Study on the Driving Path of Contractors’ Low-Carbon Behavior under Institutional Logic and Technological Logic

Abstract

:1. Introduction

2. Theoretical Basis and Research Hypothesis

2.1. Low-Carbon Behavior of Contractors

2.2. Drivers of Low-Carbon Behavior of Contractors

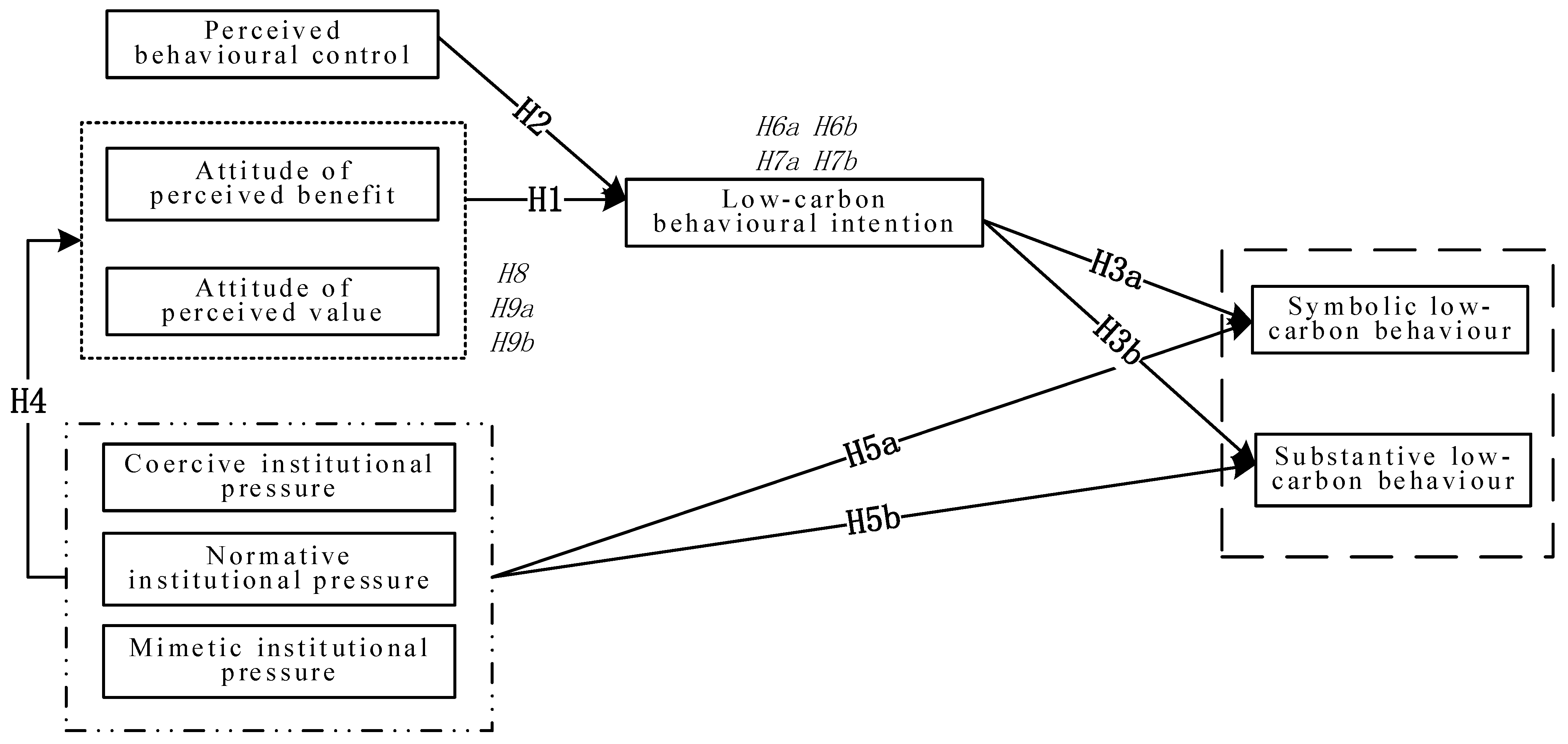

2.3. Research Hypothesis

2.3.1. Behavioral Attitude and Behavioral Intention

2.3.2. Perceived Behavioral Control and Behavioral Intention

2.3.3. Behavioral Intention and Low-Carbon Behavior

2.3.4. Institutional Pressure and Behavioral Attitude

2.3.5. Institutional Pressure and LCB

2.3.6. The Mediating Role of Low-Carbon Behavioral Intention

2.3.7. The Mediating Role of Low-Carbon Behavioral Attitude

3. Methodology

3.1. Questionnaire Design and Data Sampling

3.2. Measurement of Variables

4. Data Analysis

4.1. Reliability Analysis and Validity Analysis

4.2. Common Method Bias Test

4.3. Hypothesis Testing

4.3.1. Direct Effect Tests

4.3.2. Mediating Effect Test

4.4. Analysis of Pathway Differences

5. Implication of the Study

6. Conclusions and Limitations

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Lu, J.C.; OuYang, H.X.; Han, L. Evolutionary Mechanism of Low-carbon Transformation of Construction Enterprises under Multi-agent Interaction Games. Evolutionary. J. Beijing Inst. Technol. (Soc. Sci. Ed.) 2019, 21, 17–26. [Google Scholar]

- Xie, L.; Huang, M.; Xia, B.; Skitmore, M. Megaproject Environmentally Responsible Behavior in China: A Test of the Theory of Planned Behavior. Int. J. Environ. Res. Public Health 2022, 19, 6581. [Google Scholar] [CrossRef] [PubMed]

