Exploring the Dynamic Shock of Unconventional Monetary Policy Channels on Income Inequality: A Panel VAR Approach

Abstract

:1. Introduction

2. Theoretical Framework

2.1. Theoretical Channels of Monetary Policy and Income and Wealth Inequality

2.2. Theoretical Channels of Monetary Policy and Income and Wealth Inequality

2.2.1. Effects of Conventional Monetary Policy on Inequality

2.2.2. Effects of Unconventional Monetary Policy on Inequality

2.2.3. Effects of Macroprudential Policy on Inequality

3. Methodological and Data

3.1. Data

3.2. Panel Vector Auto Regression (PVAR) Approach

4. Analysis of Results and Data Analysis

4.1. Data Analysis

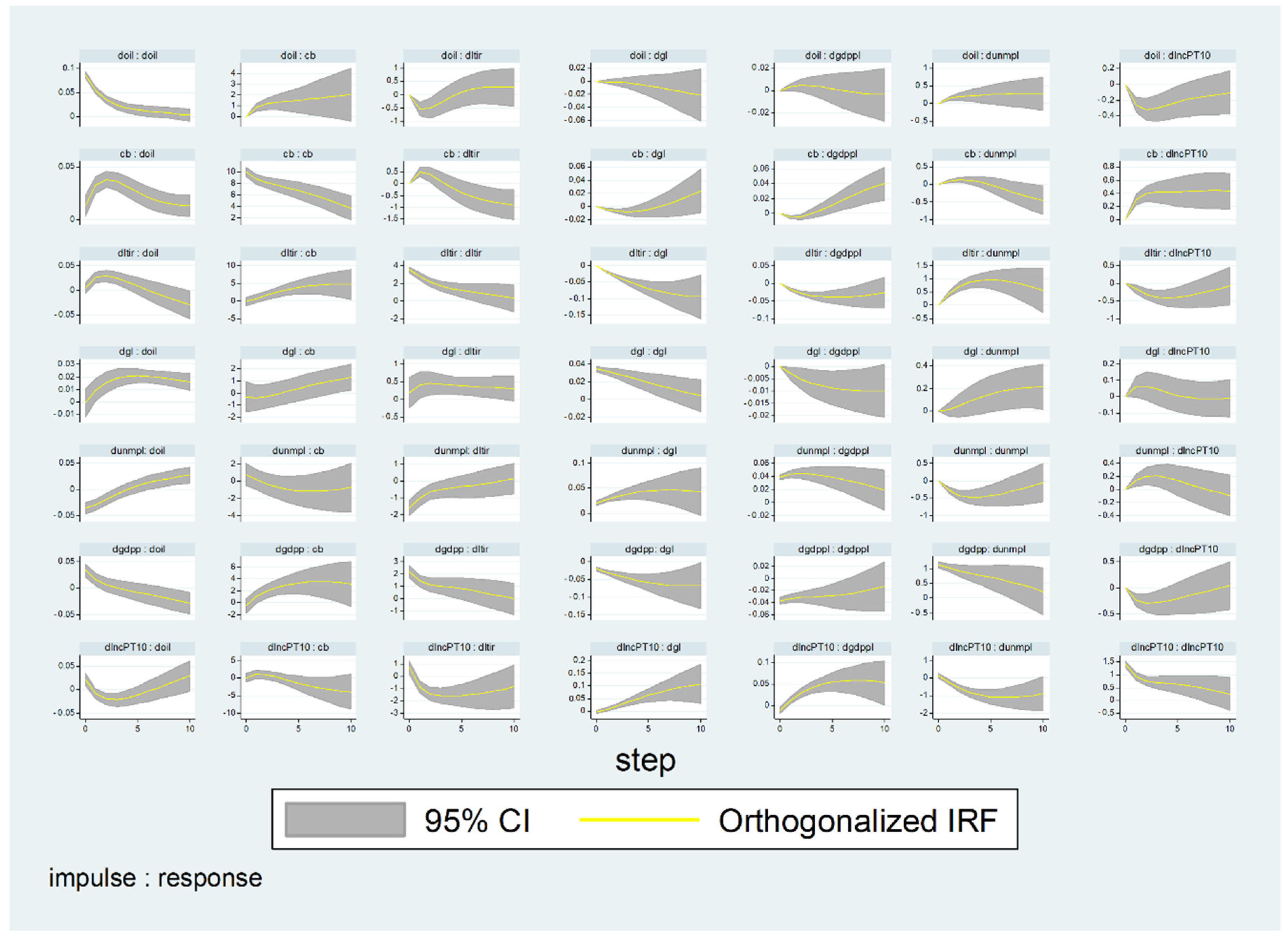

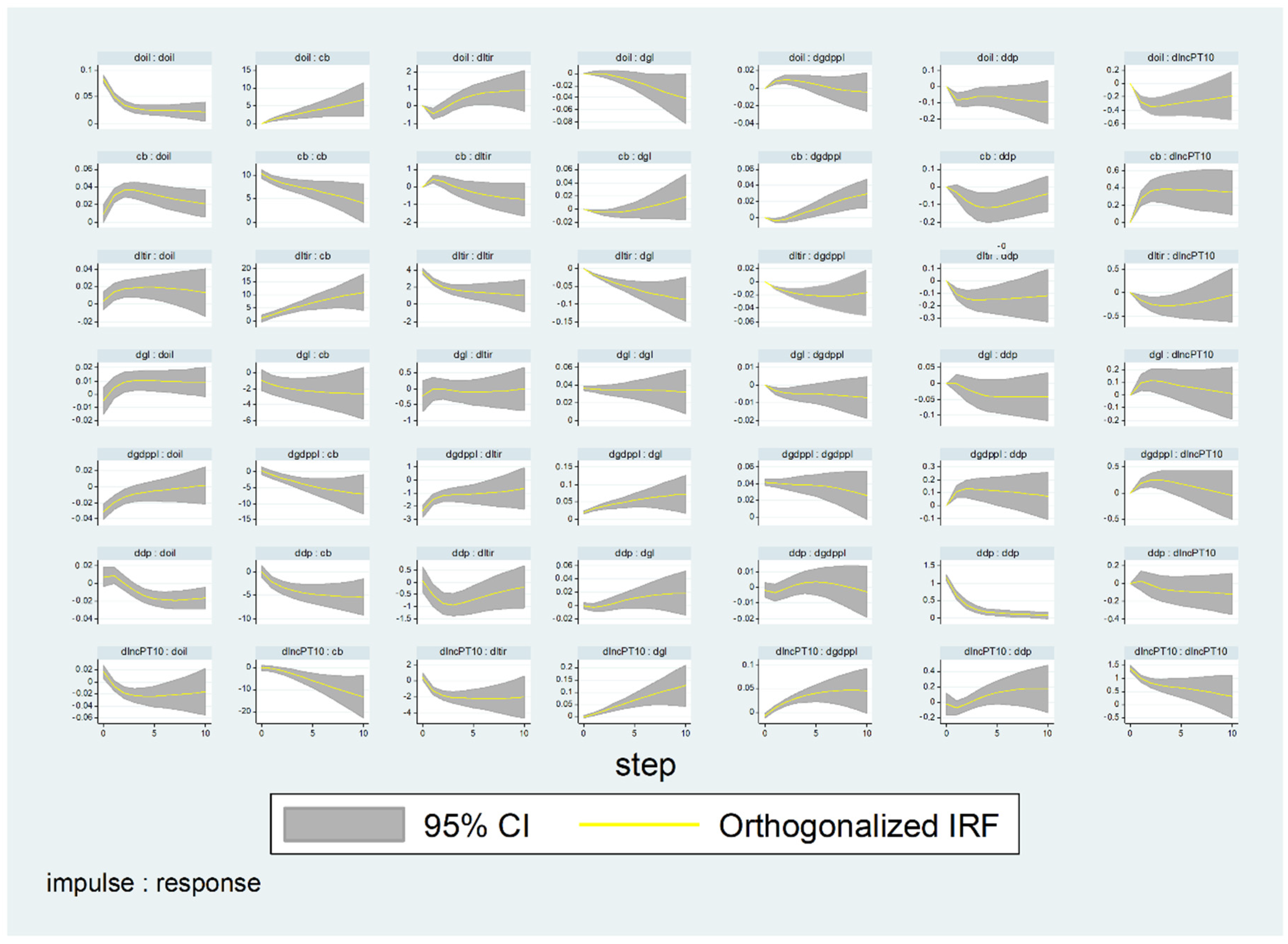

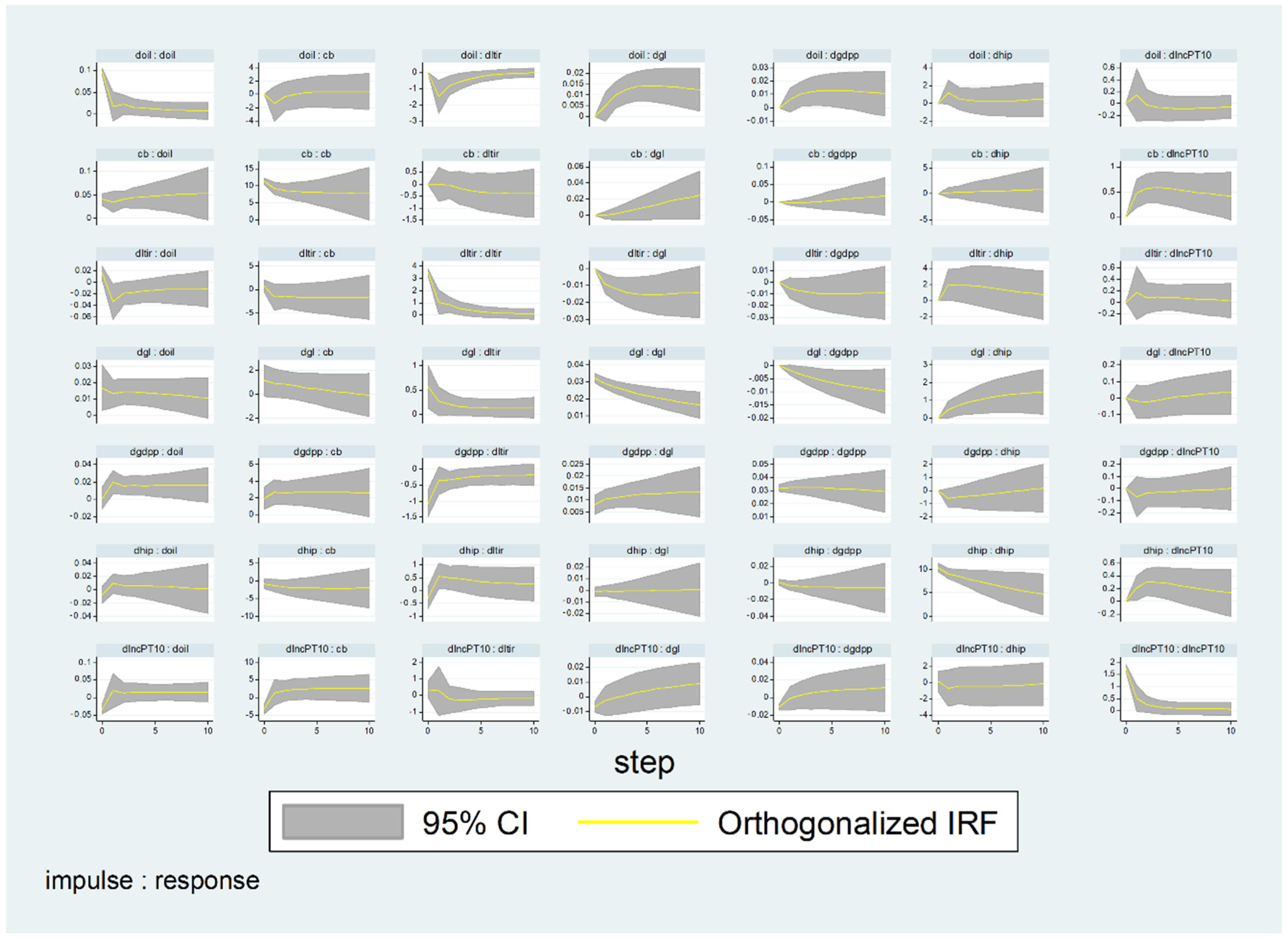

4.2. The Results of the PVAR and Interpretations

