1. Introduction

In 2020, China announced at the UN Climate Conference that its carbon dioxide emissions would peak by 2030 and become carbon neutral by 2060. The carbon emissions from buildings account for more than 40% of the total carbon emissions in the whole cycle [

1,

2,

3]. Housing is one of the top four sources of carbon emissions in Europe, accounting for a significant share of the total carbon emissions in society [

4]. Carbon emissions run through all aspects of the construction industry. There is plenty of room to reduce carbon emissions in building materials and construction [

5,

6]. In the context of carbon peak and carbon neutral, it is very important to reduce the carbon emissions of the construction industry. Prefabricated construction enterprises (PCEs) need to transfer a large number of operations in traditional construction methods from the construction site to the construction factory. These constructs and fittings are installed to construct the building through reliable connections [

7]. The goal of carbon peak and carbon neutrality promotes the development of PCEs towards green digital innovation [

8].

The construction industry can be developed by accelerating the transformation of traditional construction methods. First, the traditional construction industry is based on on-site manual work. This approach has problems, such as low resource utilization efficiency and construction safety [

9]. The parts of prefabricated buildings are made in a factory and assembled on site with reliable connections. As a result, this approach has the characteristics of standardized design, factory production, construction and prefabricated, integration of decoration, management information, intelligent application, and so on [

10]. Second, in the past few decades, the progress of the cast-in-place concrete building model has benefitted from China’s abundant labor resources. However, with the gradual disappearance of the demographic dividend and the rapid increase in labor costs, labor-intensive production mode will be unsustainable. At the same time, it not only accelerated the upgrading of the traditional construction industry to the industrialization of construction but also promoted the overall progress of the construction industry [

11,

12]. Third, the traditional construction industry has caused great damage to the ecology and environment, mainly reflected in the carbon emissions [

13]. The modular, industrial production of prefabricated components can also minimize the discharge of construction waste, save consumables, and reduce air, noise, and other pollution. Therefore, it can reduce carbon emissions over the life of the building [

14,

15,

16,

17,

18]. If prefabricated buildings can replace conventional buildings on a large scale in the future, carbon emissions will be greatly reduced.

However, the development of PCEs in China is still facing great challenges. The first is that PCEs are increasingly demanding carbon reduction [

19]. At present, many developed countries have decoupled carbon emissions from economic development, but China is still in the stage of increasing carbon emissions and has not reached the peak [

20]. As one of the industries with high carbon emissions, carbon emission reduction means that the production mode, technological level, material selection, and business model in the industry will face innovation. The goal of carbon peak and carbon neutrality puts forward new requirements for the traditional construction industry. It also means that PCEs have higher requirements for carbon reduction [

21,

22]. The second is the low degree of intelligent PCEs [

23]. In the prefabricated building industry, chain technology, prefabricated shear wall structure connection, site installation and construction and acceptance methods, and other key technologies are not yet mature. In addition, related technical standards, norms, and construction methods cannot keep up, resulting in varying degrees of constraints on its development [

24]. In the degree of standardization, the modular production and standardization of building components are relatively low. General components are used less. These conditions result in low construction efficiency and a high cost of prefabricated buildings. It is difficult to give full play to the advantages of industrialization [

25].

In the face of the above problems, PCEs solve them through green digital innovation projects. In recent years, promoting the development of PCEs through research and development projects has become a hot spot of scholars’ research [

26,

27,

28,

29]. Many companies are also carrying out this activity. In April 2021, the Yunnan Kunming Steel Construction Group Co., Ltd. Green Prefabricated Building Innovation Studio was established. The green prefabricated building design research and development innovation group, green and intelligent manufacturing innovation group, and green building construction and installation method innovation group were set up. They promote advanced concepts and technology to solve the technical bottleneck of production and operation. In May of the same year, the Hubei Provincial Intelligent Construction Science and Technology Innovation Consortium was established. In addition, in order to empower the transformation and upgrading of the construction industry in Hubei Province, all the member units will jointly summarize and form a list of key technologies of intelligent construction.

