Does Banking Accessibility Matter in Assuring the Economic Growth in the Digitization Context? Evidence from Central and Eastern European Countries

Abstract

:1. Introduction

2. Literature Review

2.1. Financial Development and Macroeconomic Performance

2.2. Financial Accessibility and Economic Growth

2.3. Financial Development and Digitization

3. Data and Methodology

- -

- Independent variables related to the traditional financial accessibility—the oldest typology of financial access to the banking sector derived from the primary operations of a bank: the number of commercial bank branches per 100,000 adults; the number of commercial bank branches per 1000 km2; outstanding loans from commercial banks (% of GDP); outstanding deposits at commercial banks (% of GDP).

- -

- Independent variables related to the digital financial accessibility—the newest typology of financial access to the banking sector derived from the necessity to embrace the digital technology and to transpose it into the banks’ activity: the number of credit cards per 1000 adults; number of debit cards per 1000 adults; the number of ATMs per 100,000 adults; the number of ATMs per 1000 km2 and individuals using the internet for internet banking.

- Yit = the dependent variable, which is lnGDP, used to quantify the performance of the economic sector,

- FAdit = the independent variables, which can be lnATMS_AD, lnATMS_KM, lnCREDCARD, lnDEBCARD, lnEBANKING used to quantify the financial accessibility in the banking system through the digital components,

- FAtit = the independent variables, which can be lnBANKBR_AD, lnBANKBR_KM, lnDEPOSITS, lnLOANS, used to quantify the financial accessibility in the banking system through the traditional components,

- Z = the control variables, which can be lnTRADE.

- αj, βj, γj = the associated coefficients of the variables,

- i = the country,

- t = the period,

- δt = the time dummy variable,

- εit = the standard error of the regression.

