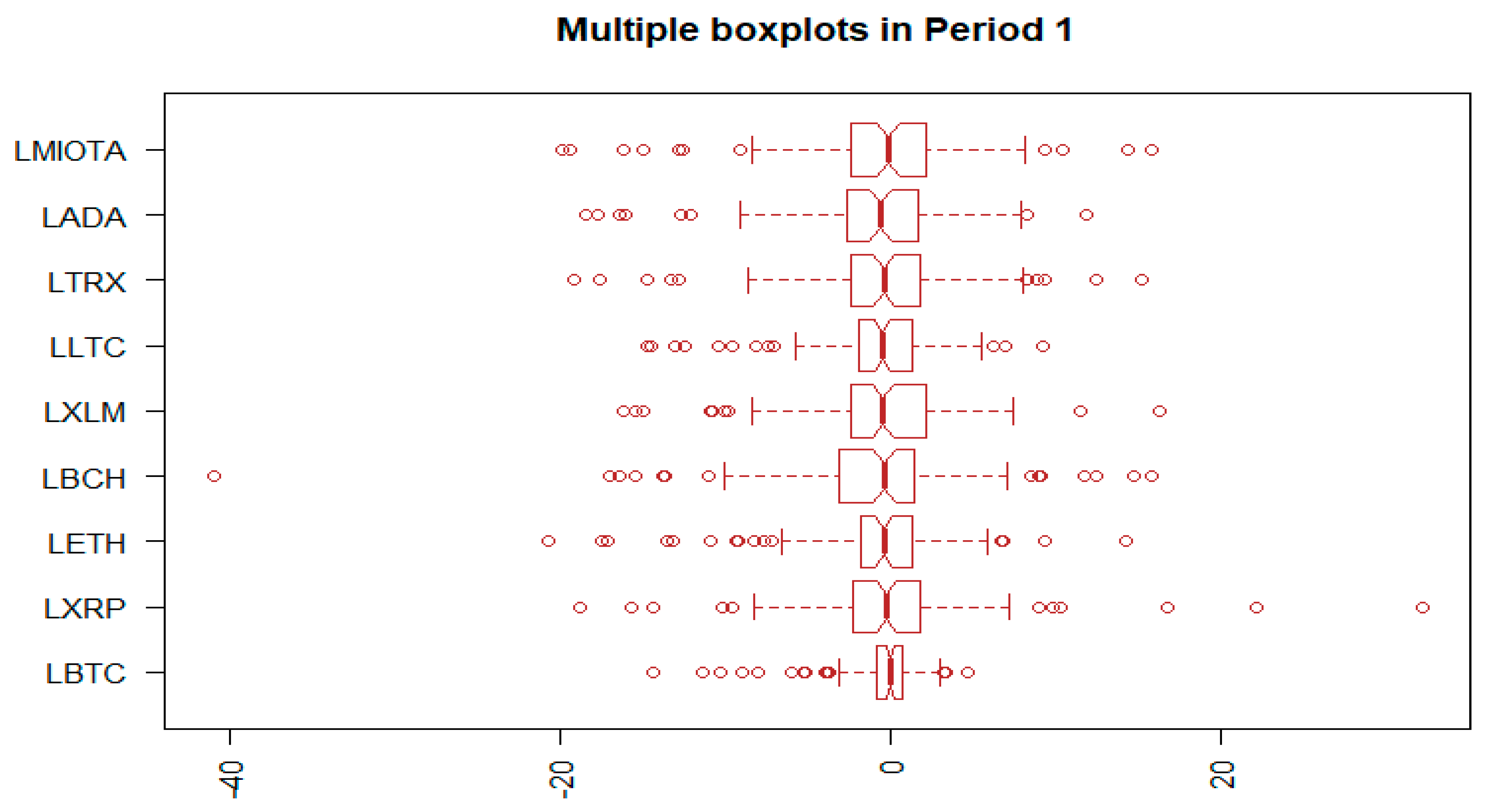

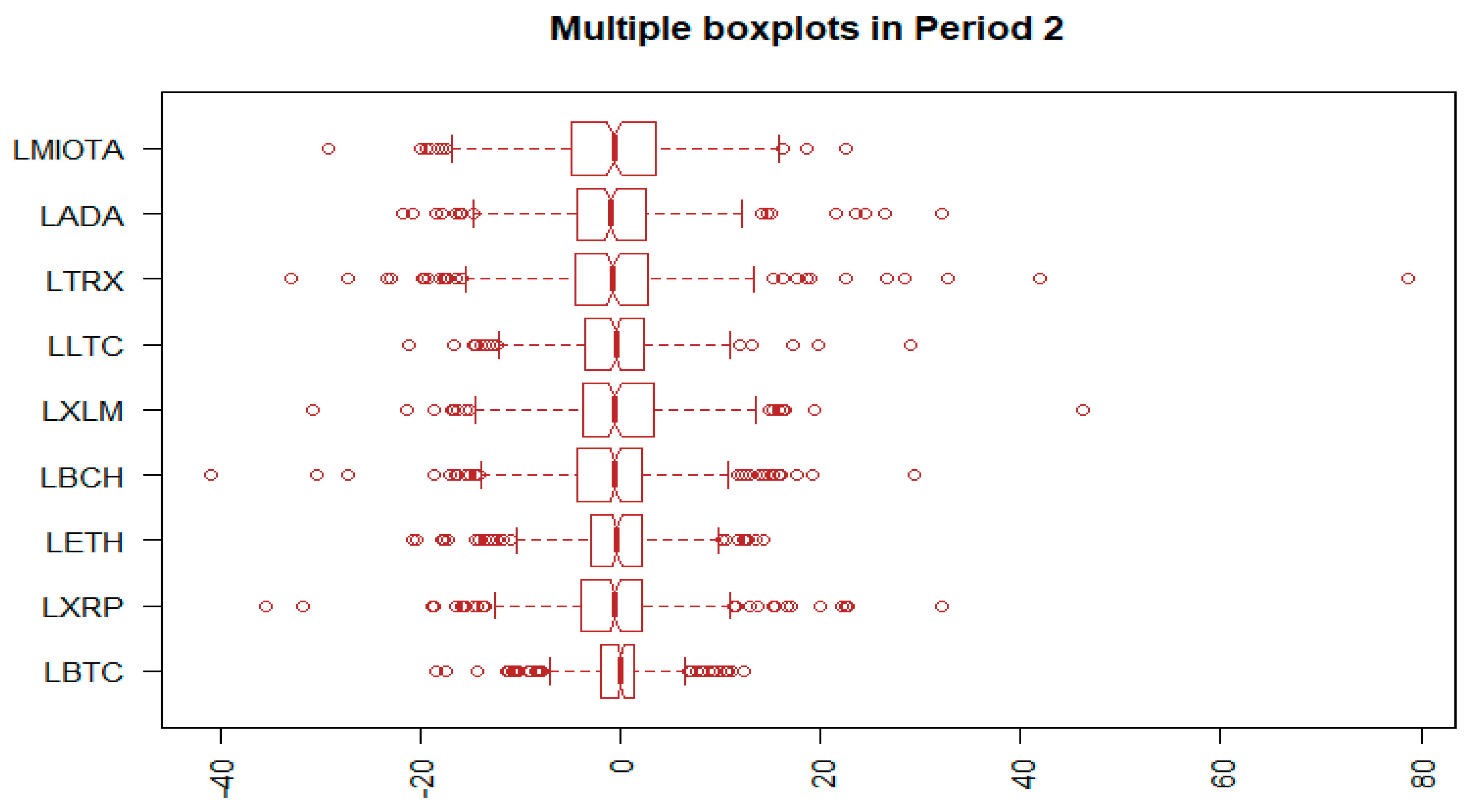

Figure 3 and

Figure 4 support the arguments by addressing boxplots of the cryptocurrencies in each period. All cryptocurrencies tend to have extreme log returns on both sides (high kurtosis) and in

Figure 3, XRP shows the positively-skewed distribution in the more recent period (period 1). Panels A and B in

Table 2 and

Table 3 show the correlations of the nine cryptocurrencies for each period. We report both Pearson’s and Kendall’s correlation coefficients. Based on the Pearson’s correlation matrix, the magnitude of correlation coefficients tends to be higher toward to the recent period (from period 1 to 2) except in several pairs, especially XRP-related pairs (BTC-XRP from 0.68 to 0.54), which show lower magnitudes.

