Understanding the Effects of Social Media Marketing on Customers’ Bank Loyalty: A SEM Approach

,

,  ,

,

Abstract

:1. Introduction

2. Literature Review

2.1. Social Media Features (SMF)

2.2. Electronic Word of Mouth (EWM)

2.3. Informativeness (INF)

2.4. Customer Loyalty (CL)

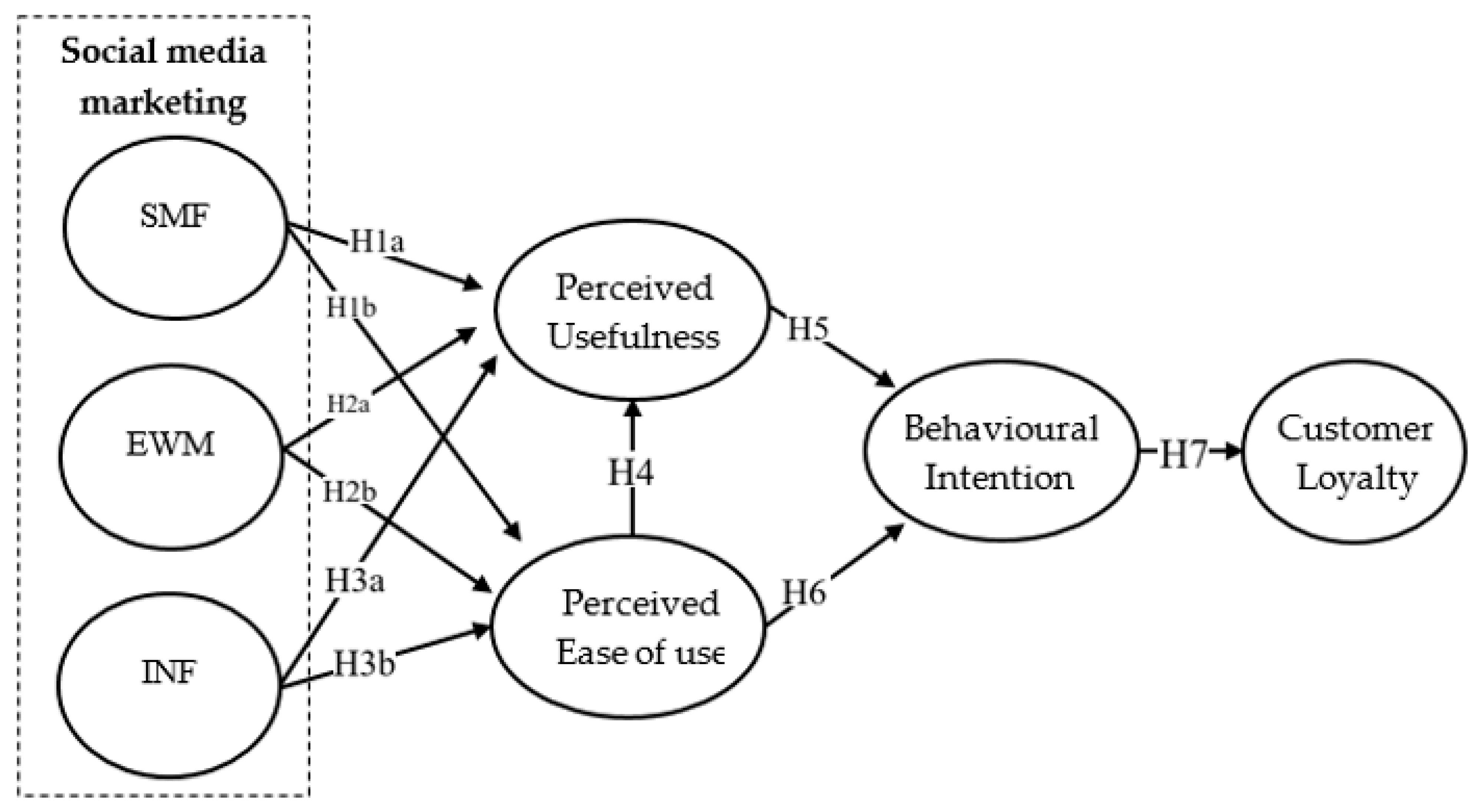

3. Hypothesis Development

4. Research Methods

4.1. TAM Model

4.2. Data Collection and Sample

4.3. Instrument and Measurement

5. Results

5.1. Descriptive Statistics

5.2. Measurement Model Test

5.3. Hypothesis Testing

6. Discussion

6.1. Theoretical Contributions and Practical Implications

6.2. Theoretical Practical Implications

7. Conclusions

Limitations and Future Research

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

| Gender: | □ Male | □ Female | … |

| Age: | □ 25–35 | □ 36–45 | □ More 45 |

| Education degree: | □ Bachelor | □ Master | □ PhD |

| Living location: | □ Urban | □ Rural | □ Bedouin (Desert) |

| Social status: | □ Single | □ Married | □ Widowed. |

| Social media features | |

| 1 | Their social media is enjoyable. |

| 2 | Their social media is pleasing. |

| 3 | Using social media can improve my shopping performance. |

| 4 | Using social media can increase my shopping productivity. |

| Word of mouth | |

| 1 | When I have the opportunity, I am willing to talk about the advantages of the bank of Jordan I have dealt with friends and relatives. |

| 2 | I encourage my friends and relatives to buy cards/accounts/loan banks of Jordan. |

| 3 | I am proud to tell my friends and relatives that I have chosen a good quality card/accounts/loan. |

| 4 | I always introduce the cards/accounts/loan bank of Jordan to everyone when possible. |

| Informativeness | |

| 1 | Social media are good sources of product information. |

| 2 | Social media supplies relevant information. |

| 3 | Social media is informative about the banks’ products. |

| Perceived ease of use | |

| 1 | The social media platforms make it easy for you to find the content you need |

| 2 | Social media platforms provide useful content. |

| 3 | The social media platforms make it easy for you to choose what you want to bank of Jordan service. |

| 4 | I find it easy to get the social media platforms to do what I want it to do. |

