The Effects of Service Quality Performance on Customer Satisfaction for Non-Banking Financial Institutions in an Emerging Economy

,

,  ,

,  and

and

Abstract

:1. Introduction

2. Literature Review and Hypothesis Development

2.1. Service Quality

2.2. Underpinning Models of Service Quality

2.2.1. Gronroos Model

2.2.2. Gap Theory of SQ (SERVQUAL)

2.2.3. SERVPERF Model

2.2.4. CARTER Model

2.3. Customer Satisfaction

2.4. Service Quality and Customer Satisfaction

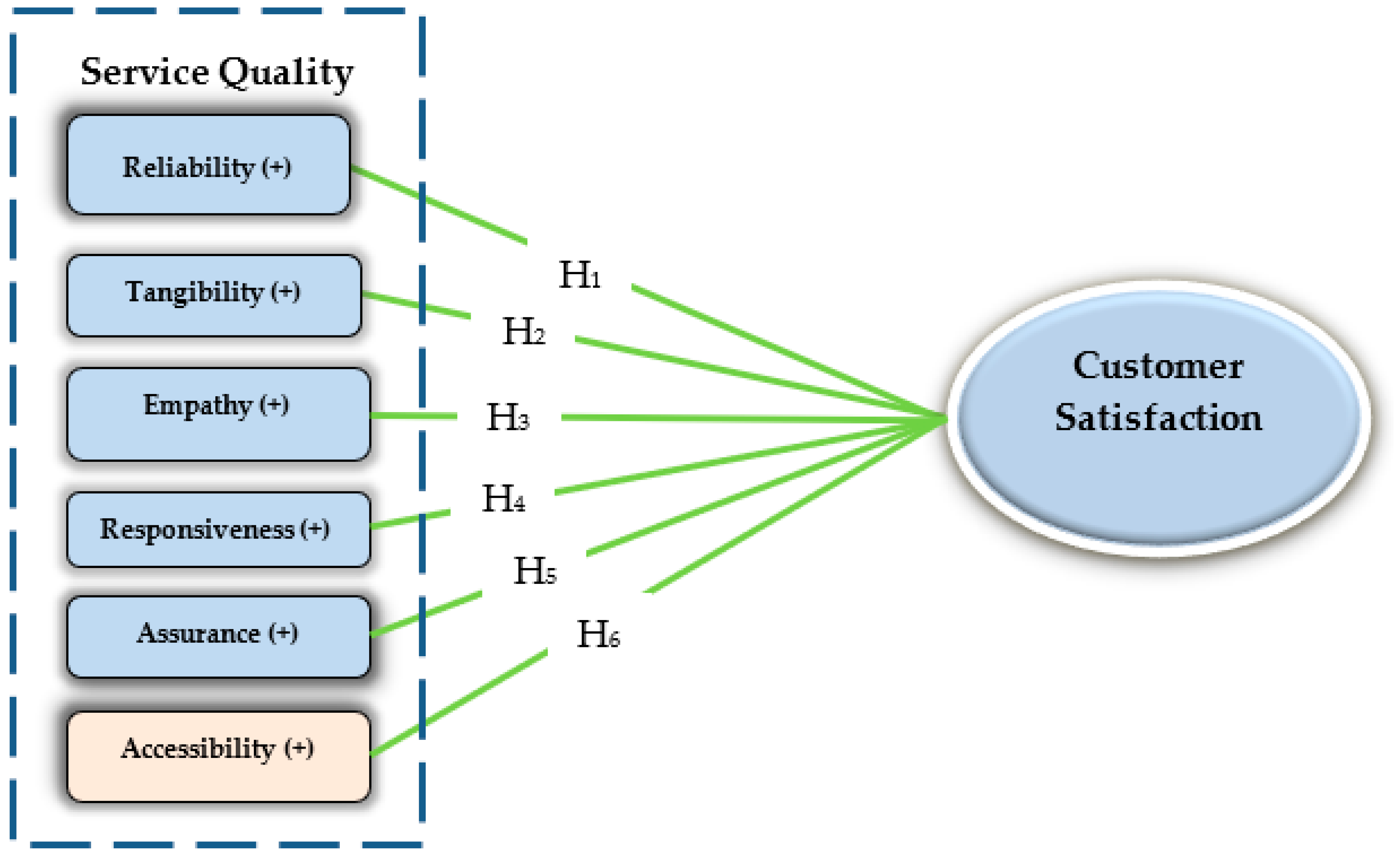

2.5. Hypothesis Development

2.5.1. Reliability

2.5.2. Tangibility

2.5.3. Empathy

2.5.4. Responsiveness

2.5.5. Assurance

2.5.6. Accessibility

3. The Methodology of the Study

3.1. Research Design

3.2. Measurement Instrument

4. Results

4.1. Respondents’ Profile

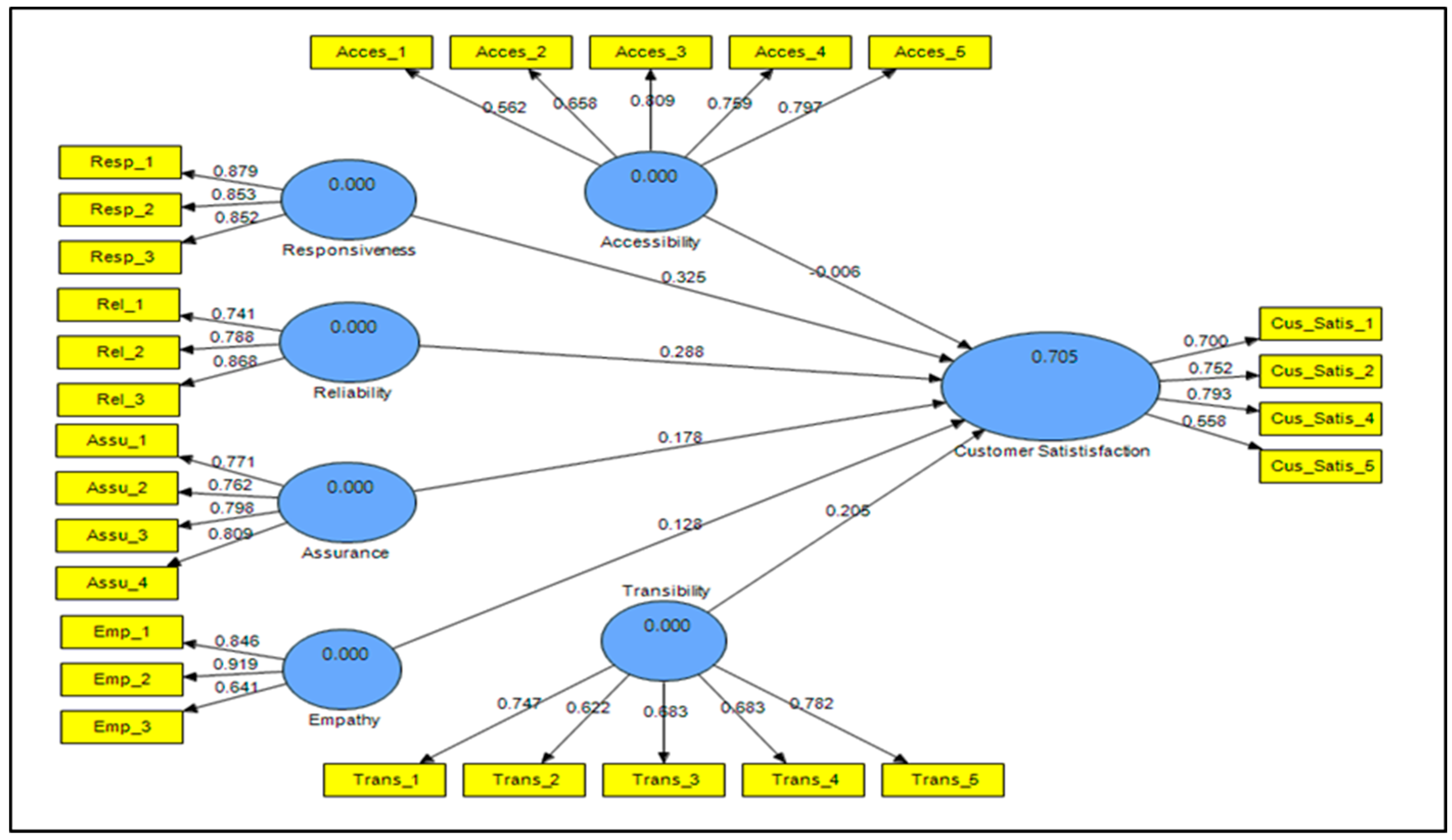

4.2. Assessment of the Measurement Model (Determinants) for Service Quality of NBFI

4.3. Assessment of the Structural Equation Model for Service Quality of NBFI

5. Discussion

6. Conclusions

6.1. Policy Implications

6.2. Contribution to the Theory

6.3. Limitations and Future Direction of the Study

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Abdelhadi, Abdelhakim. 2021. Patients’ Satisfactions on the Waiting Period at the Emergency Units. Comparison Study before and during COVID-19 Pandemic. Journal of Public Health Research 10: 1956. [Google Scholar] [CrossRef]

- Ali, Muhammad, and Syed Ali Raza. 2017. Service Quality Perception and Customer Satisfaction in Islamic Banks of Pakistan: The Modified SERVQUAL Model. Total Quality Management & Business Excellence 28: 559–77. [Google Scholar]