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| t-Stati | incPT10 | incPT1 | Gini | cb | dp | G | gdpp | hip | Ltir | Oil | Unmpl |

|---|---|---|---|---|---|---|---|---|---|---|---|

| incPT10 | 1.00 | ||||||||||

| incPT1 | −0.34 (−6.37) | 1.00 | |||||||||

| Gini | −50.99 (−4.90) | −0.34 (−2.79) | 1.00 | ||||||||

| cb | 0.16 (2.91) | −0.21 (−3.74) | 0.30 (5.45) | 1.00 | |||||||

| dp | −0.02 (−3.38) | 0.39 (8.36) | 0.30 (5.45) | 0.13 (2.43) | 1.00 | ||||||

| G | −0.49 (−9.96) | 0.20 (3.63) | 0.30 (5.45) | −0.24 (−4.40) | −0.24 (−4.44) | 1.00 | |||||

| gdpp | 0.28 (5.03) | −0.35 (−6.54) | 0.30 (5.45) | −0.40 (2.7) | −0.59 (−3.98) | −0.29 (2.99) | 1.00 | ||||

| Hip | −0.30 (−2.78) | −0.20 (−4.55) | 0.30 (5.45) | −0.17 (−2.99) | −0.19 (−3.40) | 0.23 (4.22) | −0.40 (−3.22) | 1.00 | |||

| Ltir | −0.28 (−5.17) | 0.26 (4.72) | 0.30 (5.45) | −0.16 (−2.88) | 0.28 (2.48) | 0.57 (8.98) | −0.23 (3.81) | 0.19 (3.47) | 1.00 | ||

