Defect Repair Deposit and Insurance Premium for a New Home Warranty in Korea

Abstract

:1. Introduction

2. Literature Study

2.1. A New Home Warranty

2.2. Importance of a Warranty

2.3. Warranty Programs

2.4. Warranty Companies in Korea

2.5. Role of the Korean Warranty Companies

2.6. Metrics and Evaluation of Insurance Premiums

3. Materials and Methods

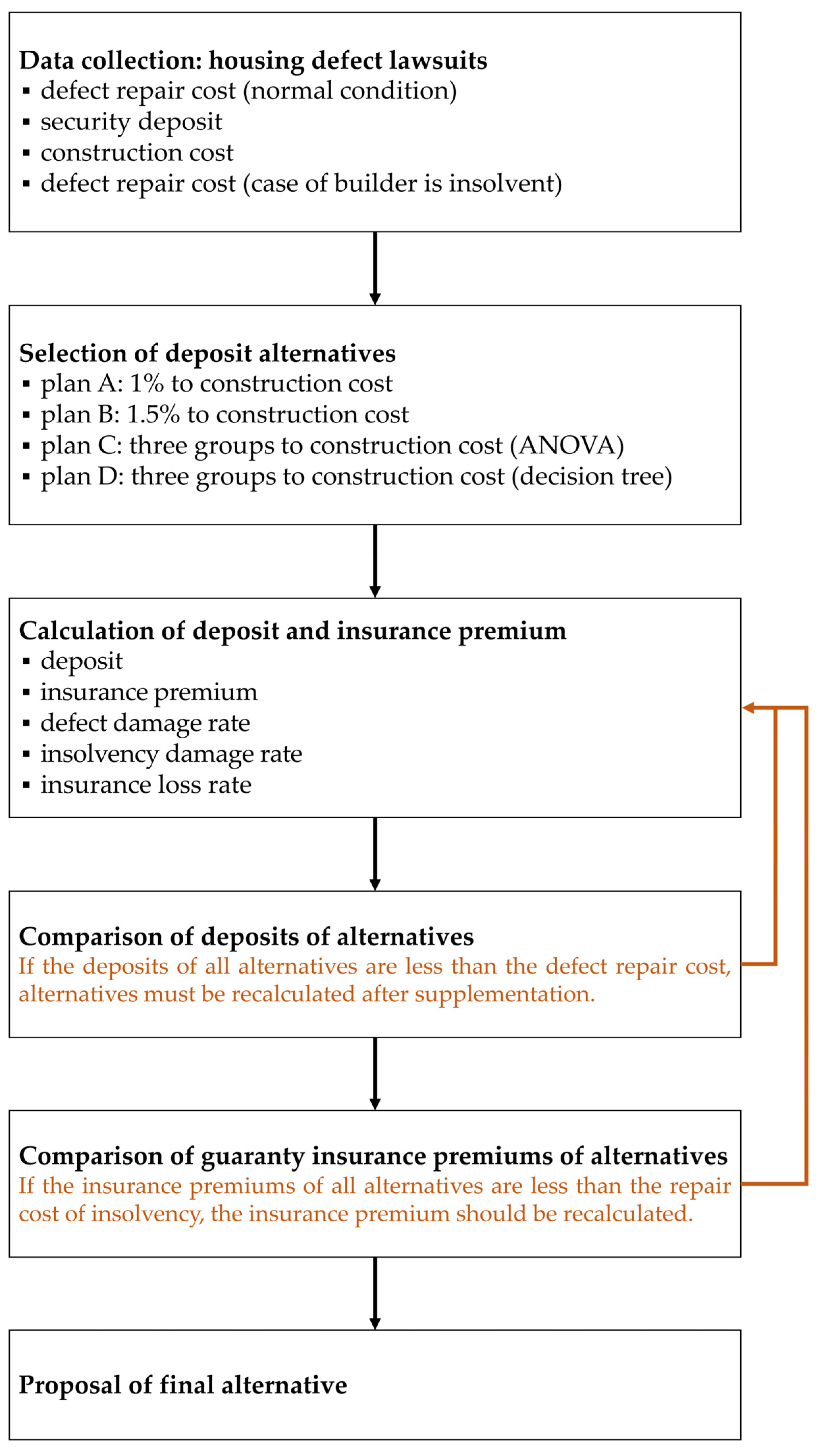

3.1. Framework

- (1)

- Data collection: The defect repair cost, security deposit, construction cost, and repair cost data, in the case where there is builder insolvency, are collected from cases of housing defect lawsuits.

- (2)

- Selection of deposit alternatives: Three alternative plans proposed in previous studies and one additional alternative plan proposed in this study are adopted. The current standards and the four alternative plans are compared.

