Forecasting Stock Market Indices Using the Recurrent Neural Network Based Hybrid Models: CNN-LSTM, GRU-CNN, and Ensemble Models

Abstract

:1. Introduction

- Novel RNN-based hybrid models are proposed to forecast one-time-step and multi-time-step closing prices of the DAX, DOW, and S&P500 indices by utilizing neural network structures: CNN-LSTM, GRU-CNN, and ensemble models.

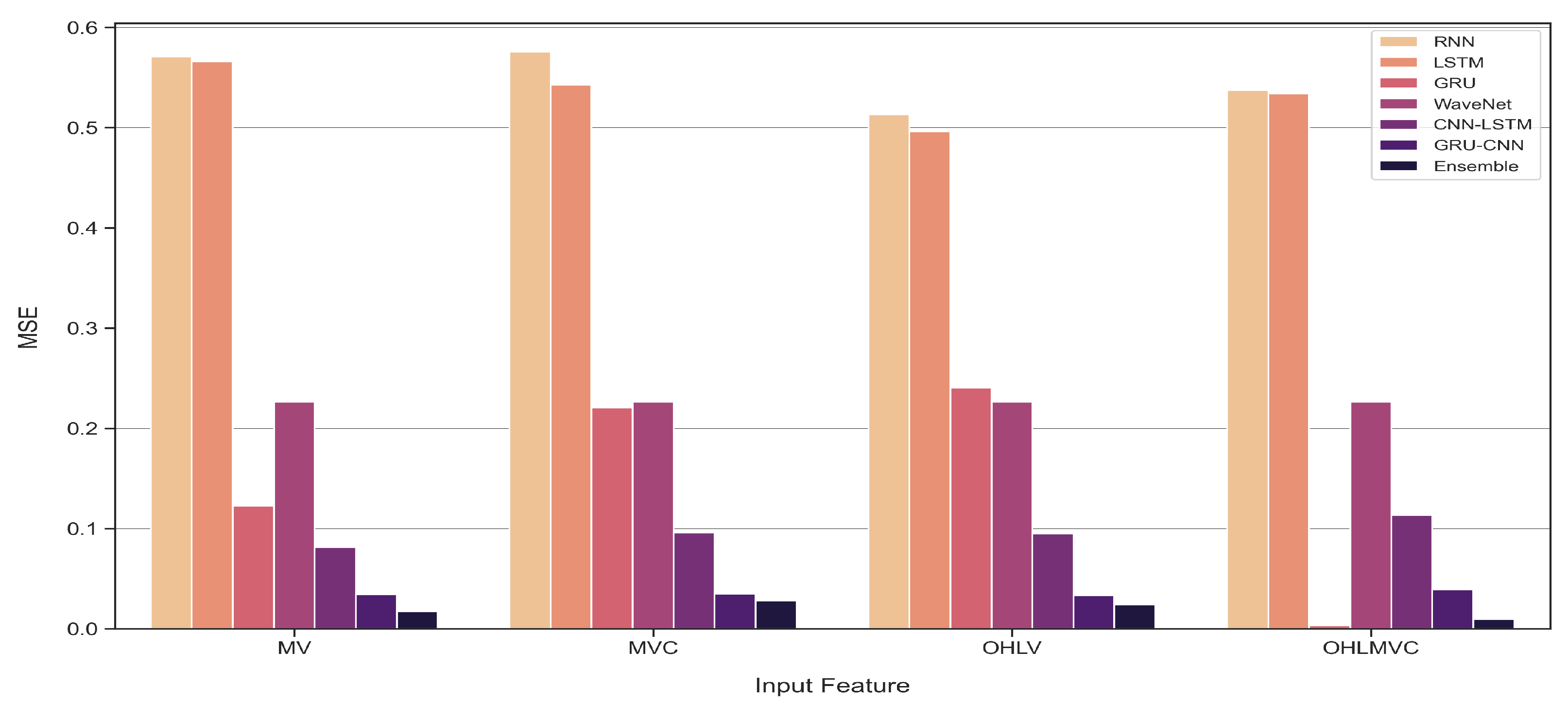

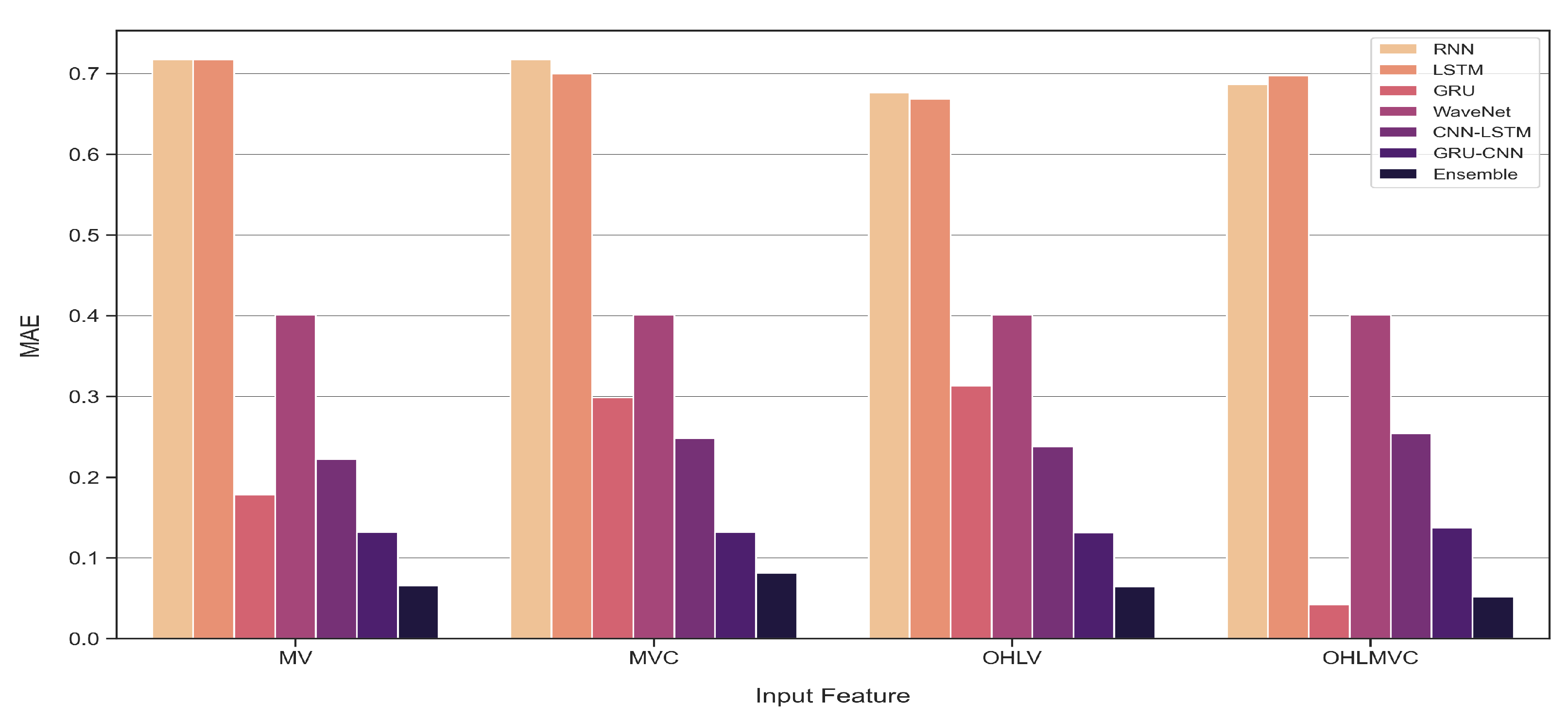

- The novel feature, which is the average of the high and low prices of stock market indices, is used as an input feature.

- Comparisons between the proposed and traditional benchmark models with various look-back periods and features are presented.

- The experimental results indicate that the proposed models outperform the benchmark models in 48.1% and 40.7% of the cases in terms of the mean squared error (MSE) and mean absolute error (MAE), respectively, in the case of one-time-step forecasting and 81.5% of the cases in terms of the MSE and MAE in the case of multi-time-step forecasting.

- Further, compared with previous studies that involved using open, high, and low prices, and trading volume of stock market indices as features, in this study, we evaluate the performance of our models by adding a novel feature to reduce the influence of the highest and lowest prices. The results confirm that the newly proposed feature contributes to improving the performance of the models in forecasting stock market indices.

- In particular, the ensemble model provides significant results for one-time-step forecasting.

2. Background and Related Work

2.1. Deep-Learning Background

2.1.1. ANN

2.1.2. MLP

2.1.3. CNN

2.1.4. RNN

2.1.5. LSTM

2.1.6. GRU

2.2. Related Work

3. Materials and Methods

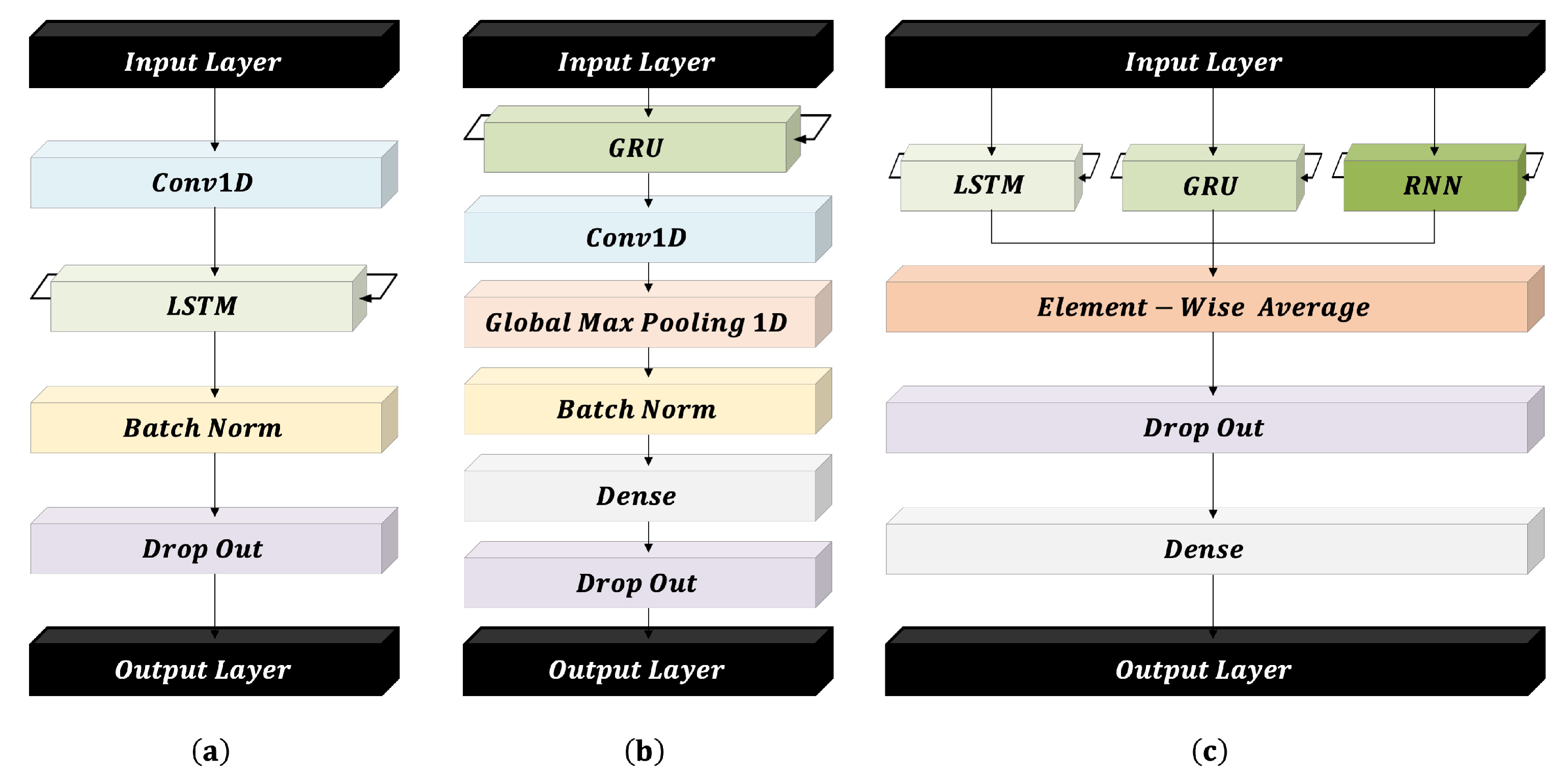

3.1. Proposed Models

3.1.1. Proposed CNN-LSTM Model

3.1.2. Proposed GRU-CNN Model

3.1.3. Proposed Ensemble Model

3.2. Implementation Details

3.2.1. Dataset

- (1)

- DAX: Deutscher Aktienindex, which is a stock market index consisting of the 40 (expanded from 30 in 2021) major German blue-chip companies trading on the Frankfurt stock exchange.