4. Results

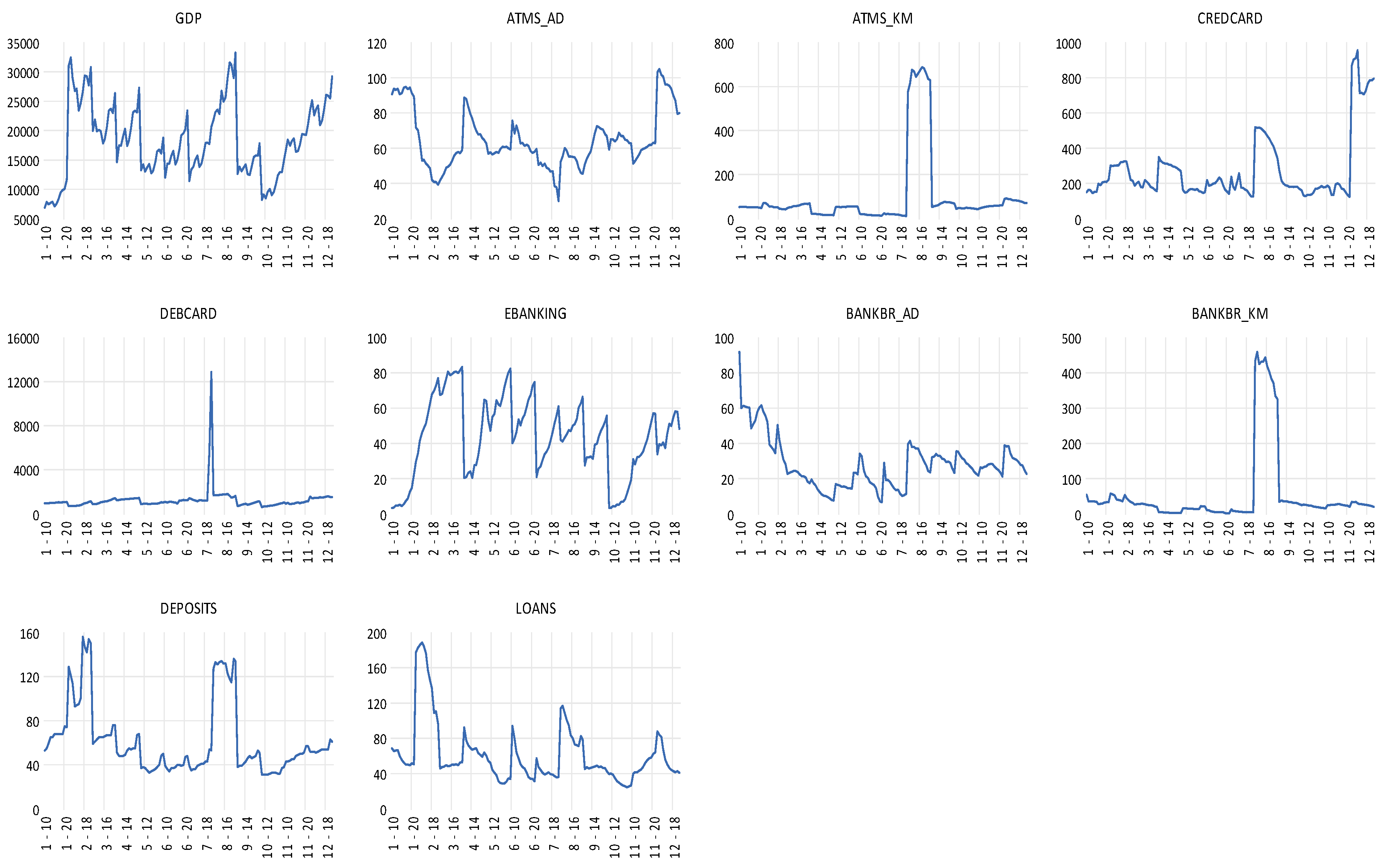

4.1. Evolution of Selected Indicators in CEECs

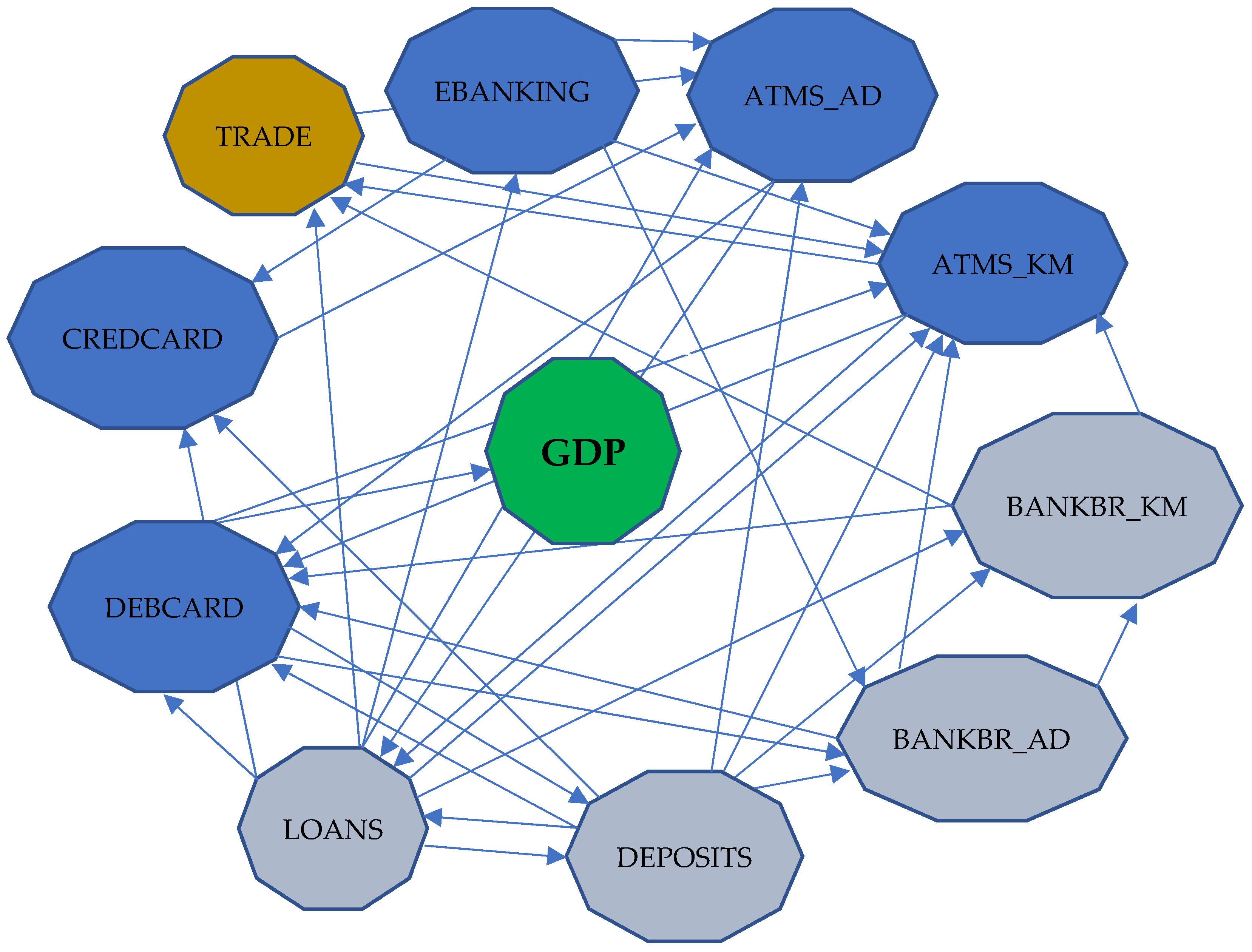

4.2. Estimation of Impact and Causality of Financial Accessibility on the Economic Growth

5. Discussions

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Mowes, T.; Puschmann, T.; Alt, R. Service-Based Integration of IT Innovations in Customer-Bank-Interaction; Wirtschaftsinformatik: Zurich, Switzerland, 2011. [Google Scholar]

- Schumpeter, J.A. The Theory of Economic Development; Harvard University Press: Cambridge, MA, USA, 1911. [Google Scholar]

- Stiglitz, J.E.; Weiss, A. Incentive effects of terminations: Applications to the credit and labor markets. Am. Econ. Rev. 1983, 73, 912–927. [Google Scholar]

- Greenwood, J.; Jovanovic, B. Financial development, growth, and the distribution of income. J. Political Econ. 1990, 98, 1076–1107. [Google Scholar] [CrossRef] [Green Version]

- Levine, R. Financial development, and economic growth: Views and agenda. J. Econ. Lit. 1997, 35, 688–726. [Google Scholar]

- Beck, T. Financial development, and international trade: Is there a link? J. Int. Econ. 2002, 57, 107–131. [Google Scholar] [CrossRef]

- Robinson, J. The generalization of the general theory. In The Rate of Interest and Other Essays; Macmillan: London, UK, 1952. [Google Scholar]

- Lucas, R.E. On the mechanics of economic development. J. Monet. Econ. 1988, 22, 3–42. [Google Scholar] [CrossRef]

