The Effect of Inflation Targeting (IT) Policy on the Inflation Uncertainty and Economic Growth in Selected African and European Countries

Abstract

:1. Introduction

2. Literature Review

2.1. The Theoretical Reasoning

2.2. The Recent Empirical Studies

3. Methodology and Data

3.1. Methodology

3.1.1. GARCH Model Approach

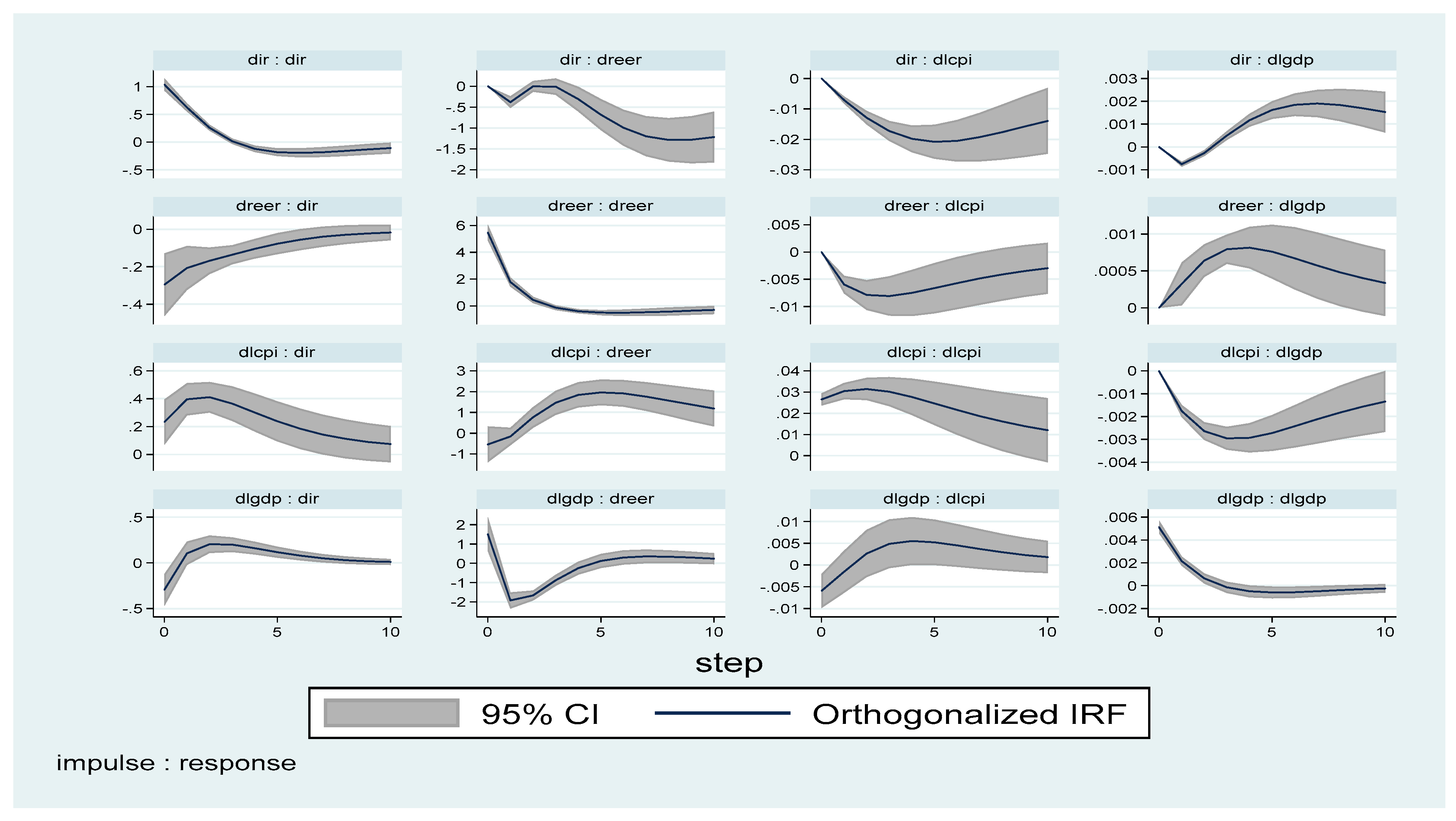

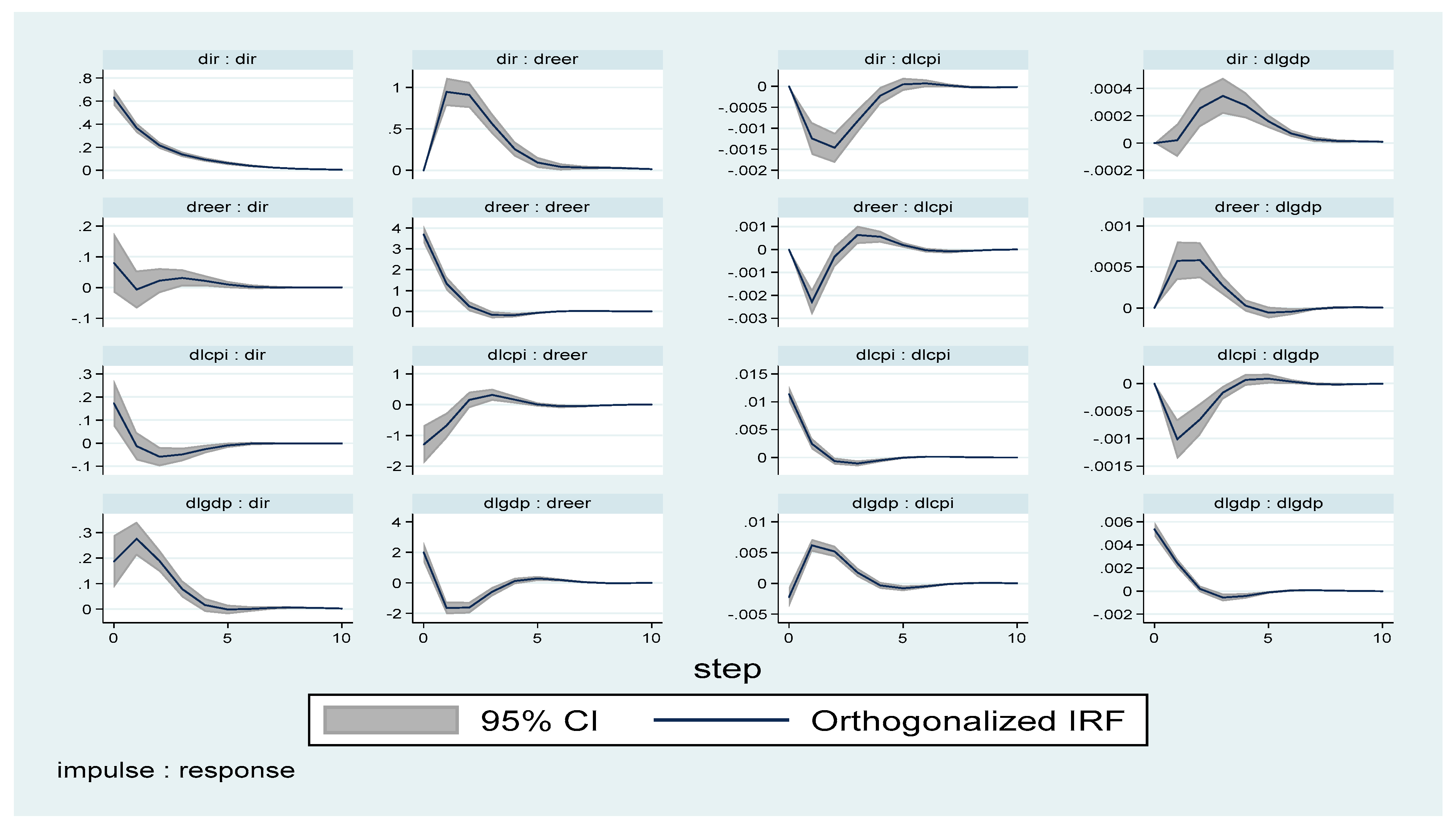

3.1.2. PVAR Model Approach

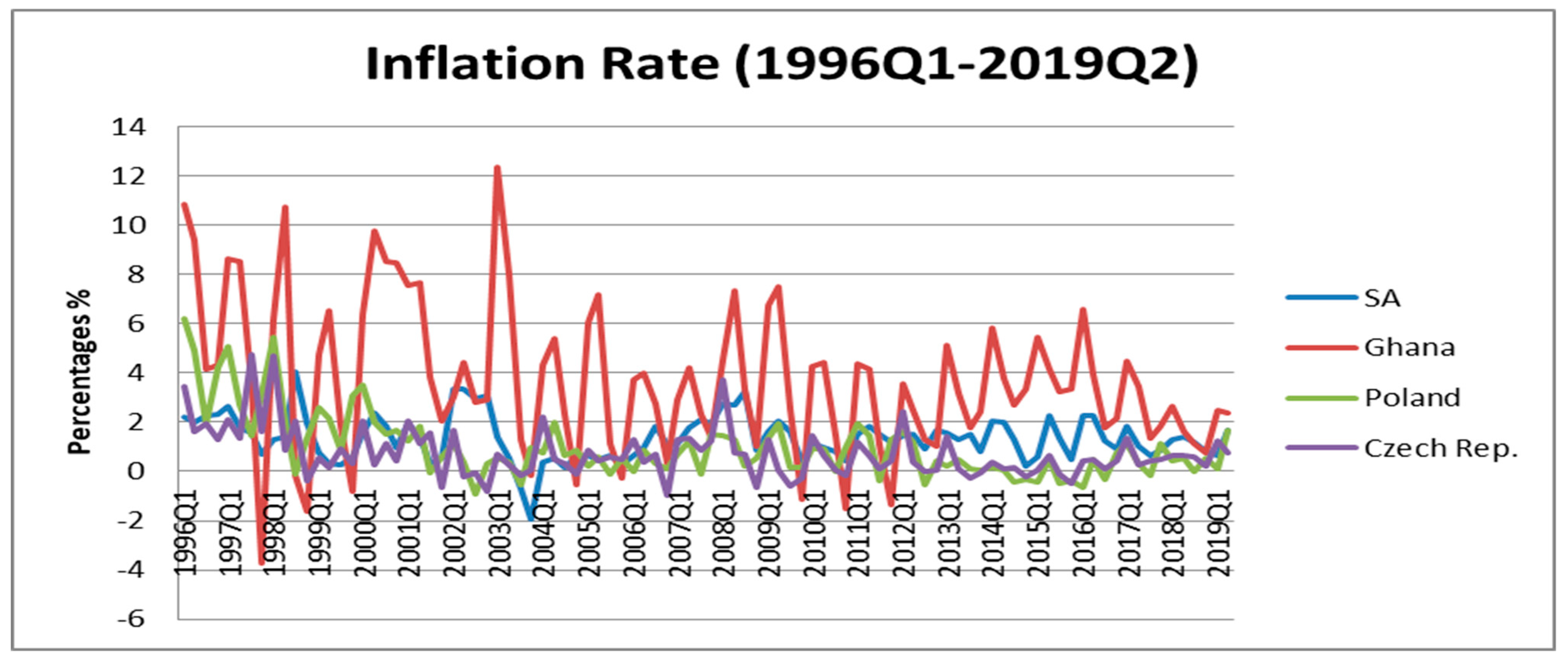

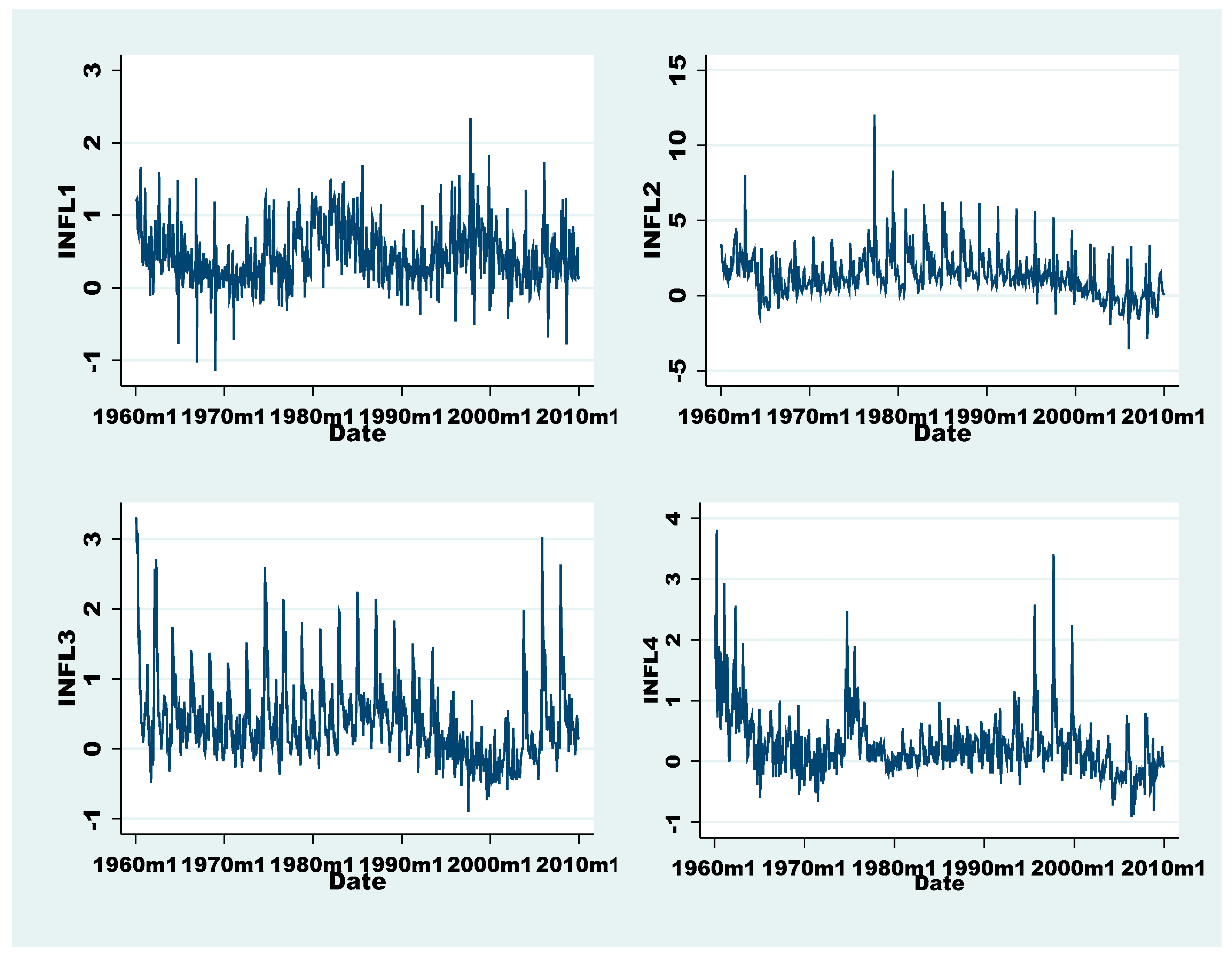

3.2. Sample and Data

4. Empirical Results and Discussion

4.1. Time Series Analysis

4.2. Panel Data Analysis

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Abango, Mohammed A., Hadrat Yusif, and Adam Issifu. 