- He, Q.H.; Wang, Z.L.; Wang, G.; Zuo, J.; Wu, G.D.; Liu, B.S. To be green or not to be: How environmental regulations shape contractor greenwashing behaviors in construction projects. Sustain. Cities Soc. 2020, 63, 102462. [Google Scholar] [CrossRef]

- Chen, L.W.; Zhao, S.W.; Zhang, Z.J. Research on Related Drivers for Green Building Development—A Literature Review. Resour. Dev. Mark. 2018, 34, 1229–1236. [Google Scholar]

- Zhang, L.; Zhou, J.L. Drivers and Barriers of Developing Low-carbon Buildings in China: Real Estate Developers’ Perspectives. Int. J. Environ. Technol. 2015, 18, 254–272. [Google Scholar] [CrossRef]

- Farrukh, A.; Mathrani, S.; Sajjad, A. A Natural Resource and Institutional Theory-Based View of Green-Lean-Six Sigma Drivers for Environmental Management. Bus. Strategy Environ. 2022, 31, 1074–1090. [Google Scholar] [CrossRef]

- Jiang, H.T.; Chen, Z.X.; Ren, R.; Zhang, Y.C.; Yang, D.N.; Zhang, Y.L. Substantive and Symbolic Corporate LCB: Intra-Firm Influences. Econ. Sci. 2017, 218, 88–100. [Google Scholar]

- Yao, Q.; Hu, H.Y.; Feng, Y.Z. A Literature Review of Corporate Greenwashing and Prospects. Ecol. Econ. 2022, 38, 86–92+108. [Google Scholar]

- Dong, B.K.; Chang, X.F.; Yang, Y.F. Research on the Influence of Manufacturing Firms’ Internal Capabilities on Their Green Innovation Cooperation Under Institutional Pressure. J. Beijing Univ. Technol. (Soc. Sci. Ed.) 2022, 22, 171–186. [Google Scholar]

- Meyer, J.W.; Rowan, B. Institutionalized Organizations: Formal Structure as Myth and Ceremony. Am. J. Sociol. 1977, 83, 340–363. [Google Scholar] [CrossRef] [Green Version]

- Paulraj, A. Environmental Motivations: A Classification Scheme and Its Impact on Environmental Strategies and Practices. Bus. Strategy Environ. 2009, 18, 453–468. [Google Scholar] [CrossRef]