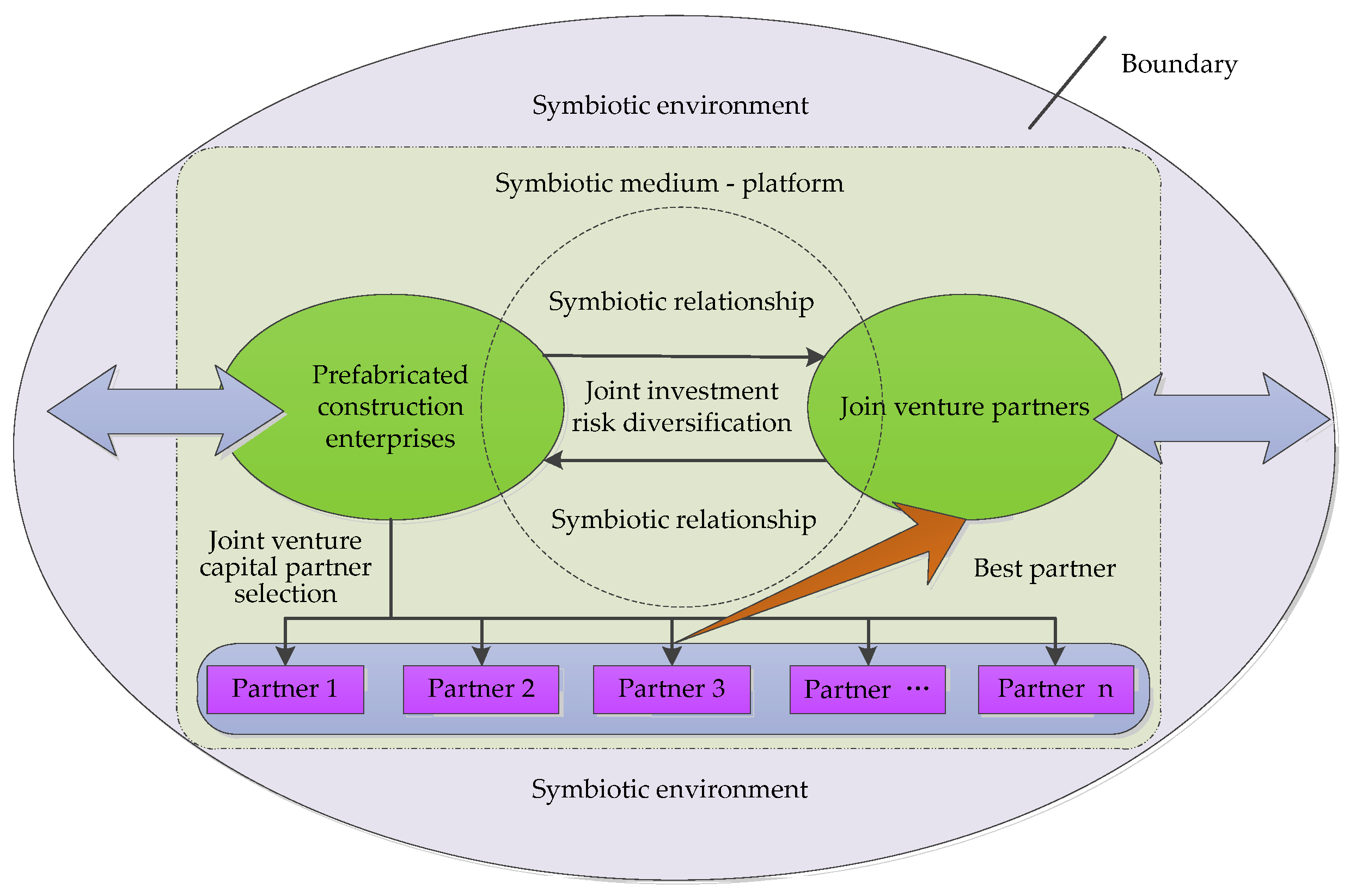

As the spillover effect of technological innovation becomes more and more prominent, how to effectively conduct digital green innovation activities has become a very important problem in the development of PCEs. In the process of promoting the development of PCEs, they have to face huge financial and risk pressure. In addition, other PCEs are also searching for methods. In the market, there is more cooperation between PCEs, which provides a way to solve this dilemma. However, it also involves the issue of partner selection [

30]. At present, many systematic approaches provide ideas for choosing joint investment partners, but there are still some shortcomings.

