1. Introduction

The CMA is a quadrilateral monetary arrangement made up of Namibia, South Africa, Lesotho, and Eswatini (LENS). The main aim of its establishment is to enhance development among participant economies and effectively foster the coordination of economic policies (

Wörgötter and Brixiova 2019). This agreement places South Africa as the domineering or anchor country, which sets the economic pace for other participant countries. These small member countries submit their exchange rate policies to the South African Reserve Bank (SARB), hence, a fixed exchange rate system of the South African Rand against the Lesotho Loti, Namibian Dollar, and Eswatini Lilangeni on a one-to-one basis was established (

Seleteng 2016). The CMA agreement restrains small member countries: Namibia, Eswatini, and Lesotho (LEN), from exercising total discretion in monetary policy formulation and implementation (

Seoela 2020). At the same time, South Africa expresses total dominance when formulating the monetary policy of the entire region (

Nagar 2020). However, South Africa (SA) primarily targets its own economy when executing monetary policy (

Kamati 2014). The implications of the anchor country’s monetary policy decisions are deemed to be conveyed to all participant members (

Kamati 2020).

Monetary policy is a vital tool utilised for stimulating growth, reducing unemployment, and achieving stable prices in an economy through the monetary transmission mechanism (MTM) process. According to

Nagar (

2020), as much as monetary policy is a critical instrument for improving the performance of an economy and stabilising prices, it is vulnerable to shocks which can be detrimental to economic goals.

In the CMA region, the empirical evidence portrays that despite the regional collaboration, the countries are still experiencing poor economic growth (in terms of real GDP). For example, in 2020, on average, the RGDP_G of the CMA region declined to −6.91%, individually, Lesotho’s real GDP growth rate decreased to −11.06%, Namibia’s to −7.98%, Eswatini’s to −1.64% and South Africa’s to −6.96% (

World Bank Development Indicators 2022). Poor economic growth discourages firms from investing; businesses become unwilling to hire workers, and consumer spending becomes low, leading to low productivity, high price levels, job losses, or high unemployment (

Nagar 2020).

In such a case, monetary policy authorities employ expansionary or loose monetary policy that lowers the interest rate or indirectly increases the money supply to stimulate the economy (

Nagar 2020). In the literature, the traditional Keynesian theory suggests that an easing of monetary policy decreases the cost of borrowing or lowers the interest rate, which induces higher investment spending and more growth in output (

Mishkin 1995). Moreover,

Kamati (

2020) asserted that in the CMA, the Taylor rule is instrumental in explaining how South African monetary authorities regulate the interest rate to stimulate economic performance.

Monetary policy shock is defined as an unanticipated variation in a monetary tool, such as money supply or short-term interest rate, that accounts for changes in prices or output (

Nielsen et al. 2005). Monetary policy shocks can result in a positive or negative impact on economic performance. For instance, the study of

Kamati (

2014), using an SVAR framework in Namibia, revealed that a positive monetary policy shock resulted in a decline in output, a fall in inflation, and a decrease in credit. However, although Namibia is a member of the CMA, the study did not examine the impact of the monetary policy shock in the CMA region. Moreover,

Cheng (

2006), using an SVAR econometric model, investigated the effect of a shock on prices, output, and exchange rate in Kenya from 1997 to 2005. The findings revealed that a tight monetary policy was followed by a price decrease, with an insignificant effect on output.

According to the general equilibrium theory, when a shock occurs, the economy adjusts itself to restore the economy to equilibrium creating a business cycle (

Ennis 2018).

Ennis (

2018) asserted that movements in business cycles could be compared with trends in the short-term interest rate. Their argument stems from the view that the interest rate is a useful monetary policy instrument for inducing appropriate adjustment policies for economic stabilisation.

