Preferences of Young Polish Renters: Findings from the Mediation Analysis

1

Department of Building Engineering, Warsaw University of Technology, 00-637 Warsaw, Poland

2

Innovative City Department, Warsaw School of Economics, 02-554 Warsaw, Poland

3

Faculty of Economics and Business Sciences, Universidad de Granada, 18071 Granada, Spain

*

Author to whom correspondence should be addressed.

Buildings 2023, 13(4), 920; https://doi.org/10.3390/buildings13040920

Submission received: 1 March 2023

/

Revised: 23 March 2023

/

Accepted: 27 March 2023

/

Published: 30 March 2023

(This article belongs to the Special Issue Trends in Real Estate Economics and Livability)

Abstract

:The worsening housing problems of young adults in many countries have become a worldwide problem. Researchers point to a number of factors that influence young people’s decisions to own or rent their own apartments or houses. The term generation of renters or the lost generation has appeared in the literature in relation to the young adult generation. This article offers insights into the housing preferences of young adults aged 18 to 45 in Poland, with a particular focus on the renter cohort. Conclusions are drawn about whether young adults who are already renting prefer to buy an apartment or house rather than maintain their status quo, and what determines their decisions in this regard. The study identifies a number of socioeconomic factors that influence the housing decisions of young renters in Poland. It addresses some of the problems and challenges of today’s housing market and, in particular, examines what leads young Polish renters to switch from renting to buying their first home or, alternatively, to live in a rented apartment for years (thus showing indifference to homeownership). Some of the reasons for the change in attitude toward this issue are highlighted. The study is quantitative in nature, relying on an online survey and a mediation analysis that is particularly well suited to explaining the relationship between many different variables. Of the eight hypotheses tested in the study (using mediation analysis), only three could be proven, namely that the amount of rent payments and other costs for economic reasons influences the willingness to buy an apartment or a house, and also that the length of the rental period has a negative influence on the willingness to buy a house. Finally, the mediation model provides evidence that the higher a young renter’s tolerance threshold for mortgage interest compared to “rent payments”, the more inclined they are to buy an apartment or house. The study suggests that the housing finance subsystem has some shortcomings as far as financing young people is concerned. Strategically, there are two complementary solutions that could be implemented: (1) a long-term home savings plan or program and (2) innovative housing loan options tailored to the financial situation of young people.

1. Introduction

Finding a place to live is one of the biggest and most important decisions in life. People who are faced with the choice of owning or renting a home do not find the decision easy [1]. This is because they have to choose between alternatives with very different costs/characteristics; essentially, it is a routine decision made under uncertain conditions. Before such decisions are made, several scenarios are usually run, in which appropriate assumptions are made about the elements affecting the value of the property in the future (e.g., the risk of depreciation, etc.), and its financing (i.e., the creditworthiness of the buyer), as well as the living situation of the parties involved [2]. In summary, individuals or entire households face an extremely serious problem, which from their point of view consists of making important decisions under uncertain conditions. While renting an apartment or house involves recurring low costs in the form of rent payments and offers some decision flexibility due to low barriers to entry and exit, owning requires a high one-time initial investment that comes with much less decision flexibility. Aside from the financial aspects (i.e., whether or not one can afford to own a home), preference in this regard may depend on the expected duration of use of the home itself. Home ownership may be preferable for long-term use, while for short-term use, renting a house is usually considered the better option for obvious reasons. For example, Hargreaves [3] has shown that people generally prefer homeownership to renting when the assumed useful life is more than 3 years. However, there is a caveat: this applies when the rate of appreciation of real estate is higher than the rate of inflation. A higher interest rate on the borrowed capital increases the time needed to break even [3]. This topic gains importance against the backdrop of the current cycle of significant interest rate hikes and the politics of dear money. More importantly, the problem is that the duration of housing use is usually not known in advance and may depend on a whole range of different factors [2]. In our daily lives, there are events that can completely change our previous decisions, including those related to owning or renting an apartment or house. One example is the coronavirus pandemic. Another example is the current, very disturbing, and unexpected increase in inflation and the deterioration of living conditions.

There is a general view that renting is a reasonable alternative to homeownership. Erbel [4], for example, discourages young adults from buying a house, arguing that homeownership usually hinders mobility (i.e., geographic and occupational mobility), even though globalization has opened up the world and one can now work anywhere on the globe. Beugnot et al. [5] argue that homeownership impedes mobility because it limits job searches in the economy and imposes additional costs associated with relocation (when a job is far away). However, it is worth considering whether renting from the perspective of young adults is a trend resulting from new trends and preferences that are unique to them, or whether it is an economic necessity that is a consequence of the low incomes of young people who cannot afford homeownership and therefore opt for affordable rental housing. Data show that 45.1% of young adults aged 25–34 still live with their parents, which is probably not their preferred situation and is an undesirable phenomenon from a sociological perspective [6]. Thus, it is worth looking for a rationale for this phenomenon, i.e., for the fact that a large group of young people do not rent an apartment, but continue to live with their parents. It is quite possible that the total cost of rent is too high for them. On the other hand, if rent payments are almost as high as the cost of a mortgage, the renters might consider owning their own apartment or house. So why do they not? To understand the behavior of young adults in the housing market in its complex socioeconomic context, both now and in the future, it will be extremely important to examine many similar issues and answer a whole series of questions. These questions should address the following areas: housing preferences in the context of economic and socio-cultural conditions, lifestyle, utility analysis, etc. It is also worth seeking answers to the question of whether the existing 30-year mortgage annuity (i.e., a repayment mortgage) is attractive enough to the cohort of renters expressing a need for homeownership to encourage them to purchase a home. Perhaps, from the banking sector’s perspective, it is possible to offer borrowers a more attractive loan package that is tailored to their income level, occupational status, etc.

The aim of this study is to analyze the main factors influencing the housing preferences of young adults in Poland, focusing on the analysis of the preferences of those who have already rented an apartment or a house. Using a customized questionnaire survey and a mediation model, the study provides insights into the Polish housing market and analyzes the motivations of young Polish renters. It identifies a range of factors that influence their decisions and choices. The study targets young adults between the ages of 25 and 45. It analyzes their attitudes and their ability and willingness to buy an apartment or house financed with a mortgage loan. Housing is a popular topic of public debate in Poland, but most of it is conducted online or as a commercial initiative of the private sector (mostly developers) [7,8]. On the other hand, there is a lack of solid academic research on the cognitions of young renters in Poland. The present study is an attempt to fill this gap.

The structure of the study is very simple. Section 2 discusses previous empirical findings and relevant theoretical concepts. Section 3 outlines the analytical framework, data collection methods and mediation model, including descriptive statistics and methodology. Section 4 provides a detailed presentation of the results, followed by a discussion in Section 5. Finally, conclusions from the conducted research are drawn and presented in Section 6.

2. Empirical Evidence

The importance of home ownership and housing studies has been repeatedly addressed in the literature, and there are numerous studies on the subject [9,10,11,12,13,14,15]. Problems have been increasing for years, but in recent years, housing problems among young adults have increased particularly markedly in many countries [14,16]. A wide range of factors have been found to influence young people’s housing decisions [17,18]. There are studies that show that among the various factors that influence this market, economic factors are the most important [19]; they have a greater influence on housing choices than, for example, social, or cultural factors. Economic factors include factors such as housing prices, income and wealth, and interest rates, but also factors such as tax regulations influenced by state governments [20,21]. In turn, other studies point to the significant influence of inflation factors and, in particular, the relevance of the relationship between homeownership and inflation [22]. There are also quite a number of studies that point to the significant social [11] and economic benefits of homeownership compared to renting [9,12,13,15,23,24]. Among the benefits, researchers list better social outcomes [11,12], greater civic awareness [9,13,15], less crime and fewer so-called pathological incidents [23], and better cognitive and behavioral performance and learning outcomes [12]. Homeownership creates the right conditions to support and encourage families [24]. In addition, easy access to homeownership leads to higher birth rates [25]. Moreover, homeownership leads to significantly higher life satisfaction [24,26]. Higher homeownership rates are also generally associated with higher housing prices [11].

People’s attitudes toward housing choice are also influenced by certain economic, political, and cultural dimensions of consumption, where countries differ [27]. Nevertheless, positive or negative attitudes toward homeownership are also significantly influenced by the socialization process [1], which is why some researchers point out the urgent need for numerous debates and information campaigns on this topic [27]. It is obvious that there is a significant relationship between socialization and public information campaigns. Such campaigns are later reflected in appropriate public housing policies and form the basis for public debates [27]. It is important to note when considering the preferred form of housing that ownership has generally been preferred to renting so far, unless there are financial constraints (i.e., assuming that a person facing this type of choice can afford both) [16]. For example, one study showed that Americans prefer homeownership [15]. More specifically, 86% of respondents clearly preferred homeownership to renting. Only 26% of respondents said they chose to rent their apartments due to pure conviction rather than for financial reasons.

As for the topic of housing preferences, one cannot avoid addressing housing markets (since these issues are inextricably linked). In this issue, speculation and occasional collapses of housing bubbles play an important role, reflected in market conditions and, in particular, in economic uncertainties and difficulties in accessing mortgage financing [8]. This is exactly how the situation looked for a while after the sub-crisis more than a decade ago, and most importantly, the general uncertainty spilled over to the whole world, including Poland [10,28]. This is important because in the post-crisis period, people are generally less likely to opt for home ownership [10]. It is important to note that the crisis hit mainly the countries where the share of the construction sector in GDP is the highest [29], such as Spain [30]. Consequently, the shock of the crisis hit young Spaniards the hardest and led to a significant increase in their interest in renting compared to homeownership [30]. This is a dangerous phenomenon, since it affects socioeconomic aspects and issues of human identity and subjectivity, as well as the tendency of young people to start a family and their emancipation [31]. If such a situation persists over the long term and is accompanied by changes in young people’s norms and aspirations (and this is often the case), the social impact of such cohabitation could be difficult to manage. The countries most vulnerable to severe social changes are those where the crisis could not be contained relatively quickly, disrupting previously prevalent living arrangements, and where the living conditions and lifestyles of young adults have been forced in some way, intentionally or unintentionally.

