Market Needs, Opportunities and Barriers for the Floating Wind Industry

Abstract

:1. Introduction

2. Floating Wind Farms

- Hywind wind farm.

- Kincardine wind farm.

- Windfloat wind farm.

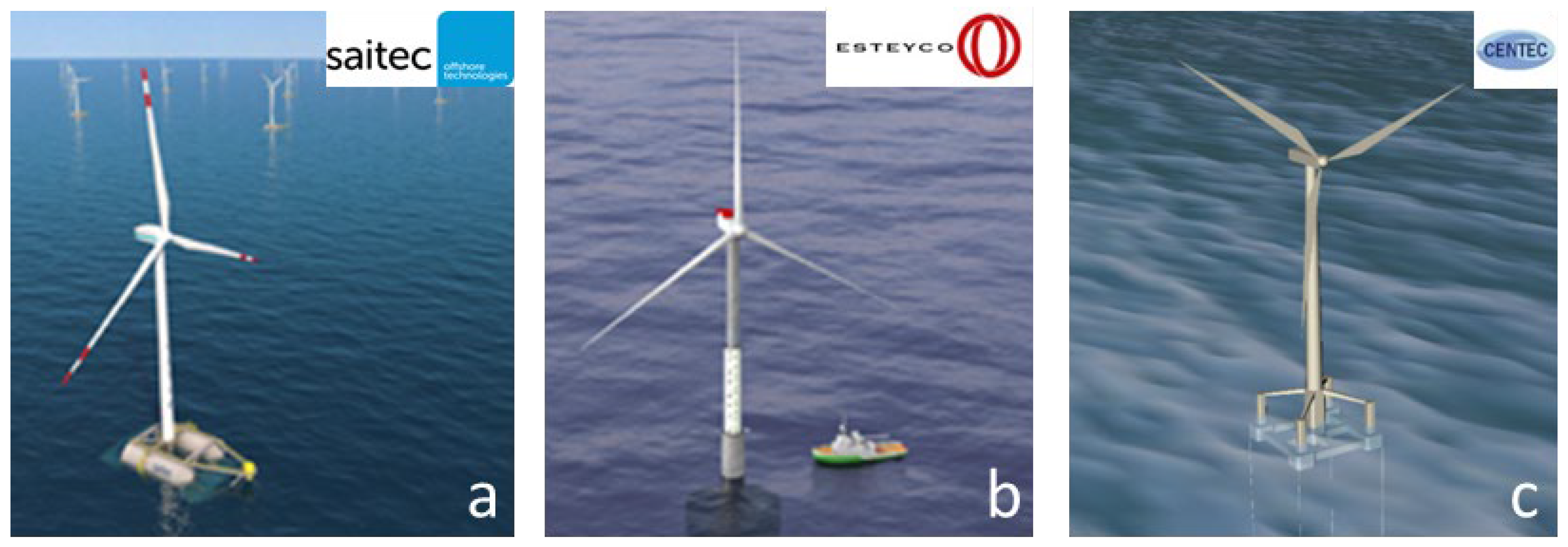

3. Technology Review

4. Floating Wind Power in Numbers

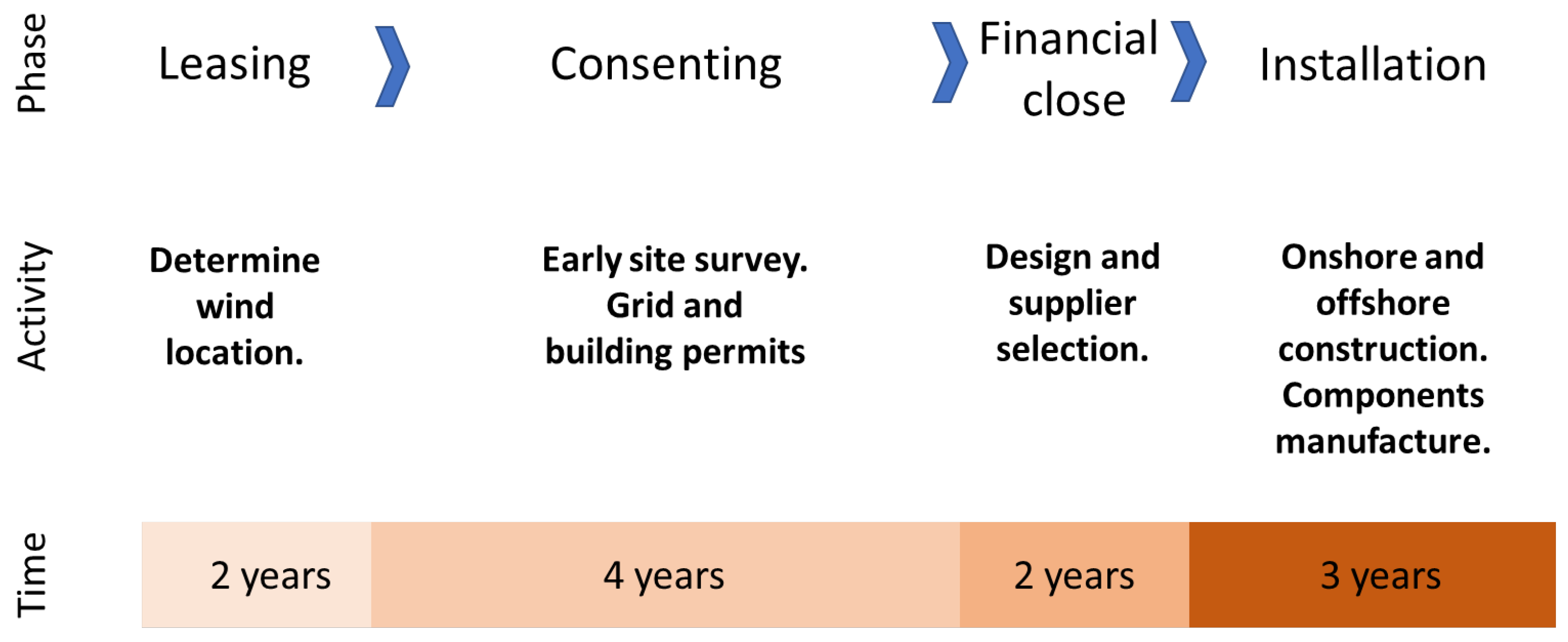

4.1. Offshore Wind Farm Development Stages

- Leasing: This comprises selecting wind farm locations, managing the environment, maritime spatial planning (MSP), and others. The leasing task is complete with adjudicating the right to explore the wind resource in a given space to a developer as part of a competitive process. Typically, it takes 2 years.

- Consenting: This comprises the obtaining of construction and operation permits. The early site surveys and the front-end engineering design parallel the permitting process. The process takes 2 + 2 years to obtain the data and consent. Some projects can take significantly longer due to economic or environmental reasons. Obtaining the licenses to install and operate the project means the end of the consenting step.

- Financial close: A detailed design and favorable financial investment are included in this step. Moreover, the power purchase agreement is mandatory in this phase. A time slot of 2 years from consent is required due to the competitive auctions. The possibility of failing at this stage is high; nevertheless, the impact on development rates is not considered.