| Perceived usefulness | |

| 1 | Using social media platforms enhances my effectiveness on the bank of Jordan service. |

| 2 | Using social media platforms makes it easier to bank of Jordan service. |

| 3 | Using social media platforms improves my bank of Jordan service. |

| 4 | Overall, I find the social media platforms useful in my bank of Jordan service. |

| Customer loyalty | |

| 1 | I consider myself to be loyal to the bank of Jordan. |

| 2 | The bank of Jordan would be my first choice. |

| 3 | I will not buy other brands if the bank of Jordan product is available at the store. |

References

- Shankar, A.; Jebarajakirthy, C. Ashaduzzaman How do electronic word of mouth practices contribute to mobile banking adoption? J. Retail. Consum. Serv. 2019, 52, 101920. [Google Scholar] [CrossRef]

- Alghizzawi, M. A survey of the role of social media platforms in viral marketing: The influence of eWOM. Int. J. Inf. Technol. Lang. Stud. 2019, 3, 54–60. [Google Scholar]

- Cao, Y.; Qin, X.; Li, J.; Long, Q.; Hu, B. Exploring seniors’ continuance intention to use mobile social network sites in China: A cognitive-affective-conative model. Univers. Access Inf. Soc. 2020, 21, 71–92. [Google Scholar] [CrossRef]

- Milla, A.C.; Mataruna-Dos-Santos, L.J. Social Media Preferences, Interrelations Between the Social Media Characteristics and Culture: A View of Arab Nations. Asian Soc. Sci. 2019, 15, 71–77. [Google Scholar] [CrossRef]

- Lim, J.S.; Hwang, Y.; Kim, S.; Biocca, F.A. How social media engagement leads to sports channel loyalty: Mediating roles of social presence and channel commitment. Comput. Hum. Behav. 2015, 46, 158–167. [Google Scholar] [CrossRef]

- Alzahmi, A. Electronic marketing for financial services: A case study on Islamic banks in the United Arab Emirates. Int. J. Innov. Eng. Res. Technol. 2020, 7, 110–116. [Google Scholar]

- Sharma, M.; Banerjee, S.; Paul, J. Role of social media on mobile banking adoption among consumers. Technol. Forecast. Soc. Chang. 2022, 180, 121720. [Google Scholar] [CrossRef]

- Onarelly, A.K.; Tantuah, N.; Satria, H.W. The effect of social media e-marketing towards consumers shopping behavior. J. Vokasi Indones. 2018, 6, 1. [Google Scholar] [CrossRef] [Green Version]