| Oil | 0.11 (2.89) | −0.12 (−2.26) | 0.30 (5.45) | −0.24 (−4.31) | −0.27 (−4.86) | 0.19 (3.52) | 0.12 (2.09) | 0.58 (12.48) | −0.34 (−3.99) | 1.00 | |

| Unmpl | −0.34 (−6.43) | 0.50 (16.36) | 0.30 (5.45) | −0.20 (−3.63) | 0.26 (4.77) | 0.57 (2.99) | −0.61 (−4.92) | −0.59 (−2.90) | 0.34.98 (2.33) | 0.55 (2.99) | 1.00 |

| Lag | CD | J | J-P.v | MBIC | MAIC | MQIC |

|---|---|---|---|---|---|---|

| 1 | 0.99 | 135.95 | 0.23 | −572.77 | −114.04 | −297.83 |

| 2 | 0.99 | 107.24 | 0.29 | −459.74 | −92.75 | −239.78 |

| 3 | 0.99 | 77.61 | 0.39 | −347.62 | −72.38 | −182.65 |

| 4 | 0.99 | 50.90 | 0.43 | −232.59 | −49.09 | −122.61 |

| 5 | 0.99 | 27.72 | 0.32 | −114.01 | −22.27 | −59.02 |

| 6 | 0.99 | … | … | … | … | … |

References

- Abrigo, Michael, and Inessa Love. 2016. Estimation of panel vector autoregression in Stata. The Stata Journal 16: 778–804. [Google Scholar] [CrossRef]