A number of studies also point to another phenomenon: namely that for many young adults the alternative to buying their own home is no longer renting, but having to share housing with their parents, which significantly deteriorates their emancipatory abilities [7,20,32] and also affects the quality of their social life [30,31,33]. Thus, young people today start their own families much later, which is of course significantly influenced by the lack of their own housing [16,32]. Unfortunately, the truth is that no previous generation has lived with their parents as long as today’s [16,32]. In this context, it is worth considering the example of Spain, which is traditionally considered a pro-ownership society when it comes to the choice of housing. The great financial crisis in the first decade of this century completely disrupted social expectations and aspirations regarding choices in this area. The difficult situation of young adults means that their parents play a greater role [20,30,31,33,34], whether through financial transfers (donations) and loans or in-kind contributions. Housing preferences are therefore increasingly determined by the social and socioeconomic class of young adults’ parents. In this context, it should also be mentioned that parents of young adults exercise a kind of control over their children who are recipients of housing capital, which manifests itself in influencing their standardized social and economic choices [35]. It is also important to point out that the importance of parents’ material status increases as housing prices continue to rise and affordability decreases [33,34]. In particular, the problem of the importance of parental support factors is beginning to affect women more [34].

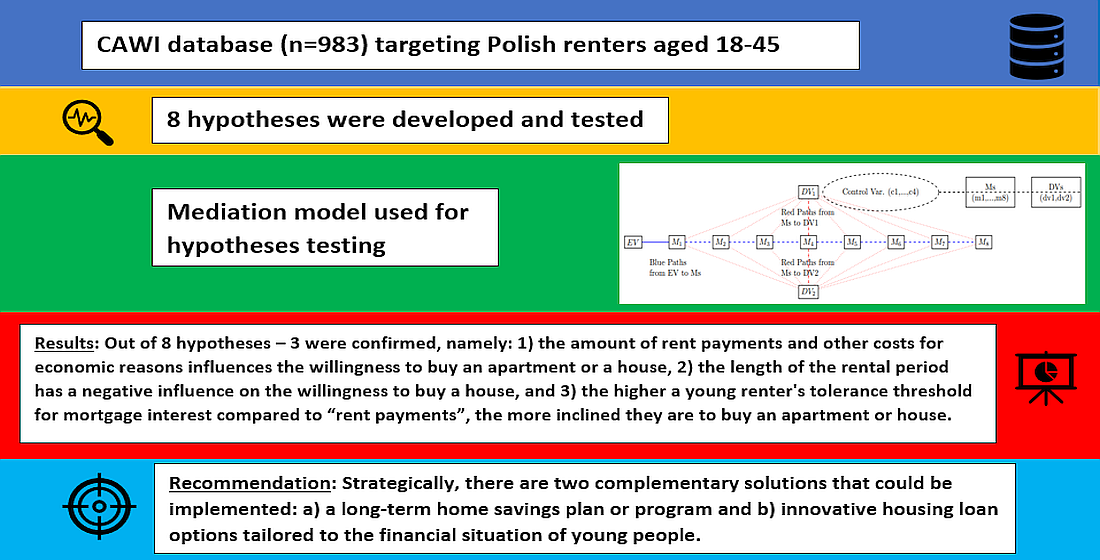

Precisely because of the pervasive market and social uncertainty [16,36], the perspective changes when it comes to financial burdens of any kind. The way rent is viewed is also changing. Increasing uncertainty and more frequent black swan events lead to increased risk aversion, which leads to increasing interest in rent [16]. It is certainly the case that the option to rent gives people a greater sense of flexibility, as it offers the possibility of moving out at any time, which in the context of many economic uncertainties (binary events such as the COVID-19 pandemic, the potential collapse of many businesses, and the possibility of losing one’s job) provides a sense of greater security. The lack of access to housing for young adults leads to unequal housing conditions, lower social participation, and an increasingly visible wealth gap between generations. According to Willetts, the older generations have benefited from an exceptional situation, but it has and will burden the welfare of the younger generations, which is unfair [37]. According to the author, the demographic boomers not only dominate culturally through their power as an extremely large consumer market, but have also amassed huge amounts of wealth and real estate, all at the expense of younger generations. The phenomenon of the wealth gap between generations is most likely to be observed in the markets with the highest prices and the lowest prices, where the opportunities to buy a house are rather limited [34]. The housing status of young adults is also strongly influenced by government social policies [20], as evidenced by relevant research showing a negative impact of government benefits on attitudes toward homeownership [20]. Cultural differences also play an important role. Where these values are closer to family values, and where the household is seen as a certain symbol of security and refuge, the level of homeownership tends to be higher (see Figure 1). Figure 1 shows some structural and systemic differences between countries that are not directly related to the economy and that are reflected in the popularity of homeownership. In Hungary, Slovakia, or Spain, for example, home ownership is generally considered better than in Germany or Austria, which are richer in terms of GDP per capita [22].

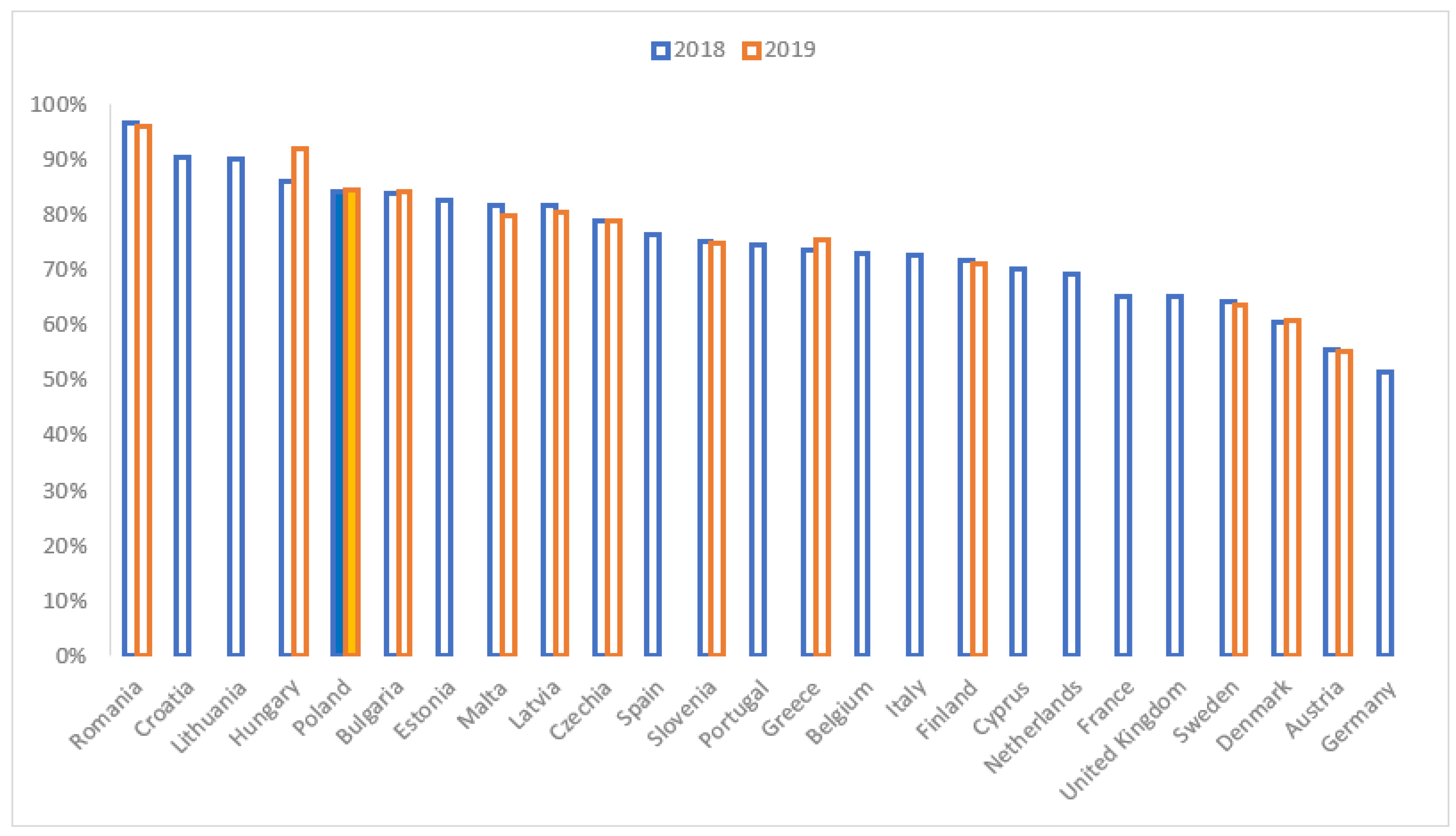

The differences in attitudes among people in different countries are due to non-price aspects, which include demographic factors, institutional conditions, government housing policies [20], cultural differences, etc., in addition to purely economic factors related to prices and supply [2,22]. Decisions about the preferred housing type may be related to lifestyle [16] or, for example, to a particular cultural background and heritage. From a purely economic perspective, housing type is determined by housing prices themselves (so-called affordability) [38], inflation [22], uncertainty about future income [2], risk factors related to job and employment stability, and potential financial support from a life partner [2]. In this context, the increasing number of one-person households is pointed out [2]. As for housing prices, they have risen sharply in many countries in recent decades. Figure 2 shows the percentage change in average apartment/house prices over 2010–2021 in various European countries. In Poland, prices have increased by 39.92% in this period (i.e., in these 11 years). However, as Figure 2 shows, in many countries, prices have increased even more (in Estonia, Latvia, Hungary, and the Czech Republic, for example). The above data are consistent with the data in the study by Sobieraj and Metelski [39].

