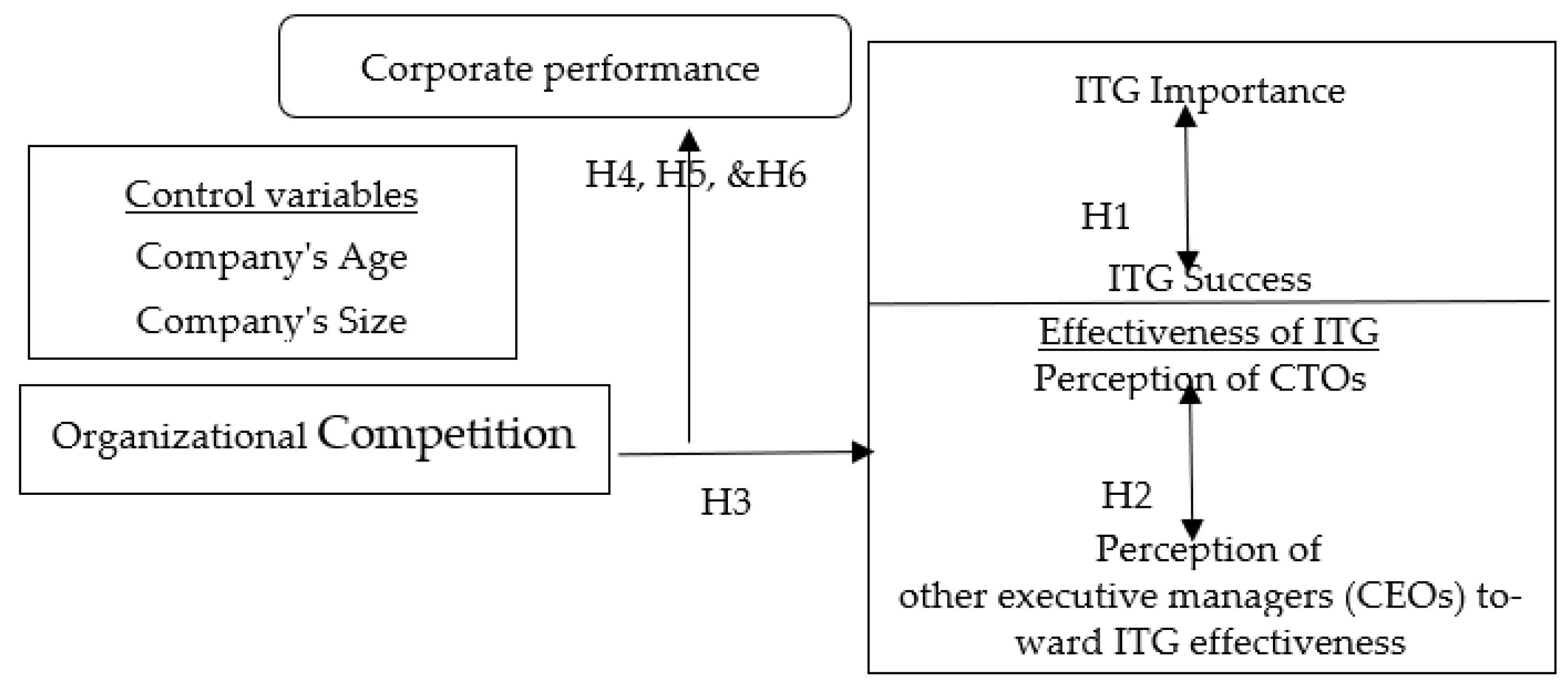

This section represents the study design, which reveals how the relationship between ITG and bank performance is examined by taking into consideration the effect of OC. It also explains how the variables of the study, including ITG, are calculated. In addition, it clarifies how data are collected and how the sample is chosen. Finally, it represents a diagram that depicts the relationships among the study variables.

