How to Hedge against Inflation Risk in Vietnam

Department of Accounting, Chaoyang University of Technology, Taichung City 41349, Taiwan

Economies 2023, 11(3), 94; https://doi.org/10.3390/economies11030094

Submission received: 15 January 2023

/

Revised: 8 March 2023

/

Accepted: 9 March 2023

/

Published: 14 March 2023

(This article belongs to the Section Macroeconomics, Monetary Economics, and Financial Markets)

Abstract

:Vietnam has experienced galloping inflation and faced serious dollarization since its reform. To effectively control inflation for promoting price stability, it is necessary to find efficacious leading indicators and a hedging mechanism. Using monthly data over the period from January 1997 to June 2020, this study finds the predictive power and hedge effectiveness of both gold and the US dollar on inflation in the long-run and short-run within the asymmetric framework. Especially, the response of inflation to the shocks of gold price and the US dollar is quick and decisive, disclosing the sensitivity of inflation to these two variables.

Keywords:

asymmetric cointegration; gold price; inflation hedge; MSI-VAR(1) model; the US dollar; VietnamJEL Classification:

C22; L85; P441. Introduction

One of the most vital responsibilities of policymakers in several countries is to control inflation for promoting two long-run goals: price stability and sustainable economic growth, since inflation connects tightly to the purchasing power of currency within its border and affects its standing on the international markets. Therefore, the foresight of inflation is essential as policy actions to restrain inflation typically take effect only after a long lag.

Several indicators may help predict inflation, which can be roughly classified into three basic groups—commodity prices, and financial and economic variables. The specific prices of commodities such as oil and precious metals might predict inflation because they directly influence the price level of consumer goods. Financial indicators such as exchange rates, interest rates, and money growth might predict inflation since they reflect current or future monetary policy. The economic indicators including unemployment rates and GDP growth might predict inflation since they convey information on excess demand conditions in the economy.

Inflation makes the currency “shelter” in gold and the USD. Ghosh et al. (2004) study the relationship between the gold price and the USD exchange rate in the short- and long-term and concluded that gold price increases along with the inflation rate over time, allowing gold to be considered as a hedging tool. When investors are very afraid that the world economy will get worse and the stock market keeps sliding downhill, investors choose to withdraw their investments in stocks and other risky assets and switch to buying gold and holding cash (a lot of which is in USD). Therefore, in a time when people are very risk-averse, gold not only acts as a hedge against currency devaluation but also acts as a hedge in the modern era, since 1971, when the gold standard ended and gold is freely traded. However, to a certain extent, the link between gold and the US dollar still exists: a certain connection for gold has been used as money and a sign of wealth for thousands of years.

Several articles published in both scientific and financial journals show that a relationship exists between the gold price and real inflation over time. For example, Chua and Woodward (1982); Jaffe (1989), and McCown and Zimmerman (2006) all found a significant relationship between the inflation index and the gold price. Ghosh et al. (2004) and Worthington and Pahlavani (2007) all provide evidence of a long-run cointegration relationship between gold and inflation. In contrast, Tully and Lucey (2007), using the PGARCH approach, did not find a significant relationship between inflation and gold. Some studies show a relationship between gold and expected inflation such as Moore (1990) and Adrangi et al. (2003). Others show that gold is a good hedge against unexpected inflation such as Christie-David et al. (2000). Besides, Cecchetti et al. (2000) and Blose (2010) did not find a relationship.

Inflation is regarded as one of the biggest effects of currency depreciation. When the domestic currency depreciates, it loses value and purchasing power, and the prices of imported goods and materials increase relative to those that are domestically produced, making import-related goods more expensive. Since import is a part of the consumption basket, measures of inflation based on that basket will also rise in the type of cost–push inflation. However, the evidence on the hedging power of exchange rates for inflation is mixed. Several studies find that exchange rate movements are followed by substantial changes in the price level (Papell 1994; Uribe 1997; Kim 1998; Umar and Dahalan 2016; Nasir et al. 2020). Other studies suggest that exchange rate movements have temporary and small effects on price levels (Saha and Zhang 2013; Peon and Brindis 2014).

Different from the increase in the US dollar (USD) price, the rise in gold price might cause demand–pull inflation due to its conspicuous property. Gold has also served for centuries as money and has always preserved its purchasing power over long periods of time. Although gold no longer plays an essential role in the world’s monetary system, after the shift from the gold standard to a fiat money system, the price of gold is still considered by many to be a reliable leading indicator of inflation because the price of gold rises when people are afraid that paper money cannot preserve their wealth. According to Worthington and Pahlavani (2007), The demand for gold is increasing, not only for jewelry, gold coins, and bars, but also for many industries such as electronics, aerospace, and medical technology. The shreds of evidence regarding the relationship between gold prices and inflation are not consistent in studies. Some find a positive relationship between the gold price and inflation Garner (1995); Ranson and Wainright (2005); Levin et al. (2006); Worthington and Pahlavani (2007); Tkacz (2007); Wang et al. (2011); Van Hoang et al. (2016); Salisu et al. (2019); Sui et al. (2021). Others provide pieces of evidence on the bi-directional relationship between inflation and commodity prices Jaffe (1989); Ghosh et al. (2004); Kyrtsou and Labys (2006); Worthington and Pahlavani (2007).

