Deep Learning Algorithm to Predict Cryptocurrency Fluctuation Prices: Increasing Investment Awareness

Abstract

:1. Introduction

- In this work, we studied and took on the challenge of predicting how the prices of various cryptocurrencies would fluctuate. Moreover, herein, we provide a precise explanation of the problem and discuss four distinct types of characteristics. This work has the potential to contribute to the advancement of research on cryptocurrencies and to supply investors with more tools for conducting investment assessments.

- To overcome the problem of price fluctuation prediction, we propose an innovative model known as LSTM.

- The LSTM model is used to capture the time dependency aspects of the prices of cryptocurrencies, and an embedding network is presented to capture the hidden representations from linked cryptocurrencies. Both networks are employed in conjunction with each another.

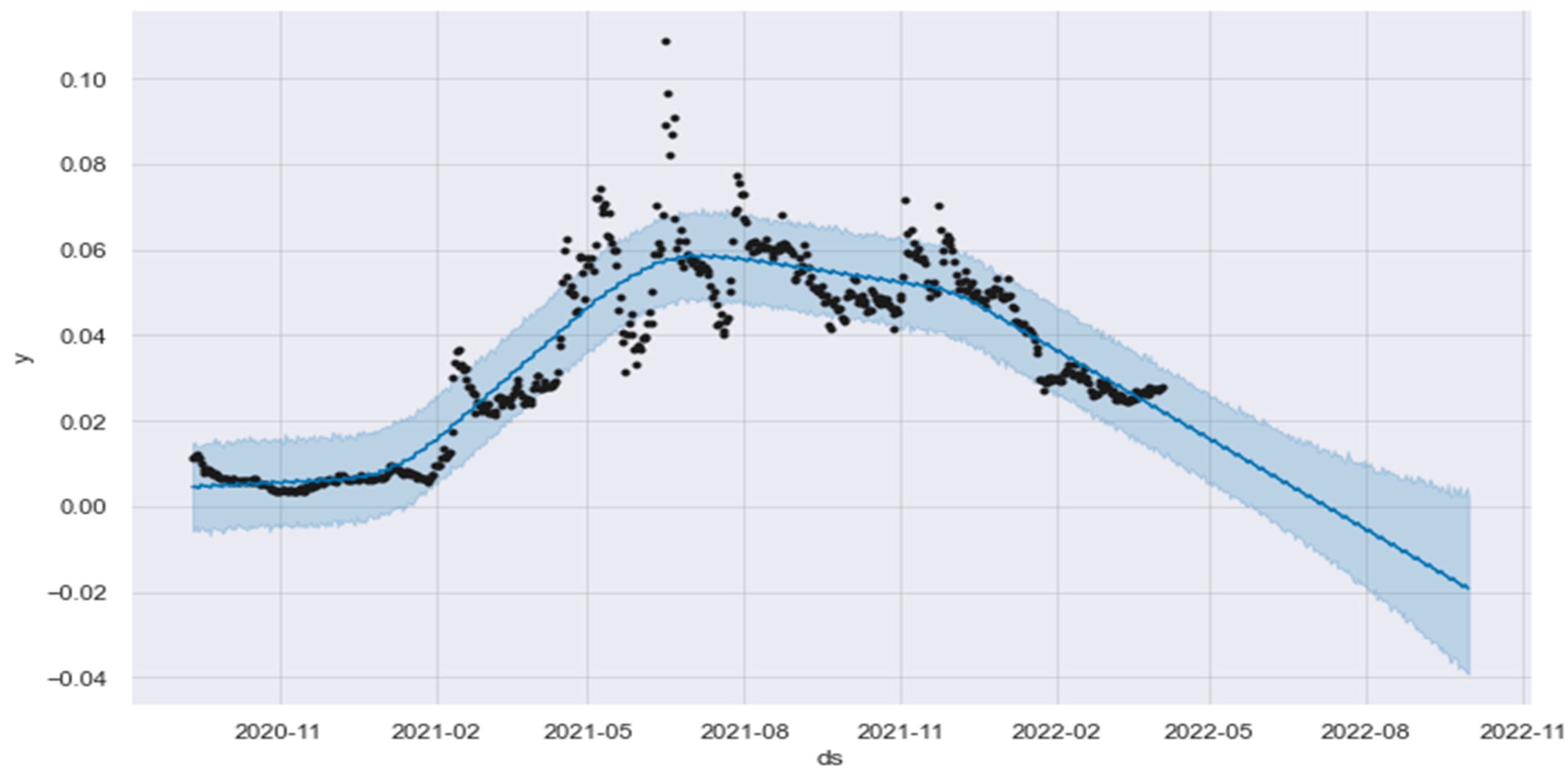

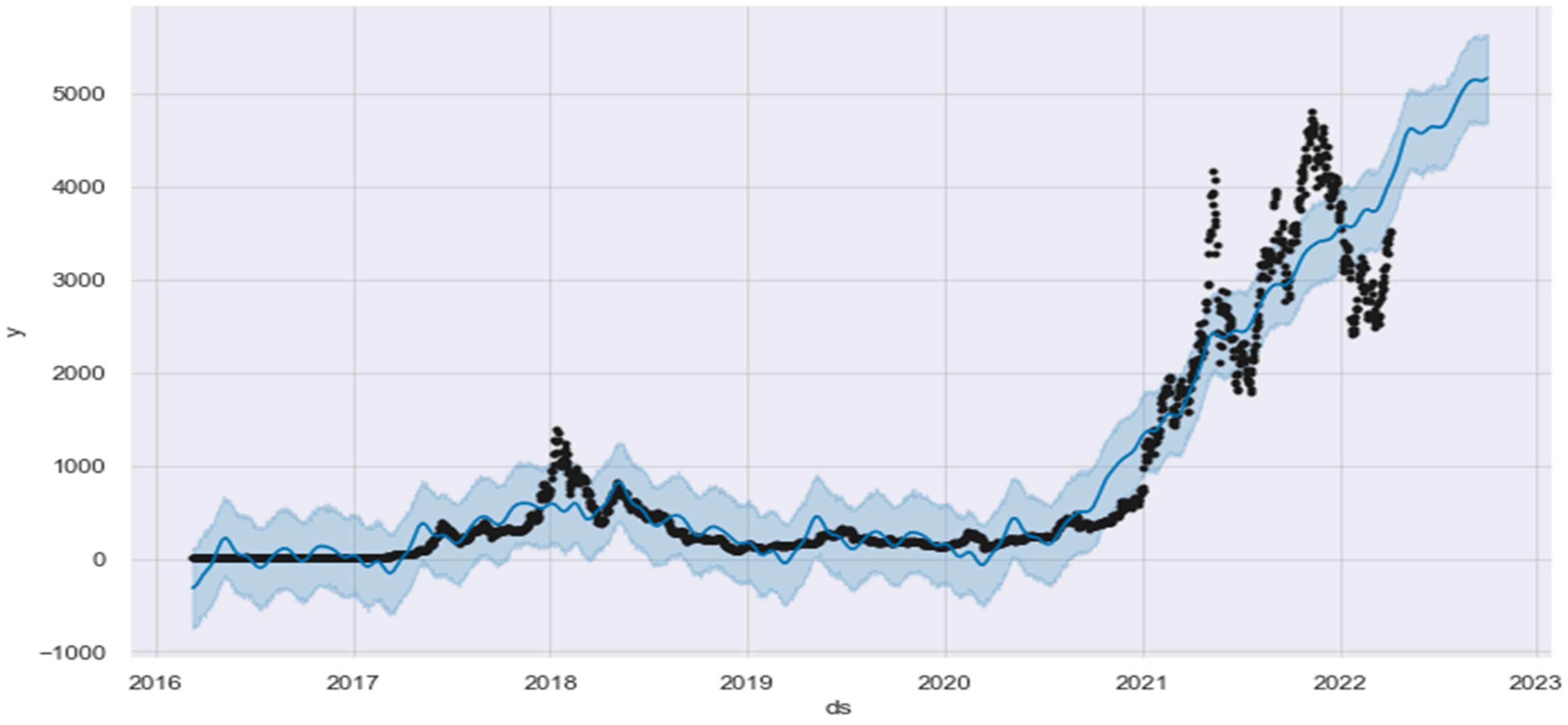

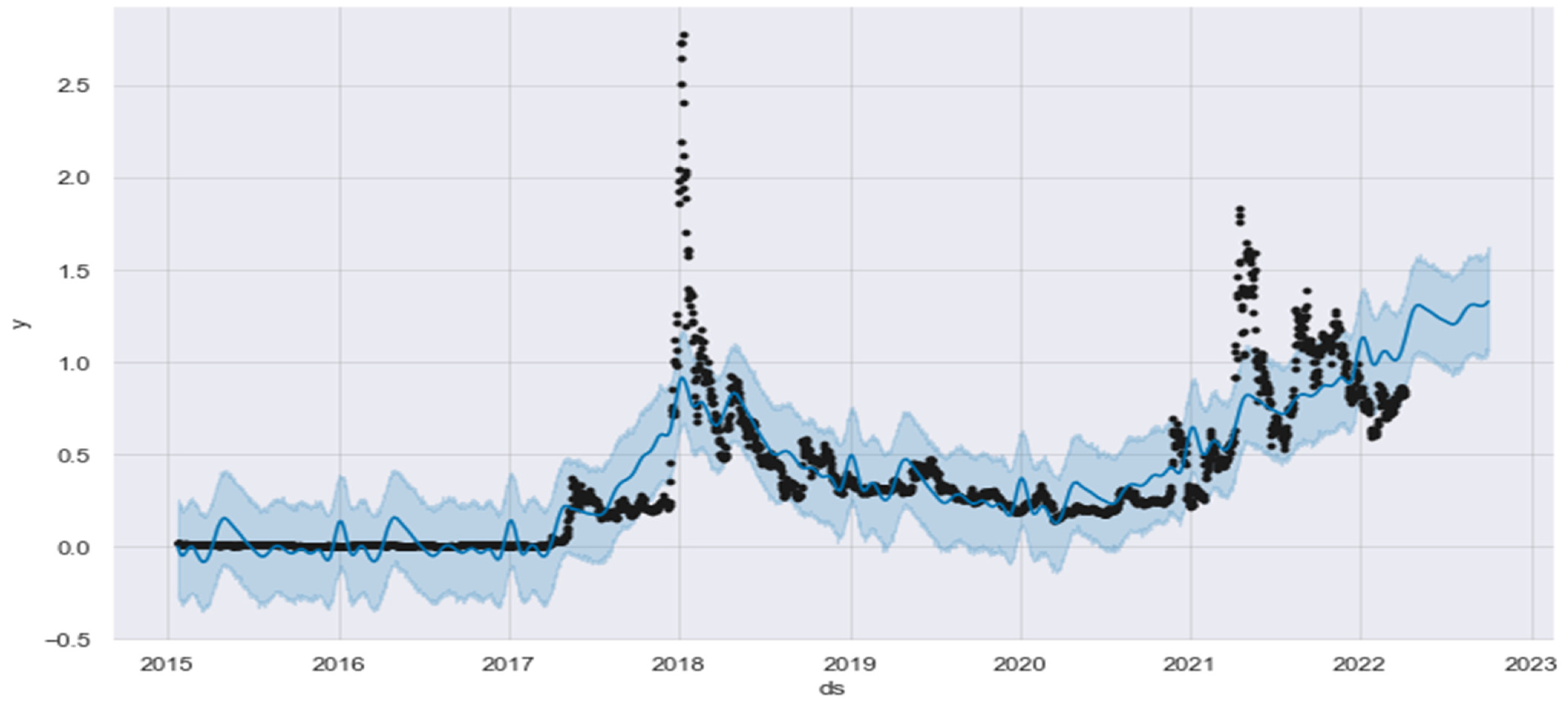

- The developed technique was used to show the future fluctuations of the prices of the different types of cryptocurrencies over a period of 180 days as a form of long-term forecasting.

- In the real-world cryptocurrency market, we experimentally demonstrated the usefulness of our LSTM model. In addition, LSTM showed state-of-the-art performance that was superior to those of all other existing models.

