1. Introduction

The high rate of global industrialization has caused serious carbon emission problems. Concentrations of greenhouse gases (GHGs) are currently very high, far greater than those at the beginning of the industrial age. A survey conducted in 2019 found that the atmospheric concentration of CO

2 had hit 409.8 ppm (parts per million), making it the highest in at least 800,000 years [

1]. CO

2 emissions not only threaten biodiversity but also pose a significant threat to sustainability [

2]. The negative impacts of climate change on the economy and society have prompted nations to look for the causes of environmental degradation and novel ways to lessen the effects of global warming and reduce carbon dioxide (CO

2) emissions [

3,

4,

5].

Reducing greenhouse gas emissions is crucial to the sustainable development of the world economy [

6]. The issue of carbon emission reduction has started to receive high levels of attention globally. In 2015, numerous countries joined the Paris Agreement [

7] in a collaborative effort to reduce emissions of GHGs. The European Union (EU) has similar objectives for combatting climate change and creating a cleaner environment. Many scholars have begun to explore the factors influencing carbon emissions, such as Mardani et al., who considered economic growth a major driver of carbon emissions [

8]. Zafar et al. also noted that Asia-Pacific industrialization increased carbon emissions [

9].

As the most populous developing nation in the world, China consumes a large amount of fossil fuels to power its rapid industrialization and urbanization [

10], the result of which is significant pollution and CO

2 emissions. As a major carbon-emitting country [

11], China has proposed the development goal of “carbon peaking and carbon neutrality”. Compliance with sustainable development goals is also a top priority for the business community [

12]. According to the eighth Sustainable Development Goal (SDG) outlined in the United Nations’ 2030 Agenda, governments must cut emissions, increase energy consumption, decarbonize energy systems, and ensure sustainable energy [

13]. SDG 9 aims to prevent environmental degradation, actively safeguard biodiversity, and maintain ecosystems that foster equitable human and economic development. Enterprises, as the main source of carbon emissions, are also the main participants in economic activities. This study focuses on sustainability at the firm level, i.e., achieving corporate sustainability. Elkington’s triple bottom line approach argues that the long-term prosperity of a company depends on a focus on three dimensions of sustainability: social, environmental and economic [

14]. Companies need to equally balance the needs of the company with these three dimensions when developing a sustainability strategy [

6]. The American financier Robert C. Higgins proposed a sustainable growth model in 1977 for the corporate SGR problem that better reflects the sustainability of a firm [

15]. In 2000, James C. Van Horne developed a steady-state equilibrium and dynamic nonequilibrium sustainable growth model based on this model to better reflect the business ability and competitiveness of a firm [

15].

However, in the study of carbon emission reduction in China, current scholars focus their research areas on the influencing factors of carbon emission reduction and the methods to reduce carbon emissions. For example, Li et al. argued that the digital economy is an important factor influencing carbon emission reduction, and they concluded that there is a U-shaped relationship between the level of digital economy development and carbon emission [

16]. Ming et al. constructed a spatial panel Durbin model and a mediating effects model to demonstrate that the digital economy directly and indirectly reduces carbon emissions [

17]. These studies all provide theoretical support for the implementation of a digital economy to mitigate carbon emissions in China. Due to the significant macro-regulatory role of the Chinese government, many scholars have also explored the effect of carbon trading-related policies on carbon emission reduction from the perspective of carbon trading. For example, Shi et al. found that carbon trading pilot projects, especially carbon allowances and prices, reduced regional carbon emissions and per capita CO

2 emissions [

15]. Huo et al. studied the low-carbon city pilot policy and found that this policy can reduce carbon emissions by changing industrial structure and promoting enterprises to develop low-carbon technologies [

18]. Li et al. used difference-in-differences (DID) and spatial Durbin models to demonstrate that the spatial spillover effect of carbon emissions trading significantly reduced carbon intensity [

19]. These studies also provide a theoretical basis for the government to test the effects of carbon trading policies and provide confidence for Chinese enterprises to reduce carbon emissions. However, the study of the influencing factors in carbon emission reduction ultimately aims to promote the effective carbon emission reduction and sustainable development of enterprises through green transformation. This is also the core issue of this study.

