NFTs and Cryptocurrencies—The Metamorphosis of the Economy under the Sign of Blockchain: A Time Series Approach

, , ,

, , ,

Abstract

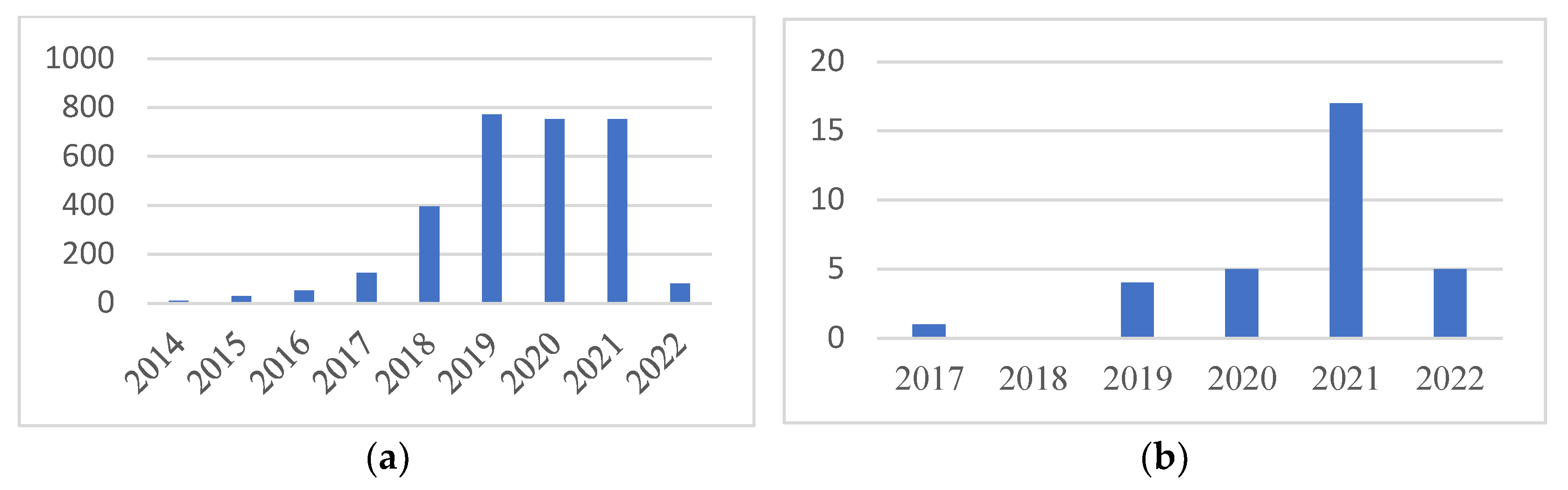

:1. Introduction

2. Literature Review

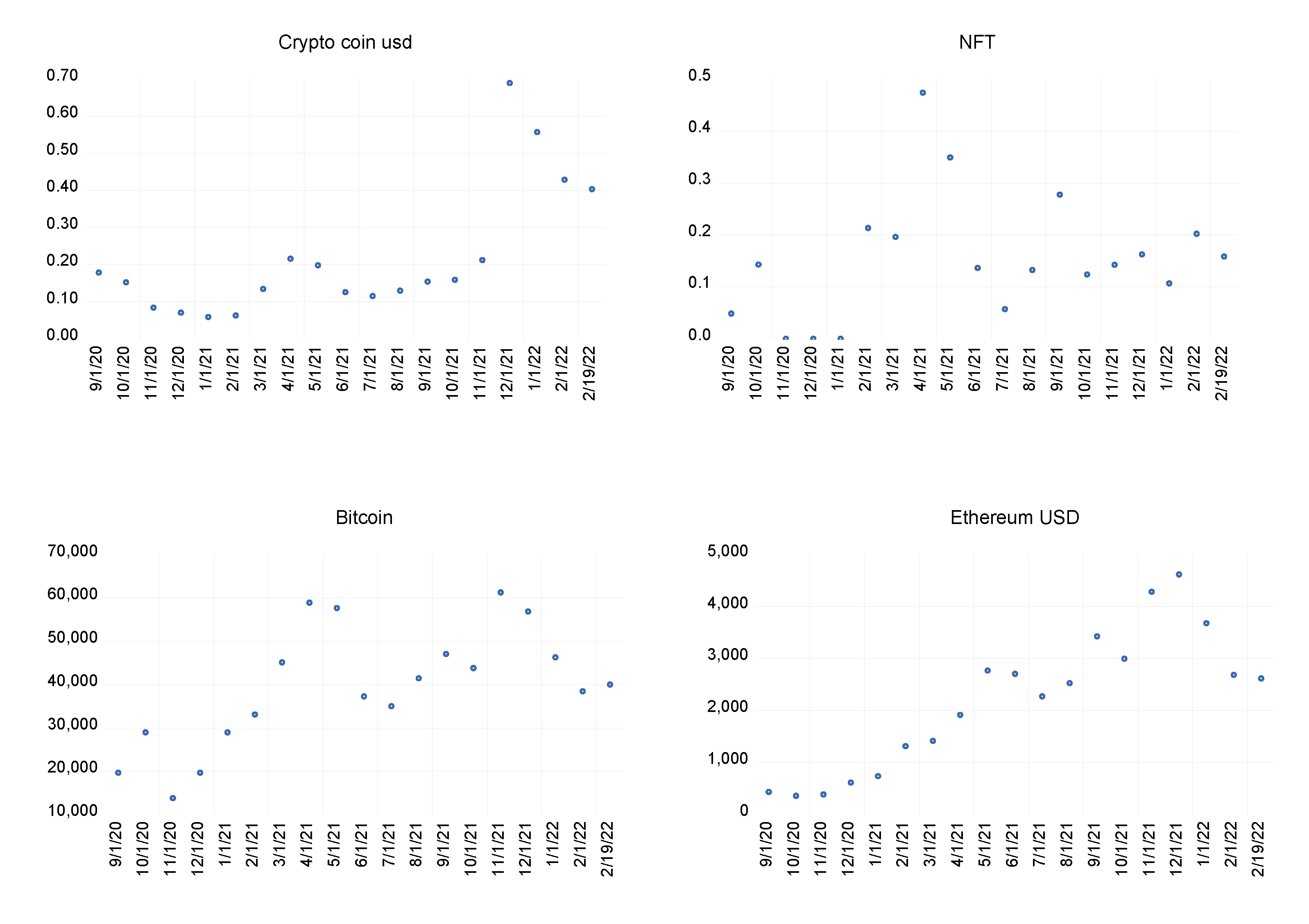

3. Data and Methodology

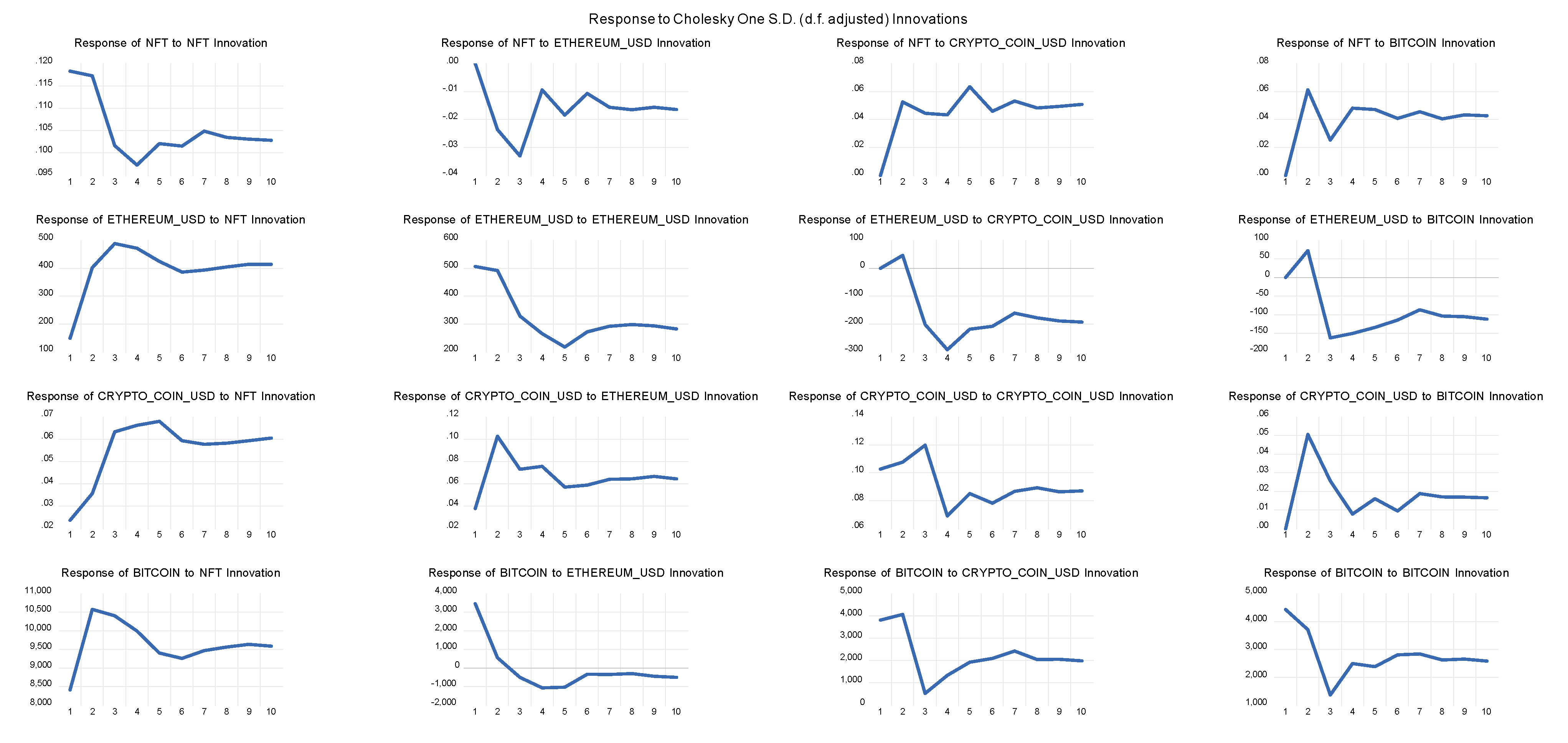

4. Empirical Results

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Akkaya, B.; Jermsittiparsert, K.; Abid Malik, M.; Kocyigit, Y. Emerging Trends in and Strategies for Industry 4.0 during and beyond COVID-19; De Gruyter: Berlin, Germany, 2021; p. 167. [Google Scholar]

- Amin, H.; Malik, M.A.; Akkaya, B. Development and Validation of Digital Literacy Scale (DLS) and its Implication for Higher Education. Int. J. Distance Educ. E-Learn. 2021, 7, 24–43. [Google Scholar] [CrossRef]

