An Empirical Framework for Assessing the Digital Technologies Users’ Acceptance in Project Management

Department of Economics, Accounting and International Business, University of Craiova, 200585 Craiova, Romania

Electronics 2022, 11(23), 3872; https://doi.org/10.3390/electronics11233872

Submission received: 19 October 2022

/

Revised: 14 November 2022

/

Accepted: 21 November 2022

/

Published: 23 November 2022

(This article belongs to the Special Issue Recent Applications of Emerging Digital Technologies in Economy and Society)

Abstract

:The technological advances and trends that have manifested in the direction of globalization have determined unprecedented economic expansion and exponential social development. Organizations have increasingly implemented digital technologies to face new challenges in all activities. Project management has more intensively implemented digitized technologies, such as big data, artificial intelligence, and cloud computing, taking into account the complexity of projects. This study aims to evaluate employees’ perceptions of the organizations involved in implementing the projects adopting digital technologies within the accounting and organizational information systems to digitize the project management process. The empirical study consists of a survey of 486 respondents from among project management specialists in Romania. The research uses the technology acceptance model (TAM) and structural equation modeling to assess user perceptions of digital technologies. The research results show that implementing digital technologies improves all activities in the project management process. Among the characteristics of digital technologies, customization is the most important characteristic that leads to increased efficiency and effectiveness of project management, followed by innovation. Furthermore, the perception of increasing the efficiency and effectiveness of project management exerts a significant and positive influence on the behavioral intention to use digital technologies and their actual use, leading to their easier acceptance.

1. Introduction

Given the challenges of globalization, technological advances, and the acceleration of the free movement of goods, citizens, capital, and information, the complexity of organizational activities is exponentially increasing. Digital technologies can significantly contribute by digitizing accounting and managerial information systems to improve efficiency and effectiveness within organizations [1,2,3,4,5,6]. The latest technologies that can transform project management are artificial intelligence (AI), Big Data (BD), blockchain (BC), and cloud computing (CC).

Digital technologies imply the modification of business models through automating many activities traditionally carried out by human resources and adapting the operating system to the new needs of the digital society. The increase in the speed of technological innovations has led to rapid technological developments, improving communication by reducing time and distance [7]. Chesbrough [8] showed that, due to increasingly accelerated innovation processes, managers must rethink the entire value creation chain, including project management, based on accounting and managerial information systems that profoundly transform at a paradigmatic level. Digital transformation in project management will increase the number of projects an organization can manage due to the increased ability to manage large volumes of data and make quick decisions [9].

Users’ acceptance of implementing the latest digital technologies in existing software solutions for project management and non-computerized activities is a gap identified following the literature review. The current paper addresses this gap, aiming to highlight how new digital technologies impact project management in organizations by investigating the perception of specialists in project management. The current paper uses the technology acceptance model (TAM) [10] to assess users’ acceptance of implementing the latest digital technologies in project management. TAM is a “valid and robust model that has been widely used, but which potentially has wider applicability” [11]. Although project management has recently been heavily computerized, new digital technologies are paradigmatically changing operationalization. Therefore, the paper emphasizes the impact of new digital technologies on the perception of users in project management and the degree of user acceptance of new technologies. The structure of the paper presents six sections. First, the introduction and literature review presents the research topic and the opinions of researchers in the field. Secondly, the paper provides the research methodology and the results obtained. Finally, the paper displays the discussions and conclusions. The last section concludes by emphasizing the need for additional theoretical and empirical research on implementing digital technologies and their effect on project management within organizations.

2. Literature Review

2.1. Corporate Digital Transformation Strategy

International Business Machines (IBM) [12] defined digital transformation as a strategic change in a business model that manifests by integrating traditional elements with digital elements. The result is a new business model based on the paradigm of digital transformation. For International Data Corporation (IDC) [13], digital transformation represents an innovative and continuous process of adapting the organization to the new realities of society, including innovation. Furthermore, Ismail et al. [14] considered that implementing digital technologies creates significant added value through their innovative character, affecting essential areas of the organization, such as management, marketing, and accounting. Finally, Kim and Kim [6] viewed digital transformation as a management strategy that assists the organization in satisfying the needs of existing customers to a greater degree and creating new markets by adapting traditional organizational processes to the ways of conducting activities based on digital technologies, such as AI, BD, BC, and CC.

Multinational organizations adapt to new customer demands by adopting digital technologies to maximize profits while maintaining and increasing competitive advantages. Though digital transformation strategies vary, it is essential to ensure the technological capabilities to produce and use data [15].

Chanias et al. [16] showed that the development of technologies for collecting, managing, and processing data, as well as adopting decisions, must be the basis of fundamental strategies of innovation, management, and marketing. Contemporary organizations are restructuring their activities and adapting their business models, giving birth to a new digital ecosystem that transcends the traditional corporate environment [17]. These organizations introduce the innovation process into the organizational culture, focusing change management in the development, production, marketing, and accounting fields on the new coordinates of digital transformation.

Warner and Wäger [18] analyzed the resources and digital technological innovation within financial accounting and managerial information systems that directly affect project management through increasing transparency, accessibility, and speed of digital activities. Various researchers have emphasized the fundamental change in the financial-accounting sector through digitization using BC, BD, and CC, creating a new business model—fintech [19,20,21,22,23,24,25]. At the foundation of digital transformation is the collection and sharing of data through CC, BD, and BC, but the engine of digital transformation are AI technologies that allow the substitution of the human factor by the machine under certain conditions [26,27,28,29,30,31]. As a result, the entire value chain within the organization is increasingly digitized, from developing products and services to selling and then analyzing the efficiency and effectiveness of the activities carried out. All this takes place within a segmented or integrated digital platform, on top of which are AI solutions that are increasingly taking over one of the essential management processes of the organization: the decision-making process.

2.2. Digital Transformation of Financial Accounting and Managerial Information Systems

Digital technologies are transforming financial, accounting, and managerial information systems, affecting management, marketing, and accounting professional activities. The technological transformations of financial, accounting, and management information systems have been extensively researched in recent years [32,33,34,35], reviewing the challenges and opportunities offered by new technologies. Financial, accounting, and managerial information systems can undergo fundamental changes due to implementing digital technologies, but new paradigms are necessary to understand new ways of carrying out activities [36].

Although various types of research highlight the impact of digital transformation on accounting and managerial information systems [37,38,39,40,41], there have not been many empirical studies as a result of the implementation of digital technologies in a disparate way and based on the expertise of IT specialists, and even less on the experience of professionals in management. That is why it is necessary to understand the perception of those who use financial, accounting, and managerial information systems in project management.

Most studies focusing on the digital transformation of accounting and management information systems have BD as their target technology because it greatly facilitates the activity of the accelerated increase in the volume of data necessary for decision-making. Whether researching the strategic change of the accounting profession [42] or the relationship between the impact of BD on financial, accounting, and management information systems and corporate reporting [43], researchers have revealed the absolute necessity of implementing this technology in the operation of financial, accounting, and managerial information systems.

Although AI is still in the early stages of implementation within accounting and managerial information systems, the basis of some activities in fields such as management and marketing, several researchers have addressed the impact of AI on financial, accounting, and managerial information systems [44,45,46,47,48,49].

One of the technologies investigated concerning financial, accounting, and managerial information systems is BC. BC is a data register ensures transparency, accessibility, security, and safety. Various researchers have analyzed the impact of BC on financial, accounting, and managerial information systems [35,50,51,52,53], as well as its implications for the safety and security of the contained data [54]. Yu et al. [51] argued that public blockchains could be used as a platform for firms to voluntarily disclose short-term information: “In the long run, the application could effectively reduce errors in revenue disclosure and management, increase the quality of accounting information, and alleviate information asymmetry” Karajovic et al. [52] (p. 37). presented a more conceptual and philosophical idea for the long-term implications of blockchains.

Gardner and Bryson [55] explored the impact of technological transformations on financial, accounting, and managerial information systems, and also highlighted one of the main characteristics of technological innovation: that innovation destroys jobs and creates new jobs at the same time, but with a higher required skill level. Gardner and Bryson [55] (p. 42) described: “three levels of innovation within organizations: process, product, and business model innovations”. Process innovations involve introducing new technologies into the organization’s current activities and implicitly into the financial, accounting, and managerial information systems. Product innovations imply the emergence of IT solutions based on new technologies that lead to the improvement of existing products. The third level involves a paradigmatic change, creating new business models, including complete digital transformation. For this, organizations must have partnership agreements with digital technology companies and implement new technologies in a planned and strategic manner in financial, accounting, and managerial information systems, so that project management activities are redefined by the new digital bases.