- (2)

- DOW: Dow Jones Industrial Average, which is a stock market index of 30 prominent companies in the United States.

- (3)

- S&P500: Standard and Poor’s 500, which is a stock market index of 500 large companies in the United States.

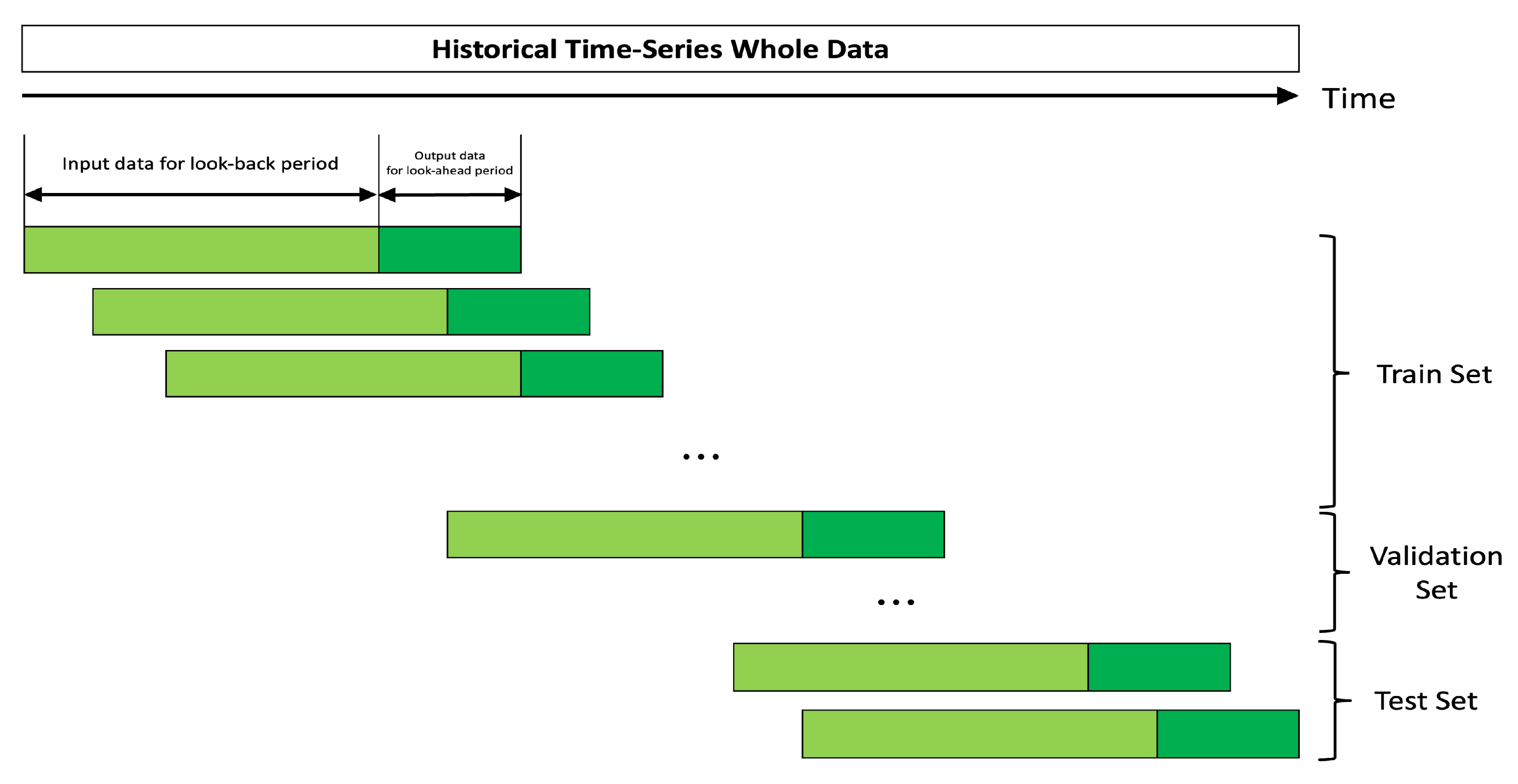

3.2.2. Generation of the Inputs and Outputs Using the Sliding Window Technique

3.2.3. Software and Hardware

3.2.4. Experimental Setting

3.2.5. Predictive Performance Metrics

4. Experimental Results

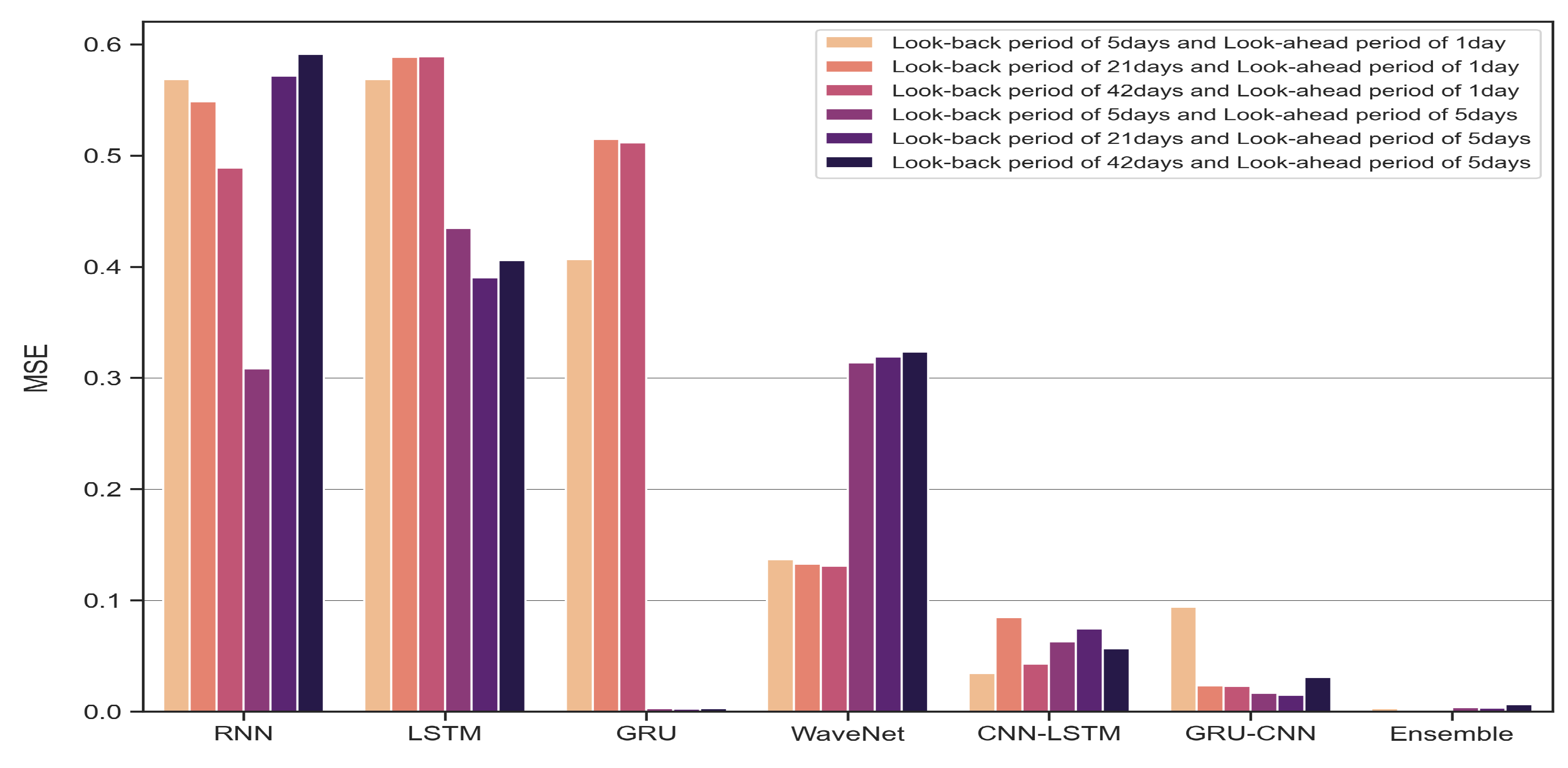

4.1. Benchmark Models

- RNN: Two RNN layers with 128 units and a dense layer with a look-ahead period of units;

- LSTM: An LSTM layer with 128 units and a dense layer with a look-ahead period of units;

- GRU: A GRU layer with 128 units and a dense layer with a look-ahead period of units;