The reasons explained for the mixed empirical evidence might be the differences in economic structure, degrees of openness, and monetary strategy. During the transition from a centrally planned to a market-oriented economy, Vietnam has been facing galloping inflation. The dollarization became severe in the early 1990s when the country was suffering an inflation crisis. At that time, gold and the US dollar were chosen to hold for protecting the value of a property. Since then, any increase in expected inflation might cause people to recall this hard experience and, hence, to collect gold and the US dollar. Indexation is notably seen in real estate values, which are preferred to price in the US dollar or gold. Fluctuations in the values of USD and gold, therefore, have immediate impacts on real estate prices and, thus, might contribute to increased consumer prices.

This article aims at exploring whether gold and the US dollar price movements can, to any degree, lead to movements of future inflation in Vietnam. To the best of my knowledge, this is one of the few studies bringing the asymmetric framework into the examination of the relationship between gold and inflation, as well as the US dollar and inflation. The asymmetric cointegration test and the dynamic MSI-VAR(1) model are employed to examine the asymmetric inflation hedge of gold and the US dollar in both the long-run and short-run. The evidence shows that both gold price and the US dollar not only present their effective hedge in the long-run but also work as leading indicators for future inflation in the short-run. The response of inflation to the shock of gold returns and USD appreciation significantly occurs in the first four months; in other words, the hedging power in the short-run is greater than in the long-run. The asymmetry effect, multiple breaks, and outlier detection in time series allowed in this article are also the main contribution of this empirical study.

2. Methodology

The Markov switching (MS) model developed by Hamilton (1989) is one of the most important models in econometrics because it allows for both changes in mean and variance, multiple breaks, and time series outlier detection. Following Krolzig (2000), the Markov switching vector autoregressive (MSI-VAR(p)) process is developed for exploring the inflation hedge of gold price and the US dollar (USD). The basic switching model can be extended to a dynamic one in the form of lagged endogenous variables and serially correlated errors.

In general, an autoregressive model of order p with M-state Markov-switching intercept (MSI) is as follows:

where represents the inflation rates at time t. is the mean, estimated by the equation , depending on the regime at time t. are the autoregressive coefficients. is the error term following , and is the variance estimated by the equation , depending on the regime at time t.

Frühwirth-Schnatter (2006) provides a fine overview of this approach. The most straightforward method to add dynamics to a switching model is to combine lagged endogenous variables. This dynamic MSI-VAR(p) model allows us to not only detect potential regime shifts in the high and low inflation but also investigate the impacts of inflation on the gold price and the US dollar (USD) exchange rate and vice versa. The empirical models are designed as follows:

Model 1: The inflation hedge of the US dollar (USD)

Model 2: The inflation hedge of gold price

where is the inflation rate at time t, is the gold return rate at time t, and is USD return rates at time t. are the coefficients of the regime means. is the innovation process accompanied with the parameter shift functions that represents the variance depending on regime . p is the lagged endogenous regressor.

The requirement of first-order Markov assumption is the dependence on the previous state of probability of being in a regime, so that:

These probabilities are presented in a transition matrix of an ergodic M-state Markov process as follows:

where the -th element stands for the probability of shifting from regime in period to regime in period . Since the Markov switching (MS) model is also nested with structural breaks, it can be used for detecting sustained breaks.

A major advantage of this dynamic MSI-VAR model is its flexibility in modeling time series subject to regime shifts, and it is generally able to capture the potential of regime shifts in the time-series data of CPI, USD, and gold price without considering structural breaks, to the extent that these variables have experienced several unstable periods and high volatility over the last three decades. Krolzig (2000) suggests that considering the regime-switching characteristics of the economic process may provide a better predictive method than the time-varying linear model and traditional robustness methods if there exist permanent breaks.