- Installation: This step includes offshore and onshore construction, grid connection, manufacture, and pre-assembly of components before installation. Almost 3 years are required to complete this phase. The wind farm is considered commissioned after starting with generating and transmitting power back to shore.

4.2. Global Wind Energy Council

4.3. Wind Europe

- Below EUR 50/MWh in 2030—Very low LCOE.

- Between EUR 50/MWh and EUR 65/MWh in 2030—Low LCOE.

- Between EUR 65/MWh and EUR 80/MWh in 2030—Medium LCOE.

- Over EUR 80/MWh in 2030—High LCOE.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Sub Region | Capacity Allocated (GW) | Offshore Area (km2) | Portion of Area with d > 50 m | |||

|---|---|---|---|---|---|---|

| Very Low LCOE | Low LCOE | Mid LCOE | High LCOE | |||

| IE01 | 6.7 | 1340 | 0% | 60% | 0% | 0% |

| IE02 | 15.5 | 3100 | 0% | 11% | 37% | 48% |

| FR01 | 20.9 | 4180 | 4% | 45% | 14% | 0% |

| FR02 | 19.6 | 3920 | 0% | 23% | 52% | 15% |

| UK01 | 2.6 | 520 | 2% | 49% | 21% | 4% |

| UK05 | 8.5 | 1700 | 0% | 35% | 25% | 2% |

4.4. European Commission: An EU Strategy to Harness the Potential of Offshore Renewable Energy for a Climate-Neutral Future

5. Floating Wind Energy Market

5.1. Research and Development Trends and the Future of the Floating Wind Industry

5.2. The Port Activities in the Floating Wind Industry

5.3. The Environmental Considerations

5.4. Social Aspects

5.5. Legal Aspects

5.6. Technological Aspects

5.7. Floating Offshore Wind Barriers for Commercialization

- 1.