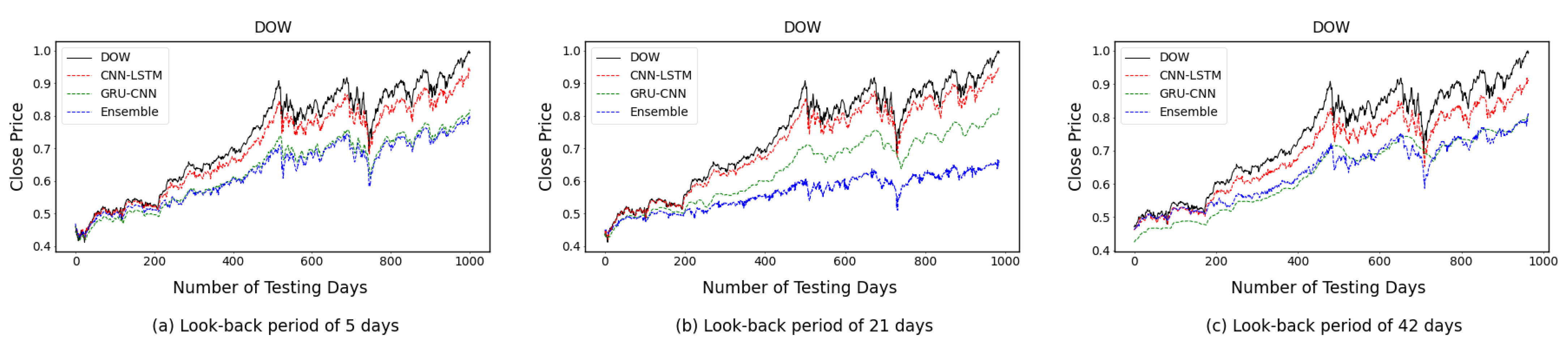

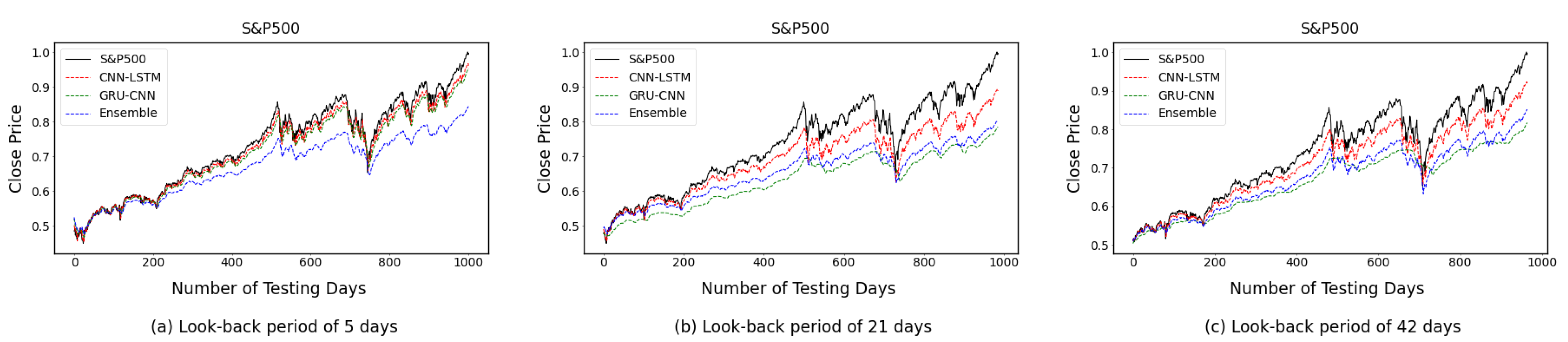

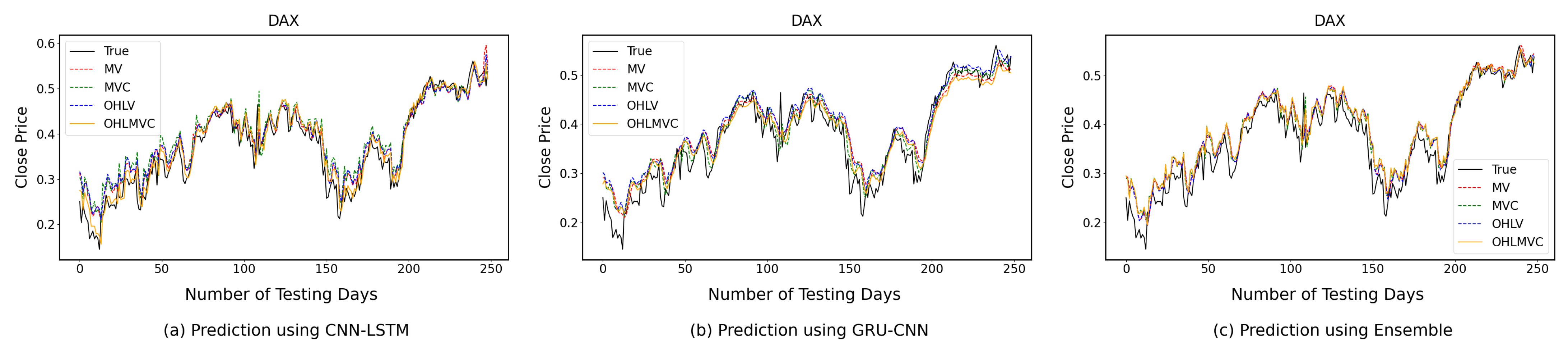

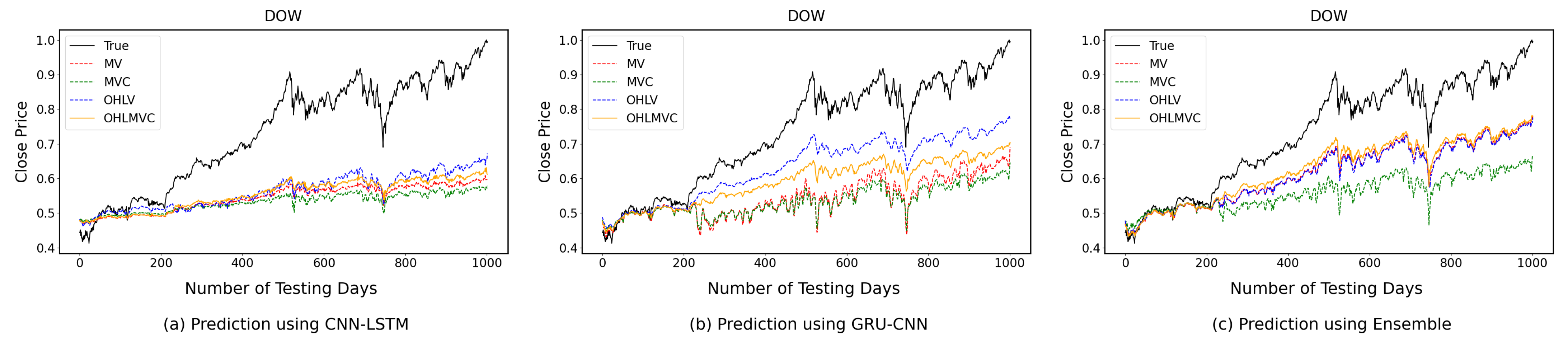

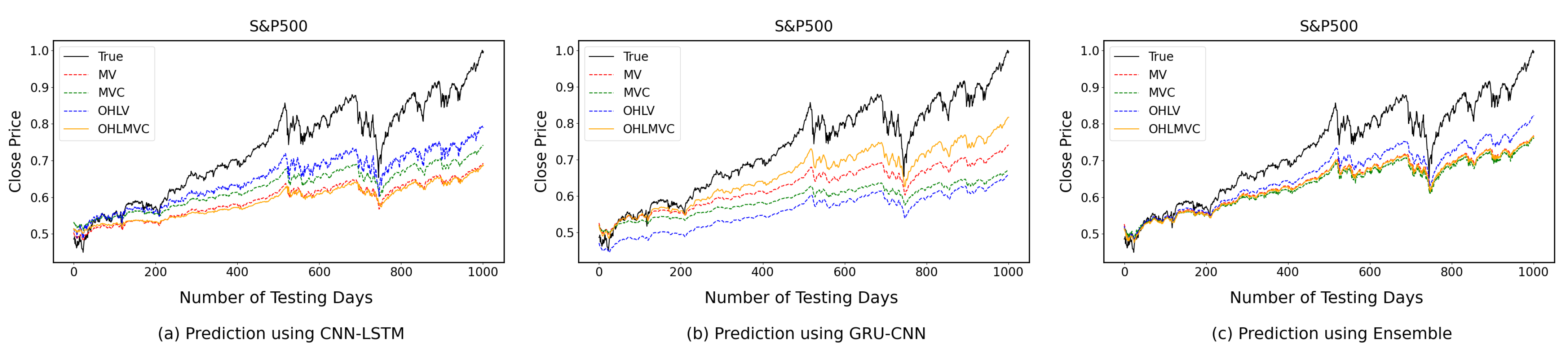

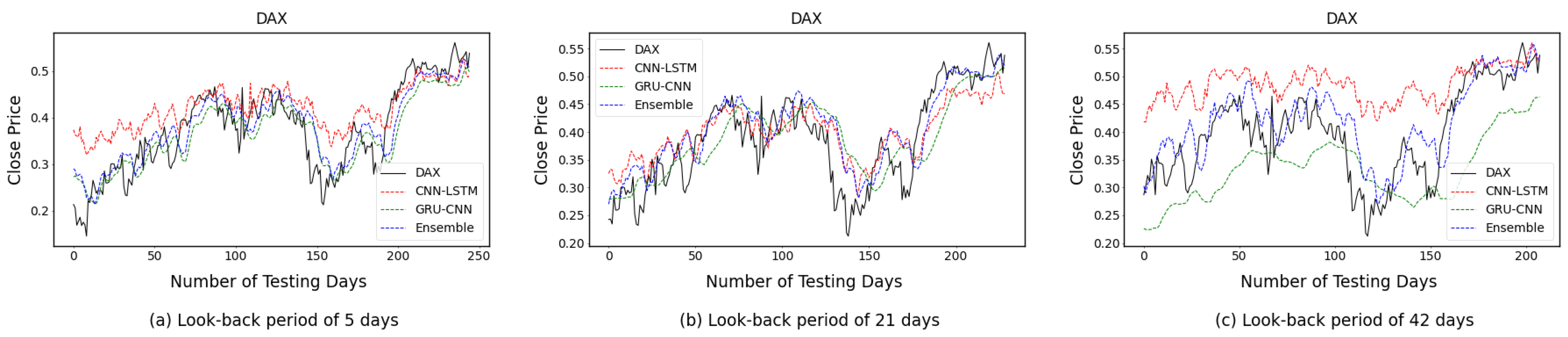

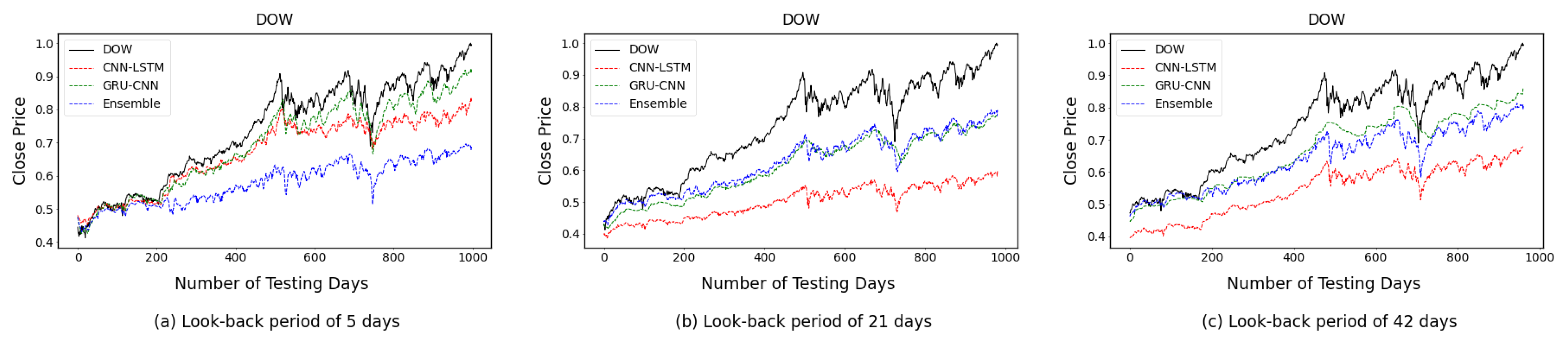

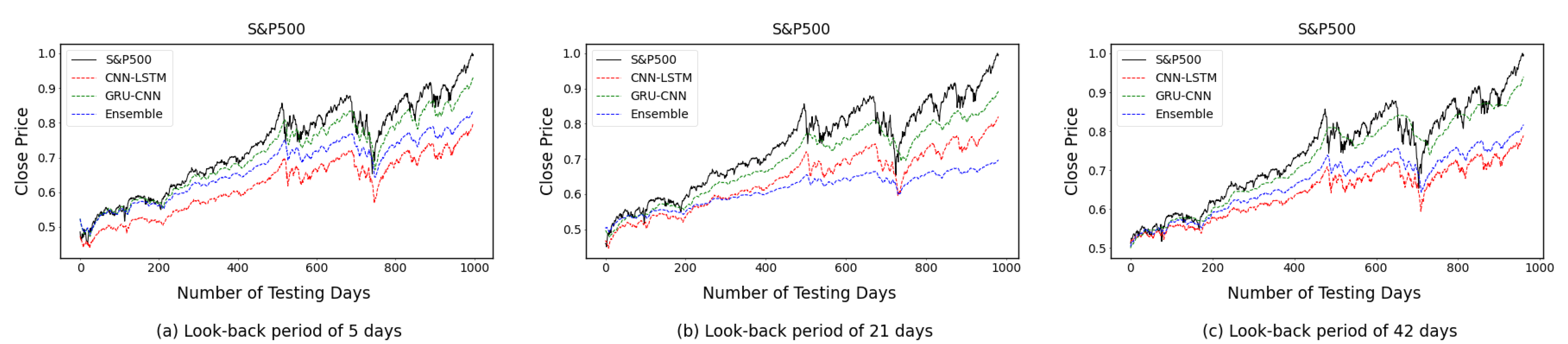

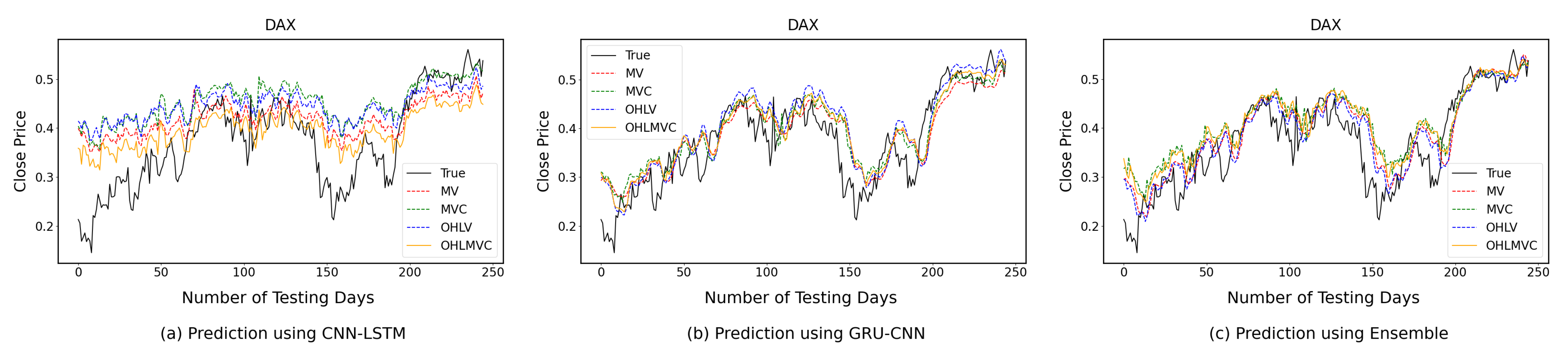

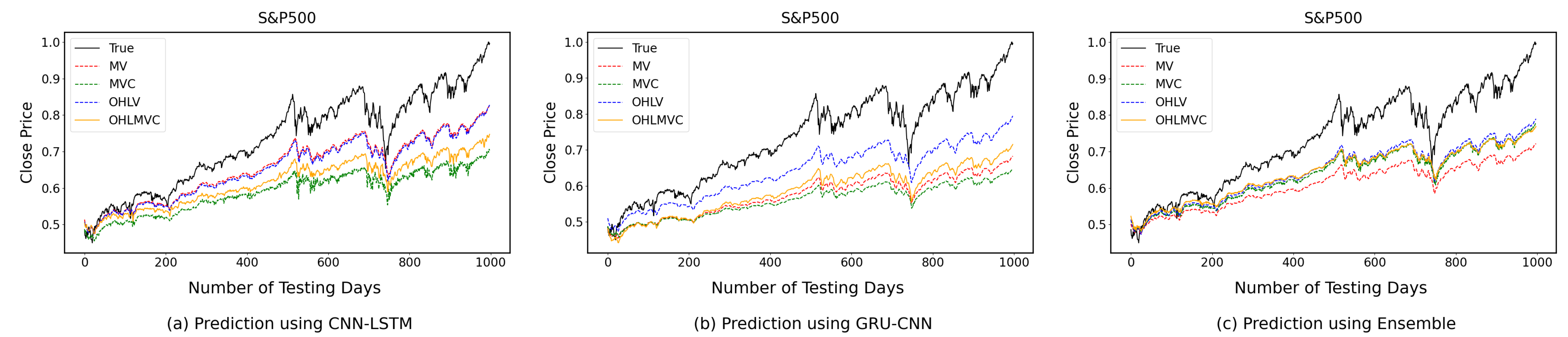

4.2. One-Time-Step Prediction Comparisons between Proposed and Benchmark Models

4.3. Multi-Time-Step Prediction Comparisons between Proposed and Benchmark Models

5. Discussion

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Abbreviations

| Adam | Adaptive Moment Estimation |

| ANN | Artificial Neural Network |

| ARIMA | Autoregressive Integrated Moving Average |

| ARMA | Autoregressive and Moving Average |

| CNN | Convolutional Neural Network |

| DAX | Deutscher Aktienindex |

| DOW | Dow Jones Industrial Average |

| GAN | Generative Adversarial Network |

| GRU | Gated Recurrent Unit |

| LSTM | Long Short Term Memory |

| MAE | Mean Absolute Error |

| MLP | Multilayer Perceptron |

| MSE | Mean Squared Error |

| ReLU | Rectified Linear Unit |

| RMSProp | Root Mean Square Propagation |

| RNN | Recurrent Neural Network |

| S&P500 | Standard and Poor’s 500 |

References

- Tan, T.; Quek, C.; Ng, G. Brain-inspired genetic complementary learning for stock market prediction. In Proceedings of the IEEE Congress on Evolutionary Computation, Edinburgh, UK, 2–5 September 2005; Volume 3, pp. 2653–2660. [Google Scholar] [CrossRef]

- Wang, J.Z.; Wang, J.J.; Zhang, Z.G.; Guo, S.P. Forecasting stock indices with back propagation neural network. Expert Syst. Appl. 2011, 38, 14346–14355. [Google Scholar] [CrossRef]

- Fama, E.F. The behavior of stock market prices. J. Bus. 1965, 38, 34–105. [Google Scholar] [CrossRef] [Green Version]

- Zhang, X.; Liang, X.; Zhiyuli, A.; Zhang, S.; Xu, R.; Wu, B. AT-LSTM: An Attention-based LSTM Model for Financial Time Series Prediction. IOP Conf. Ser. Mater. Sci. Eng. 2019, 569, 052037. [Google Scholar] [CrossRef]

- Shields, R.; Zein, S.A.E.; Brunet, N.V. An Analysis on the NASDAQ’s Potential for Sustainable Investment Practices during the Financial Shock from COVID-19. Sustainability 2021, 13, 3748. [Google Scholar] [CrossRef]

- Daradkeh, M.K. A Hybrid Data Analytics Framework with Sentiment Convergence and Multi-Feature Fusion for Stock Trend Prediction. Electronics 2022, 11, 250. [Google Scholar] [CrossRef]

- Abrishami, S.; Turek, M.; Choudhury, A.R.; Kumar, P. Enhancing Profit by Predicting Stock Prices using Deep Neural Networks. In Proceedings of the IEEE 31st International Conference on Tools with Artificial Intelligence (ICTAI), Portland, OR, USA, 4–6 November 2019; pp. 1551–1556. [Google Scholar]

- Aggarwal, S.; Aggarwal, S. Deep Investment in Financial Markets using Deep Learning Models. Int. J. Comput. Appl. 2017, 162, 40–43. [Google Scholar] [CrossRef]

- Graves, A.; Rahman Mohamed, A.; Hinton, G. Speech Recognition With Deep Recurrent Neural Networks. In Proceedings of the IEEE International Conference on Acoustics, Speech and Signal Processing, Vancouver, BC, Canada, 26–31 May 2013; pp. 6645–6649. [Google Scholar]

- Xu, K.; Ba, J.; Kiros, R.; Cho, K.; Courville, A.; Salakhudinov, R.; Zemel, R.; Bengio, Y. Show, Attend and Tell: Neural Image Caption Generation with Visual Attention. In Proceedings of the 32nd International Conference on Machine Learning, Lille, France, 7–9 July 2015; Volume 37, pp. 2048–2057. [Google Scholar]

- Zhu, Y.; Groth, O.; Bernstein, M.S.; Li, F. Visual7W: Grounded Question Answering in Images. In Proceedings of the IEEE Conference on Computer Vision and Pattern Recognition (CVPR), Las Vegas, NV, USA, 26 June–1 July 2016; pp. 4995–5004. [Google Scholar]

- Ren, B. The use of machine translation algorithm based on residual and LSTM neural network in translation teaching. PLoS ONE 2020, 15, e0240663. [Google Scholar] [CrossRef]

- Bhandari, H.N.; Rimal, B.; Pokhrel, N.R.; Rimal, R.; Dahal, K.R.; Khatri, R.K. Predicting stock market index using LSTM. Mach. Learn. Appl. 2022, 9, 100320. [Google Scholar] [CrossRef]

- Walczak, S.; Cerpa, N. Artificial Neural Networks. In Encyclopedia of Physical Science and Technology, 3rd ed.; Academic Press: New York, NY, USA, 2003; pp. 631–645. [Google Scholar] [CrossRef]

- Rumelhart, D.E.; Hinton, G.E.; Williams, R.J. Learning representations by back-propagating errors. Nature 1986, 323, 533–536. [Google Scholar] [CrossRef]

- Mcculloch, W.; Pitts, W. A Logical Calculus of Ideas Immanent in Nervous Activity. Bull. Math. Biophys. 1943, 5, 115–133. [Google Scholar] [CrossRef]

- Minsky, M.; Papert, S. Perceptrons: An Introduction to Computational Geometry; MIT Press: Cambridge, MA, USA, 1969. [Google Scholar]