3. Empirical Results

3.1. Data and Tests

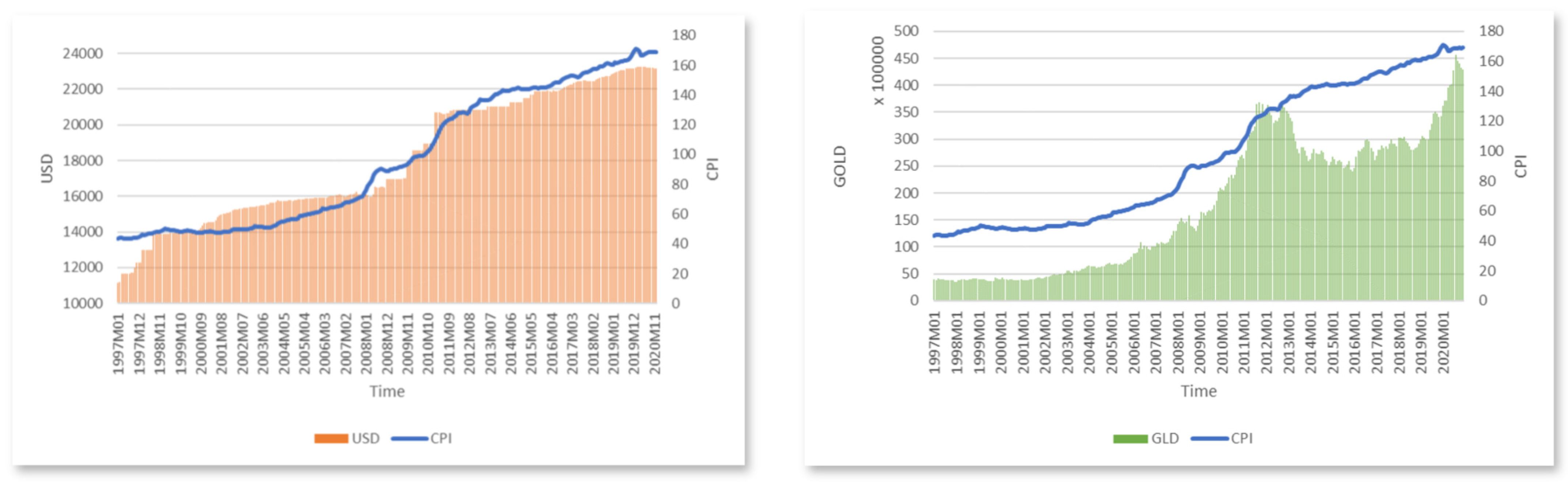

The analysis is based on the monthly data of the consumer price index (CPI), domestic currency per US dollar (USD), and gold price (GLD) for the period from January 1997 to December 2020. The consumer price index (CPI) and the domestic currency per US dollar (USD) are obtained from the international financial statistics (IFS) database of the International Monetary Fund (IMF), and the gold price (GLD) is obtained from the world gold council. Gold is priced in Vietnamese Dong per ounce based on the London pm fix. The sample includes 288 observations which are used for examining the inflation hedging effectiveness of USD and gold investment in Vietnam. When carrying out the test as well as the estimation, all variables are formed in a natural logarithm. The origin time trends and volatility of the three variables are displayed in Figure 1.

Table 1 reports the descriptive statistics of CPI, USD, and gold prices. The means of these three variables are all positive, indicating their increasing tendency of them during the sample period. After the demise of the Bretton Woods international monetary system in 1971, many countries chose the floating exchange rate policy while others selected to operate under currency pegs. Vietnam followed the second one and has shifted its monetary policy to “managed floats” that allow their local currency to fluctuate within a 3507.33 over time. The skewness and kurtosis show the right-skewed and platykurtic distributions of variables. Furthermore, Jarque–Bera statistics significantly reject the hypothesis of normality for all three variables.

The i.i.d (independent and identically distributed) characteristic of one series does not change after being switched to any linear or nonlinear series. It can be inferred that the reason for rejecting the normality hypothesis could be autocorrelation. As the descriptive statistics of the sample stated in Table 1, the value shows the high serial correlation and the conditional heteroscedasticity of variables. These characteristics may conceal the nonlinearity of data.

This study mainly utilizes the dynamic MSI-VAR model to examine the inflation–hedging effectiveness of USD and gold investment in Vietnam. The empirical process has proceeded in two steps. First, the unit root test is employed to CPI, USD, and gold prices for identifying their stationarity. It is then followed by the cointegration test for finding the long-run relationship among variables. Second, if the asymmetric cointegrations among variables are clarified, the inflation hedge of USD and gold prices are explored with the dynamic MSI-VAR model.

Nelson and Plosser (1982) found that the non-stationarity of macroeconomic variables may lead to spurious regression because the hypothesis of stationarity or residual stationarity of regression is not satisfied. Unit root tests are commonly used to verify the integrated order of time series and to decide the level or differential variable for the empirical process. The unit root test results are reported in Table 2. The stationarity of variables is tested with the Augmented Dickey–Fuller (ADF) and the Phillips–Perron (PP) regressive equation including both intercept and time trend. The optimal lag length is selected according to the Schwartz information criterion (SIC). The test results show that the integration orders of the three variables are I(1) at the level and I(0) at the first difference.

The results of the Engle–Granger test for linear cointegration are reported in Table 3. According to these results, the relationship between CPI and USD, as well as CPI and gold price, cannot get rid of the long-run time trend.

Table 4 presents the results of asymmetric cointegration with the threshold autoregression (TAR) model proposed by Enders and Siklos (2001) for testing the long-run relationship between two couple of variables. The optimal lag lengths are selected by two criteria including SC (Schwarz information criterion), and HQ (Hannan–Quinn information criterion) for which the maximum lag of 15 periods is applied. Both criteria choose the lag as 1 period, which seems reasonable for monthly data to respond to the dynamic hedge of USD and gold price on inflation, conforming to the intuition on economics. Therefore, this study adopts the lag length of 1 to test for cointegration as well as to estimate the model. The results of TAR prove the presence of asymmetric cointegration between CPI and USD, as well as CPI and gold prices. Therefore, the dynamic MSI-VAR(1) model that allows for changes in mean and variance, multiple breaks, and time series outliers detection, is more appropriate for examining the inflation hedge of USD and gold investment.