- Alkhazaleh, Ayman Mansour Khalaf, and Hossam Haddad. 2021. How Does the Fintech Services Delivery Affect Customer Satisfaction: A Scenario of Jordanian Banking Sector. Strategic Change 30: 405–13. [Google Scholar] [CrossRef]

- Amin, Muslim, and Zaidi Isa. 2008. An Examination of the Relationship between Service Quality Perception and Customer Satisfaction. Management 1: 191–209. [Google Scholar] [CrossRef] [Green Version]

- Andaleeb, Syed Saad, and Carolyn Conway. 2006. Customer Satisfaction in the Restaurant Industry: An Examination of the Transaction-Specific Model. Journal of Services Marketing 20: 3–11. [Google Scholar] [CrossRef]

- Anderson, Eugene W., and Mary W. Sullivan. 1993. The Antecedents and Consequences of Customer Satisfaction for Firms. Marketing Science 12: 125–43. [Google Scholar] [CrossRef]

- Arasli, Huseyin, Salime Mehtap-Smadi, and Salih Turan Katircioglu. 2005. Customer Service Quality in the Greek Cypriot Banking Industry. Managing Service Quality: An International Journal 15: 41–56. [Google Scholar] [CrossRef]

- Ashraf, Dawood, Mohsin Khawaja, and M Ishaq Bhatti. 2022. Raising Capital amid Economic Policy Uncertainty: An Empirical Investigation. Financial Innovation 8: 1–32. [Google Scholar] [CrossRef]

- Babakus, Emin, and Gregory W. Boller. 1992. An Empirical Assessment of the SERVQUAL Scale. Journal of Business Research 24: 253–68. [Google Scholar] [CrossRef]

- Baghla, Aditi, and Amandeep Garai. 2016. Service Quality in the Retail Banking Sector-A Study of Selected Public and New Indian Private Sector Banks in India. IJAR 2: 598–603. [Google Scholar]

- Baqué, Nils, Alban Ferati, and Rahul Singh. 2021. Customer Satisfaction in the Cooperative Banking Industry: A Quantitative Approach. Available online: https://www.diva-portal.org/smash/get/diva2:1574507/FULLTEXT01.pdf (accessed on 3 February 2023).