- (3)

- Calculation of deposit and guaranty insurance premium: The deposit and guaranty insurance premium based on the data in (1) about the current standard and alternative plans in (2) are recalculated, and this is used to calculate the defect damage rate, insolvency damage rate, and insurance loss rate. The guaranty insurance premium is calculated by applying the insurance premium rate of the Korea Housing and Urban Guarantee Corporation, a representative guaranty company in Korea.

- (4)

- Comparison of deposits of alternatives: The deposits and defect repair costs of the four alternative plans recalculated in (3) are compared. If the deposits of all the alternative plans are less than the defect repair cost, these alternative plans are inappropriate as a standard, and the deposits and other miscellaneous items must be recalculated after supplementation.

- (5)

- Comparison of guaranty insurance premiums of alternatives: The guaranty insurance premiums of the four alternative plans recalculated in (3) and the repair cost in the case of insolvency are compared. If the guaranty insurance premiums of all alternative plans are less than the repair cost of builder insolvency, these alternative plans cannot protect the insolvency case. Therefore, the guaranty insurance premium should be recalculated.

- (6)

- Proposal of final alternative: It is proposed to select a reasonable and stable alternative plan by comparing whether the alternative plans for deposits and guaranty insurance premiums are appropriate.

3.2. Object and Scope

3.3. Data Collection

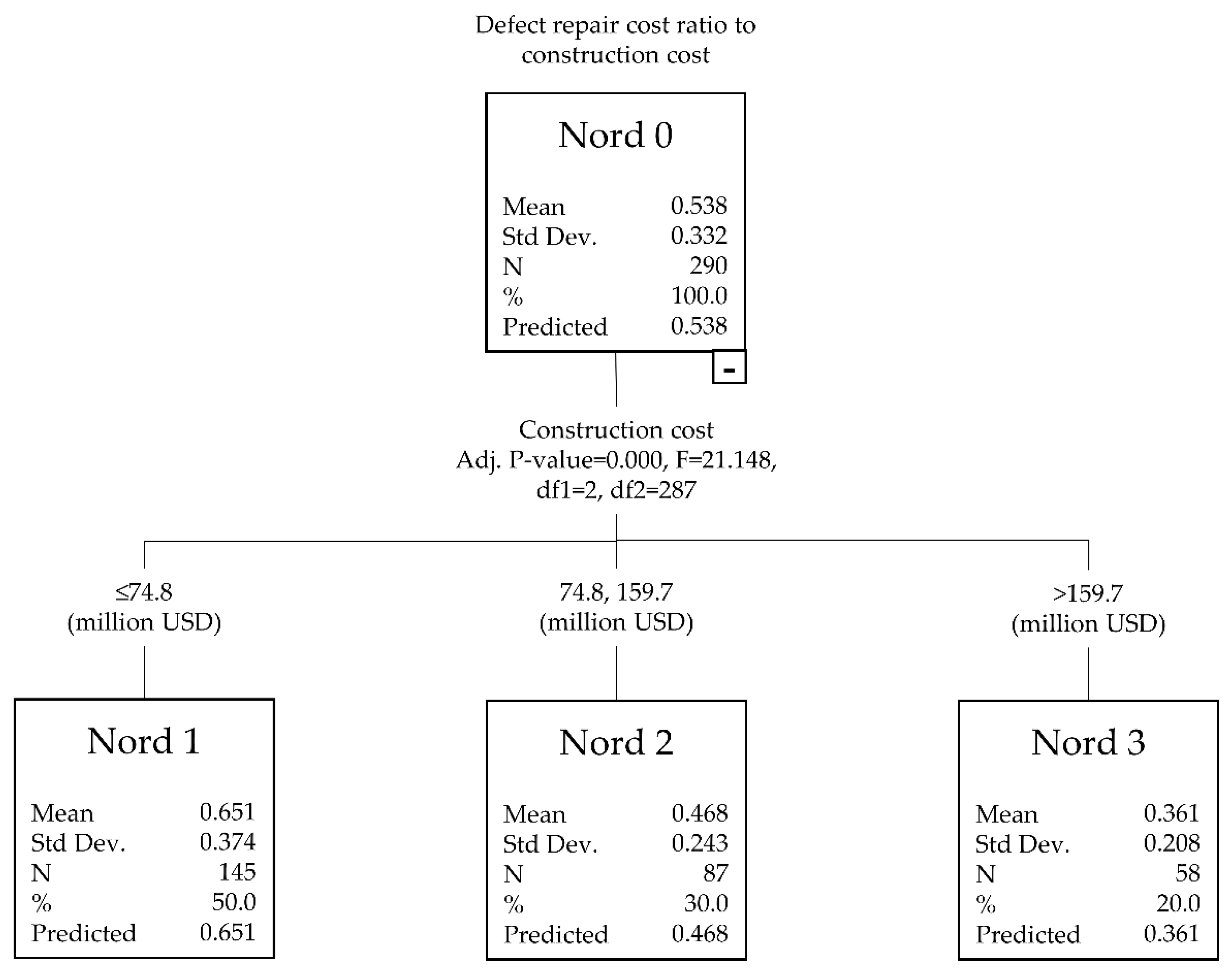

3.4. Alternative Plans for Deposit

3.5. Comparison

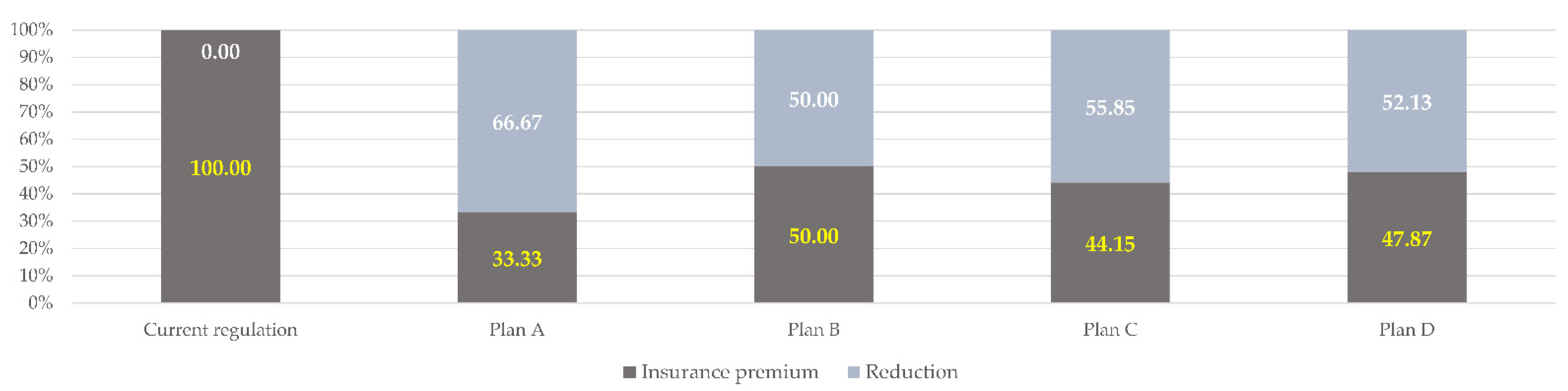

4. Results

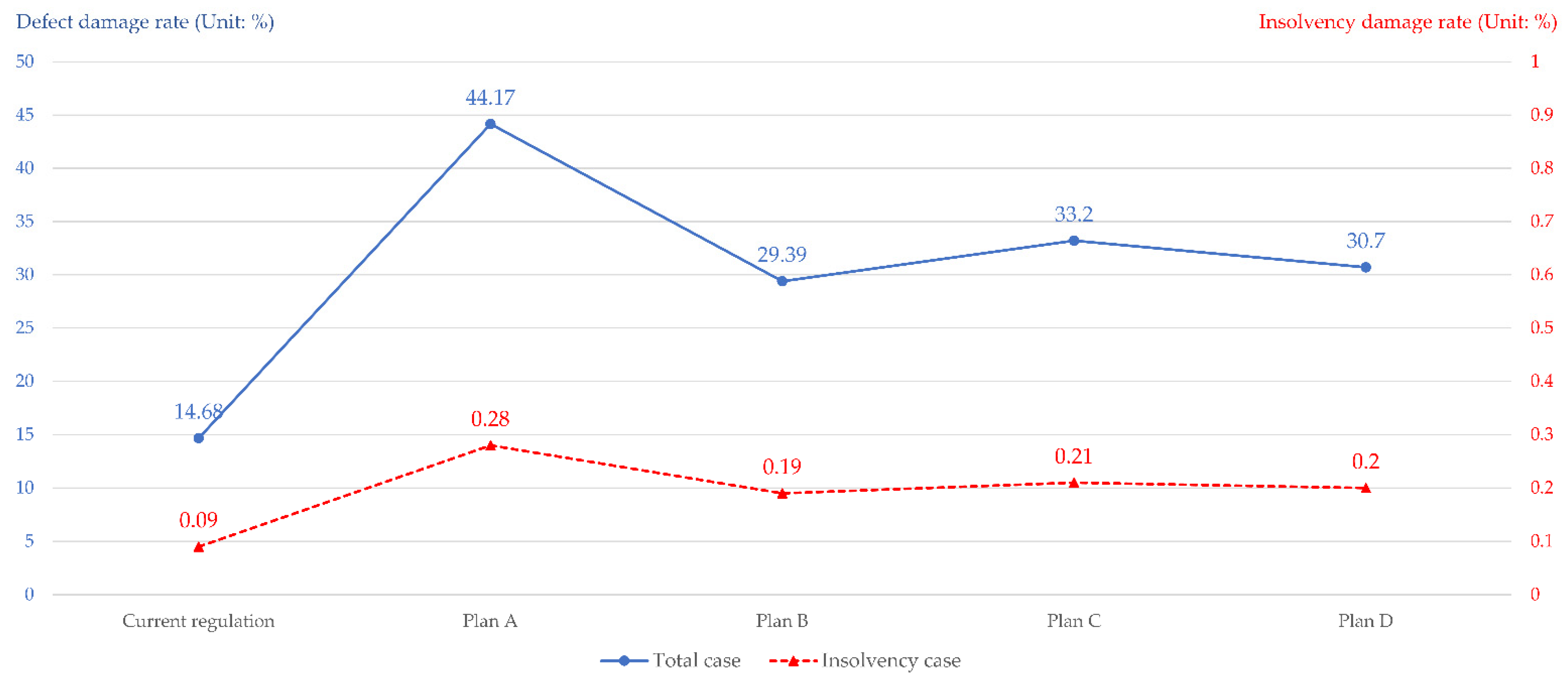

4.1. Deposit and Damage

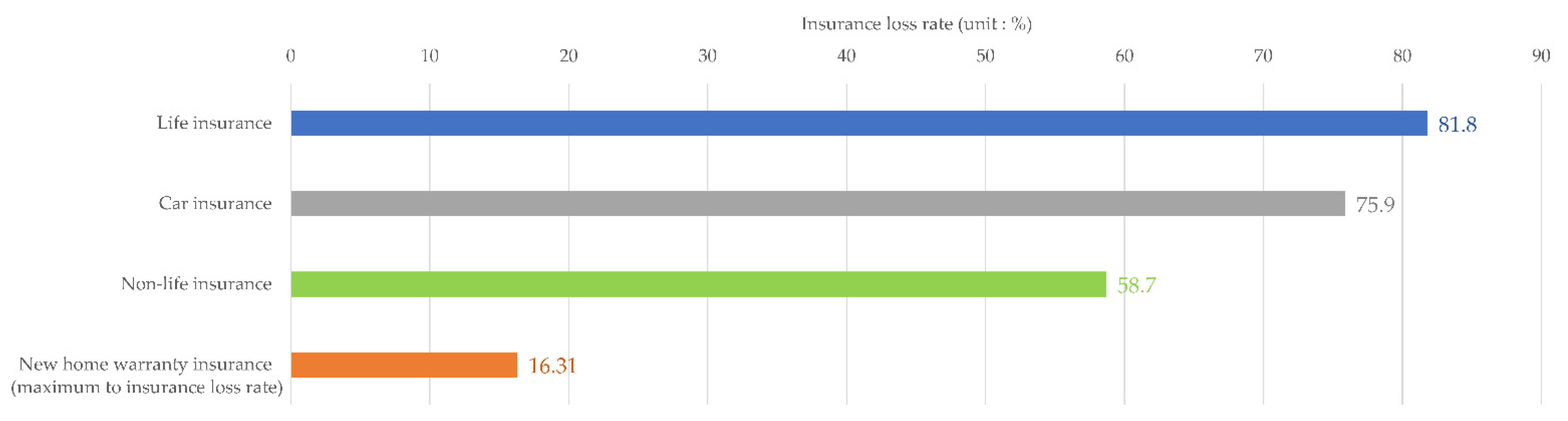

4.2. Insurance Premium and Loss

5. Discussion

5.1. Justification to Revise the New Home Warranty

5.2. Best Alternative Plan

