Public Debt, Governance, and Growth in Developing Countries: An Application of Quantile via Moments

Abstract

:1. Introduction

2. Literature Review

3. Methodology

3.1. Data

3.2. Empirical Model

3.3. Method

4. Result and Discussion

4.1. Descriptive Analysis

4.2. Main Results

5. Discussion

6. Conclusions and Policy Implications

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Bhat, K.U.; Chen, S.; Chen, Y.; Jebran, K. Debt capacity, debt choice, and underinvestment problem: Evidence from China. Econ. Res.-Ekon. Istraživanja 2020, 33, 267–287. [Google Scholar] [CrossRef]

- Gómez-Puig, M.; Sosvilla-Rivero, S.; Martínez-Zarzoso, I. On the heterogeneous link between public debt and economic growth. J. Int. Financ. Mark. Inst. Money 2022, 77, 101528. [Google Scholar] [CrossRef]

- Petrović, P.; Arsić, M.; Nojković, A. Increasing public investment can be an effective policy in bad times: Evidence from emerging EU economies. Econ. Model. 2021, 94, 580–597. [Google Scholar] [CrossRef]

- Baum, A.; Checherita-Westphal, C.; Rother, P. Debt and growth: New evidence for the euro area. J. Int. Money Financ. 2013, 32, 809–821. [Google Scholar] [CrossRef] [Green Version]

- Mohsin, M.; Ullah, H.; Iqbal, N.; Iqbal, W.; Taghizadeh-Hesary, F. How external debt led to economic growth in South Asia: A policy perspective analysis from quantile regression. Econ. Anal. Policy 2021, 72, 423–437. [Google Scholar] [CrossRef]

- Yasar, N. The Causal Relationship Between Foreign Debt and Economic Growth: Evidence from Commonwealth Independent States. Foreign Trade Rev. 2021, 56, 415–429. [Google Scholar] [CrossRef]

- Asteriou, D.; Pilbeam, K.; Pratiwi, C.E. Public debt and economic growth: Panel data evidence for Asian countries. J. Econ. Financ. 2021, 45, 270–287. [Google Scholar] [CrossRef]

- Shittu, W.O.; Hassan, S.; Nawaz, M.A. The nexus between external debt, corruption and economic growth: Evidence from five SSA countries. Afr. J. Econ. Manag. Stud. 2018, 9, 319–334. [Google Scholar] [CrossRef]

- Pjanić, M.; Milenković, N.; Andrašić, J.; Kalaš, B.; Mirović, V. Public debt's predictors in EU: Evidence from members and non-members of European Monetary Union. Econ. Res.-Ekon. Istraživanja 2020, 33, 3562–3579. [Google Scholar] [CrossRef]

- Law, S.H.; Ng, C.H.; Kutan, A.M.; Law, Z.K. Public debt and economic growth in developing countries: Non-linearity and threshold analysis. Econ. Model. 2021, 98, 26–40. [Google Scholar] [CrossRef]

- Wang, M.L.; Ntim, V.S.; Yang, J.; Zheng, Q.; Geng, L. Effect of institutional quality and foreign direct investment on economic growth and environmental quality: Evidence from African countries. Econ. Res.-Ekon. Istraživanja 2022, 35, 4065–4091. [Google Scholar] [CrossRef]

- Al Mamun, M.; Sohag, K.; Hassan, M.K. Governance, resources and growth. Econ. Model. 2017, 63, 238–261. [Google Scholar] [CrossRef]

- Fraj, S.H.; Hamdaoui, M.; Maktouf, S. Governance and economic growth: The role of the exchange rate regime. Int. Econ. 2018, 156, 326–364. [Google Scholar] [CrossRef]

- Knack, S.; Keefer, P. Institutions and economic performance: Cross-country tests using alternative institutional measures. Econ. Politics 1995, 7, 207–227. [Google Scholar] [CrossRef]

- Nguyen, C.V.; Giang, L.T.; Tran, A.N.; Do, H.T. Do good governance and public administration improve economic growth and poverty reduction? The case of Vietnam. Int. Public Manag. J. 2021, 24, 131–161. [Google Scholar] [CrossRef]

- Azam, M. Governance and economic growth: Evidence from 14 Latin America and Caribbean countries. J. Knowl. Econ. 2022, 13, 1470–1495. [Google Scholar] [CrossRef]

- Sarpong, S.Y.; Bein, M.A. Effects of good governance, sustainable development and aid on quality of life: Evidence from sub-saharan Africa. Afr. Dev. Rev. 2021, 33, 25–37. [Google Scholar] [CrossRef]

- Mauro, P. Corruption and growth. Q. J. Econ. 1995, 110, 681–712. [Google Scholar] [CrossRef]