- Barbara, R Lewis, and W Mitchell Vincent. 1990. Defining and Measuring the Quality of Customer Service. Marketing Intelligence & Planning 8: 11–17. [Google Scholar]

- Barclay, Donald, Clarence Higgings, and Ronald Thompson. 1995. The Partial Least Squares (PLS) Approach to Casual Modeling: Personal Computer Adoption and Use as an Illustration. Technology Studies 2: 285–309. [Google Scholar]

- Bashir, Md Abdul, Mass Hareeza Ali, Lam Mun Wai, Mohammad Imtiaz Hossain, and Md Shumonur Rahaman. 2020. Mediating Effect of Customer Perceived Value on the Relationship between Service Quality and Customer Satisfaction of E-Banking in Bangladesh. International Journal of Advanced Science and Technology 29: 3590–606. [Google Scholar]

- Blut, Markus. 2016. E-Service Quality: Development of a Hierarchical Model. Journal of Retailing 92: 500–17. [Google Scholar] [CrossRef] [Green Version]

- Boonlertvanich, Karin. 2019. Service Quality, Satisfaction, Trust, and Loyalty: The Moderating Role of Main-Bank and Wealth Status. Marketing 37: 278–302. [Google Scholar] [CrossRef]

- Buzzel, Robert. D., and Bradley. T. Gale. 1987. The PIMS Principles. New York: The Free Press, chp. 6. [Google Scholar]

- Caruana, Albert, Arthur H. Money, and Pierre R. Berthon. 2000. Service Quality and Satisfaction ą the Moderating Role of Value. European Journal of Marketing 34: 1338–53. [Google Scholar] [CrossRef]

- Chatzoglou, Prodromos, Dimitrios Chatzoudes, Eftichia Vraimaki, and Eleni Leivaditou. 2014. Measuring Citizen Satisfaction Using the SERVQUAL Approach: The Case of the ‘Hellenic Post’. Procedia Economics and Finance 9: 349–60. [Google Scholar] [CrossRef] [Green Version]

- Chonsalasin, Dissakoon, Sajjakaj Jomnonkwao, and Vatanavongs Ratanavaraha. 2021. Measurement Model of Passengers’ Expectations of Airport Service Quality. International Journal of Transportation Science and Technology 10: 342–52. [Google Scholar] [CrossRef]

- Choudhury, Koushiki. 2014. The Influence of Customer-Perceived Service Quality on Customers’ Behavioural Intentions: A Study of Public and Private Sector Banks, Class and Mass Banking and Consumer Policy Implications. International Review on Public and Nonprofit Marketing 11: 47–73. [Google Scholar] [CrossRef]

- Cohen, Jacob. 1988. Statistical Power Analysis for the Behavioral Sciences. Cambridge: Academic Press. [Google Scholar]

- Collis, Jill, and Roger Hussey. 2013. Business Research: A Practical Guide for Undergraduate and Postgraduate Students: Macmillan International Higher Education. London: Palgrave Macmillan. [Google Scholar]

- Cronin, J. Joseph, Jr., and Steven A. Taylor. 1992. Measuring Service Quality: A Reexamination and Extension. Journal of Marketing 56: 55–68. [Google Scholar] [CrossRef]

- Dabholkar, Pratibha A., C. David Shepherd, and Dayle I. Thorpe. 2000. A Comprehensive Framework for Service Quality: An Investigation of Critical Conceptual and Measurement Issues through a Longitudinal Study. Journal of Retailing 76: 139–73. [Google Scholar] [CrossRef]

- Derksen, Frans, Jozien Bensing, and Antoine Lagro-Janssen. 2013. Effectiveness of Empathy in General Practice: A Systematic Review. British Journal of General Practice 63: e76–e84. [Google Scholar] [CrossRef] [Green Version]

- Devesh, Sonal. 2019. Service Quality Dimensions and Customer Satisfaction: Empirical Evidence from Retail Banking Sector in Oman. Total Quality Management & Business Excellence 30: 1616–29. [Google Scholar]

- Donthu, Naveen, and Boonghee Yoo. 1998. Cultural Influences on Service Quality Expectations. Journal of Service Research 1: 178–86. [Google Scholar] [CrossRef]

- Endara, Yousef Mohamed, Asbi B. Ali, and Mohd Shukri Ab Yajid. 2019. The Influence of Culture on Service Quality Leading to Customer Satisfaction and Moderation Role of Type of Bank. Journal of Islamic Accounting and Business Research 10: 134–54. [Google Scholar] [CrossRef]

- Ennew, Christine, Nigel Waite, and Róisín Waite. 2013. Financial Services Marketing: An International Guide to Principles and Practice. Abingdon-on-Thames: Routledge. [Google Scholar]

- Famiyeh, Samuel, Disraeli Asante-Darko, and Amoako Kwarteng. 2018. Service Quality, Customer Satisfaction, and Loyalty in the Banking Sector: The Moderating Role of Organizational Culture. International Journal of Quality & Reliability Management 35: 1546–67. [Google Scholar]

- Fase, Martin MG, and R C N Abma. 2003. Financial Environment and Economic Growth in Selected Asian Countries. Journal of Asian Economics 14: 11–21. [Google Scholar] [CrossRef]

- Fida, Bashir Ahmad, Umar Ahmed, Yousuf Al-Balushi, and Dharmendra Singh. 2020. Impact of Service Quality on Customer Loyalty and Customer Satisfaction in Islamic Banks in the Sultanate of Oman. SAGE Open 10: 2158244020919517. [Google Scholar] [CrossRef]