2019. Monetary aggregates targeting, inflation targeting and inflation stabilization in Ghana. African Development Review 31: 448–61. [Google Scholar] [CrossRef]

- Abo-Zaid, Salem, and Didem Tuzemen. 2012. Inflation Targeting: A three-decade perspective. Journal of Policy Modeling 34: 621–45. [Google Scholar] [CrossRef]

- Abrigo, Michael R. M., and Inessa Love. 2016. Estimation of panel vector autoregression in Stata. The Stata Journal 16: 778–804. [Google Scholar] [CrossRef] [Green Version]

- Agénor, Pierre-Richard, and Luiz Awazu Pereira da Silva. 2019. Integrated Inflation Targeting-Another Perspective from the Developing World. Manchester: Bank for International Settlements (BIS), University of Manchester. [Google Scholar]

- Antonakakis, Nikolaos, Christina Christou, Luis A. Gil-Alana, and Rangan Gupta. 2021. Inflation-targeting and inflation volatility: International evidence from the cosine-squared cepstrum. International Economics 167: 29–38. [Google Scholar] [CrossRef]

- Ardakani, Omid M., N. Kundan Kishor, and Suyong Song. 2018. Re-evaluating the effectiveness of inflation targeting. Journal of Economic Dynamics and Control 90: 76–97. [Google Scholar] [CrossRef]

- Bataa, Erdenebat, Denise R. Osborn, Marianne Sensier, and Dick van Dijk. 2013. Structural breaks in the international dynamics of inflation. Review of Economics and Statistics 95: 646–59. [Google Scholar] [CrossRef]

- Bernanke, Ben S., and Michael Woodford. 2004. Introduction to “The Inflation-Targeting Debate”. In The Inflation-Targeting Debate. Chicago: University of Chicago Press, pp. 1–10. [Google Scholar]

- Bleaney, Michael, Atsuyoshi Morozumi, and Zakari Mumuni. 2020. Inflation targeting and monetary policy in Ghana. Journal of African Economies 29: 121–45. [Google Scholar] [CrossRef]

- Bollerslev, Tim. 1986. Generalized autoregressive conditional heteroskedasticity. Journal of econometrics 31: 307–27. [Google Scholar] [CrossRef] [Green Version]

- Bratsiotis, George J., Jakob Madsen, and Christopher Martin. 2015. Inflation targeting and inflation persistence. Economic and Political Studies 3: 3–17. [Google Scholar] [CrossRef] [Green Version]

- Breitung, Jörg, and Samarjit Das. 2005. Panel unit root tests under cross-sectional dependence. Statistica Neerlandica 59: 414–33. [Google Scholar] [CrossRef]

