Maize Productivity and Household Welfare Impacts of Mobile Money Usage in Tanzania

,

,  , , ,

, , ,  and

and

Abstract

:1. Introduction

2. Methodology

2.1. Theoretical Framework

2.2. ESR Model

2.3. Data Collection

2.3.1. An Overview of VICOBA

2.3.2. An Overview of Mbeya

2.4. Variable Description and Measurement

3. Results and Discussions

3.1. Descriptive Statistics

3.2. ESR Model Diagnostics

3.3. Determinants of MM Usage Based on the ESR Model

3.4. Determinants of Maize Productivity and Poverty Likelihood Based on the ESR Model

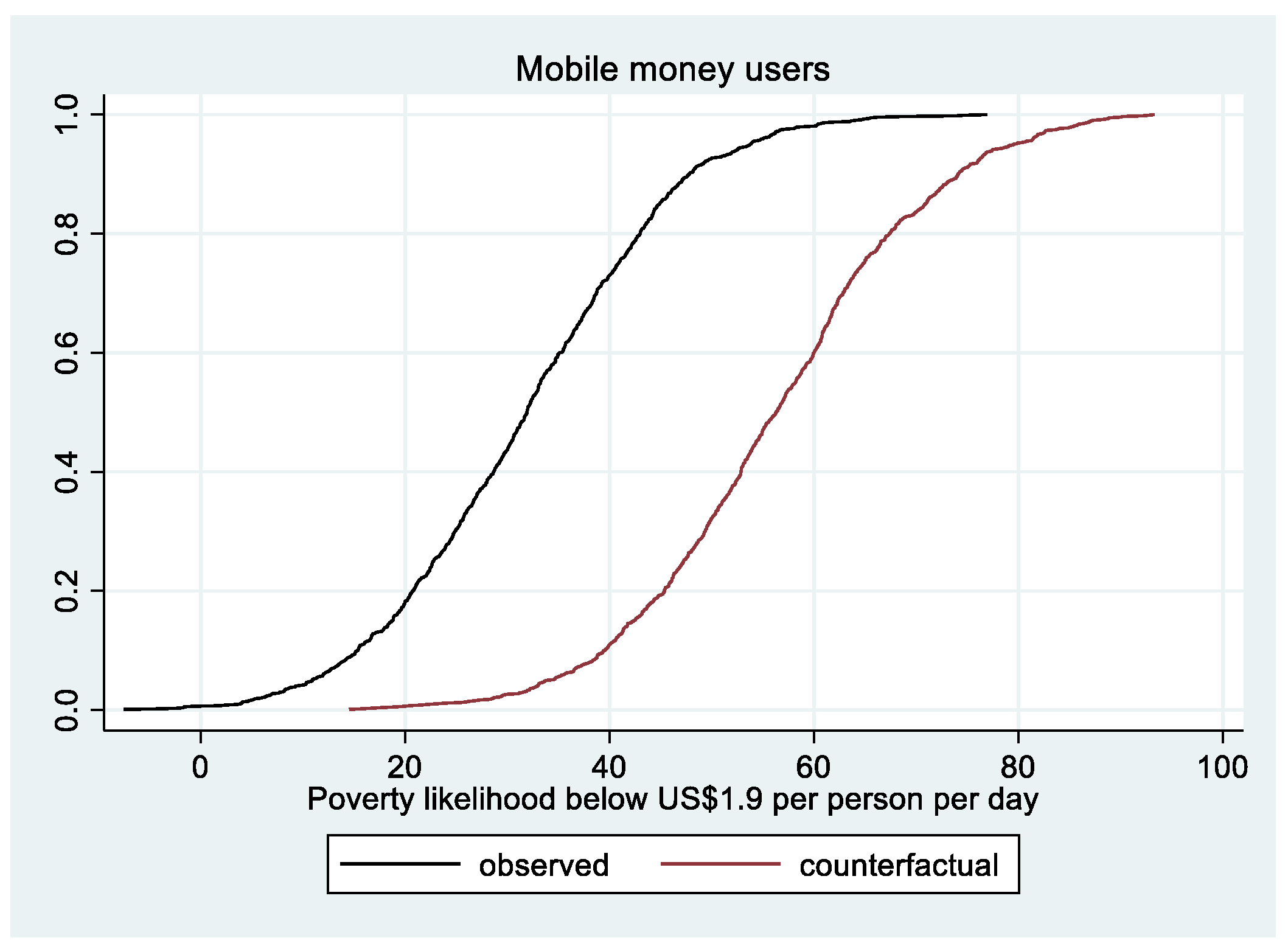

3.5. Impacts of MM Usage on Maize Productivity and Poverty Likelihood

3.6. Impacts of MM Usage by Household Type

4. Conclusions and Implications

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

| Variables | MM Usage (Equation (3)) | Maize Productivity (kg/acre) | |

|---|---|---|---|

| MM Users (Equation (4a)) | Non-Users (Equation (4b)) | ||

| Age of the head | 0.018 | 0.010 | −0.028 * |

| (0.018) | (0.013) | (0.016) | |

| Age squared | −0.000 | −0.000 | 0.000 * |

| (0.000) | (0.000) | (0.000) | |

| Household type (1 = male-headed) | 0.148 | 0.024 | 0.524 *** |

| (0.167) | (0.114) | (0.161) | |

| Education level of the head (1 = primary education) | 0.582 *** | −0.261 *** | −0.005 |