- Cooray, A.; Dzhumashev, R.; Schneider, F. How does corruption affect public debt? An empirical analysis. World Dev. 2017, 90, 115–127. [Google Scholar] [CrossRef] [Green Version]

- Kaufmann, D.; Kraay, A.; Mastruzzi, M. The worldwide governance indicators: Methodology and analytical issues. Hague J. Rule Law 2011, 3, 220–246. [Google Scholar] [CrossRef]

- Nguyen, T.A.N.; Luong, T.T.H. Fiscal Policy, Institutional Quality, and Public Debt: Evidence from Transition Countries. Sustainability 2021, 13, 10706. [Google Scholar] [CrossRef]

- Butkus, M.; Seputiene, J. Growth effect of public debt: The role of government effectiveness and trade balance. Economies 2018, 6, 62. [Google Scholar] [CrossRef] [Green Version]

- Machado, J.A.; Silva, J.S. Quantiles via moments. J. Econom. 2019, 213, 145–173. [Google Scholar] [CrossRef]

- Tempelman, J.H.; James, M. Buchanan on public-debt finance. Indep. Rev. 2007, 11, 435–449. [Google Scholar]

- Aspromourgos, T. Keynes, public debt, and the complex of interest rates. J. Hist. Econ. Thought 2018, 40, 493–512. [Google Scholar] [CrossRef] [Green Version]

- Castelnuovo, E.; Lim, G.; Pellegrino, G. Macroeconomic Policies in a Low Interest Rate Environment: Back to Keynes? Aust. Econ. Rev. 2018, 51, 70–86. [Google Scholar] [CrossRef]

- Tsoulfidis, L. Classical economists and public debt. Int. Rev. Econ. 2007, 54, 1–12. [Google Scholar] [CrossRef]

- Barreyre, N.; Delalande, N. A World of Public Debts. A Political History; Springer: Berlin/Heidelberg, Germany; Cham, Switzerland, 2020. [Google Scholar]

- Greenwald, B.C.; Stiglitz, J.E. Keynesian, new Keynesian, and new classical economics. Oxf. Econ. Pap. 1987, 39, 119–133. [Google Scholar] [CrossRef] [Green Version]

- Shahor, T. The impact of public debt on economic growth in the Israeli economy. Isr. Aff. 2018, 24, 254–264. [Google Scholar] [CrossRef]

- Ndoricimpa, A. Threshold effects of public debt on economic growth in Africa: A new evidence. J. Econ. Dev. 2020, 22, 187–207. [Google Scholar] [CrossRef]

- Sharaf, M.F. The asymmetric and threshold impact of external debt on economic growth: New evidence from Egypt. J. Bus. Socio-Econ. Dev. 2021, 2, 1–18. [Google Scholar] [CrossRef]

- Yusuf, A.; Mohd, S. The impact of government debt on economic growth in Nigeria. Cogent Econ. Financ. 2021, 9, 1946249. [Google Scholar] [CrossRef]

- Saungweme, T.; Odhiambo, N.M. Government debt, government debt service and economic growth nexus in Zambia: A multivariate analysis. Cogent Econ. Financ. 2019, 7, 1622998. [Google Scholar] [CrossRef]

- Eberhardt, M.; Presbitero, A.F. Public debt and growth: Heterogeneity and non-linearity. J. Int. Econ. 2015, 97, 45–58. [Google Scholar] [CrossRef]

- Hilton, S.K. Public debt and economic growth: Contemporary evidence from a developing economy. Asian J. Econ. Bank. 2021, 5, 173–193. [Google Scholar] [CrossRef]

- Abbas, Q.; Junqing, L.; Ramzan, M.; Fatima, S. Role of governance in debt-growth relationship: Evidence from panel data estimations. Sustainability 2021, 13, 5954. [Google Scholar] [CrossRef]

- Hammudeh, S.; Sohag, K.; Husain, S.; Husain, H.; Said, J. Non-linear relationship between economic growth and nuances of globalisation with income stratification: Roles of financial development and governance. Econ. Syst. 2020, 44, 100761. [Google Scholar] [CrossRef]

- Dey, S.R.; Tareque, M. External debt and growth: Role of stable macroeconomic policies. J. Econ. Financ. Adm. Sci. 2020, 25, 185–204. [Google Scholar] [CrossRef]

- Kharusi, S.A.; Ada, M.S. External debt and economic growth: The case of emerging economy. J. Econ. Integr. 2018, 33, 1141–1157. [Google Scholar] [CrossRef]

- Eggertsson, G.B.; Krugman, P. Debt, deleveraging, and the liquidity trap: A Fisher-Minsky-Koo approach. Q. J. Econ. 2012, 127, 1469–1513. [Google Scholar] [CrossRef] [Green Version]