In recent years, many scholars have studied partner selection in terms of the methods and index system [

31,

32,

33,

34,

35,

36,

37,

38,

39]. The research methods mainly include the partner evaluation method, the attribute weighting method, and the weighting method. As for the partner evaluation method, analytic hierarchy process (AHP) and data envelopment analysis (DEA) methods were adopted before, while some new methods and combined methods were adopted in recent years [

31,

32,

33,

34,

35]. This research is mainly committed to considering all kinds of complex factors. With respect to the attribute weighting method, there are mainly linear programming models, methods for minimum and maximum entropy values, membership, and non-membership methods. Regarding the weighting method, there are mainly techniques for the order preference by similarity to an ideal solution (TOPSIS) method, coefficient of variation method, and ideal point method [

36,

37,

38,

39]. In terms of the index system, some scholars proposed that innovation has an important impact on partner selection [

31,

32,

33]. Some scholars believed that technology plays a non-negligible role in partner selection [

34,

35,

36]. Many scholars expressed their views in choosing methods and systems, but there are still some shortcomings [

37,

38,

39]. In the selection of methods, most previous studies have focused on a single subjective or objective weight. However, there are fewer studies of intuitive fuzzy weights and their combination with objective weights. There is a lack of a certain degree of combing and summary in the construction of the system, which cannot explain the level of digital green innovation projects carried out by PCEs under the goal of double-carbon. It is not conducive to the evaluation of the implementation and a full grasp of its situation.

