Time and Frequency Spillovers between the Green Economy and Traditional Energy Markets

Abstract

:1. Introduction

2. Empirical Methodology

2.1. Time-Varying Parameter Vector Auto-Regression (TVP-VAR)

2.2. DY Spillover Index

2.3. BK Spillover Index

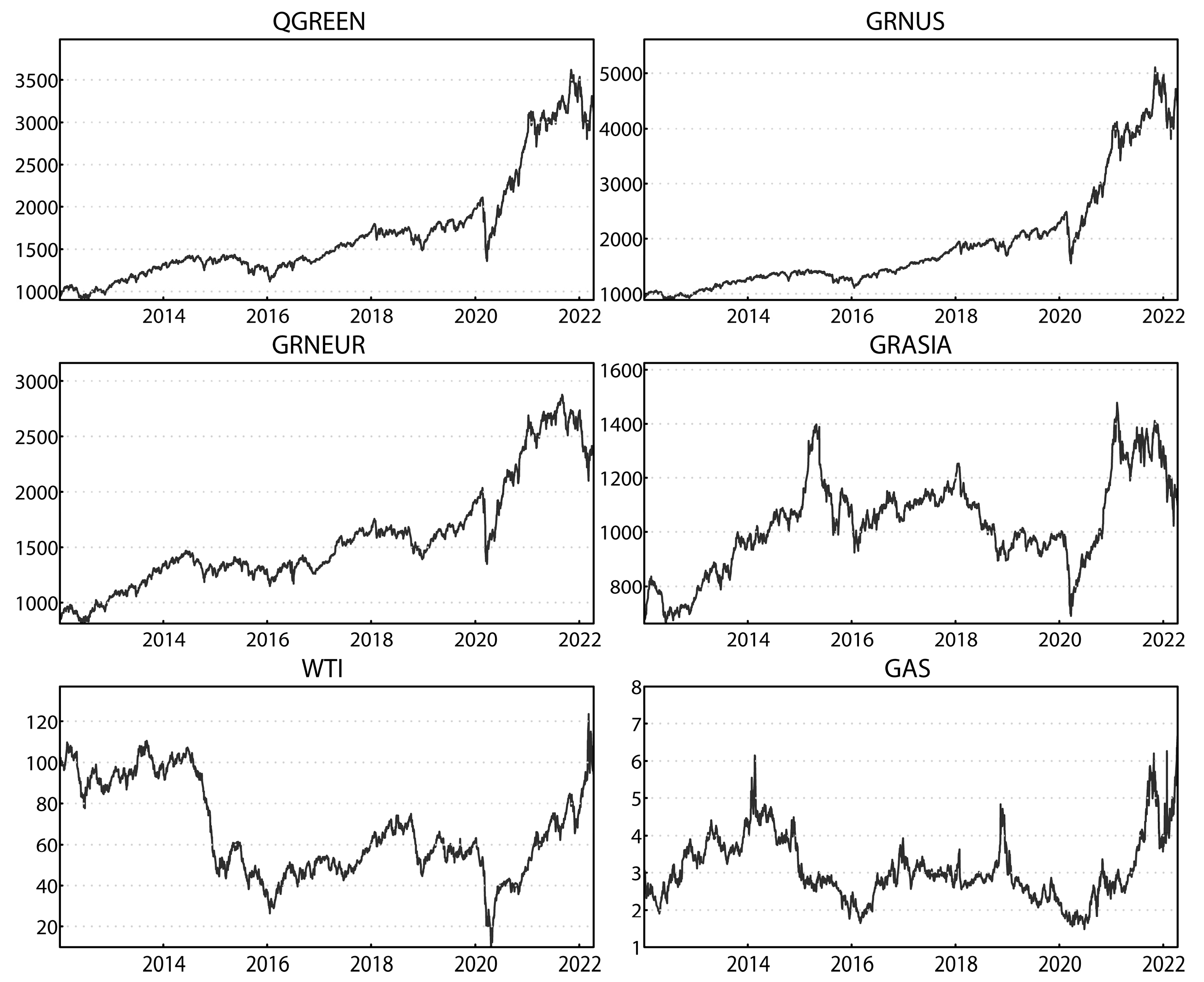

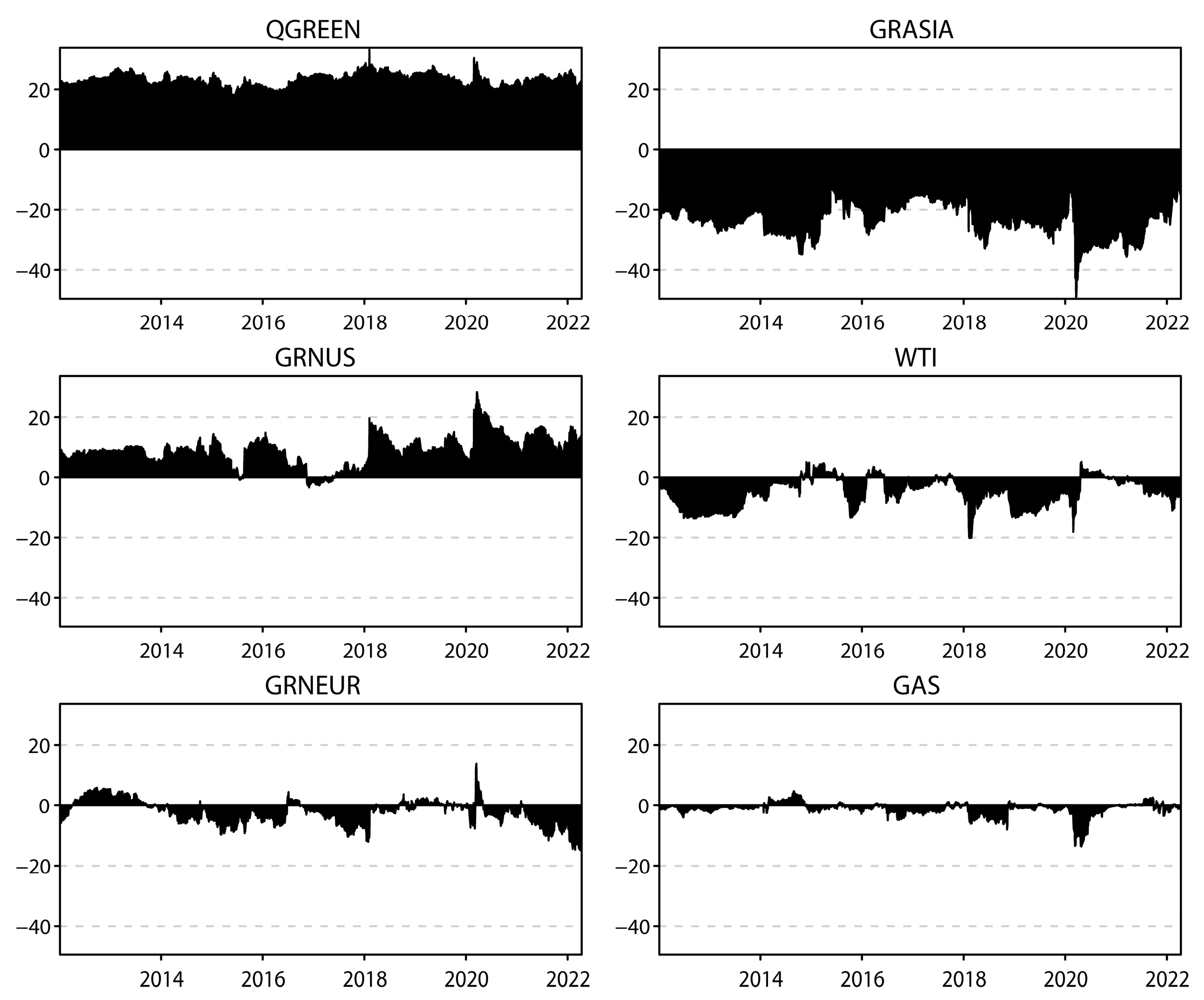

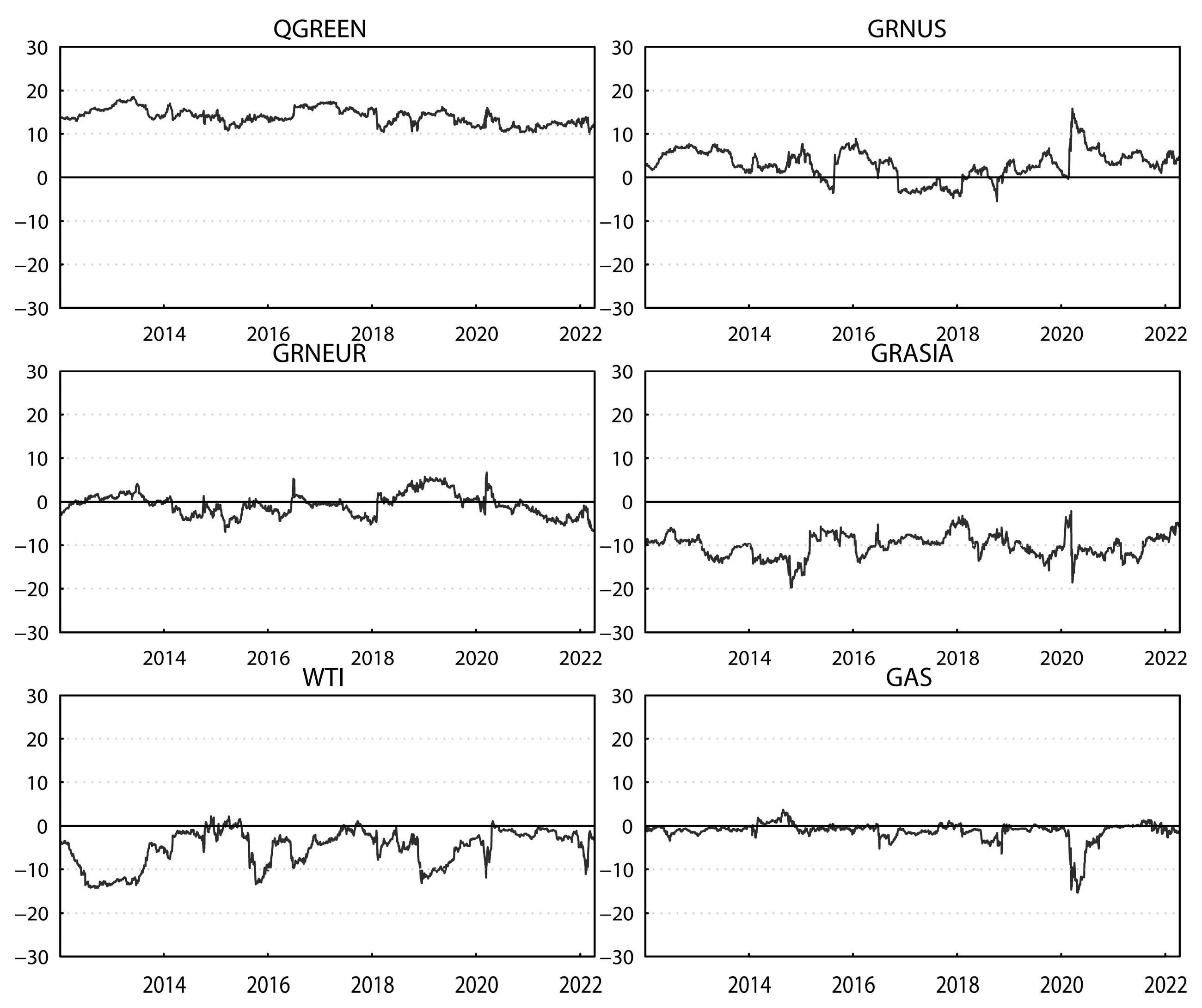

3. Data and Summary Statistics