- Liu, Z.; Cui, L.G.; Yang, J. The Institutional Logics, Legitimacy Mechanisms and the Growth of Social Enterprises. Chin. J. Manag. 2015, 12, 565–575. [Google Scholar]

- Marquis, C.; Qian, C. Corporate Social Responsibility Reporting in China: Symbol or Substance? Organ. Sci. 2014, 25, 127–148. [Google Scholar] [CrossRef] [Green Version]

- Yang, Y.F.; Ye, K.H. Analysis of the Characteristics of Low Carbon Construction and Low Carbon Competitiveness of Analysis of the Characteristics of Low Carbon Construction and Low Carbon Competitiveness of Construction Enterprises. Proj. Manag. Technol. 2015, 13, 43–47. [Google Scholar]

- Gou, Q.W.; Cai, N. Institutional Complexity and Corporate Environmental Strategy: Based on the Institutional Logic Perspective. Comp. Econ. Soc. Syst. 2015, 177, 125–138. [Google Scholar]

- Suchman, M.C. Managing Legitimacy: Strategic and Institutional Approaches. Acad. Manag. Rev. 1995, 20, 571–610. [Google Scholar] [CrossRef]

- Jin, B.; Kirsch, D.A. The Search for Alternatives to Internal Combustion: Instantiation Mechanisms of Institutional Logics among Scientists and Engineers. Ind. Innov. 2022, 29, 1231–1262. [Google Scholar] [CrossRef]

- Wu, J.; Wu, Z.; Harrigan, K.R. Process Quality Management and Technological Innovation Revisited: A Contingency Perspective from an Emerging Market. J. Technol. Transf. 2019, 44, 1871–1890. [Google Scholar] [CrossRef]

- Li, H.G.; Zhang, Y.Q.; Chen, Z.W. Technological Logic, Institutional Logic and Innovation Performance of New Ventures--An Analysis on the Development Stage of Start-up. Sci. Technol. Prog. Policy 2017, 34, 83–89. [Google Scholar]

- Chen, Y.; Xu, X.M.; Tan, L.B. A Review on Legitimacy in the Organizational Institution Theory. East. China. Econ. Manag. 2012, 26, 137–142. [Google Scholar]

- Lian, G.H.; Xu, A.T.; Zhu, Y.H. Substantive Green Innovation or Symbolic Green Innovation? The Impact of ER on Corporate Green Innovation Based on the Dual Moderating Effects. J. Innov. Knowl. 2022, 7, 100203. [Google Scholar] [CrossRef]

- Zhou, Z.F.; Nie, L.; Ji, H.Y. Does a Firm’s Low-carbon Awareness Promote LCBs? Empirical Evidence from China. J. Clean. Prod. 2020, 244, 118903. [Google Scholar] [CrossRef]

- Gou, Q.W.; Cai, N.; Xin, Y.Y. The Decoupling of Corporate Environmental Behavior: Institutional Logic Perspective. Zhejiang Soc. Sci. 2019, 270, 19–27+155–156. [Google Scholar]

- Zheng, S.Q.; Ye, K.H.; Jiang, W.Y.; Xiong, B.; Zuo, J. Stakeholder Approaches to Construction Contractors’ Corporate Social Responsibility in Developing Countries: A China Case. J. Residuals Sci. Technol. 2016, 13, 292.1–292.8. [Google Scholar]

- Zhang, L.Y.; Zhou, J.L. The Effect of Carbon Reduction Regulations on Contractors’ Awareness and Behaviors in China’s Building Sector. J. Clean. Prod. 2016, 113, 93–101. [Google Scholar] [CrossRef]

- Zott, C.; Huy, Q.N. How Entrepreneurs Use Symbolic Management to Acquire Resources. Admin. Sci. Quart. 2007, 52, 70–105. [Google Scholar] [CrossRef] [Green Version]