- Schumpeter, J.A. A Theory of Economic Development: An Inquiry into Profits, Capital, Credit, Interest, and the Business Cycle; Harvard University Press: Cambridge, MA, USA, 1934. [Google Scholar]

- McKinnon, R.I. Money, and Capital in Economic Development; Brookings Institution: Washington, DC, USA, 1973. [Google Scholar]

- Shaw, E.S. Financial Deepening in Economic Development; Oxford University Press: New York, NY, USA, 1973. [Google Scholar]

- King, R.G.; Levine, R. Finance, and growth: Schumpeter might be right. Q. J. Econ. 1993, 108, 717–737. [Google Scholar] [CrossRef]

- King, R.G.; Levine, R. Finance, entrepreneurship, and growth: Theory and evidence. J. Monet. Econ. 1993, 32, 513–542. [Google Scholar] [CrossRef]

- Levine, R.; Loayza, N.; Beck, T. Financial intermediation, and growth: Causality and causes. J. Monet. Econ. 2000, 46, 31–77. [Google Scholar] [CrossRef] [Green Version]

- Guru, K.B.; Yadav, I.S. Financial Development and Economic Growth: Panel Evidence from BRICS. J. Econ. Financ. Adm. Sci. 2019, 24, 113–126. Available online: https://ssrn.com/abstract=3399728 (accessed on 2 October 2022). [CrossRef] [Green Version]

- Bist, J.P. Financial development, and economic growth: Evidence from a panel of 16 African and non-African low-income countries. Cogent Econ. Financ. 2018, 6, 1449780. [Google Scholar] [CrossRef] [Green Version]

- Cole, D.C. Financial Development in Asia. In Asian-Pacific Economic Literature; Asia Pacific School of Economics and Government, Australian National University: Canberra, Australia, 1988; Volume 2, pp. 26–47. [Google Scholar]