- Popescu, M.C.; Balas, V.E.; Perescu-Popescu, L.; Mastorakis, N. Multilayer Perceptron and Neural Networks. WSEAS Trans. Circuits Syst. 2009, 8, 579–588. [Google Scholar]

- Lecun, Y.; Bengio, Y. Convolutional Networks for Images, Speech, and Time-Series; MIT Press: Cambridge, MA, USA, 1997. [Google Scholar]

- Krizhevsky, A.; Sutskever, I.; Hinton, G.E. ImageNet Classification with Deep Convolutional Neural Networks. In Proceedings of the 25th International Conference on Neural Information Processing Systems, NIPS’12, Lake Tahoe, NV, USA, 3–6 December 2012; Curran Associates Inc.: Red Hook, NY, USA, 2012; Volume 1, pp. 1097–1105. [Google Scholar]

- Kingma, D.P.; Ba, J.L. Adam: A Method for Stochastic Optimization. In Proceedings of the 3rd International Conference for Learning Representations (ICLR), San Diego, CA, USA, 7–9 May 2015. [Google Scholar]

- Nair, V.; Hinton, G.E. Rectified Linear Units Improve Restricted Boltzmann Machines. In Proceedings of the 27th International Conference on Machine Learning (ICML), Haifa, Israel, 21–24 June 2010; pp. 807–814. [Google Scholar]

- Srivastava, N.; Hinton, G.; Krizhevsky, A.; Sutskever, I.; Salakhutdinov, R. Dropout: A Simple Way to Prevent Neural Networks from Overfitting. J. Mach. Learn. Res. 2014, 15, 1929–1958. [Google Scholar]

- Bao, W.; Yue, J.; Rao, Y. A deep learning framework for financial time series using stacked autoencoders and long-short term memory. PLoS ONE 2017, 12, e0180944. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Rumelhart, D.E.; McClelland, J.L. Learning Internal Representations by Error Propagation. In Parallel Distributed Processing: Explorations in the Microstructure of Cognition: Foundations; MIT Press: Cambridge, MA, USA, 1987; pp. 318–362. [Google Scholar]

- Hochreiter, S.; Schmidhuber, J. Long Short-Term Memory. Neural Comput. 1997, 9, 1735–1780. [Google Scholar] [CrossRef]

- Bengio, Y.; Simard, P.; Frasconi, P. Learning long-term dependencies with gradient descent is difficult. IEEE Trans. Neural Netw. 1994, 5, 157–166. [Google Scholar] [CrossRef]

- Cho, K.; van Merriënboer, B.; Bahdanau, D.; Bengio, Y. On the Properties of Neural Machine Translation: Encoder–Decoder Approaches. In Proceedings of the SSST-8, Eighth Workshop on Syntax, Semantics and Structure in Statistical Translation, Doha, Qatar, 25 October 2014; Association for Computational Linguistics: Cedarville, OH, USA, 2014; pp. 103–111. [Google Scholar]

- Shen, G.; Tan, Q.; Zhang, H.; Zeng, P.; Xu, J. Deep Learning with Gated Recurrent Unit Networks for Financial Sequence Predictions. Procedia Comput. Sci. 2018, 131, 895–903. [Google Scholar] [CrossRef]

- Chung, J.; Gulcehre, C.; Cho, K.; Bengio, Y. Empirical Evaluation of Gated Recurrent Neural Networks on Sequence Modeling. In Proceedings of the NIPS 2014 Workshop on Deep Learning, Montreal, QC, Canada, 13 December 2014. [Google Scholar]

- Kaiser, L.; Sutskever, I. Neural GPUs Learn Algorithms. In Proceedings of the 4th International Conference on Learning Representations, ICLR, San Juan, PR, USA, 2–4 May 2016. [Google Scholar]

- Yin, W.; Kann, K.; Yu, M.; Schütze, H. Comparative Study of CNN and RNN for Natural Language Processing. arXiv 2017, arXiv:1702.01923. [Google Scholar]

- Cho, K.; van Merriënboer, B.; Gulcehre, C.; Bahdanau, D.; Bougares, F.; Schwenk, H.; Bengio, Y. Learning Phrase Representations using RNN Encoder–Decoder for Statistical Machine Translation. In Proceedings of the 2014 Conference on Empirical Methods in Natural Language Processing (EMNLP), Doha, Qatar, 25–29 October 2014; Association for Computational Linguistics: Doha, Qatar, 2014; pp. 1724–1734. [Google Scholar]

- Nguyen, T.T.; Yoon, S. A Novel Approach to Short-Term Stock Price Movement Prediction using Transfer Learning. Appl. Sci. 2019, 9, 4745. [Google Scholar] [CrossRef] [Green Version]

- Kamal, I.M.; Bae, H.; Sunghyun, S.; Yun, H. DERN: Deep Ensemble Learning Model for Short- and Long-Term Prediction of Baltic Dry Index. Appl. Sci. 2020, 10, 1504. [Google Scholar] [CrossRef] [Green Version]

- Ta, V.D.; Liu, C.M.; Tadesse, D.A. Portfolio Optimization-Based Stock Prediction Using Long-Short Term Memory Network in Quantitative Trading. Appl. Sci. 2020, 10, 437. [Google Scholar] [CrossRef] [Green Version]

- Rouf, N.; Malik, M.B.; Arif, T.; Sharma, S.; Singh, S.; Aich, S.; Kim, H.C. Stock Market Prediction Using Machine Learning Techniques: A Decade Survey on Methodologies, Recent Developments, and Future Directions. Electronics 2021, 10, 2717. [Google Scholar] [CrossRef]

- Aldhyani, T.H.H.; Alzahrani, A. Framework for Predicting and Modeling Stock Market Prices Based on Deep Learning Algorithms. Electronics 2022, 11, 3149. [Google Scholar] [CrossRef]

- Lin, Y.L.; Lai, C.J.; Pai, P.F. Using Deep Learning Techniques in Forecasting Stock Markets by Hybrid Data with Multilingual Sentiment Analysis. Electronics 2022, 11, 3513. [Google Scholar] [CrossRef]