3.1. Sample and Data

3.2. Descriptive Statistics

4. Empirical Analysis

4.1. DY Spillover Analysis

4.1.1. Static Analysis

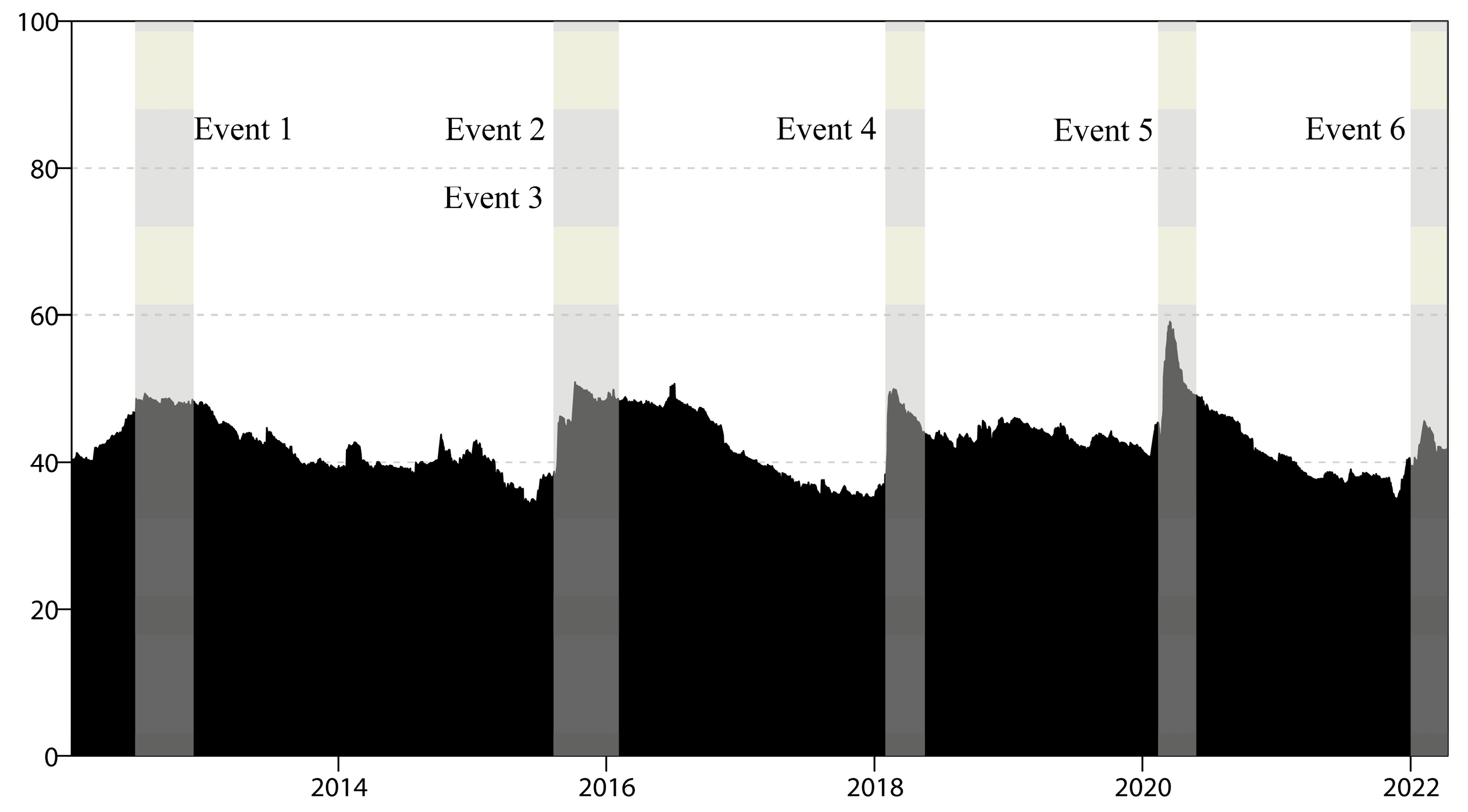

4.1.2. Dynamic Spillover Analysis

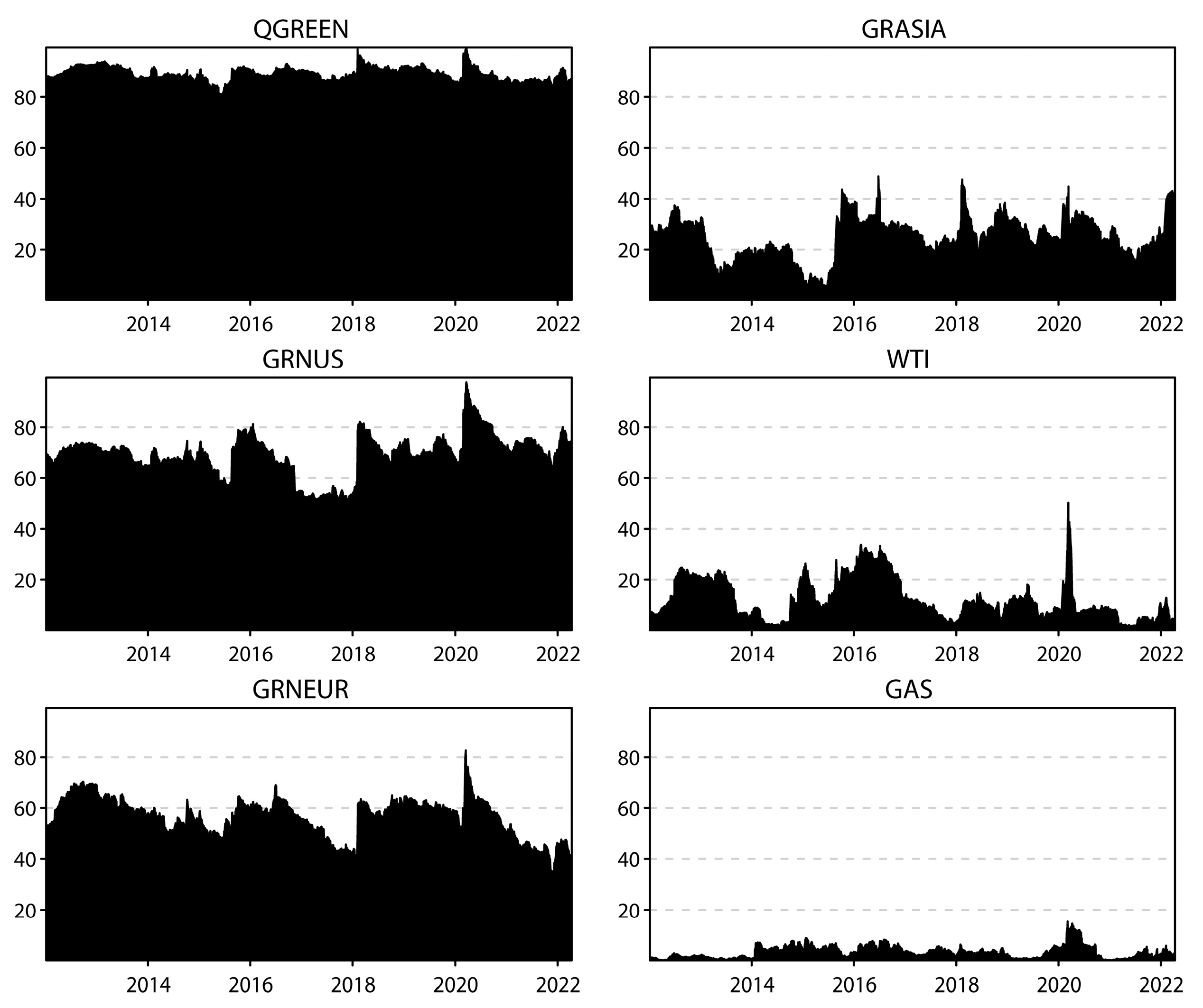

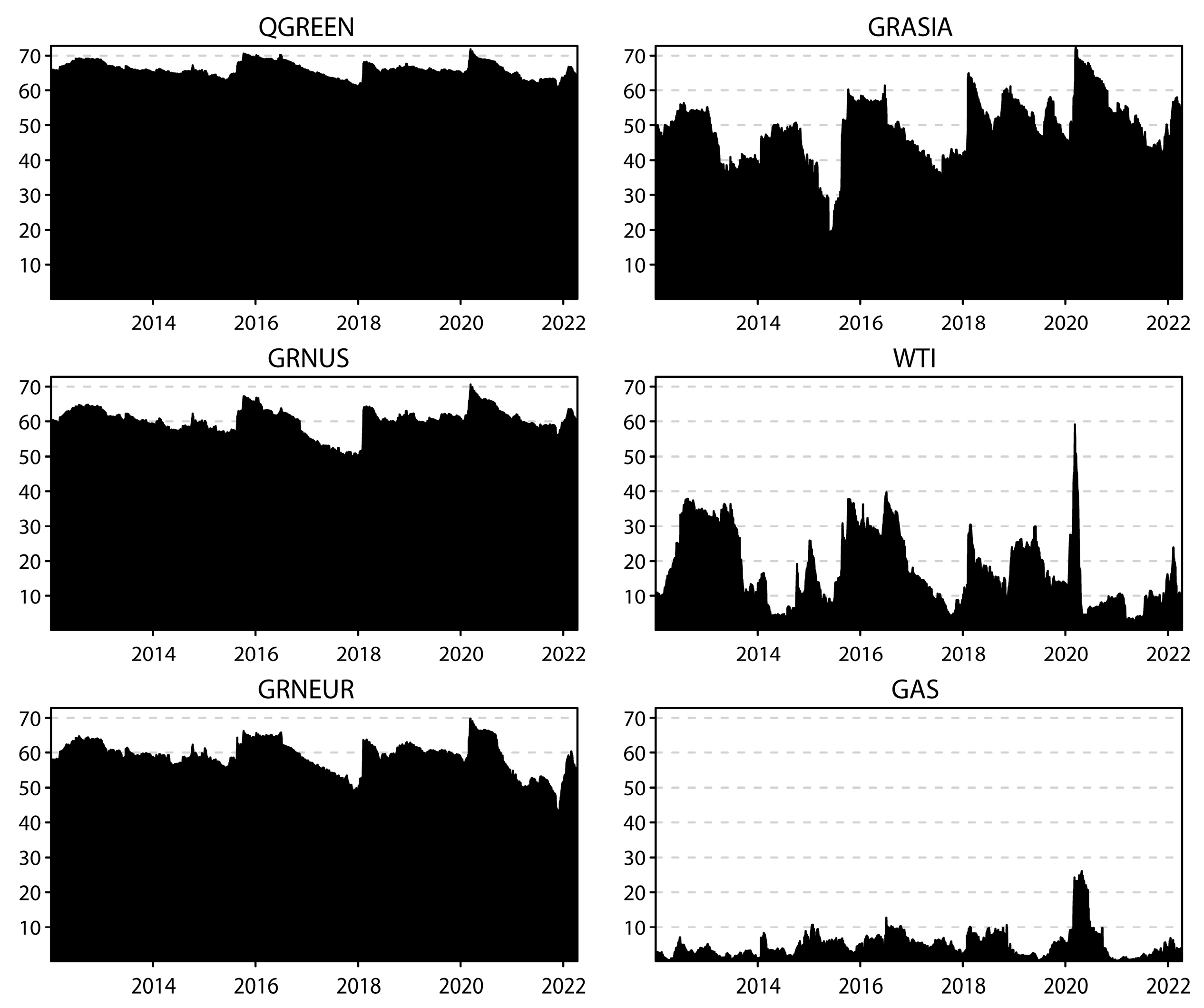

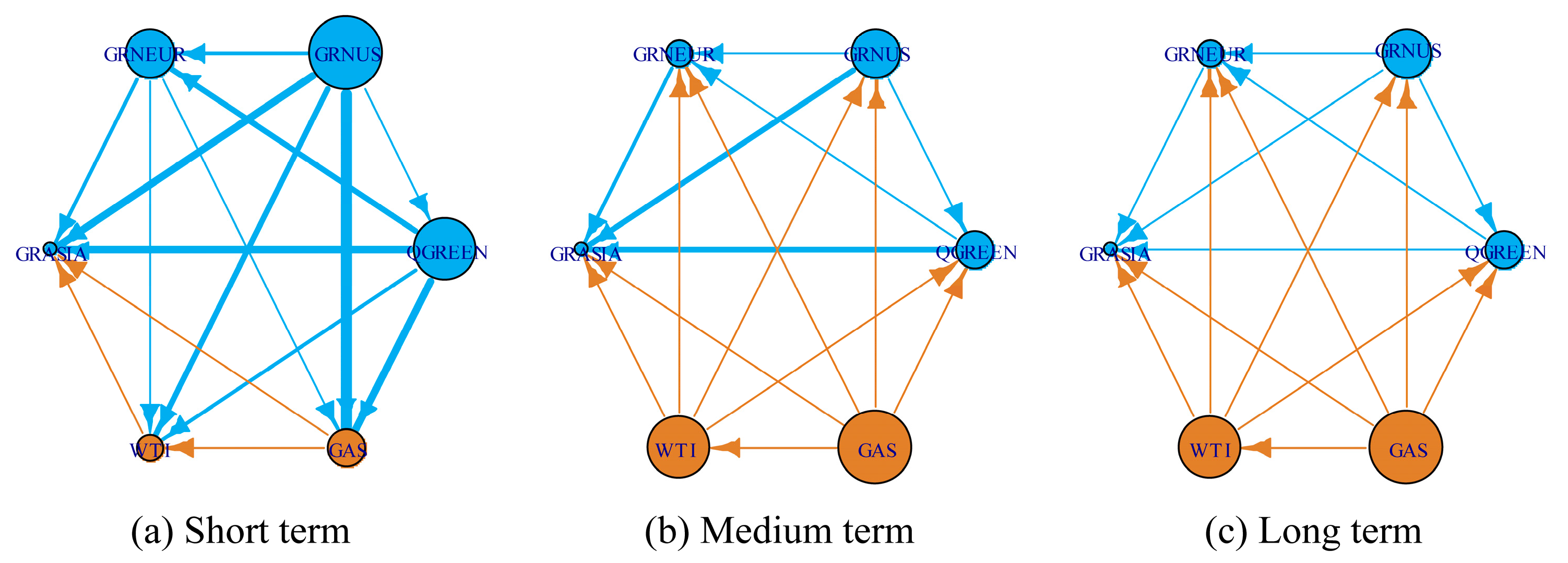

4.2. Frequency Domain Analysis

4.2.1. Static Results

4.2.2. Dynamic Results