- Maritime Spatial Planning: There is a need to increase the rate of site allocation and development for achieving, at least in Europe, the environmental commitments of the Paris Climate Agreement. This is in hands of the policymakers that need to move quickly to put in motion the long process required for a wind farm development.

- 2.

- Environmental Impact: Although the comparison with the oil and gas business is clear, it is required to ensure that focusing the energy transition on the offshore wind industry is the right decision.

- 3.

- Multiple Use: The future of offshore wind goes towards the sharing of the sea between users.

- 4.

- Expand the grid offshore and onshore: The electricity grid infrastructure in Europe needs to be able to absorb the power foreseen to be installed. This will require, most likely, the collaboration between countries, which requires a legal framework that still needs to be constructed.

- 5.

- Stable Rates: The policymakers need to stabilize the energy rates for allowing the project to capture investments. This will increase the supply chain that will feel more comfortable investing in the necessary upgrading of vessels, ports, and onshore facilities that could be amortized in longer periods.

- 6.

- Mobilizing investments: WindEurope, in the frame of Europe’s objective for 2050, estimates that CAPEX needs to be threefold for offshore wind farms and transmission grids. Their estimate requires to go from EUR 6 bn per year in 2020, to more than EUR 21 bn per year in 2025. In 2030, the investments will need to be around EUR 45 bn. In total, this means spending around 10% of the total infrastructure budget across Europe, on offshore wind.

- 7.

- Technology Readiness: The TRL achieved by different concepts such as Equinor’s spar, Ideol’s barge, or PPI’s semisubmersible, encourage the experts to believe that this will not be a drawback for the FOW future. However, for other concepts, there is still a long way to walk, but the de-risking process shall be faster every day.

- 8.

- Industrialization: The designers need to intensify their efforts for thinking about the ways to allow an industrial process that allows the cost competitiveness of offshore wind energy. The step from demonstrator or pre-series to full commercialization needs to be taken. Thinking about these fabrication, transport, and installation procedures will allow the governments to know how to upgrade the harbor facilities.

- 9.

- Scalability: The turbine sizes are in continuous growth, and it is usually overtaking the foundation designs. The recent GE 12 MW turbine is a tremendous challenge for the foundation designers. In light of the speed in which these new turbines have reached the market, it is expected that the exigencies of the floaters will be very demanding in the future.

- 10.

- High Levelized Cost of Energy: In recent years, significant cost reductions in the onshore and bottom fixed offshore wind sectors were witnessed. FOW is anticipated to follow a similar downward trend with a cost decrease of 38–50% leading to 2050, following the suggestions of IEA experts. There are several other factors which may also lead to further cost reductions.

- (a)

- One of the main advantages of FOW is the positioning in areas with higher average wind speeds, allowing to harness the best possible wind resources without depth constraints. The capacity factor can thus be improved and lead to increased electricity generation. With higher capacity factors, the levelized cost of energy (LCOE) will be reduced.

- (b)

- Technology that allows a cost-effective exchange of large turbine components offshore when floating foundation structures are moving due to wave motion. The maintenance of turbines in FOWT is a non-solved issue, the players in the industry are demanding cost-effective solutions for the large correctives of the turbines in the FOW.For spars, whose final configuration is too deep to be taken into the harbor, this would imply such prohibitive costs that it simply cannot be considered a valid option for future large commercial floating farms. Proof of this is the contest of ideas to solve this problem proposed in 2017 by Equinor. This initiative has, however, failed to provide any concept promising and ready enough to be field-tested and demonstrated, and as of today Equinor openly admits that LCM interventions for their SPAR floating wind turbines are an issue yet to be solved.With semisubmersibles, whose draught is much smaller, the full de-installation and reinstallation of complete units might be considered a viable alternative for a commercial wind farm. They would be towed to the harbor to use onshore cranes for Large Corrective Operations. Even so, the cost of the mooring and mooring large structures, disconnecting and reconnecting the dynamic riser power cables, decommissioning and recommissioning the turbine and electrical systems are very high, and required the mobilization of multiple specialized vessels and need very long operative weather windows leading to prolonged unproductive periods.

