Assessing Users’ Behavior on the Adoption of Digital Technologies in Management and Accounting Information Systems

,

,  , and

, and

Abstract

:1. Introduction

2. Literature Review

3. Materials and Methods

4. Results

5. Discussion

5.1. Empirical and Managerial Implications and Contributions

5.2. Theoretical Implications and Contributions

5.3. Limitations and Further Research

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Abbreviations

| Acronyms | |

| AI | Artificial intelligence |

| BD | Big data |

| BC | Blockchain |

| CC | Cloud computing |

| PM | Project management |

| Mk | Marketing |

| DMP | Decision-making process |

| TAM | Technology Acceptance Model |

| PMTU | Perceptual model of the technology’s usefulness |

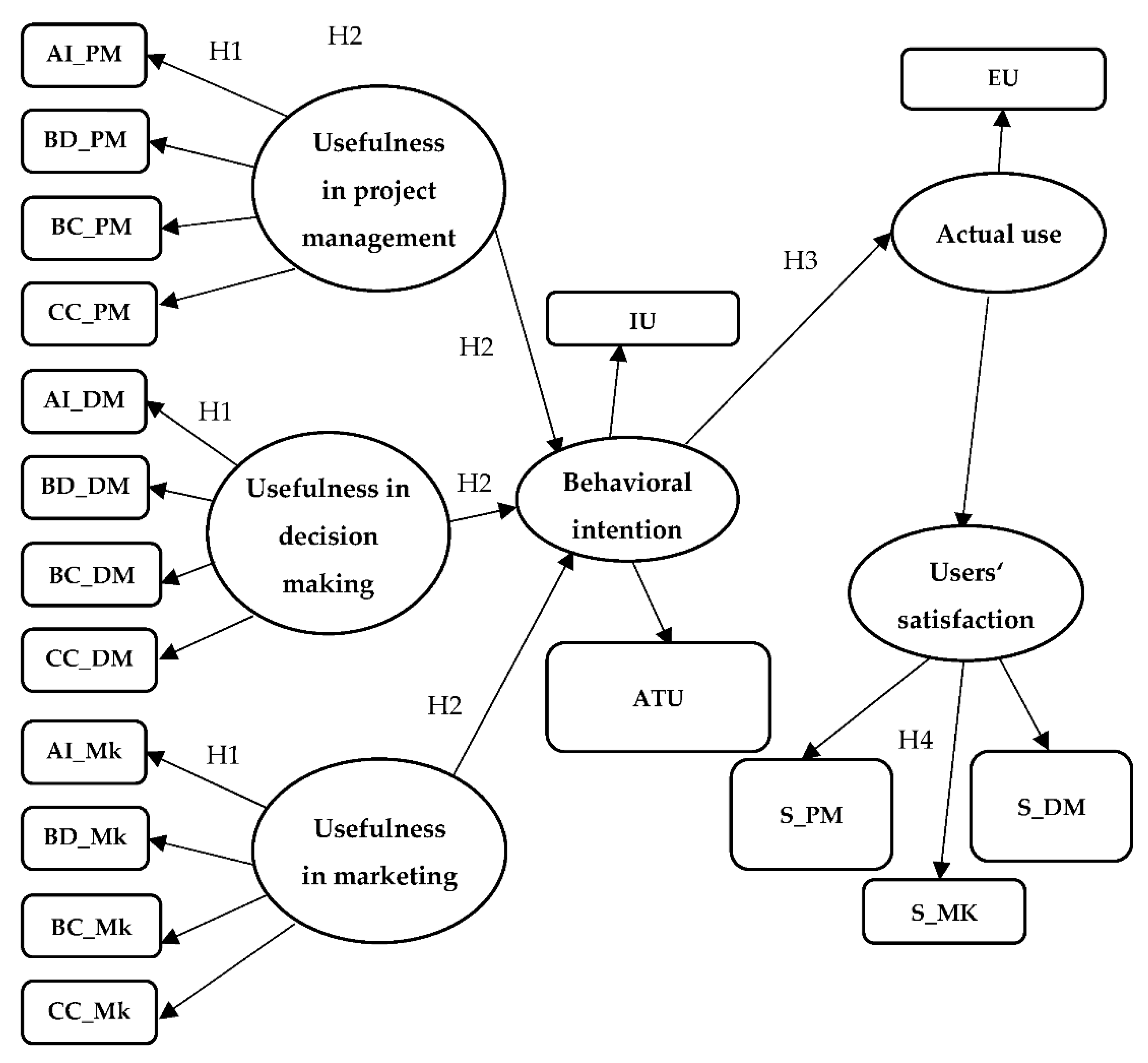

| AI_PM | The usefulness of artificial intelligence in project management |

| BD_PM | The usefulness of big data in project management |

| BC_PM | The usefulness of blockchain in project management |

| CC_PM | The usefulness of cloud computing in project management |

| AI_DM | The usefulness of artificial intelligence in decision making |

| BD_DM | The usefulness of big data in decision making |

| BC_DM | The usefulness of blockchain in decision making |

| CC_DM | The usefulness of cloud computing in decision making |

| AI_Mk | The usefulness of artificial intelligence in marketing |

| BD_Mk | The usefulness of big data in marketing |

| BC_Mk | The usefulness of blockchain in marketing |

| CC_Mk | The usefulness of cloud computing in marketing |

References

- Haenlein, M.; Kaplan, A. A brief history of artificial intelligence: On the past, present, and future of artificial intelligence. Calif. Manag. Rev. 2019, 61, 5–14. [Google Scholar] [CrossRef]

- Koh, L.; Orzes, G.; Jia, F. The fourth industrial revolution (Industry 4.0): Technologies disruption on operations and supply chain management. Int. J. Oper. Prod. Manag. 2019, 39, 817–828. [Google Scholar] [CrossRef]

- Matzler, K.; von den Eichen, S.F.; Anschober, M.; Kohler, T. The crusade of digital disruption. J. Bus. Strategy 2018, 39, 13–20. [Google Scholar] [CrossRef]