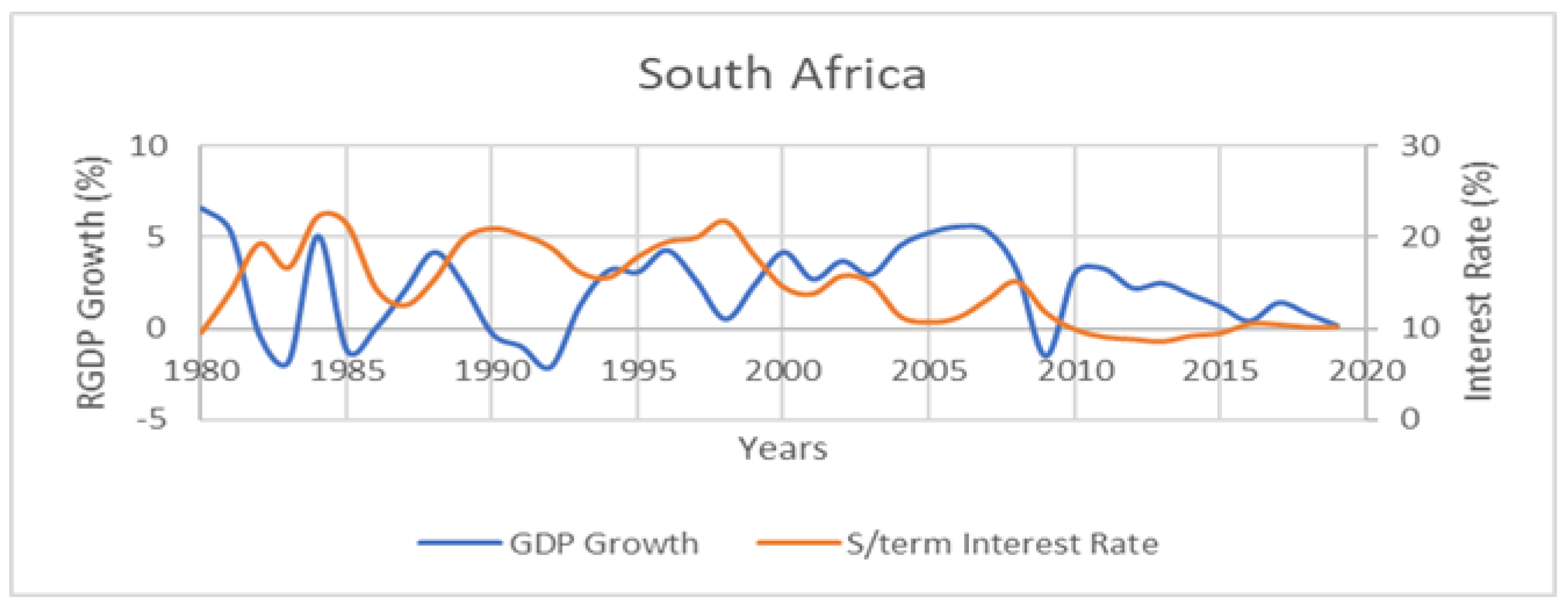

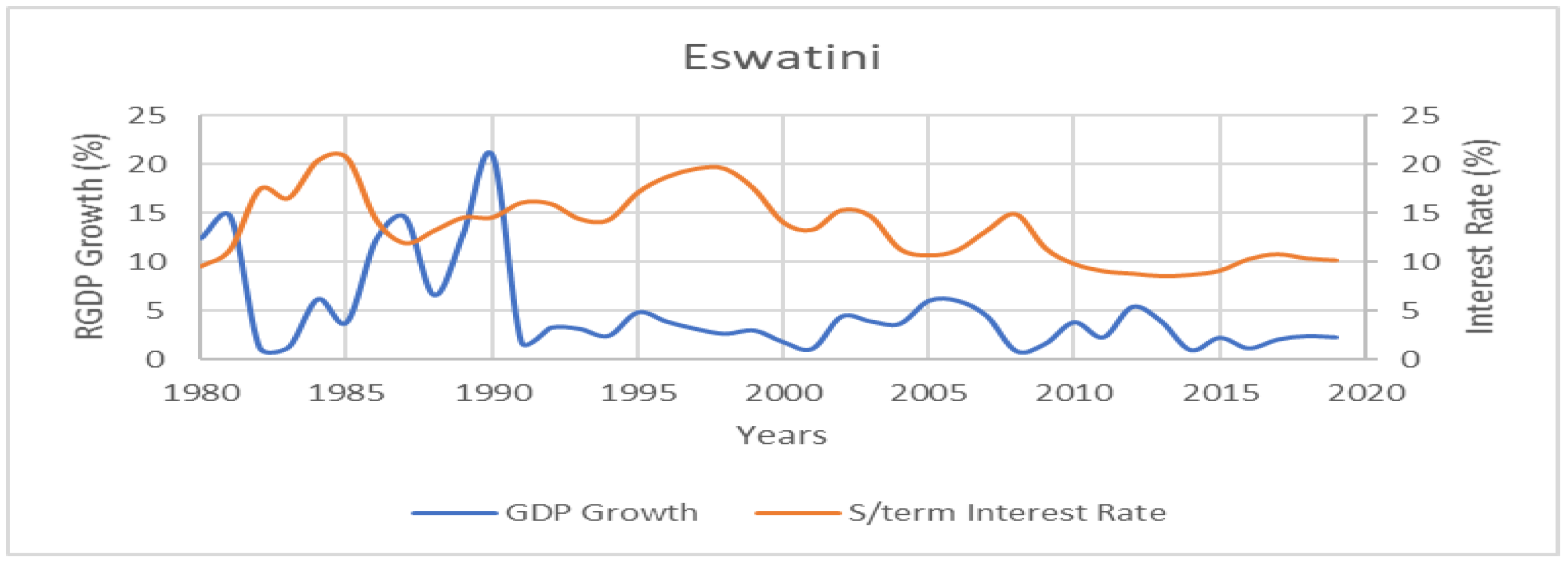

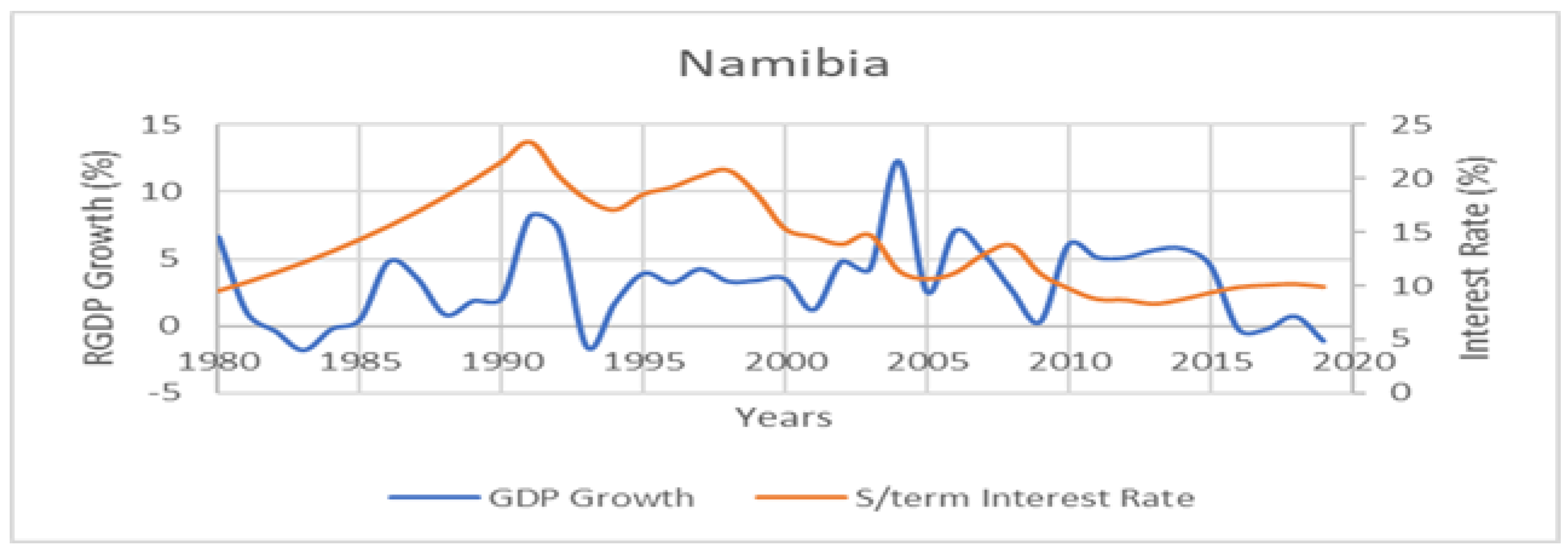

The trend analysis of the movement of the business cycles and short-term interest rates of CMA economies (

Figure 1,

Figure 2,

Figure 3 and

Figure 4) shows that only the RGDP_G of South Africa responded to the changes in short-term interest rates in line with the general theoretical expectations. Other member countries’ reactions to domestic short-term interest rate changes reflected unconventional responses. South Africa implemented an expansionary monetary policy through a decline in interest rates during recession periods and a restrictive monetary policy during periods of an economic boom. However, in other member countries,

Figure 1,

Figure 2,

Figure 3 and

Figure 4 shows the opposite. For instance, Eswatini experienced a recession from 1981 to 1983, yet its curve indicates a restrictive monetary policy was implemented. The movement in the business cycle of Lesotho in periods of recession (1987–1989), shows that a tight monetary policy was implemented instead of a loose monetary policy. Moreso, Namibia also experienced a boom between 2009 and 2010, but evidence from the business cycle movement shows that a loose monetary policy was instituted.

Moreover, despite introducing the inflation target framework by the anchor country in 2000, some CMA members have been experiencing an inflation rate beyond the target bandwidth of 3–6%. For instance, Lesotho reached an all-time high inflation rate of 35.15% in 2002 (

World Bank Development Indicators 2022). We hypothesise that shocks from South Africa might have adverse spillover effects on the performance indicators of CMA countries. The empirical observations in

Figure 1,

Figure 2,

Figure 3 and

Figure 4 reveal that despite the collaboration of CMA countries, the region poses a high vulnerability to spillover effects of monetary policy shocks from the anchor country, which could make their stabilising domestic policies ineffective. Therefore, this study fills the literature gap by investigating the impact of monetary policy shocks from the anchor country on performance variables such as output growth and inflation in the CMA region.

