Japan’s Corporate Governance Transformation: Convergence or Reconfiguration?

{kind=link}

{kind=link}

Abstract

:1. Introduction

2. Governance, Economic Inefficiencies and Corporate Scandals

2.1. Corporate Governance in Japan, a Primer

2.2. Corporate Governance Inadequacies and the First “Lost Decade” (1990–2000)

2.2.1. Capital Structure of Japanese Firms and Non-Performing Loan

2.2.2. Ineffective Board of Directors Monitoring

2.2.3. Japanese Corporate Governance Performance vs. the Rest of the World

2.3. Governance and Corporate Scandals during the 2010s

2.3.1. Japanese Corporate Culture

2.3.2. The Olympus and Toshiba Cases

2.3.3. Corporate Governance Failures

3. Governance Reforms in Japan toward a Global Convergence?

3.1. Japan’s Recent Corporate Governance Evolution

3.1.1. A Wave of Corporate Governance Reforms and a Shift of Influence

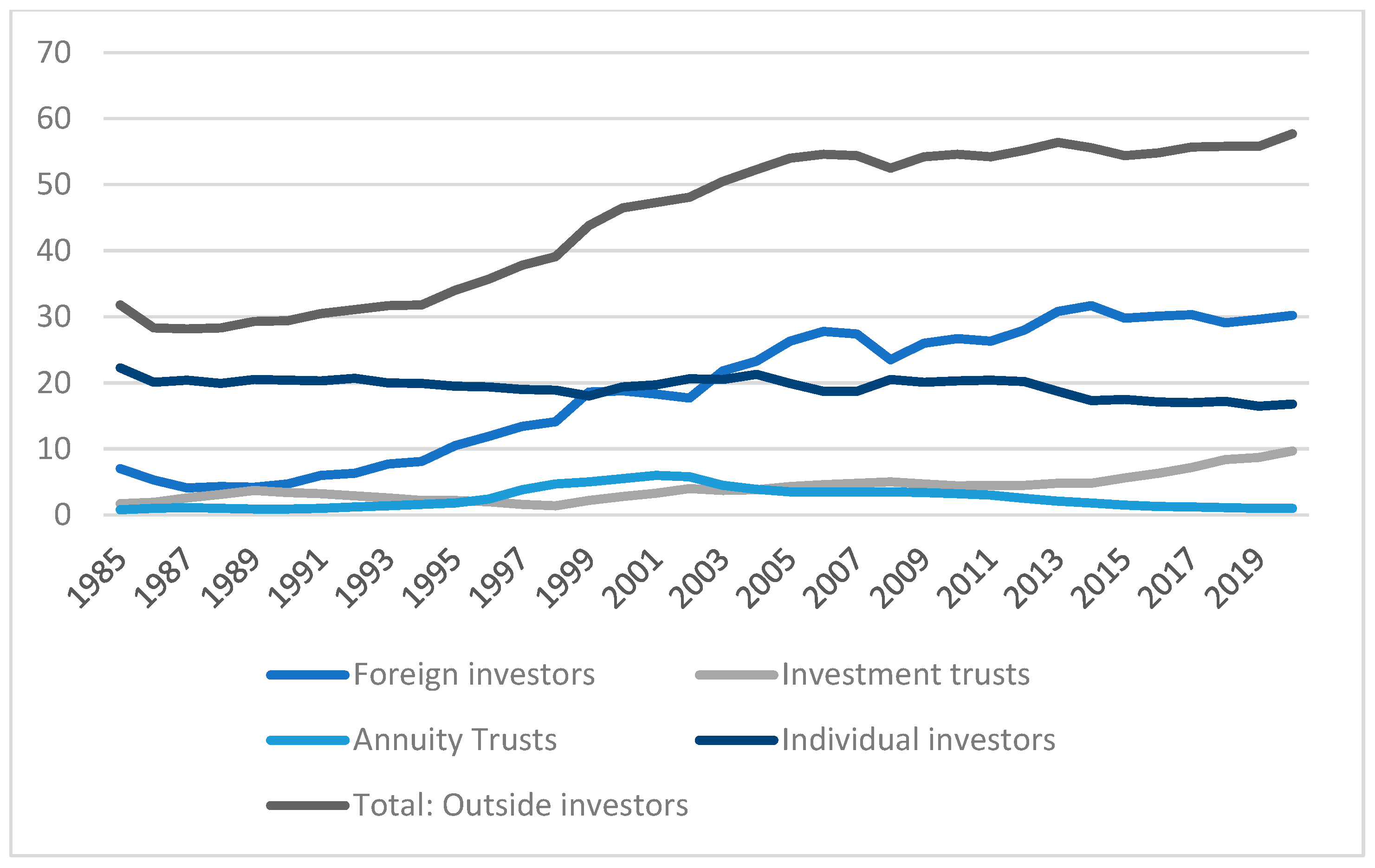

3.1.2. Ownership Structure in Japan

3.1.3. A Push toward More Independence on Boards of Directors

3.2. Limited and Difficult Compliance with International Standards

3.2.1. A Persistent Differentiation on Corporate Governance Understanding

3.2.2. Arising New Difficulties: Executive Remuneration

4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Aguilera, Ruth V., and Ilir Haxhi. 2019. Comparative Corporate Governance in Emerging Markets. In The Oxford Handbook of Management in Emerging Markets. Edited by Robert Grosse and Klaus K. Meyer. New York: Oxford University Press, pp. 185–218. [Google Scholar]

- Allen, Mike. 2022. Narrative Literature Review. In The SAGE Encyclopedia of Communication Research Methods. Thousand Oaks: SAGE Publications, Inc., pp. 1–4. [Google Scholar] [CrossRef]

- Aoki, Masahiko. 1988. Information, Incentives, and Bargaining in the Japanese Economy, 1. paperback ed. Repr. Cambridge: Cambridge University Press. [Google Scholar]