- Brito, Ricardo D., and Brianne Bystedt. 2010. Inflation targeting in emerging economies: Panel evidence. Journal of Development Economics 91: 198–210. [Google Scholar] [CrossRef]

- Broto, Carmen. 2008. Inflation Targeting in Latin America: Empirical Analysis Using Garch Models. Economic Modelling 28: 1424–34. [Google Scholar] [CrossRef] [Green Version]

- Ciżkowicz, Piotr, and Andrzej Rzońca. 2015. Inflation targeting and its discontents: The case of Poland. Acta Oeconomica 65: 107–22. [Google Scholar] [CrossRef] [Green Version]

- Comert, Hasan, and Gerald Epstein. 2011. Inflation targeting in South Africa: Friend or foe of development? Economic History of Developing Regions 26: S94–S113. [Google Scholar] [CrossRef]

- Cukierman, Alex, and Allan H. Meltzer. 1986. A theory of ambiguity, credibility, and inflation under discretion and asymmetric information. Econometrica: Journal of the Econometric Society 54: 1099–128. [Google Scholar] [CrossRef] [Green Version]

- Daboussi, Olfa Manai. 2014. Economic performance and inflation targeting in developing economies. Journal of World Economic Research 3: 1–7. [Google Scholar] [CrossRef] [Green Version]

- e Souza, Gustavo José de Guimarães, Helder Ferreira de Mendonça, and Joaquim Pinto de Andrade. 2016. Inflation targeting on output growth: A pulse dummy analysis of dynamic macroeconomic panel data. Economic Systems 40: 145–69. [Google Scholar] [CrossRef]

- Engle, Robert. 2001. GARCH 101: The use of ARCH/GARCH models in applied econometrics. Journal of Economic Perspectives 15: 157–68. [Google Scholar] [CrossRef] [Green Version]

- Erdem, Havvanur Feyza, and Rahmi Yamak. 2016. Measuring the optimal macroeconomic uncertainty index for Turkey. Economic Annals 61: 7–22. [Google Scholar] [CrossRef]

- Ewurum, Ngozi C., Chris U. Kalu, and Damian J. Nwankwo. 2017. Inflation Targeting and Economic Growth Nexus in Nigeria: Implications for Monetary Policy. International Journal of Academic Research in Business and Social Sciences 7: 12–27. [Google Scholar]

- Fosu, Nana Kwame. 2015. Inflation Targeting: The Ghanaian Experience. Ph.D. dissertation, University of Ghana, Accra, Ghana. [Google Scholar]

- Fouejieu, Armand. 2013. Coping with the recent financial crisis: Did inflation targeting makes any difference. International Economics 133: 72–92. [Google Scholar] [CrossRef] [Green Version]

- Frees, Edward W. 1995. Assessing cross-sectional correlation in panel data. Journal of Econometrics 69: 393–414. [Google Scholar] [CrossRef]

- Friedman, Milton. 1937. The use of ranks to avoid the assumption of normality implicit in the analysis of variance. Journal of the American Statistical Association 32: 675–701. [Google Scholar] [CrossRef]

- Friedman, Milton. 1977. Nobel lecture: Inflation and unemployment. Journal of Political Economy 85: 451–72. [Google Scholar] [CrossRef]

- Fromlet, Pia. 2010. Do Inflation Targeting Central Banks Focus on Inflation—An Analysis for Ten Countries? Uppsala: Department of Economics, Uppsala University. [Google Scholar]

- Gurgul, Henryk, Paweł Majdosz, and Roland Mestel. 2007. Price–volume relations of DAX companies. Financial Markets and Portfolio Management 21: 353–79. [Google Scholar] [CrossRef]

- Gylfason, Thorvaldur, and Tryggvi Thor Herbertsson. 2001. Does inflation matter for growth? Japan and the World Economy 13: 405–28. [Google Scholar] [CrossRef]

- Hammond, Gill. 2012. State of the Art of Inflation Targeting. In Handbook No. 29, Centre for Central Banking Studies. London: Bank of England. [Google Scholar]

- Harris, Richard D. F., and Elias Tzavalis. 1999. Inference for unit roots in dynamic panels where the time dimension is fixed. Journal of Econometrics 91: 201–26. [Google Scholar] [CrossRef]

- Hartmann, Matthias, and Jan Roestel. 2013. Inflation, output and uncertainty in the era of inflation targeting—A multi-economy view on causal linkages. Journal of International Money and Finance 37: 98–112. [Google Scholar] [CrossRef]

- Heintz, James, and Léonce Ndikumana. 2011. Is there a case for formal inflation targeting in sub-Saharan Africa? Journal of African Economies 20: ii67–ii103. [Google Scholar] [CrossRef] [Green Version]