There is scientific evidence of episodes of price exuberance in many countries, e.g., the U.S. and the U.K. [40], New Zealand [41], and Australia (especially with respect to rental prices) [42]. For years, residential real estate speculation and buying frenzy were fueled by excessive liquidity in the monetary system (lax monetary policy), which naturally led to some of this liquidity spilling over into residential real estate markets [39,43]. Part of the blame for this situation can be laid at the feet of the U.S. monetary authorities, whose imprudent policy of quantitative easing (in contrast to the Austrian school of economics) set a certain new standard in economics. The truth is that credit-driven economies are prone to the spread of housing booms [43,44]. The policies of national governments and central banks contribute to putting homeownership out of reach for young people for purely economic reasons. In turn, those who bought their home with a mortgage must expect that the cycle of interest rate increasing in various countries (which is currently the case) may lead to a decline in home prices, and many will face the problem of interest and principal repayments that they may not be able to afford. It should also be emphasized that government policies (after public consultations) should be prudent and judicious, as studies show that excessive governmental social assistance does not necessarily have a positive impact on homeownership rates [20]. Still further studies point in particular to the need for well-structured [45,46] and developed mortgage markets [7], which significantly accelerate the emancipation process of young adults, as they succeed more quickly in leaving their parental home and starting an independent adult life. There is scientific evidence of a strong correlation between mortgage credit availability and homeownership. This phenomenon is particularly pronounced in the group of young adults who have the greatest problems with access to capital (which could be used for down payments) at a relatively early stage of their adult life and career development [45].

To improve the outlook for the housing market as a whole in the mortgage finance system, flexibility in mortgage repayment is particularly important [46]. Due to the increasing economic turbulence in the markets, some financial engineering mechanisms are desirable to appropriately mitigate the risk so that young people are not exposed to excessive risk [46]. In this area, research has already been conducted that has shown that loans with adjustable interest rates (adjustable-rate mortgages) are the most appropriate form of financing.

Another important point is that it is becoming increasingly difficult for young people to actually identify their housing preferences [7], regardless of the level of economic development of the country from which these young people come. The point is that this phenomenon cannot be explained by the economic situation, nor by the level of development, liquidity or stability of the housing markets themselves [7]. Other studies have shown a relationship between financial strain and outstanding financial debt of young adults (mainly in the form of student loans) and the lack of desire for homeownership [47]. In other words, financial strain is a factor that does not positively influence the desire for homeownership, but rather discourages potential buyers. The increasing credit and financial burden of societies has a negative impact on young adults, which has socioeconomic consequences and demonstrably worsens their chances of homeownership [47].

Economists predict that the current processes will continue in the current decade, leading to a general decline in the relative level of home ownership [10,48]. More specifically, although there will be a net increase in the number of new homes and new households (i.e., the absolute number of homeowners will increase), overall renting will dominate as the absolute number of renters will increase by a larger proportion [10]. In general, rising housing prices and the lack of an adequate financing system mean that more and more young people will be excluded from owning a home and will become part of a generation of renters [49]. Therefore, it is likely that the housing market will be a renter’s market in the future [10]. Additionally, it is the lack of access to home ownership and the strong need of young adults to create some kind of housing for themselves that leads to a rapidly growing rental sector [16]. On the other hand, the proportion of young adults still living with their parents is also rapidly increasing [31]. These are now two strongly dominant trends that are setting the direction in which housing markets are developing worldwide [31]. It is also worth highlighting the increasing degree of financialization of housing markets themselves [31], which in many cases even makes it impossible for young adults to become homeowners [16,50]. There is also a body of research that argues for the advantage of renting over owning [17], especially when considering the average duration of homeownership. This perception of choice of housing form is justified, for example, for the US market, as pointed out by Beracha and Johnson [17]. Regarding the choice of housing form, these authors adopted the position of indifference, assuming that it is reasonable to consider the appropriate relationship between the rent and the housing price, taking into account the indicators of volatility of housing prices [17]. However, this type of evaluation should pay special attention to the specifics of the market in question, i.e., demographics, cultural factors, social habits, and so on. In other words, it is difficult to make a similar assessment for other markets, e.g., European or Polish, based on the experience of the American market, which is simply different [10,48]. It should also be emphasized that homeownership has a number of positive aspects from both macro- and micro perspectives [51]. Regarding the latter aspect, homeownership leads to greater social participation and, at the same time, to more savings in households. As for the first aspect, ownership promotes consumption and investment and has a positive impact on public finances. Additionally, it is worth noting that homeownership rates are affected by appropriate government policies, especially tax distortions [51,52]. In the case of unfavorable tax laws, the cost of owner-occupied housing increases [52]. Therefore, it is difficult to imagine a stable housing sector without government action to reduce marginal tax rates [16,52,53]. Important issues for policymakers and decision makers to consider include taxes on tangible property (cadastral), taxes on the transfer of residential property, rent-related taxes, capital gains taxes, cost of owner-occupied housing, imputed income from rental housing [53], and mortgage tax credits [16]. One proposed solution that works well is the possibility of mortgage interest deductions [53] or property tax deductions, as well as mechanisms that interact with capital gains from homeownership [16].

It is important to emphasize that, in addition to typical factors, such as location and price, certain building characteristics (e.g., energy consumption or whether the building has been modernized in this regard) may also play a role in housing preferences [54]. The energy efficiency of new buildings compared to older buildings can influence preferences when renting or buying a new home. Newer buildings designed with energy efficiency in mind may be more attractive to renters and buyers who value lower energy bills and carbon footprints [55,56]. It is important to keep this in mind. Indeed, research has shown that rental properties with higher energy scores are more likely to attract tenants [57]. In addition, government stimulus programs often target building retrofits and efficient new construction [56].

In summary, there are many aspects that influence young people’s adequate decisions about their preferred form of housing. In particular, individual decisions depend on the economic situation of a particular country, its background, and cultural values. Additionally important are appropriate programs and policies implemented at both central and local levels, i.e., different types of housing programs, adequate tax regimes, and the existence of a well-developed mortgage finance system with appropriate tools to mitigate financial risk.

3. Materials and Methods

3.1. Research Method

The study is based on a questionnaire survey, which has become a popular means of obtaining information in the information society [58]. This method is effective in the sense that it allows designing customized questionnaires that correspond to the predefined research hypotheses. Data are collected from respondents who are as representative as possible, so that the sample and its parameters correspond to the entire population under study in order to obtain reliable results. Moreover, the development of Internet technologies facilitates access to various communication channels, which makes this form of data collection and knowledge building about various economic and social phenomena attractive and relatively quick to conduct [59]. Surveys provide useful information on various topics related to economic and social life and are widely used in scientific research. Furthermore, the choice of a research method such as a questionnaire survey usually results from the specificity of the phenomenon under study and the research problems that are the subject of investigation. The respondents’ answers included in the survey are used as a basis to test the predefined research hypotheses and to confirm or reject them. A mediation model was used to test the hypotheses established in the study.

