Analysing Monetary Policy Shocks by Sign and Parametric Restrictions: The Evidence from Russia

Abstract

:1. Introduction

2. Literature Review

3. Data and Methodology

3.1. Data

3.2. The Concept of SVARs

3.3. Sign Restricted SVARS for Open Economy

4. Empirical Analysis

4.1. Preliminary Tests

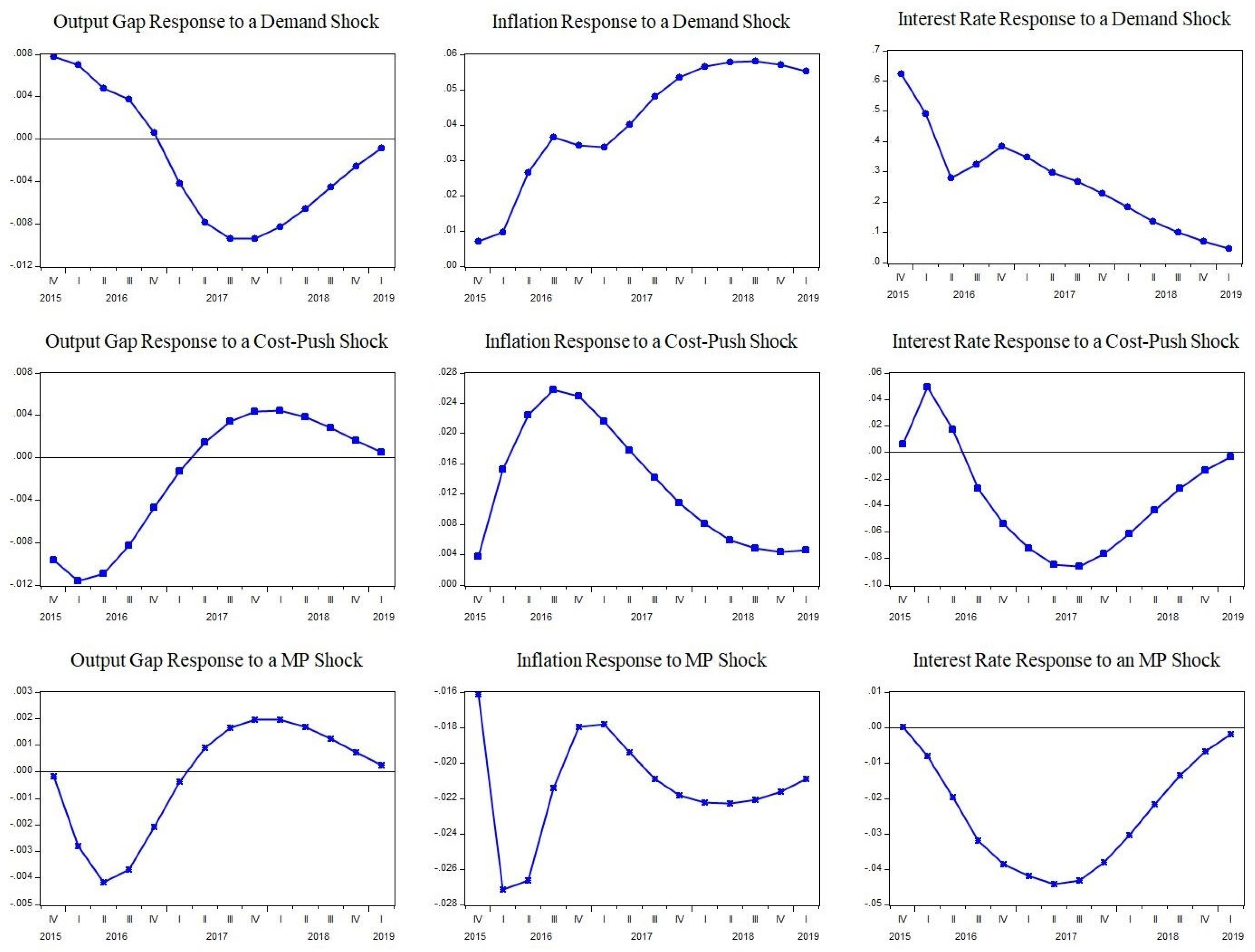

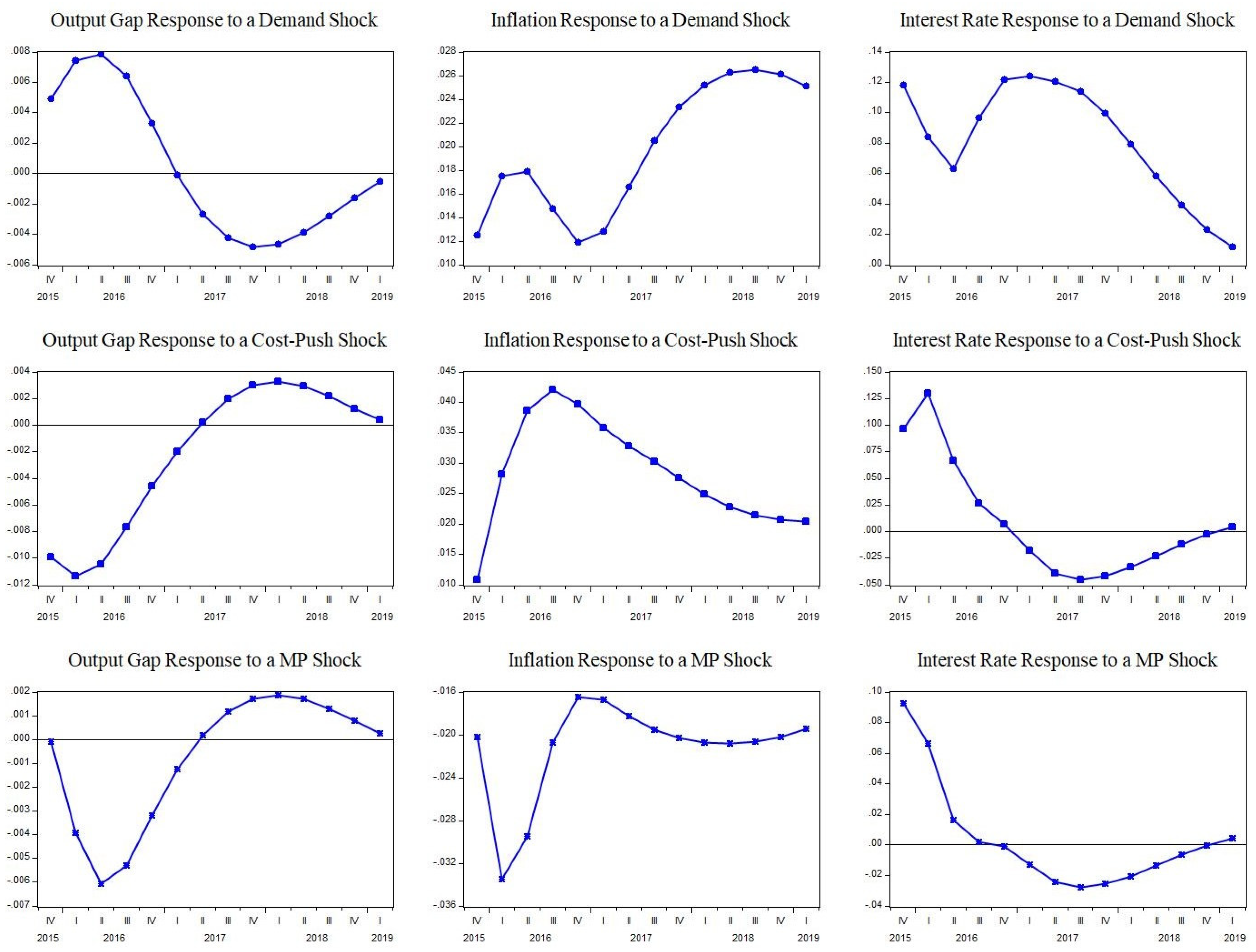

4.2. Variance Decomposition and Median Responses

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Acknowledgments

Conflicts of Interest

References

- Balke, Nathan S., and Kenneth M. Emery. 1994. Understanding the price puzzle. Federal Reserve Bank of Dallas Economic Review, Fourth Quarter, 15–26. [Google Scholar]

- Baumeister, Christiane, and Luca Benati. 2012. Unconventional Monetary Policy and the Great Recession: Estimating the Macroeconomic Effects of a Spread Compression at the Zero Lower Bound (No. 2012-21). Bank of Canada Working Paper. Street Ottawa: Bank of Canada. [Google Scholar]

- Benati, Luca. 2015. The long-run Phillips curve: A structural VAR investigation. Journal of Monetary Economics 76: 15–28. [Google Scholar] [CrossRef]