- (c)

- In the same framework as the previous, the industry is looking for cost-effective solutions for maintaining floating offshore foundations due to the capability of towing the structure to the port.

- (d)

- Cost-effective manufacturing, installation, and maintenance of the large volume of mooring lines and anchors in floating wind farms. Mooring systems and their installations are important cost contributors, particularly given the large volume of mooring lines and anchors that must be installed.

- (e)

- Cost-effective monitoring and inspection of a large number of mooring lines, cables, and foundation structures. Current solutions are based on Remotely Operated Vehicles (ROVs) or divers, feasible solutions inherited from the oil and gas industry due to the small number of lines.

6. Discussion and Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A. Asian Floating Wind Projects

| Project | Country | Pipeline Status | COD | Capacity (MW) | Water Depth (m) | Developer | Turbine Rating (MW) | Substructure |

| Fukushima floating offshore wind farm phase 1 | Japan | Installed | 2013 | 2 | 120 | Marubeni Corporation | 2 | Semisubmersible |

| Fukushima floating offshore wind farm phase 2 | Japan | Installed | 2015 | 5 | 120 | Marubeni Corporation | 5 | Semisubmersible |

| Sakiyama | Japan | Installed | 2016 | 3 | 100 | TODA Corporation | 2 | Spar |

| Kitakyusu (NEDO) | Japan | Under construction | 2019 | 3 | 70 | NEDO—Ideol | 3 | Semisubmersible |

| Hitachi Zosen | Japan | Permitting | 2024 | 400 | - | Equino— Hitachi | - | Semisubmersible |

| Macquaire | Japan | Planning | 2025 | 500 | 100 | Macquaire | - | - |

| Ulsan | South Korea | Financial close | 2019 | 0.75 | 15 | Consortium | 0.75 | Semisubmersible |

| Donghae KNOC | South Korea | Planning | 2027 | - | - | Equinor—KNOC | - | - |

| Ulsan shell | South Korea | Planning | 2027 | 200 | - | Shell—Hexicon | - | Semisubmersible |

| Ulsan Macquaire | South Korea | Planning | 2027 | 200 | - | Macquaire | - | - |

| Ulsan SK | South Korea | Planning | 2027 | 200 | - | SK—E&S | - | - |

| Ulsan KF | South Korea | Planning | 2027 | 200 | - | KF Wind—PPI | - | Semisubmersible |

| Floatinf W1N | Taiwan | Planning | 2025 | 500 | - | Eolfi—Cobra | - | - |

Appendix B. American Floating Wind Projects

| Project | Country | Pipeline Status | COD | Capacity (MW) | Water Depth (m) | Developer | Turbine Rating (MW) | Substructure |

| Castle Wind | USA | Planning | 2027 | 1000 | 900 | EnBW | 8 | Semisubmersible |

| Redwood coast | USA | Planning | 2025 | 150 | 550 | EDPR—PPI | 8 | Semisubmersible |

| Aqua Ventus I | USA | Planning | 2022 | 12 | 100 | University of Maine | 6 | Semisubmersible |

| Oahu North | USA | Planning | 2027 | 400 | 850 | AW Wind | 6 | Semisubmersible |

| Oahu South | USA | Planning | 2027 | 400 | 600 | AW Wind | 6 | Semisubmersible |

| Progression Wind | USA | Planning | 2027 | 400 | 650 | Progression Wind | 6 | Semisubmersible |

References

- U.S. Energy Information Administration. International Energy Outlook 2021; U.S. Energy Information Administration: Washington, DC, USA, 2021.

- Eurostat. Energy Balance Sheets 2017 Data, 2019th ed.; Eurostat: Luxembourg, 2019; ISBN 978-92-76-08714-4. [Google Scholar]

- Eurostat Eurostat Data Browser. Available online: https://ec.europa.eu/eurostat/en/ (accessed on 5 November 2021).