- Chen, J.F.; Chen, W.L.; Huang, C.P.; Huang, S.H.; Chen, A.P. Financial Time-Series Data Analysis Using Deep Convolutional Neural Networks. In Proceedings of the 7th International Conference on Cloud Computing and Big Data (CCBD), Macau, China, 16–18 November 2016; pp. 87–92. [Google Scholar] [CrossRef]

- Sezer, O.B.; Ozbayoglu, A.M. Algorithmic financial trading with deep convolutional neural networks: Time series to image conversion approach. Appl. Soft Comput. 2018, 70, 525–538. [Google Scholar] [CrossRef]

- Gross, W.; Lange, S.; Bödecker, J.; Blum, M. Predicting Time Series with Space-Time Convolutional and Recurrent Neural Networks. In Proceedings of the European Symposium on Artificial Neural Networks, Computational Intelligence and Machine Learning, Bruges, Belgium, 26–28 April 2017; pp. 26–28. [Google Scholar]

- Fischer, T.; Krauss, C. Deep learning with long short-term memory networks for financial market predictions. Eur. J. Oper. Res. 2018, 270, 654–669. [Google Scholar] [CrossRef] [Green Version]

- Dutta, A.; Kumar, S.; Basu, M. A Gated Recurrent Unit Approach to Bitcoin Price Prediction. J. Risk Financ. Manag. 2020, 13, 23. [Google Scholar] [CrossRef] [Green Version]

- Heaton, J.; Polson, N.; Witte, J. Deep Learning for Finance: Deep Portfolios. Appl. Stoch. Model. Bus. Ind. 2016, 33, 3–12. [Google Scholar] [CrossRef]

- Ilyas, Q.M.; Iqbal, K.; Ijaz, S.; Mehmood, A.; Bhatia, S. A Hybrid Model to Predict Stock Closing Price Using Novel Features and a Fully Modified Hodrick–Prescott Filter. Electronics 2022, 11, 3588. [Google Scholar] [CrossRef]

- Livieris, I.E.; Pintelas, E.; Pintelas, P. A CNN-LSTM model for gold price time-series forecasting. Neural Comput. Appl. 2019, 32, 17351–17360. [Google Scholar] [CrossRef]

- Livieris, I.E.; Pintelas, E.; Stavroyiannis, S.; Pintelas, P. Ensemble Deep Learning Models for Forecasting Cryptocurrency Time-Series. Algorithms 2020, 13, 121. [Google Scholar] [CrossRef]

- Zhang, K.; Zhong, G.; Dong, J.; Wang, S.; Wang, Y. Stock Market Prediction Based on Generative Adversarial Network. Procedia Comput. Sci. 2018, 147, 400–406. [Google Scholar] [CrossRef]

- Leung, M.F.; Wang, J.; Che, H. Cardinality-constrained portfolio selection via two-timescale duplex neurodynamic optimization. Neural Netw. 2022, 153, 399–410. [Google Scholar] [CrossRef] [PubMed]

- Troiano, L.; Villa, E.M.; Loia, V. Replicating a Trading Strategy by Means of LSTM for Financial Industry Applications. IEEE Trans. Ind. Inform. 2018, 14, 3226–3234. [Google Scholar] [CrossRef]

- Chalvatzis, C.; Hristu-Varsakelis, D. High-performance stock index trading: Making effective use of a deep LSTM neural network. arXiv 2019, arXiv:1902.03125. [Google Scholar]

- Park, S.; Song, H.; Lee, S. Linear programing models for portfolio optimization using a benchmark. Eur. J. Financ. 2019, 25, 435–457. [Google Scholar] [CrossRef]

- Lee, S.I.; Yoo, S.J. Threshold-based portfolio: The role of the threshold and its applications. J. Supercomput. 2020, 76, 8040–8057. [Google Scholar] [CrossRef] [Green Version]

- Sen, J.; Dutta, A.; Mehtab, S. Stock Portfolio Optimization Using a Deep Learning LSTM Model. In Proceedings of the IEEE Mysore Sub Section International Conference, Hassan, India, 24–25 October 2021; pp. 263–271. [Google Scholar]

- McKinney, W. Data Structures for Statistical Computing in Python. In Proceedings of the 9th Python in Science Conference, Austin, TX, USA, 28 June– 3 July 2010; pp. 56–61. [Google Scholar]

- Granger, C.W.J. Strategies for Modelling Nonlinear Time-Series Relationships. Econ. Rec. 1993, 69, 233–238. [Google Scholar] [CrossRef] [Green Version]

- Python Core Team. Python: A Dynamic, Open Source Programming Language. Python Software Foundation. 2019. Available online: https://www.python.org (accessed on 18 December 2022).

- Keras. 2015. Available online: https://keras.io (accessed on 18 December 2022).

- Abadi, M.; Agarwal, A.; Barham, P.; Brevdo, E.; Chen, Z.; Citro, C.; Corrado, G.S.; Davis, A.; Dean, J.; Devin, M.; et al. TensorFlow: Large-Scale Machine Learning on Heterogeneous Systems. arXiv 2015, arXiv:1603.04467. [Google Scholar]

- van der Walt, S.; Colbert, S.C.; Varoquaux, G. The NumPy Array: A Structure for Efficient Numerical Computation. Comput. Sci. Eng. 2011, 13, 22–30. [Google Scholar] [CrossRef] [Green Version]

- Pedregosa, F.; Varoquaux, G.; Gramfort, A.; Michel, V.; Thirion, B.; Grisel, O.; Blondel, M.; Prettenhofer, P.; Weiss, R.; Dubourg, V.; et al. Scikit-Learn: Machine Learning in Python. J. Mach. Learn. Res. 2011, 12, 2825–2830. [Google Scholar]

- Huber, P.J. Robust Estimation of a Location Parameter. Ann. Math. Stat. 1964, 35, 73–101. [Google Scholar] [CrossRef]

- Ku, J.; Mozifian, M.; Lee, J.; Harakeh, A.; Waslander, S.L. Joint 3D Proposal Generation and Object Detection from View Aggregation. In Proceedings of the 2018 IEEE/RSJ International Conference on Intelligent Robots and Systems (IROS), Madrid, Spain, 1–5 October 2018; pp. 1–8. [Google Scholar] [CrossRef] [Green Version]

- Glorot, X.; Bengio, Y. Understanding the difficulty of training deep feedforward neural networks. In Proceedings of the 13th International Conference on Artificial Intelligence and Statistics, Sardinia, Italy, 13–15 May 2010; Volume 9, pp. 249–256. [Google Scholar]

- Zaremba, W.; Sutskever, I.; Vinyals, O. Recurrent Neural Network Regularization. arXiv 2014, arXiv:1409.2329. [Google Scholar]

- Gal, Y.; Ghahramani, Z. A Theoretically Grounded Application of Dropout in Recurrent Neural Networks. In Advances in Neural Information Processing Systems; Lee, D., Sugiyama, M., Luxburg, U., Guyon, I., Garnett, R., Eds.; Curran Associates, Inc.: Red Hook, NY, USA, 2016; Volume 29. [Google Scholar]

- Yao, Y.; Rosasco, L.; Caponnetto, A. On Early Stopping in Gradient Descent Learning. Constr. Approx. 2007, 26, 289–315. [Google Scholar] [CrossRef]

- Tieleman, T.; Hinton, G. Lecture 6.5-rmsprop: Divide the gradient by a running average of its recent magnitude. COURSERA Neural Netw. Mach. Learn. 2012, 4, 26–31. [Google Scholar]

- van den Oord, A.; Dieleman, S.; Zen, H.; Simonyan, K.; Vinyals, O.; Graves, A.; Kalchbrenner, N.; Senior, A.W.; Kavukcuoglu, K. WaveNet: A Generative Model for Raw Audio. In Proceedings of the 9th ISCA Speech Synthesis Workshop, Sunnyvale, CA, USA, 13–15 September 2016; p. 125. [Google Scholar]

- van den Oord, A.; Kalchbrenner, N.; Espeholt, L.; Koray, K.; Vinyals, O.; Graves, A. Conditional Image Generation with PixelCNN Decoders. In Advances in Neural Information Processing Systems; Curran Associates, Inc.: Red Hook, NY, USA, 2016; Volume 29. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Model | Description |

|---|---|

| CNN-LSTM | One-dimensional convolutional layer with 32 filters of size 3 with a stride of 1 |

| LSTM layer with 128 units and tanh activation function | |

| Batch-normalization layer | |

| Dropout layer with a rate of 0.2 | |

| Dense layer with a prediction window size of units | |

| GRU-CNN | GRU layer with 128 units and the tanh activation |

| One-dimensional convolutional layer with 32 filters of size 3 with a stride of 1 | |

| One-dimensional global max-pooling layer | |

| Batch-normalization layer | |

| Dense layer with 10 units and the ReLU activation | |

| Dropout layer with a rate of 0.2 | |

| Dense layer with a prediction window size of units | |

| Ensemble | RNN layer with 128 units and the tanh activation function |

| LSTM layer with 128 units and the tanh activation function | |

| GRU layer with 128 units and the tanh activation function | |

| Average of all the hidden states from RNN, LSTM, and GRU | |

| Dropout layer with a rate of 0.2 | |

| Dense layer with 32 units and the ReLU activation function | |

| Dense layer with a prediction window size of units |

| Hyperparameter | Value |

|---|---|

| Number of epochs | 50 |

| Early stopping patience | 10 |

| Learning rate | 0.0005 |

| Batch size | 32 |

| Loss function | MSE |

| Optimizer | Adam |

| Activation function | ReLU |

| Look-Back Period | Metric | Model | 2000–2019 1 | 2017–2019 | 2019–2021 | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| DAX | DOW | S&P500 | DAX | DOW | S&P500 | DAX | DOW | S&P500 | |||||

| 5 days | MSE | RNN | 0.1505 | 0.5739 | 0.5618 | 0.1146 | 0.6942 | 0.6174 | 0.7626 | 0.8576 | 0.7843 | ||

| LSTM | 0.1505 | 0.5739 | 0.5618 | 0.1146 | 0.6942 | 0.6174 | 0.7626 | 0.8576 | 0.7843 | ||||

| GRU | 0.1505 | 0.5739 | 0.0004 | 0.0012 | 0.6942 | 0.6174 | 0.7626 | 0.8576 | 0.0049 | ||||

| WaveNet | 0.4040 | 0.0940 | 0.0886 | 0.4929 | 0.0411 | 0.0672 | 0.0177 | 0.0075 | 0.0189 | ||||

| CNN-LSTM | 0.0079 | 0.0004 | 0.0040 | 0.0539 | 0.0154 | 0.1333 | 0.0868 | 0.0045 | 0.0032 | ||||

| GRU-CNN | 0.0011 | 0.0132 | 0.0042 | 0.0014 | 0.0069 | 0.0135 | 0.0111 | 0.0103 | 0.7843 | ||||

| Ensemble | 0.0017 | 0.0075 | 0.0059 | 0.0012 | 0.0023 | 0.0011 | 0.0009 | 0.0029 | 0.0003 | ||||

| MAE | RNN | 0.3756 | 0.7410 | 0.7376 | 0.3207 | 0.8282 | 0.7779 | 0.8717 | 0.9253 | 0.8834 | |||

| LSTM | 0.3756 | 0.7410 | 0.7376 | 0.3207 | 0.8282 | 0.7779 | 0.8717 | 0.9253 | 0.8834 | ||||

| GRU | 0.3756 | 0.7410 | 0.0185 | 0.0273 | 0.8282 | 0.7779 | 0.8717 | 0.9253 | 0.0674 | ||||

| WaveNet | 0.6284 | 0.2645 | 0.2680 | 0.6942 | 0.1841 | 0.2384 | 0.1224 | 0.0781 | 0.1235 | ||||

| CNN-LSTM | 0.0827 | 0.0162 | 0.0600 | 0.2120 | 0.1188 | 0.3520 | 0.2909 | 0.0650 | 0.0544 | ||||

| GRU-CNN | 0.0255 | 0.1031 | 0.0593 | 0.0279 | 0.0779 | 0.1113 | 0.1022 | 0.0991 | 0.8834 | ||||

| Ensemble | 0.0336 | 0.0740 | 0.0651 | 0.0262 | 0.0418 | 0.0279 | 0.0244 | 0.0468 | 0.0143 | ||||

| 21 days | MSE | RNN | 0.1509 | 0.5058 | 0.5341 | 0.0982 | 0.6552 | 0.6482 | 0.7252 | 0.8119 | 0.8070 | ||