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Kang, K.; Seo, D.; Kang, J. An Analytic Study on the Construction Errors Raised in Apartment House of Korea. J. Archit. Inst. Korea Struct. Constr. 1998, 14, 355–362. Available online: https://www.dbpia.co.kr/journal/articleDetail?nodeId=NODE00364887 (accessed on 15 August 2022).

- Gurmu, A.; Krezel, A.; Ongkowijoyo, C. Fuzzy-Stochastic Model to Assess Defects in Low-Rise Residential Buildings. J. Build. Eng. 2021, 40, 102318. [Google Scholar] [CrossRef]

- Tazelaar, F.; Snijders, C. Dispute Resolution and Litigation in the Construction Industry. Evidence on Conflicts and Conflict Resolution in the Netherlands and Germany. J. Purch. Supply Manag. 2010, 16, 221–229. [Google Scholar] [CrossRef]

- Park, J.; Seo, D. Construction Defect and Maintenance Problem of Watering Apparatus and Sanitary Work in Apartment Building. Int. J. Adv. Sci. Technol. 2020, 29, 949–961. [Google Scholar]

- Estienne, J.; Kamei, K. Japan’s House Construction Warranty, and Its Reinsurance System. Saf. Sci. Rev. 2013, 3, 21–40. Available online: http://hdl.handle.net/10112/00018568 (accessed on 15 August 2022).