Conclusively, past studies in South Africa reveal that periods of restrictive monetary policy have a negative effect on output growth in South Africa, specifically industrial output (

Kutu and Ngalawa 2016;

Kabundi and Ngwenya 2011;

Seleteng 2016;

Ikhide and Uanguta 2010). However, very few studies have extended their analysis to the CMA region. There is still a lack of clarity on how monetary decisions from South Africa can influence the CMA region and the transmission channels through which the effects are conveyed. The objective of the study is focused on evaluating monetary-policy-induced innovations and how they affect macroeconomic performance indicators in the region. This study closes the literature gap by comparatively analysing the transmission of monetary policy shocks in the CMA.

2. Economic Performance in CMA

Economic performance can be defined as a measurement or indicator of how well an economy is doing in achieving its most crucial objectives (

Kashima 2017). According to

Chileshe et al. (

2018) the most predominant and key economic objectives targeted by any economy are price stability and a stable high rate of economic growth. The main objective behind the establishment of the CMA monetary union is in fostering economic advancement and development of less developed participant members (

Masha et al. 2007). In the measurement of economic performance economic growth, the Real Gross Domestic Product Growth (RGDP_G) rate has been regarded as a prominent indicator in the CMA region (

Kashima 2017). RGDP_G reveals the annual percentage change in the total value of goods and services produced in an economy adjusted for inflation (

Jane et al. 2018).

As evidenced by the graphical presentation in

Figure 5, the RGDP_G for all Common Monetary Area participants demonstrates close association from 1980 to 2021 since they trend together between these periods. The trend line depicts a below 5% growth rate, showing that the region has not been experiencing positive growth on average. The sharp peaks in the co-movement (for example in 1990 Eswatini reached an all-time highest growth rate of 21.01%, and in 2004 Namibia recorded a sharp peak of 12.27%) were attributed to the fact that both economies’ growth rate was boosted by surging exports (

Kashima 2017). In Namibia the lowest growth rate of −1.58% in 1993 and −1.25% for Lesotho in 2009, despite the close economic ties with South Africa, were due to the shift in some foreign investors who moved from these countries to invest in South Africa directly because of close proximity to South African markets (

Seleteng 2016). In 2019 the contraction and decline in the growth rate of all CMA economies could be attributed to strict lockdown measures, which constrained the trade and adversely affected the financial markets of CMA economies. However, a rebound in the growth rate of CMA economies from 2021 could be explained by the easing of lock down restrictions in support of export-oriented sectors (

Yingi 2022). In addition, another variable incorporated to measure economic performance is inflation.

Seleteng (

2016) asserted that the CMA seems to have benefited from low inflation rates after the anchor country’s inflation target framework of 2000 was introduced. However, there are periods after the CMA agreement of 1986 which reveal that inflation became more volatile in CMA countries. For instance, Eswatini recorded an all-time highest figure of 31.14% in 1988, Namibia hit its all-time highest inflation rate of 20.56% in 1992 after officially joining the CMA, Lesotho recorded an all-time highest figure of 35.15% in 2002, in the same year Namibia reached 12.72%, and in 2008 Namibia’s inflation rate was annualised at 9.7% (

World Bank Development Indicators 2022).