- Högenauer, Anna-Lena, and David Howarth. 2016. Unconventional monetary policies and the European Central Bank’s problematic democratic legitimacy. Zeitschrift für Öffentliches Recht 71: 1–24. [Google Scholar]

- Holland, A. Steven. 1995. Inflation and uncertainty: Tests for temporal ordering. Journal of Money, Credit and Banking 27: 827–37. [Google Scholar] [CrossRef]

- Horská, Helena. 2001. Inflation targeting in Poland-A comparison with the Czech Republic. Institute of World Economic 3: 237–54. [Google Scholar] [CrossRef] [Green Version]

- Im, Kyung So, M. Hashem Pesaran, and Yongcheol Shin. 2003. Testing for unit roots in heterogeneous panels. Journal of Econometrics 115: 53–74. [Google Scholar] [CrossRef]

- Jahan, Sarwat. 2012. Inflation targeting: Holding the line. Finance & Development 4: 72–73. [Google Scholar]

- Karahan, Özcan. 2012. The relationship between inflation and inflation uncertainty: Evidence from the Turkish economy. Procedia Economics and Finance 1: 219–28. [Google Scholar] [CrossRef] [Green Version]

- Kaseeram, Irrshad, and Eleftherios Contogiannis. 2011. The impact of inflation targeting on inflation volatility in South Africa. African Finance Journal 13: 34–52. [Google Scholar]

- Kontonikas, Alexandros. 2004. Inflation and inflation uncertainty in the United Kingdom, evidence from GARCH modelling. Economic Modelling 21: 525–43. [Google Scholar] [CrossRef] [Green Version]

- Kovanen, Arto. 2011. Does Money Matter for Inflation in Ghana? IMF Working Papers, Stage of Publication. pp. 1–23. Available online: http://www.imf.org/external/pubs/ft/wp/2011/wp11274.pdf (accessed on 23 August 2021).

- Krušec, Dejan. 2011. Is inflation targeting effective? Monetary transmission in Poland, the Czech Republic, Slovakia, and Hungary. Eastern European Economics 49: 52–71. [Google Scholar] [CrossRef]

- Kumo, Wolassa Lawisso. 2015. 216-Inflation Targeting Monetary Policy, Inflation Volatility and Economic Growth in South Africa. In African Development Bank Group, WP 216. Abidjan: African Development Bank, Available online: https://www.afdb.org/en/documents/document/working-paper-216-inflation-targeting-monetary-policy-inflation-volatility-and-economic-growth-in-south-africa-51137 (accessed on 23 August 2021).

- Lee, Wang-Sheng. 2011. Comparative case studies of the effects of inflation targeting in emerging economies. Oxford Economic Papers 63: 375–97. [Google Scholar] [CrossRef]

- Mavikela, Nomahlubi, Simba Mhaka, and Andrew Phiri. 2019. The inflation-growth relationship in SSA inflation-targeting countries. Studia Universitatis Babes-Bolyai Oeconomica 64: 84–102. [Google Scholar] [CrossRef] [Green Version]

- Meerza, Syed Imran Ali. 2020. Do Preconditions of Inflation Targeting Framework Matter? International Journal of Economics and Finance 12: 1–51. [Google Scholar] [CrossRef]

- Miles, William. 2008. Inflation targeting and monetary policy in Canada: What is the impact on inflation uncertainty? The North American Journal of Economics and Finance 19: 235–48. [Google Scholar] [CrossRef]

- Mishkin, Frederic S. 2000. Inflation targeting in emerging-market countries. American Economic Review 90: 105–9. [Google Scholar] [CrossRef] [Green Version]

- Mohammed, Alhassan, Yusif Hadrat, and Buabeng Emmanuel. 2016. Inflation targeting and economic growth in Ghana: An empirical investigation. Ghanaian Journal of Economics 4: 158–77. [Google Scholar]

- Mollick, André Varella, René Cabral, and Francisco G. Carneiro. 2011. Does inflation targeting matter for output growth? Evidence from industrial and emerging economies. Journal of Policy Modeling 33: 537–51. [Google Scholar] [CrossRef] [Green Version]

- Nasr, Adnen Ben, Mehmet Balcilar, Ahdi N. Ajmi, Goodness C. Aye, Rangan Gupta, and Renee Van Eyden. 2015. Causality between inflation and inflation uncertainty in South Africa: Evidence from a Markov-switching vector autoregressive model. Emerging Markets Review 24: 46–68. [Google Scholar] [CrossRef] [Green Version]

