A Biased-Randomized Iterated Local Search Algorithm for Rich Portfolio Optimization

Abstract

:1. Introduction

2. Need for New Metaheuristic- and Learning-Based Approaches

3. Problem Definition

3.1. Problem Parameters, Variables and Constraints

3.2. The Mathematical Model

3.3. Algorithm Inputs and Outputs

4. The ARPO Metaheuristic

| Algorithm 1 Main procedure of the ARPO algorithm (ILS framework). | |

| procedure ARPO(inputs, minReturn, maxTime, beta) | |

| 1: initSol ← genInitSol(inputs) | ▹ generate sol with highest possible return rate |

| 2: if {getReturn(initSol) < minReturn} then | |

| 3: return unfeasible | ▹ unfeasible problem |

| 4: end if | |

| 5: genFriendshipLists(inputs) | ▹ generate a sorted list of "friends" for each asset |

| 6: baseSol ← QPOptimize(initSol, minReturn) | ▹ optimize levels for each asset in portf. |

| 7: baseSol ← cleanSol(baseSol) | ▹ delete from portf. assets with level = 0 |

| 8: bestSol ← baseSol | ▹ initialize bestSol |

| 9: elapsedTime ← 0 | |

| 10: credit ← 0 | ▹ used in the acceptance criterion |

| 11: while {elapsedTime < maxTime} do | ▹ iterated local search |

| 12: newSol ← perturbateSol(baseSol, inputs, beta) | ▹ destruction-construction stages |

| 13: if {getMaxReturnAsset(newSol) < minReturn} then | ▹ fix solution if unfeasible |

| 14: newSol ← repairSol(newSol, inputs) | |

| 15: end if | |

| 16: if {newSol is in cache} then | ▹ already optimized levels |

| 17: newSol ← loadFromCache(newSol) | ▹ use optimized levels saved in cache |

| 18: else | ▹ apply a local search based on quadratic programming optimization |

| 19: newSol ← QPOptimize(newSol, minReturn) | ▹ optimize levels f.e. asset in portf. |

| 20: newSol ← cleanSol(newSol) | ▹ delete from portf. assets with level = 0 |

| 21: saveInCache(newSol) | |

| 22: end if | |

| 23: delta ← getRisk(newSol) - getRisk(baseSol) | ▹ newSol improves baseSol |

| 24: if {delta < 0} then | |

| 25: credit ← -delta | |

| 26: baseSol ← newSol | |

| 27: if {getRisk(newSol) < getRisk(bestSol)} then | ▹ newSol improves bestSol |

| 28: bestSol ← newSol | |

| 29: end if | |

| 30: else{delta > 0 and delta ≤ credit} | ▹ acceptance criterion |

| 31: credit ← 0 | |

| 32: baseSol ← newSol | |

| 33: end if | |

| 34: update elapsedTime | |

| 35: end while | |

| 36: return bestSol | |

| end procedure | |

| Algorithm 2 Perturbation procedure to generate new ‘promising’ solutions. | |

| procedure perturbateSol(baseSol, inputs, beta) | |

| 1: newSol ← copySol(baseSol) | |

| ▹ 1. Remove a random number of randomly selected assets (destruction stage) | |

| 2: nAssetsInSol ← getNAssetsInSol(newSol) | |

| 3: if {nAssetsInSol > 1} then | |

| 4: nAssetsToRemove ← genRandomNumber(1, nAssetsInSol - 1) | |

| 5: for {i = 1 to nAssetsToRemove} do | |

| 6: asset ← selectRandomAsset(newSol) | |

| 7: newSol ← removeAsset(asset, newSol) | |

| 8: end for | |

| 9: end if | |

| ▹ 2. Randomly select one asset in current portf. to add several of its “friends” | |

| 10: asset ← getRandomAsset(newSol) | |

| ▹ 3. Use biased rand. to add friendly assets until reaching kMax (re-construction stage) | |

| 11: while {size(newSol) < getKMax(inputs)} do | |

| 12: listOfFriendlyAssets ← getFriendlyList(asset) | ▹ Sorted list of friendly assets |

| 13: do | ▹ Randomly select a position using a Geometric(beta) prob. distribution |

| 14: position ← biasedRandom(size(listOfFriendlyAssets), beta) | |

| 15: newAsset ← getAsset(listOfFriendlyAssets, position) | |

| 16: while {newAsset in newSol} | ▹ Repeat until newAsset not in current portf. |

| 17: newSol ← addAsset(newAsset, newSol) | |

| 18: asset ← newAsset | |

| 19: end while | |

| 20: return newSol | |

| end procedure | |

| Algorithm 3 Repair procedure to make newly generated solutions feasible. | |

| procedure repairSolution(sol, inputs) | |

| 1: unusedAssets ← getAssetsNotInSol(sol, inputs) | ▹ Consider assets not in portf. |

| 2: unusedAssets ← shuffle(unusedAssets) | ▹ Random sorting of the unused assets list |

| 3: assetA ← getRandomAsset(sol) | ▹ Select a random assetA in current portf. |

| 4: sol ← deleteAsset(assetA, sol) | ▹ Delete assetA from current portf. |

| 5: for {each asset assetB in unusedAssets} do | ▹ Search unused assetB with high return |