- Housing and Home Finance Agency. Brief Summary of the Housing Act of 1954 Public Law 560, 83rd Congress 68 Stat. 590. Washington, DC, USA. 1954. Available online: https://repository.library.northeastern.edu/downloads/neu:bz60jd10c?datastream_id=content#:~{}:text=The%20Housing%20Act%20of%201954%2C%20approved%20by%20the%20President%200n,intensive%20study%20of%20the%20Federal (accessed on 15 August 2022).

- Meeks, C.; Oudekerk, E. Home Warranties: An Analysis of an Emerging Development in Consumer Protection. J. Consum. Aff. 1981, 15, 271–289. [Google Scholar] [CrossRef]

- Abbott, N. Domestic Building Contracts Act 1995. Available online: https://www.cbp.com.au/WWW_CBP/files/1c/1c76e9c7-1a64-4193-a774-2bfcd51596d6.pdf (accessed on 15 August 2022).

- Queen’s Printer. Homeowner Protection Act and Insurance Act. Available online: https://www.bclaws.gov.bc.ca/civix/document/id/complete/statreg/29_99#section7 (accessed on 15 August 2022).

- Japanese Digital Agency. Act on Assurance of Performance of Specified Housing Defect Warranty. Available online: https://elaws.e-gov.go.jp/document?lawid=419AC0000000066_20210930_503AC0000000048&keyword=%E4%BD%8F%E5%AE%85 (accessed on 15 August 2022).

- Database of Laws and Regulations. Guaranty Law of the People’s Republic of China. Available online: http://www.npc.gov.cn/zgrdw/englishnpc/Law/2007-12/12/content_1383719.htm (accessed on 15 August 2022).

- Korea Ministry of Government Legislation. Housing Act. Korean Law Information Center. Available online: https://www.law.go.kr/LSW/eng/engLsSc.do?menuId=2§ion=lawNm&query=housing+act&x=0&y=0#liBgcolor14 (accessed on 15 August 2022).

- Love, P.; Teo, P.; Morrison, J. Revisiting Quality Failure Costs in Construction. J. Constr. Eng. Manag. 2018, 144, 05017020. [Google Scholar] [CrossRef]

- Choi, J. Evaluation of Defect Repairing Bond Ratio through Defect Lawsuit Case Study in Apartment Building. Ph.D. Dissertation, Chungbuk National University, Cheongju, Republic of Korea, 2017. Available online: https://dcollection.chungbuk.ac.kr/public_resource/pdf/000000046423_20220705120413.pdf (accessed on 15 August 2022).

- Forcada, N.; Gangolells, M.; Casals, M. Factors Affecting Rework Costs in Construction. J. Constr. Eng. Manag. 2017, 20, 445–465. [Google Scholar] [CrossRef] [Green Version]

- Mills, A.; Love, P.; Williams, P. Defect costs in residential construction. J. Constr. Eng. Manag. 2009, 135, 12–16. [Google Scholar] [CrossRef]

- Josephson, P.; Larsson, B.; Li, H. Illustrative Benchmarking Rework and Rework Costs in Swedish Construction Industry. J. Manag. Eng. 2002, 18, 76–83. [Google Scholar] [CrossRef]

- Liu, Q.; Ye, G.; Feng, Y.; Wang, C.; Peng, Y. Case-based Insights into Rework Costs of Residential Building Projects in China. Int. J. Constr. Manag. 2020, 20, 347–355. [Google Scholar] [CrossRef]

- Hwang, B.; Thomas, S.; Haas, C.; Caldas, C. Measuring the Impact of Rework on Construction Cost Performance. J. Constr. Eng. Manag. 2009, 135, 187–198. [Google Scholar] [CrossRef]

- Park, M.; Seo, D. Defect Repair Cost and Home Warranty Deposit, Korea. Buildings 2022, 12, 1027. [Google Scholar] [CrossRef]

- O’Connor, J.; Koo, H. Analyzing the Quality Problems and Defects of Design Deliverables on Building Projects. J. Archit. Eng. 2020, 26, 04020034. [Google Scholar] [CrossRef]

- Abdou, A.; Haggag, M.; Khatib, O. Use of Building Defect Diagnosis in Construction Litigation: Case Study of a Residential Building. J. Leg. Aff. Disput. Resolut. Eng. Constr. 2015, 8, C4515007. [Google Scholar] [CrossRef]

- Park, J.; Seo, D. Defect Index of Timberwork in House, Korea. Forests 2021, 12, 896. [Google Scholar] [CrossRef]

- Park, J.; Seo, D. Post-Handover Quality Management Index of Electric Housing Work. Adv. Civ. Eng. 2022, 2022, 4690073. [Google Scholar] [CrossRef]

- Dreger, C. Economic Impact of the Corona Pandemic: Costs and the Recovery after the Crisis. Asia Glob. Econ. 2022, 2, 100030. [Google Scholar] [CrossRef]

- World Bank. GDP Growth. Available online: https://data.worldbank.org/indicator/NY.GDP.MKTP.KD.ZG (accessed on 19 December 2022).