- Eurostat. Energy Data 2020 Edition; European Union: Luxembourg, 2020; ISBN 978-92-76-20629-3. [Google Scholar]

- Wind Europe. Wind Energy in Europe 2020 Statistics and the Outlook for 2021–2025; Wind Europe: Brussels, Belgium, 2021. [Google Scholar]

- Díaz, H.; Guedes Soares, C. An integrated GIS approach for site selection of floating offshore wind farms in the Atlantic continental European coastline. Renew. Sustain. Energy Rev. 2020, 134, 110328. [Google Scholar] [CrossRef]

- Díaz, H.; Fonseca, R.B.; Guedes Soares, C. Site selection process for floating offshore wind farms in Madeira Islands. In Advances in Renewable Energies Offshore; Guedes Soares, C., Ed.; Taylor & Francis: London, UK, 2019; pp. 729–737. [Google Scholar]

- Akhtar, N.; Geyer, B.; Rockel, B.; Sommer, P.S.; Schrum, C. Accelerating deployment of offshore wind energy alter wind climate and reduce future power generation potentials. Sci. Rep. 2021, 11, 11826. [Google Scholar] [CrossRef] [PubMed]

- Watson, S.; Moro, A.; Reis, V.; Baniotopoulos, C.; Barth, S.; Bartoli, G.; Bauer, F.; Boelman, E.; Bosse, D.; Cherubini, A.; et al. Future emerging technologies in the wind power sector: A European perspective. Renew. Sustain. Energy Rev. 2019, 113, 109270. [Google Scholar] [CrossRef]

- European Commission the European Green Deal. Eur. Comm. 2019, 53, 24. [CrossRef]

- Salvação, N.; Bernardino, M.; Guedes Soares, C. Assessing the offshore wind energy potential along the coasts of Portugal and Galicia. In Developments in Maritime Transportation and Exploitation of Sea Resources; Guedes Soares, C., Lopez Pena, F., Eds.; Taylor & Francis Group: London, UK, 2014; pp. 995–1002. [Google Scholar] [CrossRef]

- Castro-Santos, L.; Bento, A.R.; Silva, D.; Salvação, N.; Guedes Soares, C. Economic Feasibility of Floating Offshore Wind Farms in the North of Spain. J. Mar. Sci. Eng. 2020, 8, 58. [Google Scholar] [CrossRef] [Green Version]

- Salvacao, N.; Guedes Soares, C. Resource Assessment Methods in the Offshore Wind Energy Sector. In Floating Offshore Wind Farms; Castro-Santos, L., Diaz-Casas, V., Eds.; Springer International Publishing: Berlin/Heidelberg, Germany, 2016; pp. 121–141. [Google Scholar]

- Uzunoglu, E.; Karmakar, D.; Guedes Soares, C. Floating offshore wind platforms. In Floating Offshore Wind Farms; Castro-Santos, L., Diaz-Casas, V., Eds.; Springer International Publishing: Berlin/Heidelberg, Germany, 2016; pp. 53–76. [Google Scholar]

- Wang, C.M.; Utsunomiya, T.; Wee, S.C.; Choo, Y.S. Research on floating wind turbines: A literature survey. IES J. Part A Civ. Struct. Eng. 2010, 3, 267–277. [Google Scholar] [CrossRef] [Green Version]

- Uzunoglu, E.; Guedes Soares, C. Hydrodynamic design of a free-float capable tension leg platform for a 10 MW wind turbine. Ocean Eng. 2020, 197, 106888. [Google Scholar] [CrossRef]

- Equinor Hywind Scotland. Available online: https://www.equinor.com/ (accessed on 5 November 2021).

- Principle Power Windfloat. Available online: www.principlepowerinc.com (accessed on 5 November 2021).

- Cobra Group Kincardine Floating Offshore Wind Farm. Available online: https://www.grupocobra.com/en/proyecto/kincardine-offshore-floating-wind-farm/ (accessed on 5 November 2021).

