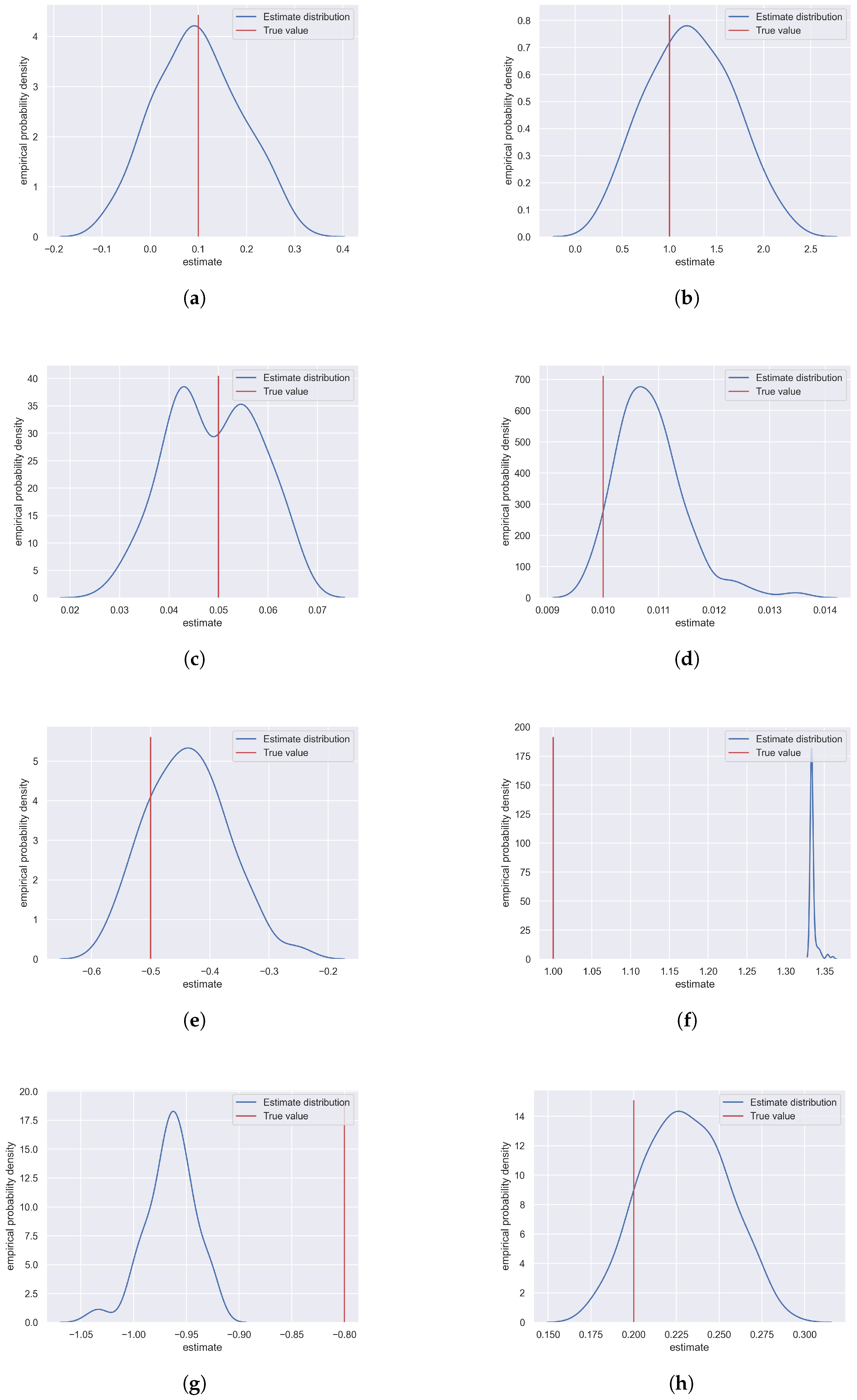

3.1.1. Estimation of

We start by finding a way to estimate the drift parameter

. First, Equation (

8) is transformed to a regression form. To this end, we introduce several additional variables. The first,

, is defined as

Let

be a series of ratios between consecutive prices of assets,

for

. Taking the above definitions into consideration, Equation (

8) can be rewritten as:

Now, let us divide both sides of this equation by

, as

is known, and at this stage, we consider

to be known too. Let us now introduce another two new variables,

as

and

as

Inserting them into Equation (

13) gives

The last expression has the form of a linear regression with

explained by

. We want to treat it with the Bayesian regression framework. To this end, we first collect all the discretised values of

and

into

n-element column vectors—

and

, respectively,

where the prime symbol is used for the transpose.