- Bernanke, Ben S., and Ilian Mihov. 1998. Measuring monetary policy. The Quarterly Journal of Economics 113: 869–902. [Google Scholar] [CrossRef]

- Berument, Hakan. 2007. Measuring monetary policy for a small open economy: Turkey. Journal of Macroeconomics 29: 411–30. [Google Scholar] [CrossRef]

- Bhattarai, Keshab. 2016. Unemployment–inflation trade-offs in OECD countries. Economic Modelling 58: 93–103. [Google Scholar] [CrossRef]

- Bjørnland, Hilde C., and Jørn I. Halvorsen. 2014. How does monetary policy respond to exchange rate movements? New international evidence. Oxford Bulletin of Economics and Statistics 76: 208–32. [Google Scholar] [CrossRef]

- Canova, Fabio, and Gianni De Nicolo. 2002. Monetary disturbances matter for business fluctuations in the G-7. Journal of Monetary Economics 49: 1131–59. [Google Scholar] [CrossRef]

- Carrillo, Julio A., and Rocio Elizondo. 2015. How Robust Are SVARs at Measuring Monetary Policy in Small Open Economies? (No. 2015-18). Working Paper. Ciudad de México: Banco de México. [Google Scholar]

- Castelnuovo, Efrem. 2012. Testing the structural interpretation of the Price Puzzle with a cost-channel model. Oxford Bulletin of Economics and Statistics 74: 425–52. [Google Scholar] [CrossRef]

- Cecchetti, Stephen G. 1996. Practical issues in monetary policy targeting. Economic Review-Federal Reserve Bank of Cleveland 32: 2–15. [Google Scholar]

- Cekin, Semih Emre, Menelik S. Geremew, and Hardik Marfatia. 2019. Monetary policy co-movement and spillover of shocks among BRICS economies. Applied Economics Letters 26: 1253–63. [Google Scholar] [CrossRef]

- Christiano, Lawrence, and Martin S. Eichenbaum. 1992. Liquidity Effects and the Monetary Transmission Mechanism. No. w3974. Cambridge: National Bureau of Economic Research. [Google Scholar]

- Christiano, Lawrence J., Martin Eichenbaum, and Charles L. Evans. 1999. Monetary policy shocks: What have we learned and to what end? Handbook of Macroeconomics 1: 65–148. [Google Scholar]

- Cho, Seonghoon, and Antonio Moreno. 2002. A Structural Estimation and Interpretation of the New Keynesian Macro Model. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=322600 (accessed on 15 May 2022).

- Cho, Seonghoon, and Antonio Moreno. 2006. A small-sample study of the New-Keynesian macro model. Journal of Money, Credit, and Banking 38: 1461–81. [Google Scholar] [CrossRef]

- Clarida, Richard, Jordi Gali, and Mark Gertler. 2000. Monetary policy rules and macroeconomic stability: Evidence and some theory. The Quarterly Journal of Economics 115: 147–80. [Google Scholar] [CrossRef] [Green Version]

- Cushman, David O., and Tao Zha. 1997. Identifying monetary policy in a small open economy under flexible exchange rates. Journal of Monetary Economics 39: 433–48. [Google Scholar] [CrossRef]

- Davies, Neville, and Paul Newbold. 1979. Some power studies of a portmanteau test of time series model specification. Biometrika 66: 153–55. [Google Scholar] [CrossRef]

- Faust, Jon. 1998. The robustness of identified VAR conclusions about money. In Carnegie-Rochester Conference Series on Public Policy. Holland: Elsevier, vol. 49, pp. 207–44. [Google Scholar]

- Fal’tsman, V. K. 2016. Problems of structural, investment, and innovation policy in the crisis period. Studies on Russian Economic Development 27: 367–73. [Google Scholar] [CrossRef]

- Farmer, Roger E. A., and Giovanni Nicolò. 2019. Some International Evidence for Keynesian Economics without the Phillips Curve. No. w25743. Cambridge: National Bureau of Economic Research. [Google Scholar]

- Fisher, Lance A., and Hyeon-seung Huh. 2016. Monetary policy and exchange rates: Further evidence using a new method for implementing sign restrictions. Journal of Macroeconomics 49: 177–91. [Google Scholar] [CrossRef]

- Fisher, Lance A., and Hyeon-seung Huh. 2019. An IV framework for combining sign and long-run parametric restrictions in SVARs. Journal of Macroeconomics 61: 103–25. [Google Scholar] [CrossRef]