- Edwards, K.D. Prospect theory: A literature review. Int. Rev. Financ. Anal. 1996, 5, 19–38. [Google Scholar] [CrossRef]

- Arcand, J.L.; Berkes, E.; Panizza, U. Too much finance? J. Econ. Growth 2015, 20, 105–148. [Google Scholar] [CrossRef]

- Beck, T.; Degryse, H.; Kneer, C. Is more finance better? Disentangling intermediation and size effects of financial systems. J. Financ. Stab. 2014, 10, 50–64. [Google Scholar] [CrossRef] [Green Version]

- International Monetary Fund. Financial Sector Assessment Program. September 2022. Available online: https://www.imf.org/en/Publications/fssa/financial-sector-assessment-program-faq (accessed on 4 September 2022).

- World Bank. Data Bank. 2022. Available online: https://databank.worldbank.org/source/world-development-indicators (accessed on 2 October 2022).

- Arora, R.U. Measuring Financial Access. In Discussion Papers in Economics; Griffith University, Department of Accounting, Finance and Economics: Brisbane, Australia, 2010; Available online: https://research-repository.griffith.edu.au/handle/10072/390305 (accessed on 23 October 2022).

- Kendall, J.; Mylenko, N.; Ponce, A. Measuring Financial Access around the World. In World Bank Policy Research Working Paper 5253; World Bank: Washington, DC, USA, 2010; Available online: https://elibrary.worldbank.org (accessed on 10 October 2022).

- Boldbaatar, M.; Lee, C.L. Financial Accessibility and Economic Growth. J. East Asian Econ. Integr. 2015, 19, 143–166. [Google Scholar] [CrossRef]

- Nguyen, H.M.; Le, Q.T.-T.; Ho, C.M.; Nguyen, T.C.; Vo, D.H. Does financial development matter for economic growth in the emerging markets? Borsa Istanb. Rev. 2022, 22, 688–698. [Google Scholar] [CrossRef]

- Dudian, M.; Popa, R. Dezvoltarea financiară şi creşterea economică în Europa Centrală şi de Est. Econ. Teor. Şi Apl. 2013, 8, 55–65. [Google Scholar]

- Solow, R.M. A Contribution to the Theory of Economic Growth. Q. J. Econ. 1956, 70, 65–94. [Google Scholar] [CrossRef]

- Habibi, F.; Zabardast, M.A. Digitalization, Education, and Economic Growth: A Comparative Analysis of Middle East and OECD Countries. Technol. Soc. 2020, 63, 101370. Available online: https://www.sciencedirect.com/science/article/abs/pii/S0160791X20302244 (accessed on 6 November 2022). [CrossRef]

- Mago, S.; Chitokwindo, S. The Impact of Mobile Banking on Financial Inclusion in Zimbabwe: A Case for Masvingo Province. Mediterr. J. Soc. Sci. 2014, 5, 221. Available online: https://www.richtmann.org/journal/index.php/mjss/article/view/263 (accessed on 4 November 2022).

- Myovella, G.; Karacuka, M.; Haucap, J. Digitalization and economic growth: A comparative analysis of Sub-Saharan Africa and OECD economies. Telecommun. Policy 2020, 44, 101856. [Google Scholar] [CrossRef]

- Owusu-Agyei, S.; Okafor, G.; Chijoke-Mgbame, A.M.; Ohalehi, P.; Hasan, F. Internet adoption and financial development in sub-Saharan Africa. Technol. Forecast. Soc. Chang. 2020, 161, 20293. [Google Scholar] [CrossRef]

- Mignamissi, D.; Djijo, T.A.J. Digital divide and financial development in Africa. Telecommun. Policy 2021, 45, 102199. [Google Scholar] [CrossRef]

- Kumar, P.; Pillai, R.; Kumar, N.; Tabash, M.I. The Tnterplay of Skills, Digital Ffinancial Literacy, Capability, and Autonomy in Financial Decision Making and Well-Being. Borsa Istanb. Rev. 2022. in press. Available online: https://www.sciencedirect.com/science/article/pii/S2214845022000837 (accessed on 31 December 2022).