Assuming a prior distribution for

to be normal with mean

and standard deviation

, it follows from the Bayesian regression general results

O’Hagan and Kendall (

1994) that the posterior distribution for

is also normal with precision (inverse of variance)

, which can be calculated as

Here,

is the precision of the prior distribution, i.e.,

. The mean

of the posterior distribution is of the following form

where

is a classical ordinary-least-square (OLS) estimator of

, i.e.,

Hence, we can sample the realisations of

as follows:

where

i indicates the

i-th sample from the posterior distribution, which has been found for

. Having a realisation of

in form of

, we can quickly turn it into a realisation of the

parameter itself by a simple transform, inverse to Equation (

11)

3.1.2. Estimation of , , and

In order to estimate the parameters related to the volatility process, i.e.,

,

, and

, we conduct a similar exercise but this time using the volatility process. Let us first rewrite Equation (

9) as

Now, let us introduce two new parameters,

and

From Equations (

24)–(

26), we obtain

In a fashion similar to the equation for the stock price, we can rewrite this last expression as

Introducing the following vectors,

allows us to rewrite the original volatility equation in form of a linear regression

where

and

Using the formulas for Bayesian regression and assuming a multivariate (two- dimensional) normal prior for

with a mean vector

and a precision matrix

, we obtain the conjugate posterior distribution that is also multivariate normal with a precision matrix given by

and mean vector given by

where again

is a standard OLS estimator of

,

We can then use this posterior distribution of

for sampling

It is worth noting that the realisation of

appears in Equation (

39); however, we have not defined it yet. This is because the distribution of

is dependent on

, and the distribution of

is dependent on

. Hence, we suggest taking the realisation of

from the previous iteration here (which is indicated by the

subscript). We address the order of performing calculations in more detail later in this article.

Obtaining realisations of the actual parameters is very easy; one simply needs to inverse the equations defining

and

:

and

where

and

are, respectively, the first and the second component of the

vector.