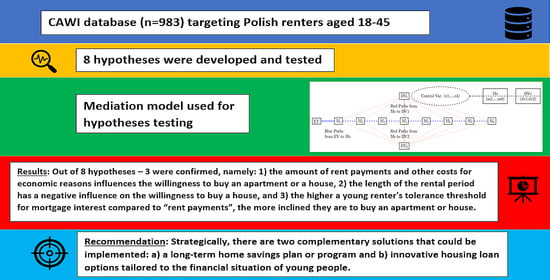

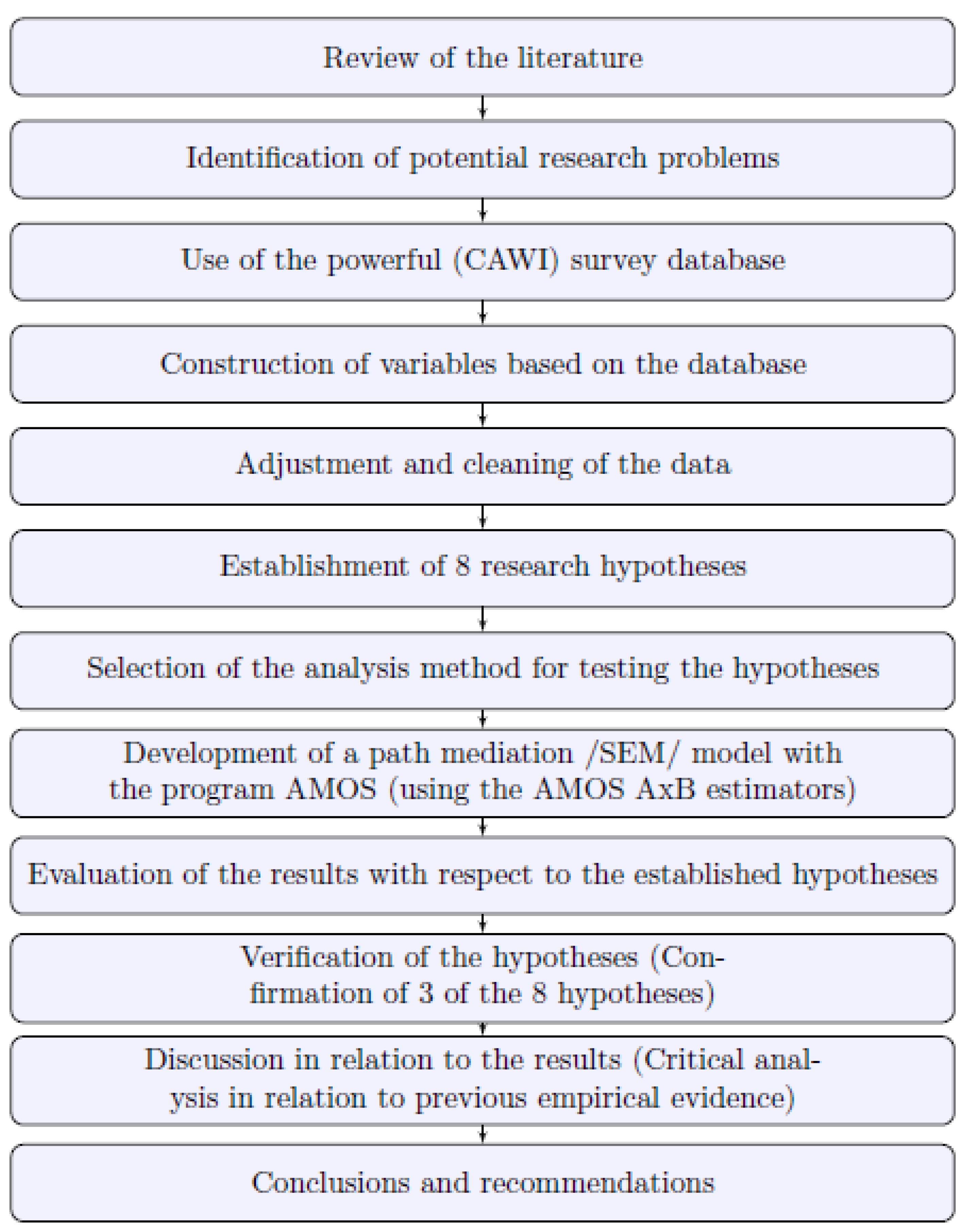

The study followed several steps to reach its conclusions and recommendations. It begins with a review of the literature to identify potential research problems. Then, a powerful survey database (CAWI) was used to construct variables based on the data. The data were cleaned to ensure accuracy and reliability. The next step was to establish some research hypotheses and choose an analysis method to test them. Briefly, a path mediation/SEM/model was used using the AMOS AxB estimator approach. After the results were analyzed, three of the eight hypotheses were confirmed. Then, the results are discussed in relation to the hypotheses raised and critically analyzed in light of previous empirical findings. Finally, some conclusions are drawn and some recommendations are made based on the findings. Overall, the study demonstrates a comprehensive and systematic approach to conducting research, from problem identification and data collection to analysis and interpretation. It draws on advanced statistical tools and critical thinking skills to make a meaningful contribution to the field. To make the procedures of the study clearer and easier to understand, the flowchart of the study is shown in Figure 3.

3.2. Data Collection

The survey was conducted in early 2021 using the Computer-Assisted Web Interview (CAWI) method on a sample of 983 respondents (n = 983), consisting of young adults between the ages of 18 and 45. CAWI is a survey method in which interviews are conducted with respondents via the Internet. This technique allows researchers to reach large numbers of people quickly and efficiently. Typically, respondents are sent a link to a website where they can complete the survey. The method requires careful sampling to ensure that respondents are representative of the population being studied, and various techniques such as stratification and weighting are used to ensure the accuracy of the results. CAWI is used in quantitative research projects in many fields, including market research, social sciences, and public opinion research.

3.3. Mediation Analysis: Hypotheses of the Study

Mediation analysis has been used in a variety of studies to identify and evaluate the mechanisms by which treatments affect an outcome by revealing intermediate variables that transfer the effect of an independent variable to a dependent variable [60]. This research method has become very popular in medical sciences, but there are also socioeconomic studies in which it has been used. Examples include studying BMI as a mediator of the relationship between smoking and insulin levels [61], evaluating the relative size of different pathways in production functions [62], and determining the sources of output effects [62]. Other applications include promoting and increasing the use of causal mediation analysis in applied education research [63], identifying mediators of health outcomes [64], exploring and assessing biological or social mechanisms to support policy making [65], and causal mediation analysis in clinical research contexts [66].

A mediation model is a particular type of analysis that examines the relationship between an independent variable and a dependent variable and assumes that a third, mediating variable (also called an intervening variable or intermediate variable or mediator) plays some role in that relationship. The entire model aims to better understand and explain this relationship. Traditional regression models examine direct changes in an endogenous variable in response to changes in a set of exogenous variables. A mediation model assumes that an explanatory variable influences an intermediate variable, which in turn influences the endogenous variable. In other words, a mediation model considers indirect causal relationships and compares them to direct relationships. It can also be considered a special case of path analysis, which assumes the inclusion of a mediating variable (mediator) when studying the relationship between two or more variables. When hypothesizing a causal sequence X → M → Y, mediating models actually attempt to illustrate the mechanisms by which X and Y are connected in some way [67]. The inclusion of a mediating variable in a model facilitates the understanding of the relationship between response and explanatory variables [68,69]. Cohen et al. [70] point out that a mediating variable can be particularly useful when direct relationships between exogenous variables and an endogenous variable are not obvious, or when there are a number of additional contextual mechanisms that significantly complicate the understanding of the relationships under study. MacKinnon [69] noted that mediation models can steer the context of the mechanisms and processes under study in previously unexplored directions through a whole range of mediating variables [69]. In general, mediation explains causal relationships that are somewhat more complex than a relationship that can be expressed as “X influences Y”. Viewing the phenomenon under study through the lens of the available literature on the subject, it can be assumed that the relationship between X and Y requires a deeper explanation than simply relying on a simple direct causal effect emanating from the independent variable (IV) on the dependent variable (DV). Since the housing market and the forces influencing it are an extremely complex system composed of many different subsystems [71], many of its relationships are the result of contextual determinants, the mediation of which can lead to a transformation of the entire system. In other words, the relationships that prevail in this market are very complex and a function of decisions made at the microeconomic and macroeconomic levels, which can be influenced, for example, by economic and housing policies.

Mediation was popularized by the work of Baron and Kenny [72], who applied it to psychological studies. They point out that several conditions (prerequisites) must be met in order to model a mediation relationship [72]. MacKinnon [68] points out that mediation analysis considers the following 3 approaches: (a) causal steps, (b) difference of coefficients, and (c) product of coefficients [68], which can be described by the following three equations:

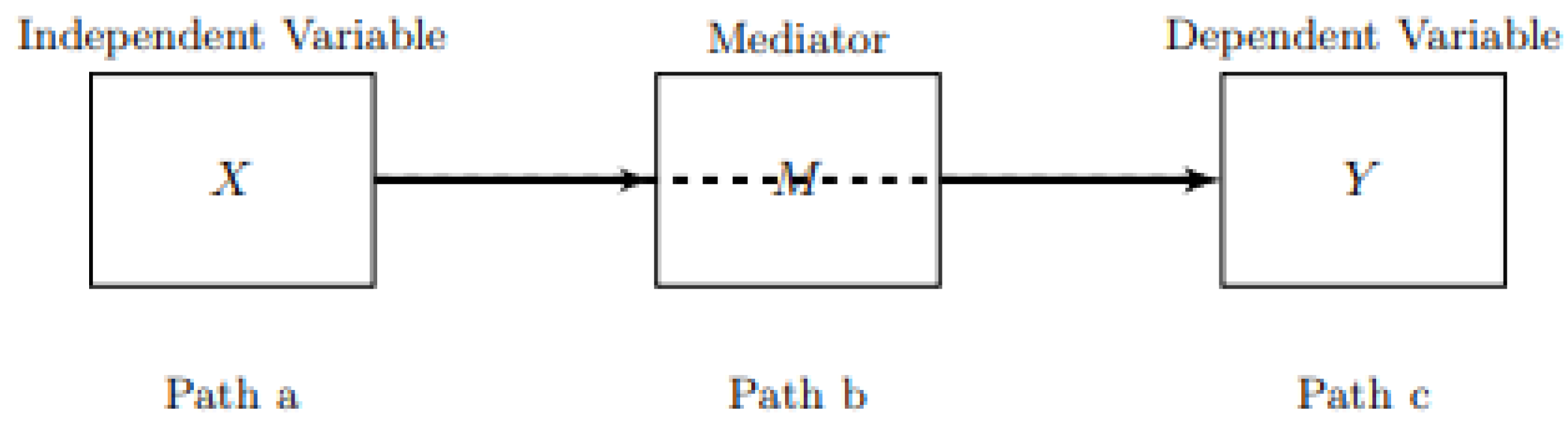

Figure 4 illustrates a simple representation of the mediation model, which reflects the relationships between two variables via a mediator.