- Evans, D.; Bratton, S.; McKee, J. Social Media Marketing; AG Printing & Publishing: Middlesex, UK, 2021. [Google Scholar]

- Urdea, A.-M.; Constantin, C.P. Exploring the impact of customer experience on customer loyalty in e-commerce. Proc. Int. Conf. Bus. Excel. 2021, 15, 672–682. [Google Scholar] [CrossRef]

- Habes, M.; Elareshi, M.; Safori, A.; Ahmad, A.K.; Al-Rahmi, W.; Cifuentes-Faura, J. Understanding Arab social TV viewers’ perceptions of virtual reality acceptance. Cogent Soc. Sci. 2023, 9, 2180145. [Google Scholar] [CrossRef]

- Al Zoubi, M.I.; Al Zoubi, A.I. An Investigation of Factors Affecting E-Marketing Customers’ Behavioral Intention to Use the Telecommunication Industry in Jordan. Int. J. Mark. Stud. 2019, 11, 125. [Google Scholar] [CrossRef]

- Husnain, M.; Akhtar, W. Relationship Marketing and Customer Loyalty: Evidence from Banking Sector in Pakistan. Glob. J. Manag. Bus. Res. 2015, 15, 1–14. [Google Scholar]

- Priansa, D.J.; Suryawardani, B. Effects of E-Marketing and Social Media Marketing on E-commerce Shopping Decisions. J. Manaj. Indones. 2020, 20, 76–82. [Google Scholar] [CrossRef]

- Singh, S. Social Media Marketing for Dummies; John Wiley & Sons: Hoboken, NJ, USA, 2010. [Google Scholar]

- Kemp, S. Digital 2021 Jordan. DataReportal—Global Digital Insights. Available online: https://datareportal.com/social-media-users (accessed on 28 November 2022).

- Ebrahim, R.S. The Role of Trust in Understanding the Impact of Social Media Marketing on Brand Equity and Brand Loyalty. J. Relatsh. Mark. 2019, 19, 287–308. [Google Scholar] [CrossRef]

- Voramontri, D.; Klieb, L. Impact of Social Media on Consumer Behaviour. Int. J. Inf. Decis. Sci. 2019, 11, 209–233. [Google Scholar] [CrossRef]

- Ramanathan, U.; Subramanian, N.; Parrott, G. Role of social media in retail network operations and marketing to enhance customer satisfaction. Int. J. Oper. Prod. Manag. 2017, 37, 105–123. [Google Scholar] [CrossRef] [Green Version]

- Jacobson, J.; Gruzd, A.; Hernández-García, Á. Social media marketing: Who is watching the watchers? J. Retail. Consum. Serv. 2020, 53, 101774. [Google Scholar] [CrossRef]

- Tashtoush, L. The Effect of Social Media on Consumer Buying Behavior in Commercial Banks. Saudi J. Bus. Manag. Stud. 2021, 6, 28–38. [Google Scholar] [CrossRef]

- Ziani, A.-K.; Elareshi, M. The impact of educated users’ interactions on social media (Facebook) in the Arab world. J. Arab. Muslim Media Res. 2018, 11, 25–44. [Google Scholar] [CrossRef]

- Sharma, B.K.; Bhatt, V.K. Impact of Social Media on Consumer Buying Behavior-A Descriptive Study on Tam Model. i-Manager’s J. Manag. 2018, 13, 34. [Google Scholar]

- Ramadani, V.; Demiri, A.; Demiri, S.S. Social media channels: The factors that influence the behavioural intention of customers. Int. J. Bus. Glob. 2014, 12, 297. [Google Scholar] [CrossRef]

- Plume, C.J.; Dwivedi, Y.K.; Slade, E.L. The New Marketing Environment. In Social Media in the Marketing Context; Elsevier: Amsterdam, The Netherlands, 2017. [Google Scholar] [CrossRef]

- Constantinides, E. Foundations of Social Media Marketing. Procedia-Soc. Behav. Sci. 2014, 148, 40–57. [Google Scholar] [CrossRef] [Green Version]

- Sarkar, S.; Khare, A. Influence of Expectation Confirmation, Network Externalities, and Flow on Use of Mobile Shopping Apps. Int. J. Hum.-Comput. Interact. 2018, 35, 1449–1460. [Google Scholar] [CrossRef]

- Schivinski, B.; Dabrowski, D. The effect of social media communication on consumer perceptions of brands. J. Mark. Commun. 2013, 22, 189–214. [Google Scholar] [CrossRef] [Green Version]