- Freixas, Xavier, and José Jorge. 2008. The role of interbank markets in monetary policy: A model with rationing. Journal of Money, Credit and Banking 40: 1151–76. [Google Scholar] [CrossRef]

- Fry, Renee, and Adrian Pagan. 2011. Sign restrictions in structural vector autoregressions: A critical review. Journal of Economic Literature 49: 938–60. [Google Scholar] [CrossRef]

- Gan, Wee Beng, and Lee Ying Soon. 2003. Characterizing the monetary transmission mechanism in a small open economy: The case of Malaysia. The Singapore Economic Review 48: 113–34. [Google Scholar] [CrossRef]

- Gerlach, Stefan, and Frank Smets. 1995. The Monetary Transmission Mechanism: Evidence from the G-7 Countries (No. 1219). CEPR Discussion Papers. Washington, DC: CEPR. [Google Scholar]

- Grilli, Vittorio, and Nouriel Roubini. 1995. Liquidity and Exchange Rates: Puzzling Evidence from the G-7 Countries. Working Papers 95-17. New York: New York University, Leonard N. Stern School of Business, Department of Economics. [Google Scholar]

- Guo, Xu, Xuejun Jiang, and Wing-Keung Wong. 2017. Stochastic Dominance and Omega Ratio: Measures to Examine Market Efficiency, Arbitrage Opportunity, and Anomaly. Economies 5: 38. [Google Scholar] [CrossRef]

- Haberis, Alex, and Andrej Sokol. 2014. A Procedure for Combining Zero and Sign Restrictions in aVAR-Identification Scheme. London: London School of Economics and Political Science, LSE Library. [Google Scholar]

- Hetzel, Robert L. 2007. Rules vs. Discretion: Lessons from the Volcker-Greenspan Era. St. Louis: Federal Reserve Bank of Richmond. [Google Scholar]

- Ho, Tai-kuang, and Kuo-chun Yeh. 2010. Measuring monetary policy in a small open economy with managed exchange rates: The case of Taiwan. Southern Economic Journal 76: 811–26. [Google Scholar] [CrossRef]

- Ilyashenko, V., and L. Kuklina. 2017. Inflation in modern Russia: Theoretical foundations, specific features of manifestation and regional dimension. Economy of Region 1: 434–45. [Google Scholar] [CrossRef]

- Inoue, Atsushi, and Lutz Kilian. 2013. Inference on impulse response functions in structural VAR models. Journal of Econometrics 177: 1–13. [Google Scholar] [CrossRef]

- Ivanova, M. A. 2016. Analysis of the nature of cause-and-effect relationship between inflation and wage in Russia. Studies on Russian Economic Development 27: 575–84. [Google Scholar] [CrossRef]

- Kilian, Lutz. 2011. Structural Vector Autoregressions (No. 8515). CEPR Discussion Papers. Washington, DC: CEPR. [Google Scholar]

- Kilian, Lutz, and Helmut Lütkepohl. 2017. Structural Vector Autoregressive Analysis. Cambridge: Cambridge University Press. [Google Scholar]

- Kim, Soyoung, and Kuntae Lim. 2018. Effects of monetary policy shocks on exchange rate in small open Economies. Journal of Macroeconomics 56: 324–39. [Google Scholar] [CrossRef]

- Korhonen, Iikka, and Riikka Nuutilainen. 2017. Breaking monetary policy rules in Russia. Russian Journal of Economics 3: 366–78. [Google Scholar] [CrossRef]

- Kreptsev, Dmitry, and Seleznev Seleznev. 2018. Forecasting for the Russian economy using small-scale DSGE models. Russian Journal of Money and Finance 77: 51–67. [Google Scholar] [CrossRef]

- Lee, King Fuei. 2009. An empirical study of the Fisher effect and the dynamic relation between nominal interest rate and inflation in Singapore. The Singapore Economic Review 54: 75–88. [Google Scholar] [CrossRef]

- Leeper, Eric M. 1997. Narrative and VAR approaches to monetary policy: Common identification problems. Journal of Monetary Economics 40: 641–57. [Google Scholar] [CrossRef]

- Mironov, Valeriy. 2015. Russian devaluation in 2014–2015: Falling into the abyss or a window of opportunity? Russian Journal of Economics 1: 217–39. [Google Scholar] [CrossRef]

- Nguyen, Chu V., Khoi Dinh Phan, and Marvin J. Williams. 2017. The transmission mechanism of Russian Central Bank’s countercyclical monetary policy since 2011: Evidence from the interest rate pass-through. Journal of Eastern European and Central Asian Research 10. [Google Scholar]