- Fornell, Claes, and David F. Larcker. 1981. Evaluating Structural Equation Models with Unobservable Variables and Measurement Error. Journal of Marketing Research 18: 39–50. [Google Scholar] [CrossRef]

- Gatari, Eva Nyawira. 2016. Factors Influencing Customer Satisfaction in the Banking Industry in Kenya: A Case Study of Investments and Mortgages (I&M) Bank Ltd. Ph.D. thesis, United States International University Africa, Nairobi, Kenya. [Google Scholar]

- Gotlieb, Jerry B., Dhruv Grewal, and Stephen W Brown. 1994. Consumer Satisfaction and Perceived Quality: Complementary or Divergent Constructs? Journal of Applied Psychology 79: 875. [Google Scholar] [CrossRef]

- Gronroos, Christian. 1988. Service Quality: The Six Criteria of Good Perceived Service. Review of Business 9: 10. [Google Scholar]

- Hair, Joe F., Christian M. Ringle, and Marko Sarstedt. 2011. PLS-SEM: Indeed a Silver Bullet. Journal of Marketing Theory and Practice 19: 139–52. [Google Scholar] [CrossRef]

- Hair, Joseph F., Jr., G. Tomas M. Hult, Christion M. Ringle, and Marko Sarstedt. 2014. A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM). New York: Sage Publications. [Google Scholar]

- Hamzah, Zalfa Laili, Siew Peng Lee, and Sedigheh Moghavvemi. 2017. Elucidating Perceived Overall Service Quality in Retail Banking. International Journal of Bank Marketing 35: 781–804. [Google Scholar] [CrossRef]

- Haron, Razali, Noradilah Abdul Subar, and Khairunisah Ibrahim. 2020. Service Quality of Islamic Banks: Satisfaction, Loyalty and the Mediating Role of Trust. Islamic Economic Studies 28: 3–23. [Google Scholar] [CrossRef]

- Hartline, Michael D., and Orville C. Ferrell. 1996. The Management of Customer-Contact Service Employees: An Empirical Investigation. Journal of Marketing 60: 52–70. [Google Scholar] [CrossRef]

- Henseler, Jörg, Christian M. Ringle, and Marko Sarstedt. 2015. A New Criterion for Assessing Discriminant Validity in Variance-Based Structural Equation Modeling. Journal of the Academy of Marketing Science 43: 115–35. [Google Scholar] [CrossRef] [Green Version]

- Hossain, Monzur, and Md Shahiduzzaman. 2002. Development of Non Bank Financial Institutions to Strengthen the Financial System of Bangladesh. Quarterly Journal of Bangladesh Institute of Bank Management 28: 1–21. [Google Scholar]

- Hui, Baldwin S., and Herman Wold. 1982. Consistency and Consistency at Large of Partial Least Squares Estimates. Systems under Indirect Observation, Part II 131: 119–30. [Google Scholar]

- Islam, Mohd Aminul, and Jamil Bin Osman. 2011. Development Impact of Non-Bank Financial Intermediaries on Economic Growth in Malaysia: An Empirical Investigation. International Journal of Business and Social Science 2: 187–98. [Google Scholar]

- Islam, Rafikul, Selim Ahmed, Mahbubar Rahman, and Ahmed Al Asheq. 2020. Determinants of Service Quality and Its Effect on Customer Satisfaction and Loyalty: An Empirical Study of Private Banking Sector. The TQM Journal 33: 1163–82. [Google Scholar] [CrossRef]

- Jahan, Nasrin, Md Julfikar Ali, and Ahmed Al Asheq. 2020. Examining the Key Determinants of Customer Satisfaction Internet Banking Services in Bangladesh. Academy of Strategic Management Journal 19: 1–6. [Google Scholar]

- Jain, Sanjay K., and Garima Gupta. 2004. Measuring Service Quality: SERVQUAL vs. SERVPERF Scales. Vikalpa 29: 25–38. [Google Scholar] [CrossRef]

- Jamal, Ahmad, and Kamal Naser. 2002. Customer Satisfaction and Retail Banking: An Assessment of Some of the Key Antecedents of Customer Satisfaction in Retail Banking. International Journal of Bank Marketing 20: 146–60. [Google Scholar] [CrossRef] [Green Version]

- Jianu, Ionel, Carmen Ţurlea, and Ionela Guşatu. 2015. The Reporting and Sustainable Business Marketing. Sustainability 8: 23. [Google Scholar] [CrossRef] [Green Version]

- Kamilia, Bahia, and Nantel Jacques. 2000. A Reliable and Valid Measurement Scale for the Perceived Service Quality of Banks. The International Journal of Bank Marketing 18: 84–91. [Google Scholar]

- Kant, Rishi, and Deepak Jaiswal. 2017. The Impact of Perceived Service Quality Dimensions on Customer Satisfaction: An Empirical Study on Public Sector Banks in India. International Journal of Bank Marketing 35: 411–30. [Google Scholar] [CrossRef]

- Khamis, Fauz Moh, and Rosemaliza AbRashid. 2018. Service Quality and Customer’s Satisfaction in Tanzania’s Islamic Banks: A Case Study at People’s Bank of Zanzibar (PBZ). Journal of Islamic Marketing 9: 884–900. [Google Scholar] [CrossRef]

- Khan, Abdul Gaffar, Reshma Pervin Lima, and Md Shahed Mahmud. 2021. Understanding the Service Quality and Customer Satisfaction of Mobile Banking in Bangladesh: Using a Structural Equation Model. Global Business Review 22: 85–100. [Google Scholar] [CrossRef]

- Khatoon, Sadia, Xu Zhengliang, and Hamid Hussain. 2020. The Mediating Effect of Customer Satisfaction on the Relationship between Electronic Banking Service Quality and Customer Purchase Intention: Evidence from the Qatar Banking Sector. SAGE Open 10: 2158244020935887. [Google Scholar] [CrossRef]