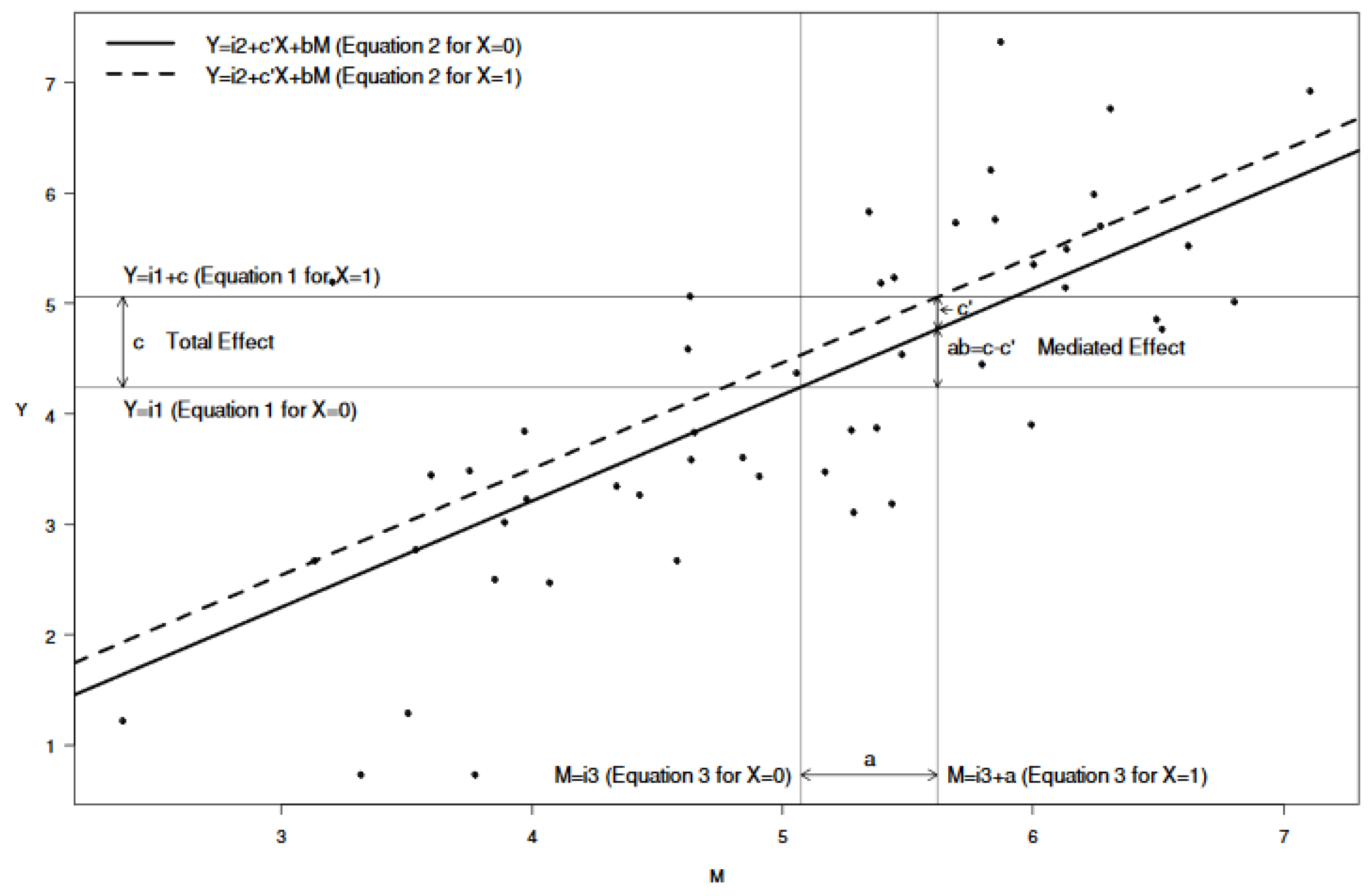

Equations (1)–(3) can also be illustrated in a graphical form (Figure 5).

In addition, it must first be determined whether we are dealing with a mediator and not a moderator. However, there is an important rule to consider in this question, namely: (1) the mediator must be an accidental result of the IVs and an accidental antecedent of the DVs; (2) the moderator must not be the accidental result of IV. First, we need to check whether the explanatory variable is a significant predictor of the response variable (explanatory variable → response variable). This can be expressed as follows:

and the β11—coefficient has to be significant.

For the same reason, the intermediate variables are regressed on the explanatory variables to test whether the latter are significant predictors of the mediating variable, which must be associated with the independent variable because otherwise it does not mediate anything (independent variable → mediator):

and the β21—coefficient has to be significant.

Last but not least, the response variable is regressed on both the mediating and explanatory variables to check whether the mediating variable significantly explains (predicts) the dependent variable:

and the β32—coefficient must be significant and β31 must be smaller in absolute value than the β11—coefficient (i.e., the coefficient of the independent variable reflecting the original effect).

In the case of the present study, all of the above criteria were met for each of the mediating variables considered. Finally, mediating effects can be tested using the approach of Baron and Kenny [72], bootstrapping, or AMOS AxB estimators [73]. For the purposes of this study, the latter method was used. The AMOS AxB estimator approach is a type of structural equation modeling that allows the estimation of indirect effects in mediation models. It relies on a maximum-likelihood estimation method to estimate the model parameters. The assumptions that must be satisfied for this approach are: normality, linearity, no multicollinearity, homoscedasticity, and no outliers. Violations of these assumptions can lead to biased estimates and erroneous conclusions. However, it is worth noting that the AMOS AxB estimator approach is relatively more robust to violations of the normality assumption than other methods, such as the Baron and Kenny [72] approach. Advantages of the AMOS AxB estimator approach include: (1) simultaneous testing of multiple mediator variables in a single model; (2) estimates of direct, indirect, and total effects of independent variables on dependent variables; and (3) a variety of fit indices and goodness-of-fit measures to assess the overall fit of the model. The software AMOS uses estimation options to fit a model to the data and provide estimates of freely varying parameters based on minimizing a function that indicates how well the model fits [74]. In addition, the AMOS AxB estimator allows user-defined estimates that can include various quantities, such as standardized regression weights and covariances between variables in the model [74].

3.4. Characteristics of the Study Sample: Variables and Data Analysis

A number of variables were selected for the study that seem relevant to this particular type of analysis (see Table 1). The questions and answers in the questionnaire form the basis for an in-depth analysis of young adults’ housing preferences. The items of the questionnaire consisted of single-choice questions. A summary of the questions and their underlying variables can be found in Table 1. Subsequently, these variables were used to develop a mediation model that accurately describes the phenomenon under study and, in particular, the relationships between different observable variables.

From a theoretical point of view, economic security is expected to be directly related to the preference to purchase an apartment or house [16,26]. Respondents who are financially secure (i.e., have a stable income) are more likely to consider buying a home. Similarly, perceptions of the level of acceptable mortgage rates are likely to affect the willingness to purchase a home. For example, Oliveira [75] points out that, in general, when mortgage rates increase, the overall cost of owning a home also increases, thus decreasing the affordability of real estate [75]. As noted by Altschaeffel et al. [76], an increase or decrease in mortgage rates affects housing price trends and should be taken into account when analyzing and evaluating the housing market and housing preferences. Similar relationships for the Belgian market were described in the work of Hoebeeck and Inghelbrecht [77]. The purpose of this study is not to evaluate the mortgage rate itself, but rather the perception and acceptable tolerance of mortgage rates that are believed to influence purchase decisions in the housing market. It is also known that housing preferences (whether owning or renting) are not only the result of the macroeconomic conditions prevailing in a given country, but are also related to sociocultural anthropology, which leads to the perception of housing as a place of refuge and a certain value base. Therefore, the model includes variables representing the social status of the respondent. They indicate either that the respondent has a family of their own (e.g., marital status, child-rearing, number of dependents) or that they intend to start a family (relationship status). Vidal et al. [78] point out that the rising costs of both raising children and housing have created an endemic resource conflict that prevents many households from achieving their desired housing outcomes. That is, in those countries where the family still holds a strong position as a social unit, home ownership tends to be higher, e.g., in Poland, but also in Spain or Hungary. The situation is different in countries that deviate from the traditional family model, e.g., Germany or Austria, where the social model is no longer so much based on family ties. As shown in Table 1, there are 8 mediating variables (binary or categorical) and 4 control variables included in the model. The independent variable and dependent variables are binary (respondents indicate certain binary preferences). The mediating variables are divided into economic variables, i.e., employment status, rent and related fees, own contribution to housing costs, and mortgage interest compared to rent, which explain, on the one hand, financial security; on the other hand, there are variables that are more social in nature, i.e., that explain the respondent’s social situation, such as whether they are single or have a partner and/or children (i.e., marital status/relationship status, number of dependents, length of tenancy). Our objective is to examine how the mediation variables influence respondents’ attitudes toward their personal housing preferences. The research hypotheses, based on logical premises as well as evidence from the literature, are listed in Table 2.

3.5. Characteristics of the Study Sample: Descriptive Statistics

A total of 981 people participated in the study, most of whom were in the 18–25 and 26–35 age groups. Study participants were divided into three age groups according to life stage and social development. The first group consisted of 18-to-25-year-olds who typically enter adulthood and begin university studies, post-secondary education, or work. This stage is associated with renting an apartment and moving out of the parental home. The second group includes the 26–35-year-olds who are established in the workforce and are looking to separate from their parents, often starting their own families. Finally, the third group includes the 36–45-year-olds who are expected to have stabilized their job and housing situation, with many already owning their own home at this point.

More specifically, 425 respondents were in the 26–35 age group, while 310 were in the 18–25 age group. The older age group of 36–45 years old was represented by 248 respondents. Of the respondents, 69.2% or 678 were women, while 30.8% or 303 were men. Previous studies have confirmed that women are more likely to be involved in the process of buying a home and more likely to make the final decision about where they want to live. Women are also more interested in the details and emotional aspects of the buying process. Men, on the other hand, tend to focus more on the financial value–price ratio of a home and its functionality. There is also a growing trend of singles interested in buying a home, with women making up the majority of this group. Women are willing to bear the additional cost of buying a home with higher standards. As a result, real estate marketing strategies are now specifically targeting women, as they tend to have the final say in the purchase decision. These findings are consistent with research conducted by Ale et al. [36] and Infor [79].

3.5.1. Characteristics of the Study Sample: Education and Residential Area (Hometown Population)

The survey results show that a significant majority of respondents, nearly two-thirds (643), had either a university degree, including a master’s or engineering degree, or a bachelor’s degree. In addition, individuals with secondary education completed 95 questionnaires. There were also respondents with lower levels of education, such as elementary education (3), secondary education (6), lower secondary education (6), vocational education (4), and academic degrees (44). Most respondents resided in Mazowieckie Voivodeship, which accounted for almost two-thirds of completed questionnaires. The other Voivodeships were represented to varying degrees, ranging from one response in Opole Voivodeship to over 40 responses in Lesser Poland and Pomerania Voivodeships. The regional distribution of respondents’ places of residence is shown in Figure 6.

More than 75.5% of respondents lived in large cities (with more than 100 thousand inhabitants), which means that their living conditions and views strongly influenced the results of the survey. Medium-sized cities were represented by 113 respondents, while rural areas and suburban regions accounted for 63 and 24 participants, respectively. Unfortunately, interest in participating in the survey was low among residents of small towns, with only 41 respondents. Better representation of this group of respondents would provide greater insight into their opinions, potentially highlight housing needs in such towns, and pave the way for practical measures to address any housing gaps. It should be noted that small towns are not among the beneficiaries of developers’ activities due to their low economic potential. However, they are subject to significant market-related pressures and suffer from a continuous population outflow due to various factors primarily related to the market [80].