| 6: if {getReturn(assetB) ≥ minReturn} then | |

| 7: sol ← addAsset(assetB, sol) | ▹ Add assetB to current port. |

| 8: return sol | |

| 9: end if | |

| 10: end for | |

| 11: end procedure | |

5. Numerical Experiments

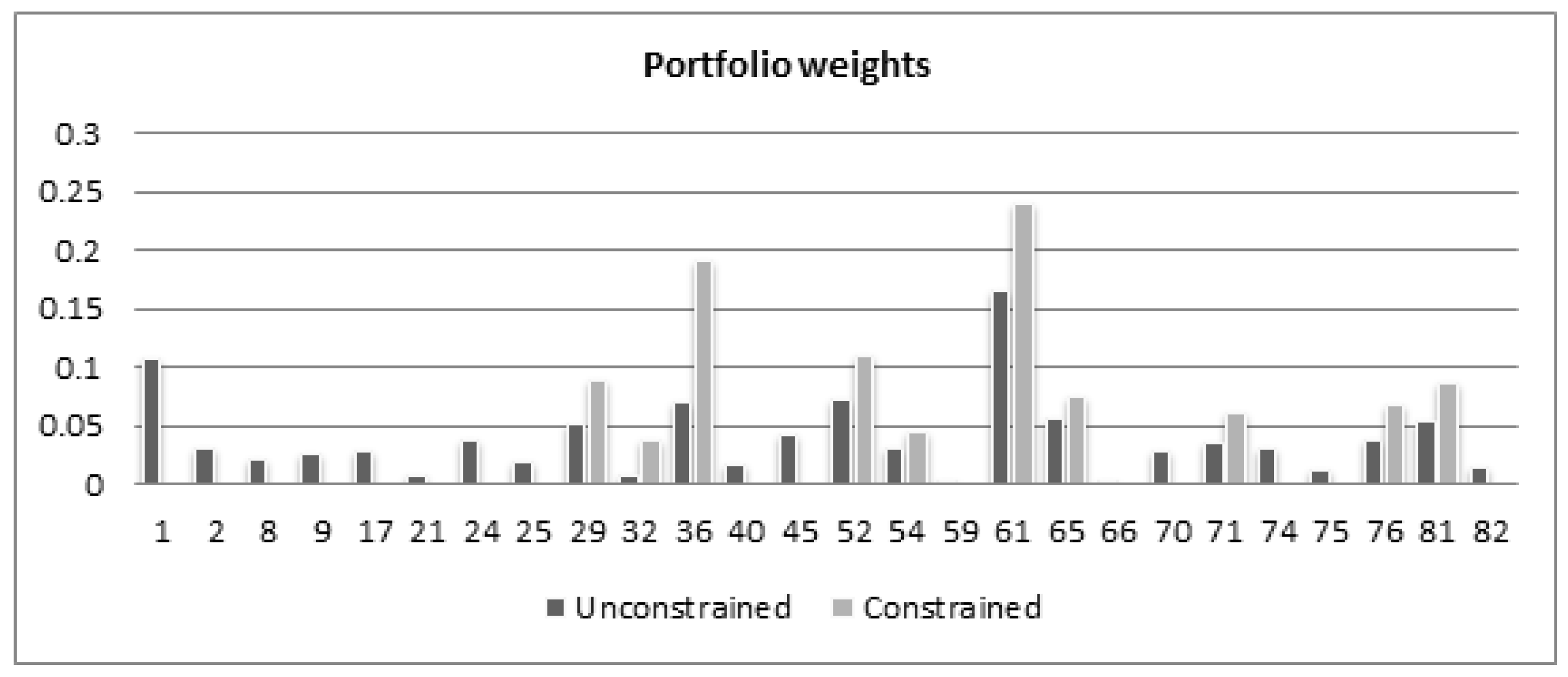

6. Discussion of Results

6.1. CEF-ARPO with Certain Inputs

6.2. CEF-ARPO with Uncertain Inputs

- Scenario 4 (S4): the minimum number of assets in the portfolio is increased from 1 to 2.

- Scenario 5 (S5): the maximum number of assets in the portfolio is decreased from 10 to 9.

- Scenario 6 (S6): Scenarios S4 and S5 are jointly considered.

- Scenario 7 (S7): the minimum quantity for all assets is increased from 0.01 to 0.015.

- Scenario 8 (S8): the maximum quantity for all assets is decreased from 1 to 0.995.

- Scenario 9 (S9): Scenarios S7 and S8 are jointly considered.

7. Conclusions

8. Future Work

Author Contributions

Funding

Conflicts of Interest

References

- Markowitz, H. Portfolio selection. J. Financ. 1952, 7, 77–91. [Google Scholar]

- Kolm, P.N.; Tütüncü, R.; Fabozzi, F.J. 60 Years of portfolio optimization: Practical challenges and current trends. Eur. J. Oper. Res. 2014, 234, 356–371. [Google Scholar] [CrossRef]

- Levy, M.; Ritov, Y. Mean–variance efficient portfolios with many assets: 50% short. Quant. Financ. 2011, 11, 1461–1471. [Google Scholar] [CrossRef]

- Leippold, M.; Trojani, F.; Vanini, P. Multiperiod mean-variance efficient portfolios with endogenous liabilities. Quant. Financ. 2011, 11, 1534–1546. [Google Scholar] [CrossRef]

- Vigna, E. On efficiency of mean–variance based portfolio selection in defined contribution pension schemes. Quant. Financ. 2014, 14, 237–258. [Google Scholar] [CrossRef]

- Fujii, M.; Takahashi, A. Making mean-variance hedging implementable in a partially observable market. Quant. Financ. 2014, 14, 1709–1724. [Google Scholar] [CrossRef] [Green Version]

- Zumbach, G. A mean/variance approach to long-term fixed-income portfolio allocation. Quant. Financ. 2013, 13, 1459–1471. [Google Scholar] [CrossRef]

- Maringer, D.G. Portfolio Management with Heuristic Optimization; Springer: Berlin, Germany, 2005. [Google Scholar]

- Sawik, B. Survey of multi-objective portfolio optimization by linear and mixed integer programming. In Applications of Management Science; Lawrence, K.D., Kleinman, G., Eds.; Emerald Group Publishing Limited: Bradford, UK, 2013; Volume 16, pp. 55–79. [Google Scholar]

- Bertsimas, D.; Pachamanova, D. Robust multiperiod portfolio management in the presence of transaction costs. Comput. Oper. Res. 2008, 35, 3–17. [Google Scholar] [CrossRef]

- Angelelli, E.; Mansini, R.; Speranza, M.G. A comparison of MAD and CVaR models with real features. J. Bank. Financ. 2007, 32, 1188–1197. [Google Scholar] [CrossRef]

- Perez, G.B.; Jones, D.F.; Tamiz, M.; Bilbao, T.A. An interactive three-stage model for mutual funds portfolio selection. Omega Int. J. Manag. Sci. 2007, 35, 75–88. [Google Scholar]

- Sawik, B. A Three Stage Lexicographic Approach for Multi-Criteria Portfolio Optimization by Mixed Integer Programming. Prz. Elektrotech. 2008, 84, 108–112. [Google Scholar]

- Sharpe, W.F. A linear programming algorithm for mutual fund portfolio selection. Manag. Sci. 1967, 13, 499–510. [Google Scholar] [CrossRef]

- Sharpe, W.F. A linear programming approximation for the general portfolio analysis problem. J. Financ. Quant. Anal. 1971, 6, 1263–1275. [Google Scholar] [CrossRef]

- Speranza, M.G. Linear programming models for portfolio optimization. Financ. Rev. l’Assoc. Fr. Finance 1993, 14, 107–123. [Google Scholar]

- Sawik, B. Downside risk approach for multi-objective portfolio optimization. In Operations Research Proceedings; Klatte, D., Luthi, H., Schmedders, K., Eds.; Springer: Berlin, Germany, 2012; pp. 191–196. [Google Scholar]

- Mansini, R.; Ogryczak, W.; Speranza, M.G. Twenty years of linear programming based portfolio optimization. Eur. J. Oper. Res. 2014, 234, 518–535. [Google Scholar] [CrossRef]

- Pae, Y.; Sabbaghi, N. Log-robust portfolio management after transaction costs. OR Spectr. 2014, 36, 95–112. [Google Scholar] [CrossRef]