- Égert, B. The 90% public debt threshold: The rise and fall of a stylised fact. Appl. Econ. 2015, 47, 3756–3770. [Google Scholar] [CrossRef]

- Kranke, M. Tomorrow's Debt, Today's Duty: Debt Sustainability as Anticipatory Global Governance. Glob. Soc. 2022, 36, 223–239. [Google Scholar] [CrossRef]

- Briceño, H.R.; Perote, J. Determinants of the public debt in the Eurozone and its sustainability amid the Covid-19 pandemic. Sustainability 2020, 12, 6456. [Google Scholar] [CrossRef]

- Appiah Kubi, S.N.K.; Malec, K.; Phiri, J.; Krivko, M.; Maitah, K.; Maitah, M.; Smutka, L. Key Drivers of Public Debt Levels: Empirical Evidence from Africa. Sustainability 2022, 14, 1220. [Google Scholar] [CrossRef]

- Dorobantu, S.; Müllner, J. Debt-side governance and the geography of project finance syndicates. J. Corp. Financ. 2019, 57, 161–179. [Google Scholar] [CrossRef]

- Canay, I.A. A simple approach to quantile regression for panel data. Econom. J. 2011, 14, 368–386. [Google Scholar] [CrossRef]

- Koenker, R. Quantile regression for longitudinal data. J. Multivar. Anal. 2004, 91, 74–89. [Google Scholar] [CrossRef] [Green Version]

- Awan, A.; Abbasi, K.R.; Rej, S.; Bandyopadhyay, A.; Lv, K. The impact of renewable energy, internet use and foreign direct investment on carbon dioxide emissions: A method of moments quantile analysis. Renew. Energy 2022, 189, 454–466. [Google Scholar] [CrossRef]

- Buchinsky, M. Changes in the US wage structure 1963–1987: Application of quantile regression. Econom. J. Econom. Soc. 1994, 62, 405–458. [Google Scholar]

- Chamberlain, G. Quantile regression, censoring, and the structure of wages. In Advances in Econometrics: Sixth World Congress; Cambridge University Press: Cambridge, UK, 1994; Volume 2, pp. 171–209. [Google Scholar]

- Koenker, R.; Hallock, K.F. Quantile regression. J. Econ. Perspect. 2001, 15, 143–156. [Google Scholar] [CrossRef]

- Cade, B.S.; Noon, B.R. A gentle introduction to quantile regression for ecologists. Front. Ecol. Environ. 2003, 1, 412–420. [Google Scholar] [CrossRef]

- Bassett, G.W.; Koenker, R. A quantile regression memoir. In Handbook of Quantile Regression; Chapman and Hall/CRC: Boca Raton, FL, USA, 2017; pp. 3–5. [Google Scholar]

- He, J. A new approach to non-linear partial differential equations. Commun. Nonlinear Sci. Numer. Simul. 1997, 2, 230–235. [Google Scholar] [CrossRef]

- Chernozhukov, V.; Rigobon, R.; Stoker, T.M. Set identification and sensitivity analysis with Tobin regressors. Quant. Econ. 2010, 1, 255–277. [Google Scholar] [CrossRef] [Green Version]

- Nuru, N.Y.; Gereziher, H.Y. The effect of fiscal policy on economic growth in South Africa: A non-linear ARDL model analysis. J. Econ. Adm. Sci. 2021, 38, 229–245. [Google Scholar] [CrossRef]

- Temsumrit, N. Democracy, institutional quality and fiscal policy cycle: Evidence from developing countries. Appl. Econ. 2022, 54, 75–98. [Google Scholar] [CrossRef]

- Darku, A.B.; Yeboah, R. Economic openness and income growth in developing countries: A regional comparative analysis. Appl. Econ. 2018, 50, 855–869. [Google Scholar] [CrossRef]

- Topcu, E.; Altinoz, B.; Aslan, A. Global evidence from the link between economic growth, natural resources, energy consumption, and gross capital formation. Resour. Policy 2020, 66, 101622. [Google Scholar] [CrossRef]

- Awuzie, B.; Monyane, T.G. Conceptualising sustainability governance implementation for infrastructure delivery systems in developing countries: Success factors. Sustainability 2020, 12, 961. [Google Scholar] [CrossRef] [Green Version]

- Erum, N.; Hussain, S. Corruption, natural resources and economic growth: Evidence from OIC countries. Resour. Policy 2019, 63, 101429. [Google Scholar] [CrossRef]

- Kaufmann, D.; Kraay, A.; Zoido-Lobatón, P. Aggregating Governance Indicators; World Bank publications: Washington, DC, USA, 1999; Volume 2195. [Google Scholar]