- Krishnamurthy, Ravichandran, B. Tamil Mani, S. Arun Kumar, and Sandhya Prabhakaran. 2010. Influence of Service Quality on Customer Satisfaction Application of Servqual Model. International Journal of Business and Management 5: 117. [Google Scholar] [CrossRef] [Green Version]

- Kumar, Mukesh, K. Sukumaran Sujit, and Vincent Charles. 2018. Deriving Managerial Implications through SERVQUAL Gap Elasticity in UAE Banking. International Journal of Quality & Reliability Management 35: 940–64. [Google Scholar]

- Ladhari, Riadh, Nizar Souiden, and Ines Ladhari. 2011. Determinants of Loyalty and Recommendation: The Role of Perceived Service Quality, Emotional Satisfaction and Image. Journal of Financial Services Marketing 16: 111–24. [Google Scholar] [CrossRef] [Green Version]

- Lee, Sanghyun, Lucette B. Comer, Alan J. Dubinsky, and Kai Schafer. 2011. The Role of Emotion in the Relationship Between Customers and Automobile Salespeople1. Journal of Managerial Issues 23: 206. [Google Scholar]

- Markovic, Stefan, Oriol Iglesias, Jatinder Jit Singh, and Vicenta Sierra. 2018. How Does the Perceived Ethicality of Corporate Services Brands Influence Loyalty and Positive Word-of-Mouth? Analyzing the Roles of Empathy, Affective Commitment, and Perceived Quality. Journal of Business Ethics 148: 721–40. [Google Scholar] [CrossRef]

- Munusamy, Jayaraman, Shankar Chelliah, and Hor Wai Mun. 2010. Service Quality Delivery and Its Impact on Customer Satisfaction in the Banking Sector in Malaysia. International Journal of Innovation, Management and Technology 1: 398. [Google Scholar]

- Murray, John, Jonathan Elms, and Mike Curran. 2019. Examining Empathy and Responsiveness in a High-Service Context. International Journal of Retail & Distribution Management 47: 1364–78. [Google Scholar]

- Nazeri, Ali, Rahman Soofifard, Mohsen Ebrahimi, and Ladan Babayof. 2019. The Effect of the Internet Banking Service Quality on Customer Satisfaction (Case Study: Refah Bank in Tehran). International Journal of Services and Operations Management 34: 65–80. [Google Scholar] [CrossRef]

- Negash, Geleta Etana. 2021. Impact of Service Quality Performance on Customer Satisfaction: A Case of Oromia International Bank (OIB), Ambo Branch, West Shoa Zone, Oromia Regional State, Ethiopia. African Journal of Marketing Management 13: 12–24. [Google Scholar]

- Nguyen, Do Thanh, Van Thanh Pham, Dung Manh Tran, and Duyen Bich T. Pham. 2020. Impact of Service Quality, Customer Satisfaction and Switching Costs on Customer Loyalty. The Journal of Asian Finance, Economics and Business 7: 395–405. [Google Scholar] [CrossRef]

- Olorunniwo, Festus, Maxwell K. Hsu, and Godwin J. Udo. 2006. Service Quality, Customer Satisfaction, and Behavioral Intentions in the Service Factory. Journal of Services Marketing 20: 59–72. [Google Scholar] [CrossRef]

- Ong, Khian Sin, Bang Nguyen, and Sharifah Faridah Syed Alwi. 2017. Consumer-Based Virtual Brand Personality (CBVBP), Customer Satisfaction and Brand Loyalty in the Online Banking Industry. International Journal of Bank Marketing 35: 370–90. [Google Scholar] [CrossRef]

- Oppewal, Harmen, and Marco Vriens. 2000. Measuring Perceived Service Quality Using Integrated Conjoint Experiments. The International Journal of Bank Marketing 18: 154–69. [Google Scholar] [CrossRef]

- Othman, AbdulQawi, and Lynn Owen. 2001. Adopting and Measuring Customer Service Quality (SQ) in Islamic Banks: A Case Study in Kuwait Finance House. International Journal of Islamic Financial Services 3: 1–26. [Google Scholar]

- Pakurár, Miklós, Hossam Haddad, János Nagy, József Popp, and Judit Oláh. 2019. The Service Quality Dimensions That Affect Customer Satisfaction in the Jordanian Banking Sector. Sustainability 11: 1113. [Google Scholar] [CrossRef] [Green Version]

- Parasuraman, Ananthanarayanan, Valarie A. Zeithaml, and Leonard L. Berry. 1988. SERVQUAL: A Multiple-Item Scale for Measuring Consumer Perceptions of Service Quality. Journal of Retailing 64: 12–40. [Google Scholar]

- Parasuraman, Ananthanarayanan, Leonard Berry, and Valerie Zeithaml. 2002. Refinement and Reassessment of the SERVQUAL Scale. Journal of Retailing 67: 114. [Google Scholar]

- Parasuraman, Anantharanthan, Valarie A. Zeithaml, and Leonard L. Berry. 1985. A Conceptual Model of Service Quality and Its Implications for Future Research. Journal of Marketing 49: 41–50. [Google Scholar] [CrossRef]

- Parasuraman, Arun, Leonard L. Berry, and Valarie A. Zeithaml. 1991. Understanding Customer Expectations of Service. Sloan Management Review 32: 39–48. [Google Scholar]

- Peitzika, Eirini, Sofia Chatzi, and Dimitra Kissa. 2020. Service Quality Expectations in the Fitness Center Context: A Validation of the Expectations Component of the SERVQUAL Scale in Greece. Services Marketing Quarterly 41: 89–104. [Google Scholar] [CrossRef]