- Aoki, Masahiko. 2001. Toward a Comparative Institutional Analysis. Comparative Institutional Analysis. Cambridge: MIT Press. [Google Scholar]

- Aoki, Masahiko, and Ronald Dore, eds. 1994. The Japanese Firm: The Sources of Competitive Strength. Oxford and New York: Oxford University Press. [Google Scholar]

- Aoki, Masahiko, Gregory Jackson, and Hideaki Miyajima, eds. 2007. Corporate Governance in Japan: Institutional Change and Organizational Diversity. Oxford and New York: Oxford University Press. [Google Scholar]

- Aronson, Bruce, and Joongi Kim, eds. 2019. Corporate Governance in Asia: A Comparative Approach. Cambridge: Cambridge University Press. [Google Scholar]

- Ballon, Robert J., and Iwao Tomita. 1989. Financial Behavior of Japanese Corporations. New York: Kodansha America. [Google Scholar]

- Bauer, Rob, Bart Frijns, Rogér Otten, and Alireza Tourani-Rad. 2008. The Impact of Corporate Governance on Corporate Performance: Evidence from Japan. Pacific-Basin Finance Journal 16: 236–51. [Google Scholar] [CrossRef]

- Bauer, Rob, Nadja Guenster, and Rogér Otten. 2004. Empirical Evidence on Corporate Governance in Europe: The Effect on Stock Returns, Firm Value and Performance. Journal of Asset Management 5: 91–104. [Google Scholar] [CrossRef]

- Bollinger, Sophie Raedersdorf. 2020. Creativity and Forms of Managerial Control in Innovation Processes: Tools, Viewpoints and Practices. European Journal of Innovation Management 23: 214–29. [Google Scholar] [CrossRef]

- Borah, Nilakshi, and Hui James. 2020. Board Leadership Structure and Corporate Headquarters Location. Journal of Economics and Finance 44: 35–58. [Google Scholar] [CrossRef]

- Boyer, Robert. 2014. From ‘Japanophilia’ to Indifference? Three Decades of Research on Contemporary Japan. In The Great Transformation of Japanese Capitalism. Edited by Sebastien Lechevalier. Nissan Institute/Routledge Japanese Studies. London: Routledge, pp. xii, xxv. [Google Scholar]