| (0.124) | (0.100) | (0.131) | |

| Marital status of the head | 0.286 | −0.168 | −0.395 ** |

| (0.187) | (0.134) | (0.179) | |

| Household size | 0.004 | −0.010 | −0.002 |

| (0.026) | (0.017) | (0.026) | |

| Total land holdings (acres) | −0.027 *** | 0.005 | −0.003 |

| (0.009) | (0.006) | (0.010) | |

| TLU | 0.035 | 0.000 | 0.017 |

| (0.024) | (0.012) | (0.027) | |

| Television ownership (1 = yes) | 0.490 *** | 0.039 | 0.151 |

| (0.112) | (0.062) | (0.170) | |

| Credit access (1 = yes) | 0.223 ** | −0.102 * | −0.064 |

| (0.094) | (0.059) | (0.108) | |

| Extension access (1 = yes) | −0.123 | 0.079 | 0.057 |

| (0.083) | (0.055) | (0.084) | |

| Group membership (1 = yes) | 0.109 | 0.072 | 0.248 * |

| (0.121) | (0.075) | (0.136) | |

| Access to irrigation water (1 = yes) | −0.025 | 0.044 | 0.021 |

| (0.091) | (0.060) | (0.093) | |

| Access to tractor (1 = yes) | 0.207 ** | 0.014 | −0.110 |

| (0.094) | (0.060) | (0.111) | |

| Access to input shop (1 = yes) | −0.305 *** | −0.094 | −0.160 |

| (0.097) | (0.066) | (0.106) | |

| Access to output buyers (1 = yes) | −0.071 | 0.111 * | −0.086 |

| (0.091) | (0.061) | (0.090) | |

| Period of membership in VICOBA (months) | 0.016 | 0.025 * | 0.034 |

| (0.021) | (0.013) | (0.023) | |

| Wealth status (share proportion in VICOBA) | 0.222 | 0.148 | 0.292 |

| (0.212) | (0.129) | (0.237) | |

| Social networks in VICOBA | 0.216 *** | ||

| (0.077) | |||

| Constant | −0.635 | 6.520 *** | 6.655 *** |

| (0.453) | (0.321) | (0.437) | |

| −0.213 *** | |||

| (0.031) | |||

| −0.356 *** | |||

| (0.037) | |||

| −1.330 *** | |||

| (0.119) | |||

| 0.019 | |||

| (0.342) | |||

| LR test of independent equations | 32.62 | ||

| Prob. > chi2 | (0.000) | ||

| Observations | 1310 | 1310 | 1310 |

| Variables | MM Usage (Equation (3)) | Poverty Likelihood USD 1.9 per Capita per Day | |

|---|---|---|---|

| MM Users (Equation (4a)) | Non-Users (Equation (4b)) | ||

| Age of the head | 0.026 | 0.584 ** | −0.518 |

| (0.019) | (0.254) | (0.444) | |

| Age square | −0.000 * | −0.007 *** | 0.003 |

| (0.000) | (0.003) | (0.005) | |

| Household type (1 = male-headed) | 0.131 | −1.335 | −13.755 *** |

| (0.176) | (2.107) | (4.343) | |

| Marital status of the head (1 = married) | 0.320 | −3.157 | 5.021 |

| (0.195) | (2.522) | (4.591) | |

| Education level of the head (1 = primary education) | 0.637 *** | −4.377 ** | −4.290 |

