Fifteen Years of Accounting Professional’s Competencies Supply and Demand: Evidencing Actors, Competency Assessment Strategies, and ‘Top Three’ Competencies

Abstract

:1. Introduction

- Which actors of the competencies’ supply–demand relationship have been identified in literature?

- Which strategies are used in the literature to assess the competencies’ supply and demand?

- What competencies have been studied over the last 15 years?

- What is the recent competencies’ supply–demand convergence?

2. Methodology

2.1. Article Collection

2.2. Data Collection

3. Results and Discussion

3.1. Competency Assessment

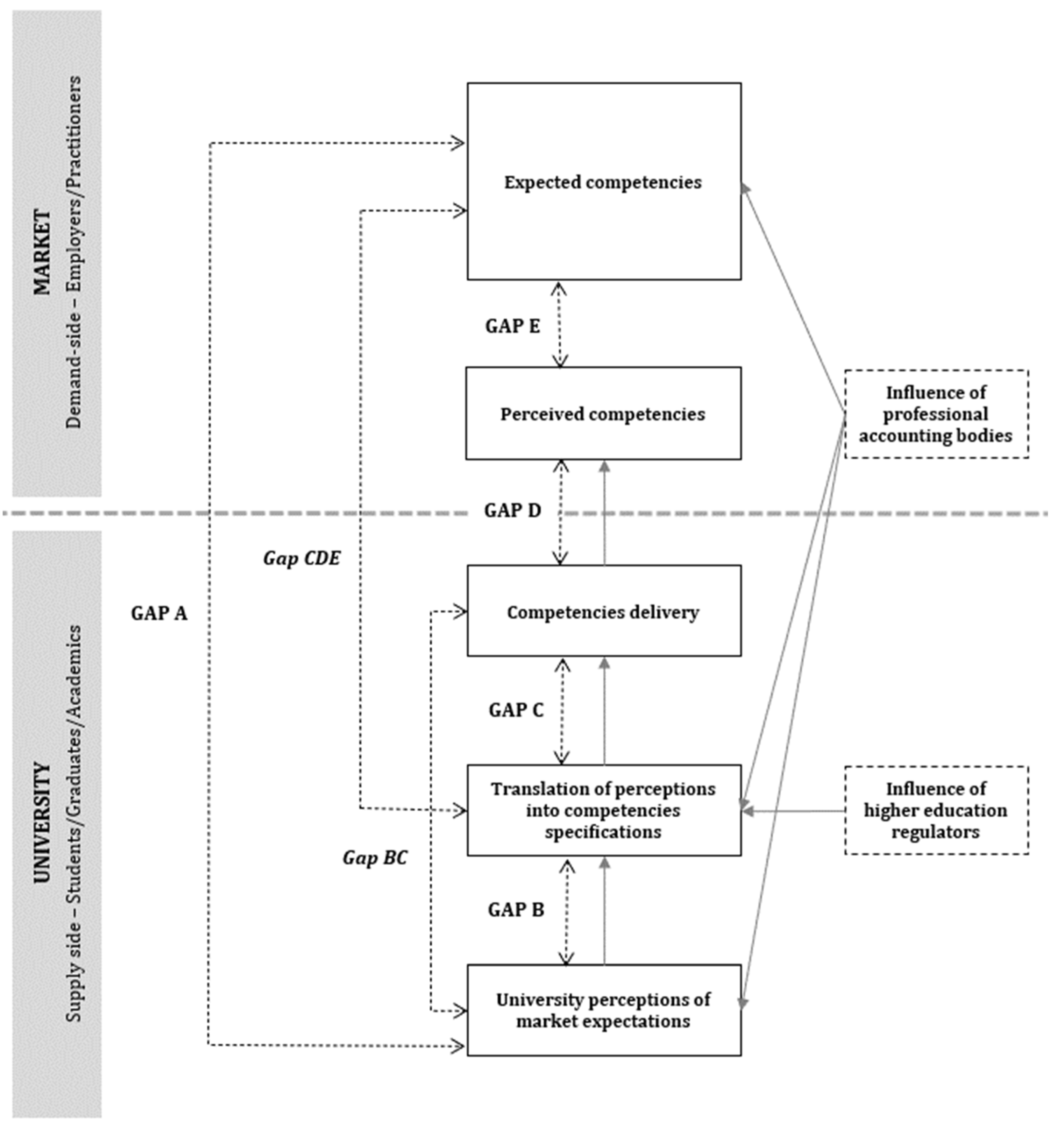

3.1.1. The Actors of the Market–University Relationship

3.1.2. Competency Assessment Perspectives

3.1.3. Perception vs. Existence

3.1.4. Competency Assessment: A Joint Analysis

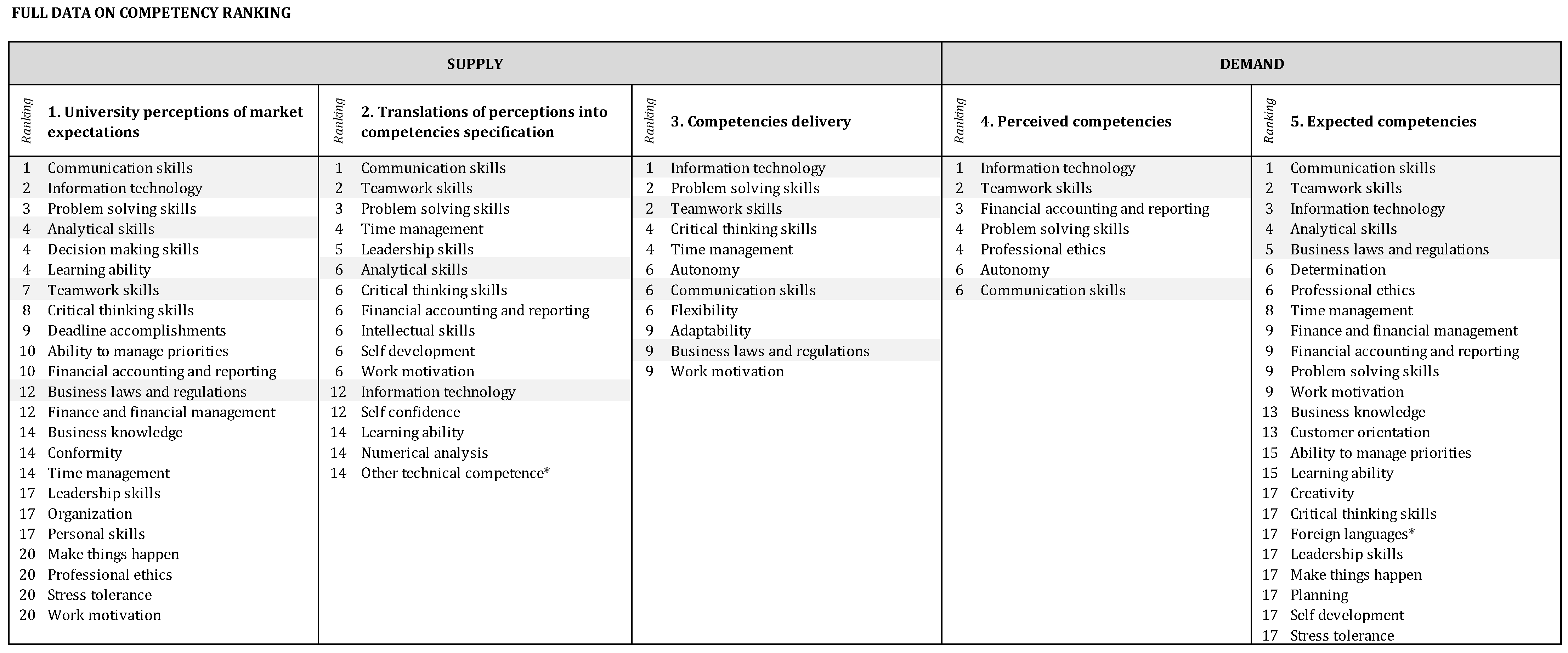

3.2. Competencies

3.2.1. Competency Categories

3.2.2. Competencies Supply and Demand Convergence

4. Conclusions, Limitations, and Future Research Suggestions

- Expanding the number of articles focusing on the fit between demand and supply, as these represent only about 9% of the articles found. This focus can help in locating gaps to overcome them then;

- To continue the study of information technology competencies. The continuous technological evolution has made digital competencies widely studied over the years. Even so, and because this evolution is still ongoing, this competency should continue to deserve the attention of researchers (Banasik and Jubb 2021; Daff 2021; Waller and Gallun 1985);

- To explore each component (actors, perspectives, constructs, and gaps) of the Kroon and Alves (2022) framework to analyze the convergence of specific competencies or contexts.

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Unit of Analysis | Unit of Observation | Frequency |

| Students | accounting sciences students; accounting students; accounting undergraduates; students; undergraduate chartered accountancy students; undergraduate students; university students | 51 |

| Graduates | accounting graduates; CIMA trainees; graduates; ICAS trainees; newly graduated students; university graduates | 16 |

| Academics | academic staff; academics; accounting academics; accounting educators; accounting faculty; accounting lecturers; accounting teachers; department chairs; educators; faculty; lecturers; professors; teachers; university accounting educators; university educators; university professors; university teachers | 41 |

| Employers | accounting employers; accounting firms; audit managers; CFO; employers; human resource and branch managers; human resource managers from accounting firms; practitioner employers; recruiters; recruitment managers from auditing firms; staff of federal parastatals; * practicing chartered accountants; * practitioners; * professional accountants; * public accountants | 56 |

| Practitioners | accountants; accounting practitioners; accounting professionals; auditors; business professionals; external auditors; finance consultants; financial managers; graduates who were between three to five years out from graduation; management accountants; managerial accounting personnel; organizations undergoing RPA implementations; practicing chartered accountants; practicing forensic auditors; practicing accountants; practicing forensic professionals; practitioners; professionals; public accountants; records management professionals, information and communication technology (ICT) professionals, and auditors; senior and junior tax practitioners; senior trainees, managers, and partners; small and micro enterprises and IT companies managers; top managers | 56 |

| Others | judiciary; professional bodies | 2 |

Appendix B