- Loebbecke, C.; Picot, A. Reflections on societal and business model transformation arising from digitization and big data analytics: A research agenda. J. Strateg. Inf. Syst. 2015, 24, 149–157. [Google Scholar] [CrossRef]

- Rachinger, M.; Rauter, R.; Müller, C.; Vorraber, W.; Schirgi, E. Digitalization and its influence on business model innovation. J. Manuf. Technol. Manag. 2019, 30, 1143–1160. [Google Scholar] [CrossRef] [Green Version]

- Lichtenthaler, U.C. Digitainability: The Combined Effects of the Megatrends Digitalization and Sustainability. J. Innov. Manag. 2021, 9, 64–80. [Google Scholar] [CrossRef]

- Marszatek, P.; Ratajczak-Mrozek, M. Introduction: Digitalization as a Driver of the Contemporary Economy. In Digitalization and Firm Performance; Ratajczak-Mrozek, M., Marszatek, P., Eds.; Palgrave Macmillan: Cham, Switzerland, 2022. [Google Scholar] [CrossRef]

- Rikhardsson, P.; Yigitbasioglu, O. Business intelligence & analytics in management accounting research: Status and future focus. Int. J. Account. Inf. Syst. 2018, 29, 37–58. [Google Scholar]

- Yoon, S. A Study on the Transformation of Accounting Based on New Technologies: Evidence from Korea. Sustainability 2020, 12, 8669. [Google Scholar] [CrossRef]

- Rao, M.T.; Jyotsna, T.G.; Sivani, M.A. Impact of Cloud Accounting: Accounting Professional’s perspective. IOSR J. Bus. Manag. 2017, 7, 53–59. Available online: https://www.iosrjournals.org/iosr-jbm/papers/Conf.17037-2017/Volume-7/11.%2053-59.pdf (accessed on 15 May 2022).

- David, D.; Cernuşca, L. The Perception of Professional Accountants Regarding the Future of the Accounting Profession in the Digital Era. CECCAR Bus. Rev. 2020, 7, 3–10. [Google Scholar] [CrossRef]

- Kinkela, K.; College, I. Practical and Ethical Considerations on the Use of Cloud Computing in Accounting. J. Financ. Account. 2013, 11, 1–8. Available online: https://www.aabri.com/manuscripts/131534.pdf (accessed on 20 June 2022).

- Zhang, C. Challenges and Strategies of Promoting Cloud Accounting. Manag. Eng. 2014, 17, 79–82. Available online: https://cdn.manaraa.com/books/Challenges%20and%20Strategies%20of%20Promoting%20Cloud%20Accounting.pdf (accessed on 18 May 2022).