Although some scholars have studied carbon emissions and sustainable development, most have focused on macroeconomic and environmental sustainability. For instance, Erdoğan et al. suggested that well-planned emission reduction plans have few adverse effects on sustainable economic growth [

20]. Yang et al. found that the reduction in carbon emissions in the COVID-19 era improved environmental performance [

21]. Additionally, micro-level studies have focused on carbon emissions, financial performance, and short-term corporate performance. Palea’s study showed that a low-carbon orientation can reduce enterprises’ environmental regulatory risk and environmental management costs [

22]. Liu et al. employed the DID technique to evaluate enterprises’ micro-level financial performance and found that carbon emissions trading enhanced non-operating income [

23]. Desai disagreed with the conclusion that corporate carbon emission reduction promotes financial performance [

24]. This study shows that although there are opposing views on exploring the micro-level aspects of corporate carbon emission reduction enhancing corporate financial performance, most of the findings indicate that carbon emission reduction has a significant impact on financial performance, especially by reducing systemic risk. Although this study selects micro-level data, it is not limited to studying the impact of corporate carbon emission reduction on corporate financial performance and environmental performance. This study considers corporate sustainability in terms of corporate profitability and competitiveness, and explores the role of carbon emission reduction in corporate sustainability.

In addition, the government, media, and corporate executives play critical roles in decreasing carbon output and promoting sustainable business practices. Many scholars have studied the relationship between government subsidies and media coverage as independent variables with corporate carbon emissions or with corporate sustainability. For example, Yunus et al. argued that the environmental pressure exerted on firms by stakeholders such as regulators, the media, and creditors is conducive to the adoption of proactive carbon management strategies [

25]. Raghunandan used empirical data to suggest that institutional investors favor the selection of stocks for socially responsible companies. Additionally, it is more beneficial to promote the sustainable development of such enterprises [

26]. In examining the government’s drive to reduce corporate carbon emissions, some scholars argue that environmental regulation techniques, such as a hybrid of control and market incentive-based approaches, can be useful for encouraging greater carbon efficiency in businesses [

27]. However, some scholars contend that environmental regulation has a “green paradox” [

28] and may discourage firms from increasing their environmental investments, effectively discouraging economic activities that damage the environment [

29]. From an executive perspective, executives with more environmentally conscious world views have constructive effects on their companies’ carbon-efficient management and green financial success [

30]. This study chooses to further investigate the mechanism of the role of corporate carbon emission reduction in enhancing corporate sustainability from the stakeholder perspective so as to fill this gap. It also provides a theoretical basis for the government and media in promoting carbon emission reduction in enterprises.

This study also has many innovative points. Firstly, the subject of this study is relatively new. This study creatively selects two topical issues of current world concern—carbon emission reduction and sustainable development capacity—as research objectives, and takes Chinese enterprises with large carbon emissions as research samples. Secondly, this study is more innovative in its measurement of variables. In the context of the digital age, the media plays an increasingly important role in guiding the green transformation of companies. While most of the literature uses the total number of news reports in the news media as a measure of media attention, this study uses the J-F coefficient (Janis and Fadner, 1965) to measure the propensity of media coverage and as a more objective measure of media monitoring. The executive perspective, on the other hand, uses word frequency to select executives’ green perceptions as a moderating variable. This variable captures the internal motivation that drives executives to make green transition decisions. Lastly, this study is more innovative in terms of research methodology. As we know, the difficulty of studying corporate carbon emission reduction from a micro perspective lies in the acquisition of corporate carbon emission data. This study refers to the globally recognized Greenhouse Gas Accounting System (GHGAS) protocol and locates the sources of carbon emissions as direct GHG emissions owned or controlled by the company and indirect GHG emissions caused by commercial energy and thermal energy procurement. Carbon emissions directly disclosed by companies are obtained directly from their annual reports and social responsibility reports, while those not disclosed are calculated with reference to the Intergovernmental Panel on Climate Change (IPCC) Guidelines for National Greenhouse Gas Inventories. Various indicators are used to measure carbon emissions to ensure the robustness of the study results and to better reflect the micro-level findings.

This study provides a theoretical framework for furthering the paradigm of studies that focus on corporations’ carbon emissions. It also serves as a guide that enriches the literature on enterprise carbon emission reduction and sustainable development and assists businesses in achieving their sustainability objectives. Specifically, it identifies the critical mechanism of the role of enterprise carbon intensity reduction in influencing firms’ sustainable growth from the standpoint of three stakeholders. This study further enriches the research on environmental governance theory and sustainable development based on corporate carbon emissions and offers theoretical help for businesses to actively reduce carbon emissions and carry out ecological remediation.