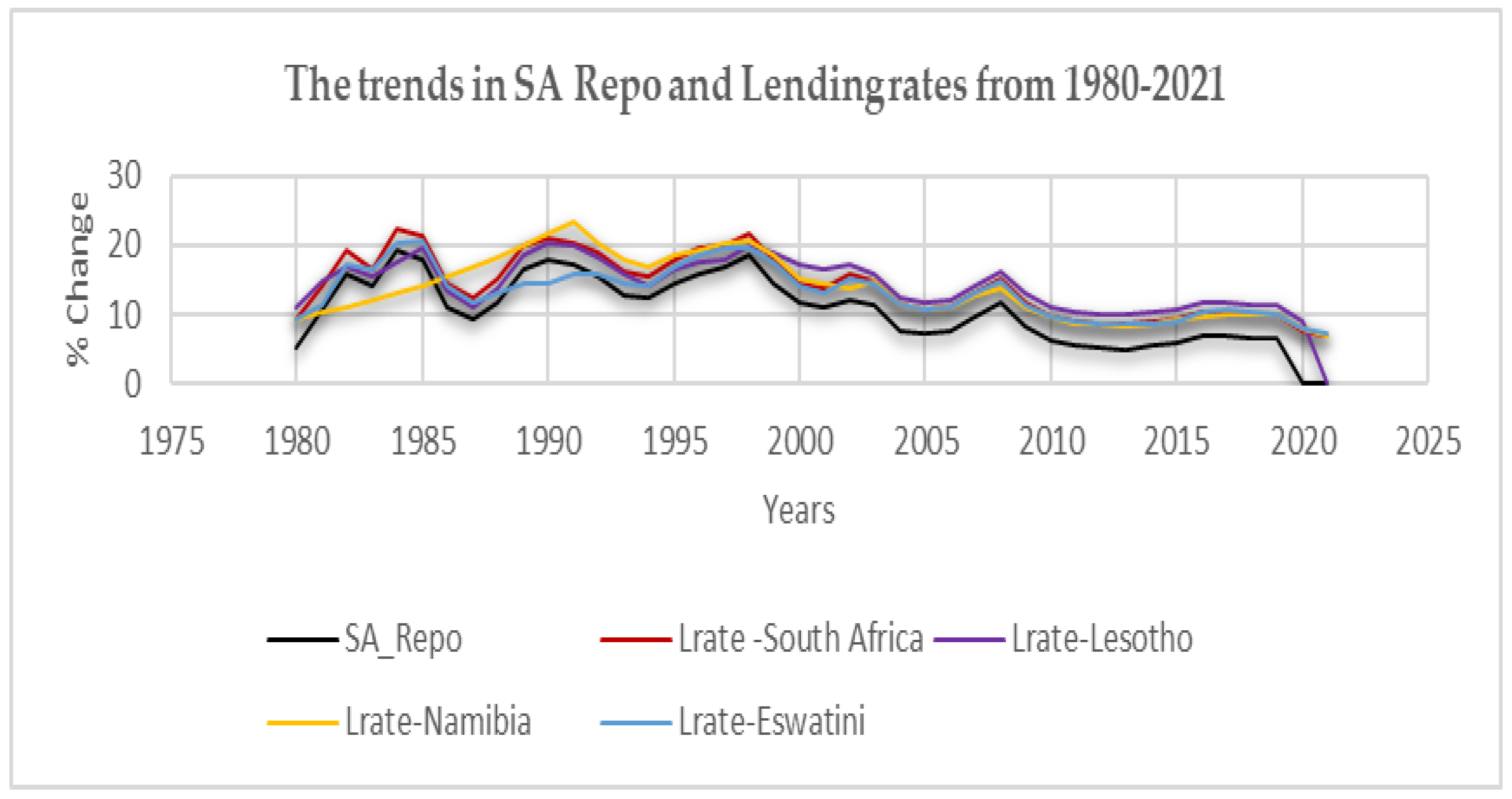

Furthermore, as depicted in

Figure 6 below, the CMA countries’ lending rates from 1980 to 2021 also show strong co-movements in the direction of the South African repo rate from 1980. The explanation of these co-movements is because the short-term interest rates in all member countries are set close to the repo rate of South Africa in order to maintain the agreed fixed peg.

3. Monetary Policy Shocks and Economic Performance

The Taylor rule and the traditional Keynesian theory forms the theoretical foundational basis for investigating the implications of the transmission of a shock from South Africa across the CMA region. According to

Rossouw and Padayachee (

2020), the Taylor rule propounds how a 1% increase in inflation is supposed to propel the central bank of South Africa to raise the short-term interest rate by more than 1%. Whereas in the traditional Keynesian theory, unlike the classical theory, it is posited that the economy does not remain at full employment equilibrium. They believe disequilibrium emanates from economic instability (

Mishkin 1995).

Furthermore, although this study is rooted in the Taylor rule and the traditional Keynesian theories on monetary policy, in the body of literature, empirical studies that examine the spillover effects of a shock from one economy to the economic performance of other economies are very few. For instance,

Mirdala (

2009) investigated the monetary spillover effects using a structural VAR econometric model in the Visegrad Group countries (Slovak Republic, Hungary, Poland, and Czech Republic). The findings revealed that a shock strongly impacted the real output of Visegrad countries, while the effect on inflation was inconclusive among the countries. In some countries, the shock resulted in an increase in inflation, while in others, it decreased.

Barigozzi et al. (

2014), using pooled data, employed a structural dynamic factor model in North European and South European countries; their findings revealed that after an expansionary policy, there are some differences in response to inflation or prices in North and South Europe. Whereas

Angeloni et al. (

2003), using the SVAR framework, found that an increase in interest rates had no observable effect on prices in the initial stages, whilst output decreased temporarily.

The most notable study of

Cavallo and Ribba (

2015) using a structural (near) VAR investigated the impact of area-wide shocks with particular attention to monetary policy shocks. Their conclusion was that a contractionary monetary policy causes similar recessionary effects in all countries and that as far as business cycle fluctuations are concerned, the largest European economies were mainly explained by common area-wide shocks, whereas in the second category of economies comprising Portugal, Ireland, and Greece, national shocks played a greater role.

Moreso,

Georgiadis (

2016), employed a Global VAR (GVAR) model to assess the global spillovers from identified US monetary policy shocks. The study found out that US monetary policy generates sizable output spillovers to the rest of the world, which are larger than the domestic effects in the US for many economies. The results suggested that policy makers could mitigate their economies’ vulnerability to US monetary policy by fostering trade integration as well as domestic financial market development, increasing the flexibility of exchange rates, and reducing frictions in labour markets.