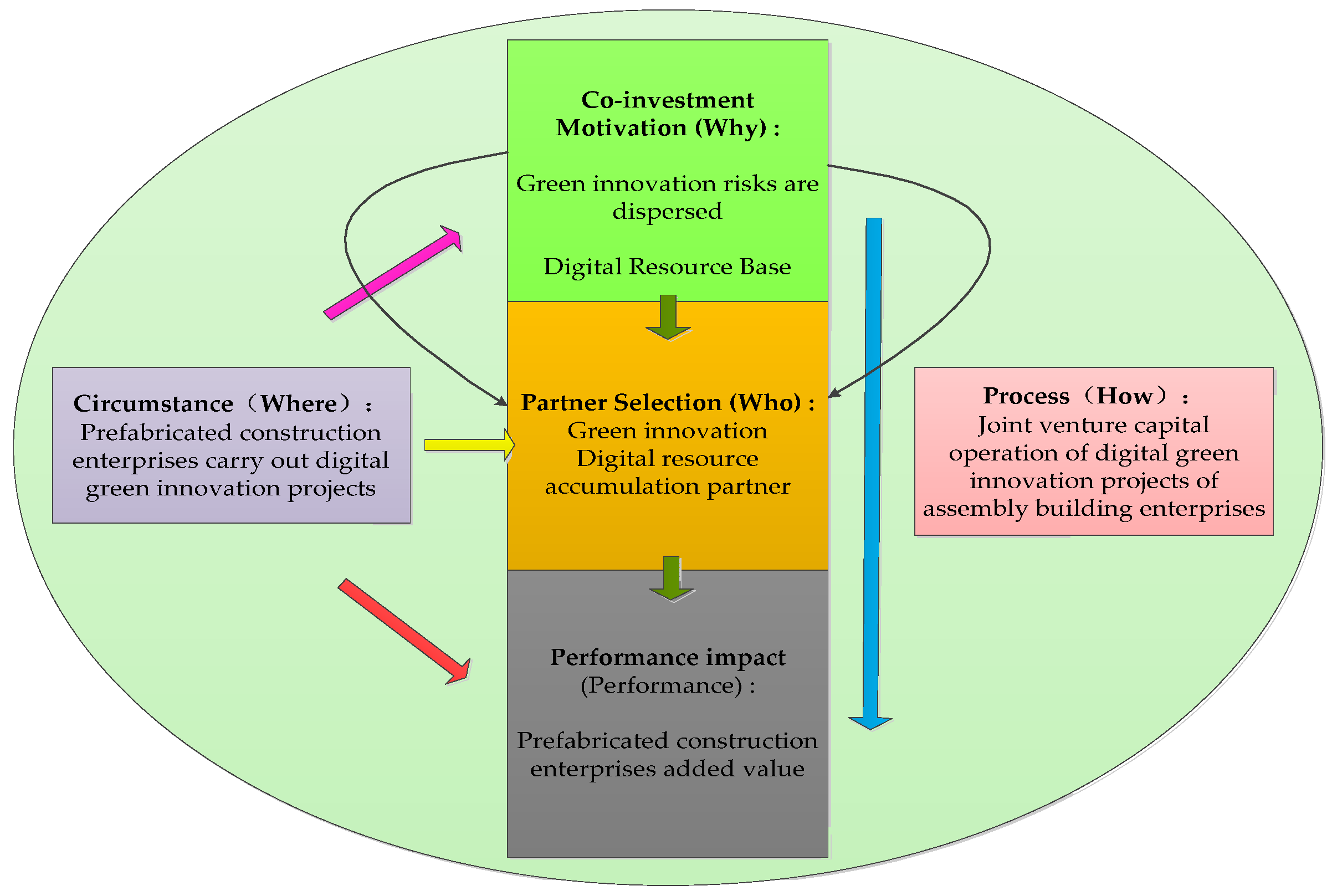

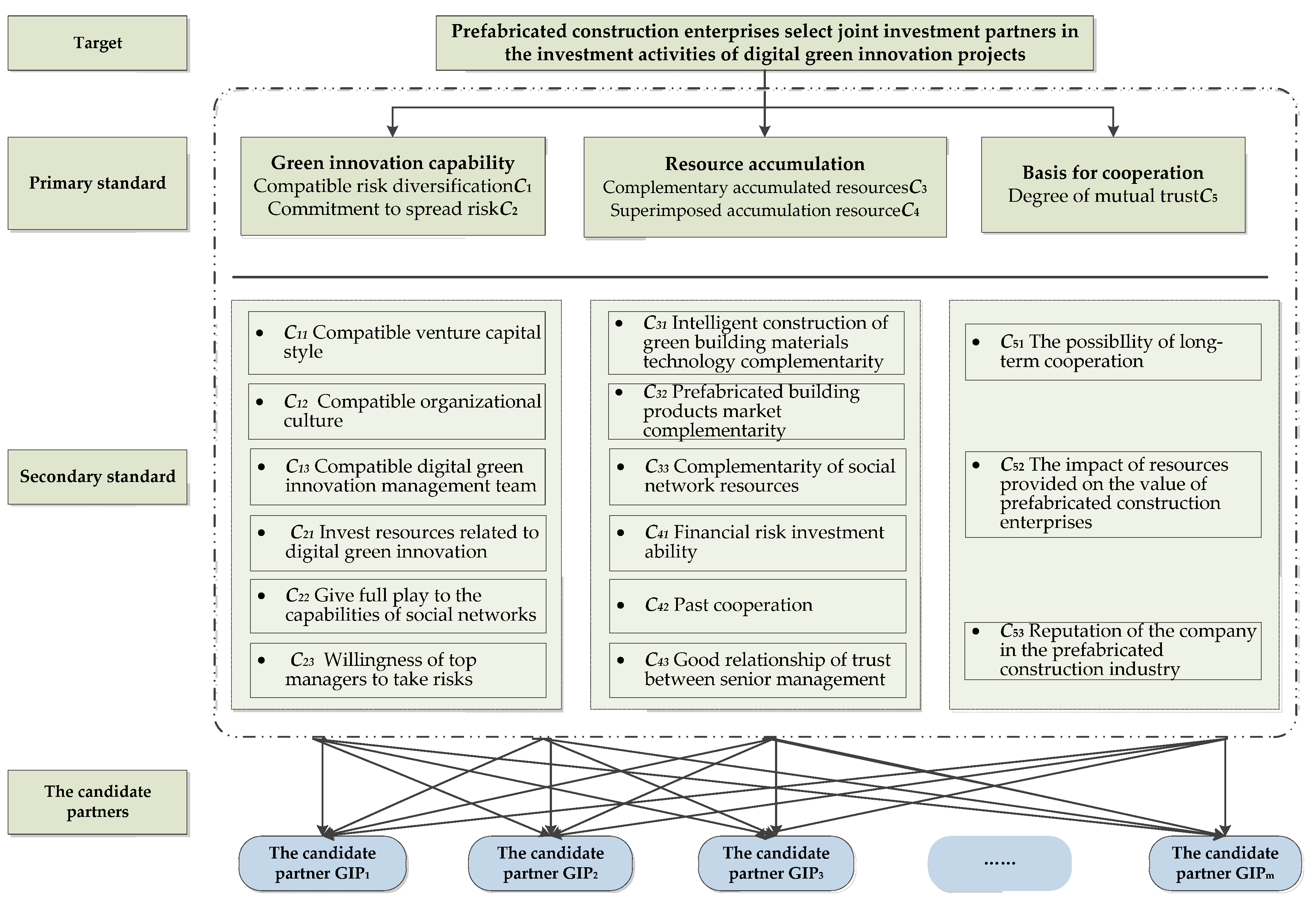

To solve the above problems, the purpose of this research is to build a research system to select joint investment partners and select scientific methods to promote the digital green innovation development of PCEs. Firstly, a new fuzzy entropy comprehensive evaluation formula is proposed based on the entropy method and TOPSIS method. Second, combined with the existing research index system, this paper divides the joint venture capital partners of PCEs into risk indicators and resource indicators under the dual-carbon goal. This study builds a research system of PCEs choosing joint investment partners in the investment activities of digital green innovation projects. This study expounds the relevant theory and proposes the fusion method.

The rest of this paper is as follows.

Section 2 is a literature review and frame system. The methodology is elucidated in

Section 3.

Section 4 is the empirical study. Conclusions and future prospects are presented in

Section 5.