When we look into the results of the Kendall’s coefficients; however, the trends addressed in the Pearson’s results [

33] show the opposite directions. Most correlation pairs in the Kendall’s coefficient table were lower from period 1 to 2 (the recent period). However, with regard to the seemingly contradictory direction between the two types of correlation coefficients we suggest that Kendall’s reflects the skewed and fat-tailed distribution feature of the return data of cryptocurrencies. Kendall’s correlation coefficients are the rank correlation, a non-parametric test that measures the strength of dependence between two variables, whereas Pearson’s are calculated based on the normality assumption. Principal component analysis (hereafter, PCA) is an effective multivariate statistical analysis technique for reducing the dimension of large data sets with minimal loss of information and extracting their structural features ([

2]). It transforms a number of correlated variables into a series of linearly uncorrelated variables called principal components by projecting the observation results onto axes to capture the maximum amount of variability in the original data. The first principal component explains the largest possible variability of the original data, and each succeeding component in turn explains the highest variability under the constraint that it is orthogonal to the preceding components. PCA is optimal from the perspective of minimizing the square distance between the observed values in the input space and the mapped values in the low-dimensional subspace ([

12]).

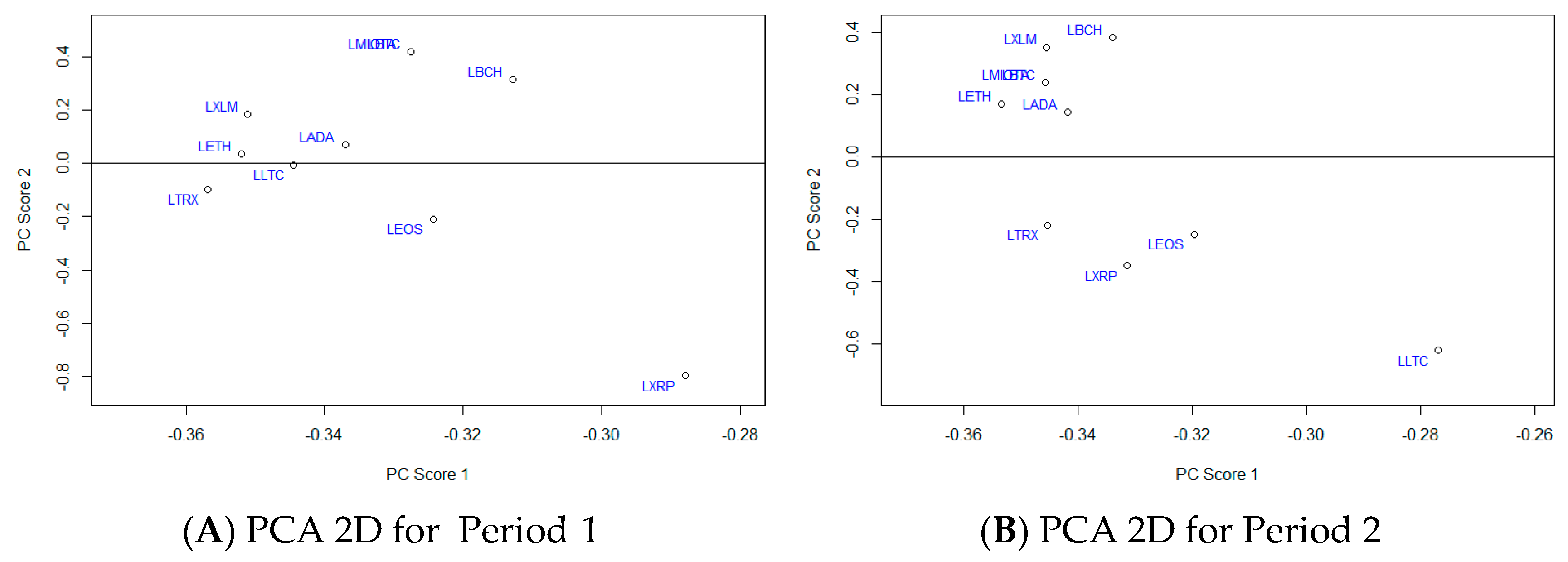

Table 4 shows the PCA [

34] results for periods 1 and 2. The proportion of variance explained by the first principal component in period 1 is 81% whereas it is 75% in period 2.

Figure 5 addresses the factor loadings of the first two main components in panels A and Band the three main components (panels C and D). ETH, TRX, and XLM are the variables with high magnitude (an absolute term) of factor loadings in the first component in both periods. Interestingly, the signs of the factor scores are positive across all factors in period 1. In the second component, BCH, XLM, and BTC, has factor loadings that are influential on both periods. In period 1, the XRP return series shows the largest factor loading in an absolute term, around −0.8, in the second component, whereas LTC does the same in period 2.

Table 5 shows the value of the AIC (Akaike’s information criterion) of different GARCH models (GARCH, TGARCH, and IGARCH) across nine cryptocurrencies in each period. We include TGARCH to handle the asymmetric distribution of errors which is commonly known for cryptocurrencies ([