- Acemoglu, D.; Johnson, S. Institutions, corporate governance. Corp. Gov. Cap. Flows A Glob. Econ. 2003, 1, 32. [Google Scholar]

- Islam, M.R.; McGillivray, M. Wealth inequality, governance and economic growth. Econ. Model. 2020, 88, 1–13. [Google Scholar] [CrossRef]

- Abdelbary, I.; Benhin, J. Governance, capital and economic growth in the Arab Region. Q. Rev. Econ. Financ. 2019, 73, 184–191. [Google Scholar] [CrossRef]

- Bekana, D.M. Innovation and economic growth in sub-Saharan Africa: Why institutions matter? An empirical study aross 37 countries. Arthaniti J. Econ. Theory Pract. 2021, 20, 161–200. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Variable | Definition | Source | Scale of Measurement |

|---|---|---|---|

| Economic growth (GDP) | GDP per capita is obtained by dividing the gross domestic product by the total population. | World Development Indicators (WDI) The World Bank | GDP per capita (Constant in 2010) |

| Government debt | External debt per cent of GDP | Government Finance Statistics of IMF | Debt to GDP ratio |

| Quality of governance (QoG) | The index of governance has been compiled by the moving average method from the ICRG dataset. | Developed by author using the ICRG dataset | Author compilation |

| Trade openness (TO) | Trade is the sum of imports and exports of services and goods as a % of GDP | WDI The World Bank | Trade (as % of GDP) |

| Labor force (LF) | LF includes people ages 15 and older who supply labor to produce goods and services during a specified period. | WDI The World Bank | Population aged (15 and above). Per cent of the total population |

| Fixed capital formation (FCF) | Gross FCF (% of GDP) is used to measure the capital constant 2010 USD. | WDI The World Bank | Gross FCF as % of GDP) |

| Variable | Observation | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|---|