- Huang, N. Discussion on the Application of Cloud Accounting in Enterprise Accounting Informatization. In Proceedings of the International Conference on Economics, Social Science, Arts, Education, and Management Engineering, Huhhot, China, 30–31 July 2016; pp. 136–139. [Google Scholar] [CrossRef]

- Ionescu, B.S.; Prichici, C.; Tudoran, L. Cloud Accounting—A Technology That May Change the Accounting Profession in Romania. Audit. Financ. J. 2018, 12, 3–15. Available online: https://www.cafr.ro/uploads/AF%202%202014-e16d.pdf (accessed on 5 May 2022).

- Christauskas, C.; Misevicience, R. Cloud computing based accounting for small to medium-sized business. Inz. Ekon. Eng. Econ. 2012, 23, 14–21. [Google Scholar] [CrossRef]

- Bhimani, A.; Willcocks, L. Digitisation, Big Data and the transformation of accounting information. Account. Bus. Res. 2014, 44, 469–490. [Google Scholar] [CrossRef]

- Stoica, O.C.; Ionescu-Feleagă, L. Digitalization in Accounting: A Structured Literature Review. In Proceedings of the 4th International Conference on Economics and Social Sciences: Resilience and Economic Intelligence through Digitalization and Big Data Analytics, Sciendo, Bucharest, Romania, 10–11 June 2021; pp. 453–464. [Google Scholar] [CrossRef]

- Kokina, J.; Kozlowski, S. The Next Frontier in Data Analytics. J. Account. 2016, 222, 58. Available online: https://ssrn.com/abstract=3334728 (accessed on 23 May 2022).

- Deloitte. AI-Augmented Government: Using Cognitive Technologies to Redesign Public Sector Work. 2017. Available online: https://www2.deloitte.com/content/dam/insights/us/articles/3832_AI-augmented-government/DUP_AI-augmented-government.pdf (accessed on 18 June 2022).

- Parot, A.; Michell, K.; Kristjanpoller, W.D. Using Artificial Neural Networks to forecast Exchange Rate, including VAR-VECM residual analysis and prediction linear combination. Intell. Syst. Account. Financ. Manag. 2019, 26, 3–15. [Google Scholar] [CrossRef] [Green Version]

- Paschen, U.; Pitt, C.; Kietzmann, J. Artificial intelligence: Building blocks and an innovation typology. Bus. Horiz. 2020, 63, 147–155. [Google Scholar] [CrossRef]

- KPMG. Rise of the Humans: The Integration of Digital and Human Labor. Available online: https://assets.kpmg/content/dam/kpmg/us/pdf/2017/09/us-rise-of-the-humans.pdf (accessed on 15 June 2022).

- PwC. Sizing the Prize. What’s the Real Value of AI for Your Business, and How Can You Capitalize? Available online: https://www.pwc.com/gx/en/issues/data-and-analytics/publications/artificial-intelligence-study.html (accessed on 15 June 2022).

- Lee, H.; Yoon, N.; Park, S.; Lee, C.; Hwang, S. A study on the accounting information system based on blockchain. Korean Account. J. 2019, 28, 273–300. [Google Scholar] [CrossRef]

- Andersen, N. Blockchain Technology: A Game-Changer in Accounting. 2016. Available online: https://www2.deloitte.com/content/dam/Deloitte/de/Documents/Innovation/Blockchain_A%20game-changer%20in%20accounting.pdf (accessed on 2 June 2022).

- Brandon, D. The Blockchain: The Future of Business Information Systems. Int. J. Acad. Bus. World 2016, 10, 33–40. Available online: https://jwpress.com/Journals/IJABW/BackIssues/IJABW-Fall-2016.pdf#page=28 (accessed on 19 May 2022).

- Kakavand, H.; Kost De Sevres, N.; Chilton, B. The Blockchain Revolution: An Analysis of Regulation and Technology Related to Distributed Ledger Technologies. 2017. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2849251 (accessed on 7 June 2022).