- Peng, Lee Siew, and Sedigheh Moghavvemi. 2015. The Dimension of Service Quality and Its Impact on Customer Satisfaction, Trust, and Loyalty: A Case of Malaysian Banks. Asian Journal of Business and Accounting 8: 91–121. [Google Scholar]

- Phan, Tien, Vinh Thai, and Thao Vu. 2021. Port Service Quality (PSQ) and Customer Satisfaction: An Exploratory Study of Container Ports in Vietnam. Maritime Business Review 6: 72–94. [Google Scholar] [CrossRef]

- Pooya, Alireza, Mehran Abed Khorasani, and Simin Gholamian Ghouzhdi. 2020. Investigating the Effect of Perceived Quality of Self-Service Banking on Customer Satisfaction. International Journal of Islamic and Middle Eastern Finance and Management 13: 263–80. [Google Scholar] [CrossRef]

- Potluri, Rajasekhara Mouly, Srinivas Rao Angati, and M Srinivasa Narayana. 2016. A Structural Compendium on Service Quality and Customer Satisfaction: A Survey of Banks in India. Journal of Transnational Management 21: 12–28. [Google Scholar] [CrossRef]

- Powell, Philip A., and Jennifer Roberts. 2017. Situational Determinants of Cognitive, Affective, and Compassionate Empathy in Naturalistic Digital Interactions. Computers in Human Behavior 68: 137–48. [Google Scholar] [CrossRef] [Green Version]

- Rahman, Md Atikur, Md Julfikar Ali, Zhang Kejing, Rupali Dilip Taru, and Zahidur Rahman Mamoon. 2020. Investigating the Effect of Service Quality on Bank Customers’ Satisfaction in Bangladesh. The Journal of Asian Finance, Economics and Business 7: 823–29. [Google Scholar] [CrossRef]

- Rashid, Md Harun Ur, Mohammad Nurunnabi, Mahfuzur Rahman, and Md Abdul Kaium Masud. 2020. Exploring the Relationship between Customer Loyalty and Financial Performance of Banks: Customer Open Innovation Perspective. Journal of Open Innovation: Technology, Market, and Complexity 6: 108. [Google Scholar] [CrossRef]

- Rasyida, Dyah R., M. Mujiya Ulkhaq, Priska R. Setiowati, and Nadia A. Setyorini. 2016. Assessing Service Quality: A Combination of SERVPERF and Importance-Performance Analysis. In MATEC Web of Conferences, the 3rd International Conference on Industrial Engineering and Applications (ICIEA 2016). Les Ulis: EDP Sciences, vol. 68, p. 06003. [Google Scholar] [CrossRef] [Green Version]

- Reinartz, Werner, Michael Haenlein, and Jörg Henseler. 2009. An Empirical Comparison of the Efficacy of Covariance-Based and Variance-Based SEM. International Journal of Research in Marketing 26: 332–44. [Google Scholar] [CrossRef] [Green Version]

- Ringle, Christian M., Sven Wende, and A. S. Will. 2015. SmartPLS. 2.0 (M3) Beta. Hamburg: University of Hamburg. [Google Scholar]

- Rioja, Felix, and Neven Valev. 2004. Finance and the Sources of Growth at Various Stages of Economic Development. Economic Inquiry 42: 127–40. [Google Scholar] [CrossRef]

- Ross, Dhyana Sharon, and Ramesh Venkatesh. 2015. An Empirical Study of the Factors Influencing Quality of Healthcare and Its Effects on Patient Satisfaction. International Journal of Innovative Research in Science, Engineering and Technology 4: 54–59. [Google Scholar]

- Sardana, Shivani, and Venkata N. Bajpai. 2020. E-Banking Service Quality and Customer Satisfaction: An Exploratory Study on India. International Journal of Services and Operations Management 35: 223–47. [Google Scholar] [CrossRef]

- Schneider, Benjamin, and Susan S. White. 2004. Service Quality: Research Perspectives. Thousand Oaks: Sage Publication. [Google Scholar]

- Selvakumar, J. Joshua. 2015. Impact of Service Quality on Customer Satisfaction in Public Sector and Private Sector Banks. Purushartha: A Journal of Management, Ethics and Spirituality 8: 1–12. [Google Scholar]

- Seth, Nitin, Sanjeev Gopalrao Deshmukh, and Prem Vrat. 2005. Service Quality Models: A Review. International Journal of Quality & Reliability Management 22: 913–49. [Google Scholar]

- Shayestehfar, Reza, and Bita Yazdani. 2019. Bank Service Quality: A Comparison of Service Quality between BSI Branches in Isfahan and Dubai. The TQM Journal 31: 28–51. [Google Scholar] [CrossRef]

- Shi, Yan, Abu Bakkar Siddik, Mohammad Masukujjaman, Guangwen Zheng, Muhammad Hamayun, and Abdullah Mohammed Ibrahim. 2022. The Antecedents of Willingness to Adopt and Pay for the IoT in the Agricultural Industry: An Application of the UTAUT 2 Theory. Sustainability 14: 6640. [Google Scholar] [CrossRef]

- Shokouhyar, Sajjad, Sina Shokoohyar, and Sepehr Safari. 2020. Research on the Influence of After-Sales Service Quality Factors on Customer Satisfaction. Journal of Retailing and Consumer Services 56: 102139. [Google Scholar] [CrossRef]

- Slack, Neale J., and Gurmeet Singh. 2020. The Effect of Service Quality on Customer Satisfaction and Loyalty and the Mediating Role of Customer Satisfaction: Supermarkets in Fiji. The TQM Journal 32: 543–58. [Google Scholar] [CrossRef]

- The Business Standard. 2020. Six More Non-Bank Financial Institutions in Trouble. Available online: https://tbsnews.net/economy/banking/six-more-non-bank-financial-institutions-trouble (accessed on 3 February 2023).