| IES 2 Technical Competence | Competencies |

| Technical competencies as provided in IES 2 | audit and assurance; |

| business and organizational environment; | |

| business laws and regulations; | |

| business strategy and management; | |

| economics; | |

| finance and financial management; | |

| financial accounting and reporting; | |

| governance, risk management, and internal control; | |

| information technology; | |

| management accounting; | |

| taxation. | |

| Technical competencies not provided in IES 2 | administrative and secretarial activities; |

| foreign languages; | |

| human resource management. | |

| IES 3 Professional skills | Competencies |

| Intellectual | analytical skills; critical-thinking skills; decision-making skills; numerical analysis; problem-solving skills. |

| Interpersonal and communication skills | communication skills; empathy; interpersonal skills; negotiation; persuasion; teamwork skills. |

| Organizational skills | ability to manage priorities; attendance and punctuality; business knowledge; customer orientation; employee development; leadership skills; make things happen; organizational sensitivity; planning and organization; strategic vision. |

| Personal | adaptability; ambition; attention to detail; autonomy; conformity; creativity; determination; energy; flexibility; humility; initiative; innovation; learning ability; proactivity; rationalization; resilience; results orientation; rigor; self confidence; self development; stress tolerance; tenacity; work motivation. |

| IES 4 Professional values, ethics, and attitudes | Competencies |

| Commitment to the public interest | professional ethics; independence; integrity; responsibility; confidentiality and discretion. |

| Ethical principles | |

| Professional skepticism and professional judgment |

Appendix C

References

- Abayadeera, Nadana, and Kim Watty. 2014. The expectation-performance gap in generic skills in accounting graduates. Asian Review of Accounting 22: 56–72. [Google Scholar] [CrossRef]

- Abayadeera, Nadana, and Kim Watty. 2016. Generic skills in accounting education in a developing country: Exploratory evidence from Sri Lanka. Asian Review of Accounting 24: 149–70. [Google Scholar] [CrossRef]

- Abdul Latif, Nurul Ezhawati, Faizal Mohamed Yusuf, Nurazrin Mat Tarmezi, Siti Zalika Rosly, and Zairul Nurshazana Zainuddin. 2019. The Application of Critical Thinking in Accounting Education: A Literature Review. International Journal of Higher Education 8: 57. [Google Scholar] [CrossRef]

- Adhariani, Desi. 2020. The influence of the ASEAN economic community on the future of the management accounting profession. Meditari Accountancy Research 28: 587–611. [Google Scholar] [CrossRef]

- Adhariani, Desi, Sylvia Siregar, and Rini Yulius. 2019. Borderless with uinequal opportunity? Experts’ perspectives on the ASEAN Economic Community and impact on Indonesian accountant profession. The Qualitative Report 24: 1147–67. [Google Scholar] [CrossRef]

- Agrawal, Prerana, Jacqueline Birt, Mark Holub, and Warrick van Zyl. 2021. Professional scepticism and the accounting classroom. Accounting Education 30: 213–33. [Google Scholar] [CrossRef]

- Ahmed, Ibrahim Elsiddig. 2019. Bridging the gap between governmental accounting education and practice. Accounting 5: 21–30. [Google Scholar] [CrossRef]

- Akande, Joseph Olorunfemi, and Sulaiman Olusegun Atiku. 2021. Developing Industry 4.0 accountants: Implications for higher education institutions in Namibia. Development and Learning in Organizations. ahead-of-print. [Google Scholar] [CrossRef]

- Al Mallak, Mohammed Ali, Lin Mei Tan, and Fawzi Laswad. 2020. Generic skills in accounting education in Saudi Arabia: Students’ perceptions. Asian Review of Accounting 28: 395–421. [Google Scholar] [CrossRef]