- Dai, J.; Wang, Y.; Vasarhelyi, M.A. Blockchain: An emerging solution for fraud prevention. CPA J. 2017, 87, 12–14. [Google Scholar]

- Bible, W.; Raphael, J.; Riviello, M.; Taylor, P.; Valiente, I.O. Blockchain Technology and Its Potential Impact on the Audit and Assurance Profession. 2017. Available online: https://us.aicpa.org/content/dam/aicpa/interestareas/frc/assuranceadvisoryservices/downloadabledocuments/blockchain-technology-and-its-potential-impact-on-the-audit-and-assurance-profession.pdf (accessed on 25 April 2022).

- ICAEW. Blockchain and the Future of Accountancy. Available online: https://www.icaew.com/technical/technology/blockchain/blockchain-articles/blockchain-and-the-accounting-perspective (accessed on 22 June 2022).

- Mistry, I.; Tanwar, S.; Tyagi, S.; Kumar, N. Blockchain for 5G-enabled IoT for industrial automation: A systematic review, solutions, and challenges. Mech. Syst. Signal Process 2020, 135, 106382. [Google Scholar] [CrossRef]

- Gonçalves, M.J.A.; da Silva, A.C.F.; Ferreira, C.G. The Future of Accounting: How Will Digital Transformation Impact the Sector? Informatics 2022, 9, 19. [Google Scholar] [CrossRef]

- Quattrone, P. Management accounting goes digital: Will the move make it wiser? Manag. Account. Res. 2016, 31, 118–122. [Google Scholar] [CrossRef] [Green Version]

- Richins, G.; Stapleton, A.; Stratopoulos, T.; Wong, C. Big Data Analytics: Opportunity or Threat for the Accounting Profession? J. Inf. Syst. 2017, 31, 63–79. [Google Scholar] [CrossRef]

- Moll, J.; Yigitbasioglu, O. The role of internet-related technologies in shaping the work of accountants: New directions for accounting research. Br. Account. Rev. 2019, 51, 100833. [Google Scholar] [CrossRef]

- Damerji, H.; Salimi, A. Mediating effect of use perceptions on technology readiness and adoption of artificial intelligence in accounting. Account. Educ. 2021, 30, 107–130. [Google Scholar] [CrossRef]

- Liu, J.; Zhu, Y.; Serapio, M.G.; Cavusgil, S.T. The new generation of millennial entrepreneurs: A review and call for research. Int. Bus. Rev. 2019, 28, 101581. [Google Scholar] [CrossRef]

- Knudsen, D.R. Elusive boundaries, power relations, and knowledge production: A systematic review of the literature on digitalization in accounting. Int. J. Account. Inf. Syst. 2020, 36, 100441. [Google Scholar] [CrossRef]

- Chaplin, S. Accounting Education and the Prerequisite Skills of Accounting Graduates: Are Accounting Firms’ Moving the Boundaries? Aust. Account. Rev. 2016, 27, 61–70. [Google Scholar] [CrossRef]

- Yu, J.; Pan, F. Influence of External Pressures on the Digital Transformation of Institutions. 2020. Available online: https://www.diva-portal.org/smash/get/diva2:1451289/FULLTEXT01.pdf (accessed on 8 June 2022).

- Hinings, B.; Gegenhuber, T.; Greenwood, R. Digital innovation and transformation: An institutional perspective. Inf. Organ. 2018, 28, 52–61. [Google Scholar] [CrossRef]

- Fischer, M.; Imgrund, F.; Janiesch, C.; Winkelmann, A. Strategy archetypes for digital transformation: Defining meta objectives using business process management. Inf. Manag. 2020, 57, 103262. [Google Scholar] [CrossRef]

- Ionescu, B.; Ionescu, I.; Bendovschi, A.; Tudoran, L. Traditional accounting vs. cloud accounting. In Proceedings of the 8th International Conference Accounting and Management Informational Systems, Bucharest, Romania, 12–13 June 2013; pp. 106–125. [Google Scholar]

- Phillips, B.A. How Cloud Computing Will Change Accounting Forever. 2012. Available online: https://docplayer.net/2537016-How-the-cloud-will-change-accounting-forever.html (accessed on 16 June 2022).

- FSB (Financial Stability Board). Artificial Intelligence and Machine Learning in Financial Services: Market Developments and Financial Stability Implications. 2017. Available online: http://www.fsb.org/wp-content/uploads/P011117.pdf (accessed on 2 July 2022).