3.2. Empirical Findings

Table 5 provides the regime-varying results of the MSI-VAR(1) model. The results of Model 1 and Model 2 present the estimated coefficients of the regime mean δ, β, α, and γ corresponding to endogenous variables. The differences in the regime-specific means correspond to high and low momentum periods where the high momentum period refers to high inflation rates or high return rates and the low momentum period refers to as low inflation rates or low returns.

Model 1 is designed for testing the inflation hedge of the US dollar (USD). Within regime 1, the USD returns in period t − 1 positively influence inflation rates of period t (0.558), while the effects of inflation rates of period t − 1 on both the USD returns and inflation rates of period t are significant and positive. Within regime 2, these interactions between the USD return and inflation rates present almost the same results as those of regime 1. Since the positive returns of the US dollar also mean its appreciation against the Vietnamese Dong (VND) or the depreciation of the Vietnamese Dong (VND) against the US dollar. These results also mean that the higher appreciation of the US dollar against the Vietnamese Dong in the previous month can lead to higher inflation rates in both high and low inflation regimes. It is also found that inflation rates of period t − 1 raise the appreciation of the USD. In other words, the US dollar completely hedges against inflation.

For the inflation hedge of the gold price, the results of Model 2 show that the influences of gold return in period t − 1 on inflation rates and inflation rates in period t − 1 on the gold price are positive and obvious in regime 1, but not significant in regime 2. Meanwhile, the higher inflation rates also lead to higher gold prices in the high return regime of gold. These results reveal that the hedging power of gold price on inflation is effective when inflation rates are high.

In both regimes, the US dollar significantly leads to inflation and vice versa. These bidirectional positive effects show the inflation hedge of the USD is strong and complete. Whereas, the hedging power of the gold price is not complete since it is only obvious in the high inflation regime. Furthermore, the effect of inflation is significant on the USD, disclosing the valid implementation of exchange controls over the US dollar. These findings are somewhat consistent with those of Ghosh et al. (2004), Wang et al. (2011), and Sui et al. (2021).

For testing the model validation, the residuals from the fitted models that provide information on their adequacy are applied and displayed in Figure 2. It is found that the dynamic MSI-VAR(1) models fitted for the US dollar and gold returns are adequate, as their residuals do not present autocorrelation.