| (0.125) | (2.050) | (3.186) | |

| Total land holdings (acres) | −0.022 ** | −0.394 *** | −0.741 *** |

| (0.010) | (0.118) | (0.255) | |

| TLU | 0.030 | −0.043 | 0.485 |

| (0.026) | (0.206) | (0.695) | |

| Household size | −0.022 | 5.750 *** | 6.748 *** |

| (0.028) | (0.324) | (0.694) | |

| Dependency ratio | 0.014 | 8.962 *** | 5.387 *** |

| (0.063) | (0.741) | (1.523) | |

| Credit access (1 = yes) | 0.272 *** | −5.315 *** | −1.632 |

| (0.098) | (1.079) | (2.803) | |

| Tractor access (1 = yes) | 0.294 *** | −1.126 | 5.522 * |

| (0.100) | (1.105) | (2.965) | |

| Group membership (1 = yes) | 0.167 | −0.536 | −1.196 |

| (0.126) | (1.338) | (3.565) | |

| Access to irrigation water (1 = yes) | −0.029 | −0.872 | −2.370 |

| (0.096) | (1.097) | (2.439) | |

| Access to output buyers (1 = yes) | −0.012 | 3.010 *** | 0.950 |

| (0.096) | (0.992) | (2.321) | |

| Period of membership in VICOBA (months) | 0.022 | −0.334 | −0.332 |

| (0.021) | (0.233) | (0.595) | |

| Share proportions in VICOBA | 0.346 | −0.293 | −2.593 |

| (0.220) | (2.328) | (6.168) | |

| Social networks in VICOBA | 0.348 *** | −2.266 * | 3.758 |

| (0.093) | (1.218) | (2.547) | |

| Access to input shops (=yes) | −0.379 *** | ||

| (0.097) | |||

| Constant | −0.751 | −37.672 *** | 18.217 |

| (0.607) | (7.929) | (14.074) | |

| 2.623 *** | |||

| (0.024) | |||

| 2.966 *** | |||

| (0.085) | |||

| −0.124 | |||

| (0.143) | |||

| 0.508 ** | |||

| (0.254) | |||

| LR test of independent equations. | 3.01 | ||

| Prob. > chi2 | (0.0826) | ||

| Observations | 1310 | 1310 | 1310 |

References

- Abiona, Olukorede, and Martin Foureaux Koppensteiner. 2020. Financial Inclusion, Shocks and Poverty: Evidence from the Expansion of Mobile Money in Tanzania. Journal of Human Resources 57: 1–63. [Google Scholar] [CrossRef] [Green Version]

- Adams, Richard H., and Alfredo Cuecuecha. 2013. The Impact of Remittances on Investment and Poverty In Ghana. World Development 50: 24–40. [Google Scholar] [CrossRef]

- Ahlén, Marie. 2012. Rural Member-Based Microfinance Institutions: A Field Study Assessing the Impacts of SACCOS and VICOBA in Babati District, Tanzania. A Thesis Submitted to the School of Life Sciences, Södertörn University in Partial Fulfilment of the Requirements of a B.Sc. Degree, School of Life Sciences Bachelor’s Thesis 15 ECTS, Spring Semester 2012 Environment and Development Educational Programme. Available online: https://www.diva-portal.org/smash/get/diva2:544512/FULLTEXT01.pdfLoiske (accessed on 22 January 2023).

- Amoah, Anthony, Kofi Korle, and Rexford Kweku Asiama. 2020. Mobile Money as a Financial Inclusion Instrument: What Are the Determinants? International Journal of Social Economics 47: 1283–97. [Google Scholar] [CrossRef]

- Andrianaivo, Mihasonirina, and Kangni Kpodar. 2012. Mobile Phones, Financial Inclusion, and Growth. Review of Economics and Institutions 3: 30. [Google Scholar] [CrossRef] [Green Version]

- Arnold, Julia, and Sarah Gammage. 2019. Gender and Financial Inclusion: The Critical Role for Holistic Programming. Development in Practice 29: 965–73. [Google Scholar] [CrossRef]

- Bank of Tanzania. 2021. Financial Sector Supervision Annual Report 2021 25th Edition. Available online: https://www.bot.go.tz/Publications/Filter/41 (accessed on 23 January 2023).

- Bao, Weining, Jian Ni, and Shubhranshu Singh. 2018. Informal Lending in Emerging Markets. Marketing Science 37: 123–37. [Google Scholar] [CrossRef]

- Batista, Catia, and Pedro C. Vicente. 2020. Improving Access to Savings through Mobile Money: Experimental Evidence from African Smallholder Farmers. World Development 129: 104905. [Google Scholar] [CrossRef] [Green Version]

- Boamah, Emmanuel Frimpong, and Nadine S. Murshid. 2019. Techno-Market Fix? Decoding Wealth through Mobile Money in the Global South. Geoforum 106: 253–62. [Google Scholar] [CrossRef]

- Bongomin, George Okello Candiya, Francis Yosa, Joseph Baleke Yiga Lubega, Pierre Yourougou, and Alain Manzi Amani. 2021. Financial Intermediation by Microfinance Banks in Rural Sub-Saharan Africa: Financial Intermediation Theoretical Approach. Journal of Comparative International Management 24: 2. [Google Scholar] [CrossRef]

- Chale, Patricia, and Ulingeta Mbamba. 2014. The Role of Mobile Money Services on Growth of Small and Medium Enterprises in Tanzania. Evidence from Kinondoni District in Dar es Salaam. Business Management Review 17: 81–89. [Google Scholar]

- Chamboko, Richard. 2022. On the Role of Gender and Age in the Use of Digital Financial Services in Zimbabwe. International Journal of Financial Studies 10: 82. [Google Scholar] [CrossRef]

- Demirgüç-Kunt, Asli, Leora F. Klapper, and Dorothe Singer. 2013. Financial Inclusion and Legal Discrimination against Women: Evidence from Developing Countries. World Bank Policy Research Working Paper 6416. Washington, DC: World Bank. [Google Scholar]

- Demirgüç-Kunt, Asli, Leora F. Klapper, Dorothe Singer, and Peter Van Oudheusden. 2017. The Global Findex Database 2014: Measuring Financial Inclusion around the World. World Bank Policy Research Working Paper 7255. Washington, DC: The World Bank. [Google Scholar]

- Desiere, Sam, Wytse Vellema, and Marijke D’Haese. 2015. A Validity Assessment of the Progress Out of Poverty Index (PPI) TM. Evaluation and Program Planning 49: 10–18. [Google Scholar] [CrossRef] [PubMed]

- Di Falco, Salvatore, Marcella Veronesi, and Mahmud Yesuf. 2011. Does Adaptation to Climate Change Provide Food Security? A Micro-Perspective from Ethiopia. American Journal of Agricultural Economics 93: 829–46. [Google Scholar] [CrossRef] [Green Version]

- Donovan, K. 2012. Mobile Money for Financial Inclusion. In Information and Communications for Development (pp. 61–73). Available online: https://elibrary.worldbank.org/doi/abs/10.1596/9780821389911_ch04 (accessed on 23 January 2023).