- Zhang, Y.; Zhou, X.H.; Zhang, H.; Sui, Y. Development of the Scale of Symbolic Action and Its Impact on the Legitimacy of New Ventures: Moderating Effect of Environmental Munificence. J. Syst. Manag. 2023, 32, 154–166. [Google Scholar]

- Berrone, P.; Gomez-Mejia, L.R. Environmental Performance and Executive Compensation: An Integrated Agency-Institutional Perspective. Acad. Manag. J. 2009, 52, 103–126. [Google Scholar] [CrossRef]

- Chen, C.; Ding, J.Y. Research on the Influencing Factors of the Contractor’s Promotion of Project Value-added Behaviors. J. Wuhan Univ. Technol. (Inf. Manag. Eng.) 2018, 40, 649–655. [Google Scholar]

- Yan, L.; Guo, L.; Han, Y.F. Study on the Factors Influencing the Contractor’s Performance Behaviors in the Context of Project General Contracting--Based on Theory of Planned Behavior. Soft Sci. 2019, 33, 126–134. [Google Scholar]

- Wu, Z.; Ann, T.W.; Shen, L. Investigating the Determinants of Contractor’s Construction and Demolition Waste Management Behavior in Mainland China. Waste Manag. 2017, 60, 290–300. [Google Scholar] [CrossRef]

- Zhang, G.; Zhang, X.J. Driver Factors of Corporate Green Innovative Strategy Based on Planning Behavior Theory. J. Bus. Econ. 2013, 261, 47–56. [Google Scholar]

- Gatignon, H.; Xuereb, J.M. Strategic Orientation of the Firm and New Product Performance. J. Mark. Res. 1997, 34, 77–90. [Google Scholar] [CrossRef]

- Schwartz, M.S.; Carroll, A.B. Corporate Social Responsibility: A Three-Domain Approach. Bus. Ethics Q. 2003, 13, 503–530. [Google Scholar] [CrossRef]

- Dimaggio, P.J.; Powell, W.W. The Iron Cage Revisited: Institutional Isomorphism and Collective Rationality in Organizational Fields. Am. Sociol. Rev. 1983, 48, 147–160. [Google Scholar] [CrossRef] [Green Version]

- Kurdi, S.; Apriliyanto, N. Implementation of Quick Response Code in Indonesian Restaurants: Integration of Protection Motivation Theory and Theory of Planned Behavior. J. Mantik 2022, 6, 1920–1928. [Google Scholar]

- Hagger, M.S.; Cheung, M.W.L.; Ajzen, I.; Hamilton, K. Perceived Behavioral Control Moderating Effects in the Theory of Planned Behavior: A meta-analysis. Health Psychol. 2022, 41, 155–167. [Google Scholar] [CrossRef]

- Liñán, F.; Santos, F.J. Does Social Capital Affect Entrepreneurial Intentions? Int. Adv. Econ. Res. 2007, 13, 443–453. [Google Scholar] [CrossRef]

- Feng, Z. Conformity or Compliance: Corporations’ Choice of Social Responsibility under Institutional Pressure. Financ. Econ. 2014, 313, 82–90. [Google Scholar]

- Wu, L.D.; Wang, K.; Huang, H.X. A Research Review of External Environment Uncertainty. Chin. J. Manag. 2012, 9, 1712–1717. [Google Scholar]

- Zhao, X.L.; Yao, J.; Liu, Z.W.; Song, C. A Study on Low Carbon Oriented Firm Behavior Management Based on ABM Model. Manag. Rev. 2013, 25, 91–99. [Google Scholar]

- Hao, Y.H.; Tang, Y.H.; Wang, S.X. On Institution Rationality and Behavior Logic of Corporate Social Responsibility:From the Perspective of Legitimacy. J. Bus. Econ. 2012, 249, 74–81. [Google Scholar]

- Buysse, K.; Verbeke, A. Proactive Environmental Strategies: A Stakeholder Management Perspective. Strateg. Manag. J. 2003, 24, 453–470. [Google Scholar] [CrossRef]