- Nguyen, Tran Thai Ha, Massoud Moslepour, Thi Thuy Van Vo, and Wing-Keung Wong. 2020. State Ownership, Profitability, Risk-Taking Behavior, and Investment: An Empirical Approach to get better Trading Strategy for Listed Corporates in Vietnam. Economies 8: 46. [Google Scholar] [CrossRef]

- Njindan Iyke, Bernard. 2016. Are Monetary Policy Disturbances Important in Ghana? Some Evidence from Agnostic Identification. No. 70205. Munich: University Library of Munich, Germany. [Google Scholar]

- OECD. 2019. Main Economic Indicators—Complete Database. Main Economic Indicators (Database). Available online: https://www.oecd-ilibrary.org/economics/data/main-economic-indicators/main-economic-indicators-complete-database_data-00052-en (accessed on 22 September 2019).

- Ouliaris, Sam, Adrian Pagan, and Jorje Restrepo. 2016. Quantitative Macroeconomic Modeling with Structural Vector Autoregressions—An Eviews Implementation. Washington, DC: IMF Institute for Capacity Development. [Google Scholar]

- Ouliaris, Sam, and Adrian Pagan. 2016. A method for working with sign restrictions in structural equation modelling. Oxford Bulletin of Economics and Statistics 78: 605–22. [Google Scholar] [CrossRef]

- Pagliacci, Carolina. 2019. Are we ignoring supply shocks? A proposal for monitoring cyclical fluctuations. Empirical Economics 56: 445–67. [Google Scholar] [CrossRef]

- Panagopoulos, Yannis, and Ekaterini Tsouma. 2019. The effect of negative policy rates on the interest-rate pass-through mechanism in the eurozone. Review of Keynesian Economics 7: 247–62. [Google Scholar] [CrossRef]

- Peersman, Gert. 2005. What caused the early millennium slowdown? Evidence based on vector autoregressions. Journal of Applied Econometrics 20: 185–207. [Google Scholar] [CrossRef]

- Puah, Chin-Hong, Chong-Yang Sim, Mui-Yin Chin, and M. Affendy Arip. 2019. The new Keynesian trade-off between output and inflation: Time series based evidence from Russia. Business and Economic Horizons (BEH) 15: 126–36. [Google Scholar]

- Rubio-Ramirez, Juan F., Daniel F. Waggoner, and Tao Zha. 2010. Structural vector autoregressions: Theory of identification and algorithms for inference. The Review of Economic Studies 77: 665–96. [Google Scholar] [CrossRef]

- Rusnák, Marek, Tomas Havranek, and Roman Horváth. 2013. How to solve the price puzzle? A meta-analysis. Journal of Money, Credit and Banking 45: 37–70. [Google Scholar] [CrossRef]

- Scholl, Almuth, and Harald Uhlig. 2008. New evidence on the puzzles: Results from agnostic identification on monetary policy and exchange rates. Journal of International Economics 76: 1–13. [Google Scholar] [CrossRef]

- Shin, Yongcheol, and Peter Schmidt. 1992. The KPSS stationarity test as a unit root test. Economics Letters 38: 387–92. [Google Scholar] [CrossRef]

- Sims, Christopher A. 1980. Macroeconomics and reality. Econometrica: Journal of the Econometric Society 48: 1–48. [Google Scholar] [CrossRef]

- Sims, Christopher A. 1992. Interpreting the macroeconomic time series facts: The effects of monetary policy. European Economic Review 36: 975–1000. [Google Scholar] [CrossRef]

- Sims, Christopher A., and Tao Zha. 2006. Does Monetary Policy Generate Recessions. Macroeconomic Dynamics 10: 231. [Google Scholar] [CrossRef]

- Uhlig, Harald. 2005. What are the effects of monetary policy on output? Results from an agnostic identification procedure. Journal of Monetary Economics 52: 381–419. [Google Scholar] [CrossRef]

- Vdovichenko, Anna G., and Victoria G. Voronina. 2006. Monetary policy rules and their application in Russia. Research in International Business and Finance 20: 145–62. [Google Scholar] [CrossRef]

- Wang, Bin. 2019. Measuring the natural rate of interest of China: A time-varying perspective. Economics Letters 176: 117–20. [Google Scholar] [CrossRef]