4.3. COVID-19 Pandemic Impact Analysis

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Ali, E.B.; Anufriev, V.P.; Amfo, B. Green economy implementation in Ghana as a road map for a sustainable development drive: A review. Sci. Afr. 2021, 12, e00756. [Google Scholar] [CrossRef]

- Jin, X. Guang Yuan Low-carbon Development Path Based on SWOT Analysis. J. Sustain. Dev. 2012, 5, 78–83. [Google Scholar] [CrossRef] [Green Version]

- IEA. World Energy Outlook 2022. 2022. Available online: https://www.iea.org/reports/world-energy-outlook-2022/executive-summary (accessed on 16 March 2023).

- Ren, B.; Lucey, B. A clean, green haven?—Examining the relationship between clean energy, clean and dirty cryptocurrencies. Energy Econ. 2022, 109, 105951. [Google Scholar] [CrossRef]

- Urom, C.; Mzoughi, H.; Ndubuisi, G.; Guesmi, K. Directional predictability and time-frequency spillovers among clean energy sectors and oil price uncertainty. Q. Rev. Econ. Financ. 2022, 85, 32–341. [Google Scholar] [CrossRef]

- Sharma, G.D.; Sarker, T.; Rao, A.; Talan, G.; Jain, M. Revisiting conventional and green finance spillover in post-COVID world: Evidence from robust econometric models. Glob. Financ. J. 2022, 51, 100691. [Google Scholar] [CrossRef]