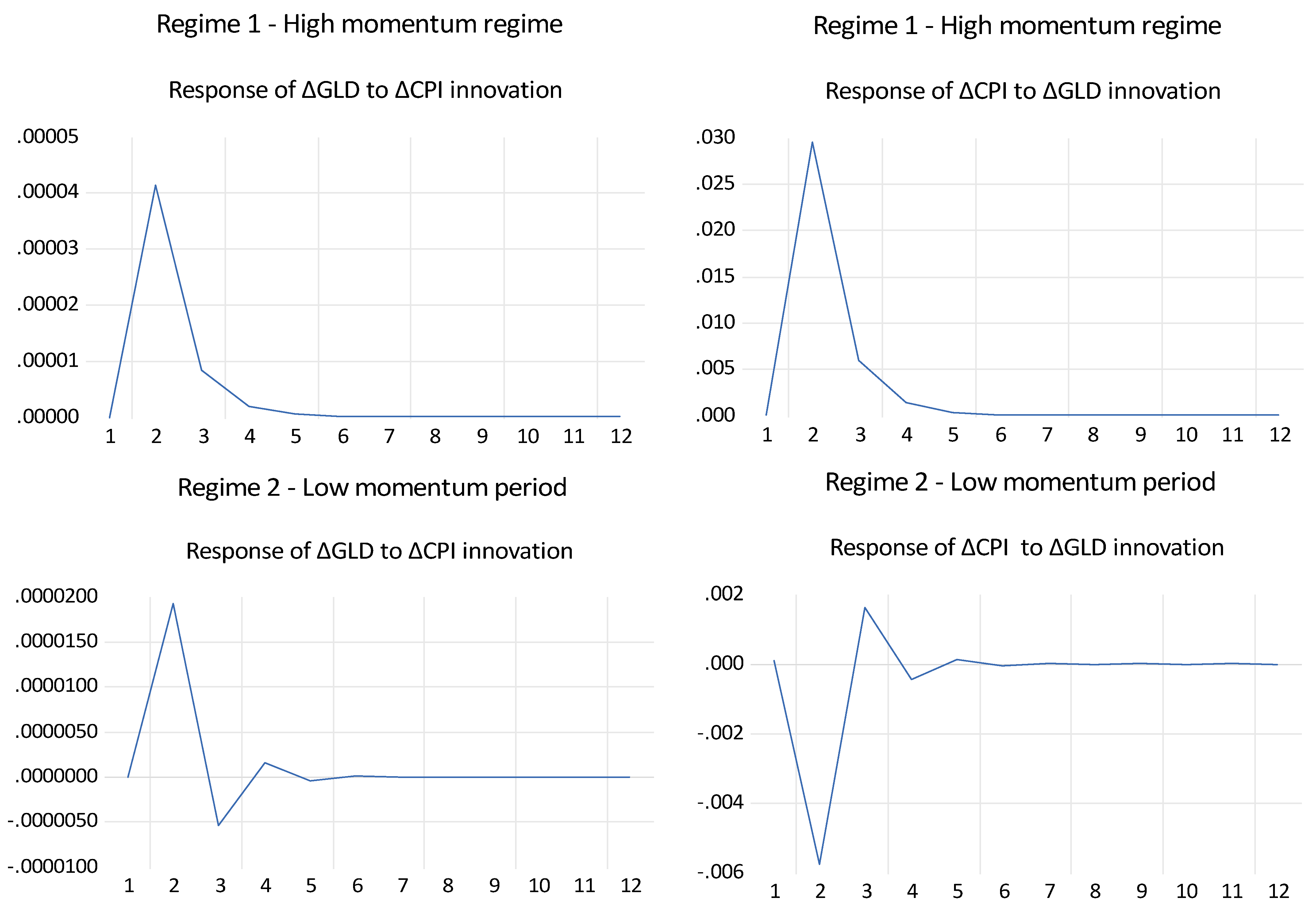

The impulse response analysis is applied to tracing the behaviors of variables to the sudden shocks from others on the current and future values of the endogenous variables. A shock to one variable simultaneously spreads and influences other endogenous variables through the lag of the VAR.

Figure 3 and Figure 4 offer evidences of the interferences between variables through the dynamic impulse response in the next 12 periods (1 year). This figure focuses on comparing the effects of the impulse response in different regimes. Regarding the impulse response of the USD, the effect directions are almost the same in both regimes, the reactions between the ∆CPI and ∆USD are quick and decisive in regime 1, then turn slower and longer in regime 2. The immediate response of the USD returns to inflation shock, and the response of inflation rates to the USD shock are all positive. The response of gold returns to the CPI shock are positive in regime 1, but it turns negative from period 3 to 4 in regime 2.

The response of inflation rates to gold shock changed from a negative to a positive value and then close to zero in regime 2. All the results show that the impact of the gold returns and the USD appreciation on inflation rates occurring in the first 4 periods, that is, the short-term effect is greater than the long-term, or inflation is sensitive to gold prices and the USD exchange.

The empirical results of this study prove the short-run as well as long-run inflation hedge of gold prices and the US dollar in Vietnam. Gold and the US dollar have been regarded as a “safe haven” of inflation by people for a long time Ghosh et al. (2004); McCown and Zimmerman (2006); Baur and Lucey (2010); Baur and McDermott (2010); Ali et al. (2021). This behavior is caused by the past galloping inflation, the weak monetary policy, and the traditional habitude of owning gold. Any signal of high inflation may cause a fast and decisive response of gold price and the US dollar price, and vice versa. Conforming to expectation, the rise of gold price and the US dollar is passed to inflation through commodity prices. When the US dollar appreciates, cost–push inflation may occur via the pass-through mechanism from exchange rates to domestic prices. The rise of gold price induces demand–pull inflation; hence, it has no impact on inflation rates in low inflation regimes. Inflation has been contained and growth has been high, particularly in Vietnam since the beginning of the reform. The economy mainly relies on the US dollar coming from foreign investment, trade, remittances from overseas Vietnamese, loans, and official development assistance (ODA). Consequently, Vietnam’s economy and its people are very sensitive to this currency. Along with the high rate of inflation and fragile economy, the US dollar and gold have played a very important role and worked as the inflation-leading indicators in Vietnam.

This study analyzes the inflation hedging power of the US dollar and gold price in Vietnam in both the long-run and short-run within the asymmetric framework. The Engle–Granger and TAR cointegration test are applied for long-run hedges and the dynamic MSI-VAR(1) model is used for short-run hedges. The findings of this study provide policymakers with a look inside the fragile economy of Vietnam, where the dollarization issue is severe, inflation is not stable, and people have less confidence in monetary policy. Investors are also provided a detailed insight into the importance of inflation uncertainty control via investment in gold and the US dollar, which could help investment managers, funds, and foundations to find the appropriate inflation hedge tools when investing in Vietnam or an economy similar to Vietnam.

4. Conclusions

Within the non-linear framework, this study aims to examine the inflation-predictive power of gold price and the US dollar in Vietnam with the asymmetric cointegration test and the dynamic MSI-VAR(1) model. The empirical results show that both the gold prices and the US dollar present an effective hedge against Vietnam’s inflation. The reasons explained for this ability are a fragile economy, unstable inflation rates, and people’s confidence in monetary policy. The policymakers may face a challenge of how to persuade people to believe in the effective monetary policy and to lessen the serious dollarization.

This study makes two contributions to the existing literature. First, this study contributes to knowledge of the inflation hedge of gold price and the US dollar against Vietnam’s inflation within the asymmetric framework. Second, the methodology allows for both regime shifts, providing a better predictive method than the time-varying linear model. Along with increasing prices, inflation heavily pressures Vietnam’s economy. The findings of this study hope to supply a valuable suggestion on valuation and determination on monetary strategy for policymakers and on inflation risk management, as well as the US dollar and gold investment for investors, consumers, and banks. From the academic perspective, the methodology employed has never been used before on the same topic and contributes some new findings to the existing literature.