- Al-Aroud, Shaher Falah. 2021. Evaluation of accounting education and the extent of compatibility and the labor market needs: Field study: External auditors auditin Jordan. International Journal of Entrepreneurship 25: 1–10. [Google Scholar]

- Albu, Cătălin Nicolae, Nadia Albu, Robert Faff, and Allan Hodgson. 2011. Accounting competencies and the changing role of accountants in emerging economies: The case of Romania. Accounting in Europe 8: 155–84. [Google Scholar] [CrossRef]

- Al-Hattami, Hamood Mohammed. 2021. University accounting curriculum, IT, and job market demands: Evidence from Yemen. SAGE Open 11: 21582440211007111. [Google Scholar] [CrossRef]

- Alshbili, Ibrahem, and Ahmed A. Elamer. 2020. The vocational skills gap in accounting education curricula: Empirical evidence from the UK. International Journal of Management in Education 14: 271–92. [Google Scholar] [CrossRef]

- Andiola, Lindsay M., Erin Masters, and Carolyn Norman. 2020. Integrating technology and data analytic skills into the accounting curriculum: Accounting department leaders’ experiences and insights. Journal of Accounting Education 50: 100655. [Google Scholar] [CrossRef]

- Anis, Ahmed. 2017. Auditors’ and accounting educators’ perceptions of accounting education gaps and audit quality in Egypt. Journal of Accounting in Emerging Economies 7: 337–51. [Google Scholar] [CrossRef]

- Araujo, Valdineide dos Santos, Djalmir Gomes Santos, Paulo Roberto Nóbrega Cavalcante, and Edmery Tavares Barbosa. 2015. Academic formation in accounting sciences and its relationship with the labor market: The perception of the accounting sciences’ students of a higher education federal institution. Revista De Gestão, Finanças E Contabilidade 5: 123–39. [Google Scholar]

- Aryanti, Cornelia, and Desi Adhariani. 2020. Students’ Perceptions and Expectation Gap on the Skills and Knowledge of Accounting Graduates. The Journal of Asian Finance, Economics and Business 7: 649–57. [Google Scholar] [CrossRef]

- Asonitou, Sofia, and Trevor Hassall. 2019. Which skills and competences to develop in accountants in a country in crisis? The International Journal of Management Education 17: 100308. [Google Scholar] [CrossRef]

- Awayiga, Joseph Y., Joseph M. Onumah, and Mathew Tsamenyi. 2010. Knowledge and skills development of accounting graduates: The perceptions of graduates and employers in Ghana. Accounting Education 19: 139–58. [Google Scholar] [CrossRef]

- Baker, William M. 2013. Empirically assessing the importance of computer skills. Journal of Education for Business 88: 345–51. [Google Scholar] [CrossRef]

- Ballou, Brian, Dan L. Heitger, and Dale Stoel. 2018. Data-driven decision-making and its impact on accounting undergraduate curriculum. Journal of Accounting Education 44: 14–24. [Google Scholar] [CrossRef]

- Banasik, Ewa, and Christine Jubb. 2021. Are accounting programs future-ready? Employability skills. Australian Accounting Review 31: 256–67. [Google Scholar] [CrossRef]

- Barrett, Gerald V., and Robert L. Depinet. 1991. A reconsideration of testing for competence rather than for intelligence. American Psychologist 46: 1012–24. [Google Scholar] [CrossRef] [PubMed]

- Berková, Kateřina, Pavel Krpálek, and Katarína Krpálková Krelová. 2019. Future economic professionals: Development of practical skills and competencies in higher education from the point of view of international employers. Economic Annals-XXI 176: 91–98. [Google Scholar] [CrossRef]

- Berková, Kateřina, Andrea Kubišová, and Dana Kolářová. 2021. Differences of opinion among students of Czech higher education institutions on the competences of accountants required by the labour market. Universal Journal of Accounting and Finance 9: 1009–18. [Google Scholar] [CrossRef]

- Berry, Reanna, and Wesley Routon. 2020. Soft skill change perceptions of accounting majors: Current practitioner views versus their own reality. Journal of Accounting Education 53: 100691. [Google Scholar] [CrossRef]

- Bhasin, Madan Lal. 2016. Contribution of forensic accounting to corporate governance: An exploratory study of an asian country. International Business Management 10: 479–92. [Google Scholar] [CrossRef]

- Birkett, William P. 2002. Competency Profiles for Management Accounting Practice and Practitioners: A Report of the AIB, Accountants in Business Section of the International Federation of Accountants. New York: IFAC. [Google Scholar]

- Boyatzis, Richard E. 1982. The Competent Manager: A Model for Effective Performance. New York: John Wiley & Sons, Inc. [Google Scholar]

- Bruna, Inta, Kastytis Senkus, Rasa Subaciene, and Ruta Sneidere. 2017. Evaluation of perception of accountant’s role at the enterprise in Latvia and Lithuania. European Research Studies Journal XX: 143–63. [Google Scholar] [CrossRef]

- Bui, Binh, and Brenda Porter. 2010. The Expectation-Performance Gap in Accounting Education: An Exploratory Study. Accounting Education 19: 23–50. [Google Scholar] [CrossRef]

- Bui, Binh, and Charl de Villiers. 2017. Business strategies and management accounting in response to climate change risk exposure and regulatory uncertainty. The British Accounting Review 49: 4–24. [Google Scholar] [CrossRef]

- Burns, John, and Robert W. Scapens. 2000. Conceptualizing management accounting change: An institutional framework. Management Accounting Research 11: 3–25. [Google Scholar] [CrossRef]

- Camacho, Leticia. 2015. The communication skills accounting firms desire in new hires. Journal of Business & Finance Librarianship 20: 318–29. [Google Scholar] [CrossRef]

- Cernușca, Lucian. 2020. Soft and hard skills in accounting field-empiric results and implication for the accountancy profession. Studia Universitatis „Vasile Goldis” Arad Economics Series 30: 33–56. [Google Scholar] [CrossRef]

- Chaffer, Caroline, and Jill Webb. 2017. An evaluation of competency development in accounting trainees. Accounting Education 26: 431–58. [Google Scholar] [CrossRef]

- Chaplin, Sally. 2017. Accounting education and the prerequisite skills of accounting graduates: Are accounting firms’ moving the boundaries? Australian Accounting Review 27: 61–70. [Google Scholar] [CrossRef]

- Coady, Peggy, Seán Byrne, and John Casey. 2018. Positioning of emotional intelligence skills within the overall skillset of practice-based accountants: Employer and graduate requirements. Accounting Education 27: 94–120. [Google Scholar] [CrossRef]

- Crawford, Louise, Christine Helliar, and Elizabeth A. Monk. 2011. Generic skills in audit education. Accounting Education 20: 115–31. [Google Scholar] [CrossRef]

- da Camara, Pedro B. 2017. Dicionário de Competências. RH Editora. Available online: https://books.google.pt/books?id=xhAoswEACAAJ (accessed on 28 November 2022).