- Ding, Q.; Huang, J.; Zhang, H. Time-frequency spillovers among carbon, fossil energy and clean energy markets: The effects of attention to climate change. Int. Rev. Financ. Anal. 2022, 83, 102222. [Google Scholar] [CrossRef]

- Hosseini, S.E. An outlook on the global development of renewable and sustainable energy at the time of COVID-19. Energy Res. Soc. Sci. 2020, 68, 101633. [Google Scholar] [CrossRef]

- Hoang, A.T.; Nižetić, S.; Olcer, A.I.; Ong, H.C.; Chen, W.H.; Chong, C.T.; Thomas, S.; Bandh, S.A.; Nguyen, X.P. Impacts of COVID-19 pandemic on the global energy system and the shift progress to renewable energy: Opportunities, challenges, and policy implications. Energy Policy 2021, 154, 112322. [Google Scholar] [CrossRef]

- Eroğlu, H. Effects of COVID-19 outbreak on environment and renewable energy sector. Environ. Dev. Sustain. 2021, 23, 4782–4790. [Google Scholar] [CrossRef]

- Bhuiyan, M.A.; An, J.; Mikhaylov, A.; Moiseev, N.; Danish, M.S.S. Renewable Energy Deployment and COVID-19 Measures for Sustainable Development. Sustainability 2021, 13, 4418. [Google Scholar] [CrossRef]

- Diebold, F.X.; Yilmaz, K. Better to give than to receive: Predictive directional measurement of volatility spillovers. Int. J. Forecast. 2012, 28, 57–66. [Google Scholar] [CrossRef] [Green Version]

- Korobilis, D.; Yilmaz, K. Measuring Dynamic Connectedness with Large Bayesian VAR Models. SSRN Electron. J. 2018, 3099725. [Google Scholar] [CrossRef] [Green Version]

- Antonakakis, N.; Gabauer, D.; Gupta, R. International monetary policy spillovers: Evidence from a time-varying parameter vector autoregression. Int. Rev. Financ. Anal. 2019, 65, 101382. [Google Scholar] [CrossRef]

- Baruník, J.; Křehlík, T. Measuring the Frequency Dynamics of Financial Connectedness and Systemic Risk*. J. Financ. Econom. 2018, 16, 271–296. [Google Scholar] [CrossRef]

- Stiassny, A. A spectral decomposition for structural VAR models. Empir. Econ. 1996, 21, 535–555. [Google Scholar] [CrossRef]

- Reboredo, J.C.; Rivera-Castro, M.A.; Ugolini, A. Waveletbased test of co-movement and causality between oil and renewable energy stock prices. Energy Econ. 2017, 61, 241–252. [Google Scholar] [CrossRef]

- Bouoiyour, J.; Gauthier, M.; Bouri, E. Which is leading: Renewable or brown energy assets? Energy Econ. 2023, 117, 106339. [Google Scholar] [CrossRef]

- Li, J.; Umar, M.; Huo, J. The spillover effect between Chinese crude oil futures market and Chinese green energy stock market. Energy Econ. 2023, 119, 106568. [Google Scholar] [CrossRef]

- Saeed, T.; Bouri, E.; Tran, D.K. Hedging strategies of green assets against dirty energy assets. Energies 2020, 13, 3141. [Google Scholar] [CrossRef]

- Saeed, T.; Bouri, E.; Alsulami, H. Extreme return connectedness and its determinants between clean/green and dirty energy investments. Energy Econ. 2021, 96, 105017. [Google Scholar] [CrossRef]

- Xi, Y.; Zeng, Q.; Lu, X.; Huynh, T.L. Oil and renewable energy stock markets: Unique role of extreme shocks. Energy Econ. 2022, 109, 105995. [Google Scholar] [CrossRef]

- Ferrer, R.; Shahzad, S.J.H.; López, R.; Jareño, F. Time and frequency dynamics of connectedness between renewable energy stocks and crude oil prices. Energy Econ. 2018, 76, 1–20. [Google Scholar] [CrossRef]

- Chen, Y.; Wei, Y.; Bai, L.; Zhang, J. Can Green Economy stocks hedge natural gas market risk? Evidence during Russia-Ukraine conflict and other crisis periods. Financ. Res. Lett. 2023, 53, 103632. [Google Scholar] [CrossRef]

- Strohsal, T.; Proaño, C.R.; Wolters, J. Characterizing the financial cycle: Evidence from a frequency domain analysis. J. Bank. Financ. 2019, 106, 568–591. [Google Scholar] [CrossRef] [Green Version]

- Urom, C.; Mzoughi, H.; Abid, I.; Brahim, M. Green markets integration in different time scales: A regional analysis. Energy Econ. 2021, 98, 105254. [Google Scholar] [CrossRef]

- Gunay, S.; Muhammed, S.; Elkanj, N. Risk transmissions between regional green economy indices: Evidence from the US, Europe and Asia. J. Clean. Prod. 2022, 379, 134752. [Google Scholar] [CrossRef]

- Naeem, M.A.; Peng, Z.; Suleman, M.T.; Nepal, R.; Shahzad, S.J.H. Time and frequency connectedness among oil shocks, electricity and clean energy markets. Energy Econ. 2020, 91, 104914. [Google Scholar] [CrossRef]

- Foglia, M.; Eliana, A. Volatility Connectedness between Clean Energy Firms and Crude Oil in the COVID-19 Era. Sustainability 2020, 12, 9863. [Google Scholar] [CrossRef]

- Antonakakis, N.; Gabauer, D.; Gupta, R.; Plakandaras, V. Dynamic connectedness of uncertainty across developed economies: A time-varying approach. Econ. Lett. 2018, 166, 63–75. [Google Scholar] [CrossRef] [Green Version]