2. Materials and Methods

2.1. Data Sets

2.2. Normalization Method

2.3. LSTM Algorithm

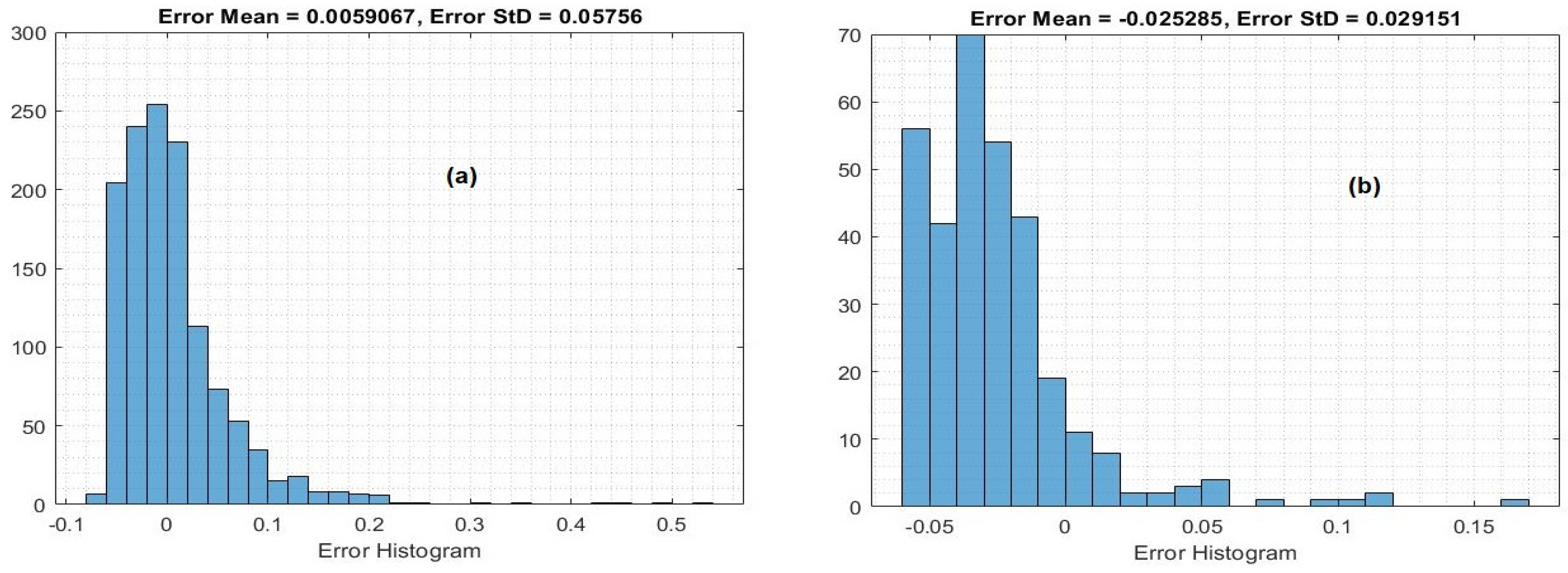

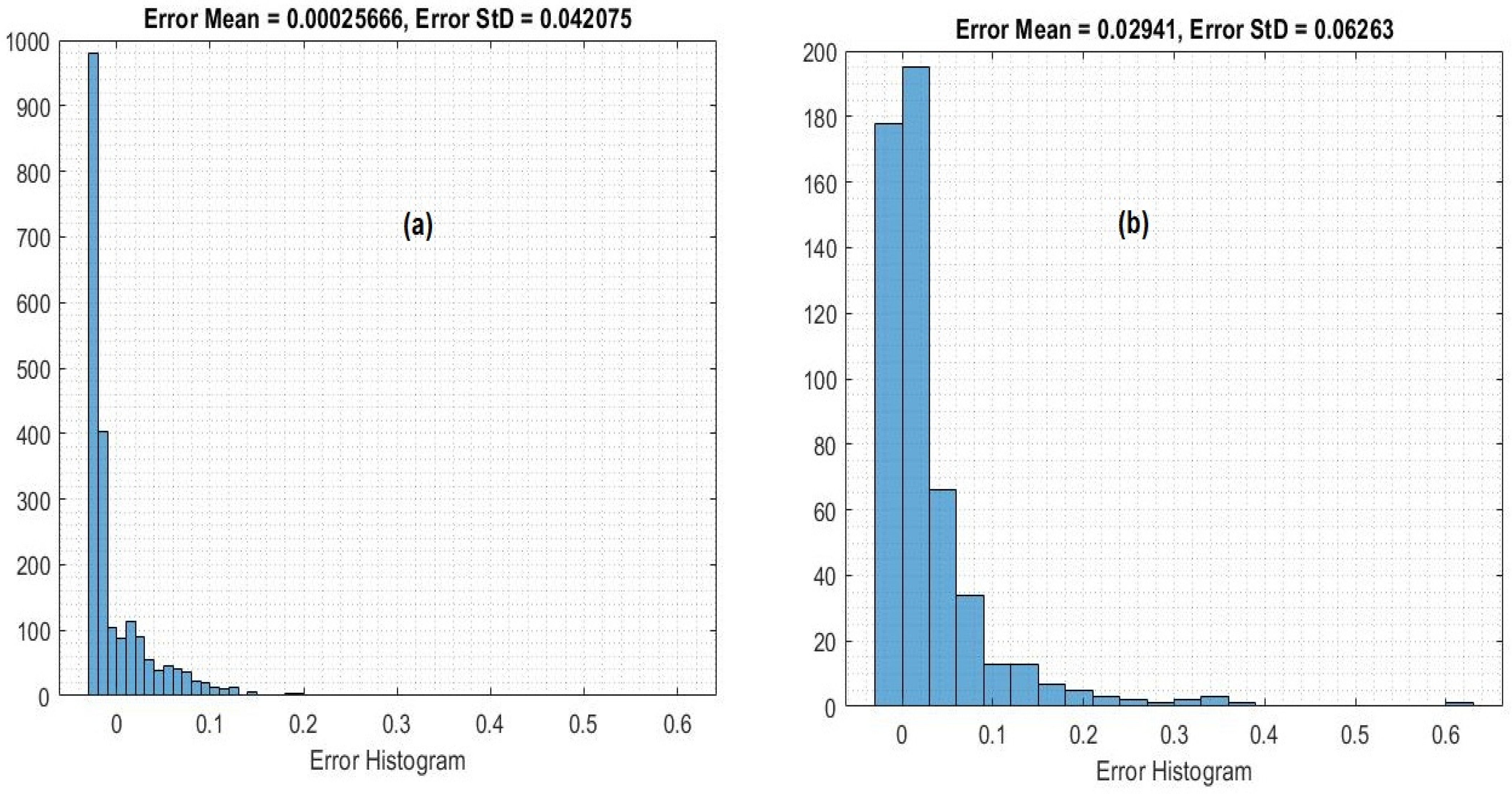

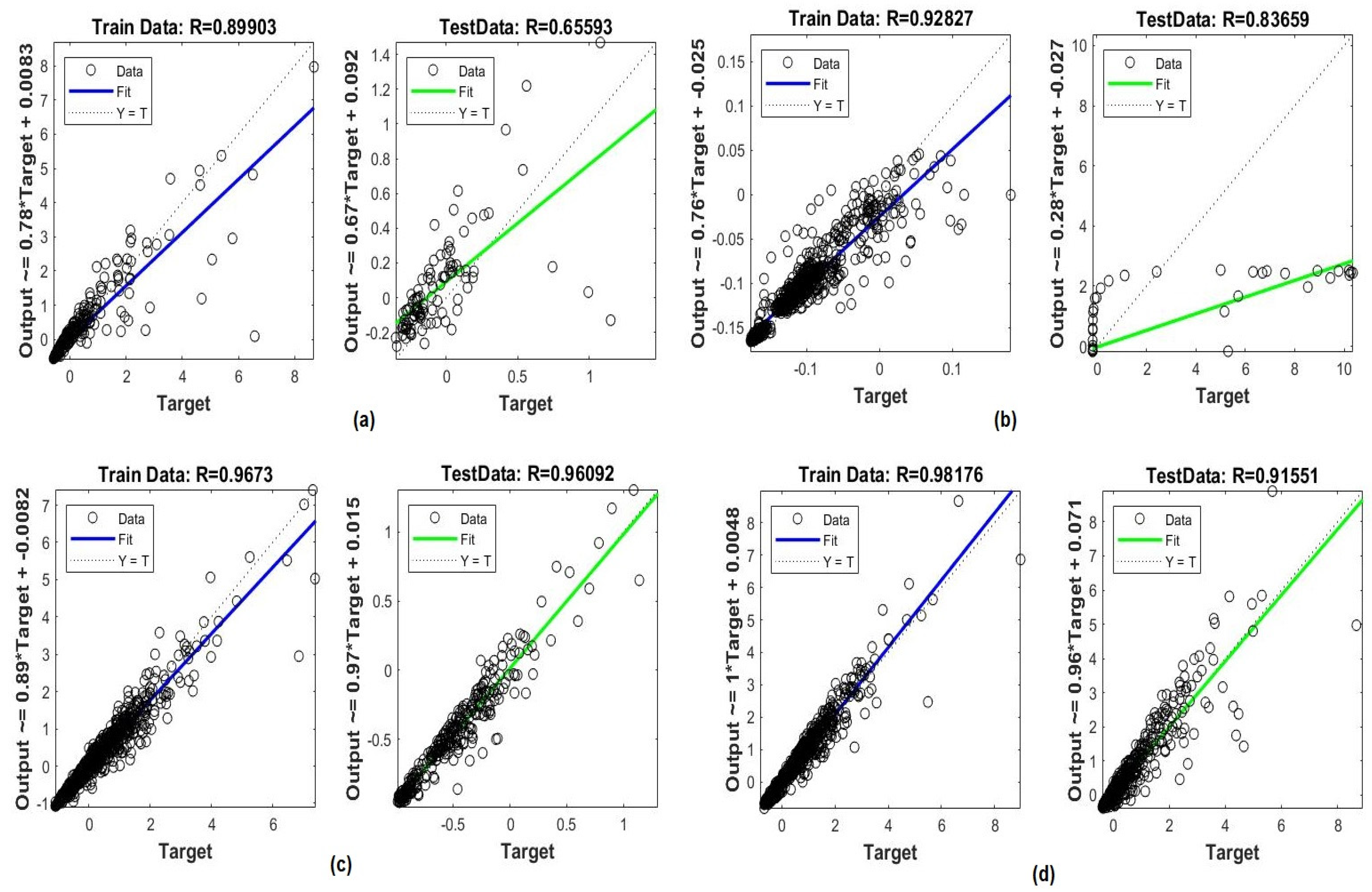

2.4. Performance Measurement

3. Experiments

3.1. Environment Developing System

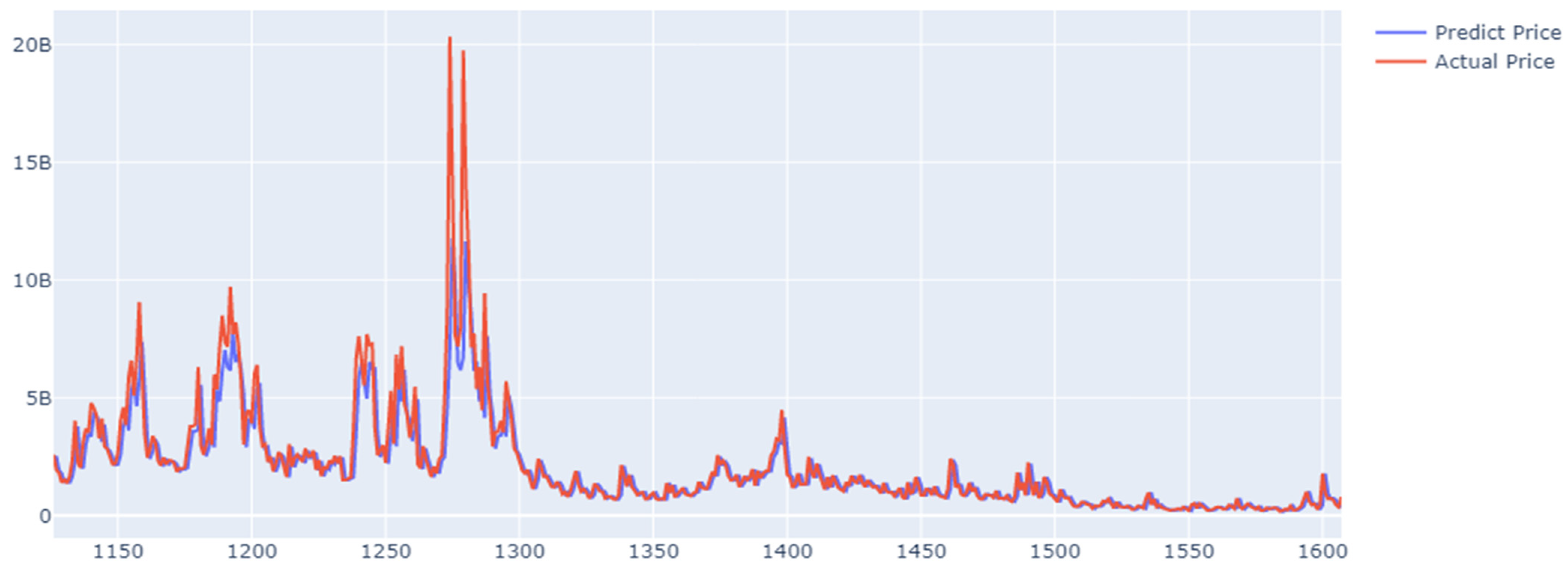

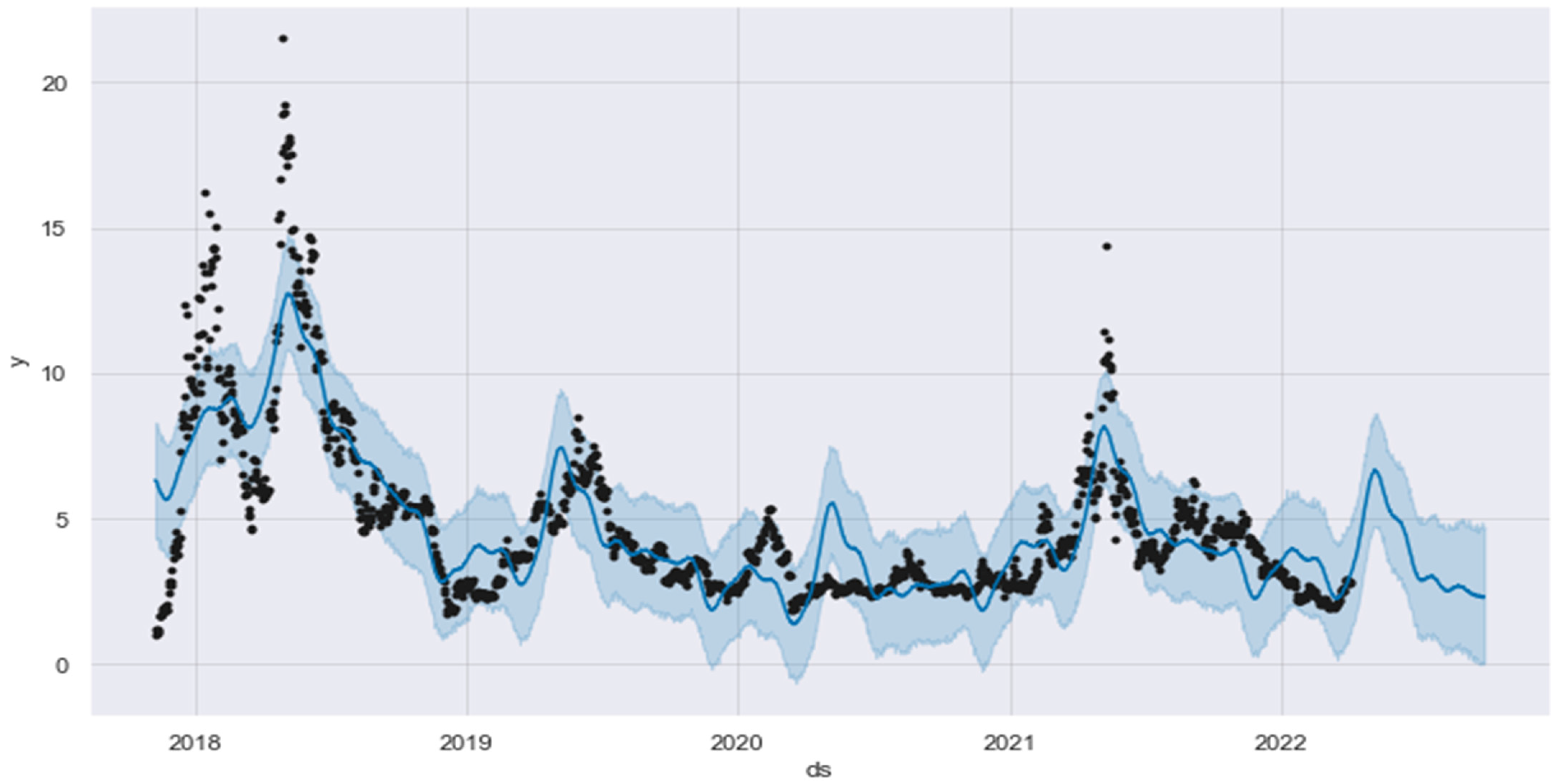

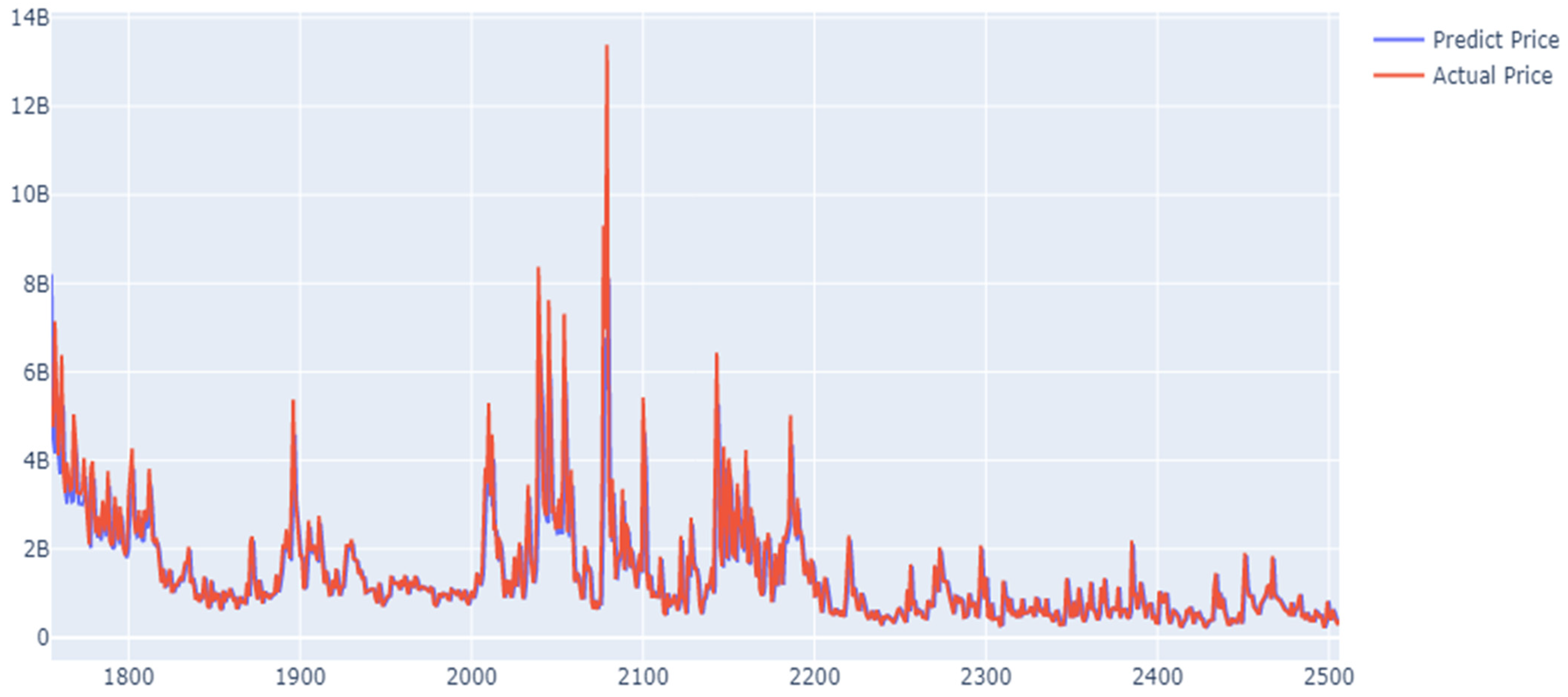

3.2. Results

3.2.1. Results of the LSTM Model for the AMP Cryptocurrency

3.2.2. Results for the Ethereum Digital Cryptocurrency

3.2.3. Results of the EOS Digital Cryptocurrency

3.2.4. Results of the XRP Digital Cryptocurrency

4. Discussion

5. Conclusions

- The first step in preprocessing each cryptocurrency data set was data imputation, which was performed to account for missing values. The step was followed by data reshaping, which was performed so that the LSTM algorithms could be applied to the data.

- The data set was normalized using the MinMax transformation approach and then reorganized so that it could be used in a multivariate model. The following stage involved separating the data into training and testing sets. For every coin, we used a 70% success rate in training and a 20% success rate in testing.

- The Pearson correlation approach was used to find any relationships between the various characteristics of the cryptocurrencies. In the course of this inquiry, a multivariate prediction model, as opposed to one that was based solely on a single variable, was constructed using Close, Open, High/Low, and Volume as variables.