- Acharya, Viral, Katharina Bergant, Matteo Crosignani, Tim Eisert, and Fergal McCann. 2017. The Anatomy of the Transmission of Macroprudential Policies: Evidence from Ireland. Presented at 16th International Conference on Credit Risk Evaluation, Interest Rates, Growth, and Regulation, Ireland, September; Available online: https://www.atlantafed.org/-/media/documents/news/conferences/2017/1102-financial-regulation-fit-for-the-future/acharya-bergant-crosignani-eisert-mccann.pdf (accessed on 24 February 2022).

- Acharya, Viral, Katharina Bergant, Matteo Crosignani, Tim Eisert, and Fergal McCann. 2020. The Anatomy of the Transmission of Macroprudential Policies. IMF Working Papers. Washington, DC: IMF, vol. 2020, p. 58. [Google Scholar] [CrossRef]

- Albert, Juan-Francisco, Nerea Gómez-Fernández, and Carlos Ochando. 2019. Effects of unconventional monetary policy on income and wealth distribution: Evidence from United States and Eurozone. Panoeconomicus 66: 535–58. [Google Scholar] [CrossRef]

- Alvaredo, Facundo, Lucas Chancel, Thomas Piketty, Emmanuel Saez, and Gabriel Zucman. 2018. The elephant curve of global inequality and growth. AEA Papers and Proceedings 108: 103–8. [Google Scholar] [CrossRef]

- Alves, José, and Tomás Silva. 2020. An Empirical Assessment of Monetary Policy Channels on Income and Wealth Disparities. REM Working Paper 0144-2020. Available online: https://rem.rc.iseg.ulisboa.pt/wps/pdf/REM_WP_0144_2020.pdf (accessed on 24 February 2022).

- Amaral, Pedro. 2017. Monetary policy and inequality. In Economic Commentary. No. 1. Retrieved from Federal Reserve Bank of Cleveland Economic Commentary. Cleveland: Federal Reserve Bank of Cleveland. [Google Scholar]

- Apanisile, Olumuyiwa Tolulope. 2021. Monetary policy shocks and income inequality in Nigeria: Do effects of anticipated and unanticipated shocks differ? African Journal of Economic Review 9: 1–18. [Google Scholar] [CrossRef]

- Asteriou, Dimitris, and Stephen Hall. 2007. Applied Econometrics: A Modern Approach. New York: Palgrave Macmillan. [Google Scholar]

- Atkinson, Tony. 2014. Public Economics in an Age of Austerity. New York: Routledge. [Google Scholar]

- Batrancea, Larissa, Malar Mozhi Rathnaswamy, and Ioan Batrancea. 2021a. A panel data analysis of economic growth determinants in 34 African countries. Journal of Risk and Financial Management 14: 260. [Google Scholar] [CrossRef]

- Batrancea, Larissa, Mircea Iosif Rus, Ema Speranta Masca, and Ioan Dan Morar. 2021b. Fiscal Pressure as a Trigger of Financial Performance for the Energy Industry: An Empirical Investigation across a 16-Year Period. Energies 14: 3769. [Google Scholar] [CrossRef]

- Berisha, Edmond, John Meszaros, and Eric Olson. 2018. Income inequality, equities, household debt, and interest rates: Evidence from a century of data. Journal of International Money and Finance 80: 1–14. [Google Scholar] [CrossRef]

- Bernanke, Ben. 2015. Monetary Policy and Inequality. Ben Bernanke’s Blog at Brookings. Washington, DC: White House. [Google Scholar]

- Bhattacharya, Debapam. 2005. Asymptotic inference from multi-stage surveys. Journal of Econometrics 126: 145–71. [Google Scholar] [CrossRef]

- Bivens, Josh. 2015. Gauging the Impact of the Fed on Inequality during the Great Recession”, Hutchins Center on fiscal & monetary Policy at Brooking’s. Working Paper 12. Available online: https://files.epi.org/2015/quantitative-easing-and-inequality-josh-bivens.pdf (accessed on 2 February 2022).

- Bordo, Michael D., and Christopher M. Meissner. 2012. Does inequality lead to a financial crisis? Journal of International Money and Finance 31: 2147–61. [Google Scholar] [CrossRef]

- Brunnermeier, Markus K., Thomas M. Eisenbach, and Yuliy Sannikov. 2012. Macroeconomics with Financial Frictions: A Survey. Available online: https://scholar.princeton.edu/sites/default/files/survey_macrofinance.pdf (accessed on 15 February 2022).