- Chopra, R.; Sharma, G.D. Application of Artificial Intelligence in Stock Market Forecasting: A Critique, Review, and Research Agenda. J. Risk Financ. Manag. 2021, 14, 526. [Google Scholar] [CrossRef]

- Khan, S.A.R.; Godil, D.I.; Bibi, M.; Yu, Z.; Rizvi, S.M.A. The Economic and Social Impact of Teleworking in Romania: Present Practices and Post Pandemic Developments. Amfiteatru Econ. 2021, 23, 787–804. [Google Scholar]

- Iordache, A.M.M.; Dura, C.C.; Coculescu, C.; Isac, C.; Preda, A. Using Neural Networks in Order to Analyze Telework Adaptability across the European Union Countries: A Case Study of the Most Relevant Scenarios to Occur in Romania. Int. J. Environ. Res. Public Health 2021, 18, 10586. [Google Scholar] [CrossRef] [PubMed]

- Pan, K.; Yue, X.G. Multidimensional effect of COVID-19 on the economy: Evidence from survey data. Econ. Res.-Ekon. Istraživanja 2021, 35, 1658–1685. [Google Scholar] [CrossRef]

- Vasile, V.; Panait, M.; Apostu, S.A. Financial inclusion paradigm shift in the postpandemic period. digital-divide and gender gap. Int. J. Environ. Res. Public Health 2021, 18, 10938. [Google Scholar] [CrossRef] [PubMed]

- Anghelache, C.; Anghel, M.G.; Iacob, Ș.V.; Panait, M.; Rădulescu, I.G.; Brezoi, A.G.; Miron, A. The Effects of Health Crisis on Economic Growth, Health and Movement of Population. Sustainability 2022, 14, 4613. [Google Scholar] [CrossRef]