- Lapavitsas, C. The Return of Inflation and the Weakness of the Side of Production. Jpn. Political Econ. 2022, 48, 149–169. [Google Scholar] [CrossRef]

- Fernández, M.; Alonso, S.; Forradellas, R.; Jorge-Vázquez, J. From the Great Recession to the COVID-19 Pandemic: The Risk of Expansionary Monetary Policies. Risks 2022, 10, 23. [Google Scholar] [CrossRef]

- Business Live. List of Construction Firms that have Collapsed into Administration Since 2021. Available online: https://www.business-live.co.uk/enterprise/list-construction-firms-collapsed-administration-22927348 (accessed on 15 August 2022).

- Levelset. California Construction Bankruptcies May 2022: Trend of Liquidation Bankruptcies Continues from April to May. Available online: https://www.levelset.com/news/california-construction-bankruptcies-may-2022/ (accessed on 15 August 2022).

- Canadian Minister of Industry. 2022 Insolvency Statistics in Canada. May 2022. Available online: https://publications.gc.ca/site/eng/9.507914/publication.html (accessed on 15 August 2022).

- China Internet Information Center. Company Bankruptcies in Japan Rise in April-September: Survey. Available online: http://www.china.org.cn/world/Off_the_Wire/2022-10/16/content_78469008.htm (accessed on 30 October 2022).

- Koreatimes. Specter of Bankruptcy Looms over Builders. Available online: https://www.koreatimes.co.kr/www/tech/2022/11/419_338275.html?utm_source=RD (accessed on 30 October 2022).

- Matsumoto, K.; Matsumura, S.; Tonami, T.; Numaoi, T.; Hokura, S.; Suganuma, Y.; Inagaki, N. Housing and Home Warranty Programs World Research; Organization for Housing Warranty: Tokyo, Japan, 2005. [Google Scholar]

- Inside Housing. Number of House Builder Insolvencies up 75% This Year. Available online: https://www.insidehousing.co.uk/news/news/number-of-house-builder-insolvencies-up-75-this-year-76422 (accessed on 15 August 2022).

- Smith, D. Builders’ Warranty: First Resort or Last Resort or does It really Matter? Presented at the Institute of Actuaries of Australia XVth General Insurance Seminar, Sydney, NSW, Australia, 16–19 October 2005; Available online: https://actuaries.asn.au/Library/gipaper_smith_paper0510.pdf (accessed on 30 October 2022).

- New Zealand Media and Entertainment. Over 10,000 New Home Warranties at Risk. Available online: https://www.nzherald.co.nz/business/over-10000-new-home-warranties-at-risk/D7YLV5IF2XM2UMPKIHHB4KR5PM/ (accessed on 15 August 2022).

- Yoo, H. Analysis if the Efficiency of Bank Mergers in Korea. Ph.D. Dissertation, Korea Maritime and Ocean University, Busan, Republic of Korea, 2001. Available online: http://www.riss.kr/search/download/FullTextDownload.do?control_no=d7ac573b50f4cc8d&p_mat_type=be54d9b8bc7cdb09&p_submat_type=b51fa0b5ced94fec&fulltext_kind=dbbea9ba84e4b1bc&t_gubun=&convertFlag=&naverYN=&outLink=&nationalLibraryLocalBibno=KDM200116073&searchGubun=true&colName=bib_t&DDODFlag=&loginFlag=1&url_type=&query=%ED%95%9C%EA%B5%AD+%EC%9D%80%ED%96%89+%ED%8C%8C%EC%82%B0&content_page=&url=&dbName=&dbId=&an=&dbNameDpShort=&pissn=&eissn= (accessed on 15 August 2022).

- Kwon, N. A Study on the Determinants of Failure of Savings Bank: Analysis of the Effects on Asset Size and Loan Behavior. Master’s Thesis, Hanyang University, Seoul, Republic of Korea, 2019. Available online: http://hanyang.dcollection.net/public_resource/pdf/200000436316_20221121131146.pdf (accessed on 15 August 2022).

- Jung, H.; Kim, J.; Hong, G. Impacts of the COVID-19 Crisis on Single-Person Households in South Korea. J. Asian Econ. 2022, 84, 101557. [Google Scholar] [CrossRef] [PubMed]

- Petrini, G.; Teixeira, L. Determinants of Residential Investment Growth Rate in the US Economy (1992–2019). Rev. Political Econ. 2022, 1–18. [Google Scholar] [CrossRef]

- Tarne, R.; Bezemer, D.; Theobald, T. The effect of borrower-specific loan-to-value policies on household debt, wealth inequality and consumption volatility: An agent-based analysis. J. Econ. Dyn. Control 2022, 144, 104526. [Google Scholar] [CrossRef]

- Residential Warranty Company. 10 Year New Home Warranty Features. Available online: https://www.rwcwarranty.com/builders/warranty-options/10-year-new-home-warranty-4/ (accessed on 15 August 2022).