2.3. Digital Transformation Influence on Project Management

Considering the complexity of project management, digital technologies greatly facilitate project tasks. Project management is a multidimensional structure that includes a series of activities from different subfields of management: strategic management (through project planning and scheduling), human resources management (project staff management), financial accounting management (budgeting activities), risk management, and quality management. Approaching the complexity of projects with the help of new technologies and digital transformation makes the work of professionals in the field much more accessible [56,57], which causes profound changes in project management. In addition, the possibility of upgrading IT solutions based on new digital technologies increases users’ perception of ease of use [58].

Digital transformation in project management will lead to an increase in the number of projects as a result of the increased ability to manage large volumes of data and make quick decisions, but it could also influence the perception of many project activities, which could be transferred in whole or in part to AI solutions. Furthermore, the innovativeness of new digital technologies determines an increase in the efficiency and effectiveness of projects [9].

Regarding project management processes, CC ensures transparency, high data accessibility, and extended communication possibilities with clients or project product recipients [59,60,61,62,63]. Furthermore, AI provides tools for repetitive decision-making in projects and extended costing and forecasting capabilities [56]. As a result of the implementation of digital technologies and the possibility of managing large volumes of data, the decision-making process substantially changes in terms of speed and quality assurance. In addition, the use of digital technologies and the implementation of dedicated IT solutions facilitate the planning and monitoring of projects, including, for example, the continuous evaluation of their effectiveness [64].

These new digital technologies help improve existing software (e.g., MeisterTask, Basecamp, Teamwork Projects, Trello, etc.) by adding the autonomy feature. As a result, IT solutions implemented in project management that include technologies such as BD, AI, CC, and BC will be able to perform repetitive tasks without the intervention of the human factor [62]. In addition, the operational costs for running the projects decreased due to the reductions in human resource costs and the reduction of the execution durations of the project phases [56,61,62,63].

Based on the results of previous research, the paper proposes the following hypothesis:

Hypothesis H1:

Innovativeness and complexity are the characteristics that most influence the efficiency and effectiveness of activities in the perception of project management specialists.

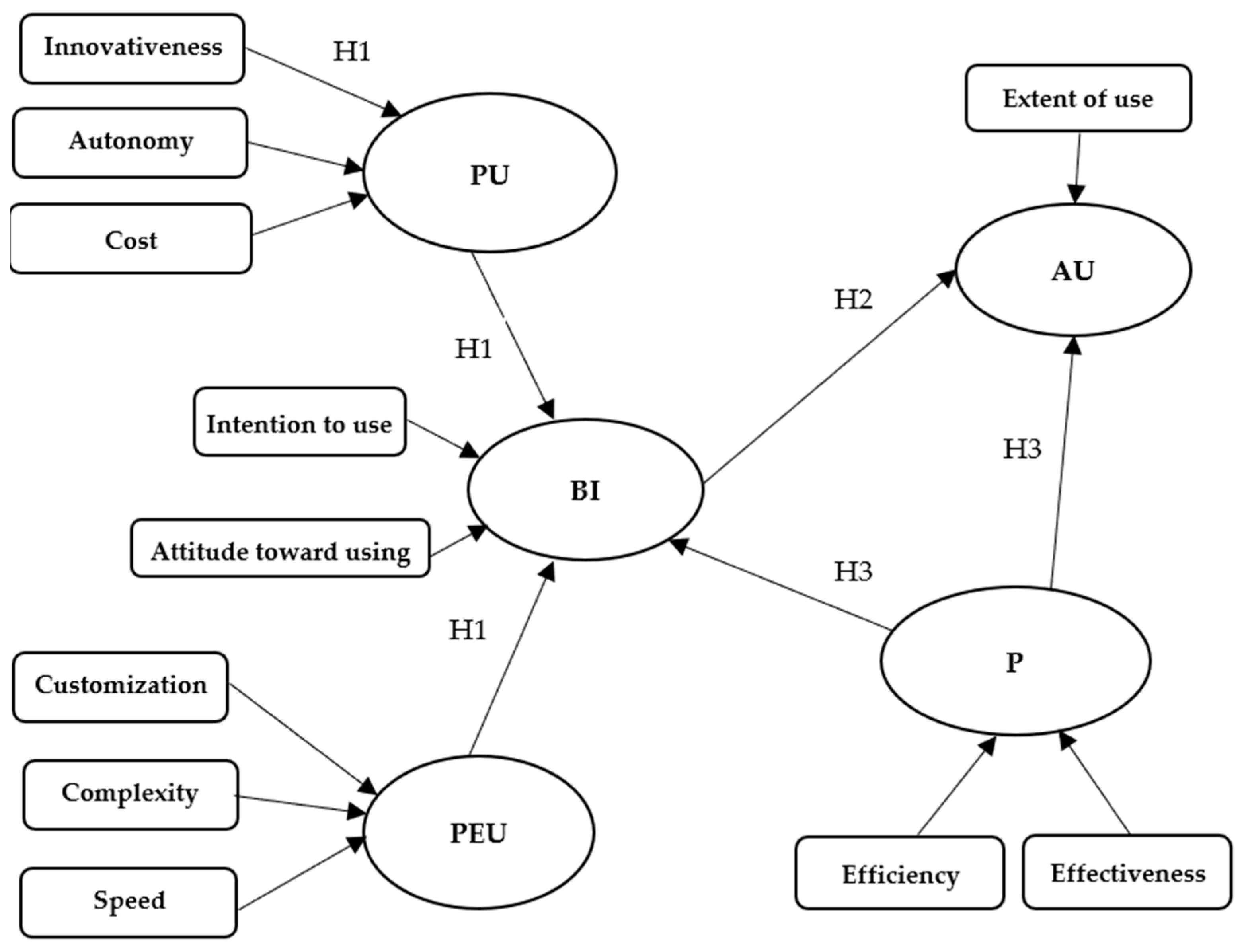

The most important aspect of digital transformation in project management is the users’ acceptance of implementing new digital technologies within existing IT solutions and their actual use due to the perception of increased efficiency and effectiveness of the activity. Even if companies invest in implementing new digital technologies, it is necessary to understand the acceptance by users of the new technologies [65,66]. The TAM model proposed by Davis [10] has been widely used in the literature during the adoption of new technology by users [11]. TAM starts from the premise that the technology adoption rate does not depend on its features, but on how these features are reflected in users’ perceptions [11]. Based on TAM, some researchers have studied the relationship between perceived usefulness (PU) and perceived ease of use (PEU), and users’ behavioral intentions to use newly introduced technology [66,67,68,69,70,71,72]. Davis [65] and other researchers, who developed the TAM model, showed that behavioral intention (BI), determined by PU and PEU, influences actual use (AU), studying and analyzing why people accept or not the implementation of new technologies in financial, accounting and managerial information systems of the organization. All other external factors indirectly influence BI through PU and PEU. Thus, the model’s endogenous variables, PU and PEU, are the critical variables for TAM. New digital technologies strongly impact project management and how activities are carried out in project-based organizations. Measuring the degree of acceptance by project management professionals of new particular technologies is a gap that the current paper addresses using the TAM model, which has been widely used in other fields. Figure 1 illustrates the research model of accepting digital technologies within financial, accounting, and managerial information systems to digitize project management processes.

After considering the results of previous papers on the TAM model, the current paper proposes the following hypothesis:

Hypothesis H2:

PU and PEU positively directly and indirectly influence BI and AU, respectively, in terms of the perception of project management specialists.

Within the TAM model applied to the acceptance of new digital technologies in project management, we selected, based on the literature review [10,11,66,67,68,69,70,71,72], as antecedents of PU innovativeness, autonomy, cost, and antecedents of PEU customization, complexity, and speed (Figure 1). In addition, based on the findings in the literature on the acceptance of technologies within financial, accounting, and managerial information systems [1,2,6,9], we introduced, as an endogenous variable of the model the performance (P), which has antecedents the efficiency and effectiveness perceived by users. Therefore, the increase in P due to increased perceived effectiveness and efficiency affects future BI and AU. As a result, the current paper proposes the following hypothesis:

Hypothesis H3:

P significantly positively influences BI and AU in the perception of project management specialists.