- Bănescu, C.; Boboc, C.; Ghiță, S.; Vasile, V. Tourism in Digital Era. In Proceedings of the 7th BASIQ International Conference on New Trends in Sustainable Business and Consumption, Foggia, Italy, 3–5 June 2021; pp. 3–5. [Google Scholar]

- Belhadi, A.; Mani, V.; Kamble, S.S.; Khan, S.A.R.; Verma, S. Artificial intelligence-driven innovation for enhancing supply chain resilience and performance under the effect of supply chain dynamism: An empirical investigation. Ann. Oper. Res. 2021, 3, 1–26. [Google Scholar] [CrossRef]

- Bunduchi, E.; Vasile, V.; Ștefan, D.; Comes, C.A. Reshaping jobs in healthcare sector based on digital transformation. Rom. Stat. Rev. 2022, 1, 66–84. [Google Scholar]

- Sharma, G.D.; Yadav, A.; Chopra, R. Artificial intelligence and effective governance: A review, critique and research agenda. Sustain. Futures 2020, 2, 100004. [Google Scholar] [CrossRef]

- Popescu, A. Non-Fungible Tokens (NFT)-Innovation Beyond the Craze. In Proceedings of the 5th International Conference on Innovation in Business, Economics and Marketing Research, online, 27–29 May 2021. [Google Scholar]

- Yousaf, Z.; Radulescu, M.; Sinisi, C.I.; Serbanescu, L.; Păunescu, L.M. Towards sustainable digital innovation of SMEs from the developing countries in the context of the digital economy and frugal environment. Sustainability 2021, 13, 5715. [Google Scholar] [CrossRef]

- Zhen, Z.; Yousaf, Z.; Radulescu, M.; Yasir, M. Nexus of digital organizational culture, capabilities, organizational readiness, and innovation: Investigation of SMEs operating in the digital economy. Sustainability 2021, 13, 720. [Google Scholar] [CrossRef]

- Dowling, M. Is non-fungible token pricing driven by cryptocurrencies? Financ. Res. Lett. 2022, 44, 102097. [Google Scholar] [CrossRef]

- Nassani, A.A.; Sinisi, C.; Paunescu, L.; Yousaf, Z.; Haffar, M.; Kabbani, A. Nexus of Innovation Network, Digital Innovation and Frugal Innovation towards Innovation Performance: Investigation of Energy Firms. Sustainability 2022, 14, 4330. [Google Scholar] [CrossRef]

- Manta, O. Financial Technologies (FinTech), Instruments, mechanisms and financial products. Intern. Audit. Risk Manag. 2018, 52, 78–102. [Google Scholar]

- Ionescu, R.; Radulescu, I. Behavioral finance and the fast evolving world of fintech. Econ. Insights–Trends Chall. 2019, 8, 47–57. [Google Scholar]

- Sharma, G.D.; Jain, M.; Mahendru, M.; Bansal, S.; Kumar, G. Emergence of Bitcoin as an investment alternative: A systematic review and research agenda. Int. J. Bus. Inf. 2019, 14, 47–84. [Google Scholar]

- Pu, R.; Teresiene, D.; Pieczulis, I.; Kong, J.; Yue, X.G. The interaction between banking sector and financial technology companies: Qualitative assessment—A case of lithuania. Risks 2021, 9, 21. [Google Scholar] [CrossRef]

- Raimi, L.; Panait, M.; Hysa, E. Financial Inclusion in ASEAN Countries–A Gender Gap Perspective and Policy Prescriptions. LUMEN Proc. 2021, 15, 38–55. [Google Scholar]

- Răzvan, I. Financial Literacy in the Digital Age: Challenges and Opportunities in the European Union. Rev. Estrateg. Organ. 2021, 10, 1–16. [Google Scholar] [CrossRef]

- Manta, O.; Pop, N. The virtual currency and financial blockchain technology. Current trends in digital finance. Financ. Stud. 2017, 21, 45–59. [Google Scholar]

- Rehman Khan, S.A.; Yu, Z.; Sarwat, S.; Godil, D.I.; Amin, S.; Shujaat, S. The role of block chain technology in circular economy practices to improve organisational performance. Int. J. Logist. Res. Appl. 2021, 25, 605–622. [Google Scholar] [CrossRef]