- Wilson, L. 30-Minute Social Media Marketing (SMM) Actions; Emerald Publishing Ltd.: Bingley, UK, 2019; pp. 57–71. [Google Scholar] [CrossRef]

- Permatasari, A.; Laydi, F. The effects of social media advertising on consumer purchase intention: A case study of Indonesian family start-up enterprises. Int. J. Technol. Transf. Commer. 2018, 16, 159. [Google Scholar] [CrossRef]

- Fox, G.; Longart, P. Electronic word-of-mouth: Successful communication strategies for restaurants. Tour. Hosp. Manag. 2016, 22, 211–223. [Google Scholar] [CrossRef]

- Sosanuy, W.; Siripipatthanakul, S.; Nurittamont, W.; Phayaphrom, B. Effect of electronic word of mouth (e-WOM) and perceived value on purchase intention during the COVID-19 pandemic: The case of ready-to-eat food. Int. J. Behav. Anal. 2021, 1, 1–16. [Google Scholar]

- Siagian, H.; Tarigan, Z.J.H.; Ubud, S. The effect of electronic word of mouth on online customer loyalty through perceived ease of use and information sharing. Int. J. Data Netw. Sci. 2022, 6, 1155–1168. [Google Scholar] [CrossRef]

- Nurittamont, W. Understanding service quality and service loyalty: An empirical study of mobile phone network service in the central region of Thailand. In Proceedings of the 2016 WEI International Academic Conference, Vienna, Austria, 11–13 April 2016; pp. 140–146. [Google Scholar]

- Anggraini, V.A.; Hananto, A. The Role of Social Media Marketing Activities on Customer Equity Drivers and Customer Loyalty. AFEBI Manag. Bus. Rev. 2020, 5, 1–15. [Google Scholar] [CrossRef]

- Minazzi, R. The digitization of word-of-mouth. In Social Media Marketing in Tourism and Hospitality; Springer: Berlin/Heidelberg, Germany, 2015; pp. 21–45. [Google Scholar]

- Mehrad, D.; Mohammadi, S. Word of Mouth impact on the adoption of mobile banking in Iran. Telemat. Inform. 2017, 34, 1351–1363. [Google Scholar] [CrossRef]

- Lubis, A.N.; Lumbanraja, P.; Hasibuan, B.K. Evaluation on e-marketing exposure practice to minimize the customers’ online shopping purchase regret. Cogent Bus. Manag. 2022, 9, 2016039. [Google Scholar] [CrossRef]

- Ku, Y.-C.; Wei, C.-P.; Hsiao, H.-W. To whom should I listen? Finding reputable reviewers in opinion-sharing communities. Decis. Support Syst. 2012, 53, 534–542. [Google Scholar] [CrossRef]

- Ying, Z.; Jianqiu, Z.; Akram, U.; Rasool, H. TAM Model Evidence for Online Social Commerce Purchase Intention. Inf. Resour. Manag. J. 2021, 34, 86–108. [Google Scholar] [CrossRef]

- Wu, R.; Wang, G.; Yan, L. The effects of online store informativeness and entertainment on consumers’ approach behaviors: Empirical evidence from China. Asia Pacific J. Mark. Logist. 2019, 32, 1327–1342. [Google Scholar] [CrossRef]

- Lee, J.; Hong, I.B. Predicting positive user responses to social media advertising: The roles of emotional appeal, informativeness, and creativity. Int. J. Inf. Manag. 2016, 36, 360–373. [Google Scholar] [CrossRef]

- Yadav, M.; Rahman, Z. The influence of social media marketing activities on customer loyalty: A study of e-commerce industry. Benchmarking 2018, 25, 3882–3905. [Google Scholar] [CrossRef]

- Mohd Thas Thaker, H.; Khaliq, A.; Ah Mand, A.; Iqbal Hussain, H.; Mohd Thas Thaker, M.A.B.; Allah Pitchay, A.B. Exploring the drivers of social media marketing in Malaysian Islamic banks: An analysis via smart PLS approach. J. Islam. Mark. 2020, 12, 145–165. [Google Scholar] [CrossRef]

- Kim, Y.B.; Joo, H.C.; Lee, B.G. How to forecast behavioral effects on mobile advertising in the smart environment using the technology acceptance model and web advertising effect model. KSII Trans. Internet Inf. Syst. 2016, 10, 4997–5013. [Google Scholar]