- Boyer, Robert, Hiroyasu Uemura, and Akinori Isogai. 2012. Diversity and Transformations of Asian Capitalisms. Abingdon and New York: Routledge. [Google Scholar]

- Bozec, Richard, and Yves Bozec. 2012. The Use of Governance Indexes in the Governance-Performance Relationship Literature: International Evidence: The Use of Governance Indexes in the Governance-Performance. Canadian Journal of Administrative Sciences/Revue Canadienne Des Sciences de l’Administration 29: 79–98. [Google Scholar] [CrossRef]

- Brown, J. Owen, Jerry Hays, and Martin T. Stuebs Jr. 2016. Modeling Accountant Whistleblowing Intentions: Applying the Theory of Planned Behavior and the Fraud Triangle. Accounting & The Public Interest 16: 28–56. [Google Scholar] [CrossRef]

- Burger-Helmchen, Thierry, and Erica J. Siegel. 2020. Some Thoughts On CSR in Relation to B Corp Labels. Entrepreneurship Research Journal 10: 20200231. [Google Scholar] [CrossRef]

- Carney, Michael, Marc Van Essen, Saul Estrin, and Daniel Shapiro. 2018. Business Groups Reconsidered: Beyond Paragons and Parasites. Academy of Management Perspectives 32: 493–516. [Google Scholar] [CrossRef]

- Carraz, Rene, and Yuko Harayama. 2019. Japan’s Innovation Systems at the Crossroads: Society 5.0. In Panorama: Insights into Asian and European Affairs. Singapore: Konrad-Adenauer-Stiftung e.V., pp. 33–45. [Google Scholar]

- Cernat, Lucian. 2004. The Emerging European Corporate Governance Model: Anglo-Saxon, Continental, or Still the Century of Diversity? Journal of European Public Policy 11: 147–66. [Google Scholar] [CrossRef]

- Dicko, Saidatou. 2020. Does Ownership Structure Influence the Relationship between Firms’ Political Connections and Financial Performance? International Journal of Corporate Governance 11: 47–75. [Google Scholar] [CrossRef]

- Dinh, Trung Quang, and Andrea Calabrò. 2019. Asian Family Firms through Corporate Governance and Institutions: A Systematic Review of the Literature and Agenda for Future Research. International Journal of Management Reviews 21: 50–75. [Google Scholar] [CrossRef]

- Dore, Ronald. 1998. Asian Crisis and the Future of the Japanese Model. Cambridge Journal of Economics 22: 773. [Google Scholar] [CrossRef]

- Dore, Ronald. 2005. Deviant or Different? Corporate Governance in Japan and Germany. Corporate Governance: An International Review 13: 437–46. [Google Scholar] [CrossRef]

- Dutta, Saurav K., and Raef Lawson. 2018. Accouting Fraud at Japanese Companies: Ethical and Governance Failings Have Contributed to a Large Outbreak of Corporate Scandals in Japan. Strategic Finance 11: 40–47. [Google Scholar]

- El-Helaly, Moataz, Nermeen F. Shehata, and Reem El-Sherif. 2018. National Corporate Governance, GMI Ratings and Earnings Management. Asian Review of Accounting 26: 373–90. [Google Scholar] [CrossRef]

- Feils, Dorothee, Manzur Rahman, and Florin Şabac. 2018. Corporate Governance Systems Diversity: A Coasian Perspective on Stakeholder Rights. Journal of Business Ethics 150: 451–66. [Google Scholar] [CrossRef]

- Fukao, Mitsuhiro. 2003. Japan’s Lost Decade and Its Financial System. World Economy 26: 365–84. [Google Scholar] [CrossRef]

- Gedajlovic, Eric, and Daniel M. Shapiro. 2002. Ownership Structure and Firm Profitability in Japan. Academy of Management Journal 45: 565–75. [Google Scholar] [CrossRef]

- Gilson, Ronald J., and Curtis J. Milhaupt. 2005. Choice as Regulatory Reform: The Case of Japanese Corporate Governance. The American Journal of Comparative Law 53: 343–77. [Google Scholar] [CrossRef]