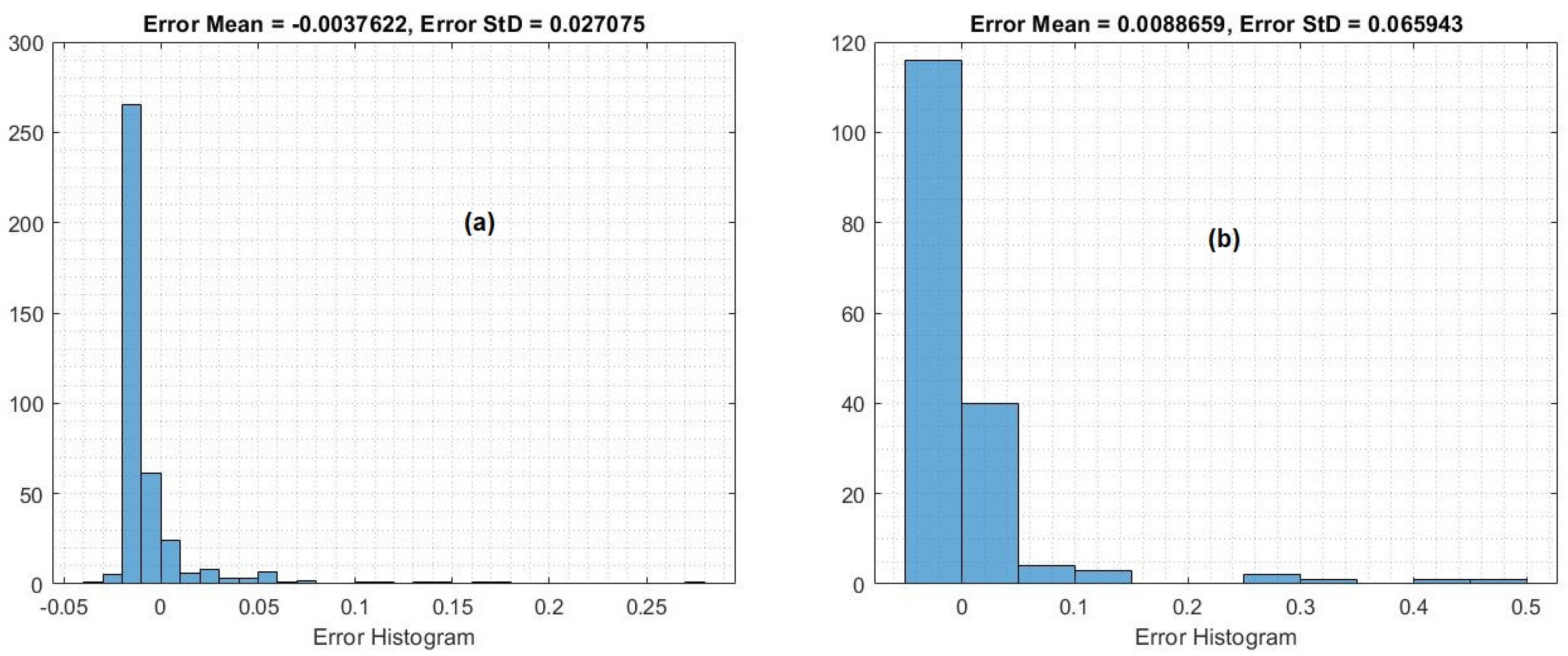

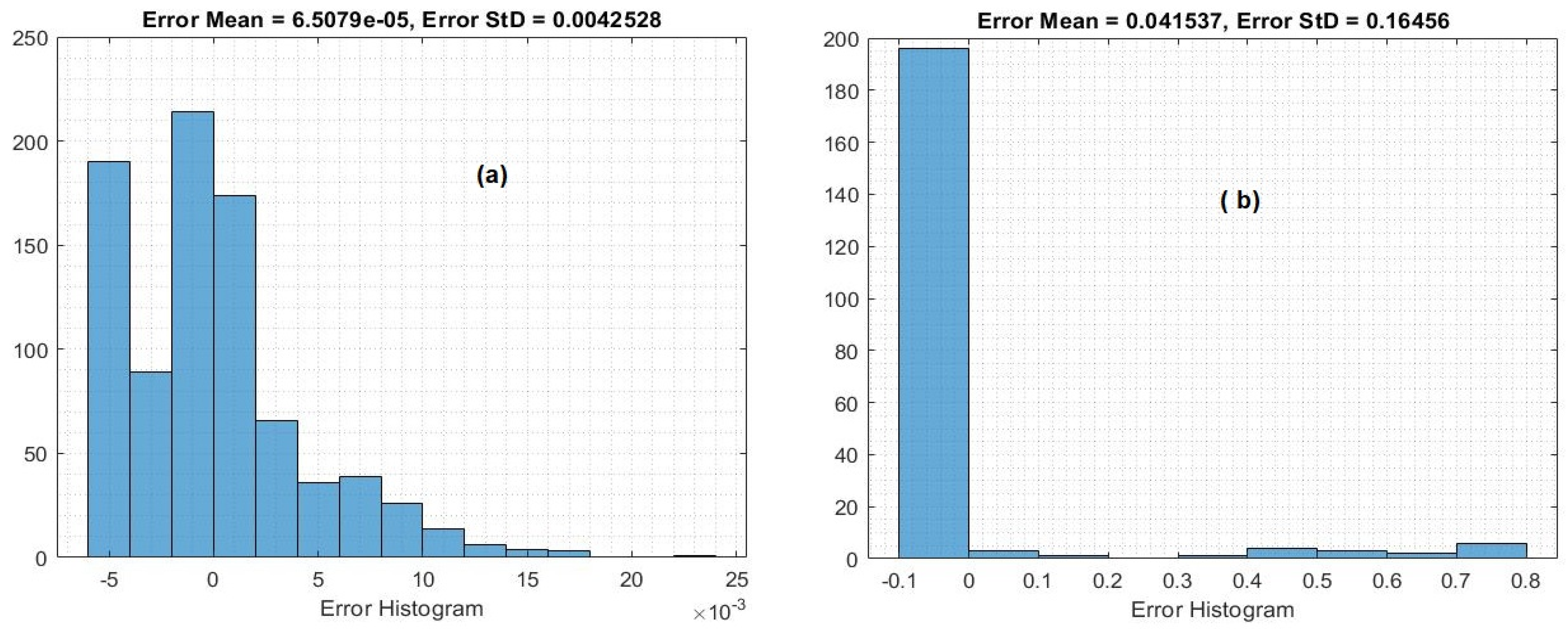

- In the forecasts of the future prices of cryptocurrencies for a period of 180 days, Ethereum and XRP showed increasing prices, whereas AMP showed a decreasing price.

- The results of the experiments demonstrated that the defined features were appropriate for the problem that we presented, and a state-of-the-art performance level, higher than all baseline values, could be attained by our suggested LSTM model. In addition, we analyzed the effects of various parameters on the issues we presented. This research has the potential to provide the groundwork for a genuine trading environment for investors to utilize in the near future.

- One contribution of this study is that it provides investors and policymakers with a solid understanding of the volatility of the most widely used cryptocurrencies. The LSTM model was utilized in this investigation, in which we examined the volatility of four cryptocurrencies, namelym AMP, Ethereum, EOS, and XRP. The data sets were collected at different time intervals.

- One limitation of this study was the use of four cryptocurrencies for the testing of the proposed prediction model.

- In the future, one of our goals is to create accurate prediction models that can be used to make forecasts for all cryptocurrencies, as well as to conduct an evaluation of the proposed model using data for all cryptocurrencies.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Nakamoto, S. Bitcoin: A Peer-To-Peer Electronic Cash System. Bitcoin. 2008. Available online: https://git.dhimmel.com/bitcoin-whitepaper/ (accessed on 5 May 2022).

- Corbet, S.; Lucey, B.; Urquhart, A.; Yarovaya, L. Cryptocurrencies as a financial asset: A systematic analysis. Int. Rev. Financ. Anal. 2019, 62, 182–199. [Google Scholar] [CrossRef] [Green Version]

- Zheng, Z.; Xie, S.; Dai, H.; Chen, X.; Wang, H. An overview of blockchain technology: Architecture, Consensus, and Future Trends. In Proceedings of the 2017 IEEE 6th International Congress on Big Data (BigData Congress), Honolulu, HI, USA, 25–30 June 2017. [Google Scholar]

- Zheng, Z.; Xie, S.; Dai, H.N.; Chen, X.; Wang, H. Blockchain challenges and opportunities: A survey. Int. J. Web Grid Serv. 2018, 14, 352–375. [Google Scholar] [CrossRef]

- Li, L.; Liu, J.; Chang, X.; Liu, T.; Liu, J. Toward conditionally anonymous Bitcoin transactions: A lightweight-script approach. Inf. Sci. 2020, 509, 290–303. [Google Scholar] [CrossRef]

- Böhme, R.; Christin, N.; Edelman, B.; Moore, T. Bitcoin: Economics, technology, and governance. J. Econ. Perspect. 2015, 29, 213–238. [Google Scholar] [CrossRef] [Green Version]

- Garcia, D.; Tessone, C.J.; Mavrodiev, P.; Perony, N. The digital traces of bubbles: Feedback cycles between socio-economic signals in the Bitcoin economy. J. R. Soc. Interface 2014, 11, 20140623. [Google Scholar] [CrossRef] [PubMed]

- Yu, J.H.; Kang, J.; Park, S. Information availability and return volatility in the bitcoin Market: Analyzing diferences of user opinion and interest. Inf. Processing Manag. 2019, 56, 721–732. [Google Scholar] [CrossRef]

- Gu, S.; Kelly, B.; Xiu, D. Empirical asset pricing via machine learning. Rev. Financ. Stud. 2020, 33, 2223–2273. [Google Scholar] [CrossRef] [Green Version]

- Feng, G.; Giglio, S.; Xiu, D. Taming the factor zoo: A test of new factors. J. Financ. 2020, 75, 1327–1370. [Google Scholar] [CrossRef]

- Jaquart, P.; Dann, D.; Martin, C. Machine learning for bitcoin pricing—A structured literature review WI 2020 Proceedings. In Wirtschaftsinformatik (Zentrale Tracks); GITO Verlag: Berlin, Germany, 2020; pp. 174–188. [Google Scholar]

- Coinmarketcap. Available online: https://coinmarketcap.com (accessed on 15 September 2020).

- Fama, E.F. Efficient capital markets: A review of theory and empirical work. J. Financ. 1970, 25, 383–417. [Google Scholar] [CrossRef]

- Lo, A.W. The Adaptive Markets Hypothesis Adaptive Markets; Princeton University Press: Princeton, NJ, USA, 2019; Volume 30, pp. 176–221. [Google Scholar]

- Fama, E.F.; MacBeth, J.D. Risk, return, and equilibrium: Empirical tests. J. Polit. Econ. 1973, 81, 607–636. [Google Scholar] [CrossRef]

- Fama, E.F.; French, K.R. Dissecting anomalies. J. Financ. 2007, 63, 1653–1678. [Google Scholar] [CrossRef]

- Fischer, T.; Krauss, C. Deep learning with long short-term memory networks for financial market predictions. Eur. J. Oper. Res. 2018, 270, 654–669. [Google Scholar] [CrossRef] [Green Version]

- Krollner, B.; Vanstone, B.; Finnie, G. Financial time series forecasting with machine learning techniques: A survey. In Proceedings of the 18th European Symposium on Artificial Neural Networks: Computational and Machine Learning, Bruges, Belgium, 28–30 April 2010; Springer: Berlin/Heidelberg, Germany, 2010; pp. 1–7. [Google Scholar]

- Siami-Namini, S.; Namin, A.S. Forecasting Economics and Financial Time Series: ARIMA vs. LSTM. arXiv 2018, arXiv:1803.06386. Available online: https://arxiv.org/abs/1803.06386v1 (accessed on 2 February 2020).