- Duvendack, Maren, and Philip Mader. 2019. Impact of financial inclusion in low and middle-income countries: A systematic review of reviews. Campbell Systematic Reviews 15: e1012. [Google Scholar] [CrossRef] [Green Version]

- Eckhoff, Sarah, Grace Majara Kibombo, Melch Muhame Natukunda, Christian Pennotti, and Karen Vandergaag. 2019. What Works to Increase Financial Inclusion and Women’s Financial Autonomy? Intentional Designs Showing Promise. Development in Practice 29: 974–87. [Google Scholar] [CrossRef]

- Economides, Nicholas, and Przemyslaw Jeziorski. 2017. Mobile Money in Tanzania. Marketing Science 36: 815–37. [Google Scholar] [CrossRef]

- Fanta, Ashenafi Beyene, Kingstone Mutsonziwa, Roelof Goosen, Matthew Emanuel, and Nikki Kettles. 2016. The Role of Mobile Money in Financial Inclusion in the SADC Region: Evidence Using FinScope Surveys. Available online: https://www.researchgate.net/profile/Ashenafi_Fanta/publication/311576448_The_role_of_mobile_money_in_financial_inclusion_in_the_SADC_region (accessed on 23 January 2023).

- FITS. 2013. Mobile Money in Tanzania Use, Barriers and Opportunities. Washington, DC: InterMedia. [Google Scholar]

- FSDT. 2017. Finscope Tanzania: Insight that Drive Innovation. Available online: https://www.fsdt.or.tz/wp-content/uploads/2017/09/Finscope.pdf (accessed on 21 August 2022).

- Greene, William H. 2003. Econometric Analysis. New York: Prentice Hall. [Google Scholar]

- Hamdan, Jana S., Katharina Lehmann-Uschner, and Lukas Menkhoff. 2021. Mobile Money, Financial Inclusion, and Unmet Opportunities. Evidence from Uganda. Journal of Development Studies 58: 671–91. [Google Scholar] [CrossRef]

- Heckman, James J. 1979. Statistical Models for Discrete Panel Data. Chicago: Department of Economics and Graduate School of Business, the University of Chicago, p. 81. [Google Scholar]

- Hussain, A. H. M. Belayeth, Noraida Endut, Sumonkanti Das, Mohammed Thanvir Ahmed Chowdhury, Nadia Haque, Sumena Sultana, and Khandaker Jafor Ahmed. 2019. Does Financial Inclusion Increase Financial Resilience? Evidence from Bangladesh. Development in Practice 29: 798–807. [Google Scholar] [CrossRef]

- IOM. 2014. Mobile Money Services: A Bank in Your Pocket. ACPOBS/2014/BN13. Available online: https://publications.iom.int/system/files/pdf/mobile_money.pdf (accessed on 18 October 2022).

- Issahaku, Haruna, Benjamin Musah Abu, and Paul Kwame Nkegbe. 2018. Does the Use of Mobile Phones by Smallholder Maize Farmers Affect Productivity in Ghana? Journal of African Business 19: 302–22. [Google Scholar] [CrossRef]

- Jack, William, and Tavneet Suri. 2014. Risk Sharing and Transactions Costs: Evidence from Kenya’s Mobile Money Revolution. The American Economic Review 104: 183–223. [Google Scholar] [CrossRef]

- Kast, Felipe, Stephan Meier, and Dina Pomeranz. 2018. Saving More in Groups: Field Experimental Evidence from Chile. Journal of Development Economics 133: 275–94. [Google Scholar] [CrossRef] [Green Version]

- Kiconco, Rebecca I., Gerrit Rooks, and Chris Snijders. 2020. Learning Mobile Money in Social Networks: Comparing a Rural and Urban Region in Uganda. Computers in Human Behavior 103: 214–25. [Google Scholar] [CrossRef]

- Kikulwe, Enoch M., Elisabeth Fischer, and Matin Qaim. 2014. Mobile Money, Smallholder Farmers, and Poverty in Kenya. PLoS ONE 9: e109804. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Kim, Kyungha. 2021. Assessing the Impact of Mobile Money on Improving the Financial Inclusion of Nairobi Women. Journal of Gender Studies 31: 306–22. [Google Scholar] [CrossRef]

- Kirui, Oliver K., Julius J. Okello, Rose A. Nyikal, and Georgina W. Njiraini. 2013. Impact of Mobile Phone-Based Money Transfer Services in Agriculture: Evidence from Kenya. Quarterly Journal of International Agriculture 52: 141–62. [Google Scholar]

- Kumar, Rishi, and D. C. Pathak. 2022. Financial Awareness: A Bridge to Financial Inclusion. Development in Practice 32: 968–80. [Google Scholar] [CrossRef]

- Lado Haule, Alice. 2015. Contribution of Village Community Banks in Household Rice Production: A Case of Morogoro District. A Dissertation Submitted to the Institute of Development Studies in Partial Fulfillment of the Requirements for the Award of the Master of Science in Development Policy (MSc. DP) Degree of Mzumbe University. Available online: http://scholar.mzumbe.ac.tz/bitstream/handle/11192/946/MSc_DP_Alice%20lado%20Haule_2015.pdf?sequence=1 (accessed on 22 January 2023).