- Stiglitz, J.E. Information and the Change in the Paradigm in Economics, Part 1. Am. Econ. 2003, 47, 6–26. Available online: https://journals.sagepub.com/doi/10.1177/056943450304700202 (accessed on 4 November 2022). [CrossRef]

- Feyen, E.; Frost, J.; Gambacorta, L.; Natarajan, H.; Saal, M. Fintech and the Digital Transformation of Financial Services: Implications for Market Structure and Public Policy. In BIS Papers; Monetary and Economic Department: Basel, Switzerland, 2021. [Google Scholar]

- Bădîrcea, R.M.; Manta, A.G.; Florea, N.M.; Popescu, J.; Manta, F.L.; Puiu, S. E-Commerce and the Factors Affecting Its Development in the Age of Digital Technology: Empirical Evidence at EU–27 Level. Sustainability 2022, 14, 101. Available online: https://www.mdpi.com/2071-1050/14/1/101 (accessed on 2 November 2022). [CrossRef]

- Eurostat. Data Browser. 2022. Available online: https://ec.europa.eu/eurostat/databrowser/view/tin00099/default/table?lang=en (accessed on 20 December 2022).

- Beck, T.; Demirguc-Kunt, A.; Laeven, L.; Levine, R. Finance, Firm Size, and Growth. J. Money Credit. Bank. 2008, 40, 1379–1405. [Google Scholar] [CrossRef] [Green Version]

- Dumitrescu, E.-I.; Hurlin, C. Testing for Granger Non-causality in Heterogeneous Panels. Econ. Model. 2012, 29, 1450–1460. [Google Scholar] [CrossRef] [Green Version]

- International Monetary Fund. Financial Access Survey (FAS). Available online: https://data.imf.org/?sk=E5DCAB7E-A5CA-4892-A6EA-598B5463A34C&sId=1390030341854 (accessed on 7 September 2022).

- World Bank Group. Europe 4.0. Addressing the Digital Dilemma. 2020. Available online: https://openknowledge.worldbank.org/handle/10986/34746 (accessed on 31 December 2022).

- Hamit-Haggar, M. Greenhouse gas emissions, energy consumption and economic growth: A panel cointegration analysis from Canadian industrial sector perspective. Energy Econ. 2012, 34, 358. [Google Scholar] [CrossRef]

- Levin, A.; Lin, C.F.; Chu, C. Unit Root Tests in Panel Data: Asymptotic and Finite-Sample Properties. J. Econom. 2002, 108, 1–24. [Google Scholar] [CrossRef]

- Kao, C. Spurious regression and residual-based tests for cointegration in panel data. J. Econom. 1999, 90, 1–44. [Google Scholar] [CrossRef]

- Pedroni, P. Fully Modified OLS for Heterogeneous Cointegrated Panels; No 2000-03; Department of Economics Working Papers, Department of Economics, Williams College: Williamstown, MA, USA, 2000. [Google Scholar]

- Phillips, P.; Hansen, B. Statistical Inference in Instrumental Variables Regression with I (1) Processes. Rev. Econ. Stud. 1990, 57, 99–125. [Google Scholar] [CrossRef]

- Moody’s Analytics. The Impact of Payment Cards on Economic Growth. 2021. Available online: https://www.google.com/url?sa=t&rct=j&q=&esrc=s&source=web&cd=&ved=2ahUKEwiLitHUsqT8AhXKM-wKHTHKClMQFnoECCYQAQ&url=https%3A%2F%2Fusa.visa.com%2Fcontent%2Fdam%2FVCOM%2Fregional%2Fna%2Fus%2Fvisa-everywhere%2Fdocuments%2Fthe-impact-of-payment-cards-on-economic-growth.pdf&usg=AOvVaw0u7ZVHq9OnjwXqpLfUo8Ao (accessed on 31 December 2022).

{kind=link}

{kind=link}

| Acronym | Definition | Variable Type | Unit of Measure | Time Period | Data Source |

|---|---|---|---|---|---|

| GDP | Gross Domestic Product per capita | Dependent variable | Current USD | 2010–2021 | World Development Indicators |

| ATMS_AD | Number of Automated teller machines (ATMs) per 100,000 adults | Independent variable/Digital financial accessibility | Per 100,000 adults | 2010–2021 | World Bank, International Monetary Fund |

| ATMS_KM | Number of Automated teller machines (ATMs) per 1000 km2 | Independent variable/Digital financial accessibility | Per 1000 km2 | 2010–2021 | World Bank, International Monetary Fund |