- Bruni, R.; Cesarone, F.; Scozzari, A.; Tardella, F. A linear risk-return model for enhanced indexation in portfolio optimization. OR Spectr. 2015, 37, 735–759. [Google Scholar] [CrossRef]

- Wolfe, P. The simplex method for quadratic programming. Econometrica 1959, 27, 382–398. [Google Scholar] [CrossRef]

- Pachamanova, D.A.; Fabozzi, F.J. Simulation and Optimization in Finance; John Wiley and Sons: Hoboken, NJ, USA, 2010. [Google Scholar]

- Sawik, B. Bi-criteria portfolio optimization models with percentile and symmetric risk measures by mathematical programming. Prz. Elektrotech. 2012, 88, 176–180. [Google Scholar]

- Pınar, M.Ç. Robust scenario optimization based on downside-risk measure for multi-period portfolio selection. OR Spectr. 2007, 29, 295–309. [Google Scholar] [CrossRef]

- Ólafsson, S. Chapter 21 Metaheuristics. In Handbooks in Operations Research and Management Science 13; Elsevier: Amsterdam, The Netherlands, 2006; pp. 633–654. [Google Scholar]

- Jourdan, L.; Basseur, M.; Talbi, E.G. Hybridizing exact methods and metaheuristics: A taxonomy. Eur. J. Oper. Res. 2009, 199, 620–629. [Google Scholar] [CrossRef]

- Blum, C.; Puchinger, J.; Raidl, G.R.; Roli, A. Hybrid metaheuristics in combinatorial optimization: A survey. Appl. Soft Comput. 2011, 11, 4135–4151. [Google Scholar] [CrossRef] [Green Version]

- Boussaïd, I.; Lepagnot, J.; Siarry, P. A survey on optimization metaheuristics. Inf. Sci. 2013, 237, 82–117. [Google Scholar] [CrossRef]

- Tobin, J. Liquidity preference as behavior towards risk. Rev. Econ. Stud. 1958, 25, 65–86. [Google Scholar] [CrossRef]

- Tobin, J. The theory of portfolio selection. In The Theory of Interest Rates; Hahn, F., Brechling, F., Eds.; Macmillan & Co. Ltd.: London, UK, 1965; pp. 3–51. [Google Scholar]

- Bienstock, D. Computational study of a family of mixed-integer quadratic programming problems. Math. Program. 1996, 74, 121–140. [Google Scholar] [CrossRef] [Green Version]

- Chang, T.J.; Meade, N.; Beasley, J.E.; Sharaiha, Y.M. Heuristics for cardinality constrained portfolio optimisation. Comput. Oper. Res. 2000, 27, 1271–1302. [Google Scholar] [CrossRef]

- Jobst, N.J.; Horniman, M.D.; Lucas, C.A.; Mitra, G. Computational aspects of alternative portfolio selection models in the presence of discrete asset choice constraints. Quant. Financ. 2001, 1, 489–501. [Google Scholar] [CrossRef] [Green Version]

- Lourenço, H.; Martin, O.; Stützle, T. Iterated local search: Framework and applications. In Handbook of Metaheuristics; Gendreau, M., Potvin, J.Y., Eds.; International Series in Operations Research & Management Science; Springer: New York, NY, USA, 2010; Volume 146, pp. 363–397. [Google Scholar]

- Ferrer, A.; Guimarans, D.; Ramalhinho, H.; Juan, A.A. A BRILS metaheuristic for non-smooth flow-shop problems with failure-risk costs. Expert Syst. Appl. 2016, 44, 177–186. [Google Scholar] [CrossRef]

- Grasas, A.; Juan, A.A.; Faulin, J.; de Armas, J.; Ramalhinho, H. Biased randomization of heuristics using skewed probability distributions: A survey and some applications. Comput. Ind. Eng. 2017, 110, 216–228. [Google Scholar] [CrossRef]

- Dominguez, O.; Guimarans, D.; Juan, A.A.; de la Nuez, I. A biased-randomised large neighbourhood search for the two-dimensional vehicle routing problem with backhauls. Eur. J. Oper. Res. 2016, 255, 442–462. [Google Scholar] [CrossRef]

- Gonzalez-Neira, E.M.; Ferone, D.; Hatami, S.; Juan, A.A. A biased-randomized simheuristic for the distributed assembly permutation flowshop problem with stochastic processing times. Simul. Model. Pract. Theory 2017, 79, 23–36. [Google Scholar] [CrossRef]

- Schaerf, A. Local search techniques for constrained portfolio selection problems. Comput. Econ. 2002, 20, 177–190. [Google Scholar] [CrossRef]

- Moral-Escudero, R.; Ruiz-Torrubiano, R.; Suárez, A. Selection of optimal investment portfolios with cardinality constraints. In Proceedings of the IEEE Congress on Evolutionary Computation, Vancouver, BC, Canada, 16–21 July 2006; IEEE Press: New York, NY, USA, 2006; pp. 2382–2388. [Google Scholar]

- Di Gaspero, L.; Tollo, G.D.; Roli, A.; Schaerf, A. Hybrid metaheuristics for constrained portfolio selection problems. Quant. Financ. 2011, 11, 1473–1487. [Google Scholar] [CrossRef]

- Michaud, R.O. The Markowitz optimization enigma: Is ‘optimized’ optimal? Financ. Anal. J. 1989, 45, 31–42. [Google Scholar] [CrossRef]

- Kallberg, J.G.; Ziemba, W.T. Mis-specifications in portfolio selection problems. In Risk and Capital; Springer-Verlag: New York, NY, USA, 1984; pp. 74–87. [Google Scholar]

- DeMiguel, V.; Garlappi, L.; Uppal, R. Optimal versus naïve diversification: How inefficient is the 1/N portfolio strategy? Rev. Financ. Stud. 2009, 22, 1915–1953. [Google Scholar] [CrossRef]

- Jorion, P. International portfolio diversification with estimation risk. J. Bus. 1985, 58, 259–278. [Google Scholar] [CrossRef]

- Maringer, D.G.; Kellerer, H. Optimization of cardinality constrained portfolios with a hybrid local search algorithm. OR Spectr. 2003, 25, 481–495. [Google Scholar] [CrossRef]

- Baule, R. Optimal portfolio selection for the small investor considering risk and transaction costs. OR Spectr. 2010, 32, 61–76. [Google Scholar] [CrossRef]

- Blume, M.E.; Friend, I. The asset structure of individual portfolios and some implications for utility functions. J. Financ. 1975, 30, 585–603. [Google Scholar] [CrossRef]

- Guiso, L.; Jappelli, T.; Terlizzese, D. Income risk, borrowing constraints, and portfolio choice. Am. Econ. Rev. 1996, 86, 158–172. [Google Scholar]

- Jansen, R.; van Dijk, R. Optimal benchmark tracking with small portfolios. J. Portf. Manag. 2002, 28, 9–22. [Google Scholar] [CrossRef]