- Kaiser, L. Seasonality in cryptocurrencies. Financ. Res. Lett. 2019, 31, 232–238. [Google Scholar] [CrossRef]

- Aldhyani, T.H.H.; Alkahtani, H. A Bidirectional Long Short-Term Memory Model Algorithm for Predicting COVID-19 in Gulf Countries. Life 2021, 11, 1118. [Google Scholar] [CrossRef] [PubMed]

- Enke, D.; Thawornwong, S. The use of data mining and neural networks for forecasting stock market returns. Expert Syst. Appl. 2005, 29, 927–940. [Google Scholar] [CrossRef]

- Huang, W.; Nakamori, Y.; Wang, S.-Y. Forecasting stock market movement direction with support vector machine. Comput. Oper. Res. 2005, 32, 2513–2522. [Google Scholar] [CrossRef]

- Sheta, A.F.; Ahmed, S.E.M.; Faris, H. A comparison between regression, artificial neural networks and support vector machines for predicting stock market index. Soft Comput. 2015, 7, 8. [Google Scholar]

- McNally, S.; Roche, J.; Caton, S. Predicting the Price of Bitcoin Using Machine Learning. In Proceedings of the 26th Euromicro International Conference on Parallel, Distributed and Network-Based Processing (PDP), Cambridge, UK, 21–23 March 2018. [Google Scholar]

- Andrianto, Y. The Effect of Cryptocurrency on Investment Portfolio Effectiveness. J. Financ. Account. 2017, 5, 229–238. [Google Scholar] [CrossRef] [Green Version]

- Derbentsev, V.; Babenko, V.; Khrustalev, K.; Obruch, H.; Khrustalova, S. Comparative Performance of Machine Learning Ensemble Algorithms for Forecasting Cryptocurrency Prices. Int. J. Eng. Trans. A Basics 2021, 34, 140–148. [Google Scholar]

- Patel, M.M.; Tanwar, S.; Gupta, R.; Kumar, N. A Deep Learning-based Cryptocurrency Price Prediction Scheme for Financial Institutions. J. Inf. Secur. Appl. 2020, 55, 102583. [Google Scholar] [CrossRef]

- Miura, R.; Pichl, L.; Kaizoji, T. Artificial Neural Networks for Realized Volatility Prediction in Cryptocurrency Time Series. In Advances in Neural Networks—ISNN 2019; Lu, H., Tang, H., Wang, Z., Eds.; Lecture Notes in Computer Science; Springer: Cham, Switzerland, 2019; Volume 11554. [Google Scholar]

- Huang, J.-Z.; Huang, W.; Ni, J. Predicting bitcoin returns using high-dimensional technical indicators. J. Financ. Data Sci. 2019, 5, 140–155. [Google Scholar] [CrossRef]

- Chen, Z.; Li, C.; Sun, W. Bitcoin price prediction using machine learning: An approach to sample dimension engineering. J. Comput. Appl. Math. 2020, 365, 112395. [Google Scholar] [CrossRef]

- Kubat, M.; Matwin, S. Addressing the curse of imbalanced training sets: One-sided selection. In Proceedings of the 14th International Conference on Machine Learning, Nashville, TN, USA, 8–12 July 1997; Citeseer, Morgan Kaufmann: San Francisco, CA, USA, 1997; pp. 179–186. [Google Scholar]

- Peng, Y.; Albuquerque, P.H.M.; de Sá, J.M.C.; Padula, A.J.A.; Montenegro, M.R. The best of two worlds: Forecasting high frequency volatility for cryptocurrencies and traditional currencies with Support Vector Regression. Expert Syst. Appl. 2018, 97, 177–192. [Google Scholar] [CrossRef]

- Thakkar, A.; Chaudhari, K. A comprehensive survey on portfolio optimization, stock price and trend prediction using particle swarm optimization. Arch. Comput. Methods Eng. 2020, 28, 2133–2164. [Google Scholar] [CrossRef]

- Chaudhari, K.; Thakkar, A. iCREST: International cross-reference to exchange-based stock trend prediction using long short-term memory. In Applied Soft Computing and Communication Networks; Springer: Singapore, 2021; pp. 323–338. [Google Scholar]

- Altan, A.; Karasu, S.; Bekiros, S. Digital currency forecasting with chaotic meta-heuristic bio-inspired signal processing techniques. Chaos Solitons Fractals 2019, 126, 325–336. [Google Scholar] [CrossRef]

- Zhang, S.; Li, M.; Yan, C. The Empirical Analysis of Bitcoin Price Prediction Based on Deep Learning Integration Method. Comput. Intell. Neurosci. 2022, 2022, 1265837. [Google Scholar] [CrossRef] [PubMed]

- Alessandretti, L.; ElBahrawy, A.; Aiello, L.M.; Baronchelli, A. Anticipating cryptocurrency prices using machine learning. Complexity 2018, 2018, 8983590. [Google Scholar] [CrossRef]

- Jain, A.; Tripathi, S.; DharDwivedi, H.; Saxena, P. Forecasting Price of Cryptocurrencies Using Tweets Sentiment Analysis. In Proceedings of the 2018 Eleventh International Conference on Contemporary Computing (IC3), Noida, India, 2–4 August 2018; pp. 1–7. [Google Scholar]

- Kumar, D.; Rath, S. Predicting the Trends of Price for Ethereum Using Deep Learning Techniques. In Artificial Intelligence and Evolutionary Computations in Engineering Systems; Springer: Berlin/Heidelberg, Germany, 2020; pp. 103–114. [Google Scholar]

- Livieris, I.E.; Pintelas, E.; Stavroyiannis, S.; Pintelas, P. Ensemble Deep Learning Models for Forecasting Cryptocurrency Time-Series. Algorithms 2020, 13, 121. [Google Scholar] [CrossRef]

- Ji, S.; Kim, J.; Im, H. A comparative study of Bitcoin price prediction using deep learning. Mathematics 2019, 7, 898. [Google Scholar] [CrossRef] [Green Version]

- Huisu, J.; Lee, J.; Ko, H.; Lee, W. Predicting bitcoin prices by using rolling window lstm model. In Proceedings of the KDD Data Science in Fintech Workshop, London, UK, 19–23 August 2018. [Google Scholar]

- Alkahtani, H.; Aldhyani, T.H.H. Artificial Intelligence Algorithms for Malware Detection in Android-Operated Mobile Devices. Sensors 2022, 22, 2268. [Google Scholar] [CrossRef]

- Wu, C.H.; Lu, C.C.; Ma, Y.F.; Lu, R.S. A new forecasting framework for bitcoin price with LSTM. In Proceedings of the 2018 IEEE International Conference on Data Mining Workshops (ICDMW), Singapore, 17–20 November 2018; pp. 168–175. [Google Scholar]

- Dutta, A.; Kumar, S.; Basu, M. A Gated Recurrent Unit Approach to Bitcoin Price Prediction. J. Risk Financ. Manag. 2020, 13, 23. [Google Scholar] [CrossRef] [Green Version]

- Greaves, A.; Au, B. Using the Bitcoin Transaction Graph to Predict the Price of Bitcoin; Stanford University: Stanford, CA, USA, 2015. [Google Scholar]

- Kurbucz, M.T. Predicting the price of Bitcoin by the most frequent edges of its transaction network. Econ. Lett. 2019, 184, 108655. [Google Scholar] [CrossRef]

- Jang, H.; Lee, J. An empirical study on modeling and prediction of bitcoin prices with bayesian neural networks based on blockchain information. IEEE Access 2017, 6, 5427–5437. [Google Scholar] [CrossRef]

- Aldhyani, T.H.H.; Alkahtani, H. Attacks to Automatous Vehicles: A Deep Learning Algorithm for Cybersecurity. Sensors 2022, 22, 360. [Google Scholar] [CrossRef]

- Alkahtani, H.; Aldhyani, T.; Al-Yaari, M. Adaptive anomaly detection framework model objects in cyberspace. Appl. Bionics Biomech. 2020, 2020, 6660489. [Google Scholar] [CrossRef]

- Yamak, P.T.; Yujian, L.; Gadosey, P.K. A Comparison between ARIMA, LSTM, and GRU for Time Series Forecasting. In Proceedings of the 2nd International Conference on Algorithms, Computing and Artificial Intelligence, Sanya, China, 20–22 December 2019; pp. 49–55. [Google Scholar]