| BANKBR_AD | Number of commercial bank branches per 100,000 adults | Independent variable/Traditional financial accessibility | Per 100,000 adults | 2010–2021 | World Bank, International Monetary Fund |

| BANKBR_KM | Number of commercial bank branches per 1000 km2 | Independent variable/Traditional financial accessibility | Per 1000 km2 | 2010–2021 | World Bank, International Monetary Fund |

| CREDCARD | Number of credit cards per 1000 adults | Independent variable/Digital financial accessibility | No. of credit cards | 2010–2021 | World Bank, International Monetary Fund |

| DEBCARD | Number of debit cards per 1000 adults | Independent variable/Digital financial accessibility | No. of debit cards | 2010–2021 | World Bank, International Monetary Fund |

| EBANKING | Individuals using the internet for internet banking | Independent variable/Digital financial accessibility | Percentage of individuals | 2010–2021 | Eurostat |

| DEPOSITS | Outstanding deposits at commercial banks | Independent variable/Traditional financial accessibility | % Of GDP | 2010–2021 | World Bank, International Monetary Fund |

| LOANS | Outstanding loans from commercial banks | Independent variable/Traditional financial accessibility | % Of GDP | 2010–2021 | World Bank, International Monetary Fund |

| TRADE | Sum of exports and imports of goods and services measured as a share of GDP | Control variable | % Of GDP | 2010–2021 | World Bank, International Monetary Fund |

| Correlation Probability | LNGDP | LNATMS_AD | LNATMS_KM | LNBANKBR_AD | LNBANKBR_KM | LNCREDCARD | LNDEBCARD | LNDEPOSITS | LNEBANKING | LNLOANS | LNTRADE |

|---|---|---|---|---|---|---|---|---|---|---|---|

| LNGDP | 1.00 | ||||||||||

| ----- | |||||||||||

| LNATMS_AD | −0.33 | 1.00 | |||||||||

| 0.00 | ----- | ||||||||||

| LNATMS_KM | 0.30 | 0.00 | 1.00 | ||||||||

| 0.00 | 0.96 | ----- | |||||||||

| LNBANKBR_AD | −0.23 | 0.36 | 0.50 | 1.00 | |||||||

| 0.00 | 0.00 | 0.00 | ----- | ||||||||

| LNBANKBR_KM | 0.19 | −0.04 | 0.94 | 0.70 | 1.00 | ||||||

| 0.01 | 0.60 | 0.00 | 0.00 | ----- | |||||||

| LNCREDCARD | 0.56 | 0.33 | 0.44 | 0.19 | 0.34 | 1.00 | |||||

| 0.00 | 0.00 | 0.00 | 0.01 | 0.00 | ----- | ||||||

| LNDEBCARD | 0.36 | −0.12 | 0.09 | −0.30 | −0.03 | 0.32 | 1.00 | ||||

| 0.00 | 0.12 | 0.28 | 0.00 | 0.70 | 0.00 | ----- | |||||

| LNDEPOSITS | 0.60 | −0.17 | 0.59 | 0.36 | 0.62 | 0.45 | 0.24 | 1.00 | |||

| 0.00 | 0.03 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | ----- | ||||

| LNEBANKING | 0.76 | −0.46 | 0.08 | −0.45 | −0.03 | 0.22 | 0.30 | 0.27 | 1.00 | ||

| 0.00 | 0.00 | 0.33 | 0.00 | 0.67 | 0.00 | 0.00 | 0.00 | ----- | |||

| LNLOANS | 0.47 | 0.00 | 0.31 | 0.41 | 0.40 | 0.46 | 0.00 | 0.75 | 0.14 | 1.00 | |

| 0.00 | 0.91 | 0.00 | 0.00 | 0.00 | 0.00 | 0.91 | 0.00 | 0.07 | ----- | ||

| LNTRADE | 0.56 | −0.17 | 0.54 | −0.09 | 0.40 | 0.41 | 0.43 | 0.55 | 0.50 | 0.35 | 1.00 |

| 0.00 | 0.03 | 0.00 | 0.26 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | ----- |

| LNGDP | LNATMS_AD | LNATMS_KM | LNBANKBR_AD | LNBANKBR_KM | LNCREDCARD | LNDEBCARD | LNDEPOSITS | LNLOANS | LNEBANKING | LNTRADE | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Mean | 9.74 | 4.13 | 3.97 | 3.21 | 3.05 | 5.45 | 7.02 | 4.01 | 4.00 | 3.53 | 4.95 |