3. Materials and Methods

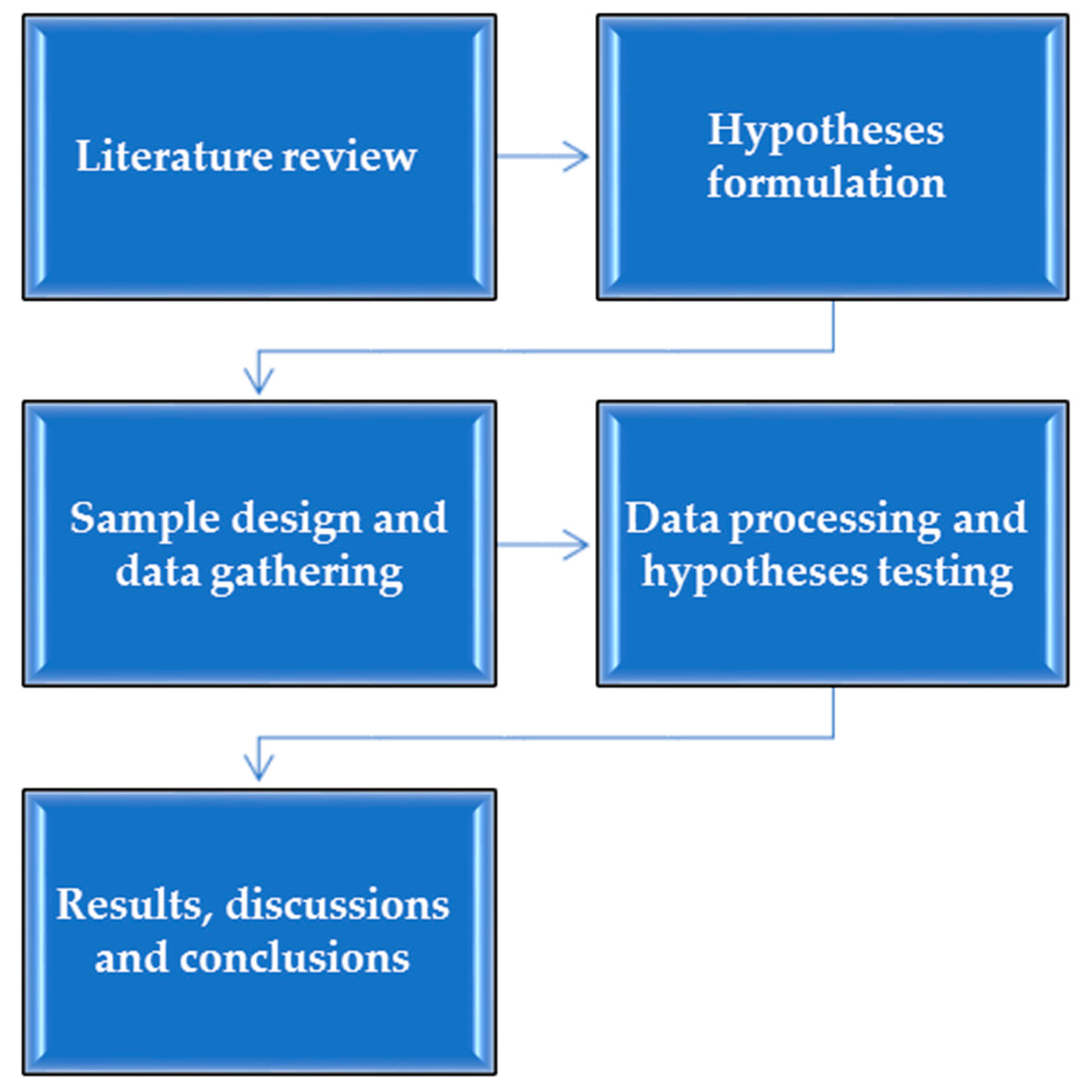

Research on implementing digital technologies in financial, accounting, and managerial information systems in project management assumes five stages. Figure 2 shows the research process.

The research variables (questionnaire items) were selected based on the literature review [10,11,66,67,68,69,70,71,72]. Finally, the questionnaire was used in a survey, and the collected data were processed and interpreted to conclude the impact of digital transformation on project management. Table A1 in Appendix A shows the questionnaire items.

The survey was conducted between June and August 2022. The studied population consisted of Romanian employees working in project management. A total of 486 returned questionnaires were valid out of 500. The sample had a level of confidence of 95%, with a margin of error being 4.42%. Among the total respondents, 52.9% were male, and 47.1% were female. The structure according to age was as follows: 25.1% of respondents were aged 18–30 years; 42% were aged 31–45 years, and 32.9% were aged 46–65 years. The questionnaire used the Likert scale, with five levels for all items. Table 1 shows the structure of the questionnaire and the scales.

PU, PEU, BI, AU, and P are the TAM model’s endogenous (latent) variables. Table 2 shows the descriptive statistics characterizing the observable variables (items in the questionnaire).

The paper used structural equation modeling and artificial neural network analysis to test research hypotheses. Structural equation modeling allows the assessment of the relationships established among the model’s latent (endogenous) variables [73]. Artificial neural network analysis [74] allows for determining the influences of variables in an input layer on the variables in an output layer.