- Díaz, H.; Rodrigues, J.M.; Guedes Soares, C. Evaluation of an offshore floating wind power project on the Galician coast. In Proceedings of the International Conference on Offshore Mechanics and Arctic Engineering—OMAE, Trondheim, Norway, 25–30 June 2017; Volume 10. [Google Scholar] [CrossRef]

- Díaz, H.; Rodrigues, J.M.; Guedes Soares, C. Preliminary cost assessment of an offshore floating wind farm installation on the Galician coast. In Progress in Renewable Energies Offshore; Guedes Soares, C., Ed.; Taylor & Francis Group: London, UK, 2016; pp. 843–850. [Google Scholar]

- International Bank for Reconstruction and Development/The World Bank. The Energy Progress Report 2018; International Bank for Reconstruction and Development/The World Bank: Washington, DC, USA, 2018. [Google Scholar]

- Bashetty, S.; Ozcelik, S. Review on dynamics of offshore floating wind turbine platforms. Energies 2021, 14, 6026. [Google Scholar] [CrossRef]

- Huijs, F.; De Bruijn, R.; Savenije, F. Concept design verification of a semi-submersible floating wind turbine using coupled simulations. Energy Procedia 2014, 53, 2–12. [Google Scholar] [CrossRef] [Green Version]

- Jiang, Z.; Yttervik, R.; Gao, Z.; Sandvik, P.C. Design, modelling, and analysis of a large floating dock for spar floating wind turbine installation. Mar. Struct. 2020, 72, 102781. [Google Scholar] [CrossRef]

- Matha, D.; Sandner, F.; Molins, C.; Campos, A.; Cheng, P.W. Efficient preliminary floating offshore wind turbine design and testing methodologies and application to a concrete spar design. Philos. Trans. R. Soc. A Math. Phys. Eng. Sci. 2015, 373, 20140350. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Uzunoglu, E.; Guedes Soares, C. A system for the hydrodynamic design of tension leg platforms of floating wind turbines. Ocean Eng. 2019, 171, 78–92. [Google Scholar] [CrossRef]

- ARCWIND. Project Arcwind. Available online: http://www.arcwind.eu/ (accessed on 5 November 2021).

- Baita-Saavedra, E.; Cordal-Iglesias, D.; Filgueira-Vizoso, A.; Morató, À.; Lamas-Galdo, I.; Álvarez-Feal, C.; Carral, L.; Castro-Santos, L. An economic analysis of an innovative floating offshore wind platform built with concrete: The SATH® platform. Appl. Sci. 2020, 10, 3678. [Google Scholar] [CrossRef]

- Cartelle-Barros, J.J.; Cordal-Iglesias, D.; Baita-Saavedra, E.; Filgueira-Vizoso, A.; Couñago-Lorenzo, B.; Vigara, F.; Cortés, C.; Cerdán, L.; Nieto, J.; Serna, J.; et al. Pathways to bring the costs down of floating offshore wind farms in the Atlantic Area. Wind Energy Sci. Discuss. 2019, 2019, 1–12. [Google Scholar]

- Global Wind Energy Council Green Recovery Data and Analysis. Available online: https://gwec.net/ (accessed on 5 November 2021).

- WindEurope Policy. Available online: https://windeurope.org/ (accessed on 5 November 2021).

- Wind Europe. Floating Offshore Wind Vision Statement; Wind Europe: Brussels, Belgium, 2017. [Google Scholar]

- Global Wind Energy Council. GWEC Global Wind Report 2019; Global Wind Energy Council: Brussels, Belgium, 2019. [Google Scholar]

- Global Wind Energy Council. Global Offshore Wind: Annual Market Report 2020; Global Wind Energy Council: Brussels, Belgium, 2020. [Google Scholar]

- IRENA. Future of Wind: Deployment, Investment, Technology, Grid Integration and Socio-Economic Aspects; IRENA: Abu Dhabi, United Arab Emirates, 2019. [Google Scholar]

- Wind Europe. Floating Offshore Wind Energy—A Policy Blueprint for Europe; Wind Europe: Brussels, Belgium, 2019. [Google Scholar]

- European Union. An EU Strategy to Harness the Potential of Offshore Renewable Energy for a Climate Neutral Future; European Union: Luxembourg, 2020. [Google Scholar]

- Díaz, H.; Guedes Soares, C. Review of the current status, technology and future trends of offshore wind farms. Ocean Eng. 2020, 209, 107381. [Google Scholar] [CrossRef]