- Lee, Lung-Fei, and Robert P. Trost. 1978. Estimation of Some Limited Dependent Variable Models with Application to Housing Demand. Journal of Econometrics 8: 357–82. [Google Scholar] [CrossRef] [Green Version]

- Lee, Lung-Fei. 1982. Some Approaches to the Correction of Selectivity Bias. The Review of Economic Studies 49: 355–72. [Google Scholar] [CrossRef] [Green Version]

- Lokshin, Michael, and Zurab Sajaia. 2004. Maximum Likelihood Estimation of Endogenous Switching Regression Models. Stata Journal 4: 282–89. [Google Scholar] [CrossRef] [Green Version]

- Maddala, Gangadharrao S. 1983. Limited Dependent and Qualitative Variables in Econometrics. Cambridge: Cambridge University Press. [Google Scholar]

- Maddala, Gangadharrao S. 1986. Disequilibrum, Self-Selection and Switching Models. In Handbook of Econometrics, 1st ed. Edited by Zvi Griliches and Michael D. Intriligator. Edmonton: Elsevier, vol. 3, Chapter 28. pp. 1633–88. [Google Scholar]

- Mahmoud, Zeinab. 2019. Determinants of Mobile Money Adoption. Paper presented at the 2nd Europe-Middle East-North African Regional Conference of the International Telecommunications Society (ITS): “Leveraging Technologies for Growth”, Aswan, Egypt, February 18–21; Calgary and Edmonton: International Telecommunications Society (ITS). Available online: http://hdl.handle.net/10419/201742 (accessed on 20 August 2022).

- Manda, Julius, Arega D. Alene, Adane H. Tufa, Tahirou Abdoulaye, Tesfamicheal Wossen, David Chikoye, and Victor Manyong. 2019. The Poverty Impacts of Improved Cowpea Varieties in Nigeria: A Counterfactual Analysis. World Development 122: 261–71. [Google Scholar] [CrossRef]

- Motta, Victor, and Lauro Emilio Gonzalez Farias. 2022. Determinants of Financial Inclusion In Latin America And The Caribbean. Development in Practice 32: 1063–77. [Google Scholar] [CrossRef]

- Mukong, Alfred Kechia, and Lwanga Elizabeth Nanziri. 2021. Social Networks and Technology Adoption: Evidence from Mobile Money in Uganda. Cogent Economics and Finance 9: 1913857. [Google Scholar] [CrossRef]

- Munyegera, Ggombe Kasim, and Tomoya Matsumoto. 2016. Mobile Money, Remittances, and Poverty: Panel Evidence from Rural Uganda. World Development 79: 127–37. [Google Scholar] [CrossRef]

- Munyegera, Ggombe Kasim, and Tomoya Matsumoto. 2018. ICT For Financial Access: Mobile Money and The Financial Behavior of Rural Households in Uganda. Review of Development Economics 22: 45–66. [Google Scholar] [CrossRef]

- Murendo, Conrad, and Meike Wollni. 2016. Mobile Money and Household Food Security in Uganda. Global Food Discussion Papers, No. 76, Georg-August-Universität Göttingen, Research Training Group (RTG) 1666–Global Food, Göttingen. Available online: http://hdl.handle.net/10419/126092 (accessed on 4 July 2022).

- Murendo, Conrad, Meike Wollni, Alan De Brauw, and Nicholas Mugabi. 2018. Social Network Effects on Mobile Money Adoption in Uganda. The Journal of Development Studies 54: 327–42. [Google Scholar] [CrossRef] [Green Version]

- Mwalupaso, Gershom Endelani, Shangao Wang, Sanzidur Rahman, Essiagnon John-Philippe Alavo, and Xu Tian. 2019. Agricultural Informatization and Technical Efficiency in Maize Production in Zambia. Sustainability 11: 2451. [Google Scholar] [CrossRef] [Green Version]

- NBS (National Bureau of Statistics). 2021. National Sample Census of Agriculture 2019/20. Available online: https://www.nbs.go.tz/nbs/takwimu/Agriculture/2019-20_Agri_Census_Main_Report.pdf (accessed on 24 January 2023).