4. Results

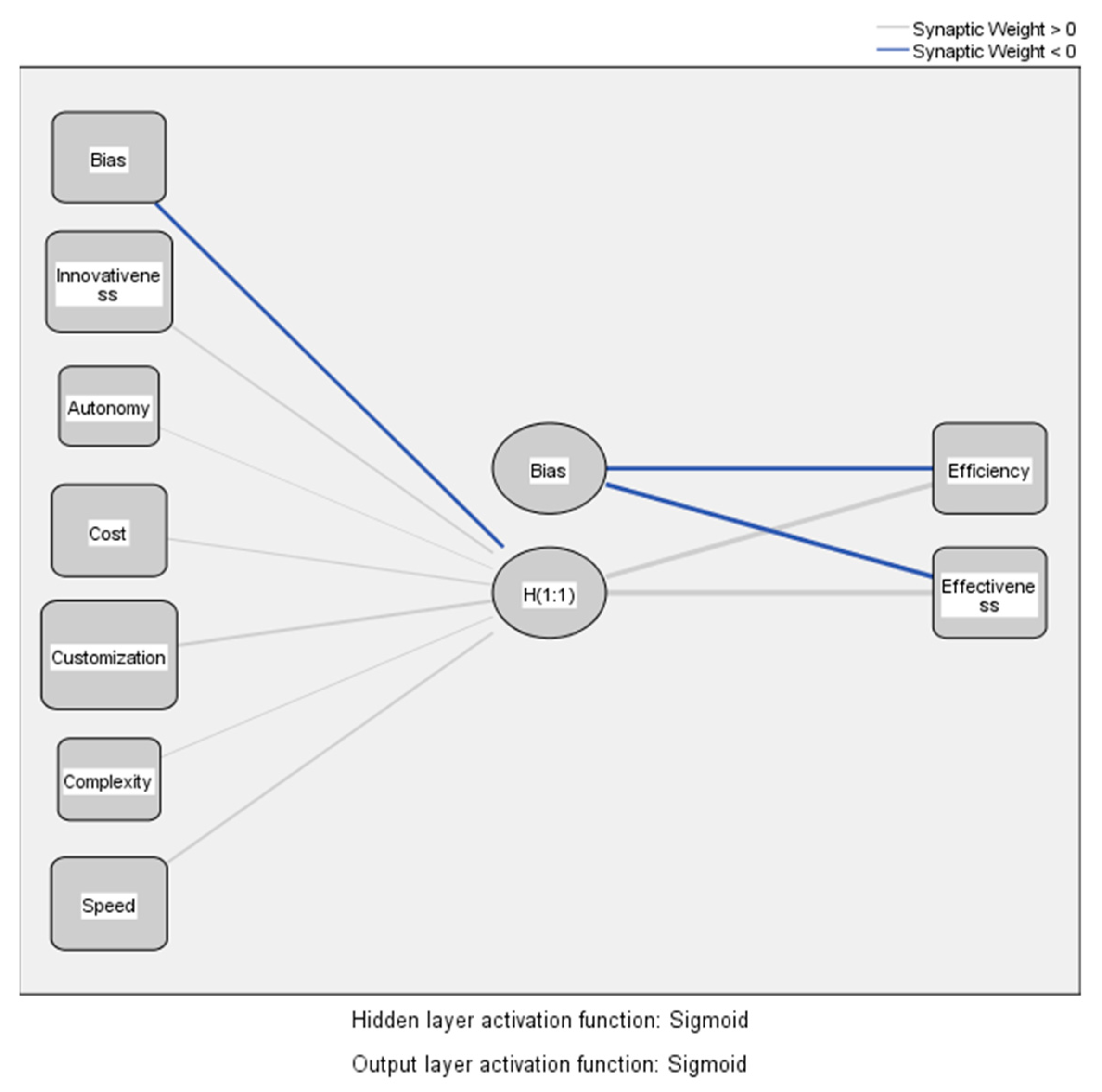

To investigate hypothesis H1, we used the analysis of artificial neural networks. The multilayer perceptron includes in the input layer the characteristics of new technologies implemented in project management (innovativeness, autonomy, cost, customization, complexity, and speed), and in the output layer, the efficiency and effectiveness perceived by the users of these technologies in project management. Between these two layers is an interposed hidden layer represented by the users’ behavioral intention, starting with the perception of the characteristics (Figure 3). The activation function of the hidden layer and the output layer is sigmoid, and the average relative error of the model is 0.236. External influences are the biases acting on the hidden and output layers.

Figure 3 and Table 3 indicate that innovativeness and customization are the characteristics that most influence the efficiency and effectiveness of activities in the perception of project management specialists. Therefore, hypothesis H1 is partially valid. Customization is the most important characteristic that increases the efficiency and effectiveness of the project management employees’ work, followed by innovation.

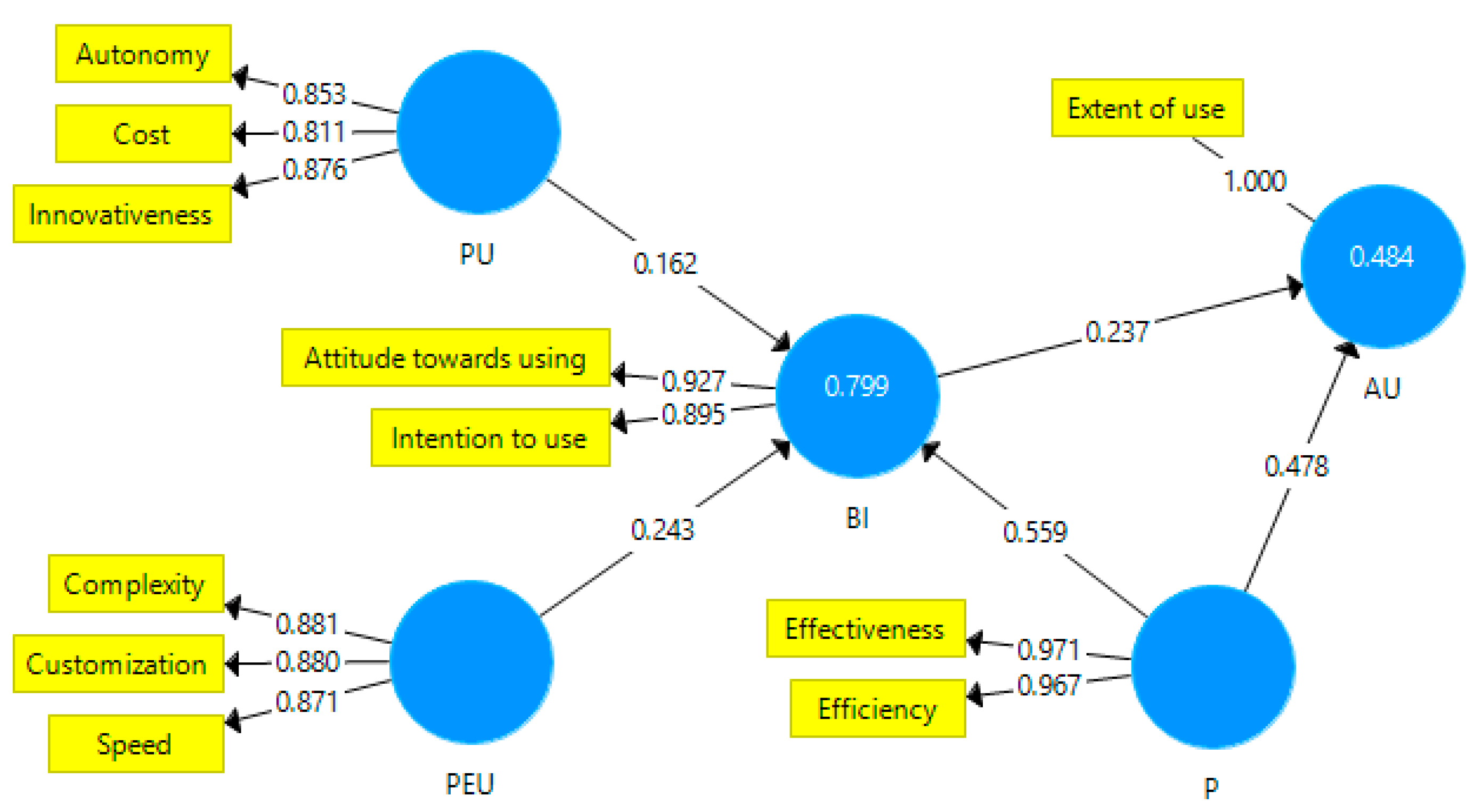

To research the applicability of the TAM model regarding the acceptance of digital technologies in project management, we used the SmartPLS v3.0 software. SmartPLS v3.0 allows partial least squares structural equation modeling. Furthermore, all exogenous variables (represented by questionnaire items) must have a loading greater than 0.7 [73]. Figure 4 shows the TAM model applied in project management.

In order to be valid and reliable, the model must meet certain conditions: Cronbach’s Alpha and Composite Reliability must have values above 0.7; the Average Variance Extracted must have values above 0.7; and SRMR must be below 0.08 [73]. Therefore, the model is valid and reliable (Table 4), with the SRMR being 0.065.

Investigating discriminant validity using the Fornell-Larcker criterion (Table 5), the paper found the model valid.

All values in the matrix are below the values on the main diagonal in both row and column [73].

Following a bootstrapping procedure in SmartPLS 3.0 (with 500 subsamples and a significance level of 0.05), the path coefficients in the TAM model indicate significant positive direct influences among model variables (Table 6).

Hypothesis H2 is partially valid. PU and PEU exert a directly significant positive influence on BI. However, the influence of PU and PEU indirectly exerted on AU with BI as a moderator are relatively small. Hypothesis H3 is valid. P exerts a significant positive influence on BI and AU in the perception of project management specialists. The direct influences on BI and AU are strong (0.559 and 0.478). P also exerts a significant indirect influence (0.133) on future AU, with BI as the moderator.

The proposed conceptual model tested with SEM demonstrates high predictive performance for the PLS path model. Table 7 presents the indicators that describe the model’s predictive performance for the latent variables (actual use and behavioral intention).

The model’s predictive performance provides the opportunity to use the model on other samples in the field of project management or other areas of organizational activity.

5. Discussion

The rapid transformation of the digital environment represents both an opportunity and a challenge for all contemporary organizations due to the development of various technologies (AI, BD, BC, and CC). Furthermore, starting in 2020, the COVID-19 pandemic forced the digitization of many organizational activities, and digital technology became an opportunity for consolidation and accelerated development [75].

An organization’s digital transformation strategy involves the adaptation of traditional activities to digital models or the emergence of new activities generated. Implementing digital technologies allows for a much better response to the challenges of the management and a marketing environment that is constantly changing [6,76]. Contemporary organizations are developing new business models based on digital technologies, accelerating digital transformation [77]. The role of financial, accounting, and managerial information systems in information management is essential to ensure the information necessary for decision-making in project management. Financial, accounting, and managerial information systems are the basis of essential processes in project management: decision-making [3,4,5]. To successfully implement business models based on digital transformation, organizations need to intervene in the organizational culture, change existing organizational processes, and generate a positive perception of digital transformation from their employees [6].