- Bullard, James. 2014. Income Inequality and Monetary Policy: A Framework with Answers to Three Questions. Federal Reserve Bank of St. Louis. Available online: https://www.stlouisfed.org/-/media/project/frbstl/stlouisfed/Files/PDFs/Bullard/remarks/Bullard_CFR_26June2014_Final.pdf (accessed on 15 December 2021).

- Carney, Mark. 2016. Speech by Mr Mark Carney, Governor of the Bank of England and Chairman of the Financial Stability Board, at the Bank of England. London. June 30. Available online: https://www.bis.org/review/r160704c.pdf (accessed on 15 December 2021).

- Carpantier, Jean-Francois, Javier Olivera, and Philippe Van Kerm. 2018. Macroprudential policy and household wealth inequality. Journal of International Money and Finance 85: 262–77. [Google Scholar] [CrossRef]

- Carpenter, Seth B., and William M. Rodgers III. 2004. The disparate labor market impacts of monetary policy. Journal of Policy Analysis and Management 23: 813–30. [Google Scholar] [CrossRef]

- Casiraghi, Marco, Eugenio Gaiotti, Lisa Rodano, and Alessandro Secchi. 2018. A ‘reverse Robin Hood’? The distributional implications of non-standard monetary policy for Italian households. Journal of International Money and Finance 85: 215–35. [Google Scholar] [CrossRef]

- Cerutti, Eugenio, Stijn Claessens, and Luc Laeven. 2017. The use and effectiveness of macroprudential policies: New evidence. Journal of Financial Stability 28: 203–24. [Google Scholar] [CrossRef]

- Charemza, Wojaciech, and Derek Deadman. 1992. New Directions in Econometric Practice: General to Specific Modelling, Cointegration, and Vector Autoregression. Cheltenham: Edward Elgar Publishing, p. 370. [Google Scholar]

- Coibion, Olivier, Yuriy Gorodnichenko, Lorenz Kueng, and John Silvia. 2012. Innocent Bystanders? Monetary Policy and Inequality in the U.S. NBER Working Paper, 18170. Available online: http://www.nber.org/papers/w18170 (accessed on 2 February 2022).

- Coibion, Olivier, Yuriy Gorodnichenko, Lorenz Kueng, and John Silvia. 2017. Innocent Bystanders? Monetary Policy and Inequality. Journal of Monetary Economics 88: 70–89. [Google Scholar] [CrossRef]

- Colciago, Andrea, Anna Samarina, and Jakob de Haan. 2019. Central bank policies and income and wealth inequality: A survey. Journal of Economic Surveys 33: 1199–231. [Google Scholar] [CrossRef]

- Corak, Miles. 2013. Income Inequality, equality of opportunity, and intergenerational mobility. The Journal of Economic Perspectives 27: 79–102. [Google Scholar] [CrossRef]

- Davtyan, Karen. 2016. Income Inequality and Monetary Policy: An Analysis of the Long Run Relation. Research Institute of Applied Economics Working Papers. vol. 4, pp. 1–37. Available online: https://www.ub.edu/irea/working_papers/2016/201604.pdf (accessed on 21 January 2022).

- Diebold, Francis X., and Kamil Yilmaz. 2012. Better to give than to receive: Predictive directional measurement of volatility spillovers. International Journal of Forecasting 28: 57–66. [Google Scholar] [CrossRef]

- Doepke, Matthias, and Martin Schneider. 2006. Inflation and the redistribution of nominal wealth. Journal of Political Economy 114: 1069–97. [Google Scholar] [CrossRef]

- Dolado, Juan J., Gergő Motyovszki, and Evi Pappa. 2021. Monetary policy and inequality under labor market frictions and capital-skill complementarity. American Economic Journal: Macroeconomics 13: 292–332. [Google Scholar] [CrossRef]

- Domanski, Dietrich, Michela Scatigna, and Anna Zabai. 2016. Wealth Inequality and Monetary Policy. BIS Quarterly Review. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2744862 (accessed on 10 June 2022).

- Doumbia, Djeneba, and Tidiane Kinda. 2019. Reallocating Public Spending to Reduce Income Inequality: Can It Work? IMF Working Paper No. 19/188. Available online: https://ssrn.com/abstract=3471379 (accessed on 20 February 2022).

- El Herradi, Mehdi, and Aurélien Leroy. 2019. Monetary Policy and the Top One Percent: Evidence from a Century of Modern Economic History. De Nederlandsche Bank Working Paper No. 632 (2019). Available online: https://ssrn.com/abstract=3379740 (accessed on 10 June 2022).