- Evans, J.L.; Archer, S.H. Diversification and the reduction of dispersion: An empirical analysis. J. Financ. 1968, 23, 761–767. [Google Scholar]

- Lloyd, W.P.; Hand, J.H.; Modani, N.K. The effect of portfolio construction rules on the relationship between portfolio size and effective diversification. J. Financ. Res. 1981, 4, 183–193. [Google Scholar] [CrossRef]

- Nawrocki, D.N. Portfolio Optimization, Heuristics and the ‘Butterfly Effect’. J. Financ. Plan.-Denver 2000, 13, 68–75. [Google Scholar]

- Elton, E.J.; Gruber, M.J.; Padberg, M.W. Simple criteria for optimal portfolio selection. J. Financ. 1976, 31, 1341–1357. [Google Scholar] [CrossRef]

- Nawrocki, D.N. A comparison of risk measures when used in a simple portfolio selection heuristic. J. Bus. Financ. Account. 1983, 10, 183–194. [Google Scholar] [CrossRef]

- Crama, Y.; Schyns, M. Simulated annealing for complex portfolio selection problems. Eur. J. Oper. Res. 2003, 150, 546–571. [Google Scholar] [CrossRef] [Green Version]

- Derigs, U.; Nickel, N.H. Meta-heuristic based decision support for portfolio optimization with a case study on tracking error minimization in passive portfolio management. OR Spectr. 2003, 25, 345–378. [Google Scholar]

- Armañanzas, R.; Lozano, J.A. A multiobjective approach to the portfolio optimization problem. In Proceedings of the IEEE Congress on Evolutionary Computation, Edinburgh, UK, 2–4 September 2005; IEEE Press: New York, NY, USA, 2005; Volume 2, pp. 1388–1395. [Google Scholar]

- Fernández, A.; Gómez, S. Portfolio selection using neural networks. Comput. Oper. Res. 2007, 34, 1177–1191. [Google Scholar] [CrossRef] [Green Version]

- Rundo, F.; Trenta, F.; di Stallo, A.L.; Battiato, S. Grid trading system robot (GTSbot): A novel mathematical algorithm for trading FX market. Appl. Sci. 2019, 9, 1796. [Google Scholar] [CrossRef]

- Hu, Y.J.; Lin, S.J. Deep reinforcement learning for optimizing finance portfolio management. In Proceedings of the 2019 Amity International Conference on Artificial Intelligence (AICAI), Dubai, United Arab Emirates, 4–6 February 2019; IEEE Press: New York, NY, USA, 2019; pp. 14–20. [Google Scholar]

- Zhang, W.; Zhou, C. Deep learning algorithm to solve portfolio management with proportional transaction cost. In Proceedings of the 2019 IEEE Conference on Computational Intelligence for Financial Engineering & Economics (CIFEr), Shenzhen, China, 4–5 May 2019; IEEE Press: New York, NY, USA, 2019; pp. 1–10. [Google Scholar]

- Calvet, L.; de Armas, J.; Masip, D.; Juan, A.A. Learnheuristics: Hybridizing metaheuristics with machine learning for optimization with dynamic inputs. Open Math. 2017, 15, 261–280. [Google Scholar] [CrossRef]

- Di Tollo, G.; Roli, A. Metaheuristics for the portfolio selection problem. Int. J. Oper. Res. 2008, 5, 13–35. [Google Scholar]

- Jain, A.; Jain, P.K.; McInish, T.H.; McKenzie, M. Worldwide reach of short selling regulations. J. Financ. Econ. 2013, 109, 177–197. [Google Scholar] [CrossRef]

- Juan, A.A.; Faulin, J.; Ruiz, R.; Barrios, B.; Caballé, S. The SR-GCWS hybrid algorithm for solving the capacitated vehicle routing problem. Appl. Soft Comput. 2010, 10, 215–224. [Google Scholar] [CrossRef]

- Juan, A.A.; Faulin, J.; Jorba, J.; Riera, D.; Masip, D.; Barrios, B. On the use of Monte Carlo simulation, cache and splitting techniques to improve the Clarke and Wright savings heuristics. J. Oper. Res. Soc. 2011, 62, 1085–1097. [Google Scholar] [CrossRef]

- Burke, E.; Curtois, T.; Hyde, M.; Kendall, G.; Ochoa, G.; Petrovic, S.; Vázquez-Rodríguez, J.A.; Gendreau, M. Iterated local search vs. hyper-heuristics: Towards general-purpose search algorithms. In Proceedings of the IEEE Congress on Evolutionary Computation, Barcelona, Spain, 18–23 July 2010; IEEE Press: New York, NY, USA, 2010; pp. 3073–3080. [Google Scholar]

- Nouraniy, Y.; Andresen, B. A comparison of simulated annealing cooling strategies. J. Phys. A Math. Gen. 1998, 31, 8373–8385. [Google Scholar] [CrossRef]

- Sawik, T. Selection of supply portfolio under disruption risks. Omega Int. J. Manag. Sci. 2011, 39, 194–208. [Google Scholar] [CrossRef]

- Sawik, T. Selection of resilient supply portfolio under disruption risks. Omega Int. J. Manag. Sci. 2013, 41, 259–269. [Google Scholar] [CrossRef]

- Heckmann, I.; Comes, T.; Nickel, S. A critical review on supply chain risk—Definition, measure and modeling. Omega Int. J. Manag. Sci. 2015, 52, 119–132. [Google Scholar] [CrossRef]

- Cai, X.; Rajasekaran, S.; Zhang, F. Efficient Approximate Algorithms for the Closest Pair Problem in High Dimensional Spaces. In Advances in Knowledge Discovery and Data Mining, Proceedings of the Pacific-Asia Conference on Knowledge Discovery and Data Mining PAKDD 2018: Advances in Knowledge Discovery and Data Mining, Melbourne, VIC, Australia, 3–6 June 2018; Phung, D., Tseng, V., Webb, G., Ho, B., Ganji, M., Rashidi, L., Eds.; Lecture Notes in Computer Science; Springer: Cham, Switzerland, 2018; Volume 10939, pp. 151–163. [Google Scholar]