Matt et al. [78] showed that in the process of digital transformation, in addition to innovation strategies, the human resources that develop and manage innovative digital technologies must be taken into account. Therefore, the digital transformation process must be intertwined with organizational culture, and employees must not perceive this process as a threat represented by the mechanical substitution of the human factor. Digital technologies are tools to ease workloads and increase qualification levels. Previous research [79,80,81] has determined that the success of digital transformation strategies depends on the full acceptance by human resources of digital technologies and effective organizational change management.

The current paper proposes a model of acceptance for new digital technologies (TAM) in project management. The current research demonstrates, in line with the findings of Venkatesh and Davis [68], that extending the TAM by including new antecedents characterizing perceived usefulness and ease of use is feasible, leading to model improvement. The paper highlights that among the characteristics of digital technologies taken into account (innovativeness, autonomy, cost, customization, complexity, and speed), customization is the most important characteristic that leads to increasing the efficiency and effectiveness of the project management employees’ work, followed by innovativeness (Hypothesis H1). Similarly to [68,70,82], we believe that additional research is needed on TAM in project management to identify new antecedents of perceived usefulness and ease of use, highlighting the major contingency factors that moderate the effects of the model’s endogenous variables. In line with the results of [68], the paper found that the primary variables of the TAM model (perceived usefulness and perceived ease to use) exert a significant positive influence on behavioral intention, which in turn exerts a significant positive influence on actual use (Hypothesis H2).

Given that digital technologies are becoming increasingly complex and present in project management decision-making and operational processes, this research demonstrates a similarity to [70], that perceived usefulness and ease of use are determinants of behavioral intention. Furthermore, the perception of increasing the efficiency and effectiveness of project management activity exerts a significant positive influence on behavioral intention and actual use (Hypothesis H3). These results also align with the findings of studies from other areas [71,72] that have looked at factors influencing actual use and behavioral intentions influencing new technologies that use TAM. Organizations should also ensure that digital technologies are easy to implement, leading to improved performance through increased efficiency and effectiveness [72].

The opportunities offered by digital technologies are substantial; many processes within accounting and managerial information systems can be carried out with the help of AI, BD, BC, and CC IT solutions. However, although there are many opportunities, there are also several risks, obstacles, and challenges; one of which is the reluctance of project management professionals to confidently adopt digital technologies in their work and use them to make their work easier and achieve better results [83].

Previous research has shown that digital transformation exerts a substantial influence not only on how tasks are carried out within projects, but also affects project planning, project processes, communication and customer relations, and the management of the human resources involved in the project [15,57,76]. Implementing digital technologies in project management leads to changes in project activities, the methodologies used [56], and the way specific processes are carried out, such as, for example, team communication [61].

6. Conclusions

The changes generated by the fourth industrial revolution and the challenges of mobility restrictions presented by the COVID-19 pandemic determined the adoption of transformation strategies based on digital technologies (AI, BD, BC, and CC) that accelerated the digital innovation of organizations. As a result, digital transformation exerts its influence not only on the effective ways of carrying out activities, but also on the strategies adopted, business models, organizational structures, or the skills required of human resources.

6.1. Empirical and Managerial Implications

Based on the results of this study, it is recommended that all organizations continue implementing digital technologies with the support of the organization’s employees. All activities in the project management process can be improved by implementing digital technologies, given the complexity of this process. Among the activities specific to the project management process, calendar programming of activities, risk management, and financial-accounting analysis of the project are the activities that benefit the most from the adoption of digital technologies in terms of the perception of the employees in the organizations.

Among the characteristics of digital technologies taken into account in the empirical study based on the results of previous research (innovativeness, autonomy, cost, customization, complexity, and speed), customization is the most important characteristic that leads to an increase in the efficiency and effectiveness of the activity of project management employees, followed by innovation. Therefore, managers must emphasize these characteristics in facilitating the acceptance of new technologies. Furthermore, the perception of increasing the efficiency and effectiveness of project management employee activity exerts a significant positive influence on the behavioral intention to use digital technologies and their actual use. Increasing the efficiency and effectiveness of activities reduces resistance to change and fear of job losses due to new technologies.

6.2. Theoretical Implications

The literature review identified a gap in empirical research concerning the impact assessment of digital technologies on the financial, accounting, and managerial information systems in terms of the perception of specialists in the field of project management, who use the information obtained through CC and BD, shared through BC and CC, and partially processed with AI. Therefore, conceptual models need to be built, tested, validated, and confirmed through further research, which is crucial for future research. After evaluating the general perception of specialists in project management, we concluded that it is necessary to develop new studies that deepen and consolidate the results obtained after empirical research.

6.3. Limitations and Further Research

One limitation of the current paper is geographical representation (employees of the organizations in Romania). This study evaluates the employees’ perception of the organizations on the effects of the adoption of digital technologies within the financial, accounting, and managerial information systems to digitize the management process of projects. Future research should assess employee perceptions of organizations in other countries, in different contexts, and extend to other management areas. Furthermore, another direction could be to evaluate the impact of each technology on management processes within organizations.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Conflicts of Interest

The author declares no conflict of interest.

Appendix A

Table A1.

Questionnaire items.

| Variables | Items |

|---|---|

| Demographic variables | What is your gender? |

| What is your age range? | |

| PU | On a scale from 1 to 5 (1—non-important, 5—most important), what do you think is the importance of the innovativeness feature on the usefulness of the new digital technology? |

| On a scale from 1 to 5 (1—non-important, 5—most important), what do you think is the importance of the autonomy feature on the usefulness of the new digital technology? | |

| On a scale from 1 to 5 (1—non-important, 5—most important), what do you think is the importance of the cost feature on the usefulness of the new digital technology? | |

| PEU | On a scale from 1 to 5 (1—non-important, 5—most important), what do you think is the importance of the customization feature on the easy-to-use of the new digital technology? |

| On a scale from 1 to 5 (1—non-important, 5—most important), what do you think is the importance of the complexity feature on the easy-to-use of the new digital technology? | |

| On a scale from 1 to 5 (1—non-important, 5—most important), what do you think is the importance of the speed feature on the easy-to-use of the new digital technology? | |

| BI | On a scale from 1 to 5 (1—very poor, 5—very good), what do you think about using new digital technology in project management? |

| On a scale from 1 to 5 (1—very small, 5—very tall), how much do you plan to use the new digital technologies in your activity? | |

| AU | On a scale from 1 to 5 (1—minimal, 5—maximal extent), what do you think will be the degree of use of the new digital technologies? |

| P | On a scale from 1 to 5 (1—very low, 5—very high), what do you think is your efficiency after implementing the new digital technology? |

| On a scale from 1 to 5 (1—very low, 5—very high), what do you think is your effectiveness after implementing the new digital technology? |

References

- Welch, E.W.; Pandey, S.K. E-government and Bureaucracy: Toward a Better Understanding of Intranet Implementation and its Effect on Red Tape. J. Public Adm. Res. Theory 2006, 17, 379–404. [Google Scholar] [CrossRef]

- Welch, E.W.; Feeney, M.K. Technology in Government: How Organizational Culture Mediates Information and Communication Technology Outcomes. Gov. Inf. Q. 2014, 31, 506–512. [Google Scholar] [CrossRef]

- Pickard, M.D.; Cokins, G. From Bean Counters to Bean Growers: Accountants as Data Analysts—A Customer Profitability Example. J. Inf. Syst. 2015, 29, 151–164. [Google Scholar] [CrossRef]

- Huerta, E.; Jensen, S. An Accounting Information Systems Perspective on Data Analytics and Big Data. J. Inf. Syst. 2017, 31, 101–114. [Google Scholar] [CrossRef]

- Coyne, E.M.; Coyne, J.G.; Walker, K.B. Big Data information governance by accountants. Int. J. Account. Inf. Manag. 2018, 26, 153–170. [Google Scholar] [CrossRef] [Green Version]