3. Research Methodology and Design

3.1. Data and Sample

In 2015, many nations joined the Paris Agreement, and the world began to intensively investigate new energy conservation and carbon reduction strategies. In 2015, the new Environmental Protection Law passed by China was considered the most stringent in the world. It filled all the gaps in previous laws related to management and oversight, preservation of the environment, prevention of pollution, disclosure of data, and citizen involvement. Additionally, it clarifies the legal liability of businesses contaminating the environment as well as the significant expense of pollution control. While we consider that the carbon emission reduction actions of Chinese enterprises will increase significantly in the current domestic and international situation, owing to insufficient access to carbon emission reduction data for enterprises before 2015, we set the sample period as 2015–2020.

The Shanghai and Shenzhen A-share market is one of the largest domestic stock markets in China, with a very large market scale that reflects the overall situation of China’s domestic economy, the operation of industrial policies, etc. Moreover, the Shanghai Stock Exchange and Shenzhen Stock Exchange have been issuing social responsibility guidelines since 2006, requiring listed companies to disclose environmental information. The listed companies in Shanghai and Shenzhen A-shares were chosen as they are more representative and the data are more available.

We used the China Stock Market & Accounting Research (CSMAR) database to choose all A-share market companies listed from 2015 to 2020 on the Shanghai and Shenzhen stock exchanges. Special treatment, special treatment*, and special transfer status enterprises were omitted from the sample. The sample data for the finance industry, which is not a high-carbon industry, were also eliminated, as were samples with significant gaps in essential information. The variables were winsorized at the upper and lower 1% levels to reduce outliers (excluding dummy variables). Furthermore, we treated continuous variables logarithmically to eliminate heteroscedasticity interference. Following screening, a valid sample size of 11,822 was obtained. Stata 17.0 was used to clean and analyze the data and to generate statistical analysis findings.

The majority of Chinese businesses’ carbon emissions information is disclosed in their social responsibility, sustainability, and environmental reports. In this study, the carbon emissions data of Chinese listed companies were manually collected using crawler technology through the above-mentioned channels. Data on government environmental protection subsidies were obtained manually using web crawlers from annual company reports, social responsibility reports, company websites, and environmental department websites. Media monitoring-related data were obtained from the reported data in the CFND, a financial news database of Chinese listed companies. Data on the green perceptions of executives were obtained primarily from annual company reports. Finally, data on corporate financial indicators and other related variables were derived primarily from the CSMAR database.

3.2. Definition and Measurement of Variables

3.2.1. Explained Variables

Corporate sustainability is the independent variable in this study because it describes a company’s capacity to accomplish its strategic goals and protect its market position for long-term survival and perpetual growth, which allow a company to remain dominant, maintain profitability, and grow robustly in highly competitive fields. This study uses the Van Horne static model cited by Wu et al. [

63,

64] to measure a firm’s profitability and competitiveness sustainability. Namely,

3.2.2. Explanatory Variables

Carbon intensity, defined as greenhouse gas emissions per unit of revenue, is a credible statistic that can supplement climate risk metrics. To make the indication easier to read, it was multiplied by 100 based on the formula used by Chapple et al. [

65] to determine the carbon intensity.

According to Zhang et al. [

66], firms accounting for GHGs must utilize the globally recognized Greenhouse Gas Accounting System (GHGAS) protocol. The calculation technique released by the National Development and Reform Commission (NDRC) is the same as that described above. The GHG accounting method divides enterprise carbon emissions into three categories. Companies must report Scope 1 and Scope 2 carbon emissions under GHG accounting. Scope 3 includes all indirect emissions from non-company sources. This research focuses on Scope 1 and Scope 2, owing to data availability and reliability. Scope 1 comprises direct GHG emissions from sources owned by the company or under the company’s control, such as combustion emissions from boilers, furnaces, cars, etc., and process equipment emissions from chemical manufacturing. Scope 2 covers the indirect GHG emissions caused by commercial energy and heat purchases.

We found that businesses’ carbon emissions can be divided into two distinct categories. The first is carbon emissions that are stated directly in enterprises’ annual and social responsibility reports. In the second category, enterprises do not directly disclose their carbon emissions but calculate and reveal different types of fossil energy, electricity, and heat consumption. We separate Scope 1 and Scope 2 emissions and sum them according to the “Guidelines on Enterprise Greenhouse Gas Emissions Accounting Methods and Reporting” (hereinafter referred to as “Guidelines”) issued by the NDRC for different industries. The final summation of the two types of carbon emissions is used as the scope of the independent variables in this study.