3.1. Study Design

In this study, it is presumed that the proper fit between (

ITG) and the bank competition would affect the bank’s performance. It is expected that the more the fit between

ITG and bank competition, the better the performance achieved would be. In other words, what matters is not the level of

ITG as much as the proper match between

ITG and competition, which requires a proper analysis. It is worth clarifying that there are several perspectives of fit along with several mathematical and statistical tests to examine the appropriate match between two variables (

Venkatraman 1989). In this study, residual analysis is used to examine the appropriate match between

ITG and competition.

Building upon that, two basic equations will be used to test the hypotheses of the study. Equation (1) examines the relationship between

OC and the

ITG effectiveness. It describes what the matching is like between

ITG effectiveness and

OC.

where:

= information technology governance effectiveness of bank ,

= organizational competition of bank during 2015–5019,

= residuals (error term).

Equation (2) investigates the relationship between the appropriate match and a bank’s performance by regressing the absolute values of the residuals calculated in Equation (1) on the bank’s performance. The relationship between the bank’s performance and the residual values is controlled by two variables that are expected to affect performance, which are the bank size and the bank age. This procedure is consistent with the perspective that bank performance is affected by its size and age, which is a well-established procedure in the literature regarding bank performance (

Dias et al. 2020).

where:

= bank’s performance of bank during 2015–2019,

= absolute value of residuals from Equation (1),

= logarithm total assets of bank during 2015–2019,

= age of bank in 2017 “the middle of the study period”,

= residuals (error term).

According to the residual analysis, it is presumed that the lower the residuals derived from Equation (1) the higher the proper fit is between (

ITG) and the bank competition, and hence higher performance is expected (

Gordon et al. 2009;

Gordon and Smith 1992;

Duncan and Moores 1989;

Venkatraman 1989; and

Drazin and Van de Ven 1985). This means that the absolute values of residuals have an inverse effect on bank performance. To judge that

ITG level affects bank’s performance, one can rely upon the performance of one year only, However, measuring the performance of banks over a period of five years instead of one year, for example, results in an indicator that is less biased and less affected by the circumstances of one year regarding the bank’s performance. However, the model will be rerun with one year, which is 2019, to check the consistency of the study results.

3.2. Measurement of Variables

This section of the study provides information about the variables used to examine the hypotheses of the study, which are ITG, OC, and bank performance.

Regarding

ITG, a review of the literature on

ITG effectiveness shows lack of consensus on the definition of

ITG as well as on how to measure

ITG effectiveness.

Simonsson and Johnson (

2005) and

Wu et al. (

2015), as examples, include several definitions of

ITG. In the current study the definition of

Weill and Ross (

2004, p. 2) is adopted, which defines

ITG as “

specifying the decision rights and accountability framework to encourage desirable behaviour in using IT”. Concerning measuring

ITG,

Goodhue and Thompson (

1995), for example, suggest that

ITG can be assessed based on the utilization of IT and the fit of IT with the tasks it supports.

Van Grembergen and De Haes (

2005) developed an

ITG-balanced scorecard to evaluate

ITG.

Bowen et al. (

2007) found that

ITG can be assessed based on the understanding of both business and IT objectives, business and IT personnel involvement in IT decisions, communicating IT strategies and policies, and on business and IT personnel involvement in IT decisions.

Prasad et al. (

2010) measured

ITG effectiveness through the effectiveness of an IT steering committee.

Weill and Ross (

2004) focus on the external quality of

ITG by showing how

ITG is successful in achieving four outcomes by using information technology, which are the cost-effective use of information technology, the effective use of information technology for growth, the effective use of information technology for asset utilization, and the effective use of information technology for business flexibility. The success in achieving these four outcomes is weighted by the importance of each outcome for the organization. This approach measures the performance of information technology governance through the value of the services provided by information technology from the point of view of the organization, and in a manner is characterized by direct understanding and simplicity. This approach is well accepted and used by researchers, and it is considered by the Information Systems Audit and Control Association and the Information Technology Governance Institute. Therefore, this approach is adopted in the current study. However, a fifth objective of (

ITG) is also added to calculate

ITG in this study, which is the compliance of the company with legal and regulatory requirements. This objective was introduced by

Bowen et al. (

2007).