- Kim, S.-B.; Kim, D. ICT Implementation and Its Effect on Public Organizations: The Case of Digital Customs and Risk Management in Korea. Sustainability 2020, 12, 3421. [Google Scholar] [CrossRef] [Green Version]

- Pazaitis, A. Breaking the Chains of Open Innovation: Post-Blockchain and the Case of Sensorica. Information 2020, 11, 104. [Google Scholar] [CrossRef] [Green Version]

- Chesbrough, H.W. Open Innovation: The New Imperative for Creating and Profiting from Technology; Harvard Business Review Press: Brighton, MA USA, 2006; p. 272. [Google Scholar]

- Schoper, Y.G.; Wald, A.; Ingason, H.T.; Fridgeirsson, T.V. Projectification in Western Economies: A Comparative Study of Germany,. Norway and Iceland. Int. J. Proj. Manag. 2018, 36, 71–82. [Google Scholar] [CrossRef]

- Davis, F.D.; Bagozzi, R.P.; Warshaw, P.R. User Acceptance of Computer Technology: A Comparison of Two Theoretical Models. Manag. Sci. 1989, 35, 982–1003. [Google Scholar] [CrossRef] [Green Version]

- King, W.R.; He, J. A meta-analysis of the technology acceptance model. Inf. Manag. 2006, 43, 740–755. [Google Scholar] [CrossRef]

- International Business Machines (IBM). Digital Transformation: Creating New Business Models Where Digital Meets Physical; IBM: Armonk, NY, USA, 2011. [Google Scholar]

- International Data Corporation (IDC). Digital Transformation (DX): An Opportunity and an Imperative; IDC: Needham, MA, USA, 2015. [Google Scholar]

- Ismail, M.H.; Khater, M.; Zaki, M. Digital business transformation and strategy: What do we know so far. Camb. Serv. Alliance 2017, 10, 1–35. [Google Scholar]

- Westerman, G.; Calméjane, C.; Bonnet, D.; Ferraris, P.; McAfee, A. Digital Transformation: A Roadmap for Billion-dollar Organizations. 2011. Available online: https://www.capgemini.com/wp-content/uploads/2017/07/Digital_Transformation__A_Road-Map_for_Billion-Dollar_Organizations.pdf (accessed on 21 May 2022).

- Chanias, S.; Myers, M.D.; Hess, T. Digital transformation strategy making in pre-digital organizations: The case of a financial services provider. J. Strateg. Inf. Syst. 2019, 28, 17–33. [Google Scholar] [CrossRef]

- Nguyen, T.H.; Nguyen, V.H.; Huy, D.T.N. Transforming the University Management Model in the Concept of Digital Transformation. Rev. Geintec-Gest. Inov. E Tecnol. 2021, 11, 380–387. [Google Scholar] [CrossRef]

- Warner, K.S.; Wäger, M. Building dynamic capabilities for digital transformation: An ongoing process of strategic renewal. Long Range Plan. 2019, 52, 326–349. [Google Scholar] [CrossRef]

- Andersen, N. Blockchain Technology: A Game-Changer in Accounting. 2016. Available online: https://www2.deloitte.com/content/dam/Deloitte/de/Documents/Innovation/Blockchain_A%20game-changer%20in%20accounting.pdf (accessed on 11 May 2022).

- Brandon, D. The Blockchain: The future of business information systems. Int. J. Acad. Bus. World 2016, 10, 33–40. [Google Scholar]

- Kakavand, H.; Kost de Sevres, N.; Chilton, B. The Blockchain Revolution: An Analysis of Regulation and Technology Related to Distributed Ledger Technologies. 2017. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2849251. [CrossRef] [Green Version]

- Dai, J.; Wang, Y.; Vasarhelyi, M.A. Blockchain: An emerging solution for fraud prevention. CPA J. 2017, 87, 12–14. [Google Scholar]

- Bible, W.; Raphael, J.; Riviello, M.; Taylor, P.; Valiente, I.O. Blockchain Technology and Its Potential Impact on the Audit and Assurance Profession. 2017. Available online: https://us.aicpa.org/content/dam/aicpa/interestareas/frc/assuranceadvisoryservices/downloadabledocuments/blockchain-technology-and-its-potential-impact-on-the-audit-and-assurance-profession.pdf (accessed on 25 April 2022).

- Mistry, I.; Tanwar, S.; Tyagi, S.; Kumar, N. Blockchain for 5G-enabled IoT for industrial automation: A systematic review, solutions, and challenges. Mech. Syst. Signal Process. 2020, 135, 106382. [Google Scholar] [CrossRef]

- ICAEW. Blockchain and The Future of Accountancy. Available online: https://www.icaew.com/technical/technology/blockchain/blockchain-articles/blockchain-and-the-accounting-perspective (accessed on 22 March 2022).

- Bhimani, A.; Willcocks, L. Digitisation, Big Data and the transformation of accounting information. Account. Bus. Res. 2014, 44, 469–490. [Google Scholar] [CrossRef]

- Loebbecke, C.; Picot, A. Reflections on societal and business model transformation arising from digitization and big data analytics: A research agenda. J. Strateg. Inf. Syst. 2015, 24, 149–157. [Google Scholar] [CrossRef]

- Matzler, K.; von den Eichen, S.F.; Anschober, M.; Kohler, T. The crusade of digital disruption. J. Bus. Strategy 2018, 39, 13–20. [Google Scholar] [CrossRef]

- Huang, M.; Rust, T.R. Artificial intelligence in service. J. Serv. Res. 2018, 21, 155–172. [Google Scholar] [CrossRef]

- Rachinger, M.; Rauter, R.; Müller, C.; Vorraber, W.; Schirgi, E. Digitalization and its influence on business model innovation. J. Manuf. Technol. Manag. 2019, 30, 1143–1160. [Google Scholar] [CrossRef]

- Stoica, O.C.; Ionescu-Feleagă, L. Digitalization in Accounting: A Structured Literature Review. In Proceedings of the 4th International Conference on Economics and Social Sciences: Resilience and Economic Intelligence through Digitalization and Big Data Analytics, Sciendo, Bucharest, Romania, 10–11 June 2021; pp. 453–464. [Google Scholar] [CrossRef]

- Belfo, F.P.; Trigo, A. Accounting Information Systems: Tradition and Future Directions. Procedía Technol. 2013, 9, 536–546. [Google Scholar] [CrossRef] [Green Version]

- Taipaleenmäki, J.; Ikäheimo, S. On the convergence of management accounting and financial accounting—the role of information technology in accounting change. Int. J. Account. Inf. Syst. 2013, 14, 321–348. [Google Scholar] [CrossRef]

- Arnold, V. The changing technological environment and the future of behavioral research in accounting. Account. Financ. 2018, 58, 315–339. [Google Scholar] [CrossRef]

- Kroon, N.; Alves, M.d.C.; Martins, I. The Impacts of Emerging Technologies on Accountants’ Role and Skills: Connecting to Open Innovation—A Systematic Literature Review. J. Open Innov. Technol. Mark. Complex. 2021, 7, 163. [Google Scholar] [CrossRef]

- Marrone, M.; Hazelton, J. The disruptive and transformative potential of new technologies for accounting, accountants and accountability: A review of current literature and call for further research. Med. Account. Res. 2019, 27, 677–694. [Google Scholar] [CrossRef]

- Chiu, V.; Liu, Q.; Muehlmann, B.; Baldwin, A.A. A bibliometric analysis of accounting information systems journals and their emerging technologies contributions. Int. J. Account. Inf. Syst. 2019, 32, 24–43. [Google Scholar] [CrossRef]

- Abad-Segura, E.; González-Zamar, M.-D. Research Analysis on Emerging Technologies in Corporate Accounting. Mathematics 2020, 8, 1589. [Google Scholar] [CrossRef]

- Fullana, O.; Ruiz, J. Accounting Information Systems in the Blockchain Era. 2020. Available online: https://ssrn.com/abstract=3517142 (accessed on 7 July 2020).