- Șcheau, M.C.; Crăciunescu, S.L.; Brici, I.; Achim, M.V. A cryptocurrency spectrum short analysis. J. Risk Financ. Manag. 2020, 13, 184. [Google Scholar] [CrossRef]

- Dowling, M. Fertile LAND: Pricing non-fungible tokens. Financ. Res. Lett. 2022, 44, 102096. [Google Scholar] [CrossRef]

- Baker, B.; Pizzo, A.; Su, Y. Non-Fungible Tokens: A Research Primer and Implications for Sport Management. Sports Innov. J. 2022, 3, 1–15. [Google Scholar] [CrossRef]

- Valeonti, F.; Bikakis, A.; Terras, M.; Speed, C.; Hudson-Smith, A.; Chalkias, K. Crypto collectibles, museum funding and OpenGLAM: Challenges, opportunities and the potential of Non-Fungible Tokens (NFTs). Appl. Sci. 2021, 11, 9931. [Google Scholar]

- Chen, Y. Blockchain tokens and the potential democratization of entrepreneurship and innovation. Bus. Horiz. 2018, 61, 567–575. [Google Scholar] [CrossRef]

- Chohan, R.; Paschen, J. What marketers need to know about non-fungible tokens (NFTs). Bus. Horiz. 2021, in press. [Google Scholar] [CrossRef]

- Wilson, K.B.; Karg, A.; Ghaderi, H. Prospecting non-fungible tokens in the digital economy: Stakeholders and ecosystem, risk and opportunity. Bus. Horiz. 2021, 65, 657–670. [Google Scholar] [CrossRef]

- Mofokeng, N.; Fatima, T. Future tourism trends: Utilizing non-fungible tokens to aid wildlife conservation. Afr. J. Hosp. Tour. Leis. 2018, 7, 1–20. [Google Scholar]

- Bamakan, S.M.H.; Nezhadsistani, N.; Bodaghi, O.; Qu, Q. Patents and intellectual property assets as non-fungible tokens; key technologies and challenges. Sci. Rep. 2022, 12, 2178. [Google Scholar] [CrossRef] [PubMed]

- Borri, N.; Liu, Y.; Tsyvinski, A. The Economics of Non-Fungible Tokens. 2022. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4052045 (accessed on 12 June 2022).

- Bao, H.; Roubaud, D. Recent Development in Fintech: Non-Fungible Token. FinTech 2021, 1, 3. [Google Scholar] [CrossRef]

- Davis, F.D. Perceived usefulness, perceived ease of use and user acceptance of information technology. MIS Q. 1989, 13, 319–339. [Google Scholar] [CrossRef]

- Venkatesh, V.; Morris, M.G.; Davis, G.B.; Davis, F.D. User acceptance of information technology: Toward a unified view. MIS Q. 2003, 27, 425–478. [Google Scholar] [CrossRef]

- Rogers, E.M. Diffusion of Innovations, 5th ed.; Free Press: New York, NY, USA, 2003. [Google Scholar]

- Fernandez, P. Non-Fungible Tokens and Libraries. Libr. Hi Tech News 2021, 38, 7–9. [Google Scholar] [CrossRef]

- Idelberger, F.; Mezei, P. Non-fungible tokens. Internet Policy Rev. 2022, 11. [Google Scholar] [CrossRef]

- Truby, J.; Brown, R.D.; Dahdal, A.; Ibrahim, I. Blockchain, climate damage, and death: Policy interventions to reduce the carbon emissions, mortality, and net-zero implications of non-fungible tokens and Bitcoin. Energy Res. Soc. Sci. 2022, 88, 102499. [Google Scholar] [CrossRef]

- Dierksmeier, C.; Seele, P. Cryptocurrencies and business ethics. J. Bus. Ethics 2018, 152, 1–14. [Google Scholar] [CrossRef]

- Teichmann, F.; Falker, M.C. Money laundering through cryptocurrencies. In Artificial Intelligence Anthropogenic Nature vs. Social Origin, Proceedings of the 13th International Scientific and Practical Conference, Rezekne, Latvia, 17–18 June 2021; Springer: Cham, Switzerland, 2021; pp. 500–511. [Google Scholar]