- Daff, Lyn. 2021. Employers’ perspectives of accounting graduates and their world of work: Software use and ICT competencies. Accounting Education 30: 495–524. [Google Scholar] [CrossRef]

- de Lange, Paul, Beverly Jackling, and Anne-Marie Gut. 2006. Accounting graduates’ perceptions of skills emphasis in undergraduate courses: An investigation from two Victorian universities. Accounting and Finance 46: 365–86. [Google Scholar] [CrossRef]

- de Villiers, R. R., and H. A. Viviers. 2018. Evaluating the efeective development of pervasive skills: The perceptions of students at two South African SAICA-accredited universities. Journal for New Generation Sciences 16: 17–39. [Google Scholar]

- Debreceny, Roger S., Stephanie M. Farewell, Audrey N. Scarlata, and Dan N. Stone. 2020. Knowledge and skills in complex assurance engagements: The case of XBRL. Journal of Information Systems 34: 21–45. [Google Scholar] [CrossRef]

- Denyer, David, and David Tranfield. 2009. Producing a systematic review. In The Sage Handbook of Organizational Research Methods. Los Angeles: SAGE Publications Ltd., pp. 671–89. [Google Scholar]

- Dolce, Valentina, Federica Emanuel, Maurizio Cisi, and Chiara Ghislieri. 2020. The soft skills of accounting graduates: Perceptions versus expectations. Accounting Education 29: 57–76. [Google Scholar] [CrossRef]

- dos Santos, Andreza Moura, Tania Nobre Gonçalves Ferreira Amorim, and Tácio Marques da Cunha. 2021. The accountant’s competences from the point of view of professionals working in the city of Vitória de Santo Antão—PE. Revista Ambiente Contábil 13: 355–79. [Google Scholar] [CrossRef]

- Douglas, Shonagh, and Elizabeth Gammie. 2019. An investigation into the development of non-technical skills by undergraduate accounting programmes. Accounting Education 28: 304–32. [Google Scholar] [CrossRef]

- Dunbar, Kirsty, Gregory Laing, and Monte Wynder. 2016. A content analysis of accounting job advertisements: Skills requirements for graduates. E-Journal of Business Education & Scholarship of Teaching 10: 58–72. [Google Scholar]

- Ellström, Per-Erik. 1998. The many meanings of occupational competence and qualification. In Key Qualifications in Work and Education. Edited by Wim J. Nijhof and Jan N. Streumer. Dodrecht: Springer, pp. 266–73. [Google Scholar] [CrossRef]

- Gasparyan, Armen Yuri, Lilit Ayvazyan, and George D. Kitas. 2013. Multidisciplinary bibliographic databases. Journal of Korean Medical Science 28: 1270–75. [Google Scholar] [CrossRef] [PubMed]

- Ghani, Erlane K., and Kamaruzzaman Muhammad. 2019. Industry 4.0: Employers expectations of accounting graduates and its implications on teaching and learning practices. International Journal of Education and Practice 7: 19–29. [Google Scholar] [CrossRef]

- Ghani, Erlane K., Rosdiana Rappa, and Ardi Gunardi. 2018. Employers’perceived accounting graduates’ soft skills. Academy of Accounting and Financial Studies Journal 22: 1–11. [Google Scholar]

- Gray, F. Elizabeth. 2010. Specific oral communication skills desired in new accountancy graduates. Business Communication Quarterly 73: 40–67. [Google Scholar] [CrossRef]

- Gray, F. Elizabeth, and Niki Murray. 2011. ‘A distinguishing factor’: Oral communication skills in new accountancy graduates. Accounting Education 20: 275–94. [Google Scholar] [CrossRef]

- Hamid, Sharifah Fadzlon Abdul, Zairul Nurshazana Zainuddin, and Suzana Sulaiman. 2016. Competences level and its perceived importance: A case study in Malaysian companies. Asia-Pacific Management Accounting Journal 11: 223–46. [Google Scholar]

- Hassall, Trevor, John Joyce, José Luis Arquero Montaño, and José Antonio Donoso Anes. 2005. Priorities for the development of vocational skills in management accountants: A European perspective. Accounting Forum 29: 379–94. [Google Scholar] [CrossRef]

- Hassall, Trevor, John Joyce, José Luis Arquero Montaño, and José María González González. 2010. The vocational skill priorities of Malaysian and UK students. Asian Review of Accounting 18: 20–29. [Google Scholar] [CrossRef]

- Howcroft, Douglas. 2017. Graduates’ vocational skills for the management accountancy profession: Exploring the accounting education expectation-performance gap. Accounting Education 26: 459–81. [Google Scholar] [CrossRef]

- Irafahmi, Diana Tien, P. John Williams, and Rosemary Kerr. 2021. Written communication: The professional competency often neglected in auditing courses. Accounting Education 30: 304–24. [Google Scholar] [CrossRef]

- Ismail, Zuriadah, Anis Suriati Ahmad, and Aidi Ahmi. 2020. Perceived employability skills of accounting graduates: The insights from employers. Elementary Education Online 19: 36–41. [Google Scholar] [CrossRef]

- Jackling, Beverly, and Paul de Lange. 2009. Do accounting graduates’ skills meet the expectations of employers? A matter of convergence or divergence. Accounting Education 18: 369–85. [Google Scholar] [CrossRef]

- Johnson, Steve, Bunney Schmidt, Steve Teeter, and Jonathan Henage. 2008. Using the Albrecht and Sack study to guide curriculum decisions. In Advances in Accounting Education. Bingley: Emerald (MCB UP), vol. 9, pp. 251–66. [Google Scholar] [CrossRef]

- Jones, Rob. 2014. Bridging the gap: Engaging in scholarship with accountancy employers to enhance understanding of skills development and employability. Accounting Education 23: 527–41. [Google Scholar] [CrossRef]

- Junger da Silva, Raphael, Roberto Tommasetti, Monica Zaidan Gomes, and Marcelo Alvaro da Silva Macedo. 2020. Accountants’ IT responsibilities and competencies from a student perspective. Higher Education, Skills and Work-Based Learning 11: 471–86. [Google Scholar] [CrossRef]

- Kavanagh, Marie H., and Lyndal Drennan. 2008. What skills and attributes does an accounting graduate need? Evidence from student perceptions and employer expectations. Accounting & Finance 48: 279–300. [Google Scholar] [CrossRef]

- Keneley, Monica, and Beverley Jackling. 2011. The acquisition of generic skills of culturally-diverse student cohorts. Accounting Education 20: 605–23. [Google Scholar] [CrossRef]

- Kennedy, Frances A., and Richard B. Dull. 2008. Transferable team skills for accounting students. Accounting Education 17: 213–24. [Google Scholar] [CrossRef]

- King, Alexander Z. 2021. Data analytics in association to advance collegiate schools of business–accredited U.S. university accounting programs: A quantitative research study. Journal of Education for Business 97: 1–9. [Google Scholar] [CrossRef]