The survey questionnaire included a question on occupational activity aimed at determining the respondent’s current occupational status. It was closely related to other questions concerning the source of income, housing situation, age of the respondent, etc. The question about the respondent’s permanent residence seems to have some significance, as it is generally easier to find a job in larger cities (i.e., the answer can be considered a proxy for the respondent’s financial situation).

In the survey, the occupational situation of the respondents was as follows: Approximately 83% of participants (819 individuals) reported being employed, while nearly 26% (254 individuals) reported being students. Raising children was reported as the current occupation of 122 respondents, and 53 individuals were actively seeking employment. In addition, 23 respondents indicated that they were attending school. The survey allowed respondents to select several options when answering the question about their occupation, which resulted in some individuals indicating a combination of studying and/or working and raising children, and so on. Therefore, the group of students and learners is reported separately. In addition, there were 156 participants who were students and had a job. Respondents could give multiple answers to the question about their sources of income. The results show that 63.8% of respondents (624 individuals) were employed and that an employment contract was their primary source of income. Task-specific contracts or mandate contracts proved to be the main source of income for 9.8% of respondents (96 people). In turn, self-employment was the main source of income for 102 respondents (10.4%). Table 3 provides an overview of the respondents’ sources of income, divided into primary and secondary income.

In terms of changes in income across age groups, as people move to the next age group, their main source of income also changes. Understandably, most dependents were from the 18-to-25-year-old age group; they also had the highest number of “casual contracts” (i.e., task-specific or mandated contracts). Employment contracts were mainly the domain of the middle age group, while business activities were mainly carried out by people in the second and third age groups. Of the respondents, 399 individuals, or 40.6%, reported owning their own home, while 247 respondents (25.1%) reported living with their parents. The remaining participants, representing more than one-third of all respondents (34.3%), reported living in rental housing, of which 270 individuals (27.5%) rented from a non-relative.

3.5.2. Characteristics of the Study Sample: Home Ownership Structure and Housing Quality

One of the questions aimed to determine the current housing status of the respondents. The purpose was to determine the extent to which respondents had already satisfied their need to “stand on their own two feet”. Responses to this question correlated with other survey responses and reflect the potential of the housing market and the problems faced by those interested in homeownership, in addition to respondents’ individual housing situations. Another question asked about the “number of people living under one roof”. The results show that most respondents lived with a partner/husband/wife—34.6%, followed by married couples or domestic partnerships with a child/children—23.5%, and single people—13.9%. For more details, see Table 4.

Respondents also had the opportunity to provide their own answers. There were 35 responses classified as “other reasons”, which mainly referred to single persons, i.e., widows/widowers, divorced persons, or persons living with their parents. Another question aimed to find out the number of occupants per room in the occupied housing units. Almost ¾ (72.8%) indicated that there was no more than 1 person per room in the place where they lived. More than ¼ of respondents said they had no more than 2 people per room, and only 15 people (1.5%) said there were between 2 and 3 people per room.

3.5.3. Housing Preferences of Young Adults Living with Their Families

When asked why they lived with their parents/siblings or friends, 74.4 percent of all respondents indicated that this question was not relevant to them. Of those respondents who did provide an answer, 252 provided various explanations, with the majority citing financial challenges as the primary reason. For example, 146 respondents indicated that financial constraints prevented them from renting or buying an apartment, with responses such as “I/We can not afford to rent”, “I/We can not afford to buy an apartment or house”, and “I/We are afraid of credit loans”. Meanwhile, 67 respondents said that they chose this housing option for convenience. In addition, 15.5% of those living with their parents and 4% of all survey respondents gave “other reasons” as their answer. Since there were quite a lot of answers of this type in total, it was decided to take a closer look at them. It turned out that 38.5% of those who stated “other reasons” fell into the “financial difficulties” group. They explained that they had to live together in order to accumulate enough savings to buy a house, or they reported that they could not afford to live alone due to a low income. A number of people were assigned to the “convenience reasons” group (e.g., grandparents taking care of their grandchildren, but also children taking care of their parents), i.e., such a living situation proves convenient for both parties—parents and adult children. There was still a group of young adults who indicated that they lived with their parents while waiting for their own apartment, which they had already bought, and that they were saving for its completion and furnishing. Overall, the responses found under the label of “other reasons” were substantially revised in light of the objective of the entire survey, and eventually a number of responses were moved to the group of financial insecurity or lack of sufficient funds, while the group indicating commonly understood reasons of convenience and/or temporary necessities, advantages, and benefits was increased (the group of respondents who fell under the heading of “other reasons” was reduced). This adjustment resulted in 241 respondents being classified as “living with their parents” for a variety of reasons, namely, financial difficulties (ongoing financial insecurity/fear for future financial security)—161 persons; convenience (ease of living/feeling obligated to other family members)—74 persons; other reasons—6 persons.

3.5.4. Attractiveness of Renting an Apartment among Young Adults

The survey also examines how attractive renting an apartment or house was in the eyes of young adults. With current challenges in mind, the following research question was considered: at what stage does the desire for stability and home ownership outweigh the convenience and attractiveness of rental housing for young adults? The above question was answered based on respondents’ answers to one of the survey questions, which was: If you live with your parents/siblings or friends, please indicate why? When analyzing each age group, the survey data showed a remarkable discrepancy between those who lived with their parents or others and those who did not (because they already had their own apartment or house). The results show that it was primarily young adults in the lowest age group, i.e., ages 18–25, commonly referred to as “student age”, who lived with their parents or siblings. However, even in this age group, there were people who wanted to have their own apartment.

3.5.5. Is Renting More of a Lifestyle and an Underestimation of the Benefits of Ownership?

The question of whether the respondents would like to acquire their own apartment or house as a basis for their future was answered positively by 553 people (56.3 percent of the respondents). Of these people, 320 (32.6 percent) said they wanted to buy a house because they did not currently own one, while 180 people (18.3 percent) wanted to buy a larger house, and 53 people (5.4 percent) wanted a house in a different location. In addition, 221 respondents were not interested in purchasing a home, and 89 people had no opinion on the subject. Finally, 120 people gave “other reasons” and provided more detailed justifications. A large number of responses categorized under the “other reasons” label (12.2%) needed clarification to explain interest in housing preference. Responses were classified as follows: (1) 71 respondents indicated that they were not interested in purchasing a home because they either already owned a home, were awaiting commissioning, or were already in the process of completing a home they had already purchased; (2) 2 respondents indicated that they would inherit a home from their parents; (3) 10 respondents indicated that they intended to buy a house for investment purposes; (4) 22 respondents were “fresh in the process” of buying/building an apartment or house; (5) 2 respondents did not intend to buy a house, although they could not specify the exact reason, e.g., lack of money or other reasons; (6) 8 people planned to buy a home (1 indicated she did not qualify for a mortgage loan—a widow with 2 children; 7 planned to buy a smaller home to move away from their parents); and (7) 4 people responded that the question did not apply to them.

The above analysis shows that of the 120 survey respondents who gave an open-ended response, 105 respondents had to be assigned to the “I/We do not want to buy a home” group, which was justified in detail by these respondents (e.g., I/We inherit a home, already own one, or are finishing one, etc.). In turn, the responses of 8 people from another group were merged with the group: “I/We want to buy a home because I/We do not have one”. The reasons for willingness to buy a house are shown in Table 5.

As shown in Table 5, about one-third of survey respondents, or 328 people, expressed interest in buying an apartment or house for their own use because they did not currently own one. This figure coincides with the number of people who rent an apartment or a room—327. From the survey, it can be concluded that the desire to buy a home was widespread among the participants of the survey. In addition, it is noteworthy that 22.7% of respondents wanted to buy a larger apartment or one located in a different place. Examination of the responses shows that renting an apartment was not a matter of preference for young adults, but rather a constraint. Moreover, young adults’ decision to rent an apartment should not be taken as a disregard for the importance of homeownership. On the contrary, those who were forced to rent expressed a desire to own their own home.

3.5.6. Expected Shifts in Mortgage Financing among Younger Generations

Young adults’ need or desire to own a home did not match their financial capabilities. When asked, “Why are you hesitant or unable to buy a home?”, 290 people responded, “I/We do not have enough funds for my/our own share (mortgage prepayment)”; 117 people responded, “I/We cannot afford to repay the mortgage loan”; and 192 people provided the response, “I/We do not want to expose myself/ourself to financial hardship for the rest of my/our life”. It is important to highlight that a large number of respondents (599 people, or 61%) considered the mortgage system unaffordable. The responses—“I/We cannot afford to repay the mortgage loan” and “I/We do not want to expose myself/ourself to financial hardship in my/our lifetime”—do not have the same meaning. In fact, the reasons given by the respondents are different from each other. However, it should be noted that each respondent had the opportunity to provide multiple answers, resulting in non-aggregated responses (the number of responses exceeded the number of respondents). Therefore, to facilitate further analysis, it was assumed that people who gave two or three reasons considered them to be equivalent. For example, responses such as “I/we cannot afford to repay the mortgage loan” and “I/we do not have the funds for my/our own share (mortgage payment)” were considered equivalent. When these responses were weighted by 1/2 and 1/3, respectively, and added together, the total number of respondents was 44 (out of 983 respondents), or 44.9% of all survey respondents. Financial difficulty (reported by 440 respondents) as a reason for inability to buy a home is shown separately in Table 6.

It should be emphasized that among the reasons for people’s inability to buy an apartment or house, insufficient funds for a down payment was cited as the main reason (51%) in all age groups. Another reason was “high credit risk”, while the lowest number of respondents cited “insufficient funds for mortgage repayment”. However, the importance of each reason varied from one age group to another. For the youngest group, insufficient funds to pay their own way was the most problematic aspect (58%), followed by unwillingness to take out a long-term mortgage loan (24%). The survey results show the importance of considering these factors when promoting homeownership, especially for younger people who face significant financial constraints. In contrast, the question of funds to repay the loan proved least problematic (18%). Fewer people in the “middle” age group were concerned about their own contribution (51%), while reluctance to take out a long-term loan increased (36%). Only 13 percent of participants indicated that they were likely to experience financial difficulties in repaying loans. The significant increase in pessimistic attitudes about repaying long-term loans suggests inherent economic and social changes that occur later in people’s lives. In addition, 54% of respondents did not want to be exposed to financial difficulties throughout their life. Finally, it was found that one-third of the participants, or 33 percent, reported that they did not have sufficient resources to contribute themselves. Similarly, 13 percent of respondents from the same age group lacked the financial means to repay loans.