- Uddin, K. M. Salah, Nymatul Jannat Nipa, and Mamunur Rashid. 2015. Identification the Factors Influencing Customer Satisfaction on Service Quality in Jamuna Bank. International Journal of Business and Economic Research 4: 30–35. [Google Scholar] [CrossRef] [Green Version]

- Umoke, MaryJoy, Prince Christian Ifeanachor Umoke, Ignatius O. Nwimo, Chioma Adaora Nwalieji, Rosemary N. Onwe, Nwafor Emmanuel Ifeanyi, and Agbaje Samson Olaoluwa. 2020. Patients’ Satisfaction with Quality of Care in General Hospitals in Ebonyi State, Nigeria, Using SERVQUAL Theory. SAGE Open Medicine 8: 2050312120945129. [Google Scholar] [CrossRef]

- Vencataya, Lomendra, Sharmila Pudaruth, Roubina Juwaheer, Ganess Dirpal, and Nebeelah Sumodhee. 2019. Assessing the Impact of Service Quality Dimensions on Customer Satisfaction in Commercial Banks of Mauritius. Studies in Business and Economics 14: 259–70. [Google Scholar] [CrossRef] [Green Version]

- Vittas, Dimitri. 1997. The Role of Non-Bank Financial Intermediaries in Egypt and Other MENA Countries. Washington, DC: Development Research Group, World Bank. Available online: https://papers.ssrn.com/sol3/Delivery.cfm/698.pdf?abstractid=620529&mirid=1 (accessed on 3 February 2023).

- Wang, Yonggui, Hing-Po Lo, and Yongheng Yang. 2004. An Integrated Framework for Service Quality, Customer Value, Satisfaction: Evidence from China’s Telecommunication Industry. Information Systems Frontiers 6: 325–40. [Google Scholar] [CrossRef]

- Yarimoglu, Emel Kursunluoglu. 2014. A Review on Dimensions of Service Quality Models. Journal of Marketing Management 2: 79–93. [Google Scholar]

- Yun, Jeewoo, and Jungkun Park. 2022. The Effects of Chatbot Service Recovery with Emotion Words on Customer Satisfaction, Repurchase Intention, and Positive Word-of-Mouth. Frontiers in Psychology 13: 2912. [Google Scholar] [CrossRef] [PubMed]

- Zeithaml, Valarie A., Ananthanarayanan Parasuraman, Leonard L. Berry, and Leonard L. Berry. 1990. Delivering Quality Service: Balancing Customer Perceptions and Expectations. New York: Simon and Schuster. [Google Scholar]

- Zhang, Min, Xueping He, Fang Qin, Wenbiao Fu, and Zhen He. 2019. Service Quality Measurement for Omni-Channel Retail: Scale Development and Validation. Total Quality Management & Business Excellence 30: S210–S226. [Google Scholar]

- Zia, Adil. 2020. Discovering the Linear Relationship of Service Quality, Satisfaction, Attitude and Loyalty for Banks in Albaha, Saudi Arabia. PSU Research Review 6: 90–104. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Aspects | Classification | Frequency | Percentage |

|---|---|---|---|

| Gender | Male | 175 | 85.36% |

| Female | 30 | 14.64% | |

| Age | ≤25 years | 38 | 18.54% |

| 26–33 years | 68 | 33.17% | |

| 34–49 years | 88 | 42.92% | |

| ≥50 years | 11 | 5.36% | |

| Marital status | Married | 145 | 70.73% |

| Unmarried | 60 | 29.27% | |

| Education Level | No Education | 12 | 5.85% |

| SSC | 9 | 4.39% | |

| HSC | 29 | 14.14% | |

| Graduate | 93 | 45.36% | |

| Postgraduate | 62 | 30.24% | |

| Occupation | Private Service | 61 | 29.76% |

| Government service | 25 | 12.19% | |

| Business | 100 | 48.78% | |

| Housewife | 7 | 3.41% | |

| Student/unemployed | 13 | 6.34% |

| Construct | No. of Items | Indicators | Loadings | Composite Reliability | Average Variance Extracted (AVE) | |

|---|---|---|---|---|---|---|

| Accessibility | 5 | Acces_1 | NBFIs have enough seats | 0.562 | 0.844 | 0.520 |

| Acces_2 | Moving inside is easy and comfortable | 0.658 | ||||

| Acces_3 | The location is suitable to access | 0.809 | ||||

| Acces_4 | NBFIs have an easy parking area | 0.759 | ||||

| Acces_5 | Office and transaction hours are suitable | 0.797 | ||||

| Assurance | 5 | Assu_1 | NBFIs’ employees provide trustworthy, consistent and efficient service to clients | 0.771 | 0.866 | 0.620 |

| Assu_2 | NBFIs ensure a complete and safe transaction | 0.762 | ||||

| Assu_3 | NBFIs’ staff courteously talk with their customers | 0.798 | ||||

| Assu_4 | Staff have sufficient expertise to answer customers’ questions | 0.809 | ||||

| Assu_5 | Bank employees’ information is clear and comprehensible | 0.135 * | ||||

| Empathy | 5 | Emp_1 | The employees of NBFIs give special attention to the customer | 0.846 | 0.849 | 0.660 |

| Emp_2 | Staff offer customers guidance and suggestions | 0.919 | ||||

| Emp_3 | Employees understand the clients’ needs | 0.641 | ||||

| Emp_4 | NBFIs have my best interests at heart | 0.267 * | ||||

| Emp_5 | NBFIs give me individual attention | −0.1 * | ||||

| Reliability | 5 | Rel_1 | NBFIs are genuine in solving claims | 0.741 | 0.842 | 0.640 |

| Rel_2 | NBFIs complete service at the promised time | 0.788 | ||||

| Rel_3 | Clients’ records always come free of errors | 0.868 | ||||

| Rel_4 | The NBFI periodically sends financial records to my current address to inform balance | 0.088 * | ||||