- Bansal, P.; Roth, K. Why Companies Go Green: A Model of Ecological Responsiveness. Acad. Manag. J. 2000, 43, 717–736. [Google Scholar] [CrossRef]

- Hair, J.F.; Ringle, C.M.; Sarstedt, M. PLS-SEM: Indeed a Silver Bullet. J. Mark. Theory Prac. 2011, 19, 139–152. [Google Scholar] [CrossRef]

- Banerjee, S.B.; Iyer, E.S.; Kashyap, R.K. Corporate Environmentalism: Antecedents and Influence of Industry Type. J. Mark. 2003, 67, 106–122. [Google Scholar] [CrossRef]

- Beck, L.; Ajzen, I. Predicting Dishonest Actions Using the Theory of Planned Behavior. J. Res. Pers. 1991, 25, 285–301. [Google Scholar] [CrossRef]

- Taylor, S.; Todd, P. Decomposition and Crossover Effects in the Theory of Planned Behavior: A Study of Consumer Adoption Intentions. Int. J. Res. Mark. 1995, 12, 137–155. [Google Scholar] [CrossRef]

- Zhu, Q.; Geng, Y. Drivers and Barriers of Extended Supply Chain Practices for Energy Saving and Emission Reduction Among Chinese Manufacturers. J. Clean. Prod. 2013, 40, 6–12. [Google Scholar] [CrossRef]

- Teo, H.H.; Wei, K.K.; Benbasat, I. Predicting Intention to Adopt Interorganizational Linkages: An Institutional Perspective. Mis. Quart. 2003, 27, 19–49. [Google Scholar] [CrossRef] [Green Version]

- Boiral, O.; Henri, J.F. Modelling the Impact of ISO 14001 on Environmental Performance: A Comparative Approach. J. Environ. Manag. 2012, 99, 84–97. [Google Scholar] [CrossRef]

- Giblin, M.J.; Burruss, G.W. Developing a Measurement Model of Institutional Processes in Policing. Policing 2009, 32, 351–376. [Google Scholar] [CrossRef]

- Zheng, X.; Lu, Y.J.; LI, Y.K. Formation of Interorganizational Relational Behavior in Megaprojects: Perspective of the Extended Theory of Planned Behavior. J. Manag. Eng. 2018, 34, 04017052. [Google Scholar] [CrossRef]

- Fornell, C.; Larcker, D.F. Structural Equation Models with Unobservable Variables and Measurement Error: Algebra and Statistics. J. Mark. Res. 1981, 18, 382–388. [Google Scholar] [CrossRef]

- Chin, W.W. The Partial Least Squares Approach to Structural Equation Modeling. Mod. Method Bus. Res. 1998, 295, 295–336. [Google Scholar]

- Hu, L.; Bentler, P.M. Fit Indices in Covariance Structure Modeling: Sensitivity to Underparameterized Model Misspecification. Psychol. Methods 1998, 3, 424. [Google Scholar] [CrossRef]

- Zhou, S.; Zhou, A.; Feng, J.Z.; Jiang, S.S. Dynamic Capabilities and Organizational Performance: The Mediating Role of Innovation. J. Manag. Organ. 2019, 25, 731–747. [Google Scholar] [CrossRef] [Green Version]

- Cohen, P.; West, S.G.; Aiken, L.S. Applied Multiple Regression/Correlation Analysis for the Behavioral Sciences; Psychology Press: London, UK, 2014. [Google Scholar]

- Haque, F.; Ntim, C.G. Executive Compensation, Sustainable Compensation Policy, Carbon Performance and Market Value. Brit. J. Manag. 2020, 31, 525–546. [Google Scholar] [CrossRef]

- Ren, S.L.; He, D.J.; Zhang, T.; Chen, X.H. Symbolic Reactions or Substantive Pro-environmental Behavior? An Empirical Study of Corporate Environmental Performance under the Government’s Environmental Subsidy Scheme. Bus. Strategy Environ. 2019, 28, 1148–1165. [Google Scholar] [CrossRef]