- Insurance and Care NSW. HBCF Premium Guidelines. Available online: https://www.icare.nsw.gov.au/builders-and-homeowners/builders-and-distributors/premiums/premium-rates#gref (accessed on 15 August 2022).

- HIA Insurance Services. Home Warranty Insurance Forms. Available online: https://www.hiainsurance.com.au/forms/home-warranty-forms (accessed on 15 August 2022).

- Wowa Leads Inc. Home Warranty in Canada. Available online: https://wowa.ca/home-warranty-canada (accessed on 15 August 2022).

- National House Building Council. What Is Premium Rating? Available online: https://www.nhbc.co.uk/builders/warranties-and-cover/frequently-asked-questions (accessed on 15 August 2022).

- Association of Housing Warranty Insurers. About Insurance Subscription. Available online: https://www.kashihoken.or.jp/business/shinchiku/kashihoken/subscription.html (accessed on 15 August 2022).

- Jutakuanshin Warranty Ltd. Safe House Defect Insurance. Available online: https://www.j-anshin.co.jp/service/kashihoken/estimate/ (accessed on 15 August 2022).

- Organization for Housing Warranty Ltd. Covert Insurance. Available online: https://www.mamoris.jp/kasitanpo/price/ (accessed on 15 August 2022).

- National Law Information Center. A Judged Standard, Investigated Method and Estimated Costing of Defect in Dwelling House, South Korea. 2016. Available online: http://www.law.go.kr/admRulSc.do?menuId=5&query=%ED%95%98%EC%9E%90%ED%8C%90%EC%A0%95#liBgcolor0. (accessed on 5 March 2023).

- National Law Information Center. Multi-Family Housing Management Act. South Korea, 2016. Available online: https://www.law.go.kr/lsInfoP.do?lsiSeq=185470&ancYd=20160811&ancNo=27445&efYd=20160812&nwJoYnInfo=N&efGubun=Y&chrClsCd=010202&ancYnChk=0#0000. (accessed on 5 March 2023).

- Korea Housing & Urban Guarantee Corporation. Available online: https://www.khug.or.kr/hug/web/cg/dr/cgdr000001.jsp (accessed on 15 August 2022).

- Construction Guarantee Cooperative. Available online: https://www.cgbest.co.kr/cgbest/guarantee/products01-07.do (accessed on 15 August 2022).

- Seoul Guaranty insurance Corporation. Available online: https://www.sgic.co.kr/chp/iutf/hp/insurance/CHPINFO002VM0_06.mvc?q_insrnSrlno=64 (accessed on 15 August 2022).

- Tomas Ng, S.; Fan, R.; Wong, J.; Chan, A.; Chiang, Y.; Lam, P. Coping with Structural Change in Construction: Experiences gained from Advanced Economies. Constr. Manag. Econ. 2009, 27, 165–180. [Google Scholar] [CrossRef]

- Kim, N. A Study on Legal Issue in the Formation Sale in lots Management of Condominium. Ph.D. Dissertation, Korea University, Seoul, Republic of Korea, 2013. Available online: https://dcollection.korea.ac.kr/public_resource/pdf/000000046137_20221223145246.pdf (accessed on 15 August 2022).

- Kwak, K. Model for the Prediction of the Housing Sold Guarantee Accident based on the Housing Construction Site Characteristics. Ph.D. Dissertation, Hansung University, Seoul, Republic of Korea, 2013. Available online: http://hansung.dcollection.net/public_resource/pdf/000002061012_20221223145454.pdf (accessed on 15 August 2022).

- Murphy, P.; Lakoma, K.; Eckersley, P.; Dom, B.; Jones, M. Public goods, public value, and public audit: The Redmond review and English local government. Public Money Manag. 2022, 1–9. [Google Scholar] [CrossRef]

- All Public Information in-One. Current Status of Capitals and Shareholders. 2022. Available online: https://www.alio.go.kr/item/itemReport.do?seq=2022040902417217&disclosureNo=2022040902417217. (accessed on 15 August 2022).

- Construction Guarantee Cooperative. Cooperative System. 2022. Available online: https://www.cgbest.co.kr/en/cg/cooperative.do. (accessed on 15 August 2022).

- Seoul Guaranty insurance Corporation. Summary of Major Management Status. 2022. Available online: https://www.sgic.co.kr/chp/fileDownload/download.mvc?fileId=017FDEAF902F8FBA1D611D61. (accessed on 15 August 2022).