- Klemp, George O. 1980. The Assessment of Occupational Competence: Final Report: 1. Introduction and Overview. Boston: National Institute of Education. [Google Scholar]

- Klemp, George O. 2001. Competence in context: Identifying core skills for the future. In Competence in the Learning Society. Edited by Shirley. Bern: Lang, Peter A. G., vol. 166, pp. 129–47. [Google Scholar]

- Kokina, Julia, Ruth Gilleran, Shay Blanchette, and Donna Stoddard. 2021. Accountant as digital innovator: Roles and competencies an the age of automation. Accounting Horizons 35: 153–84. [Google Scholar] [CrossRef]

- Král, Bohumil, Grzegorz Mikołajewicz, Jarosław Nowicki, and Libuše Šoljaková. 2021. Management accountants’ professional competences: Requirements in the Czech Republic and Poland. The normative approach and business practice. Acta Universitatis Agriculturae Et Silviculturae Mendelianae Brunensis 69: 379–93. [Google Scholar] [CrossRef]

- Kroon, Nanja, and Maria do Céu Alves. 2022. The accounting professional’s competency gaps. In Proceedings of the 40th International Business Information Management Association (IBIMA) Conference. Symposium Conducted at the Meeting of IBIMA. Edited by Khalid S. Soliman. Seville: IBIMA. [Google Scholar]

- Ku Bahador, Ku Maisurah, and Abrar Haider. 2017. Incorporating information technology competencies in accounting curriculum: A case study in Malaysian Higher Education Institutions. Journal of Engineering and Applied Sciences 12: 5508–13. [Google Scholar]

- Kunz, Rolien, and Herman de Jager. 2019a. Exploring the audit capabilities expectation-performance gap of newly employed first-year trainee accountants in Gauteng: Audit managers at large firms’ perceptions. South African Journal of Accounting Research 33: 145–62. [Google Scholar] [CrossRef]

- Kunz, Rolien, and Herman de Jager. 2019b. Performance of newly employed trainee accountants in Gauteng, South Africa, versus the skills expectations of employers: How big is the gap? Industry and Higher Education 33: 340–49. [Google Scholar] [CrossRef]

- Lai, Ming Ling, and Hidayah Ahamad Nawawi Nurul. 2010. Integrating ICT skills and tax software in tax education. Campus-Wide Information Systems 27: 303–17. [Google Scholar] [CrossRef]

- Lakshmi, Geeta. 2013. An exploratory study on cognitive skills and topics focused in learning objectives of finance modules: A UK perspective. Accounting Education 22: 233–47. [Google Scholar] [CrossRef]

- Leitner-Hanetseder, Susanne, Othmar M. Lehner, Christoph Eisl, and Carina Forstenlechner. 2021. A profession in transition: Actors, tasks and roles in AI-based accounting. Journal of Applied Accounting Research 22: 539–56. [Google Scholar] [CrossRef]

- Liberati, Alessandro, Douglas G. Altman, Jennifer Tetzlaff, Cynthia Mulrow, Peter C. Gøtzsche, John P. A. Ioannidis, Mike Clarke, P. J. Devereaux, Jos Kleijnen, and David Moher. 2009. The PRISMA statement for reporting systematic reviews and meta-analyses of studies that evaluate health care interventions: Explanation and elaboration. PLoS Medicine 6: e1000100. [Google Scholar] [CrossRef] [PubMed]

- Lim, Yet-Mee, Teck Heang Lee, Ching Seng Yap, and Chui Ching Ling. 2016. Employability skills, personal qualities, and early employment problems of entry-level auditors: Perspectives from employers, lecturers, auditors, and students. Journal of Education for Business 91: 185–92. [Google Scholar] [CrossRef]

- Lin, Ping, Sudha Krishnan, and Debra Grace. 2013. The Effect of Experience on Perceived Communication Skills: Comparisons between Accounting Professionals and Students. In Advances in Accounting Education: Teaching and Curriculum Innovations. Bingley: Emerald Group Publishing Limited, pp. 131–52. [Google Scholar] [CrossRef]

- Low, Mary, Vida Botes, David Dela Rue, and Jackie Allen. 2016. Accounting employers’ expectations—The ideal accounting graduates. E-Journal of Business Education & Scholarship of Teaching 10: 36–57. [Google Scholar]

- Lucia, Antoinette de, and Richard Lepsinger. 1999. The Art and Science of Competency Models: Pinpointing Critical Success Factors in Organizations. New York: Wiley. Available online: https://books.google.pt/books?id=w5pjQgAACAAJ (accessed on 27 November 2022).

- Maali, Bassam, and Ali M. Al-Attar. 2020. Accounting curricula in universities and market needs: The Jordanian case. SAGE Open 10: 2158244019899463. [Google Scholar] [CrossRef]

- Mameche, Youcef, Mohamed Ali Omri, and Najet Hassine. 2020. Compliance of accounting education programs with International Accounting Education Standards: The case of IES 3 in Tunisia. Eurasian Journal of Educational Research 20: 225–46. [Google Scholar] [CrossRef]

- Mandilas, Athanasios, Dimitrios Kourtidis, and Yiannis Petasakis. 2014. Accounting curriculum and market needs. Education + Training 56: 776–94. [Google Scholar] [CrossRef]

- Mcbride, Karen, and Christina Philippou. 2021. “Big results require big ambitions”: Big data, data analytics and accounting in masters courses. Accounting Research Journal 35: 71–100. [Google Scholar] [CrossRef]

- McClelland, David C. 1973. Testing for competence rather than for ‘intelligence’. American Psychologist 29: 1–14. [Google Scholar] [CrossRef]

- Memiyanty, Haji Abdul Rahim, Haji Abdul Aziz Rozainun, and Binshan Lin. 2010. Perception on professional capabilities of accounting graduates. International Journal of Management in Education 4: 29882. [Google Scholar] [CrossRef]

- Mgaya, K. V., and E. G. Kitindi. 2008. IT skills of academics and practising accountants in Botswana. World Review of Entrepreneurship, Management and Sustainable Development 4: 366–79. [Google Scholar] [CrossRef]

- Mgaya, K. V., and E. G. Kitindi. 2009. Essential skills needed by accounting graduates in a developing country: The views of practising accountants and accounting educators in Botswana. International Journal of Accounting, Auditing and Performance Evaluation 5: 329–51. [Google Scholar] [CrossRef]

- Mhlongo, Favourite. 2020. Pervasive skills and accounting graduates’ employment prospects: Are South African employers calling for pervasive skills when recruiting? Journal of Education 80: 49–71. [Google Scholar] [CrossRef]

- Moher, David, Alessandro Liberati, Jennifer Tetzlaff, and Douglas G. Altman. 2010. Preferred reporting items for systematic reviews and meta-analyses: The PRISMA statement. International Journal of Surgery 8: 336–41. [Google Scholar] [CrossRef] [PubMed]