| LSTM | 0.1658 | 0.5734 | 0.5602 | 0.1066 | 0.7420 | 0.6781 | 0.7555 | 0.8855 | 0.8273 | ||||

| GRU | 0.1658 | 0.5734 | 0.0002 | 0.0008 | 0.7420 | 0.6781 | 0.7555 | 0.8855 | 0.8273 | ||||

| WaveNet | 0.3877 | 0.0903 | 0.0856 | 0.4931 | 0.0371 | 0.0605 | 0.0196 | 0.0065 | 0.0154 | ||||

| CNN-LSTM | 0.0078 | 0.0159 | 0.0033 | 0.0632 | 0.0148 | 0.1074 | 0.1507 | 0.1950 | 0.2035 | ||||

| GRU-CNN | 0.0014 | 0.0356 | 0.0149 | 0.1066 | 0.0170 | 0.0193 | 0.0090 | 0.0033 | 0.0018 | ||||

| Ensemble | 0.0008 | 0.0007 | 0.0014 | 0.0009 | 0.0023 | 0.0011 | 0.0008 | 0.0011 | 0.0004 | ||||

| MAE | RNN | 0.3769 | 0.6934 | 0.7188 | 0.2927 | 0.8025 | 0.7941 | 0.8497 | 0.8987 | 0.8959 | |||

| LSTM | 0.3965 | 0.7418 | 0.7375 | 0.3074 | 0.8559 | 0.8145 | 0.8680 | 0.9401 | 0.9074 | ||||

| GRU | 0.3965 | 0.7418 | 0.0136 | 0.0222 | 0.8559 | 0.8145 | 0.8680 | 0.9401 | 0.9074 | ||||

| WaveNet | 0.6166 | 0.2596 | 0.2639 | 0.6936 | 0.1736 | 0.2251 | 0.1320 | 0.0722 | 0.1120 | ||||

| CNN-LSTM | 0.0742 | 0.1178 | 0.0473 | 0.2296 | 0.1177 | 0.3223 | 0.3865 | 0.4398 | 0.4479 | ||||

| GRU-CNN | 0.0290 | 0.1741 | 0.1135 | 0.3074 | 0.1224 | 0.1317 | 0.0888 | 0.0542 | 0.0384 | ||||

| Ensemble | 0.0211 | 0.0220 | 0.0312 | 0.0240 | 0.0426 | 0.0280 | 0.0201 | 0.0281 | 0.0160 | ||||

| 42 days | MSE | RNN | 0.1619 | 0.4885 | 0.4736 | 0.1147 | 0.5921 | 0.5475 | 0.5888 | 0.7551 | 0.6797 | ||

| LSTM | 0.1683 | 0.5904 | 0.5766 | 0.1228 | 0.7307 | 0.6683 | 0.7352 | 0.8806 | 0.8292 | ||||

| GRU | 0.1683 | 0.5904 | 0.0013 | 0.0009 | 0.7307 | 0.6683 | 0.7352 | 0.8806 | 0.8292 | ||||

| WaveNet | 0.3732 | 0.0856 | 0.0816 | 0.5011 | 0.0378 | 0.0595 | 0.0211 | 0.0058 | 0.0125 | ||||

| CNN-LSTM | 0.0025 | 0.0342 | 0.0210 | 0.0496 | 0.0783 | 0.0392 | 0.0833 | 0.0759 | 0.0004 | ||||

| GRU-CNN | 0.0035 | 0.0459 | 0.0220 | 0.0075 | 0.0128 | 0.0128 | 0.0019 | 0.0712 | 0.0270 | ||||

| Ensemble | 0.0007 | 0.0012 | 0.0007 | 0.0015 | 0.0013 | 0.0039 | 0.0009 | 0.0004 | 0.0007 | ||||

| MAE | RNN | 0.3940 | 0.6829 | 0.6795 | 0.3161 | 0.7602 | 0.7295 | 0.7644 | 0.8666 | 0.8227 | |||

| LSTM | 0.4013 | 0.7536 | 0.7486 | 0.3282 | 0.8492 | 0.8087 | 0.8561 | 0.9737 | 0.9091 | ||||

| GRU | 0.4013 | 0.7536 | 0.0343 | 0.0239 | 0.8492 | 0.8087 | 0.8561 | 0.9377 | 0.9091 | ||||

| WaveNet | 0.6053 | 0.2532 | 0.2583 | 0.6978 | 0.1723 | 0.2192 | 0.1372 | 0.0670 | 0.1001 | ||||

| CNN-LSTM | 0.0453 | 0.1844 | 0.1428 | 0.1883 | 0.2781 | 0.1910 | 0.2855 | 0.2738 | 0.0152 | ||||

| GRU-CNN | 0.0459 | 0.2004 | 0.1399 | 0.0725 | 0.1021 | 0.1074 | 0.0384 | 0.2652 | 0.1611 | ||||

| Ensemble | 0.0204 | 0.0308 | 0.0224 | 0.0289 | 0.0313 | 0.0548 | 0.0230 | 0.0167 | 0.0217 | ||||

| Look-Back Period | Optimizer | Feature | CNN-LSTM | GRU-CNN | Ensemble | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| DAX | DOW | S&P500 | DAX | DOW | S&P500 | DAX | DOW | S&P500 | |||||

| 5 days | Adam | MV | 0.0406 | 0.0228 | 0.0154 | 0.0025 | 0.0070 | 0.2717 | 0.0014 | 0.0039 | 0.0026 | ||

| MVC | 0.0534 | 0.0366 | 0.0097 | 0.0026 | 0.0054 | 0.0053 | 0.0014 | 0.0039 | 0.0026 | ||||

| OHLV | 0.0495 | 0.0068 | 0.0468 | 0.0045 | 0.0101 | 0.2674 | 0.0013 | 0.0042 | 0.0025 | ||||

| OHLMVC | 0.0496 | 0.0025 | 0.0030 | 0.0070 | 0.0096 | 0.2668 | 0.0013 | 0.0042 | 0.0025 | ||||

| RMSProp | MV | 0.0231 | 0.0239 | 0.0189 | 0.0023 | 0.0088 | 0.0063 | 0.0013 | 0.0031 | 0.0014 | |||

| MVC | 0.0972 | 0.0796 | 0.0270 | 0.0035 | 0.0197 | 0.0171 | 0.0013 | 0.0031 | 0.0014 | ||||

| OHLV | 0.0175 | 0.0133 | 0.0206 | 0.0019 | 0.0144 | 0.2223 | 0.0013 | 0.0031 | 0.0014 | ||||

| OHLMVC | 0.0330 | 0.0152 | 0.0396 | 0.0043 | 0.2513 | 0.0107 | 0.0013 | 0.0031 | 0.0014 | ||||

| 21 days | Adam | MV | 0.0174 | 0.0454 | 0.0217 | 0.0070 | 0.0133 | 0.0180 | 0.0010 | 0.0029 | 0.0011 | ||

| MVC | 0.1042 | 0.0489 | 0.1143 | 0.0030 | 0.0141 | 0.0115 | 0.0021 | 0.0040 | 0.0080 | ||||

| OHLV | 0.0739 | 0.0752 | 0.1047 | 0.0390 | 0.0186 | 0.0120 | 0.0008 | 0.0013 | 0.0010 | ||||

| OHLMVC | 0.0406 | 0.0228 | 0.0154 | 0.0054 | 0.0253 | 0.0138 | 0.0021 | 0.0040 | 0.0080 | ||||

| RMSProp | MV | 0.0295 | 0.1721 | 0.2440 | 0.0163 | 0.0183 | 0.0242 | 0.0010 | 0.0042 | 0.0060 | |||

| MVC | 0.0318 | 0.0608 | 0.1752 | 0.0395 | 0.0306 | 0.0178 | 0.0017 | 0.0185 | 0.0038 | ||||

| OHLV | 0.0477 | 0.1299 | 0.3043 | 0.0157 | 0.0229 | 0.0137 | 0.0008 | 0.0014 | 0.0015 | ||||

| OHLMVC | 0.0406 | 0.0228 | 0.0154 | 0.0284 | 0.0244 | 0.0253 | 0.0021 | 0.0040 | 0.0080 | ||||

| 42 days | Adam | MV | 0.0443 | 0.0790 | 0.0105 | 0.0163 | 0.0169 | 0.2459 | 0.0014 | 0.0028 | 0.0022 | ||

| MVC | 0.0566 | 0.0585 | 0.0426 | 0.0227 | 0.0271 | 0.2339 | 0.0010 | 0.2455 | 0.0129 | ||||

| OHLV | 0.0451 | 0.0628 | 0.0202 | 0.0043 | 0.0433 | 0.0206 | 0.0010 | 0.0010 | 0.0018 | ||||

| OHLMVC | 0.0488 | 0.1413 | 0.0102 | 0.0088 | 0.0126 | 0.0124 | 0.0019 | 0.0026 | 0.0012 | ||||

| RMSProp | MV | 0.1339 | 0.0792 | 0.1816 | 0.0084 | 0.0503 | 0.0223 | 0.0017 | 0.0036 | 0.0035 | |||

| MVC | 0.0659 | 0.2908 | 0.1823 | 0.0191 | 0.0609 | 0.3112 | 0.0012 | 0.0057 | 0.0049 | ||||

| OHLV | 0.3795 | 0.3173 | 0.0588 | 0.0079 | 0.0394 | 0.0341 | 0.0008 | 0.0021 | 0.2784 | ||||

| OHLMVC | 0.0496 | 0.0607 | 0.6410 | 0.0100 | 0.0256 | 0.0229 | 0.0010 | 0.0021 | 0.0017 | ||||

| Look-Back Period | Optimizer | Feature | CNN-LSTM | GRU-CNN | Ensemble | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| DAX | DOW | S&P500 | DAX | DOW | S&P500 | DAX | DOW | S&P500 | |||||

| 5 days | Adam | MV | 0.1635 | 0.1285 | 0.1161 | 0.0405 | 0.0778 | 0.3662 | 0.0293 | 0.0460 | 0.0391 | ||

| MVC | 0.2047 | 0.1433 | 0.0810 | 0.0413 | 0.0640 | 0.0584 | 0.0259 | 0.0578 | 0.0423 | ||||

| OHLV | 0.1952 | 0.0667 | 0.1554 | 0.0519 | 0.0934 | 0.3513 | 0.0280 | 0.0542 | 0.0358 | ||||

| OHLMVC | 0.1806 | 0.0421 | 0.0466 | 0.0639 | 0.0860 | 0.3503 | 0.0227 | 0.0373 | 0.2706 | ||||

| RMSProp | MV | 0.1344 | 0.1391 | 0.1186 | 0.0375 | 0.0765 | 0.0690 | 0.0288 | 0.0426 | 0.0311 | |||

| MVC | 0.2370 | 0.2125 | 0.1433 | 0.0472 | 0.0972 | 0.1134 | 0.0295 | 0.0556 | 0.0582 | ||||

| OHLV | 0.1057 | 0.0813 | 0.0999 | 0.0353 | 0.0926 | 0.3573 | 0.0230 | 0.0328 | 0.0279 | ||||

| OHLMVC | 0.1438 | 0.1012 | 0.1770 | 0.0578 | 0.3581 | 0.0872 | 0.0284 | 0.0666 | 0.0545 | ||||

| 21 days | Adam | MV | 0.0810 | 0.2076 | 0.1332 | 0.0679 | 0.1048 | 0.1066 | 0.0248 | 0.0439 | 0.0268 | ||

| MVC | 0.2429 | 0.1804 | 0.2890 | 0.0455 | 0.1116 | 0.0979 | 0.0340 | 0.0496 | 0.0603 | ||||

| OHLV | 0.2301 | 0.2251 | 0.2725 | 0.1417 | 0.1169 | 0.0945 | 0.0217 | 0.0309 | 0.0251 | ||||

| OHLMVC | 0.1635 | 0.1285 | 0.1161 | 0.0616 | 0.1519 | 0.1057 | 0.0340 | 0.0496 | 0.0603 | ||||

| RMSProp | MV | 0.1454 | 0.3760 | 0.3348 | 0.1017 | 0.1177 | 0.1387 | 0.0236 | 0.0526 | 0.0645 | |||

| MVC | 0.1376 | 0.2006 | 0.3381 | 0.1432 | 0.1485 | 0.1213 | 0.0342 | 0.0940 | 0.0542 | ||||

| OHLV | 0.1783 | 0.3155 | 0.4366 | 0.0902 | 0.1353 | 0.0930 | 0.0216 | 0.0291 | 0.0328 | ||||

| OHLMVC | 0.1635 | 0.1285 | 0.1161 | 0.1149 | 0.1475 | 0.1484 | 0.0340 | 0.0496 | 0.0603 | ||||

| 42 days | Adam | MV | 0.1664 | 0.2570 | 0.0850 | 0.1085 | 0.1189 | 0.3836 | 0.0284 | 0.0421 | 0.0334 | ||