- Zhang, W.; Su, Y.; Ke, R. Evaluating the Influential Priority of the Factors on Insurance Loss of Public Transit. PLoS ONE 2018, 13, e0190103. [Google Scholar] [CrossRef] [Green Version]

- Xie, S.; Luo, R.; Li, Y. Exploring Industry-Level Fairness of Auto Insurance Premiums by Statistical Modeling of Automobile Rate and Classification Data. Risks 2022, 10, 194. [Google Scholar] [CrossRef]

- Jeon, Y.; Yoon, S.; Kim, Y. International Comparison to Automobile Insurance: Focus on Insurance Loss Rate and Market Rigidity; Korea Insurance Research Institute: Seoul, Republic of Korea, 2021; Available online: https://www.kiri.or.kr/flexerView.do?FileDir=/pdf/%EC%A0%84%EB%AC%B8%EC%9E%90%EB%A3%8C&SystemFileName=nre2021-09.pdf&ftype=pdf&FileName=nre2021-09.pdf (accessed on 15 August 2022).

- Kim, K. Study on the Effects of Regional Characteristics on the Loss Ratio of Housing Fire Insurance. Ph.D. Dissertation, Changwon National University, Changwon, Republic of Korea, 2020. Available online: https://dcollection.changwon.ac.kr/public_resource/pdf/000000015845_20221124151758.pdf (accessed on 15 August 2022).

- Korea Ministry of Government Legislation. Enforcement Decree of the Housing Act. Korean Law Information Center. Available online: https://www.law.go.kr/LSW/eng/engLsSc.do?menuId=2§ion=lawNm&query=housing+act&x=0&y=0#liBgcolor0 (accessed on 15 August 2022).

- Court of Korea. Case Search Service. Available online: https://www.scourt.go.kr/portal/information/events/search/search.jsp (accessed on 15 August 2022).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Nation | Estimation Factor To Insurance Premium |

|---|---|

| United State of America | Number of homes, average sale price, a record of the contractor |

| Australia | Construction type, contract value, location of the home, icare builder rating |

| Canada | Home sales price, enrolment fee, HCRA regulatory oversight fee |

| United Kingdom | Duration of enrolment to the association, number of claims |

| Japan | Enrolment fee, inspection fee, reinsurance premium, dispute resolution fee, amount of intentional gross negligence damage |

| South Korea | Deposit, warranty fee rate, duration of the warranty |

| Warranty Company | Basis of Establishment | Type | Major Shareholder | Shareholding Rate of Major Shareholders |

|---|---|---|---|---|

| KHUGC | Housing and Urban Fund Act | Public corporation | Korean government | 70.25% |

| CGC | Framework Act on the Construction Industry | Mutual aid association | Undisclosed | Undisclosed |

| SGIC | Special Act on the Management of Public Funds | Public corporation | Korea Deposit Insurance Corporation | 93.85% |

| Index | Plan C: Park and Seo | Plan D: This Study | |||||

|---|---|---|---|---|---|---|---|

| Less than USD 62M | USD 62–125M | More than USD 125M | Less than USD 74.8M | USD 74.8–159.7M | More than USD 159.7M | ||

| DRC ratio to CC | Max | 2.22% | 1.47% | 0.93% | 2.22% | 1.47% | 0.93% |

| Mean | 0.67% | 0.50% | 0.39% | 0.65% | 0.47% | 0.37% | |

| Minimum | 0.09% | 0.00% | 0.03% | 0.09% | 0.00% | 0.03% | |

| No. of cases | 117 | 92 | 81 | 145 | 87 | 58 | |

| Suggested DRC ratio | 2.5% | 1.5% | 1.0% | 2.5% | 1.5% | 1.0% | |

| Metrics | Current Regulation (USD Million) | Plan A (USD Million) | Plan B (USD Million) | Plan C (USD Million) | Plan D (USD Million) |

|---|---|---|---|---|---|

| Deposit of total case | 981 | 326 | 490 | 433.8 | 469 |

| DRC of total case | 144 | 144 | 144 | 144 | 144 |

| DRC of insolvency case | 0.92 | 0.92 | 0.92 | 0.92 | 0.92 |

| Insurance Premium Ratio | Current Regulation (USD Million) | Plan A (USD Million) | Plan B (USD Million) | Plan C (USD Million) | Plan D (USD Million) |

|---|---|---|---|---|---|

| Max | 39.61 | 13.2 | 19.81 | 17.52 | 18.94 |

| Mean | 22.63 | 7.54 | 11.31 | 10.00 | 10.82 |

| Min | 5.64 | 1.88 | 2.82 | 2.49 | 2.70 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Park, J.; Seo, D. Defect Repair Deposit and Insurance Premium for a New Home Warranty in Korea. Buildings 2023, 13, 815. https://doi.org/10.3390/buildings13030815

Park J, Seo D. Defect Repair Deposit and Insurance Premium for a New Home Warranty in Korea. Buildings. 2023; 13(3):815. https://doi.org/10.3390/buildings13030815

Chicago/Turabian StylePark, Junmo, and Deokseok Seo. 2023. "Defect Repair Deposit and Insurance Premium for a New Home Warranty in Korea" Buildings 13, no. 3: 815. https://doi.org/10.3390/buildings13030815