- Lamboglia, R.; Lavorato, D.; Scornavacca, E.; Za, S. Exploring the relationship between audit and technology. A bibliometric analysis. Med. Account. Res. 2020, 29, 1233–1260. [Google Scholar] [CrossRef]

- Wolf, T.; Kuttner, M.; Feldbauer-Durstmüller, B.; Mitter, C. What we know about management accountants’ changing identities and roles—A systematic literature review. J. Account. Organ. Chang. 2020, 16, 311–347. [Google Scholar] [CrossRef]

- Richins, G.; Stapleton, A.; Stratopoulos, T.; Wong, C. Big Data Analytics: Opportunity or Threat for the Accounting Profession? J. Inf. Syst. 2017, 31, 63–79. [Google Scholar] [CrossRef]

- Al-Htaybat, K.; Von Alberti-Alhtaybat, L. Big Data and corporate reporting: Impacts and paradoxes. Account. Audit. Account. J. 2017, 30, 850–873. [Google Scholar] [CrossRef]

- Marshall, T.E.; Lambert, S.L. Cloud-Based Intelligent Accounting Applications: Accounting Task Automation Using IBM Watson Cognitive Computing. J. Emerg. Technol. Account. 2018, 15, 199–215. [Google Scholar] [CrossRef]

- Kokina, J.; Kozlowski, S. The next frontier in data analytics. J. Account. 2016, 222, 58. Available online: https://ssrn.com/abstract=3334728 (accessed on 23 March 2022).

- Parot, A.; Michell, K.; Kristjanpoller, W.D. Using Artificial Neural Networks to forecast Exchange Rate, including VAR-VECM residual analysis and prediction linear combination. Intell. Syst. Account. Financ. Manag. 2019, 26, 3–15. [Google Scholar] [CrossRef] [Green Version]

- Paschen, U.; Pitt, C.; Kietzmann, J. Artificial intelligence: Building blocks and an innovation typology. Bus. Horiz. 2020, 63, 147–155. [Google Scholar] [CrossRef]

- KPMG. Rise of the Humans: The Integration of Digital and Human Labor. Available online: https://advisory.kpmg.us/articles/2017/rise-of-the-humans-1.html (accessed on 15 May 2022).

- PwC. Sizing the Prize. What’s the Real Value of AI for Your Business, and How Can You Capitalise? Available online: https://www.pwc.com/gx/en/issues/data-and-analytics/publications/artificial-intelligence-study.html (accessed on 15 May 2022).

- Kokina, J.; Mancha, R.; Pachamanova, D. Blockchain: Emergent Industry Adoption and Implications for Accounting. J. Emerg. Technol. Account. 2017, 14, 91–100. [Google Scholar] [CrossRef]

- Yu, T.; Lin, Z.; Tang, Q. Blockchain: The Introduction and Its Application in Financial Accounting. J. Corp. Account. Financ. 2018, 29, 37–47. [Google Scholar] [CrossRef]

- Karajovic, M.; Kim, H.M.; Laskowski, M. Thinking outside the Block: Projected Phases of Blockchain Integration in the Accounting Industry. Aust. Account. Rev. 2019, 29, 319–330. [Google Scholar] [CrossRef]

- Fuller, S.H.; Markelevich, A. Should accountants care about blockchain? J. Corp. Account. Financ. 2020, 31, 34–46. [Google Scholar] [CrossRef]

- Secinaro, S.; Calandra, D.; Biancone, P. Blockchain, trust, and trust accounting: Can blockchain technology substitute trust created by intermediaries in trust accounting? A theoretical examination. Int. J. Manag. Pract. 2021, 14, 129–145. [Google Scholar] [CrossRef]

- Gardner, E.C.; Bryson, J.R. The dark side of the industrialisation of accountancy: Innovation, commoditization, colonization and competitiveness. Ind. Innov. 2021, 28, 42–57. [Google Scholar] [CrossRef]

- Whyte, J.; Stasis, A.; Lindkvist, C. Managing Change in the Delivery of Complex Projects: Configuration Management, Asset Information and ‘Big Data’. Int. J. Proj. Manag. 2016, 34, 339–351. [Google Scholar] [CrossRef] [Green Version]

- Kozarkiewicz, A. General and specific: The impact of digital transformation on project processes and management methods. Found. Manag. 2020, 12, 237–248. [Google Scholar] [CrossRef]

- Papadonikolaki, E.; van Oel, C.; Kagioglou, M. Organising and Managing Boundaries: A structurational View of Collaboration with Building Information Modelling (BIM). Int.J. Proj. Manag. 2019, 37, 378–394. [Google Scholar] [CrossRef]

- Kinkela, K.; College, I. Practical and ethical considerations on the use of cloud computing in accounting. J. Financ. Account. 2013, 11, 1. Available online: https://www.aabri.com/manuscripts/131534.pdf (accessed on 20 April 2022).

- Zhang, C. Challenges and Strategies of Promoting Cloud Accounting. Manag. Eng. 2014, 17, 79–82. [Google Scholar] [CrossRef]

- Huang, N. Discussion on the Application of Cloud Accounting in Enterprise Accounting Informatization. In Proceedings of the International Conference on Economics, Social Science, Arts, Education, and Management Engineering, Huhhot, China, 30–31 July 2016; pp. 136–139. [Google Scholar] [CrossRef] [Green Version]

- Ionescu, B.S.; Prichici, C.; Tudoran, L. Cloud Accounting—A Technology That May Change the Accounting Profession in Romania. Audit. Financ. J. 2018, 12, 3–15. Available online: https://www.cafr.ro/uploads/AF%202%202014-e16d.pdf (accessed on 5 May 2022).

- Guinan, P.J.; Parise, S.; Langowitz, N. Creating an Innovative Digital Project Team: Levers to Enable Digital Transformation. Bus. Horiz. 2019, 62, 717–727. [Google Scholar] [CrossRef]

- Mangla, S.K.; Raut, R.; Narwane, V.S.; Zhang, Z. Mediating Effect of Big Data Analytics on Project Performance of Small and Medium Enterprises. J. Enterp. Inf. Manag. 2020, 34, 168–198. [Google Scholar] [CrossRef]

- Sichel, D.E. The Computer Revolution: An Economic Perspective; Brookings Institution: Washington, DC, USA, 1997. [Google Scholar]

- Park, E.S.; Park, M.S. Factors of the Technology Acceptance Model for Construction IT. Appl. Sci. 2020, 10, 8299. [Google Scholar] [CrossRef]

- Chau, P.Y.K. An empirical assessment of a modified technology acceptance model. J. Manag. Inf. Syst. 1996, 13, 185–204. [Google Scholar] [CrossRef]

- Venkatesh, V.; Davis, F.D. A Theoretical Extension of the Technology Acceptance Model: Four Longitudinal Field Studies. Manag. Sci. 2000, 46, 186–204. [Google Scholar] [CrossRef] [Green Version]

- Gefen, D. TAM or just plain habit: A look at experienced online shoppers. J. Organ. End User Comput. 2003, 15, 1–13. [Google Scholar] [CrossRef] [Green Version]

- Venkatesh, V.; Bala, H. Technology Acceptance Model 3 and a Research Agenda on Interventions. Decis. Sci. 2008, 39, 273–315. [Google Scholar] [CrossRef] [Green Version]

- Ngubelanga, A.; Duffett, R. Modeling Mobile Commerce Applications’ Antecedents of Customer Satisfaction among Millennials: An Extended TAM Perspective. Sustainability 2021, 13, 5973. [Google Scholar] [CrossRef]

- Na, S.; Heo, S.; Han, S.; Shin, Y.; Roh, Y. Acceptance Model of Artificial Intelligence (AI)-Based Technologies in Construction Firms: Applying the Technology Acceptance Model (TAM) in Combination with the Technology-Organisation-Environment (TOE) Framework. Buildings 2022, 12, 90. [Google Scholar] [CrossRef]

- Hair, J.F.; Hult, G.T.M.; Ringle, C.M.; Sarstedt, M.A. Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM), 2nd ed.; Sage: Thousand Oaks, CA, USA, 2017. [Google Scholar]

- I.B.M. SPSS—Neural Networks. 2012. Available online: https://www.ibm.com/downloads/cas/N7LLA2LB (accessed on 15 May 2022).