30]). In period 1, the IGARCH model provides the lowest AIC except for XRP, BCH, and LTC where the TGARCH models have the lowest AIC. In period 2, however, IGARCH shows the lowest AIC over all of cryptocurrencies. Given the value of the AIC model selection criterion, this indicates that in general IGARCH is superior to other GARCH family models.

Table 6 shows the reliability of the IGARCH with ARMA (0,0) with LBTC for Period 1 and Period 2 even though

is statistically significant at the significance level (0.10) for Period 1.

Table 7,

Table 8 and

Table 9 demonstrate representative results regarding forecast accuracy for an h-step-ahead forecast. We report out-of-sample MSE losses in both the SV and GARCH models with the observed time series data, where the evaluation is based on two different volatility proxies for the conditional volatility. The forecast losses of the models are systematically lower over all horizons and across all cryptocurrencies. The results exhibit the superior forecasting accuracy of the SV method over the GARCH models, especially in volatility forecasting over longer time horizons. For example, 3 day out-of-sample MSEs (Mean Squared Errors) (using the variance as a conditional volatility) of the BTC over period 1 are 8.485 and 8.165 for IGARCH and SV, respectively, and those of period 2 are 8.038 and 7.407, respectively. When the forecasting time horizon is the longest (

h = 44), the MSE of the SV method is 5.761 in period 1, whereas that of the IGARCH is 9.198. Thus, the SV method has better forecasting accuracy than the IGARCH as the forecasting horizon is longer.

This trend is shown in all other cryptocurrencies, regardless of the conditional volatility types (MSE1 and MSE2). This difference of MSEs between TGARCH and SV is high in TRX, ADA, and MIOTA while ETH has almost no difference in period 1 (5.669 for the TGARCH and 6.625 for the SV method). In general, the SV method shows better forecasting accuracy than the GARCH models across all the cryptocurrencies, especially in volatility forecasting over longer time horizons. One plausible reason is that the SV model allows for two error processes and thus is more flexible for modeling financial time series, while the GARCH model considers a single error term. In addition to that, the SV model allow us to use the Bayesian approach to determine the inferences for the volatilities of time series using simulation algorithms such as the Markov Chain Monte Carlo (MCMC) methods whereas the GARCH family models have the difficulty of obtaining the maximum likelihood estimates caused by the complexity of the likelihood function. Therefore, the SV model offers a better in-sample fit ([

3]).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}