- Sebastião, H.; Godinho, P. Forecasting and trading cryptocurrencies with machine learning under changing market conditions. Financ. Innov. 2021, 7, 3. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Description | Feature Type | Feature |

|---|---|---|

| Time | Date | Lowest cryptocurrency price for the day |

| Low | Numerical | Highest cryptocurrency price for the day |

| High | Numerical | Opening cryptocurrency price for the day |

| Open | Numerical | Closing cryptocurrency price for the day |

| Close | Numerical | Cryptocurrency volume traded on the day |

| Volume | Numerical |

| Cryptocurrency | Start Time | End Time |

|---|---|---|

| AMP | 9 November 2020 | 3 April 2022 |

| Ethereum | 3 October 2016 | 4 April 2022 |

| EOS | 9 November 2017 | 4 April 2022 |

| XRP | 25 May 2015 | 4 April 2022 |

| MSE | RMSE | NRMES | |

|---|---|---|---|

| Training | 0.00360 | 0.0579 | 0.08877 |

| Testing | 0.0999 | 0.04289 | 0.00184 |

| Date | Yhat_Lower | Yhat_Upper |

|---|---|---|

| 15 September 2022 | 0.033358 | 0.004007 |

| 16 September 2022 | 0.035122 | 0.002405 |

| 17 September 2022 | 0.034185 | 0.004088 |

| 18 September 2022 | 0.035289 | 0.004145 |

| 19 September 2022 | 0.035550 | 0.002510 |

| 20 September 2022 | 0.036466 | 0.003886 |

| 21 September 2022 | 0.036169 | 0.003065 |

| 22 September 2022 | 0.037635 | 0.002911 |

| 23 September 2022 | 0.038176 | 0.002818 |

| 24 September 2022 | 0.038944 | 0.002759 |

| 25 September 2022 | 0.038174 | 0.003079 |

| 26 September 2022 | 0.039046 | 0.002894 |

| 27 September 2022 | 0.038900 | 0.001161 |

| 28 September 2022 | 0.038788 | 0.003102 |

| 29 September 2022 | 0.039680 | 0.002595 |

| 30 September 2022 | 0.039357 | 0.003808 |

| MSE | RMSE | NRMES | |

|---|---|---|---|

| Training | 0.1616 | 0.1693 | 0.02868 |

| Testing | 0.00422 | 0.004250 | 1.807 × 100−5 |

| Date | Yhat_Lower | Yhat_Upper |

|---|---|---|

| 15 September 2022 | 4677.903908 | 5609.095990 |

| 16 September 2022 | 4688.538587 | 5621.289890 |

| 17 September 2022 | 4702.770108 | 5591.677580 |

| 18 September 2022 | 4678.111597 | 5621.169491 |

| 19 September 2022 | 4693.603383 | 5617.486797 |

| 20 September 2022 | 4665.613444 | 5575.324879 |

| 21 September 2022 | 4710.074374 | 5597.400108 |

| 22 September 2022 | 4729.771186 | 5589.593962 |

| 23 September 2022 | 4694.120456 | 5632.626349 |

| 24 September 2022 | 4691.720817 | 5597.651285 |

| 25 September 2022 | 4688.440977 | 5605.991738 |

| 26 September 2022 | 4684.430926 | 5620.691021 |

| 27 September 2022 | 4720.283419 | 5616.356363 |

| 28 September 2022 | 4714.168725 | 5619.857287 |

| 29 September 2022 | 4708.096961 | 5624.059944 |

| 30 September 2022 | 4691.083387 | 5624.886372 |

| 15 September 2022 | 4711.686727 | 5620.812830 |

| MSE | RMSE | NRMES | |

|---|---|---|---|

| Training | 0.0525 | 0.0578 | 0.003345 |

| Testing | 0.0365 | 0.03855 | 0.00148 |

| Date | Yhat_Lower | Yhat_Upper |

|---|---|---|

| 15 September 2022 | 0.086412 | 4.678990 |

| 16 September 2022 | 0.085707 | 4.755874 |

| 17 September 2022 | 0.213080 | 4.694373 |

| 18 September 2022 | 0.066792 | 4.649735 |

| 19 September 2022 | 0.003034 | 4.635850 |

| 20 September 2022 | 0.126749 | 4.700749 |

| 21 September 2022 | 0.161347 | 4.492018 |

| 22 September 2022 | 0.046488 | 4.559961 |

| 23 September 2022 | 0.180359 | 4.621102 |

| 24 September 2022 | 0.119862 | 4.652601 |

| 25 September 2022 | 0.033037 | 4.476590 |

| 26 September 2022 | −0.143718 | 4.640157 |

| 27 September 2022 | 0.011772 | 4.778431 |

| 28 September 2022 | 0.234930 | 4.649232 |

| 29 September 2022 | 0.068225 | 4.841558 |

| 30 September 2022 | −0.156779 | 4.636795 |

| 1 October 2022 | −0.058128 | 4.701538 |

| MSE | RMSE | NRMES | |

|---|---|---|---|

| Training | 0.04042 | 0.042066 | 0.001769 |

| Testing | 0.06324 | 0.06913 | 0.0478 |

| Date | Yhat_Lower | Yhat_Upper |

|---|---|---|

| 15 September 2022 | 1.030358 | 1.582593 |

| 16 September 2022 | 1.041182 | 1.565411 |

| 17 September 2022 | 1.042217 | 1.576260 |

| 18 September 2022 | 1.033677 | 1.569240 |

| 19 September 2022 | 1.042646 | 1.585327 |

| 20 September 2022 | 1.033797 | 1.591424 |

| 21 September 2022 | 1.014597 | 1.575083 |

| 22 September 2022 | 1.044477 | 1.570961 |

| 23 September 2022 | 1.036621 | 1.583856 |

| 24 September 2022 | 1.040493 | 1.575192 |

| 25 September 2022 | 1.022004 | 1.620774 |

| 26 September 2022 | 1.026047 | 1.575642 |

| 27 September 2022 | 1.037790 | 1.577444 |

| 28 September 2022 | 1.049407 | 1.588724 |

| 29 September 2022 | 1.033513 | 1.605739 |

| 30 September 2022 | 1.053632 | 1.607500 |

| 1 October 2022 | 1.050816 | 1.602266 |

| Reference | Model | Currency | Results |

|---|---|---|---|

| [52] | Logistic regression and linear discriminant analysis | LTC | R2 score LR: 66% LDA: 65.3% |

| [53] | Random forests (RFs) and support vector machines (SVMs) | Ethereum and Litecoin | RMSE: SVM = 19.69 RF = 5.05 |

| Proposed system (LSTM) | AMP | MSE = 0.000745 RMSE = 0.042 | |

| Proposed system (LSTM) | Ethereum | MSE = 0.02868 RMSE = 0.042 | |

| Proposed system (LSTM) | EOS | MSE = 0.003345 RMSE = 0.0385 | |

| Proposed system (LSTM) | XRP | MSE = 0.001769 RMSE = 0.069 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ammer, M.A.; Aldhyani, T.H.H. Deep Learning Algorithm to Predict Cryptocurrency Fluctuation Prices: Increasing Investment Awareness. Electronics 2022, 11, 2349. https://doi.org/10.3390/electronics11152349

Ammer MA, Aldhyani THH. Deep Learning Algorithm to Predict Cryptocurrency Fluctuation Prices: Increasing Investment Awareness. Electronics. 2022; 11(15):2349. https://doi.org/10.3390/electronics11152349

Chicago/Turabian StyleAmmer, Mohammed Abdullah, and Theyazn H. H. Aldhyani. 2022. "Deep Learning Algorithm to Predict Cryptocurrency Fluctuation Prices: Increasing Investment Awareness" Electronics 11, no. 15: 2349. https://doi.org/10.3390/electronics11152349