- Ahn, S.; Jung, H.R. A study on the role of public officials in local governmental accounting. Korean Gov. Account. Rev. 2018, 16, 67–91. [Google Scholar]

- Bauguess, S. The role of big data, machine learning, and AI in assessing risks: A regulatory perspective. In Champagne Keynote Speech; Securities and Exchange Commission: New York, NY, USA, 2017. Available online: https://www.sec.gov/news/speech/bauguess-big-data-ai (accessed on 21 June 2022).

- Cho, J.S.; Ahn, S.; Jung, W. The impact of artificial intelligence on the audit market. Korean Account. J. 2018, 27, 289–330. [Google Scholar] [CrossRef]

- Raval, S. What Is a Decentralized Application? Harnessing Bitcoin’s Blockchain Technology; O’Reilly Media Inc.: Sebastopol, CA, USA, 2016. [Google Scholar]

- Iansiti, M.; Lakhani, K.R. The truth about blockchain. Harv. Bus. Rev. 2017, 95, 118–127. Available online: https://hbr.org/2017/01/the-truth-about-blockchain (accessed on 17 June 2022).

- PwC. What’s Next for Blockchain in 2016? Available online: https://assets.ctfassets.net/sdlntm3tthp6/resource-asset-r123/0d58a4b4c8e527754fac77888919eb28/259e7234-dd22-4a4d-af00-97a1f5fe183a.pdf (accessed on 20 June 2022).

- Ngubelanga, A.; Duffett, R. Modeling Mobile Commerce ‘Applications’ Antecedents of Customer Satisfaction among Millennials: An Extended TAM Perspective. Sustainability 2021, 13, 5973. [Google Scholar] [CrossRef]

- Davis, F.D. Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Q. 1989, 13, 319–340. [Google Scholar] [CrossRef]

- Ajzen, I.; Fishbein, M. A Bayesian analysis of attribution processes. Psychol. Bull. 1975, 82, 261–277. [Google Scholar] [CrossRef]

- Ajzen, I. The theory of planned behavior. Organ. Behav. Hum. Decis. Process. 1991, 50, 179–211. [Google Scholar] [CrossRef]

- King, W.R.; He, J. A meta-analysis of the technology acceptance model. Inf. Manag. 2006, 43, 740–755. [Google Scholar] [CrossRef]

- Souza, L.A.; Da Silva, M.J.P.B.M.; Ferreira, T.A.M.V. The Acceptance of Information Technology by the Accounting Area. Sist. Gest. 2017, 12, 516–524. Available online: https://www.revistasg.uff.br/sg/article/download/1239/780/ (accessed on 15 June 2022).

- Abduljalil, K.M.; Zainuddin, Y. Integrating technology acceptance model and motivational model towards intention to adopt accounting information system. Int. J. Manag. Account. Econ. 2015, 2, 346–359. [Google Scholar]

- Le, O.; Cao, Q.M. Examining the technology acceptance model using cloud-based accounting software of Vietnamese enterprises. Manag. Sci. Lett. 2020, 10, 2781–2788. [Google Scholar] [CrossRef]

- AlNasrallah, W.; Saleem, F. Determinants of the Digitalization of Accounting in an Emerging Market: The Roles of Organizational Support and Job Relevance. Sustainability 2022, 14, 6483. [Google Scholar] [CrossRef]

- Kaplan, D. Structural Equation Modeling. In International Encyclopedia of the Social and Behavioral Sciences; Neil, J., Smelser, P., Baltes, B., Eds.; Pergamon: Oxford, UK, 2001; pp. 15215–15222. [Google Scholar]

- Hair, J.F.; Hult, G.T.M.; Ringle, C.M.; Sarstedt, M.A. Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM), 2nd ed.; Sage: Thousand Oaks, CA, USA, 2017. [Google Scholar]

- Garson, D. Partial Least Squares (PLS-SEM). Available online: https://www.smartpls.com/resources/ebook_on_pls-sem.pdf (accessed on 24 October 2022).