| LGDPC | 1346 | 8.4113 | 1.1881 | 5.8700 | 11.1386 |

| DEBT | 1085 | 3.7468 | 0.7804 | 0.9894 | 5.6683 |

| TO | 1319 | 4.3568 | 0.5417 | 2.6212 | 6.0806 |

| LF | 1330 | 15.4459 | 1.8763 | 11.7334 | 20.4839 |

| FCF | 1266 | 23.6976 | 7.6414 | 0.00 | 69.6727 |

| QOG | 1177 | 0.5761 | 0.1897 | 0.1296 | 1.00 |

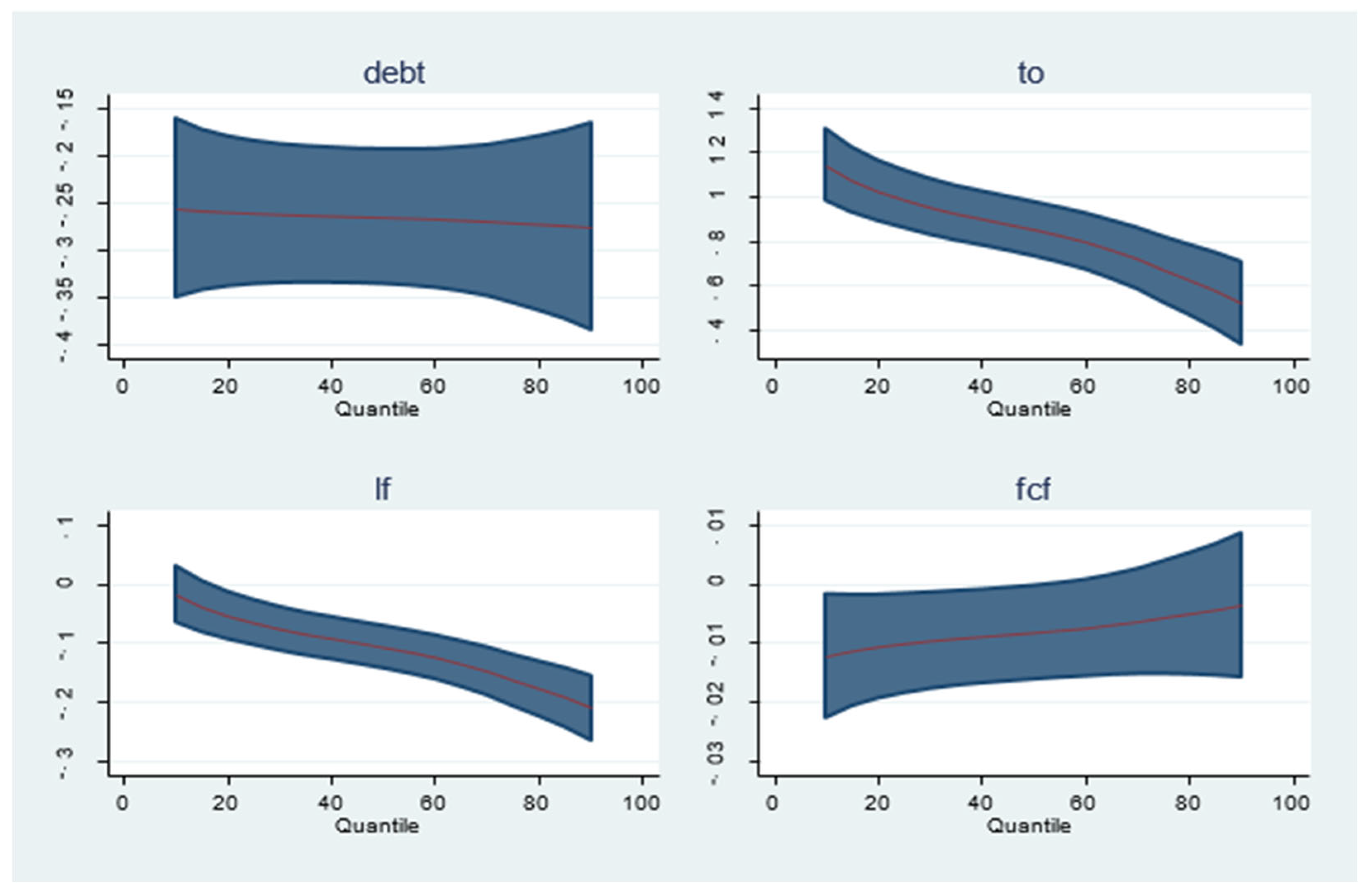

| VARIABLES | Location | Scale | q10 | q20 | q30 | q40 | q50 | q60 | q70 | q80 | q90 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| DEBT | −0.265 *** | −0.00584 | −0.256 *** | −0.259 *** | −0.262 *** | −0.263 *** | −0.265 *** | −0.266 *** | −0.269 *** | −0.272 *** | −0.275 *** |

| −0.0367 | −0.022 | −0.0484 | −0.0406 | −0.0376 | −0.0366 | −0.0366 | −0.0377 | −0.041 | −0.0473 | −0.0562 | |

| TO | 0.840 *** | −0.184 *** | 1.143 *** | 1.025 *** | 0.953 *** | 0.901 *** | 0.853 *** | 0.797 *** | 0.720 *** | 0.623 *** | 0.518 *** |

| −0.0623 | −0.0373 | −0.0825 | −0.0694 | −0.0641 | −0.0621 | −0.0622 | −0.0643 | −0.0704 | −0.0807 | −0.0948 | |

| LF | −0.112 *** | −0.0567 *** | −0.0191 | −0.0552 *** | −0.0774 *** | −0.0934 *** | −0.108 *** | −0.126 *** | −0.149 *** | −0.179 *** | −0.212 *** |

| −0.0182 | −0.0109 | −0.0242 | −0.0203 | −0.0188 | −0.0182 | −0.0182 | −0.0189 | −0.0206 | −0.0236 | −0.0277 | |

| FCF | −0.00803 ** | 0.00252 | −0.0122 ** | −0.0106 ** | −0.00958 ** | −0.00887 ** | −0.00820 ** | −0.00744 * | −0.00638 | −0.00506 | −0.00361 |

| −0.00404 | −0.00242 | −0.00532 | −0.00446 | −0.00414 | −0.00402 | −0.00402 | −0.00414 | −0.0045 | −0.0052 | −0.00617 | |

| Constant | 7.650 *** | 2.415 *** | 3.679 *** | 5.214 *** | 6.159 *** | 6.842 *** | 7.481 *** | 8.211 *** | 9.222 *** | 10.49 *** | 11.87 *** |

| −0.513 | −0.307 | −0.684 | −0.577 | −0.532 | −0.511 | −0.513 | −0.535 | −0.588 | −0.669 | −0.776 | |

| Observations | 1241 | 1241 | 1241 | 1241 | 1241 | 1241 | 1241 | 1241 | 1241 | 1241 | 1241 |