{kind=link}

{kind=link}

| Instance | Di Gaspero et al. [41] | Moral-Escudero et al. [40] | Schaerf [39] | ARPO | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| FD + QP | SD + QP | GA + QP | TS | LS + QP | ||||||

| APL | T(s) | APL | T(s) | APL | T(s) | APL | T(s) | APL | T(Std) (s) | |

| HS | 0.00366 | 1.5 | 0.00321 | 3.1 | 0.00321 | 415.1 | 0.00409 | 251 | 0.00399 | 2.0 (0.87) |

| DAX 100 | 2.66104 | 9.6 | 2.53139 | 14.1 | 2.53180 | 552.7 | 2.53617 | 531 | 2.45403 | 1.0 (1.0) |

| FTSE 100 | 2.00146 | 10.1 | 1.92146 | 16.1 | 1.92150 | 886.3 | 1.92597 | 583 | 1.88340 | 13.7 (9.28) |

| S&P 100 | 4.77157 | 11.2 | 4.69371 | 18.8 | 4.69507 | 1163.7 | 4.69507 | 713 | 4.65095 | 15.5 (8.42) |

| NIKKEI 225 | 0.24176 | 25.3 | 0.20219 | 45.9 | 0.20198 | 1465.8 | 0.20198 | 1603 | 0.20189 | 5.0 (17.20) |

| Curve Position | Required Return | UEF-Variance | ARPO-Variance | APL | Time (s) |

|---|---|---|---|---|---|

| 20 | 0.002861137 | 0.0006424068 | 0.0006424114 | 0.0007160572 | 4.212 |

| 40 | 0.002941981 | 0.0006428092 | 0.0006429074 | 0.0152766949 | 2.74 |

| 60 | 0.003022827 | 0.0006434196 | 0.0006437456 | 0.0506667811 | 1.978 |

| 80 | 0.003103671 | 0.0006442382 | 0.0006443922 | 0.0239042019 | 3.759 |

| 100 | 0.003184516 | 0.0006452648 | 0.0006454721 | 0.0321263456 | 1.226 |

| 120 | 0.003265361 | 0.0006464996 | 0.0006467783 | 0.0431090754 | 1.917 |

| 140 | 0.003346206 | 0.0006479424 | 0.0006483109 | 0.0568723393 | 2.012 |

| 160 | 0.003427051 | 0.0006495933 | 0.0006499731 | 0.0584673518 | 2.686 |

| 180 | 0.003507896 | 0.0006514524 | 0.0006516646 | 0.0325733699 | 1.491 |

| 200 | 0.003588740 | 0.0006535208 | 0.0006536148 | 0.0143836279 | 4.464 |

| 1820 | 0.010137479 | 0.0035773525 | 0.0035773526 | 0.0000027954 | 0.004 |

| 1840 | 0.010218315 | 0.0036907539 | 0.0036907539 | 0.0000000000 | 0.009 |

| 1860 | 0.010299151 | 0.0038090873 | 0.0038090873 | 0.0000000000 | 0.001 |

| 1880 | 0.010379986 | 0.0039323522 | 0.0039323522 | 0.0000000000 | 0.009 |

| 1900 | 0.010460822 | 0.0040605480 | 0.0040605480 | 0.0000000000 | 0.001 |

| 1920 | 0.010541657 | 0.0041936758 | 0.0041936758 | 0.0000000000 | 0.003 |

| 1940 | 0.010622493 | 0.0043317350 | 0.0043317350 | 0.0000000000 | 0.010 |

| 1960 | 0.010703329 | 0.0044747255 | 0.0044747255 | 0.0000000000 | 0.001 |

| 1980 | 0.010784164 | 0.0046226475 | 0.0046226476 | 0.0000021633 | 0.003 |

| 2000 | 0.010865000 | 0.0047755010 | 0.0047755010 | 0.0000000000 | 0 |

| Curve Position | Required Return | UEF-Variance | ARPO-Variance | APL | Time (s) |

|---|---|---|---|---|---|

| 20 | 0.002175078 | 0.0001368925 | 0.0001481318 | 0.0821031101 | 1.5320 |

| 40 | 0.002252039 | 0.0001370119 | 0.0001483250 | 0.0825702001 | 0.2180 |

| 60 | 0.002329001 | 0.0001372175 | 0.0001484472 | 0.0818386868 | 0.3910 |

| 80 | 0.002405963 | 0.0001375210 | 0.0001485474 | 0.0801797544 | 0.8330 |

| 100 | 0.002482925 | 0.0001379123 | 0.0001486181 | 0.0776275938 | 1.8510 |

| 120 | 0.002559887 | 0.0001383842 | 0.0001487104 | 0.0746197904 | 0.8630 |

| 140 | 0.002636849 | 0.0001389376 | 0.0001490367 | 0.0726880269 | 0.5330 |

| 160 | 0.00271381 | 0.0001395866 | 0.0001495985 | 0.0717253662 | 0.5620 |

| 180 | 0.002790771 | 0.0001403353 | 0.0001503958 | 0.0716890191 | 0.9450 |

| 200 | 0.002867732 | 0.0001411837 | 0.0001514287 | 0.0725650341 | 1.2600 |

| 1820 | 0.009101412 | 0.0008965075 | 0.0008965075 | 0.0000000000 | 0.0000 |

| 1840 | 0.009178374 | 0.0009614987 | 0.0009614987 | 0.0000000000 | 0.0000 |

| 1860 | 0.009255336 | 0.0010349696 | 0.0010351065 | 0.0001322744 | 0.0000 |

| 1880 | 0.009332288 | 0.0011354764 | 0.0011354764 | 0.0000000000 | 0.0000 |

| 1900 | 0.009409241 | 0.0012881113 | 0.0012881113 | 0.0000000000 | 0.0000 |

| 1920 | 0.009486192 | 0.0014930083 | 0.0014930083 | 0.0000000000 | 0.0000 |

| 1940 | 0.009563145 | 0.0017501725 | 0.0017501725 | 0.0000000000 | 0.0000 |

| 1960 | 0.009640096 | 0.0020595971 | 0.0020595971 | 0.0000000000 | 0.0000 |

| 1980 | 0.009717049 | 0.0024212903 | 0.0024212904 | 0.0000000413 | 0.0000 |

| 2000 | 0.009794000 | 0.0028352430 | 0.0028352430 | 0.0000000000 | 0.0000 |

| Curve Position | Required Return | UEF-Variance | ARPO-Variance | APL | Time (s) |