- Borri, E.; Tafone, A.; Romagnoli, A.; Comodi, G. A review on liquid air energy storage: History, state of the art and recent developments. Renew. Sustain. Energy Rev. 2021, 137, 110572. [Google Scholar] [CrossRef]

- King, T.; Koutmos, D. Herding and feedback trading in cryptocurrency markets. Ann. Oper. Res. 2021, 300, 79–96. [Google Scholar] [CrossRef]

- Ante, L. Non-Fungible Token (NFT) Markets on the Ethereum Blockchain: Temporal Development, Cointegration and Interrelations. SSRN 2021, 3904683. [Google Scholar] [CrossRef]

- Ko, H.; Son, B.; Lee, Y.; Jang, H.; Lee, J. The economic value of NFT: Evidence from a portfolio analysis using mean-variance framework. Financ. Res. Lett. 2022, 47, 102784. [Google Scholar] [CrossRef]

- Borri, N.; Di Giorgio, G. Systemic risk and the COVID challenge in the European banking sector. J. Bank. Financ. 2022, 140, 106073. [Google Scholar] [CrossRef]

- Schaar, L.; Kampakis, S. Non-Fungible Tokens as an Alternative Investment: Evidence from CryptoPunks. J. Br. Blockchain Assoc. 2022, 31949. [Google Scholar]

- Umar, Z.; Gubareva, M.; Teplova, T.; Tran, D.K. COVID-19 impact on NFTs and major asset classes interrelations: Insights from the wavelet coherence analysis. Financ. Res. Lett. 2022, 47, 102725. [Google Scholar] [CrossRef]

- Lucey, B.M.; Vigne, S.A.; Yarovaya, L.; Wang, Y. The cryptocurrency uncertainty index. Financ. Res. Lett. 2022, 45, 102147. [Google Scholar] [CrossRef]

- Grobys, K. When Bitcoin has the flu: On Bitcoin’s performance to hedge equity risk in the early wake of the COVID-19 outbreak. Appl. Econ. Lett. 2021, 28, 860–865. [Google Scholar] [CrossRef]

- Pinto-Gutiérrez, C.; Gaitán, S.; Jaramillo, D.; Velasquez, S. The NFT Hype: What Draws Attention to Non-Fungible Tokens? Mathematics 2022, 10, 335. [Google Scholar] [CrossRef]

- Bitcoin USD. Yahoo Finance. Available online: https://finance.yahoo.com/quote/BTC-USD/ (accessed on 15 June 2022).

- Crypto Coin USD. Yahoo Finance. Available online: https://finance.yahoo.com/quote/CRO-USD?p=CRO-USD (accessed on 21 May 2022).

- Ethereum USD. Yahoo Finance. Available online: https://finance.yahoo.com/quote/ETH-USD?p=ETH-USD (accessed on 12 June 2022).

- NFT USD. Yahoo Finance. Available online: https://finance.yahoo.com/quote/NFT-USD?p=NFT-USD&.tsrc=fin-srch (accessed on 15 June 2022).

- Nadini, M.; Alessandretti, L.; Di Giacinto, F.; Martino, M.; Aiello, L.M.; Baronchelli, A. Mapping the NFT revolution: Market trends, trade networks, and visual features. Sci. Rep. 2021, 11, 20902. [Google Scholar] [CrossRef]

- Kong, D.R.; Lin, T.C. Alternative investments in the Fintech era: The risk and return of Non-Fungible Token (NFT). SSRN 2021, 3914085. [Google Scholar] [CrossRef]

- Ante, L. The Non-Fungible Token (NFT) Market and Its Relationship with Bitcoin and Ethereum. 2021. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3861106 (accessed on 19 June 2022). [CrossRef]

- Sims, C.A. Macroeconomics and reality. Econom. J. Econom. Soc. 1980, 48, 1–48. [Google Scholar] [CrossRef]

- Zou, X. VECM model analysis of carbon emissions, GDP, and international crude oil prices. Discret. Dyn. Nat. Soc. 2018, 2018, 5350308. [Google Scholar] [CrossRef]

- Raja, M.G.; Ullah, K. Relationship between Crimes and Economic Conditions in Pakistan: A Time Series Approach. J. Asian Dev. Stud 2013, 2. [Google Scholar]