- N’dri, Lasme Mathieu, and Makoto Kakinaka. 2020. Financial Inclusion, Mobile Money, and Individual Welfare: The Case of Burkina Faso. Telecommunications Policy 44: 101926. [Google Scholar] [CrossRef]

- Okello, George, Joseph M. Ntayi, John C. Munene, and Charles Akol Malinga. 2018. Mobile Money and Financial Inclusion in Sub-Saharan Africa: The Moderating Role of Social Networks. Journal of African Business 19: 361–84. [Google Scholar] [CrossRef]

- Ouma, Shem Alfred, Teresa Maureen Odongo, and Maureen Were. 2017. Mobile Financial Services and Financial Inclusion: Is It a Boon for Savings Mobilization? Review of Development Finance 7: 29–35. [Google Scholar] [CrossRef]

- Parlasca, Martin C., Constantin Johnen, and Matin Qaim. 2022. Use of Mobile Financial Services among African Farmers: Insights from Kenya. Global Food Security 32: 100590. [Google Scholar] [CrossRef]

- Peprah, James Atta, Clement Oteng, and Joshua Sebu. 2020. Mobile Money, Output and Welfare among Smallholder Farmers in Ghana. SAGE Open 10: 2158244020931114. [Google Scholar] [CrossRef]

- Schaner, Simone. 2016. The Persistent Power of Behavioral Change: Long-Run Impacts of Temporary Savings Subsidies for the Poor. NBER Working Paper 22534. Cambridge: National Bureau of Economic Research. [Google Scholar]

- Schreiner, Mark. 2016. Simple Poverty Scorecard® Poverty-Assessment Tool Tanzania. June. Available online: https://www.povertyindex.org/country/tanzania (accessed on 7 February 2022).

- SEDIT (Social and Economic Development Initiatives of Tanzania). 2023. Structure, Principles and Operation System of VICOBA Lending Scheme. Available online: https://www.seditvicoba.or.tz/about.php (accessed on 19 January 2023).

- Seetharam, Balachandran, and Drew Johnson. 2015. Mobile Money’s Impact on Tanzanian Agriculture. IEEE Software 32: 29–34. [Google Scholar] [CrossRef]

- Sekabira, Haruna, and Matin Qaim. 2017a. Mobile Money, Agricultural Marketing, and Off-Farm Income in Uganda. Agricultural Economics 48: 597–611. [Google Scholar] [CrossRef]

- Sekabira, Haruna, and Matin Qaim. 2017b. Can Mobile Phones Improve Gender Equality and Nutrition? Panel Data Evidence from Farm Households in Uganda. Food Policy 73: 95–103. [Google Scholar] [CrossRef]

- Shiferaw, Bekele, Menale Kassie, Moti Jaleta, and Chilot Yirga. 2014. Adoption of Improved Wheat Varieties and Impacts on Household Food Security in Ethiopia. Food Policy 44: 272–84. [Google Scholar] [CrossRef]

- Suri, Tavneet, and William Jack. 2016. The Long-Run Poverty and Gender Impacts of Mobile Money. Science 354: 1288–92. [Google Scholar] [CrossRef]

- Suri, Tavneet. 2017. Mobile Money. Annual Review of Economics 9: 497–20. [Google Scholar] [CrossRef]

- Tambo, Justice A., and Tobias Wünscher. 2017. Farmer-Led Innovations and Rural Poverty: Evidence from Ghana. Journal of Rural Studies 55: 263–74. [Google Scholar] [CrossRef]

- Tufa, Adane Hirpa, Arega D. Alene, Julius Manda, Shiferaw Feleke, Tesfamichael Wossen, M. G. Akinwale, David Chikoye, and Victor Manyong. 2021. The Poverty Impacts of Improved Soybean Technologies in Malawi. Agrekon 60: 297–316. [Google Scholar] [CrossRef]

- Tumaini, Israel N. 2016. The Impact of Mobile Money Services on the Growth of Micro, Small and Medium Enterprises in Nkasi District Council. Dissertation Submitted to the Faculty of Social Science in Partial Fulfilment for the Requirement of Award of the Degree of Master of Science in Economics of Mzumbe University. Available online: http://scholar.mzumbe.ac.tz/bitstream/handle/11192/1999/MSc_%20Economics_Israel%20Njabu%20T_2016.pdf?sequence=1 (accessed on 11 August 2022).

- URT. 2014. Basic Demographic and Socio-Economic Profile; Key Findings. The 2012 Population and Housing Census: Dar es Salaam, Tanzania: NBS and OCGS. Available online: https://www.nbs.go.tz/nbs/takwimu/census2012/Basic_Demographic_and_Socio-Economic_Profile_PopularVersion-KeyFindings_2012_PHC_EnglishVersion.pdf (accessed on 23 January 2023).

- URT. 2017. Mbeya Region Investment Opportunities. Available online: https://www.ptonline.com/articles/how-to-get-better-mfi-results (accessed on 20 January 2023).

- Van Hove, Leo, and Antoine Dubus. 2019. M-PESA and Financial Inclusion in Kenya: Of Paying Comes Saving? Sustainability 11: 568. [Google Scholar] [CrossRef] [Green Version]

- Wang, Jing, Xiaohua Yu, Kaiyu Lyu, and Jan-Henning Feil. 2022. The Impact of Mobile Finance Use on Livelihoods of Farmers in Rural China. Emerging Markets Finance and Trade 58: 2867–79. [Google Scholar] [CrossRef]

- World Bank. 2022. Financial Inclusion. Available online: https://www.worldbank.org/en/topic/financialinclusion/overview (accessed on 11 August 2022).