- Dahlmann, F.; Branicki, L.; Brammer, S. Managing Carbon Aspirations: The Influence of Corporate Climate Change Targets on Environmental Performance. J. Bus. Ethics 2019, 158, 1–24. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

| Elements of TPB | Connotation of the Elements | Logical Orientation | Post-Decomposition Factors | Connotation of the Factors |

|---|---|---|---|---|

| Perceived behavioral control | Contractors’ judgements and perceptions of the ease of implementing LCB | Technological logic | Perceived behavioral control (PBC) | Assessment of the resources and capabilities required for corporates to develop and apply new carbon reduction technologies |

| Behavioral attitude | Contractors’ expectations and evaluation of the likelihood of low-carbon behavioral outcomes | Technological logic | Attitude of perceived benefit (BA) | The idea of LCB due to the economic incentives created by technological innovation |

| Institutional logic | Attitude of perceived value (VA) | Corporate social responsibility in the pursuit of low-carbon environment | ||

| Subjective norm | Contractors’ perception of the expectations of key stakeholders and the willingness of contractor to conform to their implementation of LCB | Institutional logic | Coercive institutional pressure (CP) | derived from formal systems such as laws, norms, contracts, etc., which function through regulatory legitimacy |

| Normative institutional pressure (NP) | Professional codes, codes of conduct, ethics, and values set by professional bodies, the media and the public, which function through normative legitimacy | |||

| Mimetic institutional pressure (MP) | derived from a firm’s perception of the LCB of its competitors in the market, functioning through cognitive legitimacy |

| Characteristics of Sample | Category | Number | Percentage/% | Characteristics of Sample | Category | Number | Percentage/% |

|---|---|---|---|---|---|---|---|

| Gender | Male | 126 | 73 | Corporate ownership | State-owned | 80 | 46 |

| Female | 47 | 27 | Non-state-owned | 93 | 54 | ||

| Age (Year) | ≤25 | 31 | 18 | Type of project territory | Rural areas and counties | 52 | 30 |

| 26–30 | 42 | 24 | |||||

| 31–40 | 50 | 29 | Small and medium-sized cities | 48 | 28 | ||

| 41–50 | 40 | 23 | |||||

| >50 | 10 | 6 | Large cities | 73 | 42 | ||

| Academic qualification | Postgraduate and below | 29 | 17 | ||||

| Undergraduate | 88 | 51 | Project territory | Eastern China | 78 | 45 | |

| Master | 36 | 21 | South China | 12 | 7 | ||

| PhD | 10 | 6 | Central China | 14 | 8 | ||

| Experience of working (Year) | ≤5 | 36 | 21 | North China | 33 | 19 | |

| 6–10 | 42 | 24 | Northwest China | 14 | 8 | ||

| 11–15 | 26 | 15 | Southwest China | 9 | 5 | ||

| 16–20 | 22 | 13 | Northeast China | 10 | 6 | ||

| >20 | 47 | 27 | Hong Kong, Macau and Taiwan | 2 | 1 | ||

| Level of Management | Middle and senior management | 48 | 28 | Overseas countries | 2 | 1 | |

| Grassroots managers | 57 | 33 | Type of project | Housing engineering | 88 | 51 | |

| Professional and technical staff | 28 | 16 | Municipal and public works | 31 | 18 | ||

| General staff | 40 | 23 | Water resources, electricity engineering | 36 | 21 | ||

| General contracting qualification | Special grade | 90 | 52 | Road, bridge, port and navigation works | 17 | 10 | |

| Grade 1 | 64 | 37 | Project size | Small-scale projects | 42 | 24 | |

| Grade 2 | 17 | 10 | Medium-scale projects | 31 | 18 | ||

| Grade 3 | 5 | 3 | Large-scale projects | 100 | 58 |

| Latent Variables | Numbers of Items | Description of Measurement Items | Key Source(s) | CR | Cronbach’s Alpha | AVE | |