Buigut (

2009), estimated a three-variable recursive VAR for three East African Community (EAC) countries using data from 1984 and 2006. The paper found that a shock to the short-term interest rate was found to have no statistically significant effect on real output and inflation. Nevertheless,

Bikai and Kenkouo (

2015) argued that these findings are biased by the fact that the study used a sample that includes too few observations for empirical analyses, resulting in few degrees of freedom.

Bikai and Kenkouo (

2015) proposed that using a panel-SVAR model could resolve these issues because it provides an effective way of dealing with over-parameterisation. In contrast, their results found that an expansionary monetary increases prices significantly in Kenya and Uganda, while output increases in Burundi, Kenya, and Rwanda. Similar to the current study, there are very few studies that compare the effect of South Africa’s monetary policy conduct on the performance of the CMA countries.

Ikhide and Uanguta (

2010) and

Seleteng (

2016) both examined the impact of SARB’s monetary policy on the CMA economies using a VAR framework. Unlike the approach in this study,

Ikhide and Uanguta (

2010) used monthly data but excluded economic output from the estimated models, while

Seleteng (

2016) used annually aggregated data. These studies focused on how changes in the SARB’s monetary policy instrument (repo rate) affect the money supply, credit, and prices in the CMA and thus evaluate the ability of the CMA economies to undertake independent monetary policy. Both studies found statistically significant results that lending rates and price levels were instantaneously sensitive to changes in the repo rate. However,

Ikhide and Uanguta (

2010) also found that money supply is instantaneously responsive to the repo rate, while

Seleteng (

2016) did not find any significant relationship.

Overall, the previous studies show opposing views on the impact of monetary policy on economic performance. Some support that increasing interest rates (contractionary monetary policy) negatively affects the economy, while others support that it has no observable impact on the economy.

However, the monetary interdependence in the CMA region between the leading economy (South Africa) and other member countries may create a high possibility of monetary spillover effects. This implies that the transmission of monetary policy shocks from South Africa can potentially influence the performance of participant economies positively or negatively.

In the CMA, the study of

Ikhide and Uanguta (

2010) examined how innovations in the South African repo rate influence money, credit, and price levels while investigating the small member countries’ capability to undertake independent monetary policy. Their findings revealed that the repo rate (SA_REPO) is a more effective monetary tool in influencing the participant countries in the CMA than bank rates.

Ikhide and Uanguta (

2010) found that other CMA countries could not independently undertake policies. Nevertheless, as mentioned in their study, the shortage of gross domestic product data was one of the challenges they encountered. A recent study by

Seoela (

2020) found that across the participant LENS countries, lending rate spread, credit, and money supply reacted asymmetrically to monetary innovations. However,

Seoela’s (

2020) study’s main drawback was that the author used the Chow–Lin approach of disaggregating data since output data were unavailable. The main challenge of such an approach is that it yields misleading results since the covariance matrix is unknown. Hence, this study fills the literature gap by employing annual real output growth data from 1980 to 2021. Another main challenge highlighted in the results of

Seoela (

2020) was the price puzzle problem.

Seoela’s (

2020) findings reveal that inflation increases in some countries after a one-standard-deviation shock is introduced to the South African repo rate. This empirical anomaly identified in

Seoela’s (

2020) study is referred as the price puzzle.

Rossouw and Padayachee (

2020) asserted that the price puzzle occurs when monetary policy committee of South Africa implement the short-term interest rate without sufficient observation of inflation signals in the future.

Nielsen et al. (

2005) argued that including commodity prices helps to tame the price puzzle problem. This study added to the body of knowledge by including commodity prices to purge and mitigate the price puzzle problem, which was not incorporated in the studies of

Seoela (

2020),

Ikhide and Uanguta (

2010), or

Seleteng (

2016).

Moreover, past studies reveal that there is no consensus about the impact of monetary policy shocks in the CMA region.

Ikhide and Uanguta (

2010) found out that a shock in the repo rate decreases prices or inflation in CMA countries, whereas the results of

Dlamini (

2018) and

Seoela (

2020) reflect the opposite.