- Erosa, Andrés, and Gustavo Ventura. 2002. On inflation as a regressive consumption tax. Journal of Monetary Economics 49: 761–95. [Google Scholar] [CrossRef]

- Evgenidis, Anastasios, and Apostolos Fasianos. 2021. Unconventional Monetary Policy and Wealth Inequalities in Great Britain. Oxford Bulletin of Economics and Statistics 83: 115–75. [Google Scholar] [CrossRef]

- Frees, Edward. 1995. Assessing cross-sectional correlation in panel data. Journal of Econometrics 69: 393–414. [Google Scholar] [CrossRef]

- Friedman, Milton. 1937. The use of ranks to avoid the assumption of normality implicit in the analysis of variance. Journal of the American Statistical Association 32: 675–701. [Google Scholar] [CrossRef]

- Frost, Jon, and René van Stralen. 2018. Macroprudential policy and income inequality. Journal of International Money and Finance 85: 278–90. [Google Scholar] [CrossRef]

- Furceri, Davide, Prakash Loungani, and Aleksandra Zdzienicka. 2018. The effects of monetary policy shocks on inequality. Journal of International Money and Finance 85: 168–86. [Google Scholar] [CrossRef]

- Galbraith, James. 1998. Created Unequal: The Crisis in American Pay. New York: Free Press. [Google Scholar]

- Gambacorta, Leonardo, Boris Hofmann, and Gert Peersman. 2012. The Effectiveness of Unconventional Monetary Policy at the Zero Lower Bound: A Cross-Country Analysis. BIS Working Paper No. 384. Basel: Bank of International Settlements. [Google Scholar]

- Gornemann, Nils, Keith Kuester, and Makoto Nakajima. 2012. Monetary Policy with Heterogeneous Agents. FRB of Philadelphia Working Paper No. 12-21. Available online: https://ssrn.com/abstract=2147841 (accessed on 10 June 2022).

- Guerello, Chiara. 2018. Conventional and unconventional monetary policy vs. household’s income distribution: An empirical analysis for the Euro Area. Journal of International Money and Finance 85: 187–214. [Google Scholar] [CrossRef]

- Güzel, Arif Eser, and Ünal Arslan. 2019. On the nexus between exchange rate and income distribution in Turkey: ARDL bound testing analysis. Economic Journal of Emerging Markets 11: 1–7. [Google Scholar] [CrossRef]

- Harris, Richard D. F., and Elias Tzavalis. 1999. Inference for unit roots in dynamic panels where the time dimension is fixed. Journal of Econometrics 91: 201–26. [Google Scholar] [CrossRef]

- Heathcote, Jonathan, Fabrizio Perri, and Giovanni L. Violante. 2010. Unequal we stand: An empirical analysis of economic inequality in the United States, 1967–2006. Review of Economic Dynamics 13: 15–51. [Google Scholar] [CrossRef]

- Hohberger, Stefan, Romanos Priftis, and Lukas Vogel. 2020. The distributional effects of conventional monetary policy and quantitative easing: Evidence from an estimated DSGE model. Journal of Banking & Finance 113: 105483. [Google Scholar] [CrossRef]

- Huber, Evelyne, and John D. Stephens. 2014. Income inequality and redistribution in post-industrial democracies: Demographic, economic and political determinants. Socio-Economic Review 12: 245–67. [Google Scholar] [CrossRef]

- Im, Kyung So, M. Hashem Pesaran, and Yongcheol Shin. 2003. Testing for unit roots in heterogeneous panels. Journal of Econometrics 115: 53–74. [Google Scholar] [CrossRef]

- Inui, Masayuki, Nao Sudou, and Tomoaki Yamada. 2017. Effects of Monetary Policy Shocks on Inequality in Japan. Bank of Japan Working Paper 17-e-3. Available online: https://ssrn.com/abstract=2982887 (accessed on 3 January 2022).

- Israel, Karl-Friedrich, and Sophia Latsos. 2019. The Impact of (un)Conventional Expansionary Monetary Policy on Income Inequality—Lessons from Japan. Working Paper, No. 163. Leipzig: Universität Leipzig, Wirtschaftswissenschaftliche Fakultät. [Google Scholar]

- Jeanneney, S. Guillaumont, and Ping Hua. 2001. How does real exchange rate influence income inequality between urban and rural areas in China? Journal of Development Economics 64: 529–45. [Google Scholar] [CrossRef]

- Kimura, Takeshi, and Jouchi Nakajima. 2016. Identifying conventional and unconventional monetary policy shocks: A latent threshold approach. The B.E. Journal of Macroeconomics 16: 277–300. [Google Scholar] [CrossRef]

- Konstantinou, Panagiotis, Anastasios Rizos, and Artemis Stratopoulou. 2022. Macroprudential policies and income inequality in former transition economies. Economic Change and Restructuring 55: 1005–62. [Google Scholar] [CrossRef]

- Kumhof, Michael, Romain Rancière, and Pablo Winant. 2015. Inequality, leverage and crises. American Economic Review 105: 1217–45. [Google Scholar] [CrossRef]

- Lee, Yoke Yee, Hui Xin Lim, Sock Hun Lim, and Yie Tien Quek. 2017. Income Distribution and Economic Growth: A Panel Data Analysis. Unpublished Bachelor’s thesis, University Tunku Rahman, Pulau Pinang, Malaysia. [Google Scholar]