Based on the foregoing definition and objectives and using a seven-point Likert scale,

ITG will be calculated according to the following equation:

where:

n1: cost effective use of IT,

n2: the effective use of IT for growth,

n3: the effective use of IT for asset utilization,

n4: the effective use of IT for business flexibility,

n5: the use of IT for compliance of the bank with legal and regulatory requirements.

Given that there are five objectives, the maximum score is 100 and the minimum score is 14.29. Compared to

Weill and Ross (

2004) and

Bowen et al. (

2007), their maximum scores were 100 and minimum scores were 20. The difference between the minimum score in this study and the minimum scores in the former two studies is due to using a seven-point Likert scale in this study instead of a five-point Likert scale.

As for the measurement of organizational competition of banks, the competition situational factor involvement in the relationship between

ITG and bank performance is evaluated by the concentration ratio of each bank. These types of measures are suitable for testing the hypotheses of the current study because they can be calculated on the bank level. They result in a score for each bank (i.e., they measure the intra competitiveness of each bank). The concentration ratio or the market share of each bank is calculated based on the averages of five variables during the period 2015–2019, which are the percentages of total assets (TA%), credit facilities (CF%), total deposits (TD%), number of branches of each bank to the total of all banks (Branches%), and the number of ATMs of each bank to the total of all banks (ATMs%). The five variables will be condensed into one construct using exploratory factor analysis. In this study, the five observed variables above are used to extract or to develop the competition variable, which is a dimension or a latent variable. Factor analysis is a technique that can be used in order to extract latent variables. Under this analysis, the variance of each ratio is not taken as it is, but only the common variance of all ratios is taken. In addition, this analysis requires that these ratios are loaded on one construct or factor, which will be tested in the Results section. Factor analysis is followed in many fields of knowledge, especially in the field of financial ratios (see, for example, the model of

Hasan et al. (

2020, p. 55).

The higher value of concentration ratio represented by the factor score indicates higher market power of an individual bank, and thus its higher ability to create a higher price by differentiating products from those of other competitor banks. The ability of banks these days depends largely on information technology to distinguish their products in the banking sector, and the possibility of benefiting from information technology increases with the presence of a system that defines the rights and responsibilities assigned to users of this technology, that is, the existence of a system for IT governance. Therefore, it is expected that the presence of an adequate level of IT governance in these banks, in a manner commensurate with their market power, will increase the chances of improving the financial performance of these banks.

In addition to measuring competition on a bank level, it will also be measured at the level of the banking industry as a whole to provide a brief description about the level of competition in the study sample and during the study period. It is worth noting that some sectors have begun to appear in the market, such as eFAWATEERcom and mutual fund companies, which would compete with banks in some services. To achieve this goal, the concentration ratio is calculated on the industry level based on the market share of the largest three banks along with another measure, which is Hirchman–Herfindahl Index (

). This type of measure results in one score for all banks. The concentration ratio is calculated as follows:

where,

concentration ratio based on the market share (

) of the largest three banks based on total assets, credit facilities, and total deposits. The higher value of concentration ratio on the industry level indicates higher monopoly power. Meanwhile, Hirchman-Herfindahl Index (

) is calculated as follows:

where

= Hirchman–Herfindahl Index of the market shares (

) for all banks in the market based on total assets, credit facilities, and total deposits. The upper level of the

HHI is 1, while its lower level is 1/n. The higher value of

HHI indicates the lower level of competition.