- Wossen, Tesfamicheal, Tahirou Abdoulaye, Arega Alene, Mekbib G. Haile, Shiferaw Feleke, Adetunji Olanrewaju, and Victor Manyong. 2017. Impacts of extension access and cooperative membership on technology adoption and poverty. Journal of Rural Studies 54: 223–33. [Google Scholar] [CrossRef] [PubMed]

- Yao, Becatien, and Aleksan Shanoyan. 2018. The Use of Mobile Money Application and Smallholder Farmer Market Participation: Evidence from Cote d Ivoire and Tanzania. Paper Presented at the Conference of the International Association of Agricultural Economics (IAAE), Vancouver, BC, Canada, July 28–August 2. [Google Scholar]

| Variable Description | Total | MM Users | Non-Users of MM | Mean Differences |

|---|---|---|---|---|

| Number of households | 1310 | 945 | 365 | |

| Natural log of maize productivity | 6.476 | 6.532 | 6.330 | 0.202 *** |

| (0.796) | (0.783) | (0.813) | [0.050] | |

| PPI score | 43.92 | 45.32 | 40.32 | 5.002 *** |

| (11.05) | (10.38) | (11.89) | [0.708] | |

| Age of household head | 44.02 | 43.19 | 46.19 | −3.000 *** |

| (12.57) | (11.94) | (13.85) | [0.823] | |

| Household type (1 = male-headed) | 0.889 | 0.906 | 0.844 | 0.062 *** |

| (0.315) | (0.292) | (0.364) | [0.021] | |

| Marital status (1 = married) | 0.921 | 0.939 | 0.877 | 0.062 *** |

| (0.269) | (0.240) | (0.329) | [0.019] | |

| Literacy level of household head (1 = able to read and write) | 0.892 | 0.935 | 0.778 | 0.157 *** |

| (0.311) | (0.246) | (0.416) | [0.023] | |

| Total household landholdings (acre) | 4.532 | 4.441 | 4.768 | −0.327 |

| (4.457) | (4.347) | (4.727) | [0.285] | |

| Tropical Livestock Units (TLU) | 1.173 | 1.229 | 1.030 | 0.199 * |

| (2.174) | (2.351) | (1.625) | [0.114] | |

| Television ownership (1 = yes) | 0.224 | 0.279 | 0.0795 | 0.200 *** |

| (0.417) | (0.449) | (0.271) | [0.020] | |

| Household size | 5.103 | 5.126 | 5.044 | 0.082 |

| (1.594) | (1.575) | (1.642) | [0.100] | |

| Dependency ratio (natural log of dep. ratio) | 4.473 | 4.468 | 4.487 | −0.019 |

| (0.662) | (0.647) | (0.698) | [0.042] | |

| Credit access (1 = yes) | 0.238 | 0.263 | 0.173 | 0.091 *** |

| (0.426) | (0.441) | (0.378) | [0.024] | |

| Tractor access (1 = yes) | 0.388 | 0.426 | 0.288 | 0.139 *** |

| (0.487) | (0.495) | (0.453) | [0.029] | |

| Access to irrigation water (1 = yes) | 0.221 | 0.223 | 0.216 | 0.007 |

| (0.415) | (0.417) | (0.412) | [0.025] | |

| Access to input dealer (1 = yes) | 0.362 | 0.344 | 0.408 | 0.001 |

| (0.481) | (0.475) | (0.492) | [0.031] | |

| Access to output buyers (1 = yes) | 0.497 | 0.497 | 0.496 | −0.064 ** |

| (0.500) | (0.500) | (0.501) | [0.030] | |

| Group membership (1 = yes) | 0.124 | 0.139 | 0.0877 | 0.051 *** |

| (0.330) | (0.346) | (0.283) | [0.019] | |

| Period of membership in VICOBA (years) | 0.376 | 0.363 | 0.408 | 0.368 *** |

| (0.484) | (0.481) | (0.492) | [0.116] | |

| Extension access (1 = yes) | 2.779 | 2.881 | 2.514 | −0.045 |

| (2.017) | (2.089) | (1.790) | [0.030] | |

| Wealth status (share proportion in VICOBA) | 0.129 | 0.137 | 0.107 | 0.030 *** |

| (0.201) | (0.212) | (0.168) | [0.011] | |

| Social networks in VICOBA (1 = know more than half of the members in VICOBA) | 0.787 | 0.817 | 0.710 | 0.107 *** |