- Yao, S.; Chetan, M.; Griffith, D.T.; Escalera Mendoza, A.S.; Selig, M.S.; Martin, D.; Kianbakht, S.; Johnson, K.; Loth, E. Aero-structural design and optimization of 50 MW wind turbine with over 250-m blades. Wind Eng. 2021, 46, 273–295. [Google Scholar] [CrossRef]

- Schütt, M.; Anstock, F.; Schorbach, V. Progressive structural scaling of a 20 MW two-bladed offshore wind turbine rotor blade examined by finite element analyses. J. Phys. Conf. Ser. 2020, 1618, 052017. [Google Scholar] [CrossRef]

- Host, A.; Skender, H.P.; Mirković, P.A. The perspectives of port integration into the global supply Chains—The case of North Adriatic ports. Pomorstvo 2018, 32, 42–49. [Google Scholar] [CrossRef]

- Junqueira, H.; Robaina, M.; Garrido, S.; Godina, R.; Matias, J.C.O. Viability of creating an offshore wind energy cluster: A case study. Appl. Sci. 2021, 11, 308. [Google Scholar] [CrossRef]

- Cooper, B.D.; Marrone, J.F. Port requirements to support offshore wind development in North America. In Ports 2013 Success Through Diversification, Proceedings of the 13th Triennial International Conference, Seattle, WA, USA, 25–28 August 2013; ASCE: Reston, VA, USA, 2013; pp. 1473–1482. [Google Scholar] [CrossRef]

- Díaz, H.; Guedes Soares, C. A Multi-Criteria Approach to Evaluate Floating Offshore Wind Farms Siting in the Canary Islands (Spain). Energies 2021, 14, 865. [Google Scholar] [CrossRef]

- Firestone, J.; Kempton, W.; Lilley, M.B.; Samoteskul, K. Public acceptance of offshore wind power: Does perceived fairness of process matter? J. Environ. Plan. Manag. 2012, 55, 1387–1402. [Google Scholar] [CrossRef]

- Nordman, E.; VanderMolen, J.; Gajewski, B.; Isely, P.; Fan, Y.; Koches, J.; Damm, S.; Ferguson, A.; Schoolmaster, C. An integrated assessment for wind energy in Lake Michigan coastal counties. Integr. Environ. Assess. Manag. 2015, 11, 287–297. [Google Scholar] [CrossRef] [PubMed]

| Foundation | Opportunities | Barriers |

|---|---|---|

| Semisubmersible | High technology readiness levels (TRLs) | Internal forces dependent on geometries Expensive ballast system High competition between developers Heavy structure Large dimensions for future 15 MW+ turbines |

| Global market position | ||

| Several turbines integration in a foundation | ||

| Easy geometries | ||

| Full system easy transportation Depth independence Simple mooring system | ||

| Barge | Low-cost production | No global market position |

| Easy geometries | Launching technique | |

| Depth independence | Heavy structure | |

| Simple mooring system | Large dimensions for future 15 MW+ turbines | |

| Motion reduction | ||

| Flat without interspaces Full system easy transportation | ||

| Conventional Spar | High TRL | Final assembly in the position No global market position Construction complexity |

| Easy mass production with tower synergies | ||

| Material usage Simple mooring system | ||

| TLP | Low-cost production Light structure Not soil dependent for anchor system Suitable for extreme sea states Excellent stability Full system easy transportation | Expensive mooring system Redundant moorings No global market positions Low TRL Suitable intermediate depths |

| Average Rate | |||||||

|---|---|---|---|---|---|---|---|

| 2019–2025 | 2026–2030 | 2031–2035 | 2036–2040 | 2041–2045 | 2046–2050 | Total 2050 | |

| Installed GW | 1.1 | 1.8 | 2.7 | 3.9 | 3.9 | 3.4 | 85 |

| Consented GW | 1.9 | 3.4 | 3.9 | 3.8 | 3.2 | 3.1 | |

| Consented km2 | 370 | 680 | 770 | 750 | 630 | 620 | |

| Project | Country | Pipeline Status | COD | Capacity (MW) | Water Depth (m) | Developer | Turbine Rating (MW) | Substructure |