The bank performance is evaluated by three measures, which are return on investment (ROI), return on equity (ROE), and Tobin’s q. These measures are used in the study because they are the most common measures of a bank’s financial performance. ROI ratio can be calculated in different forms depending on what return means and what investment means. In general, this ratio measures the efficiency of the management in utilizing its assets to generate income despite the financial position of the bank. Therefore, and to isolate the effect of financial expenses, returns would mean net income before interest, and to isolate the effect of tax, return would mean net income before tax. However, in the current study, ROI ratio is calculated by dividing net income after interest and before tax by average assets during the year, because the nature of the work of banks results in the interest expense being within the operating expenses of the bank and not a financing expense outside the basic work of it, as, for example, the situation of the manufacturing banks. ROE ratio, which measures the return on the investments of shareholders, is calculated by dividing net income after interest and tax by average shareholders’ equity during the year. Finally, Tobin’s q, which measures the ability of management to improve the market value of the bank through the operations of the business, is calculate by dividing the sum of market capitalization and the book value of total liabilities by the book value of total assets.

3.3. Data and Sample

To test the hypotheses of the study, data were collected to measure the three study variables, which are:

ITG, organizational competition, and bank performance. To build the

ITG construct, a survey was carried out to investigate the views of senior managers of banks in Jordan. Strictly speaking, the survey was used to collect data that enable the researcher to calculate the effectiveness of information technology governance. A carefully designed questionnaire was prepared through careful study of previous research and then constructs were developed to measure the effectiveness of information technology governance (

Weill and Ross 2004). Several concerns have been expressed for the use of perceptual measures that require respondents to evaluate the effective use of IT in the five objectives of (

ITG) that are mentioned in the subsection above. The key issues center on the use of a single informant, which is the case in this study. When relying on only one informant there is a risk of underestimating the true parameters due to dishonesty and/or systematic bias (

Ketokivi and Schroeder 2004). It should be clarified that the respondents could be affected by their own values and beliefs when evaluating the effective use of

ITG. Although it is acknowledged that there is such a risk in this study, and thus this is a potential limitation, any risk of bias has been minimized by ensuring that the questionnaire was answered by senior managers including chief technology officers (CTOs) in charge of

ITG who knows about the systems of their banks. Then the questionnaire was sent to a number of specialists in this field, and modified into its final form in light of the suggestions made by the arbitrators. The reliability of the questionnaire was also checked using Cronbach’s α-values, which amounted to 90%, indicating that there was internal consistency between the items, and confirming the reliability of the constructs employed (

Hair et al. 2006). The value of alpha was also calculated for each part of the questionnaire as shown in

Table 1.

It is worth noting that the population of the study consists of all senior managers working in the licensed banks operating in Jordan during 2021. These banks are distributed into 13 Jordanian commercial banks, 4 Jordanian Islamic banks, and 6 foreign commercial banks. This definition of licensed banks does not include the financial institutions operating in Jordan. By virtue of a letter from the Association of Banks in Jordan, each operating bank in Jordan was requested to fill out 10 copies of the questionnaire by its senior managers, provided that the director of information technology was among them. The banking sector in Jordan was chosen among other sectors in this study due to the increasing interest of this sector in

ITG. This growing interest in

ITG in banks operating in Jordan led to the issuance of the instructions of governance pertaining to information and related technologies No. 65/2016 on the 25 of October 2016 (

Central Bank of Jordan 2016b). This is based on the interest of the Central Bank of Jordan to implement the rules and foundations of institutional governance in order to reduce the risks of banks and to protect them from involving useless investments and unjustified expenses in information technology that may lead to huge losses. These instructions are consistent with the instructions of institutional governance of banks including the instructions of institutional governance in Islamic banks. According to these instructions, every bank must send an achievement report to the Central Bank of Jordan related to compliance with these instructions every six months, indicating the level of achievement for each item of the instructions. They are also required to publish guidance of governance pertaining to information and related technologies on their electronic sites and they should disclose the existence of this guidance in their annual reports. The instructions also require that banks form ITG committees, IT steering committees, and IT auditing committees.

{kind=link}