The specific calculation technique for businesses that declared only fossil energy, electricity c, and heat consumption is as follows. According to the Intergovernmental Panel on Climate Change (IPCC) Guidelines for National Greenhouse Gas Inventories (2006), one fuel’s carbon emissions are determined as follows:

where

AD is the activity-level data for the consumption of this fossil fuel, which is the product of the consumption of this fuel and the average low-level heat content, and

EF is the emission factor of this fossil fuel. Fuel consumption was obtained from the data disclosed by the enterprises, and the default values of the average low-level heat content and the emission factor of the fossil fuel were obtained from the guide issued by the NDRC, which provides the commonly used official parameters.

The calculation method for electricity consumption is the same as that for fossil fuel energy consumption: AD is the power purchased by the enterprise and EF is the average emission factor of the power grid in the region where the enterprise is located. Climate change data were obtained from the National Center for Strategic Research and International Cooperation.

For thermal power consumption, the emissions factor determined by the national uniform regulations needs to be .

The total carbon emissions in this study were obtained from both direct and indirect sources.

3.2.3. Moderating Variables

Information on government environmental subsidies was gathered manually from annual firm reports, social responsibility reports, company websites, and environmental department websites. There is mention of study [

67], in which government environmental subsidies were measured by adjusting the relative levels of government environmental subsidies for adequate scaling.

The Financial News Database (CFND) coverage data from the Chinese Research Data Services (CNRDS) database were used to collect media monitoring data, which can be categorized into positive, neutral, and negative reports based on the emotion trends in media coverage. Considering that the tendency of all reports can more comprehensively reflect the indicator of media pressure and the degree of media monitoring, this study refers to Clarkson’s [

68] method and uses the Janis–Fadner (JF) coefficient, which integrates the sentiments of positive and negative media reports. To measure the tendency of media reports and treat the indicator positively for the sake of understanding, the larger the index, the more companies are under greater media pressure and scrutiny. Therefore, media coverage is defined as follows:

where

e represents negative media reports,

c represents positive media reports, and

t is the sum of

e and

c. In addition, the Janis–Fadner coefficient has a value range of [–1,1]. The closer it is to 1, the more negative the media coverage of the company, indicating that public pressure is higher and the company is under tighter supervision; the closer it is to −1, the more positive the media coverage of the company, indicating less public pressure and less supervision.

There are three main dimensions of executive green cognition: the perception of green competitive advantage, awareness of social responsibility, and perception of external pressure. Executive green cognition is defined as corporate executives’ knowledge of and psychological experiences regarding resources and environmental issues. Reyes-Menendez et al. demonstrated that longitudinal data could be obtained using text analysis [

69]. We chose textual analysis to obtain longitudinal data to effectively measure executives’ environmental perceptions. We also referred to Zhang et al.’s study [

70] to select a series of keywords based on the above three dimensions using Python and measured executives’ green perceptions by the rate of occurrence with which these terms appeared in listed corporations’ annual reports from 2015 to 2020.

3.2.4. Control Variables

Referring to the studies of Gallego-Álvarez et al. [

71] and Chen et al. [

72], we selected firm size (Size), gearing (Lev), return on assets (Roa), firm growth (Growth), cash flow ratio (Cashflow), net asset turnover (Ato), market value (Tobin-Q), equity nature (Soe), and firm age (Age) as control variables in this study. Additionally, we created a year effect (Year) and an industry effect (Industry) to make dummy variables equal to 1 if they fell within the appropriate year and industry, respectively, and 0 otherwise. Changes in the macroenvironment and government policies can cause firms’ efforts to reduce carbon emissions to vary from industry to industry and from year to year because industrial policies and macroeconomic environments change over time.

Table 1 presents all of the study variables and their explanations.

3.3. Model Design

3.3.1. Benchmark Model

To test Hypothesis 1, we constructed the following model with reference to Busch et al. [

73] to investigate the relationship between carbon intensity and corporate sustainability.