- Benitez, J.; Henseler, J.; Castillo, A.; Schuberth, F. How to perform and report an impactful analysis using partial least squares: Guidelines for confirmatory and explanatory IS research. Inf. Manag. 2020, 57, 103168. [Google Scholar] [CrossRef]

- Bromwicha, M.; Scapens, R.W. Management Accounting Research: 25 years on. Manag. Account. Res. 2016, 31, 1–9. [Google Scholar] [CrossRef]

- Howieson, B. Accounting practice in the new millennium: Is accounting education ready to meet the challenge? Br. Account. Rev. 2003, 35, 69–103. [Google Scholar] [CrossRef]

- Coman, D.M.; Ionescu, C.A.; Duicâ, A.; Coman, M.D.; Uzlau, M.C.; Stanescu, S.G.; State, V. Digitization of Accounting: The Premise of the Paradigm Shift of Role of the Professional Accountant. Appl. Sci. 2022, 12, 3359. [Google Scholar] [CrossRef]

- van Veldhoven, Z.; Vanthienen, J. Designing a Comprehensive Understanding of Digital Transformation and Its Impact. Available online: https://aisel.aisnet.org/cgi/viewcontent.cgi?article=1038&context=bled2019 (accessed on 9 June 2022).

- Lehne, M.; Sass, J.; Essenwanger, A.; Schepers, J.; Thun, S. Why digital medicine depends on interoperability. NPJ Digit. Med. 2019, 2, 1–5. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Variables | Items | Scales |

|---|---|---|

| Demographic variables | Gender | Male (1), Female (2) |

| Age | 18–30 years (1), 31–45 years (2), 46–65 years (3) | |

| Usefulness in project management | AI_PM | 1 to 5 (1—not helpful at all, 5—very useful) |

| BD_PM | ||

| BC_PM | ||

| CC_PM | ||

| Usefulness in decision making | AI_DM | |

| BD_DM | ||

| BC_DM | ||

| CC_DM | ||

| Usefulness in marketing | AI_Mk | |

| BD_Mk | ||

| BC_Mk | ||

| CC_Mk | ||

| Behavioral intention | ATU | 1 to 5 (1—not at all excited, 5—very excited) |

| IU | 1 to 5 (1—the smallest, 5—the biggest) | |

| Actual use | EU | 1 to 5 (1—minimal extent, 5—maximal extent) |

| Users’ satisfaction | S_PM | On a scale of 1 to 5 (1—very small, 5—very high) |

| S_DM | ||

| S_MK |

| Min | Max | Frequencies | Mean | Std. Deviation | Skewness | Kurtosis | |||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | |||||||

| Gender | 1 | 2 | 53.3% | 46.7% | - | - | - | 1.47 | 0.499 | 0.132 | −1.992 |

| Age | 1 | 3 | 26.1% | 42.4% | 31.5% | - | - | 2.05 | 0.758 | −0.091 | −1.251 |

| AI_PM | 2 | 5 | 0% | 5.7% | 21.3% | 44.0% | 29.0% | 3.96 | 0.855 | −0.479 | −0.428 |

| BD_PM | 1 | 5 | 0.5% | 5.7% | 35.6% | 37.0% | 21.3% | 3.73 | 0.875 | −0.121 | −0.564 |

| BC_PM | 2 | 5 | 0% | 6.1% | 23.6% | 46.7% | 23.6% | 3.88 | 0.839 | −0.393 | −0.400 |

| CC_PM | 1 | 5 | 0.7% | 4.5% | 19.0% | 44.7% | 31.1% | 4.01 | 0.863 | −0.699 | 0.260 |

| AI_DM | 2 | 5 | 5.9% | 14.5% | 22.4% | 32.0% | 25.2% | 4.03 | 0.945 | −0.595 | −0.668 |

| BD_DM | 1 | 5 | 0.7% | 9.1% | 24.9% | 37.2% | 28.1% | 3.83 | 0.935 | −0.488 | −0.514 |

| BC_DM | 2 | 5 | 0.5% | 8.2% | 23.4% | 44.9% | 23.1% | 3.75 | 0.967 | −0.191 | −0.991 |

| CC_DM | 2 | 5 | 0.2% | 15.0% | 31.3% | 34.0% | 19.5% | 3.85 | 0.992 | −0.422 | −0.890 |

| AI_Mk | 1 | 5 | 0% | 7.5% | 20.6% | 33.3% | 38.6% | 3.56 | 1.182 | −0.489 | −0.673 |

| BD_Mk | 1 | 5 | 0.2% | 10.4% | 21.1% | 42.9% | 25.4% | 3.83 | 0.963 | −0.451 | −0.543 |