- Mahfodz, A. Factors Influencing Customer Loyalty in the e-Commerce ERA: The case Study of Pos Malaysia. Ph.D. Thesis, Asia e University, Subang Jaya, Malaysia, 2020. [Google Scholar]

- Kanyama, J.; Nurittamont, W.; Siripipatthanakul, S. Hotel service quality and its effect on customer loyalty: The case of Ubon Ratchathani, Thailand during COVID-19 Pandemic. J. Manag. Bus. Health Educ. 2022, 1, 1–20. [Google Scholar]

- Taylor, S.A.; Celuch, K.; Goodwin, S. The importance of brand equity to customer loyalty. J. Prod. Brand Manag. 2004, 13, 217–227. [Google Scholar] [CrossRef]

- Davis, F.D. Perceived Usefulness, Perceived Ease of Use, and User Acceptance of Information Technology. MIS Q. 1989, 13, 319–340. [Google Scholar] [CrossRef] [Green Version]

- Davis, F.D.; Bagozzi, R.P.; Warshaw, P.R. User acceptance of computer technology: A comparison of two theoretical models. Manag. Sci. 1989, 35, 982–1003. [Google Scholar] [CrossRef] [Green Version]

- Mulia, D.; Usman, H.; Parwanto, N.B. The role of customer intimacy in increasing Islamic bank customer loyalty in using e-banking and m-banking. J. Islam. Mark. 2020, 12, 1097–1123. [Google Scholar] [CrossRef]

- Hair, J.F., Jr.; Sarstedt, M.; Hopkins, L.; Kuppelwieser, V.G. Partial least squares structural equation modeling (PLS-SEM): An emerging tool in business research. Eur. Bus. Rev. 2014, 26, 106–121. [Google Scholar] [CrossRef]

- Hu, L.; Bentler, P.M. Fit indices in covariance structure modeling: Sensitivity to underparameterized model misspecification. Psychol. Methods 1998, 3, 424. [Google Scholar] [CrossRef]

- Lohmöller, J.B. Latent Variable Path Modeling with Partial Least Squares; Physica-Verlag: Heidelberg, Germany, 1989. [Google Scholar]

- Henseler, J. Partial least squares path modeling: Quo vadis? Qual. Quant. 2018, 52, 1–8. [Google Scholar] [CrossRef] [Green Version]

- Küpper, T.; Lehmkuhl, T.; Wieneke, A.; Jung, R. Technology Use of Social Media within Customer Relationship Management: An Organizational Perspective. 2015. Available online: https://www.semanticscholar.org/paper/Technology-Use-of-Social-Media-within-Customer-An-K%C3%BCpper-Lehmkuhl/816a67102dc0c380525df33499c5cc3149a93d2e (accessed on 26 November 2022).

- Khraim, H.S. Internet Motives of Users in Jordan, UAE and KSA: A Cross-Cultural Validation of the Web Motivation Inventory (WMI). Int. J. Mark. Stud. 2016, 8, 138. [Google Scholar] [CrossRef] [Green Version]

- Habes, M.; Alghizzawi, M.; Elareshi, M.; Ziani, A.; Qudah, M.; Al Hammadi, M.M. E-Marketing and Customers’ Bank Loyalty Enhancement: Jordanians’ Perspectives. In The Implementation of Smart Technologies for Business Success and Sustainability; Springer: Berlin/Heidelberg, Germany, 2023; pp. 37–47. [Google Scholar]

- Al Kurdi, B.; Alshurideh, M.; Akour, I.; Alzoubi, H.M.; Obeidat, B.; AlHamad, A. The role of digital marketing channels on consumer buying decisions through eWOM in the Jordanian markets. Int. J. Data Netw. Sci. 2022, 6, 1175–1186. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1. Gender | |||||||||||