|---|---|---|---|---|---|

| 20 | 0.002420865 | 0.0001985238 | 0.0002060320 | 0.037820 | 24.1290 |

| 40 | 0.002479328 | 0.0001986154 | 0.0002061982 | 0.038178 | 4.7360 |

| 60 | 0.002537792 | 0.0001987642 | 0.0002065801 | 0.039322 | 21.8640 |

| 80 | 0.002596256 | 0.0001989714 | 0.0002066068 | 0.038374 | 16.4550 |

| 100 | 0.00265472 | 0.0001992442 | 0.0002068282 | 0.038064 | 25.5930 |

| 120 | 0.002713184 | 0.0001995842 | 0.0002073013 | 0.038666 | 13.9090 |

| 140 | 0.002771647 | 0.0001999959 | 0.0002080261 | 0.040152 | 26.5100 |

| 160 | 0.002830111 | 0.0002004890 | 0.0002084997 | 0.039956 | 18.1160 |

| 180 | 0.002888575 | 0.0002010665 | 0.0002089129 | 0.039024 | 15.0670 |

| 200 | 0.002947039 | 0.0002017309 | 0.0002095566 | 0.038793 | 17.4660 |

| 1820 | 0.007682888 | 0.0010170776 | 0.0010170776 | 0.000000 | 1.3320 |

| 1840 | 0.007741359 | 0.0010578347 | 0.0010581058 | 0.000256 | 0.5650 |

| 1860 | 0.00779983 | 0.0011002537 | 0.0011003206 | 0.000061 | 11.5260 |

| 1880 | 0.007858284 | 0.0011455465 | 0.0011455466 | 0.000000 | 13.3580 |

| 1900 | 0.007916738 | 0.0011954685 | 0.0011954685 | 0.000000 | 3.9120 |

| 1920 | 0.007975191 | 0.0012500871 | 0.0012500871 | 0.000000 | 28.7840 |

| 1940 | 0.008033645 | 0.0013094021 | 0.0013094021 | 0.000000 | 27.6720 |

| 1960 | 0.008092098 | 0.0013734126 | 0.0013734126 | 0.000000 | 26.4330 |

| 1980 | 0.008150551 | 0.0014421206 | 0.0014423115 | 0.000132 | 19.7400 |

| 2000 | 0.008209000 | 0.0015166351 | 0.0015166351 | 0.000000 | 0.0000 |

| Curve Position | Required Return | UEF-Variance | ARPO-Variance | APL | Time (s) |

|---|---|---|---|---|---|

| 20 | 0.002005874 | 0.0001214699 | 0.000134226 | 0.105014 | 19.1900 |

| 40 | 0.002078497 | 0.0001216461 | 0.000134619 | 0.106648 | 26.0990 |

| 60 | 0.002151121 | 0.0001219398 | 0.000135389 | 0.110297 | 20.5970 |

| 80 | 0.002223742 | 0.0001223689 | 0.000136242 | 0.113373 | 17.2350 |

| 100 | 0.002296365 | 0.0001229290 | 0.000137073 | 0.115057 | 22.1810 |

| 120 | 0.002368987 | 0.0001236105 | 0.000138075 | 0.117013 | 23.3780 |

| 140 | 0.00244161 | 0.0001244126 | 0.000139442 | 0.120799 | 22.3860 |

| 160 | 0.002514232 | 0.0001253355 | 0.000140429 | 0.120421 | 19.7720 |

| 180 | 0.002586853 | 0.0001263852 | 0.000141311 | 0.118098 | 26.2040 |

| 200 | 0.002659475 | 0.0001275649 | 0.000142711 | 0.118735 | 16.2610 |

| 1820 | 0.008541599 | 0.0012695539 | 0.001269554 | 0.000000 | 0.6500 |

| 1840 | 0.008614195 | 0.0013438638 | 0.001343864 | 0.000000 | 0.3990 |

| 1860 | 0.008686789 | 0.0014260901 | 0.00142609 | 0.000000 | 2.2590 |

| 1880 | 0.008759385 | 0.0015162347 | 0.001516235 | 0.000000 | 0.1940 |

| 1900 | 0.008831981 | 0.0016142967 | 0.001614297 | 0.000000 | 14.5950 |

| 1920 | 0.008904579 | 0.0017205530 | 0.001720553 | 0.000000 | 0.1340 |

| 1940 | 0.008977215 | 0.0018772540 | 0.001877254 | 0.000000 | 19.9680 |

| 1960 | 0.009049852 | 0.0021147413 | 0.002114741 | 0.000000 | 22.3300 |

| 1980 | 0.009122459 | 0.0024387539 | 0.002438754 | 0.000000 | 0.0070 |

| 2000 | 0.009195000 | 0.0029387241 | 0.002938724 | 0.000000 | 0.0000 |

| Curve Position | Required Return | UEF-Variance | ARPO-Variance | APL | Time (s) |

|---|---|---|---|---|---|

| 20 | 0.0001078963 | 0.0003046821 | 0.0003048207 | 0.000455 | 0.0340 |

| 40 | 0.0001469218 | 0.0003048095 | 0.0003049299 | 0.000395 | 0.0820 |

| 60 | 0.0001859471 | 0.0003050116 | 0.0003051331 | 0.000398 | 0.0850 |

| 80 | 0.0002249721 | 0.0003052881 | 0.0003054303 | 0.000466 | 0.0660 |

| 100 | 0.0002639974 | 0.0003056390 | 0.0003058216 | 0.000597 | 0.1000 |

| 120 | 0.0003030223 | 0.0003060641 | 0.0003063069 | 0.000793 | 0.1930 |

| 140 | 0.0003420475 | 0.0003065635 | 0.0003068863 | 0.001053 | 0.1930 |

| 160 | 0.0003810730 | 0.0003071384 | 0.0003075597 | 0.001372 | 0.0540 |

| 180 | 0.0004200985 | 0.0003077930 | 0.0003083271 | 0.001735 | 0.1150 |

| 200 | 0.0004591229 | 0.0003085244 | 0.0003091886 | 0.002153 | 0.0400 |

| 1820 | 0.0036202364 | 0.0007178707 | 0.0007178707 | 0.000000 | 0.0320 |

| 1840 | 0.0036592244 | 0.0007585282 | 0.0007585282 | 0.000000 | 0.0210 |

| 1860 | 0.0036982126 | 0.0008065920 | 0.0008065920 | 0.000000 | 0.0520 |

| 1880 | 0.0037372032 | 0.0008621079 | 0.0008621079 | 0.000000 | 60.6030 |

| 1900 | 0.0037762020 | 0.0009261274 | 0.0009261274 | 0.000000 | 0.0050 |

| 1920 | 0.0038152008 | 0.0009990847 | 0.0009990847 | 0.000000 | 0.0050 |

| 1940 | 0.0038541986 | 0.0010809831 | 0.0010809831 | 0.000000 | 85.8630 |

| 1960 | 0.0038931362 | 0.0011966840 | 0.0011966841 | 0.000000 | 0.0010 |

| 1980 | 0.0039320680 | 0.0013855561 | 0.0013855562 | 0.000000 | 0.0010 |

| 2000 | 0.0039710000 | 0.0016485224 | 0.0016485224 | 0.000000 | 0.0000 |

| Curve Position | Required Return | ARPO—Variance S0 | ARPO—Variance S1 | APL S1—S0 | Time (s) | ARPO—Variance S2 | APL S2—S0 | Time (s) | ARPO—Variance S3 | APL S3—S0 | Time (s) |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 20 | 0.002861137 | 0.000642411 | 0.000642777 | 0.057% | 0.848 | 0.000643991 | 0.246% | 0.194 | 0.000644237 | 0.284% | 1.991 |

| 40 | 0.002941981 | 0.000642907 | 0.000643518 | 0.095% | 0.686 | 0.000644294 | 0.216% | 0.133 | 0.000644828 | 0.299% | 0.182 |