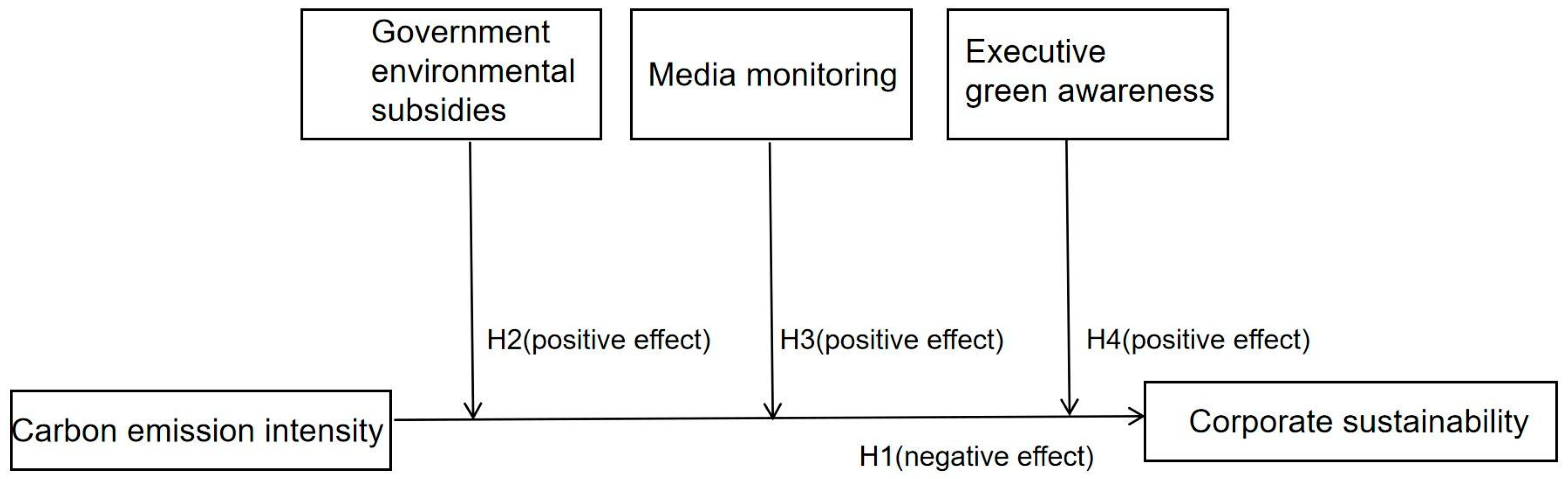

In the baseline regression model in Equation (5), the subscripts and denote individual companies and years, respectively. The explanatory variable is a firm’s ability to sustain itself (SGR). The carbon intensity of the enterprise is the explanatory variable (Ces). The control variables influence a firm’s ability to sustain itself. This study adds industry fixed effects to individual effects and year fixed effects t to lessen the effects of person heterogeneity and year features on firm sustainability, where is the random error term of the model. Robust standard error regressions were employed to address potential heteroscedasticity concerns. If is less than zero, this indicates that reducing enterprises’ carbon emission intensity has a positive impact on corporate sustainability, confirming Hypothesis 1.

3.3.2. Moderating Effect Model

We added the interaction terms of the moderating variables with corporate carbon emission intensity to the baseline regression model to investigate how they reduce carbon emission intensity and improve corporate sustainability [

74]. Hayes [

75] regenerated the transaction multiplier term after centering the variables to make the regression equation coefficients more explanatory and regressed the three sets of moderating variables with robust standard errors to account for heteroscedasticity. The model is shown below.

Model (2) modifies Model (1) by adding government environmental subsidies and their interplay with enterprise carbon emission intensity. Model (2) predicts that government environmental subsidies (Envsub) have a beneficial effect on lowering firms’ carbon emission intensities, leading to more sustainable growth if the coefficient of the interaction term has a statistically significant negative value.

Model (3) builds on Model (1) by including the moderating variable of media monitoring and its interaction term with firms’ CE intensity. Model (3) predicts that media monitoring (

Media) can further attenuate the positive effect of firms’ reduction in carbon emission intensity on improving enterprise sustainability if the interaction term’s coefficient is negative and can pass the significance test.

Model (4) incorporates the independent variable of carbon emission intensity of the firm as well as the moderating variable of executive green perception and their interaction term, all of which is based on Model (1). With a negative coefficient for the interaction term in Model (4), executive green perception (Ega) would be expected to have a beneficial influence on enhancing enterprise sustainability by decreasing the intensity of carbon emissions.

{kind=link}