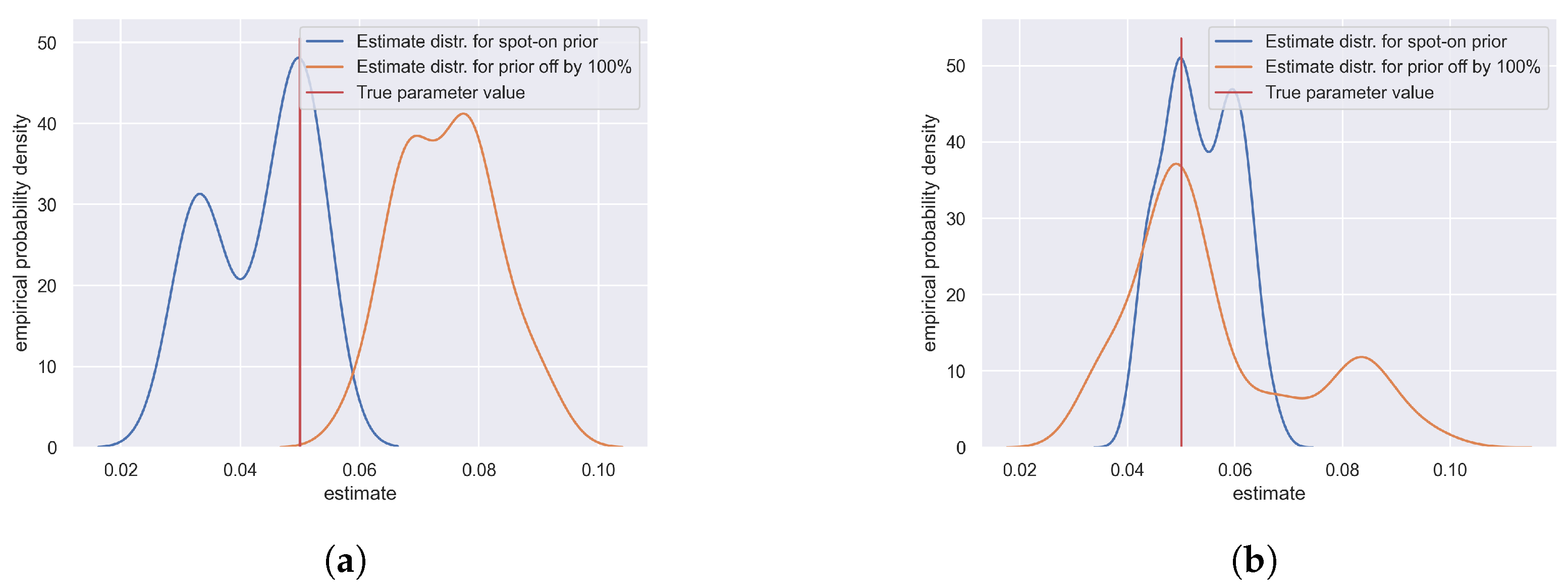

The most common approach for estimating

is assuming the inverse-gamma prior distribution for

. If the parameters of the prior distribution are

and

, then the conjugate posterior distribution is also inverse gamma

where

and

3.1.3. Estimation of

For the estimation of

, we follow an approach presented in

Jacquier et al. (

2004). We first define the residuals for the stock price equation.

and for the volatility equation,

By calculating those residuals, we try to retrieve the error terms from Equations (

1) and (2),

and

, respectively, as we know they are tied with each other by a relationship given by Equation (

10). Taking this fact into consideration, we end up with the following equation

We now introduce two new variables, traditionally called

and

. It is not difficult to deduce that the relationship between

and the newly-introduced variables

and

is

Then, Equation (

47) becomes

which is again a linear regression of

on

. Thus, we can use the exact same estimation scheme as in case of the previously described regressions. We first collect the values of

and

in two

n-element vectors:

Then we appose both vectors, forming them into an

n-by-2 matrix:

Next, we define a 2-by-2 matrix

as

If we assume a normal prior for

with mean

and precision

, the posterior distribution for

is also normal with the mean

given by

and the precision

equal to

where

,

, and

are the elements of the matrix

on positions

,

, and

respectively.

Assuming the inverse gamma prior with parameters

and

for

, the conjugate posterior distribution is also the inverse gamma with parameters

and

Thus, sampling from the posterior distribution of

can be summarised as

while when it comes to sampling from

it is

To obtain

, we simply make use of Equation (

48).