| (0.410) | (0.387) | (0.455) | [0.027] | |

| Chunya District (1 = yes) | 0.160 | 0.179 | 0.112 | −0.093 *** |

| (0.367) | (0.383) | (0.316) | [0.023] | |

| Ileje District (1 = yes) | 0.136 | 0.110 | 0.203 | 0.058 *** |

| (0.343) | (0.313) | (0.403) | [0.018] | |

| Mbarali District (1 = yes) | 0.118 | 0.134 | 0.0767 | −0.018 |

| (0.323) | (0.341) | (0.266) | [0.025] | |

| Mbeya District (1 = yes) | 0.192 | 0.187 | 0.205 | 0.041 ** |

| (0.394) | (0.390) | (0.405) | [0.020] | |

| Mbozi District (1 = yes) | 0.137 | 0.148 | 0.107 | −0.090 *** |

| (0.344) | (0.355) | (0.309) | [0.025] | |

| Momba District (1 = yes) | 0.165 | 0.140 | 0.230 | 0.036 ** |

| (0.371) | (0.347) | (0.421) | [0.016] | |

| Rungwe District (1 = yes) | 0.0916 | 0.102 | 0.0658 | 0.04 ** |

| (0.289) | (0.302) | (0.248) | [0.02] |

| Indicators | MM Users | MM Non-Users | Mean Differences |

|---|---|---|---|

| How many household members are 17 years old or younger? (0 = four or more, 10 = three, 15 = two, 20 = one, 30 = none) | 2.058 | 1.807 | 0.241 *** |

| (1.393) | (1.470) | [0.089] | |

| Do all children ages 6 to 17 years attend school? (0 = no, 3 = yes or no children in the household aged 6–17) | 10.69 | 10.76 | −0.098 |

| (7.449) | (7.666) | [0.468] | |

| Can the female head/spouse read and write? (6 = yes in Kiswahili, 13 = yes in English, 0 = no) | 5.899 | 4.983 | 0.944 *** |

| (1.360) | (2.467) | [0.138] | |

| What is the main building material of the floor of the main dwelling? (0 = earth, 11= concrete, cement, tiles, timber) | 7.944 | 5.956 | 2.020 *** |

| (4.930) | (5.489) | [0.329] | |

| What is the main building material of the roof of the main dwelling? (0= mud and grass, 8 = grass, leaves, bamboo, 9 = concrete, cement, galvanized corrugated iron sheets, asbestos sheets, tiles) | 8.840 | 8.624 | 0.268 *** |

| (0.603) | (1.353) | [0.085] | |

| How many bicycles, mopeds, motorcycles, tractors, or motor vehicles does your household own? (0 = none, 3 = one, 11 = two or more) | 0.707 | 0.481 | 0.223 *** |

| (0.455) | (0.500) | [0.030] | |

| Does your household own any radio or radio cassettes? (0 = no, 6 = yes) | 0.789 | 0.544 | 0.248 *** |

| (0.408) | (0.499) | [0.029] | |

| Does your household own any lanterns? (0 = no, 6 = yes) | 5.007 | 4.740 | 0.267 * |

| (2.231) | (2.447) | [0.148] | |

| Does your household own any irons (charcoal or electric)? (0 = no, 5 = yes) | 0.451 | 0.218 | 0.233 *** |

| (0.498) | (0.414) | [0.027] | |

| How many tables does your household own? (0 = none, 2 = one, 4 = two, 6 = three or more) | 3.007 | 2.392 | 0.628 *** |

| (1.463) | (1.447) | [0.090] | |

| PPI score | 45.40 | 40.51 | 5.002 *** |

| (10.24) | (11.75) | [0.708] | |

| Poverty likelihood (USD 1.9/person/day) | 31.81 | 40.84 | −9.264 *** |

| (18.32) | (22.01) | [1.313] |

| Outcome | MM Usage | MM Non-Usage | ATT |

|---|---|---|---|

| Maize productivity (kg/acre) | 679.85 | 555.58 | 124.27 (9.94) *** |

| Poverty likelihood (%) | 31.94 | 56.54 | −24.59 (−39.87) *** |

| MM Usage | MM Non-Usage | ATT | Mean Differences between FHHs and MHHs | |

|---|---|---|---|---|

| Maize productivity (kg/acre) | ||||

| FHH | 572.27 | 347.54 | 224.73 (7.71) *** | 115.95 (10.91) *** |

| MHH | 692.14 | 583.36 | 108.78 (8.30) *** | |

| Poverty likelihood (%) | ||||

| FHH | 28.66 | 61.19 | −32.53 (15.79) *** | −8.75 (10.70) *** |

| MHH | 32.28 | 56.05 | −23.77 (36.94) *** | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kilombele, H.; Feleke, S.; Abdoulaye, T.; Cole, S.; Sekabira, H.; Manyong, V. Maize Productivity and Household Welfare Impacts of Mobile Money Usage in Tanzania. Int. J. Financial Stud. 2023, 11, 27. https://doi.org/10.3390/ijfs11010027

Kilombele H, Feleke S, Abdoulaye T, Cole S, Sekabira H, Manyong V. Maize Productivity and Household Welfare Impacts of Mobile Money Usage in Tanzania. International Journal of Financial Studies. 2023; 11(1):27. https://doi.org/10.3390/ijfs11010027

Chicago/Turabian StyleKilombele, Happiness, Shiferaw Feleke, Tahirou Abdoulaye, Steven Cole, Haruna Sekabira, and Victor Manyong. 2023. "Maize Productivity and Household Welfare Impacts of Mobile Money Usage in Tanzania" International Journal of Financial Studies 11, no. 1: 27. https://doi.org/10.3390/ijfs11010027