| BC_Mk | 1 | 5 | 0% | 10.7% | 30.4% | 32.4% | 26.5% | 3.82 | 0.896 | −0.480 | −0.274 |

| CC_Mk | 1 | 5 | 0% | 11.6% | 22.7% | 34.5% | 31.3% | 3.58 | 0.974 | −0.104 | −0.912 |

| ATU | 1 | 5 | 3.2% | 9.3% | 26.5% | 34.2% | 26.8% | 3.72 | 1.001 | −0.410 | −0.487 |

| IU | 1 | 5 | 1.6% | 10.2% | 27.9% | 35.4% | 24.9% | 3.72 | 1.056 | −0.552 | −0.287 |

| EU | 1 | 5 | 0.5% | 6.3% | 37.6% | 34.7% | 20.9% | 3.69 | 0.887 | −0.062 | −0.625 |

| S_PM | 2 | 5 | 0% | 12.2% | 22.7% | 34.0% | 31.1% | 3.84 | 1.002 | −0.409 | −0.925 |

| S_DM | 1 | 5 | 0.5% | 8.2% | 25.6% | 36.7% | 29.0% | 3.86 | 0.946 | −0.423 | −0.604 |

| S_MK | 1 | 5 | 0.5% | 7.9% | 23.4% | 46.5% | 21.8% | 3.81 | 0.881 | −0.485 | −0.194 |

| CA | CR | AVE | |

|---|---|---|---|

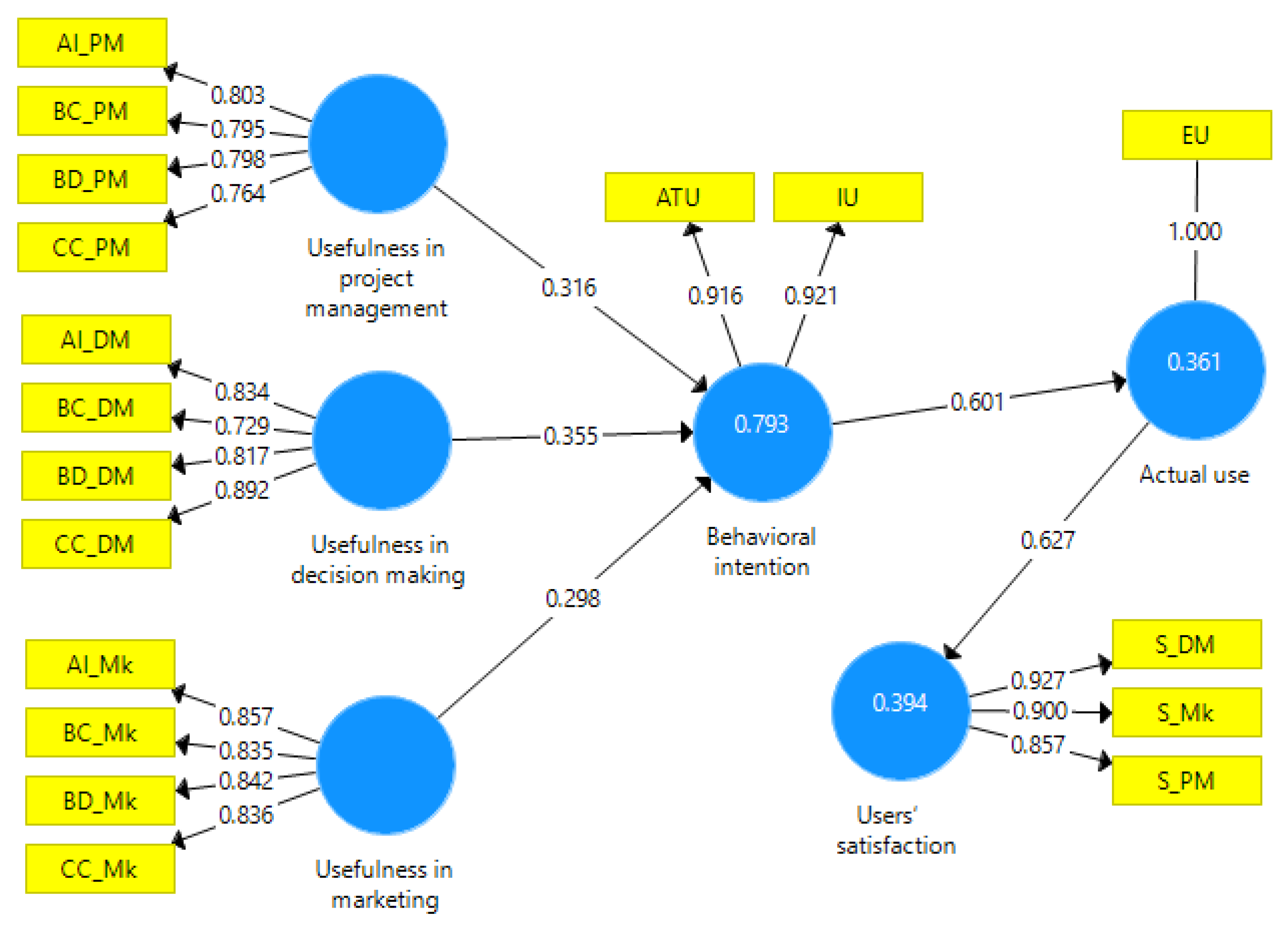

| Behavioral intention | 0.814 | 0.915 | 0.843 |

| Usefulness in decision making | 0.835 | 0.891 | 0.672 |

| Usefulness in marketing | 0.864 | 0.907 | 0.710 |

| Usefulness in project management | 0.801 | 0.869 | 0.624 |

| Users’ satisfaction | 0.878 | 0.924 | 0.802 |

| Outer Loadings for Usefulness in Decision Making | Outer Loadings for Usefulness in Marketing | Outer Loadings for Usefulness in Project Management | |

|---|---|---|---|

| AI_DM | 0.834 | ||

| BD_DM | 0.817 | ||

| BC_DM | 0.729 | ||

| CC_DM | 0.892 | ||

| AI_Mk | 0.857 | ||

| BD_Mk | 0.842 | ||

| BC_Mk | 0.835 | ||

| CC_Mk | 0.836 | ||

| AI_PM | 0.803 | ||

| BD_PM | 0.798 | ||

| BC_PM | 0.795 | ||

| CC_PM | 0.764 |

| Original Sample | T Statistics | p Values | |

|---|---|---|---|

| Usefulness in decision making −> Behavioral intention (H2) | 0.355 | 7.283 | 0.000 |