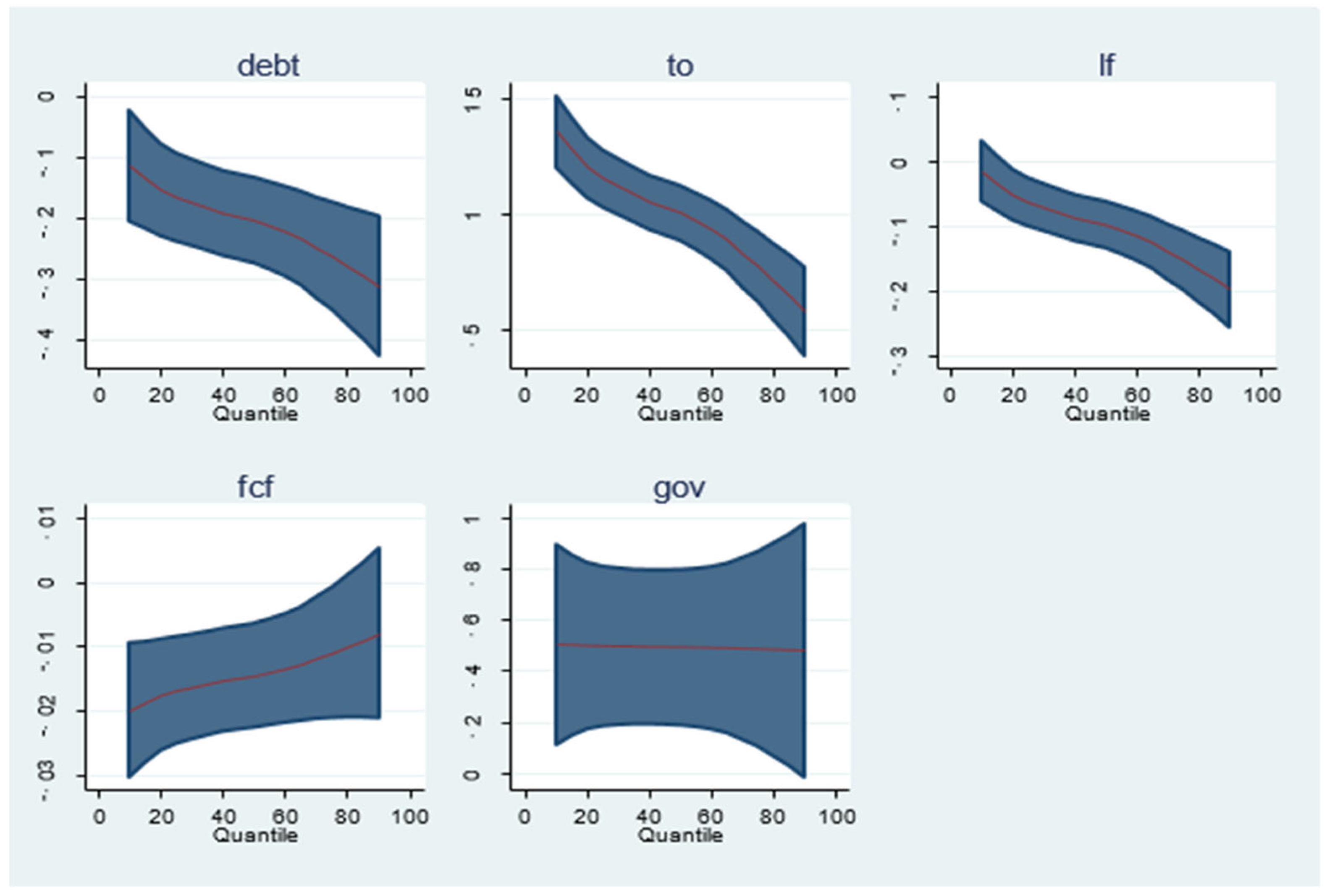

| VARIABLES | Location | Scale | q10 | q20 | q30 | q40 | q50 | q60 | q70 | q80 | q90 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| DEBT | −0.210 *** | −0.0575 *** | −0.114 ** | −0.154 *** | −0.175 *** | −0.192 *** | −0.204 *** | −0.222 *** | −0.249 *** | −0.280 *** | −0.312 *** |

| −0.0364 | −0.0222 | −0.0465 | −0.0387 | −0.0363 | −0.0357 | −0.036 | −0.0378 | −0.0424 | −0.0494 | −0.0587 | |

| TO | 0.980 *** | −0.226 *** | 1.357 *** | 1.202 *** | 1.120 *** | 1.051 *** | 1.006 *** | 0.933 *** | 0.827 *** | 0.708 *** | 0.580 *** |

| −0.0614 | −0.0373 | −0.079 | −0.0666 | −0.0613 | −0.0599 | −0.0606 | −0.0645 | −0.073 | −0.0838 | −0.0981 | |

| LF | −0.103 *** | −0.0529 *** | −0.0147 | −0.0511 *** | −0.0704 *** | −0.0865 *** | −0.0972 *** | −0.114 *** | −0.139 *** | −0.167 *** | −0.197 *** |

| −0.0184 | −0.0112 | −0.0236 | −0.0198 | −0.0184 | −0.018 | −0.0182 | −0.0192 | −0.0217 | −0.0251 | −0.0295 | |