3.6. Objectives, the Model, and Formal Results

It is important to emphasize that the questionnaire used in this study went through a long process of development and modification prior to its elaboration. It is based on interviews with young adults, especially students and graduates of Polish universities. A pilot study followed, during which the scope of the questions and answers, their logical structure, and the most appropriate response formula were finally determined. For the purposes of the pilot study, the questionnaire was developed using a Google form. Finally, the survey was adapted to the requirements of the Survio platform, which was set up specifically for this purpose. The survey was distributed online and targeted a wide range of respondents who met the established age criteria. The final version of the questionnaire was distributed among college students in the largest cities in Poland, as well as among members of scientific circles and alumni, including the alumni network of one of the faculties of the Warsaw College of Technology. In addition, the survey was published on some social networks, private and public social media, as well as on the websites of real estate agencies in various cities in Poland. The survey was accessed through an attached link. The questionnaire was titled: Home Ownership or Rental Housing? Housing Preferences of Young Adults in Poland (a questionnaire for people aged 18–45). The study not only tried to find an answer to the question whether renting an apartment or a house is more of a lifestyle or an existential necessity for young people, but also to find out what prevents young adults from buying an apartment. Intuitively, several reasons for this can be found. However, the focus of the survey was to test general perceptions by analyzing the responses of respondents in the age groups described. Part of the survey was used to find out whether respondents who rent an apartment are aware that the rental costs they incur are actually equal to the mortgage interest they would pay if they decided to buy their own apartment of similar size (and finance it with a mortgage loan). In addition, the survey aimed to determine the extent of young people’s interest in mortgages and their willingness and ability to buy an apartment or house. It is important to highlight that 1893 people participated in the survey, of which 983 answered all the questions in the questionnaire completely. Overall, the 52% response rate achieved can be considered a success in terms of the number of entries on the designed survey website.

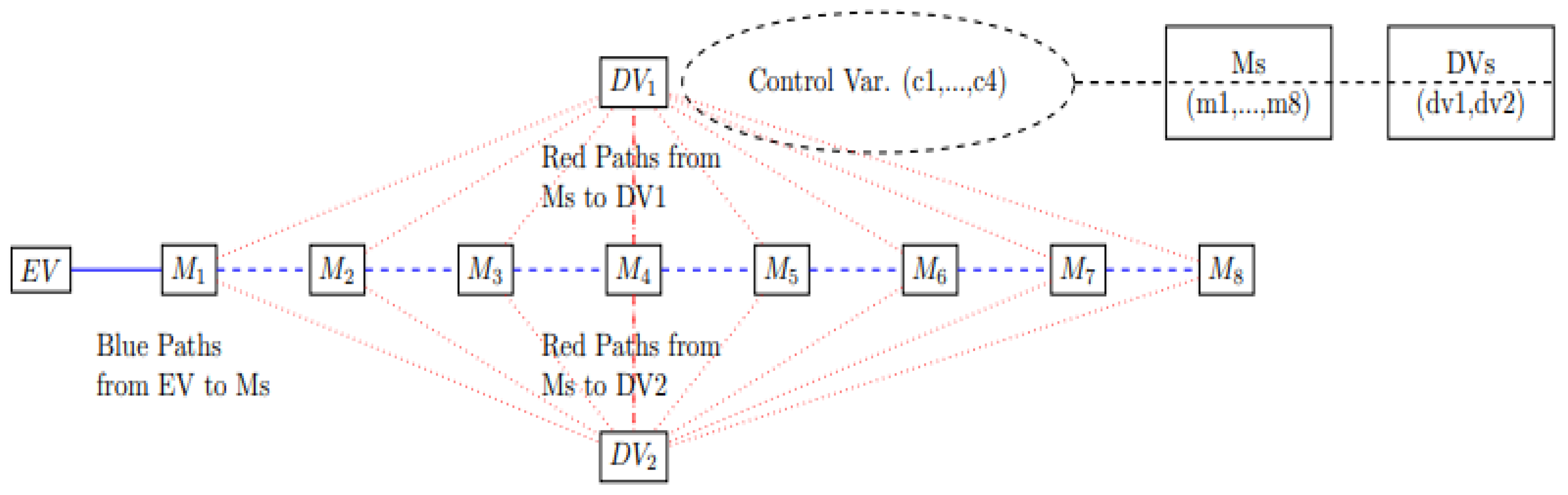

In line with the above considerations on young adults’ housing preferences, a theoretical mediation model was developed to test the original hypotheses. The theoretical mediation model, which relates to the hypotheses (presented in Table 2), in the form of a system of equations for estimation, takes into account two endogenous observed variables, namely the propensity to own an apartment or house (the variable referred to as dv1) and the preference for renting (the dv2 variable). Figure 7 shows a schematic diagram of the mediation (path) model that illustrates the interdependencies established in the initial hypotheses presented earlier.

The upper right corner of the diagram explains the role of control variables and shows that paths in a mediation model can lead from all control variables to both the independent (EV1) and dependent variables (DV1, DV2), and even to the mediator variables (Ms). Confirmation of this can be found in the Results section, where all paths are shown (and the directions of the relationships, coefficients, and p-values are given). It is important to emphasize that the inclusion of control variables in a mediation model is important because it helps to account for the effects of other variables that may affect the relationship between the independent variable, the mediator variable, and the dependent variable. This means that control variables can have direct effects on the outcome variable, independent of their influence on the mediator variable [81]. Control variables are variables that are not of primary interest in the analysis but are included to control for their potential confounding effects. In the mediation analysis conducted in this article, control variables included age, education, gender, and hometown population size, which means that they can be related to all variables of interest. Fundamentally, the role of control variables is to reduce the potential for spurious relationships among variables in the model [82]. Spurious relationships occur when two variables appear to be related, but their relationship is actually due to the influence of a third variable. By including control variables in the model, the effects of these potential confounding variables can be statistically removed. This ensures that the relationship between the independent variable, the mediator variable, and the dependent variable is not due to other extraneous factors [82].

The estimation of the structural equation models (SEM) themselves was carried out using the maximum likelihood method (ML), the least squares method (LS), or the asymptotic distribution method (ADF). The way such models are calibrated should depend largely on issues such as the nature of the data themselves (with particular reference to their distributions) and the sample size. For multidimensional normal distributions, it is advisable to use the ML method. On the other hand, if a distribution does not meet this condition, either the LS (for a sample with more than 2500 observations) or the ADF method (for a sample with more than 100 observations) are considered most appropriate, depending on the sample size [83]. Each estimated model should also be evaluated in terms of its goodness-of-fit (GoF) and the significance of the parameters obtained. In addition, there are some specific guidelines on the criteria for the evaluation of mediation models [84]. Moreover, there are quite a number of different benchmarks to evaluate the estimates and the degree of goodness-of-fit of the models. Their evaluation can be determined, for example, by comparing their estimates with two other extreme models, i.e., the baseline model and the saturated model. Such comparisons are performed using specific SEM software packages. In the present study, both STATA16 and AMOS software were used because they have built-in interfaces specifically designed for estimating mediation path models. In general, the main SEM fit measures are those that compare the estimated model with the baseline model, e.g., the Root Mean Squared Error of Approximation (RMSEA) and Comparative Fit Index (CFI), Tucker–Lewis Index (TFI), or Standardized Root Mean Squared Residual (SRMR) [see Table 7] [85,86].

For models with an RMSEA, fit measures of less than 0.08 are considered satisfactory [86,87]. The computation and interpretation of other goodness-of-fit measures, i.e., CFI and TLI, are explained in [90]. The model SEM can be evaluated using the RMSEA indicator [86]. Unlike most measures of fit, the RMSEA calculation does not compare the estimated model with the baseline model. It follows the formula: where —chi-square statistic of the estimated model, —number of degrees of freedom of the estimated model, and N— number of observations. In general, the lower the RMSEA value calculated based on the estimated model, the better its goodness-of-fit. The model is considered to be well fitted to the data if the RMSEA value is between 0.05 and 0.08 [91,92]. The values of RMSE, CFI, TLI, and SRMR also indicate a good fit of the two models to the data.