| Median | 9.78 | 4.10 | 3.97 | 3.26 | 3.20 | 5.26 | 6.96 | 3.93 | 3.91 | 3.82 | 4.97 |

| Max. | 10.41 | 4.65 | 6.53 | 4.52 | 6.12 | 6.86 | 9.46 | 5.04 | 5.24 | 4.42 | 5.77 |

| Min. | 8.83 | 3.40 | 2.42 | 1.89 | 0.51 | 4.81 | 6.43 | 3.43 | 3.20 | 1.16 | 4.26 |

| Std. Dev. | 0.37 | 0.24 | 0.92 | 0.50 | 1.24 | 0.50 | 0.34 | 0.43 | 0.44 | 0.83 | 0.31 |

| Skewness | −0.46 | 0.14 | 1.25 | −0.28 | 0.45 | 1.21 | 3.00 | 0.90 | 0.89 | −1.48 | 0.48 |

| Kurtosis | 2.62 | 2.94 | 5.09 | 3.03 | 3.82 | 3.62 | 20.83 | 2.91 | 3.72 | 4.25 | 3.79 |

| Jarque-Berra | 6.06 | 0.50 | 64.18 | 1.90 | 9.18 | 37.59 | 2126.15 | 19.50 | 22.14 | 62.39 | 9.45 |

| Prob. | 0.04 | 0.77 | 0.00 | 0.38 | 0.01 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Sum | 1403.86 | 595.87 | 571.93 | 463.06 | 439.20 | 785.27 | 1011.38 | 578.58 | 576.58 | 509.38 | 713.51 |

| Sum Sq. Dev. | 20.06 | 8.30 | 122.29 | 36.45 | 221.16 | 36.65 | 17.36 | 26.66 | 28.43 | 99.53 | 13.92 |

| Obs. | 144 | 144 | 144 | 144 | 144 | 144 | 144 | 144 | 144 | 144 | 144 |

| Methods Level/First Difference (D) | Statistic (p) in LLC | Statistic (p) in ADF | Statistic (p) in PP |