This study is limited to gold and the USD, an extension in the future could be to examine the role of securities in hedging against inflation in the context of Vietnam. Ali et al. (2023) find diversification benefits among Asian equity markets in the COVID-19 era. For investors, capital gains or dividends (in the USD) may also be adjusted accordingly when the Vietnamese currency depreciates during the investment period. Thus, besides hedging inflation, it can also increase nominal returns.

Funding

This research received no external funding.

Informed Consent Statement

Not applicable.

Data Availability Statement

All datasets on which the conclusions of the manuscript rely are from the database of the International Monetary Fund (IMF) (https://data.imf.org/regular.aspx?key=61545850) accessed on 8 March 2023, and the world gold council (https://www.gold.org/goldhub/data/gold-prices) accessed on 8 March 2023.

Conflicts of Interest

The author declares no conflict of interest.

References

- Adrangi, Bahram, Arjun Chatrath, and Kambiz Raffiee. 2003. Economic activity, inflation, and hedging: The case of gold and silver investments. The Journal of Wealth Management 6: 60–77. [Google Scholar] [CrossRef]

- Ali, Fahad, Ahmet Sensoy, and John W. Goodell. 2023. Identifying diversifiers, hedges, and safe havens among Asia Pacific equity markets during COVID-19: New results for ongoing portfolio allocation. International Review of Economics & Finance 85: 744–92. [Google Scholar] [CrossRef]

- Ali, Fahad, Yuexiang Jiang, and Ahmet Sensoy. 2021. Downside risk in Dow Jones Islamic equity indices: Precious metals and portfolio diversification before and after the COVID-19 bear market. Research in International Business and Finance 58: 101502. [Google Scholar] [CrossRef]

- Baur, Dirk G., and Brian M. Lucey. 2010. Is gold a hedge or a safe haven? An analysis of stocks, bonds and gold. Financial Review 45: 217–29. [Google Scholar] [CrossRef]

- Baur, Dirk G., and Thomas K. McDermott. 2010. Is gold a safe haven? International evidence. Journal of Banking & Finance 34: 1886–98. [Google Scholar]

- Blose, Laurence E. 2010. Gold prices, cost of carry, and expected inflation. Journal of Economics and Business 62: 35–47. [Google Scholar] [CrossRef]

- Cecchetti, Stephen G., Rita S. Chu, and Charles Steindel. 2000. The unreliability of inflation indicators. Current Issues in Economics & Finance 6: 1–6. [Google Scholar]

- Christie-David, Rohan, Mukesh Chaudhry, and Timothy W. Koch. 2000. Do macroeconomics news releases affect gold and silver prices? Journal of Economics and Business 52: 405–21. [Google Scholar] [CrossRef]

- Chua, Jess, and Richard S. Woodward. 1982. Gold as an inflation hedge: A comparative study of six major industrial countries. Journal of Business Finance & Accounting 9: 191–97. [Google Scholar]

- Enders, Walter, and Pierre L. Siklos. 2001. Cointegration and threshold adjustment. Journal of Business & Economic Statistics 19: 166–76. [Google Scholar]

- Frühwirth-Schnatter, Sylvia. 2006. Finite Mixture and Markov Switching Models. New York: Springer, vol. 425. [Google Scholar]

- Garner, C. Alan. 1995. How useful are leading indicators of inflation? Economic Review 80: 5–18. [Google Scholar]

- Ghosh, Dipak, Eric J. Levin, Peter Macmillan, and Robert E. Wright. 2004. Gold as an inflation hedge? Studies in Economics and Finance 22: 1–25. [Google Scholar] [CrossRef] [Green Version]

- Hamilton, James D. 1989. A new approach to the economic analysis of nonstationary time series and the business cycle. Econometrica: Journal of the Econometric Society 57: 357–84. [Google Scholar] [CrossRef]

- Jaffe, Jeffrey F. 1989. Gold and gold stocks as investments for institutional portfolios. Financial Analysts Journal 45: 53–59. [Google Scholar]

- Kim, Ki-Ho. 1998. US inflation and the dollar exchange rate: A vector error correction model. Applied Economics 30: 613–19. [Google Scholar] [CrossRef]

- Krolzig, Hans-Martin. 2000. Predicting Markov-Switching Vector Autoregressive Processes. Oxford: Nuffield College, pp. 1–30. [Google Scholar]

- Kyrtsou, Catherine, and Walter C. Labys. 2006. Evidence for chaotic dependence between US inflation and commodity prices. Journal of Macroeconomics 28: 256–66. [Google Scholar] [CrossRef]

- Levin, Eric J., A. Montagnoli, and R. E. Wright. 2006. Short-Run and Long-Run Determinants of the Price of Gold. London: World Gold Council. [Google Scholar]

- MacKinnon, James. 1991. Critical Values for Cointegration Tests. In Long Run Economic Relationships. Edited by R. Engle and C. Granger. Oxford: Oxford University Press, pp. 267–76. [Google Scholar]

- MacKinnon, James G. 1996. Numerical distribution functions for unit root and cointegration tests. Journal of Applied Econometrics 11: 601–18. [Google Scholar] [CrossRef]

- McCown, James Ross, and John R. Zimmerman. 2006. Is gold a zero-beta asset? Analysis of the investment potential of precious metals. Analysis of the Investment Potential of Precious Metals. [Google Scholar] [CrossRef]