| 60 | 0.003022827 | 0.000643746 | 0.000644209 | 0.072% | 0.227 | 0.000644951 | 0.187% | 0.061 | 0.000645441 | 0.263% | 0.105 |

| 80 | 0.003103671 | 0.000644392 | 0.000645228 | 0.130% | 0.102 | 0.000645594 | 0.186% | 0.324 | 0.000646286 | 0.294% | 0.030 |

| 100 | 0.003184516 | 0.000645472 | 0.000646467 | 0.154% | 0.189 | 0.00064646 | 0.153% | 0.154 | 0.000647432 | 0.304% | 0.072 |

| 120 | 0.003265361 | 0.000646778 | 0.000647925 | 0.177% | 0.026 | 0.000647665 | 0.137% | 1.397 | 0.000648805 | 0.313% | 0.035 |

| 140 | 0.003346206 | 0.000648311 | 0.000649556 | 0.192% | 0.111 | 0.000649104 | 0.122% | 0.224 | 0.000650406 | 0.323% | 0.140 |

| 160 | 0.003427051 | 0.000649973 | 0.000651174 | 0.185% | 0.413 | 0.000650778 | 0.124% | 0.025 | 0.000652234 | 0.348% | 0.050 |

| 180 | 0.003507896 | 0.000651665 | 0.000653049 | 0.212% | 0.071 | 0.000652687 | 0.157% | 0.249 | 0.000654075 | 0.370% | 0.143 |

| 200 | 0.00358874 | 0.000653615 | 0.000655182 | 0.240% | 0.228 | 0.000654567 | 0.146% | 0.043 | 0.000655994 | 0.364% | 0.369 |

| 1820 | 0.010137479 | 0.003577353 | 0.003846626 | 7.527% | 0.000 | 0.003553484 | −0.667% | 0.003 | 0.00382672 | 6.971% | 0.006 |

| 1840 | 0.010218315 | 0.003690754 | 0.003973414 | 7.659% | 0.003 | 0.003668539 | −0.602% | 0.003 | 0.003955413 | 7.171% | 0.005 |

| 1860 | 0.010299151 | 0.003809087 | 0.00410529 | 7.776% | 0.001 | 0.003788622 | −0.537% | 0.000 | 0.004089294 | 7.356% | 0.000 |

| 1880 | 0.010379986 | 0.003932352 | 0.004242251 | 7.881% | 0.000 | 0.003913731 | −0.474% | 0.002 | 0.004228359 | 7.527% | 0.000 |

| 1900 | 0.010460822 | 0.004060548 | 0.004384302 | 7.973% | 0.019 | 0.00404387 | −0.411% | 0.004 | 0.004372613 | 7.685% | 0.003 |

| 1920 | 0.010541657 | 0.004193676 | 0.004531439 | 8.054% | 0.008 | 0.004179034 | −0.349% | 0.001 | 0.004522052 | 7.830% | 0.001 |

| 1940 | 0.010622493 | 0.004331735 | 0.004683665 | 8.124% | 0.002 | 0.004319228 | −0.289% | 0.003 | 0.004676680 | 7.963% | 0.000 |

| 1960 | 0.010703329 | 0.004474726 | NF | 0.00446445 | −0.230% | 0.000 | NF | ||||

| 1980 | 0.010784164 | 0.004622648 | NF | 0.004614697 | −0.172% | 0.004 | NF | ||||

| 2000 | 0.010865 | 0.004775501 | NF | 0.004769974 | −0.116% | 0.000 | NF |

| Curve Position | Required Return | ARPO—Variance S0 | ARPO—Variance S4 | APL S4-S0 | Time (s) | ARPO—Variance S5 | APL S5—S0 | Time (s) | ARPO—Variance S6 | APL S6—S0 | Time (s) |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 20 | 0.002861137 | 0.000642411 | 0.000642411 | 0.000% | 1.446 | 0.00064252 | 0.017% | 0.557 | 0.00064252 | 0.017% | 0.254 |

| 40 | 0.002941981 | 0.000642907 | 0.000642907 | 0.000% | 0.118 | 0.000643026 | 0.019% | 0.368 | 0.000643026 | 0.019% | 0.391 |

| 60 | 0.003022827 | 0.000643746 | 0.000643746 | 0.000% | 0.127 | 0.000643875 | 0.020% | 0.527 | 0.000643875 | 0.020% | 0.256 |

| 80 | 0.003103671 | 0.000644392 | 0.000644392 | 0.000% | 0.365 | 0.000645066 | 0.105% | 0.185 | 0.000645066 | 0.105% | 0.090 |

| 100 | 0.003184516 | 0.000645472 | 0.000645472 | 0.000% | 0.338 | 0.0006466 | 0.175% | 0.191 | 0.0006466 | 0.175% | 0.285 |

| 120 | 0.003265361 | 0.000646778 | 0.000646778 | 0.000% | 0.012 | 0.000647619 | 0.130% | 0.803 | 0.000647619 | 0.130% | 0.058 |

| 140 | 0.003346206 | 0.000648311 | 0.000648311 | 0.000% | 0.101 | 0.000648891 | 0.089% | 0.171 | 0.000648891 | 0.089% | 0.138 |

| 160 | 0.003427051 | 0.000649973 | 0.000649973 | 0.000% | 0.168 | 0.000650437 | 0.071% | 0.123 | 0.000650437 | 0.071% | 0.020 |

| 180 | 0.003507896 | 0.000651665 | 0.000651665 | 0.000% | 0.589 | 0.000652259 | 0.091% | 0.408 | 0.000652259 | 0.091% | 0.131 |

| 200 | 0.00358874 | 0.000653615 | 0.000653615 | 0.000% | 0.089 | 0.000654354 | 0.113% | 0.141 | 0.000654354 | 0.113% | 0.093 |

| 1820 | 0.010137479 | 0.003577353 | 0.003577352 | 0.000% | 0.002 | 0.003577352 | 0.000% | 0.000 | 0.003577352 | 0.000% | 1.847 |

| 1840 | 0.010218315 | 0.003690754 | 0.003690754 | 0.000% | 4.421 | 0.003690754 | 0.000% | 0.002 | 0.003690754 | 0.000% | 3.000 |

| 1860 | 0.010299151 | 0.003809087 | 0.003809088 | 0.000% | 1.707 | 0.003809088 | 0.000% | 0.002 | 0.003809088 | 0.000% | 2.188 |

| 1880 | 0.010379986 | 0.003932352 | 0.003932352 | 0.000% | 1.766 | 0.003932352 | 0.000% | 0.001 | 0.003932352 | 0.000% | 0.743 |

| 1900 | 0.010460822 | 0.004060548 | 0.004060549 | 0.000% | 2.067 | 0.004060549 | 0.000% | 0.002 | 0.004060549 | 0.000% | 0.118 |