- Lenza, Michele, and Jiri Slacalek. 2019. How Does Monetary Policy Affect Income and Wealth Inequality? Evidence from Quantitative Easing in the Euro Area. ECB Working Paper Series No 2190/October 201. Luxembourg: EU Publications. [Google Scholar] [CrossRef]

- Mumtaz, Haroon, and Angeliki Theophilopoulou. 2017. The impact of monetary policy on inequality in the UK. An empirical analysis. European Economic Review 98: 410–23. [Google Scholar] [CrossRef]

- Nakajima, Makoto. 2015. Business Cycles in the Equilibrium Model of Labor Market Search and Self-insurance. International Economic Review 53: 399–432. [Google Scholar] [CrossRef]

- OECD (Organization for Economic Cooperation and Development—OECD). 2014. Society at a Glance 2014: OECD Social Indicators. Paris: OECD Publishing, pp. 1–143. [Google Scholar]

- Pesaran, Hashen. 2004. General Diagnostic Tests for Cross-Sectional Dependence in Panels. Cambridge Working Papers in Economics No. 0435. Cambridge: Faculty of Economics, The University of Cambridge. [Google Scholar] [CrossRef]

- Piketty, Thomas. 2014. “Capital in the 21st Century”. Cambridge: Harvard University Press. [Google Scholar]

- Rajan, Raghuram. 2010. “Fault Lines: How Hidden Fractures Still Threaten the World Economy”. Princeton: Princeton University Press. [Google Scholar]

- Romer, Christina D., and David H. Romer. 1999. Monetary policy and the well-being of the poor. Economic Review 84: 21–49. [Google Scholar]

- Rupprecht, Manuel. 2020. Income and wealth of euro area households in times of ultra-loose monetary policy: Stylised facts from new national and financial accounts data. Austrian Institute for Economic Research 47: 281–302. [Google Scholar] [CrossRef]

- Saiki, Ayako, and Jon Frost. 2014. Does unconventional monetary policy affect inequality? Evidence from Japan. Applied Economics 46: 4445–54. [Google Scholar] [CrossRef]

- Sánchez, Angeles, and Antonio L. Pérez-Corral. 2018. Government social expenditure and income inequalities in the European Union. Review of Public Economics 227: 133–56. Available online: https://ideas.repec.org/a/hpe/journl/y2018v227i4p133-156.html (accessed on 28 April 2022).

- Sarfati, Hedva. 2016. OECD. In it together: Why less inequality benefits all. Paris, 2015. p. 332 ISBN 978–264-23266-2. International Social Security Review 68: 115–17. [Google Scholar] [CrossRef]

- Sheng, Xin, and Rangan Gupta. 2021. The Impact of Oil Price Shocks on Income Inequality: Evidence from State-Level Data of the United States. Working Papers 202128. Department of Economics, University of Pretoria. Available online: https://www.up.ac.za/media/shared/61/WP/wp_2022_17.zp217507.pdf (accessed on 3 April 2022).

- Solt, Frederick. 2020. The standardized world Income-inequality database. Social Science Quarterly 90: 231–42. [Google Scholar] [CrossRef]

- Taghizadeh-Hesary, Farhad, Naoyuki Yoshino, and Sayoko Shimizu. 2018. The Impact of Monetary and Tax Policy on Income Inequality in Japan. ADBI Working Paper 837. Tokyo: Asian Development Bank Institute. Available online: https://www.researchgate.net/publication/325967488_The_Impact_of_Monetary_and_Tax_Policy_on_Income_Inequality_in_Japan (accessed on 23 April 2022).

- Tzur-Ilan, Nitzan. 2016. The effect of credit constraints on housing choices: The case of LTV limits. Presented at Bank of Israel Research Department Conference, Jerusalem, Israel, December; Available online: https://www.boi.org.il/he/newsandpublications/pressreleases/documents/%D7%A0%D7%99%D7%A6%D7%9F%20%D7%A6%D7%95%D7%A8%20%D7%90%D7%99%D7%9C%D7%9F.pdf (accessed on 10 June 2022).

- Wahiba, Nasfi Fkili, and Malek El Weriemmi. 2014. The relationship between Economic growth and income inequality. International Journal of Economics and Financial Issues 4: 135–43. [Google Scholar]

- Wilkinson, Richard, and Kate Pickett. 2009. The Spirit Level: Why More Equal Societies Almost Always a Bette. Edited by S. Tuters. London: Allen Lane. [Google Scholar]

- Williamson, Stephen. 2009. Monetary policy and distribution. Journal of Monetary Economics 55: 1038–53. [Google Scholar] [CrossRef]

- World Development Indicators. 2022. World Bank. Washington, DC. Available online: http://data.worldbank.org/data-catalog/world-development-indicators (accessed on 3 January 2022).

- Yellen, Chair Janet. 2014. Monetary Policy and Financial Stability; Michel Camdessus Central Banking Lecture. Washington, DC: International Monetary Fund. Available online: https://www.federalreserve.gov/newsevents/speech/yellen20140702a.htm (accessed on 20 January 2022).