4. Results

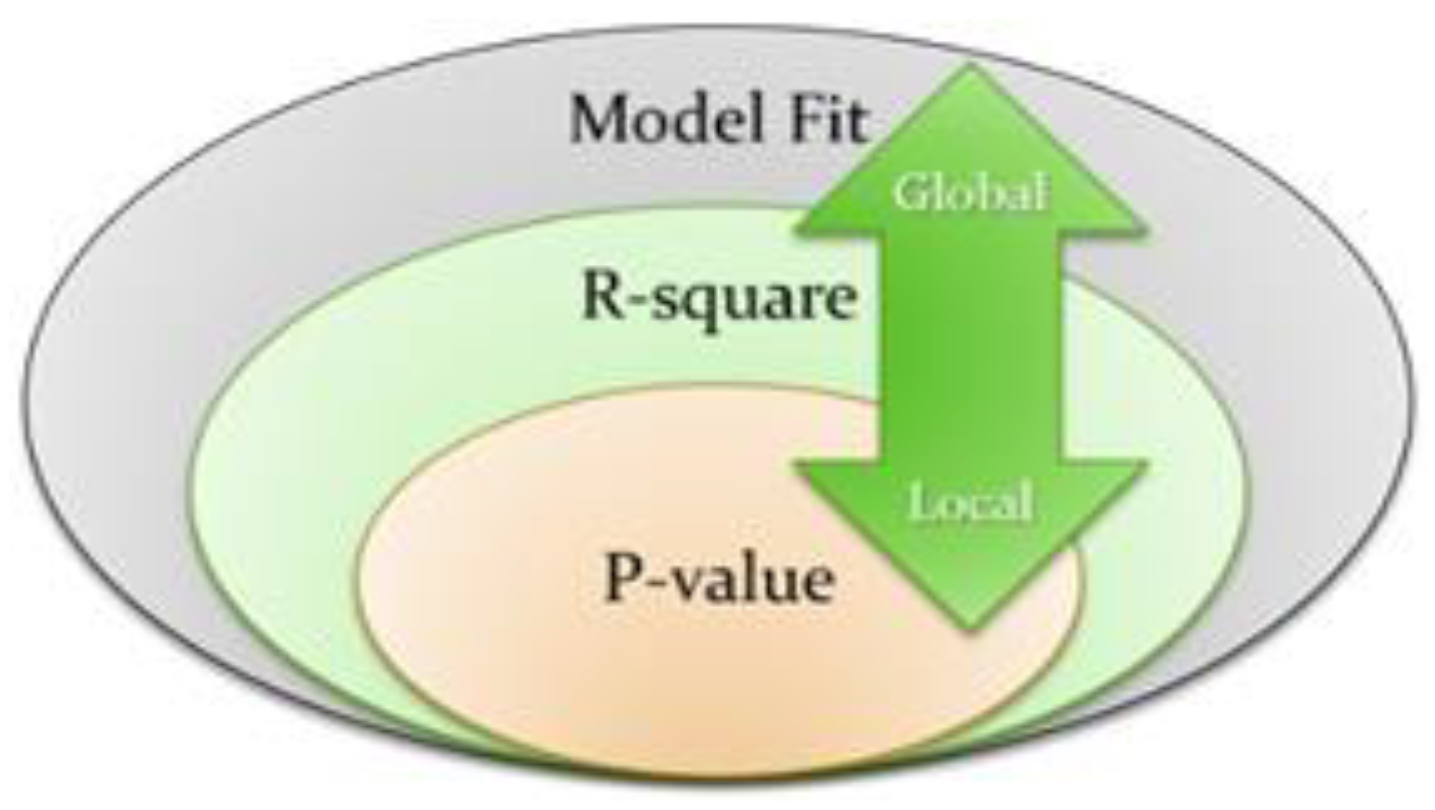

First, several important criteria for fitting the model were reviewed to further test the proposed hypotheses. These criteria take the form of global and local tests [64,93]. The strength of the local test alone is not important if the global tests are not met. Local tests assess the significance of individual paths in the model, while global tests assess the overall fit of the model [94]. The latter are the starting point for validating the obtained results and evaluating the overall fit of the model. A model that is well fitted provides more credible results. If it passes these global tests, the p-values for the hypothesized relationships are considered. On the other hand, if the p-values support the relationships under investigation, but the model itself has a poor fit, these results cannot be taken seriously [93]. Figure 8 shows the global and local test criteria that must be met to assess the reliability of the results.

The next step was to evaluate the r-squared values (i.e., the percentage of variance explained). These values must not be too low, because then the results are considered unreliable, since the variability of the explanatory variable does not explain an acceptable and satisfactory percentage of the variability of the endogenous variable [95,96]. In the case of the model developed for the purpose of this study, the r-squared value is 0.27, indicating moderately sufficient explanatory power [97,98]. It should be emphasized that the r-squared values in the mediation model (path model) are not generally accepted as a measure of effect size, and thus there is no specific threshold for what constitutes a low value [95]. Therefore, the accepted r-squared values for a mediation model depend on the context and the specific research question [98].

The last important point for evaluating the results and testing the proposed research hypotheses is the direction of the regression, indicated by the standardized and unstandardized estimates of the coefficients and, in particular, by their sign. For example, assuming that the number of dependents affects the propensity to purchase a home, and the actual results show that it has a negative effect (reducing the propensity to purchase a home), provides some sort of counterevidence. The detailed results are presented in Table 8 and Table 9.

Table 9, in turn, shows the relationships between the different variables specifically with respect to the hypotheses tested. It proves that hypotheses H3, H5, and H8 were positively verified. In the other cases, namely H1, H2, H4, H6, and H7, the hypotheses were disproved, with some contrary evidence found in two cases (H2 and H7).

First, it was found that there is a relationship between the variables EV and DV. Baron and Kenny [72] argue that in order to test a mediation model, there should be a significant relationship between EV and DV. The development of a mediation model describing the relationship between variables X and Y, which requires the inclusion of some type of intermediate variable, assumes that the relationship between EV and DV is statistically significant. This is indeed the case for the EV and both DVs used in the model under study.

Among other things, the study shows that gender has a statistically significant relationship with rental preferences. That is, women show less interest in renting an apartment or a house and are more likely to own a home (although the latter relationship is not statistically significant). The same is true for the “age group” variable. The higher the age group, the lower the propensity to buy a house. This may be due to habit or convenience. In other words, those who have rented for long enough have become accustomed to it and do not want to change their preferences. This is supported by the evidence for hypothesis H5. Similarly, the size of the resident population in the hometown leads to a higher willingness to buy a house. This can be implicitly deduced from the study of Wessel and Lunke [99]. Overall, the results show that some individuals who already live for rent consider buying an apartment or house, while others stick to the renting option, i.e., want to maintain the status quo. The beta coefficients for direct correlations are positive in both cases. This is precisely the reason that justifies that, in order to better understand the phenomenon under study, some kind of mediation model was needed to better explain these relationships by considering mediating variables. Table 10 again shows the goodness-of-fit of the obtained mediation (path) model.

5. Discussion

Rapidly deteriorating housing conditions for young adults around the world pose a serious policy challenge. This paper draws on a survey of young Polish renters aged 18 to 45 to examine their preferences for homeownership over renting. The study investigates how young Polish renters perceive renting an apartment and, in this context, formulates eight research hypotheses, of which only three could be confirmed: H3, H5, and H8. In two cases (H2 and H7), counter-evidence to the hypotheses was provided. Therefore, the following conclusions can be drawn. Length of tenancy is an important mediating variable affecting young adults’ housing preferences. The longer a person rents an apartment, the less willing they are to change their status quo. The results of the mediation analysis are consistent with findings from Zillow’s [100] report on consumer housing trends that the longer someone rents, the less desire there is for homeownership. More than half of renters who do not want to move have lived in rental housing for five or more years, the report found. Similar results were found in California, as reported by the California Department of Real Estate [101]. Therefore, it is critical for housing policy to promote homeownership awareness and encourage young people to consider homeownership at a young age. In addition, individuals who pay a higher rent are more inclined to shift their preference to homeownership. They have a better understanding of existing housing alternatives that could offer them the opportunity to pay off their mortgage at rent-like rates. The study also showed that relationship status is not a significant mediating variable (as it could not be confirmed that the variable m7 mediates the positive effect of ev1 on dv1). However, counter-evidence was found. A relationship with a partner encourages young adults already renting to maintain their status quo (and stay with the rental option). One might have expected the marital or relationship status of young adults to be a factor encouraging them to strengthen their family ties, which, according to the conventional view, requires owning a home. Moreover, previous research has shown that children who grow up in households with home ownership tend to perform better at school [17]. In addition, there is scientific evidence that homeownership is associated with better health outcomes than renting [102] and that homeowners are more likely to be satisfied with their homes, have higher self-esteem, and suffer less from economic strain, depression, and problematic alcohol use than renters [15]. Homeownership also allows families to build assets and serves as a measure of financial security [48]. However, for the cohort of Polish renters studied, the results do not support the hypothesis that individuals who live with their partner in any form (whether marital or nonmarital) also have an increased need for homeownership. Understanding this requires a deeper analysis of the nature of modern relationships and a clear understanding of the erosion of the traditional family model as it has been understood in the past. Along these lines, Simpson and Overall [103] have found that families have recently become less integrated on a global scale than in the past. This is evident from statistical data on marriage breakdown, cohabitation dissolution, and the rising number of one-person households. The authors argue that the growing insecurity associated with modern relationships can lead to a paradoxical sense of insecurity and instability among those living in such relationships. For example, individuals who declare that they are in a marriage or cohabiting relationship may not wish to risk the additional financial burdens that would result from the dissolution of such a relationship (because they are uncertain whether the relationship can be sustained in the long term). The termination of such a relationship would undoubtedly significantly complicate the borrowers’ legal situation and deprive them of their freedom and flexibility in life. In many cases, this would mean that people who have separated would have to continue to make joint loan repayments or live (with their ex-partner) in a shared apartment or house after their separation. In other words, young adults may be aware that the duration of loan repayments does not necessarily correspond to the duration of the relationship (whether marriage or cohabitation). A young couple unsure about the dissolution of their relationship may not want to buy shared housing units [104]. Instead, they might opt for a living-apart-together relationship (LAT), which involves fewer public expressions of commitment such as a shared apartment or house [105]. Renting is also an option, as it carries less risk of partnership dissolution than home ownership [106].

The variables “raising children” and “dependents” also do not prove to be statistically significant mediators of tenants’ willingness to change their preferences towards home ownership. In the case of the variable “raising children”, the opposite is the case. Young adults raising children may be afraid of the additional financial burdens that might be associated with buying a house. Raising children is already a major financial challenge by nature, so the reluctance to face additional financial risk factors should not surprise anyone. After all, buying a house and then paying off the mortgage puts borrowers at risk. To tackle this problem, the government should launch appropriate housing programs specifically targeting these people, because family policy and the fight against negative demographic trends are part of every government’s policy. According to Sobieraj and Metelski [39], programs to support young people in Poland were implemented earlier and should be adapted to the changed circumstances. Scientific research suggests that young adults raising children are fearful of the additional financial burdens associated with buying a home [107,108]. Low-income families in particular may be further burdened by expenses such as food, housing, and petrol [108].