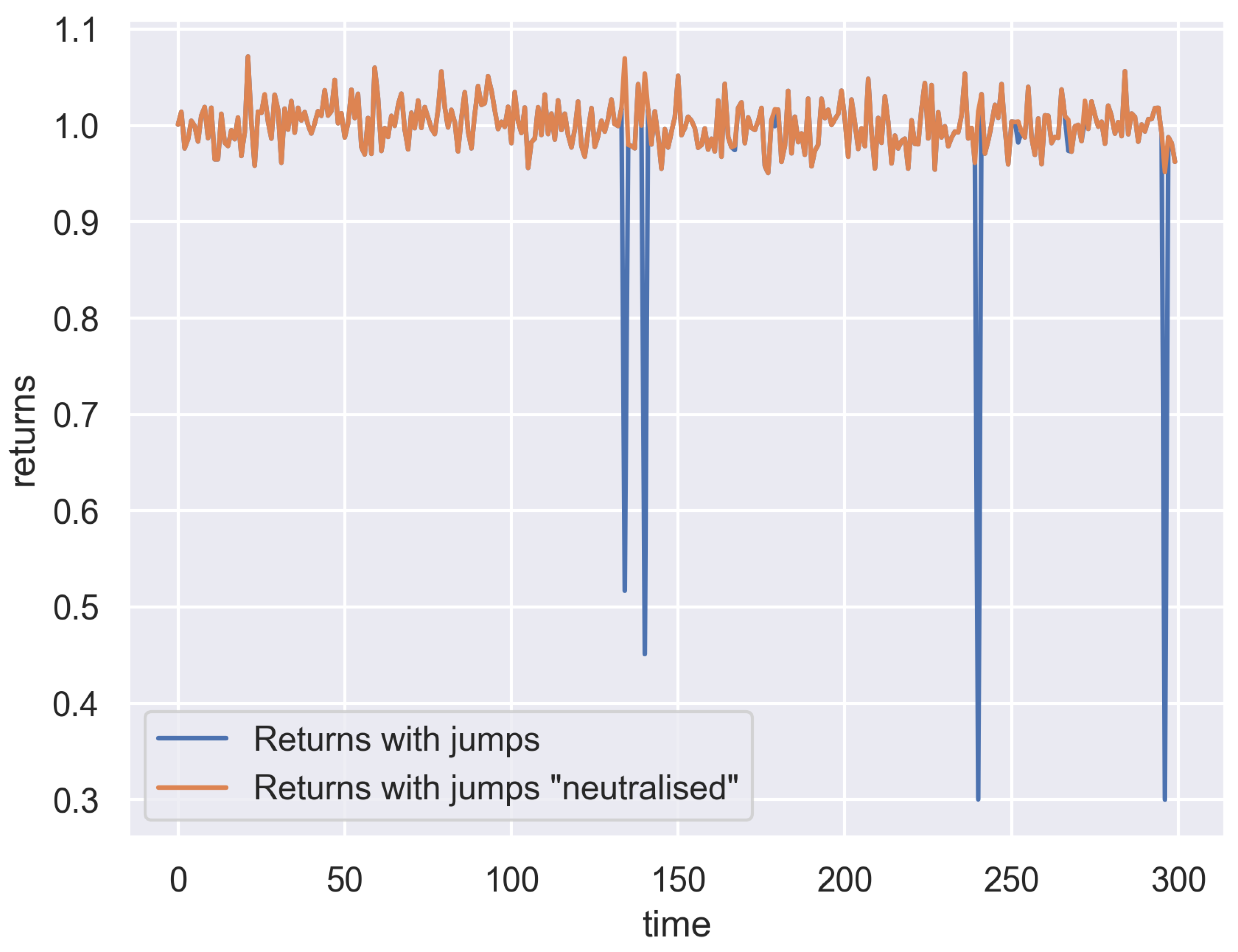

3.1.4. Estimation of —Particle Filtering

For all the estimation procedures shown in the previous sections, we assumed

to be known. However, in practice, the volatility is not a directly observable quantity, it is “hidden” in the process of prices, to which we have access. Hence, we need a way to extract the volatility from the price process, and the particle filtering methodology is extremely useful for that purpose. Here, we only sketch the outline of the particle filtering logic, namely the SIR algorithm, which we utilise to obtain the volatility estimator. For a more in-depth review of particle filtering, we suggest the works of

Johannes et al. (

2009) and

Doucet and Johansen (

2009). Here, we follow a procedure similar to the one presented in

Christoffersen et al. (

2007).

We start by fixing the number of particles

N. In each moment of time

, we produce

N particles, which represent various possible values of the volatility at that point in time. By averaging out all of those particles, we obtain an estimate of the true volatility

. The process of creating the particles is as follows: at the time

, we create

N initial particles, all with the initial value of the volatility, which we assume to be the long-term average

. Denoting each of the particles by

, for

, we have

For any subsequent moment of time, except the last one

, we define three sequences of size

N.

is a series of independent standard normal random variables

The series

contains residuals from the stock price process, where the past values of volatility are replaced by the values of the particles from the previous time step

Finally, the series

, which incorporates the possible dependency between the stock process and the volatility particles, is

Having all that, the candidates for the new particles

are created as follows

Each candidate for a particle is evaluated based on how probable it is that such a value of the volatility would generate the return that was actually observed. The measure of this probability

is a value of a normal distribution PDF function designed specifically for this purpose

1,

To be able to treat the values of the proposed measure along with the values of particles as a proper probability distribution on its own, we normalise them, so that their sum is equal to 1,

Now, we combine the particles with their respective probabilities, forming two-element vectors