- Engle, R.F.; Granger, C.W. Co-integration and error correction: Representation, estimation, and testing. Econom. J. Econom. Soc. 1987, 55, 251–276. [Google Scholar] [CrossRef]

- Khin, A.A.; Yee, C.Y.; Seng, L.S.; Wan, C.M.; Xian, G.Q. Exchange rate volatility on macroeconomic determinants in Malaysia: Vector error correction method (VECM) model. J. Glob. Bus. Soc. Entrep. (GBSE) 2017, 3, 36–45. [Google Scholar]

- Gujarati, D.N.; Porter, D.C. Basic Econometrics, 5th ed.; McGraw-Hill: New York, NY, USA, 2009. [Google Scholar]

- Sukumaran, S.; Bee, T.S.; Wasiuzzaman, S. Cryptocurrency as an Investment: The Malaysian Context. Risks 2022, 10, 86. [Google Scholar] [CrossRef]

- Abdul-Rahim, R.; Bohari, S.A.; Aman, A.; Awang, Z. Benefit–Risk Perceptions of FinTech Adoption for Sustainability from Bank Consumers’ Perspective: The Moderating Role of Fear of COVID-19. Sustainability 2022, 14, 8357. [Google Scholar] [CrossRef]

- Anifa, M.; Ramakrishnan, S.; Joghee, S.; Kabiraj, S.; Bishnoi, M.M. Fintech Innovations in the Financial Service Industry. J. Risk Financ. Manag. 2022, 15, 287. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Variables | Description | Studies in the Literature |

|---|---|---|

| NFT | NFT open price | Ante, 2021 [47], Dowling, 2022 [16]. Dowling, 2022 [27], Nadini et al., 2021 [59], Kong and Lin 2021 [60], Umar et al. [51] |

| Bitcoin | Bitcoin USD open price | Sharma et al. [12], Ante, 2021 [61], Dowling, 2022 [27], Umar et al., 2022 [51] |

| Crypto Coin USD | Crypto Coin USD open price | Ante, 2021 [47], Dowling, 2022 [16] |

| Ethereum | Ethereum open price | Ante, 2021 [47], Kong and Lin, 2021 [61] Dowling, 2022 [16], King and Koutmos Kong, 2021 [47], Truby et al., 2022 [42] |

| Variables | Mean | Standard Deviation | Min | Max | Skewness | Kurtosis |

|---|---|---|---|---|---|---|

| NFT-USD | 0.154 | 0.120 | 0.000 | 0.475 | 0.971 | 3.989 |

| Bitcoin USD | 39,668.58 | 13,713.11 | 13,780.99 | 61,320.45 | −0.155 | 2.251 |

| Crypto Coin USD | 0.217 | 0.175 | 0.059 | 0.690 | 1.518 | 4.257 |

| Ethereum | 2200.30 | 1325.39 | 360.31 | 4623.68 | 0.086 | 1.999 |

| Variables | Level | First Difference | ||

|---|---|---|---|---|

| t-Statistic | Prob. | t-Statistic | Prob. | |

| NFT-USD | −2.599 | 0.111 | −4.579 | 0.003 |

| Bitcoin USD | −1.891 | 0.328 | −3.726 | 0.014 |

| Crypto Coin USD | −1.386 | 0.566 | −4.026 | 0.008 |

| Ethereum | −1.405 | 0.556 | −3.495 | 0.022 |

| Hypothesized No. of CE(s) | Eigenvalue | Trace Statistic | 0.05 Critical Value | Prob.** |

|---|---|---|---|---|

| None | 0.770 | 49.500 | 47.856 | 0.035 |

| At most 1 | 0.543 | 24.537 | 29.797 | 0.179 |

| At most 2 | 0.375 | 11.237 | 15.495 | 0.197 |

| At most 3 | 0.174 | 3.241 | 3.842 | 0.072 |

| Hypothesized No. of CE(s) | Eigenvalue | Max-Eigen Statistic | 0.05 Critical Value | Prob.** |