- Lim, W.M. History, lessons, and ways forward from the COVID-19 pandemic. Int. J. Qual. Innov. 2021, 5, 101108. [Google Scholar]

- Vial, G. Understanding digital transformation: A review and a research agenda. J. Strateg. Inf. Syst. 2019, 28, 118–144. [Google Scholar] [CrossRef]

- Verhoef, P.C.; Broekhuizen, T.; Bart, Y.; Bhattacharya, A.; Dong, J.Q.; Fabian, N.; Haenlein, M. Digital transformation: A multidisciplinary relection and research agenda. J. Bus. Res. 2021, 122, 889–901. [Google Scholar] [CrossRef]

- Matt, C.; Hess, T.; Benlian, A. Digital transformation strategies. Bus. Inf. Syst. Eng. 2015, 57, 339–343. [Google Scholar] [CrossRef]

- Nylén, D.; Holmström, J. Digital innovation strategy: A framework for diagnosing and improving digital product and service innovation. Bus. Horiz. 2015, 58, 57–67. [Google Scholar] [CrossRef] [Green Version]

- Correani, A.; de Massis, A.; Frattini, F.; Petruzzelli, A.M.; Natalicchio, A. Implementing a digital strategy: Learning from the experience of three digital transformation projects. Calif. Manag. Rev. 2020, 62, 37–56. [Google Scholar] [CrossRef]

- Sandberg, J.; Holmström, J.; Lyytinen, K. Digitization and phase transitions in platform organizing logics: Evidence from the process automation industry. MIS Q. 2020, 44, 129–153. [Google Scholar] [CrossRef]

- Venkatesh, V.; Morris, M.G.; Davis, G.B.; Davis, F.D. User acceptance of information technology: Toward a unified view. MIS Q. 2003, 27, 425–478. [Google Scholar] [CrossRef] [Green Version]

- Burns, M.B.; Igou, A. “Alexa, Write an Audit Opinion”: Adopting Intelligent Virtual Assistants in Accounting Workplaces. J. Emerg. Technol. Account. 2019, 16, 81–92. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Figure 2.

Research process. Source: own construction.

Figure 3.

Multilayer perceptron for digital transformation in project management. Source: author’s design using SPSS v.20.

Figure 3.

Multilayer perceptron for digital transformation in project management. Source: author’s design using SPSS v.20.

Figure 4.

Empirical model. Source: author’s design using SmartPLS v3.0.

Table 1.

Questionnaire design (constructs and items).

| Variables | Items | Scales |

|---|---|---|

| Demographic variables | Gender | Male(1), Female (2) |

| Age | 18–30 years (1), 31–45 years (2), 46–65 years (3) | |

| PU | Innovativeness | 1 to 5 (1—non-important, 5—most important) |

| Autonomy | ||

| Cost | ||

| PEU | Customization | |

| Complexity | ||

| Speed | ||

| BI | Attitude toward using | 1 to 5 (1—very poor, 5—very good) |

| Intention to use | 1 to 5 (1—very small, 5—very tall) | |

| AU | Extent of use | 1 to 5 (1—minimal, 5—maximal extent) |

| P | Efficiency | On a scale of 1 to 5 (1—very low, 5—very high) |

| Effectiveness |

Table 2.

Descriptive statistics.

| Min | Max | Mean | Std. Deviation | Skewness | Kurtosis | |

|---|---|---|---|---|---|---|

| Sex | 1 | 2 | 1.47 | 0.500 | 0.116 | −1.995 |

| Age | 1 | 3 | 2.08 | 0.758 | −0.131 | −1.250 |

| Innovativeness | 1 | 5 | 3.69 | 0.868 | −0.104 | −0.531 |

| Autonomy | 2 | 5 | 3.94 | 0.851 | −0.463 | −0.399 |

| Cost | 1 | 5 | 3.96 | 0.868 | −0.624 | 0.096 |

| Customization | 1 | 5 | 3.82 | 0.942 | −0.533 | −0.419 |

| Complexity | 2 | 5 | 4.02 | 0.957 | −0.623 | −0.634 |

| Speed | 2 | 5 | 3.82 | 0.994 | −0.393 | −0.907 |

| Attitude toward using | 1 | 5 | 3.53 | 0.964 | −0.106 | −0.829 |

| Intention to use | 1 | 5 | 3.81 | 0.881 | −0.493 | −0.120 |

| Extent of use | 1 | 5 | 3.74 | 0.965 | −0.562 | −0.088 |

| Efficiency | 1 | 5 | 3.85 | 0.933 | −0.393 | −0.675 |

| Effectiveness | 1 | 5 | 3.28 | 1.287 | −0.174 | −1.062 |

Source: author’s design using SPSS v.20.

Table 3.

Predictors for digital transformation in project management.

| Predictor | Hidden Layer 1 | Output Layer | Importance | Importance Normalized | ||

|---|---|---|---|---|---|---|

| H(1:1) | Efficiency | Effectiveness | ||||

| Input Layer | (Bias) | −0.470 | ||||

| Innovativeness | 0.291 | 0.235 | 78.5% | |||

| Autonomy | 0.099 | 0.060 | 19.8% | |||

| Cost | 0.197 | 0.159 | 53.1% | |||

| Customization | 0.400 | 0.300 | 100.0% | |||

| Complexity | 0.143 | 0.078 | 26.0% | |||

| Speed | 0.307 | 0.168 | 55.9% | |||

| Hidden Layer 1 | (Bias) | −0.939 | −2.335 | |||

| H(1:1) | 4.801 | 6.472 | ||||

Source: author’s design using SPSS v.20.

Table 4.

Validity and reliability.

| Cronbach’s Alpha | Composite Reliability | Average Variance Extracted | |

|---|---|---|---|

| BI | 0.797 | 0.907 | 0.831 |

| P | 0.935 | 0.969 | 0.939 |

| PEU | 0.851 | 0.909 | 0.770 |

| PU | 0.803 | 0.884 | 0.718 |

Source: author’s design using SmartPLS v3.0.

Table 5.

Discriminant validity.

| AU | BI | P | PEU | PU | |

|---|---|---|---|---|---|

| AU | 1.000 | ||||

| BI | 0.657 | 0.911 | |||

| P | 0.686 | 0.880 | 0.969 | ||

| PEU | 0.563 | 0.791 | 0.823 | 0.877 | |

| PU | 0.605 | 0.713 | 0.748 | 0.547 | 0.847 |

Source: author’s design using SmartPLS v3.0.

Table 6.

Path coefficients.

| Coefficients | T Statistics | p Values | ||

|---|---|---|---|---|

| Direct effects | PEU—>BI (H2) | 0.243 | 6.745 | 0.000 |

| PU—>BI (H2) | 0.162 | 5.851 | 0.000 | |

| BI—>AU (H2) | 0.237 | 3.134 | 0.002 | |

| P—>AU (H3) | 0.478 | 6.914 | 0.000 | |

| P—>BI (H3) | 0.559 | 13.733 | 0.000 | |

| Specific indirect effects | PEU—>BI—>AU (H2) | 0.058 | 2.873 | 0.004 |

| PU—>BI—>AU (H2) | 0.038 | 2.605 | 0.009 | |

| P—>BI—>AU (H3) | 0.133 | 3.037 | 0.003 |

Source: author’s design using SmartPLS v3.0.

Table 7.

Predictive performance for the PLS paths model.

| RMSE | MAE | Q2_Predict | |

|---|---|---|---|

| Extent of use | 0.701 | 0.573 | 0.474 |

| Attitude towards using | 0.476 | 0.397 | 0.757 |

| Intention to use | 0.588 | 0.489 | 0.555 |

| AU | 0.728 | 0.595 | 0.474 |

| BI | 0.452 | 0.369 | 0.797 |

Source: own construction using SmartPLS v3.0.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Vărzaru, A.A. An Empirical Framework for Assessing the Digital Technologies Users’ Acceptance in Project Management. Electronics 2022, 11, 3872. https://doi.org/10.3390/electronics11233872

AMA Style

Vărzaru AA. An Empirical Framework for Assessing the Digital Technologies Users’ Acceptance in Project Management. Electronics. 2022; 11(23):3872. https://doi.org/10.3390/electronics11233872

Chicago/Turabian StyleVărzaru, Anca Antoaneta. 2022. "An Empirical Framework for Assessing the Digital Technologies Users’ Acceptance in Project Management" Electronics 11, no. 23: 3872. https://doi.org/10.3390/electronics11233872

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.