- Nelson, Daniel B., and Charles Q. Cao. 1991. Inequality constraints in the univariate GARCH model. Journal of Business & Economic Statistics 10: 229–35. [Google Scholar]

- Okun, Arthur M. 1971. The mirage of steady inflation. Brookings Papers on Economic Activity 1971: 485–98. [Google Scholar] [CrossRef] [Green Version]

- Pesaran, M. Hashem. 2004. General Diagnostic Tests for Cross-Sectional Dependence in Panels. Cambridge Working Papers in Economics No. 0435. Cambridge: The University of Cambridge, Faculty of Economics. [Google Scholar]

- Petreski, Marjan. 2014. Inflation targeting at the crossroads: Evidence from post-communist economies during the crisis. Communist and Post-Communist Studies 47: 247–60. [Google Scholar] [CrossRef] [Green Version]

- Phiri, Andrew. 2016. Inflation persistence in African countries: Does inflation targeting matter? Economics and Business Letters 5: 65–71. [Google Scholar] [CrossRef] [Green Version]

- Pourgerami, Abbas, and Keith E. Maskus. 1987. The effects of inflation on the predictability of price changes in Latin America: Some estimates and policy implications. World Development 15: 287–90. [Google Scholar] [CrossRef]

- Puni, Albert, Bright Addiyiah Osei, and Charles Barnor. 2014. Effects of inflation targeting policy on inflation rates and gross domestic product in Ghana. European Journal of Business and Management 6: 54–60. [Google Scholar]

- Sarel, Michael. 1996. Nonlinear effects of inflation on economic growth. Staff Papers 43: 199–215. [Google Scholar] [CrossRef]

- Sudacevschi, Mihaela. 2011. Pros and Cons of Inflation Targeting Strategy. LESIJ-Lex ET Scientia International Journal 18: 228–35. [Google Scholar]

- Svensson, Lars E. 1997. Inflation forecast targeting: Implementing and monitoring inflation targets. European Economic Review 41: 1111–46. [Google Scholar] [CrossRef] [Green Version]

- Tas, Bedri Kamil Onur, and Hasan Murat Ertugrul. 2013. Effect of inflation targeting on inflation uncertainty: A SWARCH analysis. Australian Economic Review 46: 444–59. [Google Scholar] [CrossRef]

- Taş, Bedri Kamil Onur. 2012. Inflation targeting and inflation uncertainty. Scottish Journal of Political Economy 59: 283–97. [Google Scholar] [CrossRef]

- Thornton, John. 2016. Inflation targeting in developing countries revisited. Finance Research Letters 16: 145–53. [Google Scholar] [CrossRef]

- Ungar, Meyer, and Ben-Zion Zilberfarb. 1993. Inflation and its Unpredictability—Theory and Empirical Evidence. Journal of Money, Credit and Banking 25: 709–20. [Google Scholar] [CrossRef]

- Valera, Harold Glenn A., Mark J. Holmes, and Gazi M. Hassan. 2018. Is inflation targeting credible in Asia? A panel GARCH approach. Empirical Economics 54: 523–46. [Google Scholar] [CrossRef]

- Van der Merwe, Ernie J. 2004. Inflation Targeting in South Africa. Pretoria: South African Reserve Bank. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Mean | Maximum | Minimum | Std. Dev. | Skewness | Kurtosis | JarqueBera | |