|---|---|---|---|---|

| None | 0.7697 | 24.9629 | 27.5843 | 0.1004 |

| At most 1 | 0.5426 | 13.2992 | 21.1316 | 0.4251 |

| At most 2 | 0.3752 | 7.9968 | 14.2646 | 0.3790 |

| At most 3 | 0.1736 | 3.2407 | 3.8415 | 0.0718 |

| Error Correction: | D(NFT) | D(Crypto Coin) | D(Ethereum) | D(Bitcoin) |

|---|---|---|---|---|

| CointEq1 | −0.6046 (0.6352) [−0.9518] | −0.7421 (0.6014) [−1.2339] | 4929.719 (2828.57) [1.7428] | 82,207.85 (58,010.9) [1.4171] |

| D(NFT(−1)) | −0.2127 (0.4155) [−0.5120] | 0.0060 (0.3934) [0.0153] | −3751.910 (1850.31) [−2.0277] | −47626.48 (37,947.8) [−1.2551] |

| D(Bitcoin(−1)) | 6.16 × 10−6 5.9 × 10−6 1.0364 | 2 × 10−6 5.6 × 10−6 0.3554 | −0.4492 (0.3201) [−1.4031] | −10.6571 (0.5427) [1.6334] |

| D(Crypto coin(−1)) | −0.0836 (0.3097) [−0.2700] | −0.4775 (0.2932) [−1.6286] | 504.2578 (1378.99) [0.3657] | 19,493.50 (28,281.5) [0.6893] |

| D(Ethereum(−1)) | −0.0001 (7.2 × 10−5) [1.4162] | 0.0001 (6.8 × 10−5) [1.8618] | −0.4492 (0.3201) [−1.4031] | −10.6571 (6.5653) [−1.6233] |

| C | 0.0107 (0.0294) [0.3649] | 0.0027 (0.0279) [0.0984] | 131.4039 (130.998) [1.0031] | 1222.143 (2686.63) [0.4549] |

| Null Hypothesis | Chi-Sq | Prob. | Decision |

|---|---|---|---|

| D(Crypto Coin) does not Granger-cause D(NFT) | 0.0073 | 0.7871 | Do not reject |

| D(NFT) does not Granger-cause D(Crypto Coin) | 0.0002 | 0.9878 | Do not reject |

| D(Ethereum) does not Granger-cause D(NFT) | 2.0057 | 0.1567 | Do not reject |

| D(NFT) does not Granger-cause D(Ethereum) | 4.1117 | 0.0426 ** | Reject |

| D(Bitcoin) does not Granger-cause D(NFT) | 1.0741 | 0.3025 | Do not reject |

| D(NFT) does not Granger-cause D(Bitcoin) | 1.5752 | 0.2095 | Do not reject |

| D(Ethereum) does not Granger-cause D(Crypto Coin) | 3.4663 | 0.0626 * | Reject |

| D(Crypto Coin) does not Granger-cause D(Ethereum) | 0.1337 | 0.7146 | Do not reject |

| D(Bitcoin) does not Granger-cause D(Crypto Coin) | 0.1263 | 0.7223 | Do not reject |

| D(Crypto Coin) does not Granger-cause D(Bitcoin) | 0.4751 | 0.4907 | Do not reject |

| D(Bitcoin) does not Granger-cause D(Ethereum) | 8.9107 | 0.0028 *** | Reject |

| D(Ethereum) does not Granger-cause D(Bitcoin) | 2.6350 | 0.1045 * | Reject |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Apostu, S.A.; Panait, M.; Vasa, L.; Mihaescu, C.; Dobrowolski, Z. NFTs and Cryptocurrencies—The Metamorphosis of the Economy under the Sign of Blockchain: A Time Series Approach. Mathematics 2022, 10, 3218. https://doi.org/10.3390/math10173218

Apostu SA, Panait M, Vasa L, Mihaescu C, Dobrowolski Z. NFTs and Cryptocurrencies—The Metamorphosis of the Economy under the Sign of Blockchain: A Time Series Approach. Mathematics. 2022; 10(17):3218. https://doi.org/10.3390/math10173218

Chicago/Turabian StyleApostu, Simona Andreea, Mirela Panait, Làszló Vasa, Constanta Mihaescu, and Zbyslaw Dobrowolski. 2022. "NFTs and Cryptocurrencies—The Metamorphosis of the Economy under the Sign of Blockchain: A Time Series Approach" Mathematics 10, no. 17: 3218. https://doi.org/10.3390/math10173218