- Gordon, A. 1998. The Wages of Affluence: Labor and Management in Postwar Japan. Cambridge: Harvard University Press. [Google Scholar]

- Guimtrandy, Fabien, and Thierry Burger-Helmchen. 2022. The Pitch: Some Face-to-Face Minutes to Build Trust. Administrative Sciences 12: 47. [Google Scholar] [CrossRef]

- Hamza, Taher, and Nada Mselmi. 2017. Corporate Governance and Equity Prices: The Effect of Board of Directors and Audit Committee Independence. Gobierno Corporativo y Precios de Las Acciones: Efecto de La Independencia de La Consejo de Administración y El Comité de Auditoría 21: 152–64. [Google Scholar] [CrossRef]

- Hayashi, Mizuki. 2013. Corporate Ownership and Governance Reforms in Japan: Influence of Globalization and U.s. Practice. Columbia Journal of Asian Law 26: 315–45. [Google Scholar]

- Hirota, Shinichi, Katsuyuki Kubo, Hideaki Miyajima, Paul Hong, and Young Won Park. 2010. Corporate Mission, Corporate Policies and Business Outcomes: Evidence from Japan. Management Decision 48: 1134–53. [Google Scholar] [CrossRef]

- Holroyd, Carin. 2022. Technological Innovation and Building a ‘Super Smart’ Society: Japan’s Vision of Society 5.0. Journal of Asian Public Policy 15: 18–31. [Google Scholar] [CrossRef]

- Hoshi, Takeo, and Anil Kashyap. 2001. Corporate Financing and Governance in Japan: The Road to the Future. Cambridge: The MIT Press. [Google Scholar]

- Jiang, Huiqin. 2019. The Positions of the Stock Exchanges towards Listing with the Weighted Voting Rights Structure: A Comparative Study. Paper presented at the Corporate Law Teachers Association’ Conference, Auckland, New Zealand, February 3–5. [Google Scholar]

- Kato, Kazuo, Meng Li, and Douglas J. Skinner. 2017. Is Japan Really a ‘Buy’? The Corporate Governance, Cash Holdings and Economic Performance of Japanese Companies. Journal of Business Finance & Accounting 44: 480–523. [Google Scholar] [CrossRef]

- Kato, Takao, and Katsuyuki Kubo. 2006. CEO Compensation and Firm Performance in Japan: Evidence from New Panel Data on Individual CEO Pay. Journal of the Japanese and International Economies 20: 1–19. [Google Scholar] [CrossRef]

- Kimura, Takuma, and Mizuki Nishikawa. 2018. Ethical Leadership and Its Cultural and Institutional Context: An Empirical Study in Japan. Journal of Business Ethics 151: 707–24. [Google Scholar] [CrossRef]

- Kinchin, Ian M., and Paulo R. M. Correia. 2021. Visualizing the Complexity of Knowledges to Support the Professional Development of University Teaching. Knowledge 1: 52–60. [Google Scholar] [CrossRef]

- Krause, Ryan, Michael C. Withers, and Matthew Semadeni. 2017. Compromise on the Board: Investigating the Antecedents and Consequences of Lead Independent Director Appointment. Academy of Management Journal 60: 2239–65. [Google Scholar] [CrossRef]

- Le Corre, Jean-Yves, and Thierry Burger-Helmchen. 2021a. Rethinking Managerial Control in the Contemporary Context. In Integrated Science. Edited by Nima Rezaie. Berlin and Heidelberg: Springer, pp. 419–38. [Google Scholar]

- Le Corre, Jean-Yves, and Thierry Burger-Helmchen. 2021b. Rethinking Managerial Control in the Contemporary Context: What Can We Learn from Recent Chinese Indigenous Management Research? In Engines of Economic Prosperity: Creating Innovation and Economic Opportunities through Entrepreneurship. Edited by Meltem Ince-Yenilmez and Burak Darici. London: Palgrave MacMillan, pp. 303–21. [Google Scholar]