- Moore, Geoffrey H. 1990. Gold prices and a leading index of inflation. Challenge 33: 52. [Google Scholar] [CrossRef]

- Nasir, Muhammad Ali, Toan Luu Duc Huynh, and Xuan Vinh Vo. 2020. Exchange rate pass-through & management of inflation expectations in a small open inflation targeting economy. International Review of Economics & Finance 69: 178–88. [Google Scholar]

- Nelson, Charles R., and Charles R. Plosser. 1982. Trends and random walks in macroeconmic time series: Some evidence and implications. Journal of Monetary Economics 10: 139–62. [Google Scholar] [CrossRef]

- Papell, David H. 1994. Exchange rates and prices: An empirical analysis. International Economic Review 35: 397–410. [Google Scholar] [CrossRef]

- Peon, Sylvia Beatriz Guillermo, and Martín Alberto Rodríguez Brindis. 2014. Analyzing the exchange rate pass-through in Mexico: Evidence post inflation targeting implementation. Ensayos sobre Política Económica 32: 18–35. [Google Scholar] [CrossRef]

- Ranson, David, and H. C. Wainright. 2005. Why Gold, Not Oil, Is the Superior Predictor of Inflation. Gold Report. London: World Gold Council. [Google Scholar]

- Saha, Shrabani, and Zhaoyong Zhang. 2013. Do exchange rates affect consumer prices? A comparative analysis for Australia, China and India. Mathematics and Computers in Simulation 93: 128–38. [Google Scholar] [CrossRef]

- Salisu, Afees A., Umar B. Ndako, and Tirimisiyu F. Oloko. 2019. Assessing the inflation hedging of gold and palladium in OECD countries. Resources Policy 62: 357–77. [Google Scholar] [CrossRef]

- Sui, Meng, Erick W. Rengifo, and Eduardo Court. 2021. Gold, inflation and exchange rate in dollarized economies–A comparative study of Turkey, Peru and the United States. International Review of Economics & Finance 71: 82–99. [Google Scholar]

- Tkacz, Greg. 2007. Gold Prices and Inflation. No. 2007, 35. Ottawa: Bank of Canada Working Paper. [Google Scholar]

- Tully, Edel, and Brian M. Lucey. 2007. A power GARCH examination of the gold market. Research in International Business and Finance 21: 316–25. [Google Scholar] [CrossRef]

- Umar, Mohammed, and Jauhari Dahalan. 2016. An application of asymmetric Toda-Yamamoto causality on exchange rate-inflation differentials in emerging economies. International Journal of Economics and Financial Issues 6: 420–26. [Google Scholar]

- Uribe, Martin. 1997. Exchange-rate-based inflation stabilization: The initial real effects of credible plans. Journal of Monetary Economics 39: 197–221. [Google Scholar] [CrossRef] [Green Version]

- Van Hoang, Thi Hong, Amine Lahiani, and David Heller. 2016. Is gold a hedge against inflation? New evidence from a nonlinear ARDL approach. Economic Modelling 54: 54–66. [Google Scholar] [CrossRef] [PubMed]

- Wang, Kuan-Min, Yuan-Ming Lee, and Thanh-Binh Nguyen Thi. 2011. Time and place where gold acts as an inflation hedge: An application of long-run and short-run threshold model. Economic Modelling 28: 806–19. [Google Scholar] [CrossRef]

- Worthington, Andrew C., and Mosayeb Pahlavani. 2007. Gold investment as an inflationary hedge: Cointegration evidence with allowance for endogenous structural breaks. Applied Financial Economics Letters 3: 259–62. [Google Scholar] [CrossRef] [Green Version]

Figure 1.

The trend of consumer price index (CPI), the US dollar (USD), and gold price (GLD).

Figure 2.

The autocorrelations with approximate 2 standard error bounds of dynamic MSI-VAR(1) models for inflation hedge of USD and GLD.

Figure 2.

The autocorrelations with approximate 2 standard error bounds of dynamic MSI-VAR(1) models for inflation hedge of USD and GLD.

Figure 3.

The impulse response between and , illustrating the mechanisms through which shocks spread over time.

Figure 3.

The impulse response between and , illustrating the mechanisms through which shocks spread over time.

Figure 4.

The impulse response between and , illustrating the mechanisms through which shocks spread over time.

Figure 4.

The impulse response between and , illustrating the mechanisms through which shocks spread over time.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Descriptive statistics.

| CPI | USD | GLD | |

|---|---|---|---|

| Mean | 97.14 | 18,044.07 | 17,824,329 |

| Standard deviation | 45.20 | 3507.33 | 12,296,869 |

| Skewness | 0.24 | 0.04 | 0.25 |

| Kurtosis | 1.40 | 1.61 | 1.61 |

| J-B | 33.32 *** | 23.20 *** | 26.25 *** |

| LB(6) | 1672.1 *** | 1626.9 *** | 1608.2 *** |

| LB2(6) | 1600.3 *** | 1423.2 *** | 1126.4 *** |

Note: The entire sample period spans from January 1997 to December 2020. J-B is the statistic of Jarque–Bera normal distribution test. Ljung–Box test is used for testing for autocorrelation of variables. LB(6) is the Ljung–Box statistics of six-month lags. is the Ljung–Box statistics for squared residuals of six-month lags. *** indicates the 1% significant level.