| FCF | −0.0141 *** | 0.00348 | −0.0200 *** | −0.0176 *** | −0.0163 *** | −0.0152 *** | −0.0145 *** | −0.0134 *** | −0.0118 ** | −0.00996 * | −0.00797 |

| −0.00418 | −0.00254 | −0.00533 | −0.00443 | −0.00416 | −0.00409 | −0.00413 | −0.00432 | −0.00484 | −0.00566 | −0.00674 | |

| QoG | 0.493 *** | −0.00678 | 0.504 ** | 0.499 *** | 0.497 *** | 0.495 *** | 0.493 *** | 0.491 *** | 0.488 *** | 0.484 ** | 0.481 * |

| −0.158 | −0.0958 | −0.201 | −0.167 | −0.157 | −0.154 | −0.156 | −0.163 | −0.182 | −0.213 | −0.254 | |

| Constant | 6.611 *** | 2.674 *** | 2.138 *** | 3.977 *** | 4.955 *** | 5.769 *** | 6.311 *** | 7.172 *** | 8.433 *** | 9.832 *** | 11.36 *** |

| −0.503 | −0.306 | −0.655 | −0.559 | −0.505 | −0.49 | −0.497 | −0.538 | −0.613 | −0.693 | −0.8 | |

| Observations | 1091 | 1091 | 1091 | 1091 | 1091 | 1091 | 1091 | 1091 | 1091 | 1091 | 1091 |