| 2. Age | −0.023 | ||||||||||

| 3. Education | −0.021 | 0.074 | |||||||||

| 4. Location | −0.029 | −0.037 | −0.051 | ||||||||

| 5. Social status | −0.075 | 0.036 | 0.081 | 0.079 | |||||||

| 6. SMF | 0.018 | −0.048 | 0.014 | −0.028 | −0.022 | ||||||

| 7. EWM | 0.058 | −0.046 | −0.014 | 0.016 | −0.034 | 0.586 ** | |||||

| 8. INF | −0.029 | −0.100 | 0.004 | −0.014 | 0.003 | 0.639 ** | 0.695 ** | ||||

| 9. PEU | 0.038 | −0.103 | 0.047 | 0.007 | −0.016 | 0.618 ** | 0.578 ** | 0.727 ** | |||

| 10. BI | 0.058 | −0.070 | 0.029 | −0.064 | −0.080 | 0.473 ** | 0.560 ** | 0.614 ** | 0.629 ** | ||

| 11. CL | 0.086 | −0.027 | 0.001 | −0.046 | −0.030 | 0.420 ** | 0.529 ** | 0.574 ** | 0.517 ** | 0.605 ** | |

| 12. PU | 0.027 | 0.108 | −0.045 | −0.028 | −0.099 | 0.691 ** | 0.583 ** | 0.561 ** | 0.490 ** | 0.501 ** | 0.435 ** |

| Factors | Items | FL | CA | CR | AVE |

|---|---|---|---|---|---|

| Social media features (SMF) | 3 | 0.819–0.844 | 0.804 | 0.884 | 0.719 |

| Electronic word of mouth (EWM) | 3 | 0.765–0.832 | 0.734 | 0.850 | 0.653 |

| Informativeness (INF) | 4 | 0.704–0.808 | 0.744 | 0.839 | 0.566 |

| Perceived usefulness (PU) | 6 | 0.696–0.794 | 0.837 | 0.881 | 0.552 |

| Perceived ease of use (PEU) | 3 | 0.851–0.869 | 0.826 | 0.896 | 0.742 |

| Behavioral intention (BI) | 4 | 0.734–0.793 | 0.756 | 0.846 | 0.578 |