Table 2.

Unit root tests.

| Variable | ADF | PP | ||

|---|---|---|---|---|

| Statistic Value | Lags | Statistic Value | Bandwidth | |

| Level | ||||

| Ln_CPI | −1.442 | [13] | −1.134 | [11] |

| Ln_USD | −2.798 | [0] | −2.792 | [6] |

| Ln_GOLD | −1.200 | [0] | −1.317 | [6] |

| First difference | ||||

| ΔLn_CPI | −3.461 ** | [12] | −9.834 *** | [9] |

| ΔLn_USD | −17.188 *** | [0] | −17.186 *** | [8] |

| ΔLn_GOLD | −14.852 *** | [0] | −14.783 *** | [3] |

Note: *** and **, respectively, indicate the 1% and 5% significant level. Both intercept and time trend are included in all test equations. The maximum lag employed is 15. The values in parentheses [.] are the adequate lag order of ADF test, which are determined by the minimum SIC. Bandwidths are those of the Newey–West correction of the PP test. Critical values of ADF and PP are referenced from MacKinnon (1991).

Table 3.

Engle–Granger test for linear cointegration.

| Variables | ADF Statistic Value | ||

|---|---|---|---|

| Ln_USD | 0.004 (7.808) *** | 0.289 (3.217) *** | −3.474 *** [12] |

| Ln_GOLD | 0.003 (5.939) *** | 0.213 (7.144) *** | −3.572 ** [12] |

Note: *** and ** indicates the 1% and 5% significant level, respectively. Long-run relation equation is . The maximum lag employed is 15. The values in parentheses [.] are the lag order. The optimal lag is determined based on AIC. The values in (.) are t statistics. (see MacKinnon 1996 for reference).

Table 4.

Test for asymmetric cointegration (TAR).

| SC | HQ | Lag | H0:ρi = 0 | H0:ρ1 = ρ2 = 0 | τ | H0:ρ1 = ρ2 | |

|---|---|---|---|---|---|---|---|

| t-Max | Φ | F | |||||

| Ln_CPI vs. Ln_USD | −4.14 ** | −4.19 ** | 1 | −3.938 *** | 28.405 *** | 0.0002 | 0.749 |

| Ln_CPI vs. Ln_GOLD | −0.92 ** | −0.97 ** | 1 | −3.8428 *** | 29.986 *** | −0.0176 | 4.121 *** |

Note: *** and ** show the 1% and 5% significant level. The maximum lag employed is 15; the optimal lag is selected by the minimum value of SC and HQ. The critical values of the t-Max and Φ tests are referenced to Enders and Siklos (2001).

Table 5.

The inflation hedge of USD and gold (dynamic MSI-VAR(1)).

| Variable | Model 1—Inflation Hedge of USD | Model 2—Inflation Hedge of Gold | ||

|---|---|---|---|---|

| Regime 1 (high momentum period) | ||||

| 0.005 | 0.060 | |||

| [0.156] | [1.322] | |||

| 0.001 *** | 0.002 *** | |||

| [3.876] | [4.153] | |||

| −0.004 | 0.558 *** | |||

| [−0.108] | [11.255] | |||

| Regime 2 (low momentum period) | ||||

| −1.136 *** | −0.443 *** | |||

| [−12.667] | [−3.278] | |||

| 0.050 *** | 0.008 *** | |||

| [25.292] | [2.635] | |||

| 0.524 *** | 0.419 * | |||

| [3.294] | [1.758] | |||

| Regime 1 (high momentum period) | ||||

| 0.334 *** | 0.021 * | |||

| [3.459] | [1.883] | |||

| 0.008 ** | 0.002 *** | |||

| [2.406] | [4.225] | |||

| 0.200 | 0.849 *** | |||

| [0.591] | [15.627] | |||

| Regime 2 (low momentum period) | ||||

| −0.278 * | −0.007 | |||

| [−1.901] | [−0.374] | |||

| 0.004 | 0.003 *** | |||

| [0.467] | [2.670] | |||

| −0.285 | −0.166 | |||

| [−0.487] | [−1.639] | |||

| 3.519 *** | 0.969 *** | |||

| 1.836 * | 1.285 | |||

| Log L | 2144.155 | 1615.871 | ||

Note: and represent the Markov transition probabilities. Log L is the value of maximum likelihood function. The values inside [.] are z-statistics. *, **, and *** represent 10%, 5%, and 1% significant level, respectively.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Thi Thanh Binh, N. How to Hedge against Inflation Risk in Vietnam. Economies 2023, 11, 94. https://doi.org/10.3390/economies11030094

AMA Style

Thi Thanh Binh N. How to Hedge against Inflation Risk in Vietnam. Economies. 2023; 11(3):94. https://doi.org/10.3390/economies11030094

Chicago/Turabian StyleThi Thanh Binh, Nguyen. 2023. "How to Hedge against Inflation Risk in Vietnam" Economies 11, no. 3: 94. https://doi.org/10.3390/economies11030094

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.