|---|---|---|---|

| LNGDP | 0.4736 (0.6821) | 6.2068 (0.9999) | 5.3062 (1.0000) |

| D(LNGDP) | −8.7173 (0.0000) | 70.2371 (0.0000) | 89.4848 (0.0000) |

| LNATMS_AD | 2.6172 (0.0044) | 24.7868 (0.4174) | 45.2246 (0.0055) |

| D(LNATMS_AD) | −7.33089 (0.0000) | 64.4144 (0.0000) | 83.6256 (0.0000) |

| LNATMS_KM | −2.84172 (0.0022) | 27.4007 (0.2861) | 42.8472 (0.0104) |

| D(LNATMS_KM) | −8.4312 (0.0000) | 69.3284 (0.0000) | 83.5382 (0.0000) |

| LNBANKBR_AD | 0.4462 (0.6723) | 20.9181 (0.6436) | 20.1283 (0.6895) |

| D(LNBANKBR_AD) | −8.3415 (0.0000) | 68.2054 (0.0000) | 75.7608 (0.0000) |

| LNBANKBR_KM | 0.1032 (0.5411) | 21.7503 (0.5942) | 21.1466 (0.6301) |

| D(LNBANKBR_KM) | −10.0839 (0.0000) | 82.8735 (0.0000) | 81.1151 (0.0000) |

| LNCREDCARD | 7.9084 (1.0000) | 29.3934 (0.2057) | 22.1827 (0.5684) |

| D(LNCREDCARD) | −5.8974 (0.0000) | 73.5488 (0.0000) | 73.3097 (0.0000) |

| LNDEBCARD | 1.4771 (0.9302) | 9.3178 (0.9968) | 9.0017 (0.9976) |

| D(LNDEBCARD) | −7.9310 (0.0000) | 66.7542 (0.0000) | 75.4400 (0.0000) |

| LNEBANKING | 1.4046 (0.9199) | 10.4029 (0.9927) | 30.5927 (0.1659) |

| D(LNEBANKING) | −2.1256 (0.0168) | 32.5087 (0.1049) | 124.255 (0.0000) |

| LNDEPOSITS | 1.2943 (0.9022) | 7.0231 (0.9997) | 11.8504 (0.9815) |

| D(LNDEPOSITS) | −9.5897 (0.0000) | 76.4336 (0.0000) | 83.6066 (0.0000) |

| LNLOANS | −5.6422 (0.0000) | 43.1841 (0.0095) | 52.0028 (0.0008) |

| D(LNLOANS) | −5.3438 (0.0000) | 43.7478 (0.0082) | 75.5901 (0.0000) |

| LNTRADE | −3.1220 (0.0009) | 47.4148 (0.0030) | 67.1239 (0.0000) |

| D(LNTRADE) | −9.7051 (0.0000) | 85.8288 (0.0000) | 86.7115 (0.0000) |

| t-Statistic | Prob. | |

|---|---|---|

| ADF | −5.302068 | 0.0010 |

| Residual variance | 0.005943 | |

| HAC variance | 0.004391 |

| Unrestricted Cointegration Rank Test (Trace and Maximum Eigenvalue) | ||||

|---|---|---|---|---|

| Hypothesized | Fisher Stat. * | Fisher Stat. * | ||

| No. of CE(s) | (From Trace Test) | Prob. | (From Max-Eigen Test) | Prob. |

| None | 809.3515 | 0.0000 | 594.8693 | 0.0000 |

| At most 1 | 214.4822 | 0.3653 | 61.00820 | 0.1039 |

| At most 2 | 153.4740 | 0.8471 | 50.84472 | 0.2292 |

| At most 3 | 102.6293 | 0.9932 | 43.04199 | 0.3223 |

| At most 4 | 59.58728 | 1.0000 | 24.86484 | 0.9686 |

| At most 5 | 34.72244 | 1.0000 | 15.18788 | 0.9995 |

| At most 6 | 19.53455 | 1.0000 | 10.02664 | 0.9999 |

| At most 7 | 9.507910 | 1.0000 | 4.844871 | 1.0000 |

| At most 8 | 4.663040 | 1.0000 | 3.917268 | 0.9995 |

| At most 9 | 0.745772 | 1.0000 | 0.745069 | 1.0000 |

| At most 10 | 0.000703 | 0.9800 | 0.000703 | 0.9800 |

| Dependent Variable: lnGDP | ||||

|---|---|---|---|---|

| Variable | Coef. | Std. Error | z-Stat. | Prob. |

| lnATMS_AD | 1.04 | 0.11 | 8.92 | 0.00 |

| lnATMS_KM | −0.80 | 0.11 | −7.02 | 0.00 |

| lnBANKBR_AD | −1.00 | 0.11 | −9.11 | 0.00 |

| lnBANKBR_KM | 0.93 | 0.11 | 8.45 | 0.00 |

| lnCREDCARD | −0.13 | 0.00 | −15.31 | 0.00 |

| lnDEBCARD | 0.06 | 0.00 | 15.41 | 0.00 |

| lnEBANKING | 0.08 | 0.01 | 7.77 | 0.00 |

| lnDEPOSITS | −0.12 | 0.00 | −18.90 | 0.00 |

| lnLOANS | 0.24 | 0.00 | 58.03 | 0.00 |

| lnTRADE | −0.39 | 0.01 | −27.66 | 0.00 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Manta, A.G.; Badareu, G.; Bădîrcea, R.M.; Doran, N.M. Does Banking Accessibility Matter in Assuring the Economic Growth in the Digitization Context? Evidence from Central and Eastern European Countries. Electronics 2023, 12, 279. https://doi.org/10.3390/electronics12020279

Manta AG, Badareu G, Bădîrcea RM, Doran NM. Does Banking Accessibility Matter in Assuring the Economic Growth in the Digitization Context? Evidence from Central and Eastern European Countries. Electronics. 2023; 12(2):279. https://doi.org/10.3390/electronics12020279

Chicago/Turabian StyleManta, Alina Georgiana, Gabriela Badareu, Roxana Maria Bădîrcea, and Nicoleta Mihaela Doran. 2023. "Does Banking Accessibility Matter in Assuring the Economic Growth in the Digitization Context? Evidence from Central and Eastern European Countries" Electronics 12, no. 2: 279. https://doi.org/10.3390/electronics12020279