| Customer loyalty (CL) | 3 | 0.770–0.830 | 0.738 | 0.851 | 0.657 |

| Item | BI | CL | EWM | INF | PEU | PU |

|---|---|---|---|---|---|---|

| Customer loyalty (CL) | 0.821 | |||||

| Electronic word of mouth (EWM) | 0.896 | 0.835 | ||||

| Informativeness (INF) | 0.874 | 0.839 | 0.858 | |||

| Perceived ease of use (PEU) | 0.761 | 0.681 | 0.735 | 0.823 | ||

| Perceived usefulness (PU) | 0.804 | 0.752 | 0.888 | 0.894 | 0.614 | |

| Social media features (SMF) | 0.682 | 0.635 | 0.832 | 0.867 | 0.701 | 0.882 |

| Index | Estimated Value in Model | Acceptable Value | |

|---|---|---|---|

| Structured Model | Estimated Model | ||

| SRMR | 0.077 | 0.098 | <0.1 |

| NFI | 0.986 | 0.988 | >0.9 |

| RMS_theta | 0.107 | <0.12 | |

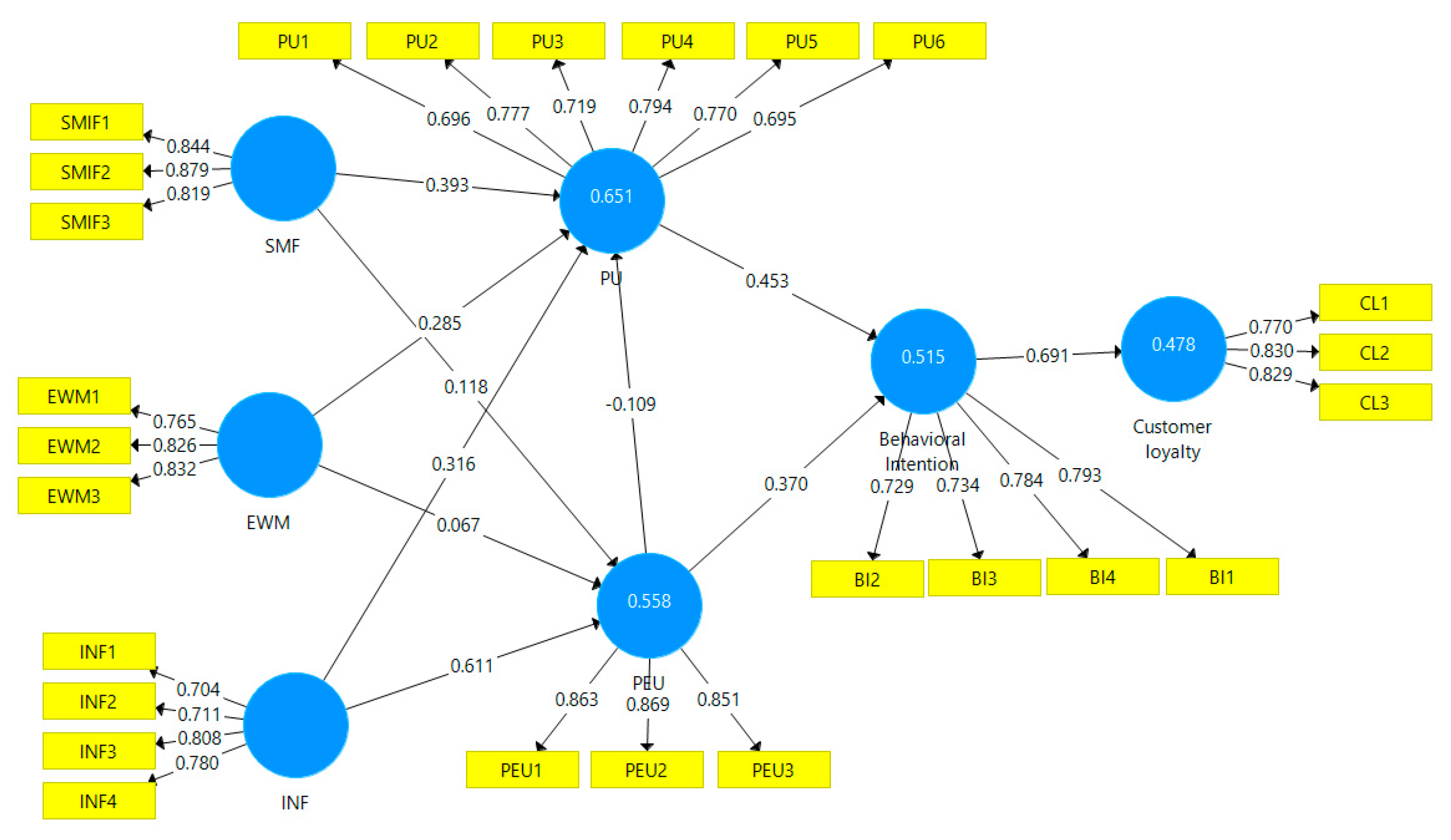

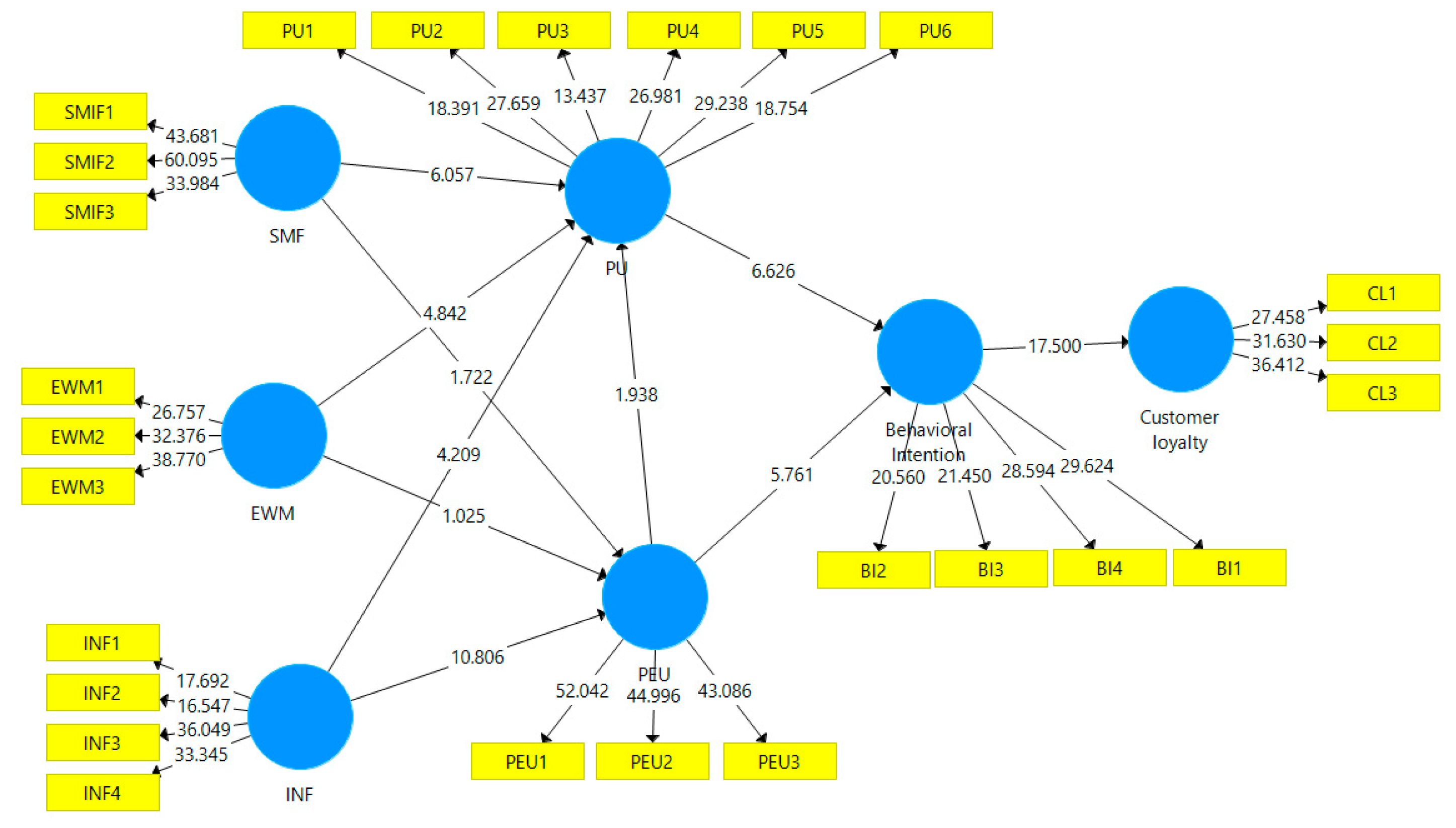

| Hypothesis | Relationship | SD | t-Value | β | Sig. |

|---|---|---|---|---|---|

| H1a | Social media features => Perceived usefulness | 0.065 | 6.057 | 0.393 | 0.000 |

| H1b | Social media features => Perceived ease of use | 0.068 | 1.722 | 0.118 | 0.086 |

| H2a | Electronic word of mouth => Perceived usefulness | 0.059 | 4.842 | 0.285 | 0.000 |

| H2b | Electronic word of mouth => Perceived ease of use | 0.066 | 1.025 | 0.067 | 0.306 |

| H3a | Informativeness => Perceived usefulness | 0.075 | 4.209 | 0.316 | 0.000 |