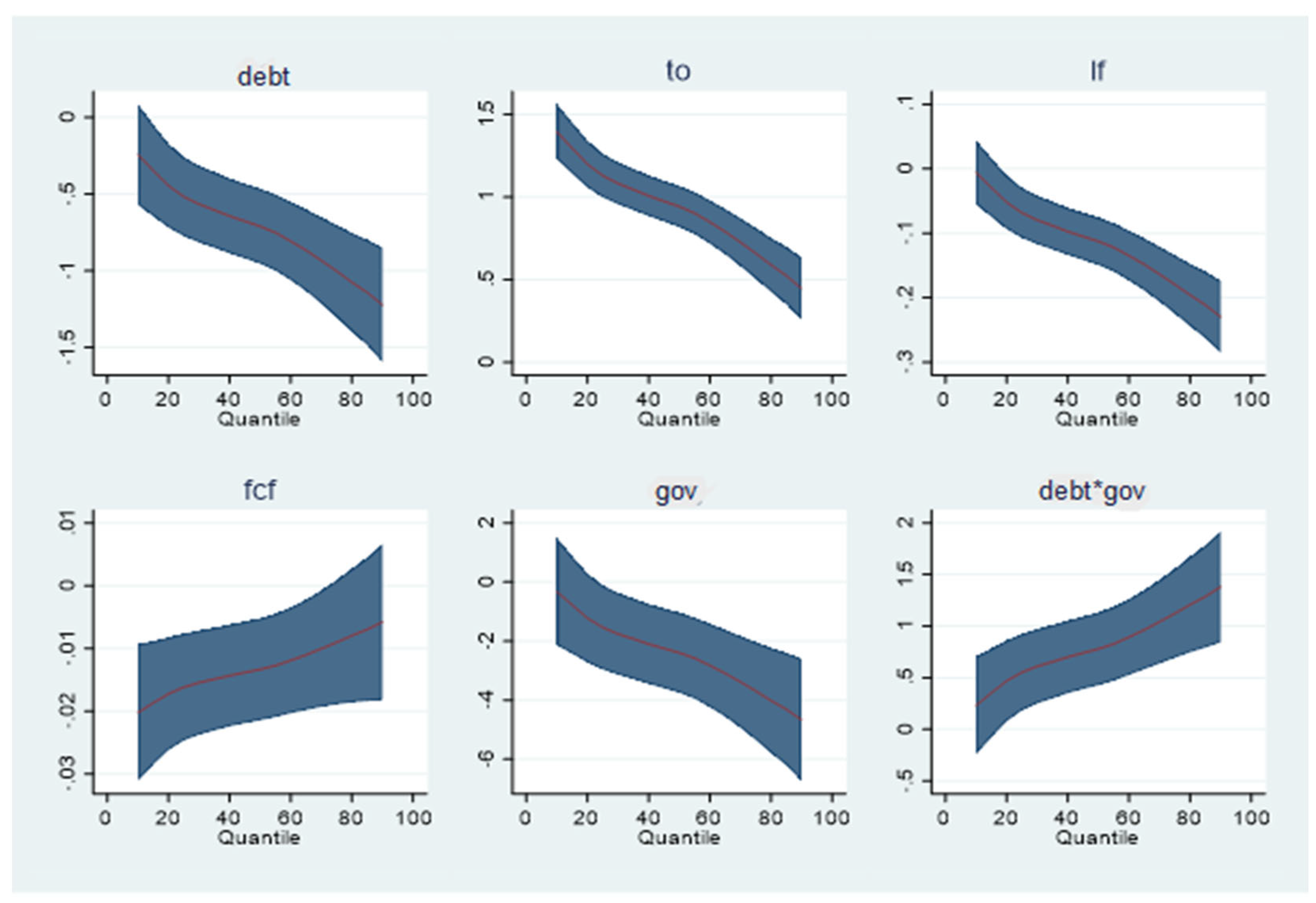

| VARIABLES | Location | Scale | q10 | q20 | q30 | q40 | q50 | q60 | q70 | q80 | q90 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| DEBT | −0.735 *** | −0.288 *** | −0.243 | −0.445 *** | −0.566 *** | −0.643 *** | −0.710 *** | −0.807 *** | −0.933 *** | −1.075 *** | −1.222 *** |

| −0.125 | −0.0755 | −0.168 | −0.139 | −0.127 | −0.124 | −0.125 | −0.13 | −0.143 | −0.163 | −0.19 | |

| TO | 0.918 *** | −0.279 *** | 1.395 *** | 1.199 *** | 1.082 *** | 1.007 *** | 0.943 *** | 0.848 *** | 0.726 *** | 0.589 *** | 0.446 *** |

| −0.0634 | −0.0382 | −0.0853 | −0.0722 | −0.0647 | −0.0625 | −0.0632 | −0.0669 | −0.0739 | −0.0831 | −0.0959 | |

| LF | −0.118 *** | −0.0659 *** | −0.00582 | −0.0521 ** | −0.0797 *** | −0.0973 *** | −0.113 *** | −0.135 *** | −0.164 *** | −0.196 *** | −0.230 *** |

| −0.0188 | −0.0114 | −0.0253 | −0.0212 | −0.0192 | −0.0186 | −0.0188 | −0.0197 | −0.0217 | −0.0246 | −0.0285 | |

| FCF | −0.0130 *** | 0.00425 * | −0.0202 *** | −0.0172 *** | −0.0154 *** | −0.0143 *** | −0.0133 *** | −0.0119 *** | −0.0100 ** | −0.00794 | −0.00577 |

| −0.00416 | −0.00251 | −0.00556 | −0.00458 | −0.00423 | −0.00413 | −0.00414 | −0.0043 | −0.00473 | −0.00543 | −0.00634 | |

| QoG | −2.505 *** | −1.277 *** | −0.326 | −1.224 | −1.757 ** | −2.099 *** | −2.395 *** | −2.826 *** | −3.383 *** | −4.012 *** | −4.666 *** |

| −0.694 | −0.419 | −0.928 | −0.767 | −0.705 | −0.688 | −0.691 | −0.719 | −0.791 | −0.906 | −1.056 | |

| DEBT * QoG | 0.809 *** | 0.339 *** | 0.231 | 0.469 ** | 0.611 *** | 0.701 *** | 0.780 *** | 0.894 *** | 1.042 *** | 1.208 *** | 1.382 *** |

| −0.181 | −0.109 | −0.242 | −0.2 | −0.184 | −0.179 | −0.18 | −0.187 | −0.206 | −0.236 | −0.275 | |

| Constant | 9.038 *** | 3.952 *** | 2.294 ** | 5.071 *** | 6.721 *** | 7.782 *** | 8.696 *** | 10.03 *** | 11.75 *** | 13.70 *** | 15.72 *** |

| −0.771 | −0.465 | −1.04 | −0.887 | −0.788 | −0.76 | −0.77 | −0.819 | −0.907 | −1.012 | −1.165 | |

| Observations | 1091 | 1091 | 1091 | 1091 | 1091 | 1091 | 1091 | 1091 | 1091 | 1091 | 1091 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Musa, K.; Sohag, K.; Said, J.; Ghapar, F.; Ali, N. Public Debt, Governance, and Growth in Developing Countries: An Application of Quantile via Moments. Mathematics 2023, 11, 650. https://doi.org/10.3390/math11030650

Musa K, Sohag K, Said J, Ghapar F, Ali N. Public Debt, Governance, and Growth in Developing Countries: An Application of Quantile via Moments. Mathematics. 2023; 11(3):650. https://doi.org/10.3390/math11030650

Chicago/Turabian StyleMusa, Kazi, Kazi Sohag, Jamaliah Said, Farha Ghapar, and Norli Ali. 2023. "Public Debt, Governance, and Growth in Developing Countries: An Application of Quantile via Moments" Mathematics 11, no. 3: 650. https://doi.org/10.3390/math11030650