|---|---|---|---|---|---|---|---|---|

| Eolink 2/10 scale prototype | France | Installed | 2018 | 0.2 | 10 | Eolink | 0.2 | Semisubmersible |

| Floatgen project | France | Installed | 2018 | 2 | 33 | Ideol | 2 | Barge |

| Groix Belle Ille | France | Approved | 2021 | 24 | 62 | Eolfi | 6 | Semisubmersible |

| Provence Grand Large | France | Approved | 2021 | 24 | 30 | EDF | 8 | Tension Leg Platform |

| Eolmed | France | Approved | 2021 | 24 | 62 | Ideol | 6.2 | Barge |

| Les Eoliennes Flotant du Golfe du Lion | France | Approved | 2021 | 24 | 71 | Engie, EDPR, Caisse de Depots | 6 | Semisubmersible |

| GICON Schwimmendes Offshore Fundament SOF Pilot | Germany | Financial close | 2022 | 2.3 | 37 | GICON | 2.3 | Tension Leg Platform |

| Hywind Demo | Norway | Installed | 2009 | 2.3 | 220 | Unitech offshore | 2.3 | Spar |

| TetraSpar Demostrator | Norway | Financial close | 2019 | 3.6 | 200 | Innogy, Shell, Stiesdal | 3.6 | Semisubmersible |

| Hywind Tampen | Norway | Permitting | 2022 | 88 | 110 | Equinor | 8 | Spar |

| NOAKA | Norway | Planning | 2023 | - | 130 | Equinor. Aker, BP | - | - |

| Windfloat Atlantic | Portugal | Financial close | 2019 | 25 | 50 | Windplus | 8 | Semisubmersible |

| DemoSath—Bimep | Spain | Approved | 2020 | 2 | 68 | Saitec offshore technologies | - | Semisubmersible |

| X1 Wind prototype—Plocan | Spain | Approved | 2021 | - | 62 | X1 wind | - | Tension Leg Platform |

| Floating Power Plant—Plocan | Spain | Approved | 2021 | - | 62 | FPP | 8 | Hybrid wave power semisubmersible |

| Hwind Scotland Pilot Park | UK | Installed | 2017 | 30 | 100 | Equinor | 6 | Spar |

| Dounreay Tri | UK | Approved | 2021 | 10 | 76 | Hexicon | 5 | Semisubmersible |

| Kinkardine Offshore wind farm—Phase 1 | UK | Installed | 2018 | 2 | 62 | Cobra | 2 | Semisubmersible |

| Kinkardine Offshore wind farm—Phase 2 | UK | Under construction | 2020 | 50 | 62 | Cobra | 9.5 | Semisubmersible |

| Country | Location | Coordinates (WGS84) | Wind Farm Capacity (MW) | Turbines | Area (km2) | Platform | |

|---|---|---|---|---|---|---|---|

| France | Lannion | 49.2 | −3.6 | 470 | 47 | 62 | Telwind 1 |

| Spain | Gran Canaria | 27.8 | −15.3 | 120 | 12 | 25.37 | |

| Portugal | Figueira da Foz | 40.2 | −9.4 | 700 | 70 | 110 | Sath 2 |

| Scotland | A15 | 58.75 | −6 | 180 | 18 | 22 | |

| Spain | Ribadeo | 44 | −7.3 | 880 | 88 | 405 | C-TLP 3 |

| Ireland | F15 | 52.7 | −10.5 | 250 | 25 | 30.3 | |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Díaz, H.; Serna, J.; Nieto, J.; Guedes Soares, C. Market Needs, Opportunities and Barriers for the Floating Wind Industry. J. Mar. Sci. Eng. 2022, 10, 934. https://doi.org/10.3390/jmse10070934

Díaz H, Serna J, Nieto J, Guedes Soares C. Market Needs, Opportunities and Barriers for the Floating Wind Industry. Journal of Marine Science and Engineering. 2022; 10(7):934. https://doi.org/10.3390/jmse10070934

Chicago/Turabian StyleDíaz, Hugo, José Serna, Javier Nieto, and C. Guedes Soares. 2022. "Market Needs, Opportunities and Barriers for the Floating Wind Industry" Journal of Marine Science and Engineering 10, no. 7: 934. https://doi.org/10.3390/jmse10070934