|---|---|---|---|---|---|---|---|

| INFL1 | 0.448632 | 2.342500 | −1.141900 | 0.445759 | 0.511178 | 4.378752 | 36.82708 (0.000) |

| INFL2 | 1.325063 | 12.04190 | −3.562100 | 1.514075 | 1.614334 | 11.55562 | 1045.286 (0.000) |

| INFL3 | 0.369033 | 3.300600 | −0.905000 | 0.610142 | 1.671739 | 7.386712 | 380.2761 (0.000) |

| INFL4 | 0.261860 | 3.808500 | −0.914400 | 0.554250 | 2.502988 | 13.67983 | 1738.982 (0.000) |

| Variable | Test | t-Test | t-Critical | Probability | Conclusion |

|---|---|---|---|---|---|

| INFL1 | ADF | −10.546 | −3.456 | 0.000 | Stationary |

| PP | −11.015 | −3.456 | 0.000 | ||

| INFL2 | ADF | −3.325 | −3.137 | 0.064 | Stationary |

| PP | −10.028 | −3.994 | 0.000 | ||

| INFL3 | ADF | −3.165 | −2.573 | 0.001 | Stationary |

| PP | −10.840 | −3.989 | 0.000 | ||

| INFL4 | ADF | −2.208 | −1.941 | 0.026 | Stationary |

| PP | −15.480 | −3.989 | 0.000 |

| Series | Q Test | LM Test |

|---|---|---|

| INFL1 | 0.2271 (0.634) | 5.314 (0.021) |

| INFL2 | 0.0177 (0.894) | 2.814 (0.093) |

| INFL3 | 0.3991 (0.528) | 34.961 (0.000) |

| INFL4 | 0.0002 (0.988) | 51.504 (0.000) |

| Country | ω | φ | α | γ |

|---|---|---|---|---|

| SA | −1.436828 ** (0.575) | 0.389435 (0.271) | 0.346622 ** (0.160) | 0.203411 ** (0.101) |

| Ghana | 0.249890 ** (0.126) | −0.282387 ** (0.143) | −0.079897 (0.165) | 0.489211 *** (0.110) |

| Poland | −0.058818 (0.044) | 0.982473 *** (0.009) | 0.019758 (0.062) | 0.016898 (0.030) |

| Czech Republic | −0.061598 * (0.035) | 0.814978 *** (0.016) | −0.298529*** (0.045) | 0.227784 *** (0.029) |

| Country | ω | φ | A | γ | σ |

|---|---|---|---|---|---|

| SA | −1.099797 ** (0.543) | 0.457902 * (0.255) | 0.347605 ** (0.164) | 0.194090 * (0.100) | −0.220864 (0.314) |

| Ghana | 0.645499 *** (0.236) | −0.454001 ** (0.181) | 0.008861 (0.162) | 0.370439 *** (0.122) | −0.748814 ** (0.346) |

| Poland | 0.027414 (0.035) | 0.937796 *** (0.016) | −0.103707 * (0.056) | 0.070724 ** (0.031) | −0.087539 *** (0.030) |

| Czech Republic | −1.483072 *** (0.297) | −1.020159 *** (0.003) | 0.007889 (0.023) | 0.087078 *** (0.015) | −2.301536 *** (0.283) |

| Tests of Cross-Sectional Independence | Pedroni Test for Cointegration | ||||

|---|---|---|---|---|---|

| Pesaran’s test | 6.579 | Pr = 0.0000 | Modified Phillips-Perron t | 2.9851 | Pr = 0.0014 |

| Friedman’s test | 151.067 | Pr = 0.0000 | Phillips-Perron t | 3.5331 | Pr = 0.0002 |

| Frees’ test | 0.608 | Pr = 0.0000 | Augmented Dickey-Fuller t | 4.3515 | Pr = 0.0000 |

| Im-Pesaran-Shin | Harris-Tzavalis | Breitung | ||

|---|---|---|---|---|

| LGDP | Levels Integration | |||

| LCPI | Levels Integration | |||

| REER | Levels Integration | |||

| IR | Levels Integration |

| AC | EC | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Coef. | Std. Err. | z | p > |z| | Coef. | Std. Err. | z | p > |z| | ||

| Dlgdp | dlgdp L1. | 0.3022894 | 0.0153366 | 19.71 | 0.000 | 0.3634332 | 0.0185804 | 19.56 | 0.000 |

| dlcpi L1. | −0.0594773 | 0.0032704 | −18.19 | 0.000 | −0.0717497 | 0.012326 | −5.82 | 0.000 | |

| dreer L1. | 0.0000195 | 0.0000223 | 0.87 | 0.383 | 0.0001552 | 0.0000305 | 5.09 | 0.000 | |

| dir L1. | −0.0007312 | 0.0000386 | −18.95 | 0.000 | 0.0000336 | 0.0000972 | 0.35 | 0.730 | |

| dum | 0.0019671 | 0.0002347 | 8.38 | 0.000 | 0.0184201 | 0.0050223 | 3.67 | 0.000 | |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Nene, S.T.; Ilesanmi, K.D.; Sekome, M. The Effect of Inflation Targeting (IT) Policy on the Inflation Uncertainty and Economic Growth in Selected African and European Countries. Economies 2022, 10, 37. https://doi.org/10.3390/economies10020037

Nene ST, Ilesanmi KD, Sekome M. The Effect of Inflation Targeting (IT) Policy on the Inflation Uncertainty and Economic Growth in Selected African and European Countries. Economies. 2022; 10(2):37. https://doi.org/10.3390/economies10020037

Chicago/Turabian StyleNene, Shelter Thelile, Kehinde Damilola Ilesanmi, and Mashapa Sekome. 2022. "The Effect of Inflation Targeting (IT) Policy on the Inflation Uncertainty and Economic Growth in Selected African and European Countries" Economies 10, no. 2: 37. https://doi.org/10.3390/economies10020037