- Montoya-del-Corte, Javier, and Gabriela Maria Farías-Martinez. 2014. Accounting training received in college vs. labor market demands: The case of Mexico. The New Educational Review 36: 168–81. [Google Scholar] [CrossRef]

- Moore, Walter B., and Andrew Felo. 2021. The evolution of accounting technology education: Analytics to STEM. Journal of Education for Business 97: 1–7. [Google Scholar] [CrossRef]

- Mosweu, Olefhile, and Mpho Ngoepe. 2019. Skills and competencies for authenticating digital records to support audit process in Botswana public sector. African Journal of Library Archives and Information Science 29: 17–28. [Google Scholar]

- Nicolaescu, Cristina, Delia David, and Pavel Farcas. 2017. Professional and transversal competencies in the accounting field: Do employers’ expectations fit students’ perceptions? Evidence from Western Romania. Studies in Business and Economics 12: 126–40. [Google Scholar] [CrossRef]

- Oliveira, Isabel, António Cardoso, Luciano Medeiros, Jorge Figueiredo, Margarida Pocinho, and Elizabeth Real de Oliveira. 2021. The auditor’s characteristics for big four audit companies: Empirical analysis in the brazilian market. Academy of Strategic Management Journal 20: 1–11. [Google Scholar]

- Olivier, Henri. 2000. Challenges facing the accountancy profession. European Accounting Review 9: 603–24. [Google Scholar] [CrossRef]

- Onumah, Joseph M., Felix Gariba, Aaron Packeys, and Reynolds A. Agyapong. 2012. The banking industry requirements of accounting graduates in Ghana. In Research in Accounting in Emerging Economies. Accounting in Africa. Edited by Venancio Tauringana and Musa Mangena. Bingley: Emerald Group Publishing Limited, vol. 12, pp. 75–105. [Google Scholar] [CrossRef]

- Osmani, Mohamad, Nitham Hindi, and Vishanth Weerakkody. 2020. Incorporating information communication technology skills in accounting education. International Journal of Information and Communication Technology Education 16: 100–10. [Google Scholar] [CrossRef]

- Osmani, Mohamad, Vishanth Weerakkody, Nitham M. Hindi, Rajab Al-Esmail, Tillal Eldabi, Kawaljeet Kapoor, and Zahir Irani. 2015. Identifying the trends and impact of graduate attributes on employability: A literature review. Tertiary Education and Management 21: 367–79. [Google Scholar] [CrossRef]

- Oussii, Ahmed Atef, and Mohamed Faker Klibi. 2017. Accounting students’ perceptions of important business communication skills for career success. Journal of Financial Reporting and Accounting 15: 208–25. [Google Scholar] [CrossRef]

- Oyerogba, Ezekiel Oluwagbemiga. 2021. Forensic auditing mechanism and fraud detection: The case of Nigerian public sector. Journal of Accounting in Emerging Economies 11: 752–75. [Google Scholar] [CrossRef]

- Page, Matthew J., Joanne E. McKenzie, Patrick M. Bossuyt, Isabelle Boutron, Tammy C. Hoffmann, Cynthia D. Mulrow, Larissa Shamseer, Jennifer M. Tetzlaff, Elie A. Akl, Sue E. Brennan, and et al. 2021. The PRISMA 2020 statement: An updated guideline for reporting systematic reviews. BMJ 372: n71. [Google Scholar] [CrossRef]

- Paguio, Rafael, and Beverley Jackling. 2016. Teamwork from accounting graduates: What do employers really expect? Accounting Research Journal 29: 348–66. [Google Scholar] [CrossRef]

- Palmer, Kristine N., Douglas E. Ziegenfuss, and Robert E. Pinsker. 2004. International knowledge, skills, and abilities of auditors/accountants. Managerial Auditing Journal 19: 889–96. [Google Scholar] [CrossRef]

- Pan, Peipei, and Hector Perera. 2012. Market relevance of university accounting programs: Evidence from Australia. Accounting Forum 36: 91–108. [Google Scholar] [CrossRef]

- Paulsson, Gert. 2012. The role of management accountants in new public management. Financial Accountability & Management 28: 378–94. [Google Scholar] [CrossRef]

- Pilipczuk, Olga. 2020. Toward cognitive management accounting. Sustainability 12: 5108. [Google Scholar] [CrossRef]

- Pitulice, Ileana Cosmina, Alina Georgiana Profiroiu, and Aurelia Stefanescu. 2018. Government acounting eucation for uiversity udergraduates. Transylvanian Review of Administrative Sciences 2018: 75–91. [Google Scholar] [CrossRef]

- Rackliffe, Usha Ramachandran, and Linda Ragland. 2016. Excel in the accounting curriculum: Perceptions from accounting professors. Accounting Education 25: 139–66. [Google Scholar] [CrossRef]

- Ragland, Linda, and Usha Ramachandran. 2014. Towards an understanding of excel functional skills needed for a career in public accounting: Perceptions from public accountants and accounting students. Journal of Accounting Education 32: 113–29. [Google Scholar] [CrossRef]

- Reddrop, Alan, and Gido Mapunda. 2019. Listening skills: Accountancy educators in retreat? Australasian Accounting, Business and Finance Journal 13: 76–89. [Google Scholar] [CrossRef]

- Richardson, William. 2005. Curriculum requirements for entry-level management accounting in Australian industry and commerce. Journal of Applied Management and Advanced Research 3: 55–66. [Google Scholar]

- Ridwan. 2017. Analysis of the competencies of accounting department graduates based on stakeholders perspective in the central Sulawesi province, Indonesia. International Journal of Civil Engineering and Technology 8: 45–53. [Google Scholar]

- Riley, Tracey J., and Kathleen A. Simons. 2016. The written communication skills that matter most for accountants. Accounting Education 25: 239–55. [Google Scholar] [CrossRef]

- Rowe, Christopher. 1995. Clarifying the use of competence and competency models in recruitment, assessment and staff development. Industrial and Commercial Training 27: 12–17. [Google Scholar] [CrossRef]

- Sanghi, Seema. 2016. The Handbook of Competency Mapping: Understanding, Designing and Implementing Competency Models in Organizations 3e, 3rd ed. London: SAGE. [Google Scholar]

- Schmidt, Jacqueline J., Brian Patrick Green, and Roland Madison. 2009. Accounting department chairs’ perceptions of the importance of communication skills. In Advances in Accounting Education. Advances in Accounting Education. Edited by Bill N. Schwartz and Anthony H. Catanach. Bingley: Emerald Group Publishing Limited, vol. 10, pp. 151–68. [Google Scholar] [CrossRef]

- Schutte, Danie, and Bianca Lovecchio. 2017. An evaluation of the competence requirements of South African accountants practising in the SME environment. Journal of Social Sciences 53: 61–72. [Google Scholar] [CrossRef]

- Senan, Nabil Ahmed Mareai. 2019. Convenience of accounting education for the requirements of Saudi labour market: An empirical study. Management Science Letters 9: 1919–32. [Google Scholar] [CrossRef]