- Le Corre, Jean-Yves, and Thierry Burger-Helmchen. 2022. Managerial Control in an Online Constructivist Learning Environment: A Teacher’s Perspective. Knowledge 2: 572–86. [Google Scholar] [CrossRef]

- Lee, Pey-Woan. 2003. Serving Two Masters—The Dual Loyalties of the Nominee Director in Corporate Groups. Journal of Business Law 9: 449. [Google Scholar]

- Lechevalier, Sébastien. 2014. The Great Transformation of Japanese Capitalism. Nissan Institute/Routledge Japanese Studies. London: Routledge. [Google Scholar]

- Limpaphayom, Piman, Daniel A. Rogers, and Noriyoshi Yanase. 2019. Bank Equity Ownership and Corporate Hedging: Evidence from Japan. Journal of Corporate Finance 58: 765–83. [Google Scholar] [CrossRef]

- Litt, David G. 2015. Japan’s New Corporate Governance Code: Outside Directors Find a Role Under ‘Abenomics’. Corporate Governance Advisor 23: 19–23. [Google Scholar]

- Luo, Qi, and Toyohiko Hachiya. 2005. Corporate Governance, Cash Holdings, and Firm Value:: Evidence from Japan. Review of Pacific Basin Financial Markets & Policies 8: 613–36. [Google Scholar] [CrossRef]

- Miwa, Yoshiro, and J. Mark Ramseyer. 2002. Banks and Economic Growth: Implications from Japanese History. The Journal of Law and Economics 45: 127–64. [Google Scholar] [CrossRef]

- Morck, Randall, and Masao Nakamura. 1999. Banks and Corporate Control in Japan. The Journal of Finance 54: 319–39. [Google Scholar] [CrossRef]

- Morck, Randall, Masao Nakamura, and M. Frank. 2001. Japanese Corporate Governance and Macroeconomic Problems. In The Japanese Business and Economic System. Edited by M. Nakamura. London: Palgrave Macmillan, pp. 325–63. [Google Scholar]

- Nakamura, Masao. 2015. Economic Development and Business Groups in Asia: Japan’s Experience and Implications. International Advances in Economic Research 21: 81–103. [Google Scholar] [CrossRef]

- Nakashima, Masumi. 2017. Can The Fraud Triangle Predict Accounting Fraud? Evidence from Japan 2017. Paper present at the 8th International Conference of the Japanese Accounting Review, Kobe, Japan, January 6. [Google Scholar]

- Neukam, Marion, and Sophie Bollinger. 2022. Encouraging Creative Teams to Integrate a Sustainable Approach to Technology. Journal of Business Research 150: 354–64. [Google Scholar] [CrossRef]

- Nguyen, Pascal, and Nahid Rahman. 2020. Institutional Ownership, Cross-shareholdings and Corporate Cash Reserves in Japan. Accounting & Finance 60: 1175–207. [Google Scholar] [CrossRef]

- Nonaka, Ikujiro, and Hiro Takeuchi. 1995. The Knowledge-Creating Company: How Japanese Companies Create the Dynamics of Innovation. Oxford: Oxford University Press Inc. [Google Scholar]

- Nonaka, Ikujiro, and Hiro Takeuchi. 2019. The Wise Company: How Companies Create Continuous Innovation. Oxford: Oxford University Press. [Google Scholar]

- Nozaki, Hironari. 2021. Chiiki Kinyu No Yukue (Outlook of Regional Finance), Keizai Kyoshitsu. Nikkei Newspaper, December 27. [Google Scholar]

- Numata, Shingo, and Fumiko Takeda. 2010. Stock Market Reactions to Audit Failure in Japan: The Case of Kanebo and ChuoAoyama. International Journal of Accounting (World Scientific Publishing Company) 45: 175–99. [Google Scholar] [CrossRef]

- Ogawa, Alicia. 2017. Toshiba and the Myth of Corporate Governance. Columbian Business School Working Paper. New York: Center on Japanese Economy and Business. [Google Scholar]

- Okumura, Ariyoshi. 2004. A Japanese View on Corporate Governance. Corporate Governance: An International Review 12: 3–4. [Google Scholar] [CrossRef]

- Olympus Corporation. 2011. Olympus Corporation Third Party Committee, 2011. Investigation Report. Available online: https://www.olympus-global.com/ (accessed on 2 February 2023).