- Wong, Wing-Keung. 2020. Editorial Statement and Research Ideas for Efficiency and Anomalies in Stock Markets. Economies 8: 10. [Google Scholar] [CrossRef]

- Woo, Kai-Yin, Chulin Mai, Michael McAleer, and Wing-Keung Wong. 2020. Review on Efficiency and Anomalies in Stock Markets. Economies 8: 20. [Google Scholar] [CrossRef]

- Yıldız, Bünyamin Fuat, Siamand Hesami, Husam Rjoub, and Wing-Keung Wong. 2021. Interpretation Of Oil Price Shocks On Macroeconomic Aggregates Of South Africa: Evidence From SVAR. Journal of Contemporary Issues in Business and Government 27: 279–87. [Google Scholar]

- Zada, Hassan, Arshad Hassan, and Wing-Keung Wong. 2021. Do jumps matter in both equity market returns and integrated volatility: A comparison of Asian Developed and Emerging Markets. Economies 9: 92. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Variable/Shocks | Demand | Cost–Push | Monetary Policy |

|---|---|---|---|

| yt | + | − | − |

| πt | + | + | − |

| it | + | + | + |

| INFL | INT | GAP | |

|---|---|---|---|

| Mean | 3.78 | 2.28 | 0.01 |

| Median | 3.92 | 2.17 | 0.02 |

| Maximum | 4.74 | 3.53 | 0.07 |

| Minimum | 1.92 | 1.44 | −0.08 |

| Std. Dev. | 0.77 | 0.51 | 0.02 |

| Jarque-Bera | 10.5 | 8.85 | 7.25 |

| Probability | 0.00 | 0.01 | 0.02 |

| Observations | 87 | 87 | 87 |

| Lag Length | AIC | SC | HQ | LM Test Result | Portmanteau Test Results |

|---|---|---|---|---|---|

| 1 | −10.20 | −9.93 | −10.14 | Serial Correlation | — |

| 2 | −11.04 | −10.44 * | −10.80 | Serial Correlation | — |

| 3 | −11.29 * | −10.42 | −10.94 * | No Serial Correlation | — |

| 4 | −11.225 | −10.10 | −10.77 | No Serial Correlation | No Serial Correlation |

| Variables | Levels | First Differences | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| ADF None | ADF Int. | PP None | PP Int. | KPSS Int. | ADF None | ADF Int. | PP None | PP Int. | KPSS Int. | |

| INFL | 1.43 | −5.99 * | 3.08 | −4.05 * | 1.12 | −1.99 *** | −3.06 * | −2.90 * | −3.78 * | 0.61 *** |

| INT | −1.31 | −2.67 *** | −1.31 | −2.70 *** | 0.47 *** | −8.26 * | −8.24 * | −8.26 * | −8.25 * | 0.13 |

| GAP | −4.37 * | −4.35 * | −3.54 * | −3.53 * | 0.03 | −5.67 * | −5.64 * | −5.73 * | −5.70 * | 0.06 |

| Variable/Shock | Time | Demand | Supply | MP |

|---|---|---|---|---|

| GAP | 2 | 93 | 6 | 1 |

| 5 | 82 | 15 | 3 | |

| 8 | 80 | 16 | 4 | |

| 10 | 79 | 18 | 3 | |

| Inflation | 2 | 9 | 90 | 1 |

| 5 | 25 | 71 | 4 | |

| 8 | 25 | 70 | 5 | |

| 10 | 22 | 71 | 6 | |

| Interest | 2 | 10 | 3 | 87 |

| 5 | 10 | 12 | 77 | |

| 8 | 19 | 20 | 61 | |

| 10 | 23 | 22 | 55 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yıldız, B.F.; Gökmenoğlu, K.K.; Wong, W.-K. Analysing Monetary Policy Shocks by Sign and Parametric Restrictions: The Evidence from Russia. Economies 2022, 10, 239. https://doi.org/10.3390/economies10100239

Yıldız BF, Gökmenoğlu KK, Wong W-K. Analysing Monetary Policy Shocks by Sign and Parametric Restrictions: The Evidence from Russia. Economies. 2022; 10(10):239. https://doi.org/10.3390/economies10100239

Chicago/Turabian StyleYıldız, Bünyamin Fuat, Korhan K. Gökmenoğlu, and Wing-Keung Wong. 2022. "Analysing Monetary Policy Shocks by Sign and Parametric Restrictions: The Evidence from Russia" Economies 10, no. 10: 239. https://doi.org/10.3390/economies10100239