- Senik, Rosmila, Martin Broad, Norazila Mat, and Suhaida Abdul Kadir. 2013. Information Technology (IT) knowledge and skills of accounting graduates: Does an expectation gap exist? Jurnal Pengurusan 38: 87–100. [Google Scholar] [CrossRef]

- Shahwan, Yousef, and Jamal Roudaki. 2009. Entry-level accounting positions competencies in the UAE: Perceptions of accounting educators and financiel managers. Journal of Global Business Advancement 2: 301–17. [Google Scholar] [CrossRef]

- Siriwardane, Harshini P., Billy Kin Hoi Hu, and Kin Yew Low. 2014. Skills, knowledge, and attitudes important for pesent-day auditors. International Journal of Auditing 18: 193–205. [Google Scholar] [CrossRef]

- Siriwardane, H. P., K.-Y. Low, and D. Blietz. 2015. Making entry-level accountants better communicators: A Singapore-based study of communication tasks, skills, and attributes. Journal of Accounting Education 33: 332–47. [Google Scholar] [CrossRef]

- Siriwardane, Harshini P., and Chris H. Durden. 2014. The communication skills of accountants: What we know and the gaps in our knowledge. Accounting Education 23: 119–34. [Google Scholar] [CrossRef]

- Smith, Bernadette, William Maguire, and Helen Haijuan Han. 2018. Generic skills in accounting: Perspectives of Chinese postgraduate students. Accounting & Finance 58: 535–59. [Google Scholar] [CrossRef]

- Snyder, Hannah. 2019. Literature review as a research methodology: An overview and guidelines. Journal of Business Research 104: 333–39. [Google Scholar] [CrossRef]

- Spencer, Lyle M., and Phd Signe M. Spencer. 1993. Competence at Work: Models for Superior Performance. New York: John Wiley & Sons. [Google Scholar]

- Spraakman, Gary, Winifred O’Grady, Davood Askarany, and Chris Akroyd. 2015. Employers’ perceptions of information technology competency requirements for management accounting graduates. Accounting Education 24: 403–22. [Google Scholar] [CrossRef]

- Stone, Gerard, and Margaret Lightbody. 2012. The nature and significance of listening skills in accounting practice. Accounting Education 21: 363–84. [Google Scholar] [CrossRef]

- Suttipun, Muttanachai. 2014. The readiness of Thai accounting students for the ASEAN Economic Comunity: An exploratory study. Asian Journal of Business and Accounting 7: 139–57. [Google Scholar]

- Tan, Lin Mei, and Fawzi Laswad. 2018. Professional skills required of accountants: What do job advertisements tell us? Accounting Education 27: 403–32. [Google Scholar] [CrossRef]

- Tan, Lin Mei, and Fawzi Laswad. 2019. Key employability skills required of tax accountants. Journal of the Australasian Tax Teachers Asscoiation 14: 211–39. [Google Scholar]

- Tenedero, Pia Patricia P., and Camilla J. Vizconde. 2015. University English and audit firms in the Philippines. Business and Professional Communication Quarterly 78: 428–53. [Google Scholar] [CrossRef]

- Terblanche, E. A. J., and B. de Clercq. 2021. A critical thinking competency framework for accounting students. Accounting Education 30: 325–54. [Google Scholar] [CrossRef]

- Towers-Clark, Jane. 2015. Undergraduate accounting students: Prepared for the workplace? Journal of International Education in Business 8: 37–48. [Google Scholar] [CrossRef]

- Tsiligiris, Vangelis, and Dorothea Bowyer. 2021. Exploring the impact of 4IR on skills and personal qualities for future accountants: A proposed conceptual framework for university accounting education. Accounting Education 30: 621–49. [Google Scholar] [CrossRef]

- Uwizeyemungu, Sylvestre, Jacques Bertrand, and Placide Poba-Nzaou. 2020. Patterns underlying required competencies for CPA professionals: A content and cluster analysis of job ads. Accounting Education 29: 109–36. [Google Scholar] [CrossRef]

- van Akkeren, Jeanette, Sherrena Buckby, and Kim MacKenzie. 2013. A metamorphosis of the traditional accountant. Pacific Accounting Review 25: 188–216. [Google Scholar] [CrossRef]

- van der Klink, Marcel R., and Jo Boon. 2003. Competencies: The triumph of a fuzzy concept. International Journal of Human Resources Developmente and Management 3: 125–37. [Google Scholar]

- van Romburgh, Henriëtte, and Nico van der Merwe. 2015. University versus practice: A pilot study to identify skills shortages that exist in first-year trainee accountants in South Africa. Industry and Higher Education 29: 141–49. [Google Scholar] [CrossRef]

- Waldmann, Erwin, and Janek Ratnatunga. 2011. A marketing approach to service quality in accounting: A case study. International Business and Economics Research Journal (IBER) 2: 29–44. [Google Scholar] [CrossRef]

- Walker, Edward R., Yinghong Zhang, Bambi A. Hora, and Paula R. Sanders. 2020. The state of cost and managerial accounting education: Management’s perspective. Journal of Higher Education Theory and Practice 20: 16–37. [Google Scholar]

- Waller, Thomas C., and Rebecca A. Gallun. 1985. Microcomputer competency requirements in the accounting industry: A pilot study. Journal of Accounting Education 3: 31–40. [Google Scholar] [CrossRef]

- Warren, J. Donald, Kevin C. Moffitt, and Paul Byrnes. 2015. How Big Data Will Change Accounting. Accounting Horizons 29: 397–407. [Google Scholar] [CrossRef]

- Webb, Jill, and Caroline Chaffer. 2016. The expectation performance gap in accounting education: A review of generic skills development in UK accounting degrees. Accounting Education 25: 349–67. [Google Scholar] [CrossRef]

- Wells, Paul, Philippa Gerbic, Ineke Kranenburg, and Jenny Bygrave. 2009. Professional skills and capabilities of accounting graduates: The New Zealand expectation gap? Accounting Education 18: 403–20. [Google Scholar] [CrossRef]

- Yanto, Heri, Soo-Fen Fam, Niswah Baroroh, and Kuat Waluyo Jati. 2018. Graduates’ accounting competencies in global business: Perceptions of Indonesian Practitioners and academics. Academy of Accounting and Financial Studies Journal 22: 1–17. [Google Scholar]

- Yoon, Sung Wook, Rishma Vedd, and Christopher Gil Jones. 2013. IFRS knowledge, skills, and abilities: A follow-up study of employer expectations for undergraduate Accounting Majors. Journal of Education for Business 88: 352–60. [Google Scholar] [CrossRef]

- Yorke, Mantz. 1992. Quality in Higher Education: A Conceptualisation and Some Observations on the Implementation of a Sectoral Quality System. Journal of Further and Higher Education 16: 90–104. [Google Scholar] [CrossRef]

- Zhyvets, Alla. 2018. Evolution of professional competencies of accountants of small enterprises in the digital economy of Ukraine. Baltic Journal of Economic Studies 4: 87. [Google Scholar] [CrossRef]