- Dai, Z.; Zhu, H.; Zhang, X. Dynamic spillover effects and portfolio strategies between crude oil, gold and Chinese stock markets related to new energy vehicle. Energy Econ. 2022, 109, 105959. [Google Scholar] [CrossRef]

- Wang, Q.; Wang, L.; Li, R. Renewable energy and economic growth revisited: The dual roles of resource dependence and anticorruption regulation. J. Clean. Prod. 2022, 337, 130514. [Google Scholar] [CrossRef]

- Jiang, P.; Fan, Y.; Klemeš, J.J. Impacts of COVID-19 on energy demand and consumption: Challenges, lessons and emerging opportunities. Appl. Energy 2021, 285, 116441. [Google Scholar] [CrossRef]

- Li, S.; Wang, Q.; Jiang, X.; Li, R. The negative impact of the COVID-19 on renewable energy growth in developing countries: Underestimated. J. Clean. Prod. 2022, 367, 132996. [Google Scholar] [CrossRef]

- Mensi, W.; Kharusi, S.A.; Vo, X.V.; Kang, S.H. Frequency connectedness and spillovers among oil and Islamic sector stock markets: Portfolio hedging implications. Borsa Istanb. Rev. 2022, 22, 1098–1117. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| QGREEN | GRNUS | GRNEUR | GRASIA | WTI | GAS | |