|---|---|---|---|---|---|---|---|

| Second-Order | First-Order | ||||||

| LBA | BA | BA1 | Reduce material and energy consumption, thus reducing costs | Banerjee [46] | 0.920 | 0.884 | 0.742 |

| BA2 | Improve project management and thus increasing profits | ||||||

| BA3 | Enhance corporate image and reputation | ||||||

| BA4 | Expand the construction market, thus increase the chances of winning tenders | ||||||

| VA | VA1 | Have a responsibility and a mission to reduce carbon emissions | Yan [30] | 0.947 | 0.916 | 0.857 | |

| VA2 | Gain a sense of achievement and honor | ||||||

| VA3 | In line with the direction of business development | ||||||

| / | PBC | PBC1 | Availability of resources, knowledge and competence | Beck [47]; Taylor [48] | 0.896 | 0.827 | 0.742 |

| PBC2 | Able to implement LCB | ||||||

| PBC3 | Easy to implement LCB | ||||||

| PBC4 | With policy support such as financial incentives and tax subsidies | ||||||

| PBC5 | Suppliers are environmentally friendly. | ||||||

| IP | CP | CP1 | National laws and regulations, standard specification requirements | Zhu [49]; Feng [39]; Teo [50] | 0.927 | 0.898 | 0.760 |

| CP2 | Legal and regulatory requirements of the project site | ||||||

| CP3 | Government regulation and penalties for carbon reduction | ||||||

| CP4 | Low-carbon requirements for employer | ||||||

| NP | NP1 | Guidance from non-governmental organizations such as trade associations | Zhu [49]; Boiral [51] | 0.795 | 0.655 | 0.571 | |

| NP2 | Press monitoring by the media | ||||||

| NP3 | Low-carbon awareness and demand from the public (including the project’s local community) | ||||||

| MP | MP1 | Level of implementation by other contractors | Teo [50]; Giblin [52] | 0.920 | 0.869 | 0.792 | |

| MP2 | Benefits of implementation for other contractors (practical effects) | ||||||

| MP3 | Implementation benefits for other contractors (industry reputation) | ||||||

| / | BI | BI1 | Intention at the beginning | Zheng [53] | 0.941 | 0.905 | 0.841 |

| BI2 | Intention for the future | ||||||

| BI3 | Intention to continue | ||||||

| LCB | SYM | SYM1 | Low-carbon concepts | Zhou [22]; Gou [15]; Jiang [7] | 0.936 | 0.917 | 0.713 |

| SYM2 | Low-carbon public service or educational activities | ||||||

| SYM3 | Promotion of low-carbon production ideas, experience and practices | ||||||

| SYM4 | Stated commitment to low-carbon management objectives | ||||||

| SYM5 | Governing documents for carbon emission reduction | ||||||

| SYM6 | Management structure for carbon emission reduction | ||||||

| SYM7 | Carbon emission reduction training for staff | ||||||

| SUB | SUB1 | Low-carbon building materials and swing materials | Zhang [5] | 0.858 | 0.805 | 0.681 | |

| SUB2 | Energy-efficient machinery and equipment | ||||||

| SUB3 | Low-carbon construction techniques and technologies | ||||||

| SUB4 | Energy efficiency | ||||||

| SUB5 | Proportion of clean energy used | ||||||

| SUB6 | Implementing an internal low-carbon control and monitoring system | ||||||

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| General Contracting Qualification | ||||||||||||||