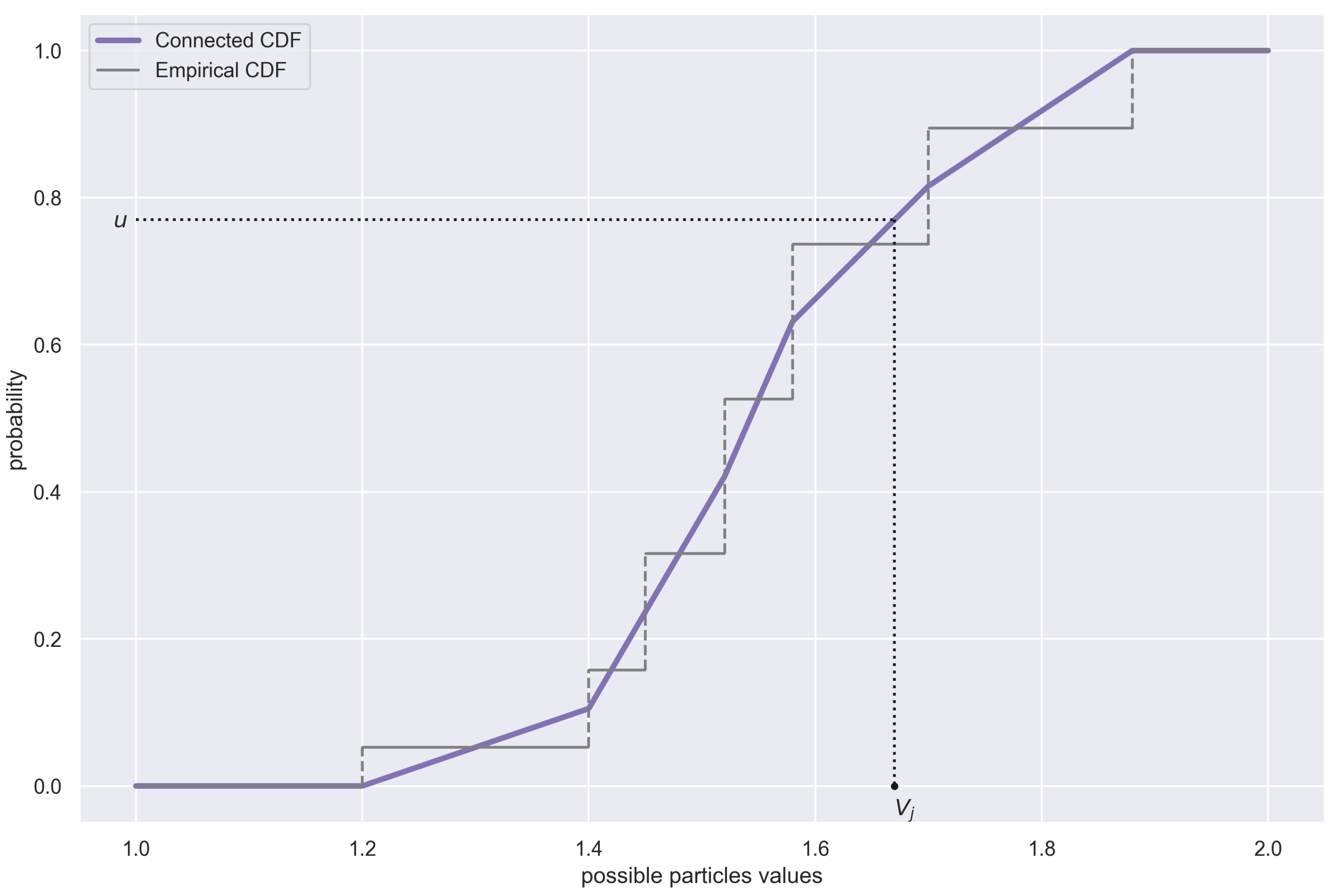

We now want to sample from the probability distribution described by to obtain the true “refined” particles. Most sources suggest drawing from it, treating it as a multinomial distribution. However, this makes all the “refined” particles have the same values as the “raw” ones, with just the proportions changed (the same “raw” particle can be drawn several times, if it has a higher probability than the others). To address this problem, we conduct the sampling in a different way. We first need to sort the values of particles in ascending order. Mathematically speaking, we create another sequence and call it , ensuring that the following conditions are all met:

The particle with the smallest value is the first in the new sequence, i.e.,

The particle with the largest value is the last in the new sequence, i.e.,

For any

, we have

We also want to keep track of the probabilities of our sorted particles; so, we order the probabilities in the same way, by defining another probability sequence

,

This step is necessary to ensure that each element of the sorted sequence of particle values

still has an original normalised probability

assigned to it. This is why it was necessary to pair up the particles and their normalised probabilities into two-element vectors, under Equation (

67). These pairs now help us approximate a continuous distribution, from which we can sample the refined particles. The “extreme” particles,

and

, will become the edges of the support of this new continuous distribution. The CDF function is given by the formula below (the time labels have been dropped for the sake of legibility, as all the variables are evaluated at

):

The formula might seem overwhelming, but there is a very easy-to-follow interpretation behind it (see

Figure 1). The new “refined” particles can be generated by drawing from the distribution given by

; the simplest way to do so is to use the inverse transform sampling.

After following the described procedure for each

, we can specify the actual estimate of the volatility process as the mean of the “refined” particles.

For , we can simply assume , which should not have any tangible negative impact on any procedure using the estimate for a sufficiently dense time discretisation grid.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}