|---|---|---|---|---|---|---|

| Mean | 0.0498 | 0.0653 | 0.0412 | 0.0197 | −0.0011 | 0.0322 |

| Median | 0.1035 | 0.1236 | 0.1069 | 0.0501 | 0.1074 | 0.0000 |

| Maximum | 7.8529 | 8.6262 | 6.3283 | 8.4938 | 31.9634 | 38.1727 |

| Minimum | −11.3357 | −10.1756 | −14.8709 | −10.0905 | −60.2675 | −30.0480 |

| Std. Deviation | 1.0191 | 1.1514 | 1.1452 | 1.1125 | 3.0973 | 3.3470 |

| Skewness | −0.8060 | −0.3911 | −1.8066 | −0.3934 | −3.0606 | 0.4983 |

| Kurtosis | 15.1736 | 11.7638 | 22.1366 | 11.0145 | 80.8018 | 15.1663 |

| JB | 15,010 *** | 7,706.1 *** | 37,753 *** | 6,455.4 *** | 606,267 *** | 14,833 *** |

| ADF | −30.8465 *** | −31.7342 *** | −32.0431 *** | −32.9478 *** | −37.4365 *** | −37.0858 *** |

| QGREEN | GRNUS | GRNEUR | GRASIA | WTI | GAS | FROM | |

|---|---|---|---|---|---|---|---|

| QGREEN | 34.16 | 30.64 | 23.03 | 8.76 | 3 | 0.41 | 65.84 |

| GRNUS | 34.55 | 39.87 | 15.78 | 6.38 | 2.9 | 0.53 | 60.13 |

| GRNEUR | 29.46 | 18.44 | 41.18 | 7.83 | 2.76 | 0.33 | 58.82 |

| GRASIA | 18.89 | 14.11 | 13.08 | 51.29 | 1.88 | 0.75 | 48.71 |

| WTI | 5.41 | 4.94 | 4.03 | 1.47 | 82.74 | 1.41 | 17.26 |

| GAS | 0.79 | 1.04 | 0.53 | 0.59 | 1.74 | 95.31 | 4.69 |

| TO | 89.1 | 69.17 | 56.44 | 25.03 | 12.28 | 3.43 | 255.44 |

| NET | 23.26 | 9.04 | −2.38 | −23.68 | −4.98 | −1.26 | 42.57 |

| Panel A: Short Term (1–5 days) | |||||||

| QGREEN | GRNUS | GRNEUR | GRASIA | WTI | GAS | FROM | |

| QGREEN | 21.32 | 18.97 | 14.49 | 5.66 | 1.78 | 0.25 | 41.16 |

| GRNUS | 22.19 | 25.71 | 10.03 | 4.18 | 1.75 | 0.35 | 38.5 |

| GRNEUR | 18.12 | 10.9 | 26.22 | 4.96 | 1.62 | 0.2 | 35.8 |

| GRASIA | 10.28 | 7.36 | 7.23 | 32.8 | 1.07 | 0.45 | 26.4 |

| WTI | 3.92 | 3.57 | 2.95 | 1.02 | 60.7 | 1.03 | 12.49 |

| GAS | 0.6 | 0.78 | 0.41 | 0.43 | 1.28 | 70.59 | 3.49 |

| TO | 55.11 | 41.58 | 35.1 | 16.26 | 7.51 | 2.29 | 157.84 |

| ALL | 76.43 | 67.28 | 61.32 | 49.06 | 68.21 | 72.88 | TCI |

| NET | 13.95 | 3.08 | −0.7 | −10.14 | −4.98 | −1.21 | 26.31 |

| Panel B: Medium Term (5–20 days) | |||||||

| QGREEN | GRNUS | GRNEUR | GRASIA | WTI | GAS | FROM | |

| QGREEN | 8.28 | 7.86 | 5.39 | 1.93 | 0.89 | 0.11 | 16.17 |

| GRNUS | 7.98 | 9.31 | 3.78 | 1.38 | 0.84 | 0.12 | 14.09 |

| GRNEUR | 7.61 | 5.36 | 9.03 | 1.82 | 0.81 | 0.08 | 15.69 |

| GRASIA | 6.18 | 4.91 | 4.11 | 10.49 | 0.56 | 0.18 | 15.94 |

| WTI | 1.01 | 0.93 | 0.71 | 0.33 | 14.62 | 0.25 | 3.23 |

| GAS | 0.14 | 0.19 | 0.08 | 0.1 | 0.31 | 16.5 | 0.82 |

| TO | 22.91 | 19.25 | 14.07 | 5.55 | 3.42 | 0.74 | 65.94 |

| ALL | 31.19 | 28.55 | 23.1 | 16.04 | 18.04 | 17.24 | TCI |

| NET | 6.74 | 5.15 | −1.62 | −10.39 | 0.19 | −0.08 | 10.99 |

| Panel C: Long Term (20–infinite days) | |||||||

| QGREEN | GRNUS | GRNEUR | GRASIA | WTI | GAS | FROM | |

| QGREEN | 4.43 | 4.22 | 2.87 | 1.01 | 0.48 | 0.06 | 8.64 |

| GRNUS | 4.22 | 4.92 | 2.01 | 0.72 | 0.45 | 0.06 | 7.48 |

| GRNEUR | 4.1 | 2.92 | 4.79 | 0.97 | 0.45 | 0.05 | 8.48 |

| GRASIA | 3.44 | 2.76 | 2.28 | 5.47 | 0.31 | 0.09 | 8.89 |

| WTI | 0.52 | 0.48 | 0.36 | 0.17 | 7.31 | 0.13 | 1.66 |

| GAS | 0.07 | 0.1 | 0.04 | 0.05 | 0.16 | 8.19 | 0.4 |

| TO | 12.35 | 10.48 | 7.56 | 2.92 | 1.85 | 0.39 | 35.55 |

| NET | 3.71 | 3 | −0.92 | −5.97 | 0.19 | −0.01 | 5.92 |

| Panel A: Pre-COVID-19 | |||||||

| QGREEN | GRNUS | GRNEUR | GRASIA | WTI | GAS | FROM | |

| QGREEN | 34.99 | 28.47 | 23.07 | 8.14 | 2 | 3.33 | 65.01 |

| GRNUS | 34.93 | 39.65 | 14.95 | 4.22 | 1.64 | 4.62 | 60.35 |

| GRNEUR | 28.02 | 13.15 | 46.02 | 6.05 | 4.46 | 2.3 | 53.98 |

| GRASIA | 11.83 | 5.85 | 9.24 | 63.68 | 4.85 | 4.56 | 36.32 |

| WTI | 5.67 | 11.72 | 0.88 | 4.92 | 72.86 | 3.97 | 27.14 |

| GAS | 4.88 | 6.54 | 3.65 | 5.14 | 4.06 | 75.72 | 24.28 |

| TO | 85.32 | 65.73 | 51.79 | 28.46 | 17.01 | 18.78 | 267.08 |

| NET | 20.31 | 5.38 | −2.19 | −7.86 | −10.14 | −5.5 | 44.51 |

| Panel B: COVID-19 | |||||||

| QGREEN | GRNUS | GRNEUR | GRASIA | WTI | GAS | FROM | |

| QGREEN | 28.16 | 28.47 | 21.89 | 11.87 | 3.26 | 6.34 | 71.84 |

| GRNUS | 28 | 30.51 | 18.7 | 11.99 | 3.28 | 7.52 | 69.49 |

| GRNEUR | 27.2 | 23.55 | 30.96 | 11.58 | 2.57 | 4.13 | 69.04 |

| GRASIA | 22.88 | 23.53 | 19.52 | 26.21 | 3.08 | 4.78 | 73.79 |

| WTI | 6.6 | 7.31 | 4.31 | 1.1 | 79.17 | 1.5 | 20.83 |

| GAS | 11.64 | 15.05 | 6.14 | 2.89 | 0.82 | 63.47 | 36.53 |

| TO | 96.32 | 97.91 | 70.57 | 39.43 | 13.01 | 24.27 | 341.52 |

| NET | 24.49 | 28.41 | 1.53 | −34.36 | −7.82 | −12.26 | 56.92 |

| Panel C: Post-COVID-19 | |||||||

| QGREEN | GRNUS | GRNEUR | GRASIA | WTI | GAS | FROM | |

| QGREEN | 37.33 | 35.38 | 16.34 | 9.11 | 1.65 | 0.2 | 62.67 |

| GRNUS | 38.11 | 41.75 | 10.67 | 7.5 | 1.69 | 0.27 | 58.25 |

| GRNEUR | 25.18 | 16.43 | 50.43 | 6.57 | 1.2 | 0.18 | 49.57 |

| GRASIA | 19.34 | 16.63 | 9.38 | 52.76 | 1.31 | 0.59 | 47.24 |

| WTI | 4.15 | 3.73 | 2.05 | 2.62 | 86.86 | 0.59 | 13.14 |

| GAS | 0.74 | 0.93 | 0.82 | 0.82 | 0.63 | 96.07 | 3.93 |

| TO | 87.51 | 73.1 | 39.26 | 26.62 | 6.48 | 1.83 | 234.79 |

| NET | 24.84 | 14.85 | −10.31 | −20.62 | −6.66 | −2.1 | 39.13 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhao, L.; He, W.; Wang, A.; Zhu, F. Time and Frequency Spillovers between the Green Economy and Traditional Energy Markets. Systems 2023, 11, 153. https://doi.org/10.3390/systems11030153

Zhao L, He W, Wang A, Zhu F. Time and Frequency Spillovers between the Green Economy and Traditional Energy Markets. Systems. 2023; 11(3):153. https://doi.org/10.3390/systems11030153

Chicago/Turabian StyleZhao, Lili, Wenke He, Anwen Wang, and Fangfei Zhu. 2023. "Time and Frequency Spillovers between the Green Economy and Traditional Energy Markets" Systems 11, no. 3: 153. https://doi.org/10.3390/systems11030153