| Corporate ownership | −0.089 | |||||||||||||

| Type of project territory | 0.082 | 0.009 | ||||||||||||

| Type of project | 0.118 | −0.208 * | −0.036 | |||||||||||

| Project size | 0.390 ** | −0.036 | 0.441 ** | 0.062 | ||||||||||

| LBA | 0.029 | −0.230 | 0.268 * | 0.144 | 0.330 ** | 0.862 | ||||||||

| VA | 0.232 ** | −0.206 * | 0.196 | 0.247 * | 0.163 | 0.830 | 0.926 | |||||||

| PBC | 0.156 * | −0.210 * | 0.160 | 0.144 | 0.129 * | 0.612 | 0.398 | 0.862 | ||||||

| CP | 0.204 * | −0.280 * | 0.254 ** | 0.137 | 0.219 ** | 0.462 | 0.414 | 0.666 | 0.872 | |||||

| NP | 0.19 | −0.268 * | 0.245 * | 0.189 | 0.152 * | 0.331 | 0.608 | 0.507 | 0.527 | 0.756 | ||||

| MI | 0.204 * | −0.176 | 0.058 | 0.216 | 0.065 | 0.306 | 0.618 | 0.511 | 0.445 | 0.607 | 0.89 | |||

| BI | 0.125 * | −0.241 | 0.236 ** | 0.142 | 0.212 ** | 0.535 | 0.615 | 0.659 | 0.564 | 0.599 | 0.557 | 0.917 | ||

| SYM | 0.217 * | −0.121 * | 0.205 | 0.075 | 0.152 | 0.303 | 0.483 | 0.316 | 0.426 | 0.579 | 0.486 | 0.409 | 0.844 | |

| SUB | 0.314 * | −0.019 | 0.175 * | 0.129 * | 0.174 * | 0.441 | 0.421 | 0.395 | 0.498 | 0.591 | 0.404 | 0.433 | 0.744 | 0.762 |

| Hypothetical Relationships | Description of Path | Path Coefficient | 95% Confidence Interval | Comment | |

|---|---|---|---|---|---|

| Upper-Bound | Lower-Bound | ||||

| H6a | LBA→BI→SYM | 0.091 ** | 0.009 | 0.173 | Significant |

| H6b | LBA→BI→SUB | 0.076 ** | 0.007 | 0.158 | Significant |

| H7a | PBC→BI→SYM | 0.092 | −0.001 | 0.251 | Not Significant |

| H7b | PBC→BI→SUB | 0.044 | −0.015 | 0.041 | Not Significant |

| H8 | IP→LBA→BI | 0.146 *** | 0.016 | 0.298 | Significant |

| H9a | IP→LBA→BI→SYM | 0.056 ** | 0.004 | 0.194 | Significant |

| H9b | IP→LBA→BI→SUB | 0.033 * | 0.002 | 0.103 | Significant |

| Groups | Description of Path | Comparison | T-Value | Conclusion |

|---|---|---|---|---|

| Group A | P1: LBA→BI→SYM | P1 vs. P2 | 2.124 * | P1 > P2 |

| P2: LBA→BI→SUB | ||||

| P3: IP→SYM | P3 vs. P4 | −1.092 (ns) | P3 = P4 | |

| P4: IP→SUB | ||||

| P5: IP→LBA→BI→SYM | P5 vs. P6 | 1.994 * | P5 > P6 | |

| P6: IP→LBA→BI→SUB | ||||

| Group B | P1: LBA→BI→SYM | P1 vs. P3 | −3.342 *** | P1 < P3 |

| P3: IP→SYM | ||||

| P2: LBA→BI→SUB | P2 vs. P4 | −4.763 *** | P2 < P4 | |

| P4: IP→SUB |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Gao, H.; Zhu, Y.-H.; Ding, J.-Y.; Li, H.-Y. Study on the Driving Path of Contractors’ Low-Carbon Behavior under Institutional Logic and Technological Logic. Buildings 2023, 13, 989. https://doi.org/10.3390/buildings13040989

Gao H, Zhu Y-H, Ding J-Y, Li H-Y. Study on the Driving Path of Contractors’ Low-Carbon Behavior under Institutional Logic and Technological Logic. Buildings. 2023; 13(4):989. https://doi.org/10.3390/buildings13040989

Chicago/Turabian StyleGao, Hui, Yu-Hong Zhu, Ji-Yong Ding, and Hong-Yang Li. 2023. "Study on the Driving Path of Contractors’ Low-Carbon Behavior under Institutional Logic and Technological Logic" Buildings 13, no. 4: 989. https://doi.org/10.3390/buildings13040989