- Zinman, Janath. 2010. Restricting consumer credit access: Household survey evidence on effects around the Oregon rate cap. Journal of Banking and Finance 34: 546–56. [Google Scholar] [CrossRef]

- Zungu, Lindokuhle Talent, and Lorraine Greyling. 2022. Investigating the asymmetric effect of income inequality on financial fragility in South Africa and selected emerging markets: A Bayesian approach with hierarchical priors. Asian Journal of Economics and Banking. forthcoming. [Google Scholar]

- Zungu, Lindokuhle Talent, Lorraine Greyling, and Nkanyiso Mbatha. 2021. Economic growth and income inequality: A non-linear econometrics analysis of the SADC region, 1995–2015. African Journal of Economic and Management Studies 12: 285–301. [Google Scholar] [CrossRef]

| Descriptive Statistics | Im-Pesaran-Shin | Harris-Tzavalis | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Variables | Mea | Std.d | Min | Max | SKW | KUR | JB-ST | JB-P | Level | 1st ∆ | Inte | Level | 1st ∆ | Inte |

| incPT10 | 50.54 | 0.06 | 30.58 | 65.44 | −0.03 | 2.19 | 8.23 | 0.01 | 1.48 | −4.96 *** | I(1) | 0.68 | −4.41 *** | I(1) |

| incPT1 | 45.39 | 0.04 | 8.10 | 63.50 | −0.33 | 2.16 | 35.51 | 0.00 | 2.46 | −6.88 *** | I(1) | 3.89 | −15.45 *** | I(1) |

| Gini | 45.29 | 6.33 | 8.100 | 63.50 | −0.30 | 3.046 | 11.60 | 0.00 | 1.77 | −5.99 *** | I(1) | 2.37 | −15.83 *** | I(1) |

| Cb | 4.12 | 3.04 | −0.36 | 22.49 | −0.07 | 3.31 | 20.14 | 0.00 | 2.87 | −6.01 ** | I(1) | 3.33 | −4.99 *** | I(1) |

| Dp | 4.710 | 3.033 | −0.36 | 22.49 | −0.45 | 3.80 | 28.66 | 0.00 | 1.99 | −3.43 *** | I(1) | 3.22 | −4.99 ** | I(1) |

| Hip | 89.14 | 26.71 | 0.10 | 162.69 | −0.34 | 2.10 | 12.92 | 0.05 | 1.33 | −3.33 ** | I(1) | 1.28 | 14.20 *** | I(1) |

| Unmpl | 6.95 | 6.24 | 0.25 | 33.29 | −0.33 | 2.97 | 9.85 | 0.03 | 2.24 | −8.85 ** | I(1) | 1.72 | −9.17 *** | I(1) |

| Ltir | 6.44 | 10.03 | −11.38 | 48.34 | −0.49 | 3.07 | 78.31 | 0.00 | −7.23 *** | I(1) | −0.72 | −3.86 ** | I(1) | |

| Oil | 4.62 | 0.27 | 4.08 | 6.57 | −0.12 | 1.98 | 80.85 | 0.00 | −0.44 | −3.79 ** | I(1) | 0.72 | −8.80 *** | I(1) |

| Stir | 92.60 | 23.61 | −38.60 | 131.24 | −0.67 | 2.51 | 69.07 | 0.06 | −4.90 * | I(0) | 0.33 | −14.59 *** | I(1) | |

| g | 8.24 | 8.34 | 14.48 | 3.62 | −0.23 | 3.09 | 76.09 | 0.00 | −1.20 | −8.99 *** | I(1) | 0.11 | −17.54 *** | I(1) |

| gpp | 10.92 | 112.60 | 75.66 | 61.90 | −0.11 | 3.87 | 70.8 | 0.08 | 0.33 | −6.11 | I(1) | 2.41 | −14.59 *** | I(1) |

| Pedroni Tests for Cointegration | Tests for Cross-Sectional Independence | ||||

|---|---|---|---|---|---|

| Augmented Dickey-Fuller t | 5.984 | Pr = 0.000 | Friedman’s test | 120.021 | Pr = 0.000 |

| Modified Phillips-Perron t | 2.669 | Pr = 0.003 | Frees’ test | 0.583 | Pr = 0.000 |

| Phillips-Perron t | 4.018 | Pr = 0.000 | Pesaran’s test | 8.243 | Pr = 0.000 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zungu, L.T.; Greyling, L. Exploring the Dynamic Shock of Unconventional Monetary Policy Channels on Income Inequality: A Panel VAR Approach. Soc. Sci. 2022, 11, 369. https://doi.org/10.3390/socsci11080369

Zungu LT, Greyling L. Exploring the Dynamic Shock of Unconventional Monetary Policy Channels on Income Inequality: A Panel VAR Approach. Social Sciences. 2022; 11(8):369. https://doi.org/10.3390/socsci11080369

Chicago/Turabian StyleZungu, Lindokuhle Talent, and Lorraine Greyling. 2022. "Exploring the Dynamic Shock of Unconventional Monetary Policy Channels on Income Inequality: A Panel VAR Approach" Social Sciences 11, no. 8: 369. https://doi.org/10.3390/socsci11080369