| Rel_5 | The staff of the NBFI is deeply concerned about the settlement of my bank-related issues | 0.12 * | ||||

| Responsive-ness | 5 | Resp_1 | Clients are always informed when their service is done spontaneously | 0.879 | 0.896 | 0.740 |

| Resp_2 | NBFIs are always ready to keep requests | 0.853 | ||||

| Resp_3 | Employees serve the client without delay or hesitation | 0.852 | ||||

| Resp_4 | Staff at the bank answer my requests quickly | 0.037 * | ||||

| Resp_5 | Bank staff adjust any mistakes rapidly | −0.03 * | ||||

| Tangibility | 6 | Trans_1 | NBFIs have modern equipment | 0.747 | 0.831 | 0.500 |

| Trans_2 | NBFIs’ layout is nicely done | 0.622 | ||||

| Trans_3 | Employees are well dressed | 0.683 | ||||

| Trans_4 | NBFIs are neat and clean | 0.683 | ||||

| Trans_5 | NBFIs’ accounting system is good | 0.782 | ||||

| Trans_6 | Hard copies such as forms, monthly reports, flyers and transaction cards are very lucrative | 0.032 * | ||||

| Customer Satisfaction | 6 | Cus_Satis_1 | I’m satisfied with the facilities of the NBFs | 0.730 | 0.797 | 0.500 |

| Cus_Satis_2 | My NBFI meets my specifications | 0.700 | ||||

| Cus_Satis_3 | Overall, my NBFI provides good value for money | 0.437 | ||||

| Cus_Satis_4 | In comparison with others, my NBFI offers excellent service quality | 0.752 | ||||

| Cus_Satis_5 | Overall, I hold a good impression of my NBFI | 0.472 | ||||

| Cus_Satis_6 | I recommend my friends and relatives to take service from NBFIs | 0.793 | ||||

| Accessibility | Assurance | Empathy | Reliability | Responsiveness | Customer Satisfaction | Tangibility | Discriminant Validity | |

|---|---|---|---|---|---|---|---|---|

| Accessibility | 0.7240 | 0 | 0 | 0 | 0 | 0 | 0 | Yes |

| Assurance | 0.4718 | 0.7852 | 0 | 0 | 0 | 0 | 0 | Yes |

| Empathy | 0.6516 | 0.1913 | 0.8109 | 0 | 0 | 0 | 0 | Yes |

| Reliability | 0.3742 | 0.366 | 0.1880 | 0.7862 | 0 | 0 | 0 | Yes |

| Responsiveness | 0.4745 | 0.6274 | 0.1716 | 0.7177 | 0.8612 | 0 | 0 | Yes |

| Customer Satisfaction | 0.7023 | 0.6066 | 0.5202 | 0.2644 | 0.4357 | 0.7626 | 0 | Yes |

| Tangibility | 0.6202 | 0.6307 | 0.4340 | 0.2055 | 0.4540 | 0.6865 | 0.7077 | Yes |

| Path Coeffi#Cient | T Statistics | Sig. Level | p Values | 90% Confidence Interval | Result | ||

|---|---|---|---|---|---|---|---|

| H1: Reliability → CS | 0.2879 | 3.4281 | *** | 0.001 | 0.15 | 0.43 | Supported |

| H2: Tangibility → CS | 0.2054 | 2.1732 | ** | 0.032 | 0.05 | 0.36 | Supported |

| H3: Empathy → CS | 0.1285 | 1.8352 | NS | 0.069 | 0.01 | 0.24 | Not Supported |

| H4: Responsiveness → CS | 0.3248 | 3.3711 | *** | 0.001 | 0.17 | 0.48 | Supported |

| H5: Assurance → CS | 0.1776 | 2.0840 | ** | 0.040 | 0.04 | 0.32 | Supported |

| H6: Accessibility → CS | −0.0064 | 0.0723 | NS | 0.943 | −0.15 | 0.14 | Not supported |

| Collinearity: VIF (Tolerance) | f2 Effect Size | q2 Effect Size | |

|---|---|---|---|

| Accessibility | 2.551 (0.392) | 0.000 | −0.001 |

| Assurance | 2.153 (0.464) | 0.035 | 0.001 |

| Empathy | 1.823 (0.548) | 0.027 | 0.000 |

| Reliability | 2.294 (0.436) | 0.119 | 0.020 |

| Responsiveness | 3.38 (0.296) | 0.092 | 0.017 |

| Tangibility | 2.163 (0.462) | 0.047 | 0.006 |

| Customer Satisfaction | R2 = 0.705, Q2 = 0.3233 | ||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wang, C.-K.; Masukujjaman, M.; Alam, S.S.; Ahmad, I.; Lin, C.-Y.; Ho, Y.-H. The Effects of Service Quality Performance on Customer Satisfaction for Non-Banking Financial Institutions in an Emerging Economy. Int. J. Financial Stud. 2023, 11, 33. https://doi.org/10.3390/ijfs11010033

Wang C-K, Masukujjaman M, Alam SS, Ahmad I, Lin C-Y, Ho Y-H. The Effects of Service Quality Performance on Customer Satisfaction for Non-Banking Financial Institutions in an Emerging Economy. International Journal of Financial Studies. 2023; 11(1):33. https://doi.org/10.3390/ijfs11010033

Chicago/Turabian StyleWang, Cheng-Kun, Mohammad Masukujjaman, Syed Shah Alam, Ismail Ahmad, Chieh-Yu Lin, and Yi-Hui Ho. 2023. "The Effects of Service Quality Performance on Customer Satisfaction for Non-Banking Financial Institutions in an Emerging Economy" International Journal of Financial Studies 11, no. 1: 33. https://doi.org/10.3390/ijfs11010033