| 1920 | 0.010541657 | 0.004193676 | 0.004193675 | 0.000% | 0.987 | 0.004193675 | 0.000% | 0.048 | 0.004193675 | 0.000% | 0.507 |

| 1940 | 0.010622493 | 0.004331735 | 0.004331735 | 0.000% | 14.906 | 0.004331735 | 0.000% | 0.001 | 0.004331735 | 0.000% | 0.685 |

| 1960 | 0.010703329 | 0.004474726 | 0.004474726 | 0.000% | 0.000 | 0.004474726 | 0.000% | 0.000 | 0.004474726 | 0.000% | 0.000 |

| 1980 | 0.010784164 | 0.004622648 | 0.004622647 | 0.000% | 0.000 | 0.004622647 | 0.000% | 0.001 | 0.004622647 | 0.000% | 0.000 |

| 2000 | 0.010865 | 0.004775501 | 0.004775501 | 0.000% | 0.000 | 0.004775501 | 0.000% | 0.000 | 0.004775501 | 0.000% | 0.000 |

| Scenario | Average APL | Non Feasible Portfolios | Time (s) |

|---|---|---|---|

| Scenario 1 | 3.324% | 3 | 0.173 |

| Scenario 2 | −0.109% | 0 | 0.141 |

| Scenario 3 | 3.274% | 3 | 0.196 |

| Scenario 4 | 0.000% | 0 | 1.460 |

| Scenario 5 | 0.042% | 0 | 0.177 |

| Scenario 6 | 0.042% | 0 | 0.540 |

| Scenario 7 | 0.013% | 0 | 0.256 |

| Scenario 8 | 0.000% | 0 | 0.192 |

| Scenario 9 | 0.013% | 0 | 0.070 |

| Curve Position | Required Return | ARPO—Variance S0 | ARPO—Variance S7 | APL S7—S0 | Time (s) | ARPO—Variance S8 | APL S8—S0 | Time (s) | ARPO—Variance S9 | APL S9—S0 | Time (s) |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 20 | 0.002861137 | 0.000642411 | 0.00064252 | 0.017% | 0.953 | 0.000642411 | 0.000% | 0.701 | 0.00064252 | 0.017% | 0.174 |

| 40 | 0.002941981 | 0.000642907 | 0.000643026 | 0.019% | 0.962 | 0.000642907 | 0.000% | 0.387 | 0.000643026 | 0.019% | 0.094 |

| 60 | 0.003022827 | 0.000643746 | 0.000643875 | 0.020% | 0.087 | 0.000643746 | 0.000% | 0.789 | 0.000643875 | 0.020% | 0.229 |

| 80 | 0.003103671 | 0.000644392 | 0.000645066 | 0.105% | 0.073 | 0.000644392 | 0.000% | 0.144 | 0.000645066 | 0.105% | 0.424 |

| 100 | 0.003184516 | 0.000645472 | 0.000646032 | 0.087% | 1.309 | 0.000645472 | 0.000% | 0.246 | 0.000646032 | 0.087% | 0.044 |

| 120 | 0.003265361 | 0.000646778 | 0.000646778 | 0.000% | 0.154 | 0.000646778 | 0.000% | 0.236 | 0.000646778 | 0.000% | 0.031 |

| 140 | 0.003346206 | 0.000648311 | 0.000648311 | 0.000% | 0.083 | 0.000648311 | 0.000% | 0.005 | 0.000648311 | 0.000% | 0.104 |

| 160 | 0.003427051 | 0.000649973 | 0.00065007 | 0.015% | 0.420 | 0.000649973 | 0.000% | 0.642 | 0.00065007 | 0.015% | 0.032 |

| 180 | 0.003507896 | 0.000651665 | 0.000651665 | 0.000% | 0.681 | 0.000651665 | 0.000% | 0.388 | 0.000651665 | 0.000% | 0.148 |

| 200 | 0.00358874 | 0.000653615 | 0.000653615 | 0.000% | 0.372 | 0.000653615 | 0.000% | 0.282 | 0.000653615 | 0.000% | 0.109 |

| 1820 | 0.010137479 | 0.003577353 | 0.003577352 | 0.000% | 0.006 | 0.003577352 | 0.000% | 0.000 | 0.003577352 | 0.000% | 0.002 |

| 1840 | 0.010218315 | 0.003690754 | 0.003690754 | 0.000% | 0.006 | 0.003690754 | 0.000% | 0.002 | 0.003690754 | 0.000% | 0.001 |

| 1860 | 0.010299151 | 0.003809087 | 0.003809088 | 0.000% | 0.000 | 0.003809088 | 0.000% | 0.001 | 0.003809088 | 0.000% | 0.000 |

| 1880 | 0.010379986 | 0.003932352 | 0.003932352 | 0.000% | 0.001 | 0.003932352 | 0.000% | 0.000 | 0.003932352 | 0.000% | 0.002 |

| 1900 | 0.010460822 | 0.004060548 | 0.004060549 | 0.000% | 0.001 | 0.004060549 | 0.000% | 0.011 | 0.004060549 | 0.000% | 0.000 |

| 1920 | 0.010541657 | 0.004193676 | 0.004193675 | 0.000% | 0.010 | 0.004193675 | 0.000% | 0.002 | 0.004193675 | 0.000% | 0.000 |

| 1940 | 0.010622493 | 0.004331735 | 0.004331735 | 0.000% | 0.001 | 0.004331735 | 0.000% | 0.000 | 0.004331735 | 0.000% | 0.003 |

| 1960 | 0.010703329 | 0.004474726 | 0.004474726 | 0.000% | 0.000 | 0.004474726 | 0.000% | 0.000 | 0.004474726 | 0.000% | 0.003 |

| 1980 | 0.010784164 | 0.004622648 | 0.004622647 | 0.000% | 0.000 | 0.004622647 | 0.000% | 0.001 | 0.004622647 | 0.000% | 0.004 |

| 2000 | 0.010865 | 0.004775501 | 0.004775501 | 0.000% | 0.000 | 0.004775501 | 0.000% | 0.000 | 0.004775501 | 0.000% | 0.000 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kizys , R.; Juan, A.A.; Sawik, B.; Calvet , L. A Biased-Randomized Iterated Local Search Algorithm for Rich Portfolio Optimization. Appl. Sci. 2019, 9, 3509. https://doi.org/10.3390/app9173509

Kizys R, Juan AA, Sawik B, Calvet L. A Biased-Randomized Iterated Local Search Algorithm for Rich Portfolio Optimization. Applied Sciences. 2019; 9(17):3509. https://doi.org/10.3390/app9173509

Chicago/Turabian StyleKizys , Renatas, Angel A. Juan, Bartosz Sawik, and Laura Calvet . 2019. "A Biased-Randomized Iterated Local Search Algorithm for Rich Portfolio Optimization" Applied Sciences 9, no. 17: 3509. https://doi.org/10.3390/app9173509