| MVC | 0.2052 | 0.1808 | 0.1750 | 0.1227 | 0.1499 | 0.3378 | 0.0245 | 0.3110 | 0.0719 | ||||

| OHLV | 0.1730 | 0.2454 | 0.1164 | 0.0523 | 0.1892 | 0.1361 | 0.0241 | 0.0263 | 0.0330 | ||||

| OHLMVC | 0.1970 | 0.3401 | 0.0741 | 0.0816 | 0.1013 | 0.1014 | 0.0336 | 0.0409 | 0.0275 | ||||

| RMSProp | MV | 0.3173 | 0.2390 | 0.2914 | 0.0753 | 0.2114 | 0.1191 | 0.0330 | 0.0510 | 0.0512 | |||

| MVC | 0.2235 | 0.5177 | 0.4117 | 0.1108 | 0.2255 | 0.4436 | 0.0259 | 0.0607 | 0.0615 | ||||

| OHLV | 0.4822 | 0.5251 | 0.2263 | 0.0692 | 0.1869 | 0.1710 | 0.0211 | 0.0371 | 0.3333 | ||||

| OHLMVC | 0.1923 | 0.2253 | 0.5319 | 0.0806 | 0.1466 | 0.3771 | 0.0233 | 0.0375 | 0.0340 | ||||

| Look-Back Period | Metric | Model | 2000–2019 1 | 2017–2019 | 2019–2021 | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| DAX | DOW | S&P500 | DAX | DOW | S&P500 | DAX | DOW | S&P500 | |||||

| 5 days | MSE | RNN | 0.0561 | 0.3050 | 0.2887 | 0.0421 | 0.3856 | 0.3378 | 0.4136 | 0.4975 | 0.4463 | ||

| LSTM | 0.1153 | 0.4377 | 0.4247 | 0.0901 | 0.5388 | 0.4804 | 0.5686 | 0.6558 | 0.5995 | ||||

| GRU | 0.0034 | 0.0012 | 0.0023 | 0.0045 | 0.0031 | 0.0031 | 0.0011 | 0.0030 | 0.0015 | ||||

| WaveNet | 0.0383 | 0.3106 | 0.2995 | 0.0218 | 0.3857 | 0.3240 | 0.4604 | 0.5215 | 0.4606 | ||||

| CNN-LSTM | 0.0070 | 0.0529 | 0.0865 | 0.0361 | 0.0070 | 0.0699 | 0.0737 | 0.1186 | 0.1112 | ||||

| GRU-CNN | 0.0023 | 0.0153 | 0.0049 | 0.0042 | 0.0299 | 0.0359 | 0.0153 | 0.0147 | 0.0261 | ||||

| Ensemble | 0.0041 | 0.0037 | 0.0037 | 0.0036 | 0.0070 | 0.0053 | 0.0013 | 0.0021 | 0.0009 | ||||

| MAE | RNN | 0.2228 | 0.5325 | 0.5223 | 0.1854 | 0.6141 | 0.5702 | 0.6407 | 0.7033 | 0.6650 | |||

| LSTM | 0.3285 | 0.6469 | 0.6411 | 0.2837 | 0.7294 | 0.6856 | 0.7527 | 0.8090 | 0.7723 | ||||

| GRU | 0.0459 | 0.0285 | 0.0407 | 0.0561 | 0.0388 | 0.0479 | 0.0348 | 0.0309 | 0.0224 | ||||

| WaveNet | 0.1732 | 0.5355 | 0.5319 | 0.1251 | 0.6155 | 0.5606 | 0.6766 | 0.7212 | 0.6762 | ||||

| CNN-LSTM | 0.0695 | 0.2155 | 0.2896 | 0.1582 | 0.0687 | 0.2522 | 0.2685 | 0.3423 | 0.3303 | ||||

| GRU-CNN | 0.0374 | 0.1141 | 0.0631 | 0.0526 | 0.1649 | 0.1791 | 0.1195 | 0.1173 | 0.1585 | ||||

| Ensemble | 0.0524 | 0.0522 | 0.0498 | 0.0460 | 0.0743 | 0.0645 | 0.0289 | 0.0394 | 0.0230 | ||||

| 21 days | MSE | RNN | 0.1692 | 0.5765 | 0.5631 | 0.1083 | 0.6957 | 0.6176 | 0.7504 | 0.8649 | 0.7967 | ||

| LSTM | 0.1127 | 0.3921 | 0.3816 | 0.0734 | 0.4769 | 0.4226 | 0.5105 | 0.5959 | 0.5468 | ||||

| GRU | 0.0023 | 0.0022 | 0.0015 | 0.0026 | 0.0036 | 0.0042 | 0.0016 | 0.0034 | 0.0141 | ||||

| WaveNet | 0.0409 | 0.3148 | 0.3031 | 0.0227 | 0.3970 | 0.3374 | 0.4482 | 0.5305 | 0.4756 | ||||

| CNN-LSTM | 0.0199 | 0.1772 | 0.0423 | 0.0432 | 0.0444 | 0.0973 | 0.0472 | 0.1140 | 0.0839 | ||||

| GRU-CNN | 0.0030 | 0.0278 | 0.0087 | 0.0092 | 0.0173 | 0.0217 | 0.0029 | 0.0071 | 0.0361 | ||||

| Ensemble | 0.0022 | 0.0017 | 0.0019 | 0.0048 | 0.0050 | 0.0094 | 0.0015 | 0.0012 | 0.0009 | ||||

| MAE | RNN | 0.4009 | 0.7440 | 0.7396 | 0.3095 | 0.8297 | 0.7794 | 0.8650 | 0.9293 | 0.8911 | |||

| LSTM | 0.3263 | 0.6129 | 0.6083 | 0.2530 | 0.6863 | 0.6437 | 0.7132 | 0.7713 | 0.7380 | ||||

| GRU | 0.0364 | 0.0403 | 0.0330 | 0.0438 | 0.0520 | 0.0540 | 0.0350 | 0.0510 | 0.1154 | ||||

| WaveNet | 0.1832 | 0.5405 | 0.5361 | 0.1264 | 0.6247 | 0.5727 | 0.6679 | 0.7275 | 0.6877 | ||||

| CNN-LSTM | 0.1318 | 0.4034 | 0.1973 | 0.1794 | 0.2017 | 0.3030 | 0.2148 | 0.3363 | 0.2865 | ||||

| GRU-CNN | 0.0429 | 0.1471 | 0.0832 | 0.0842 | 0.1213 | 0.1379 | 0.0476 | 0.0787 | 0.1876 | ||||

| Ensemble | 0.0363 | 0.0348 | 0.0364 | 0.0545 | 0.0614 | 0.0834 | 0.0309 | 0.0288 | 0.0252 | ||||

| 42 days | MSE | RNN | 0.1562 | 0.5930 | 0.5795 | 0.1045 | 0.7432 | 0.6845 | 0.7360 | 0.8848 | 0.8377 | ||

| LSTM | 0.1144 | 0.4016 | 0.3910 | 0.0849 | 0.5090 | 0.4690 | 0.4994 | 0.6070 | 0.5733 | ||||

| GRU | 0.0030 | 0.0038 | 0.0024 | 0.0040 | 0.0023 | 0.0046 | 0.0013 | 0.0011 | 0.0017 | ||||

| WaveNet | 0.0445 | 0.3203 | 0.3080 | 0.0242 | 0.3983 | 0.3445 | 0.4413 | 0.5374 | 0.4911 | ||||

| CNN-LSTM | 0.0079 | 0.0388 | 0.0654 | 0.0294 | 0.0296 | 0.0064 | 0.0709 | 0.2007 | 0.0598 | ||||

| GRU-CNN | 0.0047 | 0.0305 | 0.0060 | 0.0099 | 0.0318 | 0.0274 | 0.0357 | 0.0860 | 0.0462 | ||||

| Ensemble | 0.0023 | 0.0021 | 0.0011 | 0.0037 | 0.0269 | 0.0164 | 0.0022 | 0.0012 | 0.0011 | ||||

| MAE | RNN | 0.3823 | 0.7552 | 0.7505 | 0.2935 | 0.8560 | 0.8179 | 0.8567 | 0.9399 | 0.9137 | |||

| LSTM | 0.3301 | 0.6209 | 0.6160 | 0.2717 | 0.7075 | 0.6758 | 0.7055 | 0.7783 | 0.7556 | ||||

| GRU | 0.0432 | 0.0551 | 0.0435 | 0.0393 | 0.0609 | 0.0674 | 0.0264 | 0.0262 | 0.0338 | ||||

| WaveNe | 0.1948 | 0.5469 | 0.5416 | 0.1274 | 0.6247 | 0.5773 | 0.6625 | 0.7322 | 0.6991 | ||||

| CNN-LSTM | 0.0719 | 0.1861 | 0.2465 | 0.1268 | 0.1606 | 0.0684 | 0.2631 | 0.4461 | 0.2399 | ||||

| GRU-CNN | 0.0569 | 0.1594 | 0.0666 | 0.0901 | 0.1609 | 0.1542 | 0.1841 | 0.2913 | 0.2123 | ||||

| Ensemble | 0.0378 | 0.0390 | 0.0276 | 0.0468 | 0.1495 | 0.1132 | 0.0337 | 0.0289 | 0.0262 | ||||

| Look-Back Period | Optimizer | Feature | CNN-LSTM | GRU-CNN | Ensemble | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| DAX | DOW | S&P500 | DAX | DOW | S&P500 | DAX | DOW | S&P500 | |||||

| 5 days | Adam | MV | 0.0293 | 0.0573 | 0.0636 | 0.0085 | 0.0099 | 0.0160 | 0.0532 | 0.2397 | 0.0048 | ||

| MVC | 0.0149 | 0.0531 | 0.1266 | 0.0038 | 0.0229 | 0.0128 | 0.0028 | 0.0084 | 0.0120 | ||||

| OHLV | 0.0389 | 0.0595 | 0.0892 | 0.0073 | 0.0200 | 0.0223 | 0.0030 | 0.0043 | 0.0033 | ||||

| OHLMVC | 0.0523 | 0.0945 | 0.0803 | 0.0058 | 0.0227 | 0.0155 | 0.0024 | 0.0051 | 0.0029 | ||||

| RMSProp | MV | 0.0255 | 0.0848 | 0.0340 | 0.0036 | 0.0146 | 0.0263 | 0.0033 | 0.0074 | 0.0052 | |||

| MVC | 0.0184 | 0.0333 | 0.0926 | 0.0034 | 0.0186 | 0.0269 | 0.0031 | 0.0141 | 0.0065 | ||||

| OHLV | 0.0131 | 0.0372 | 0.0507 | 0.0038 | 0.0022 | 0.0201 | 0.0033 | 0.0037 | 0.0068 | ||||

| OHLMVC | 0.0167 | 0.0720 | 0.0803 | 0.0031 | 0.0253 | 0.0322 | 0.0027 | 0.0044 | 0.0050 | ||||

| 21 days | Adam | MV | 0.0443 | 0.0541 | 0.1509 | 0.0395 | 0.0273 | 0.0106 | 0.0030 | 0.0052 | 0.1904 | ||

| MVC | 0.1774 | 0.1768 | 0.2014 | 0.0066 | 0.0107 | 0.0217 | 0.0036 | 0.0077 | 0.0040 | ||||

| OHLV | 0.0368 | 0.1119 | 0.0745 | 0.0050 | 0.0174 | 0.0222 | 0.0028 | 0.0026 | 0.0041 | ||||

| OHLMVC | 0.0990 | 0.1957 | 0.1828 | 0.0044 | 0.0182 | 0.0105 | 0.0027 | 0.0026 | 0.0025 | ||||

| RMSProp | MV | 0.2070 | 0.1048 | 0.0475 | 0.0243 | 0.0205 | 0.0517 | 0.0026 | 0.0102 | 0.0059 | |||

| MVC | 0.0811 | 0.0669 | 0.0804 | 0.0125 | 0.0154 | 0.0519 | 0.0042 | 0.0154 | 0.0124 | ||||

| OHLV | 0.1223 | 0.0316 | 0.1723 | 0.0147 | 0.0152 | 0.0543 | 0.0044 | 0.2354 | 0.0062 | ||||

| OHLMVC | 0.0640 | 0.1376 | 0.1346 | 0.0264 | 0.0189 | 0.0496 | 0.0376 | 0.0035 | 0.0089 | ||||

| 42 days | Adam | MV | 0.0327 | 0.2019 | 0.1374 | 0.0532 | 0.0477 | 0.0562 | 0.0031 | 0.0065 | 0.0046 | ||