- Passador, Maria Lucia. 2016. Corporate Governance Models: The Japanese Experience in Context. DePaul Business & Commercial Law Journal 15: 25–53. [Google Scholar]

- Pozen, Robert C. 2018. Carlos Ghosn, Nissan, and the Need for Stronger Corporate Governance in Japan. Harvard Business Review Digital Articles 12: 1–6. [Google Scholar]

- Schembera, Stefan, Patrick Haack, and Andreas Georg Scherer. 2023. From Compliance to Progress: A Sensemaking Perspective on the Governance of Corruption. Organization Science 34: 1184–215. [Google Scholar] [CrossRef]

- Semba, Hu Dan, and Ryo Kato. 2019. Does Big N Matter for Audit Quality? Evidence from Japan. Asian Review of Accounting 27: 2–28. [Google Scholar] [CrossRef]

- Shoji, Kaori. 2018. Hyoe Yamamoto Dives into Japan’s Culture of Corporate Corruption in ‘Samurai and Idiots: The Olympus Affair’. The Japan Times. May 16. Available online: https://www.japantimes.co.jp/culture/2018/05/16/films/hyoe-yamamoto-dives-japans-culture-corporate-corruption-samurai-idiots-olympus-affair/ (accessed on 2 February 2023.).

- Skinner, Douglas J., and Suraj Srinivasan. 2012. Audit Quality and Auditor Reputation: Evidence from Japan. Accounting Review 87: 1737–65. [Google Scholar] [CrossRef]

- Songini, Lucrezia, and Luca Gnan. 2015. Family Involvement and Agency Cost Control Mechanisms in Family Small and Medium-Sized Enterprises. Journal of Small Business Management 53: 748–79. [Google Scholar] [CrossRef]

- Tasawar, Anam, and Mian Sajid Nazir. 2019. The Nexus between Effective Corporate Monitoring and CEO Compensation. International Journal of Corporate Governance 10: 81–94. [Google Scholar] [CrossRef]

- Tetsuhiro, Kishita. 2013. Corporate Governance in Established Japanese Firms: Will the Olympus Scandal Happen Again? Journal of Enterprising Culture 21: 421–46. [Google Scholar] [CrossRef]

- Tokyo Stock Exchange. 2018. Japan’s Corporate Governance Code Seeking Sustainable Corporate Growth and Increased Corporate Value over the Mid- to Long-Term. Tokyo: Tokyo Stock Exchange. [Google Scholar]

- Tokyo Stock Exchange. 2019. White Paper on Corporate Governance. Tokyo: Tokyo Stock Exchange. [Google Scholar]

- Vig, Shinu, and Manipadma Datta. 2018. Reviewing and Revisiting the Use of Corporate Governance Indices. International Journal of Corporate Governance 9: 227–41. [Google Scholar] [CrossRef]

- Yoshimori, Masaru. 2005. Does Corporate Governance Matter? Why the Corporate Performance of Toyota and Canon Is Superior to GM and Xerox. Corporate Governance: An International Review 13: 447–57. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Renou, T.; Carraz, R.; Burger-Helmchen, T. Japan’s Corporate Governance Transformation: Convergence or Reconfiguration? Adm. Sci. 2023, 13, 141. https://doi.org/10.3390/admsci13060141

Renou T, Carraz R, Burger-Helmchen T. Japan’s Corporate Governance Transformation: Convergence or Reconfiguration? Administrative Sciences. 2023; 13(6):141. https://doi.org/10.3390/admsci13060141

Chicago/Turabian StyleRenou, Theo, René Carraz, and Thierry Burger-Helmchen. 2023. "Japan’s Corporate Governance Transformation: Convergence or Reconfiguration?" Administrative Sciences 13, no. 6: 141. https://doi.org/10.3390/admsci13060141