- Zubairu, Umaru, Suhaiza Ismail, and A. H. Fatima. 2019. The quest for morally competent future Muslim accountants. Journal of Islamic Accounting and Business Research 10: 297–314. [Google Scholar] [CrossRef]

| Search Key | |

|---|---|

| (“skill” OR “skills” OR “competenc*”) AND (“accountan*” OR “account* profession*” OR “account* graduate*” OR “account* undergraduate*” OR “account* student*” OR “account* scholar*” OR “account* education” OR “account* study” OR “account* studies”) Using the Boolean operators AND and OR, we guarantee that at least one of the concepts from the first and one from the second part is included. | |

| I/E Criteria | Reason for Inclusion/Exclusion | |

|---|---|---|

| Exclusion criteria: | ||

| No full text | NFT | No full text available |

| Not empirical | NE | The article does not present empirical research (e.g., literature reviews, commentaries, etc.) |

| Not related | NR | The article does not address/focus on the accounting professional’s competencies |

| Loosely related | LR-1 | The article addresses the accounting professional’s competencies as a measure of another construct |

| LR-2 | The article addresses the accounting professional’s competencies to perform functions that are not usually those of an accountant | |

| LR-3 | The article addresses the accounting professional’s competencies as an output of a specific teaching format/case/application/choice. | |

| LR-4 | The article presents a teaching case/teaching note/instructional case | |

| Partially related | PR | The article focuses on accounting professional’s competencies without approaching their actual or future supply or demand (university/market) |

| Inclusion criteria: | ||

| Totally related | TR-1 | The article focuses on the supply of accounting professional’s competencies (taught/acquired/developed in university) |

| TR-2 | The article focuses on the demand for accounting professional’s competencies (expected/desired/required by the market) | |

| TR-3 | The article focuses on both the supply and the demand of accounting professional’s competencies | |

| TR-4 | The article focuses on the fit between the supply and the demand of accounting professional’s competencies (gaps) |

| Perspective | Definition |

|---|---|

| Competencies requirement | Competencies that are expected or required by employers when hiring new employees, in this case, particularly recent graduates. |

| Importance of the competencies | The importance of the competencies is measured in terms of the expected value that a given competency will have in an employee’s career success. |

| Competencies that should be taught in university | Depending on the actors being questioned, the competencies that should be taught in university assume different sides of the conceptual model. For example, the perception of academics is on the supply side, whereas employers’ perception is on the demand side. |

| Competencies taught in university | Competencies taught and competencies acquired are closely linked and, as such, are considered together in the conceptual model. It is possible that the competencies taught are not the same as those acquired, however, as a whole, they reflect the competencies developed in the higher education system. |

| Competencies acquired at university | |

| Demonstrated competencies | It represents the direct assessment or perception of effectively demonstrated competencies. This can be done, for example, by academics who assess their students or employers who assess their employees. |

| Gap existence | Some studies directly question participants about whether or not a competence/skills gap exists. It can assume any gap. |

| How | Who | What |

|---|---|---|

| Perception of | Academics | Importance of the competencies |

| Existence of | - | Competencies taught in university |

| Perspective/Actors | Supply | Demand | Others | Total | |||||

|---|---|---|---|---|---|---|---|---|---|

| Students | Graduates | Academics | Total | Employers | Practitioners | Total | |||

| Competencies requirement | 4 | 3 | 7 | 11 | 12 | 23 | 30 | ||

| Importance of the competencies | 19 | 3 | 19 | 41 | 23 | 24 | 47 | 2 | 90 |

| Competencies that should be taught | 3 | 2 | 4 | 9 | 7 | 3 | 10 | 19 | |

| Competencies taught in university | 10 | 6 | 10 | 26 | 0 | 26 | |||

| Competencies acquired at university | 4 | 1 | 1 | 6 | 0 | 6 | |||

| Demonstrated competencies | 7 | 2 | 4 | 13 | 10 | 11 | 21 | 34 | |

| Gap existence | 2 | 2 | 2 | 6 | 5 | 6 | 11 | 17 | |

| Total | 49 | 16 | 43 | 108 | 56 | 56 | 112 | 2 | 222 |

| International Education Standards and Competency Categories * | 2006/07 | 2008/09 | 2010/11 | 2012/13 | 2014/15 | 2016/17 | 2018/19 | 2020/21 | Total |

|---|---|---|---|---|---|---|---|---|---|

| IES 2 | |||||||||

| Financial accounting and reporting | 1 | 1 | |||||||

| Foreign languages | 1 | ||||||||

| Information technology | 1 | 1 | 2 | 1 | 1 | 5 | 13 | ||

| Miscellaneous | 1 | 2 | 3 | 6 | |||||

| IES 2 + IES 3 | |||||||||

| Information technology + Intellectual | 1 | 1 | |||||||

| Miscellaneous | 1 | 1 | 1 | 5 | 10 | 19 | |||

| IES 2 + IES 3 + IES 4 | |||||||||

| Miscellaneous | 1 | 6 | 6 | 4 | 4 | 5 | 10 | 9 | 53 |

| IES 3 | |||||||||

| Interpersonal and communication | 1 | 2 | 2 | 1 | 1 | 1 | 12 | ||

| Organizational | 1 | 1 | |||||||

| Miscellaneous | 1 | 3 | 4 | ||||||

| IES 3 + IES 4 | |||||||||

| Miscellaneous | 1 | 3 | 4 | 9 | |||||

| IES 4 | |||||||||

| Miscellaneous | 1 | 2 | |||||||

| Total | 1 | 9 | 9 | 10 | 7 | 10 | 22 | 36 | 122 |

| IES | Competency Category | Total |

|---|---|---|

| IES 2 | Financial accounting and reporting | 1 |

| Foreign languages | 1 | |

| Information technology | 13 | |

| IES 2 + IES 3 | Information technology + Intellectual | 1 |

| IES 3 | Interpersonal and communication | 12 |

| Organizational | 1 | |

| Total | 29 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kroon, N.; Alves, M.d.C. Fifteen Years of Accounting Professional’s Competencies Supply and Demand: Evidencing Actors, Competency Assessment Strategies, and ‘Top Three’ Competencies. Adm. Sci. 2023, 13, 70. https://doi.org/10.3390/admsci13030070

Kroon N, Alves MdC. Fifteen Years of Accounting Professional’s Competencies Supply and Demand: Evidencing Actors, Competency Assessment Strategies, and ‘Top Three’ Competencies. Administrative Sciences. 2023; 13(3):70. https://doi.org/10.3390/admsci13030070

Chicago/Turabian StyleKroon, Nanja, and Maria do Céu Alves. 2023. "Fifteen Years of Accounting Professional’s Competencies Supply and Demand: Evidencing Actors, Competency Assessment Strategies, and ‘Top Three’ Competencies" Administrative Sciences 13, no. 3: 70. https://doi.org/10.3390/admsci13030070