| MVC | 0.0640 | 0.0928 | 0.0850 | 0.0115 | 0.0443 | 0.0320 | 0.0062 | 0.2501 | 0.0075 | ||||

| OHLV | 0.0360 | 0.0897 | 0.0439 | 0.0168 | 0.0494 | 0.0265 | 0.0027 | 0.0101 | 0.0062 | ||||

| OHLMVC | 0.0756 | 0.1798 | 0.1960 | 0.0079 | 0.0355 | 0.0455 | 0.0028 | 0.0045 | 0.0093 | ||||

| RMSProp | MV | 0.0506 | 0.2216 | 0.1771 | 0.0111 | 0.0486 | 0.0392 | 0.0036 | 0.0156 | 0.0093 | |||

| MVC | 0.1086 | 0.4098 | 0.1259 | 0.0084 | 0.0418 | 0.0648 | 0.0033 | 0.3016 | 0.0125 | ||||

| OHLV | 0.1241 | 0.3247 | 0.1819 | 0.0052 | 0.0471 | 0.0301 | 0.2476 | 0.0065 | 0.0042 | ||||

| OHLMVC | 0.0904 | 0.1509 | 0.0706 | 0.0055 | 0.0453 | 0.0621 | 0.0030 | 0.0043 | 0.0086 | ||||

| Look-Back Period | Optimizer | Feature | CNN-LSTM | GRU-CNN | Ensemble | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| DAX | DOW | S&P500 | DAX | DOW | S&P500 | DAX | DOW | S&P500 | |||||

| 5 days | Adam | MV | 0.1349 | 0.1894 | 0.2386 | 0.0786 | 0.0920 | 0.1012 | 0.1561 | 0.3217 | 0.0551 | ||

| MVC | 0.0963 | 0.2239 | 0.3409 | 0.0528 | 0.1421 | 0.1017 | 0.0409 | 0.0781 | 0.0832 | ||||

| OHLV | 0.1654 | 0.2088 | 0.2907 | 0.0698 | 0.1321 | 0.1336 | 0.0424 | 0.0553 | 0.0457 | ||||

| OHLMVC | 0.1963 | 0.2775 | 0.2648 | 0.0631 | 0.1414 | 0.1085 | 0.0376 | 0.0572 | 0.0427 | ||||

| RMSProp | MV | 0.1277 | 0.2466 | 0.1705 | 0.0476 | 0.1098 | 0.1520 | 0.0448 | 0.0698 | 0.0569 | |||

| MVC | 0.1008 | 0.1616 | 0.2727 | 0.0472 | 0.1208 | 0.1544 | 0.0429 | 0.1027 | 0.0606 | ||||

| OHLV | 0.0868 | 0.1747 | 0.1881 | 0.0525 | 0.1397 | 0.1304 | 0.0447 | 0.0493 | 0.0620 | ||||

| OHLMVC | 0.1114 | 0.2308 | 0.2130 | 0.0434 | 0.1452 | 0.1567 | 0.0400 | 0.0531 | 0.0560 | ||||

| 21 days | Adam | MV | 0.1697 | 0.1928 | 0.3751 | 0.0828 | 0.1555 | 0.0897 | 0.0414 | 0.0603 | 0.2791 | ||

| MVC | 0.2673 | 0.4012 | 0.4062 | 0.0699 | 0.0929 | 0.1394 | 0.0457 | 0.0770 | 0.0484 | ||||

| OHLV | 0.1753 | 0.3138 | 0.2623 | 0.0582 | 0.1157 | 0.1363 | 0.0406 | 0.0417 | 0.0483 | ||||

| OHLMVC | 0.2692 | 0.4271 | 0.4016 | 0.0546 | 0.1249 | 0.0928 | 0.0396 | 0.0412 | 0.0350 | ||||

| RMSProp | MV | 0.3389 | 0.2637 | 0.1844 | 0.1218 | 0.1333 | 0.1993 | 0.0424 | 0.0859 | 0.0633 | |||

| MVC | 0.2507 | 0.2386 | 0.2320 | 0.0980 | 0.0982 | 0.2102 | 0.0535 | 0.1073 | 0.0969 | ||||

| OHLV | 0.2850 | 0.1612 | 0.3277 | 0.0990 | 0.1096 | 0.2077 | 0.0547 | 0.3192 | 0.0671 | ||||

| OHLMVC | 0.1878 | 0.3017 | 0.3532 | 0.1293 | 0.1242 | 0.2014 | 0.1280 | 0.0476 | 0.0810 | ||||

| 42 days | Adam | MV | 0.1471 | 0.4368 | 0.3548 | 0.1859 | 0.2023 | 0.1943 | 0.0415 | 0.0648 | 0.0476 | ||

| MVC | 0.1884 | 0.2731 | 0.2670 | 0.0921 | 0.1885 | 0.1613 | 0.0616 | 0.3178 | 0.0592 | ||||

| OHLV | 0.1539 | 0.2643 | 0.1849 | 0.1104 | 0.2039 | 0.1443 | 0.0394 | 0.0725 | 0.0557 | ||||

| OHLMVC | 0.2555 | 0.3332 | 0.3816 | 0.0785 | 0.1707 | 0.1935 | 0.0406 | 0.0543 | 0.0753 | ||||

| RMSProp | MV | 0.2048 | 0.4303 | 0.3616 | 0.0904 | 0.2019 | 0.1691 | 0.0473 | 0.1037 | 0.0786 | |||

| MVC | 0.2602 | 0.5322 | 0.2999 | 0.0744 | 0.1889 | 0.2186 | 0.0445 | 0.3711 | 0.0873 | ||||

| OHLV | 0.2904 | 0.5606 | 0.3259 | 0.0628 | 0.2044 | 0.1510 | 0.3172 | 0.0683 | 0.0493 | ||||

| OHLMVC | 0.2310 | 0.3181 | 0.2358 | 0.0622 | 0.1973 | 0.2204 | 0.0417 | 0.0531 | 0.0657 | ||||

| Look-Back Period | Metric | Model | One-Time-Step Prediction | Five-Time-Step Prediction | |||||

|---|---|---|---|---|---|---|---|---|---|

| DAX | DOW | S&P500 | DAX | DOW | S&P500 | ||||

| 5 days | MSE | RNN | 0.1738 | 0.3059 | 0.1043 | 0.0250 | 0.0219 | 0.1122 | |

| LSTM | 0.1735 | 0.3060 | 0.1043 | 0.0058 | 0.0076 | 0.0064 | |||

| GRU | 0.1735 | 0.3060 | 0.1043 | 0.0081 | 0.0187 | 0.0058 | |||

| WaveNet | 0.4870 | 0.3120 | 0.5712 | 0.0477 | 0.1230 | 0.0177 | |||

| CNN-LSTM | 0.1435 | 0.0560 | 0.0988 | 0.0831 | 0.0447 | 0.0912 | |||

| GRU-CNN | 0.0370 | 0.3060 | 0.0053 | 0.0101 | 0.0166 | 0.0090 | |||

| Ensemble | 0.0017 | 0.0051 | 0.0027 | 0.0126 | 0.0122 | 0.0057 | |||

| MAE | RNN | 0.3738 | 0.5163 | 0.2934 | 0.1468 | 0.1266 | 0.3053 | ||

| LSTM | 0.3726 | 0.5165 | 0.2934 | 0.0593 | 0.0640 | 0.0585 | |||

| GRU | 0.3727 | 0.5164 | 0.2934 | 0.0802 | 0.1251 | 0.0629 | |||

| WaveNet | 0.6741 | 0.5185 | 0.7456 | 0.1925 | 0.3177 | 0.1110 | |||

| CNN-LSTM | 0.3440 | 0.1587 | 0.2864 | 0.2345 | 0.1551 | 0.2666 | |||

| GRU-CNN | 0.1733 | 0.5165 | 0.0557 | 0.0901 | 0.1139 | 0.0739 | |||

| Ensemble | 0.0345 | 0.0628 | 0.0420 | 0.1025 | 0.0968 | 0.0605 | |||

| 21 days | MSE | RNN | 0.1787 | 0.3315 | 0.0995 | 0.1917 | 0.3485 | 0.1081 | |

| LSTM | 0.1785 | 0.3315 | 0.0995 | 0.0133 | 0.0070 | 0.0060 | |||

| GRU | 0.1785 | 0.3315 | 0.0995 | 0.0126 | 0.0155 | 0.0056 | |||

| WaveNet | 0.4126 | 0.2232 | 0.5259 | 0.0526 | 0.1446 | 0.0177 | |||

| CNN-LSTM | 0.0805 | 0.0225 | 0.0680 | 0.0399 | 0.0127 | 0.0595 | |||

| GRU-CNN | 0.0159 | 0.0307 | 0.0058 | 0.0245 | 0.0127 | 0.0079 | |||

| Ensemble | 0.0018 | 0.0128 | 0.0026 | 0.0115 | 0.0124 | 0.0059 | |||

| MAE | RNN | 0.3947 | 0.5588 | 0.2950 | 0.4151 | 0.5807 | 0.3127 | ||

| LSTM | 0.3940 | 0.5588 | 0.2950 | 0.1019 | 0.0645 | 0.0625 | |||

| GRU | 0.3940 | 0.5587 | 0.2950 | 0.1032 | 0.1121 | 0.0634 | |||

| WaveNet | 0.6244 | 0.4501 | 0.7168 | 0.2015 | 0.3605 | 0.1094 | |||

| CNN-LSTM | 0.2490 | 0.1076 | 0.2367 | 0.1460 | 0.0808 | 0.2231 | |||

| GRU-CNN | 0.1133 | 0.1626 | 0.0634 | 0.1429 | 0.0994 | 0.0678 | |||

| Ensemble | 0.0358 | 0.1027 | 0.0402 | 0.0966 | 0.0980 | 0.0650 | |||

| 42 days | MSE | RNN | 0.2434 | 0.4011 | 0.1446 | 0.0481 | 0.0071 | 0.1150 | |

| LSTM | 0.2434 | 0.4011 | 0.1446 | 0.0071 | 0.0040 | 0.0066 | |||

| GRU | 0.2434 | 0.4011 | 0.1446 | 0.0079 | 0.0122 | 0.0044 | |||

| WaveNet | 0.3106 | 0.1505 | 0.4595 | 0.0685 | 0.1746 | 0.0215 | |||

| CNN-LSTM | 0.0435 | 0.0027 | 0.0433 | 0.0115 | 0.0033 | 0.0597 | |||

| GRU-CNN | 0.0425 | 0.4011 | 0.0092 | 0.0351 | 0.0261 | 0.0075 | |||

| Ensemble | 0.0028 | 0.0057 | 0.0024 | 0.0092 | 0.0079 | 0.0083 | |||

| MAE | RNN | 0.4857 | 0.6314 | 0.3694 | 0.2009 | 0.0693 | 0.3288 | ||

| LSTM | 0.4857 | 0.6314 | 0.3694 | 0.0668 | 0.0517 | 0.0643 | |||

| GRU | 0.4857 | 0.6314 | 0.3694 | 0.0768 | 0.0985 | 0.0548 | |||

| WaveNet | 0.5511 | 0.3843 | 0.6730 | 0.2488 | 0.4143 | 0.1246 | |||

| CNN-LSTM | 0.1961 | 0.0456 | 0.1878 | 0.0847 | 0.0472 | 0.2295 | |||

| GRU-CNN | 0.2030 | 0.6314 | 0.0878 | 0.1805 | 0.1358 | 0.0711 | |||

| Ensemble | 0.0476 | 0.0693 | 0.0414 | 0.0846 | 0.0771 | 0.0778 | |||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Song, H.; Choi, H. Forecasting Stock Market Indices Using the Recurrent Neural Network Based Hybrid Models: CNN-LSTM, GRU-CNN, and Ensemble Models. Appl. Sci. 2023, 13, 4644. https://doi.org/10.3390/app13074644

Song H, Choi H. Forecasting Stock Market Indices Using the Recurrent Neural Network Based Hybrid Models: CNN-LSTM, GRU-CNN, and Ensemble Models. Applied Sciences. 2023; 13(7):4644. https://doi.org/10.3390/app13074644

Chicago/Turabian StyleSong, Hyunsun, and Hyunjun Choi. 2023. "Forecasting Stock Market Indices Using the Recurrent Neural Network Based Hybrid Models: CNN-LSTM, GRU-CNN, and Ensemble Models" Applied Sciences 13, no. 7: 4644. https://doi.org/10.3390/app13074644