6. Conclusions and Recommendation

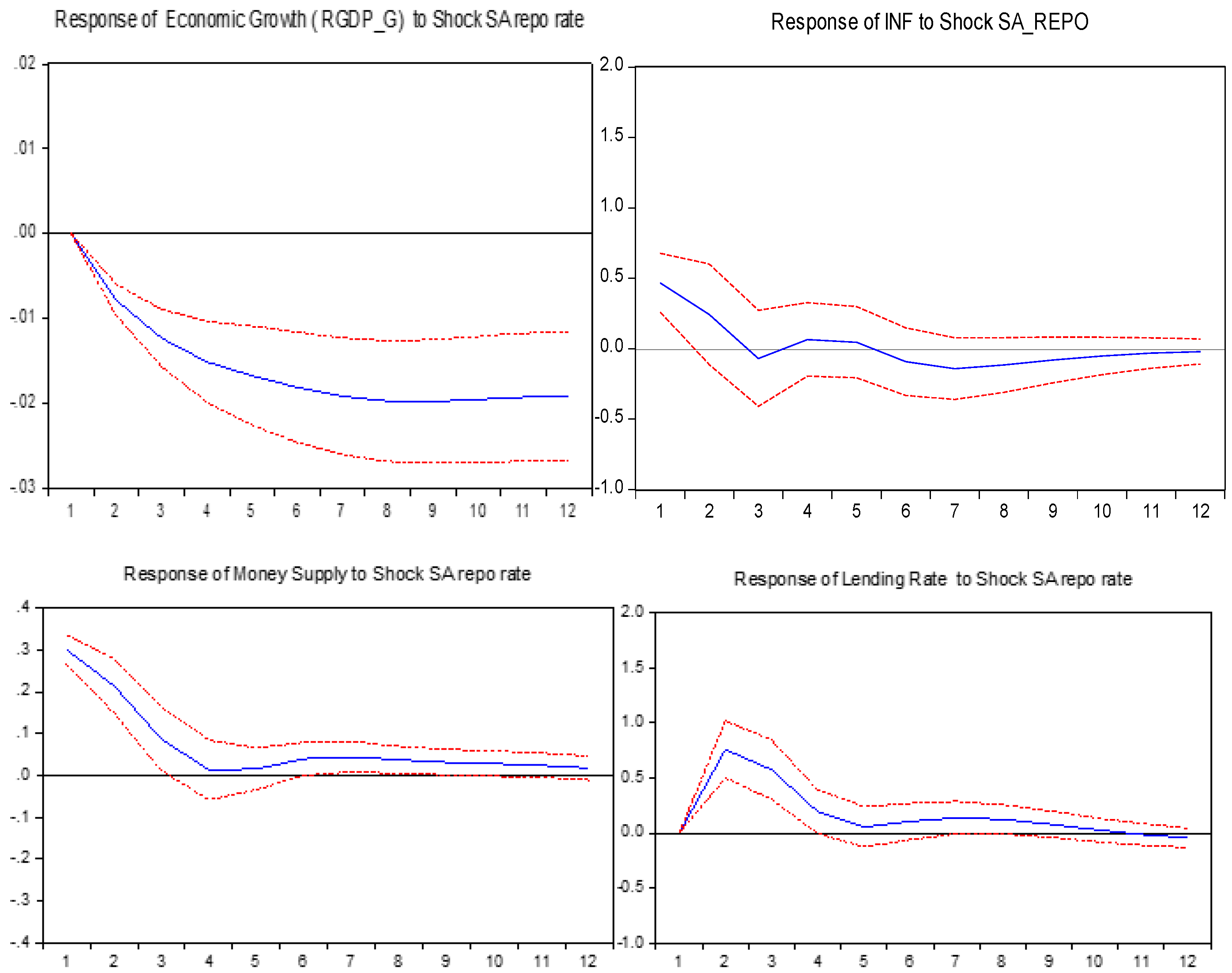

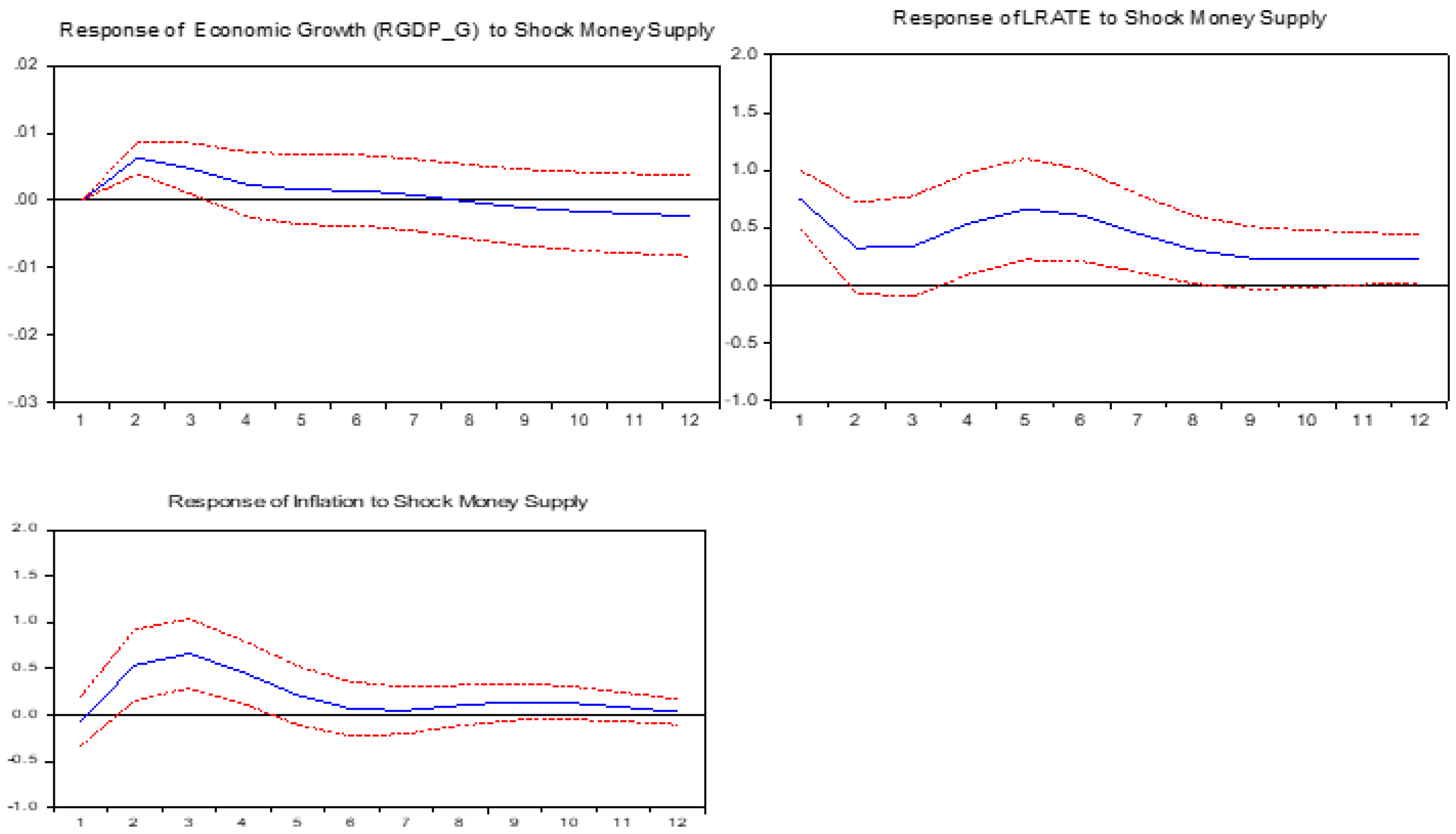

The study employed the panel-SVAR model utilising IRFs, and variance decompositions to achieve its primary objective of assessing the impact of monetary policy shocks from the leading economy on the CMA region’s economic activity. Conclusively, the study revealed that a shock from the South African repo rate or the main monetary instrument of the anchor country decreases inflation, reduces output growth, increases lending rates, and reduces the money supply in the CMA region. Based on the findings of the study it is suggested that policy makers and monetary authorities in the CMA should look inward and formulate policies towards stimulating the output of the entire region in order to offset or circumvent worsening economic performance in the CMA region.

Comparatively, although these findings were similar to the international study of

Cavallo and Ribba (

2015), which revealed that monetary policy shocks result in recessionary effects in the Euro Area. However, in the CMA, unlike in previous studies, global commodity prices were incorporated in this study as a global control variable which captures external factors since the CMA countries interact with other countries in the world market. Our findings further buttress that global commodity price as an exogenous variable has a forecasting ability which also helps in mitigating the price puzzle problem.

Sims (