| H3b | Informativeness => Perceived ease of use | 0.057 | 10.806 | 0.611 | 0.000 |

| H4 | Perceived ease of use => Perceived usefulness | 0.056 | 1.938 | −0.109 | 0.005 |

| H5 | Perceived usefulness => Behavioral intention | 0.068 | 6.626 | 0.453 | 0.000 |

| H6 | Perceived ease of use => Behavioral intention | 0.064 | 5.761 | 0.370 | 0.000 |

| H7 | Behavioral intention => Customer loyalty | 0.040 | 17.500 | 0.691 | 0.000 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Elareshi, M.; Habes, M.; Safori, A.; Attar, R.W.; Noor Al adwan, M.; Al-Rahmi, W.M. Understanding the Effects of Social Media Marketing on Customers’ Bank Loyalty: A SEM Approach. Electronics 2023, 12, 1822. https://doi.org/10.3390/electronics12081822

Elareshi M, Habes M, Safori A, Attar RW, Noor Al adwan M, Al-Rahmi WM. Understanding the Effects of Social Media Marketing on Customers’ Bank Loyalty: A SEM Approach. Electronics. 2023; 12(8):1822. https://doi.org/10.3390/electronics12081822

Chicago/Turabian StyleElareshi, Mokhtar, Mohammed Habes, Amjad Safori, Razaz Waheeb Attar, Muhammad Noor Al adwan, and Waleed Mugahed Al-Rahmi. 2023. "Understanding the Effects of Social Media Marketing on Customers’ Bank Loyalty: A SEM Approach" Electronics 12, no. 8: 1822. https://doi.org/10.3390/electronics12081822