| Usefulness in marketing −> Behavioral intention (H2) | 0.298 | 7.003 | 0.000 |

| Usefulness in project management −> Behavioral intention (H2) | 0.316 | 9.426 | 0.000 |

| Behavioral intention −> actual use (H3) | 0.601 | 20.585 | 0.000 |

| Actual use −> users’ satisfaction | 0.627 | 23.781 | 0.000 |

| Outer Loadings | Users’ Satisfaction | Path Coefficients | Behavioral Intention |

|---|---|---|---|

| S_DM | 0.927 | Usefulness in decision making | 0.355 |

| S_Mk | 0.900 | Usefulness in marketing | 0.298 |

| S_PM | 0.857 | Usefulness in project management | 0.316 |

| RMSE | MAE | Q² Predict | |

|---|---|---|---|

| Actual use | 0.757 | 0.614 | 0.432 |

| Behavioral intention | 0.462 | 0.352 | 0.789 |

| Users’ satisfaction | 0.729 | 0.607 | 0.474 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Vărzaru, A.A.; Bocean, C.G.; Mangra, M.G.; Simion, D. Assessing Users’ Behavior on the Adoption of Digital Technologies in Management and Accounting Information Systems. Electronics 2022, 11, 3613. https://doi.org/10.3390/electronics11213613

Vărzaru AA, Bocean CG, Mangra MG, Simion D. Assessing Users’ Behavior on the Adoption of Digital Technologies in Management and Accounting Information Systems. Electronics. 2022; 11(21):3613. https://doi.org/10.3390/electronics11213613

Chicago/Turabian StyleVărzaru, Anca Antoaneta, Claudiu George Bocean, Mădălina Giorgiana Mangra, and Dalia Simion. 2022. "Assessing Users’ Behavior on the Adoption of Digital Technologies in Management and Accounting Information Systems" Electronics 11, no. 21: 3613. https://doi.org/10.3390/electronics11213613