1992), the first author to comment on the empirical anomaly of the price puzzle in VARs which is associated with monetary tightening, also verified the use of commodity prices to arrest the price puzzle problem. Hence, by including global commodity prices in the SVAR this study differs from both international and national studies. Hence this study also bridged the literature gap in solving the unconventional result of the price puzzle connected with restrictive or tight monetary policy. Global commodity prices can also serve as an information variable which can help the SARB in setting policy rates accurately as opined by the proponents of the Taylor rule. This study therefore fills the literature gap by including global commodity prices which adds onto

Ikhide and Uanguta (

2010),

Seleteng (

2016), and

Seoela (

2020), whose studies did not incorporate the global variable. Finally, it is highly recommended that governmental authorities in the CMA region establish a safety net and implement policies capable of stimulating economic growth and averting poor growth. Such policies must also be able to cushion the effect of unexpected shocks from the SA monetary policy decisions and also global shocks that may hit the region of the CMA. Hence, the CMA economies are urged to deliberate on the establishment of a common pool of reserves which will assist some of its members who form part of their integrated group and might need assistance due to shocks that might have hit their economies.

The research on regional integration must be ongoing since it is at the forefront of many countries. In the CMA region, aspects such as the inclusion of the SACU revenue in analysing the spillover effects of the leading economy’s monetary policy shock and external shocks remain uncovered. This is because the CMA countries form part of the SACU countries, and the revenue from the SACU may act as a cushion to galvanise small countries from potential shocks.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}