5. Conclusions and Enlightenment

5.1. Conclusions

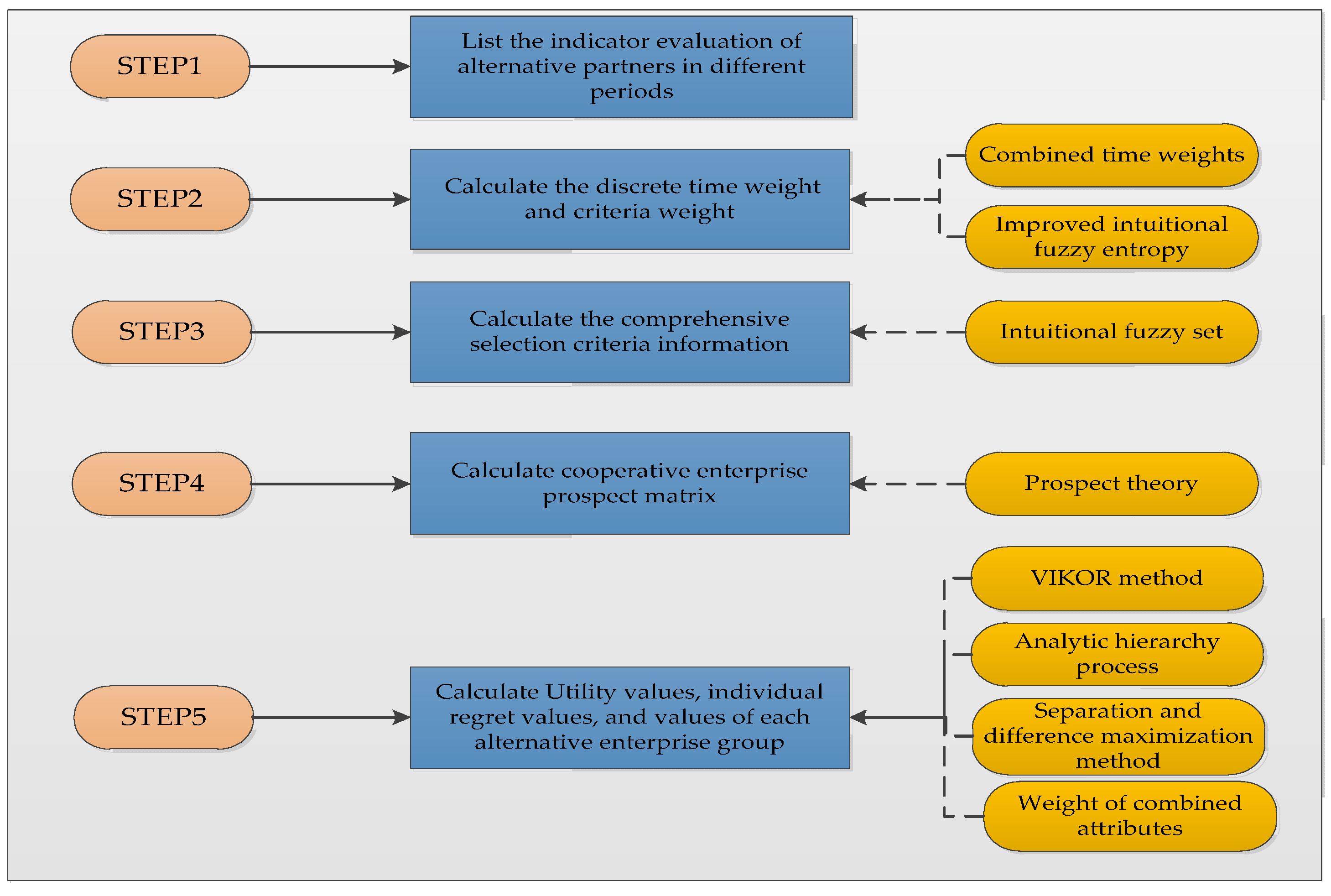

With the background of carbon peak and carbon neutrality, it is very necessary for the construction industry to carry out digital green and innovative activities. It has gradually become an inevitable trend for PCEs to adapt to the new era, create new models, and develop healthily and long-term by choosing joint investment partners in the development of digital green innovative project investment activities. First, in this study, a theoretical model for PCEs to select joint investment partners in digital green innovative project investment activities was constructed. Second, with the help of the idea of six analysis methods, this study innovatively proposed a research framework of joint venture capital 3W1H-P by integrating logical relations. Third, on this basis, the research system of selecting joint investment partners was constructed. Fourth, intuitionistic fuzzy set, intuitionistic fuzzy number aggregation operator, and intuitionistic fuzzy entropy were expounded. The combined theoretical knowledge of combined time weight, improved intuitionistic fuzzy number entropy, and the VIKOR method is proposed. This practice brings positive enlightenment to other PCEs when they choose joint investment partners to make decisions in the investment activities of digital green innovative projects.

The results are drawn as follows. This study constructed a theoretical model of PCEs selecting joint investment partners. This study proposed the research framework of 3W1H-P. This study constructed a research system for the selection of joint investment partners. The research system includes green innovation capacity indicators, cooperation basic indicators, resource accumulation indicators, etc. This study indicates that the joint venture investment network theoretical model, the joint venture investment 3W1H-P research framework, research system, and applied theory can enable Tianfeng to select the optimal partner. Further, this approach can be applied to the selection of joint investment partners by global PCEs in the development of digital green innovative project investment activities.

5.2. Implications

This study has important management implications. This study not only constructed a theoretical model in the joint venture investment network but also innovatively proposed a 3W1H-P research framework of joint venture investment by integrating logical relations with the idea of six analysis methods. On this basis, a research system for PCEs to select joint investment partners in the investment activities of digital green innovative projects was constructed. The theoretical model, research framework, and research system can be used to assist PCEs to select joint investment partners in the investment activities of digital green innovative projects. This study has important theoretical implications. In this study, intuitionistic fuzzy set, intuitionistic fuzzy number aggregation operator, intuitionistic fuzzy entropy, AHP, deviation maximization method, combinatorial attribute weight, and prospect theory were theoretically expounded, and the theoretical knowledge of combination time weight, improved intuitionistic fuzzy number entropy, and the VIKOR method was proposed.

5.3. Deficiencies and Future Prospects

There are still some limitations in this study that deserve further attention. Artificial intelligence (AI) technology is gradually applied to decision-making problems, and the combination of resource complementarity and AI plays an important role in future enlightenment. In addition, only one case study was conducted in this study, and future studies may include large sample sizes from many PCEs to verify the correctness of the theoretical models, frameworks, systems, and use of theoretical knowledge. PCEs can be classified according to the scale of R&D or enterprise size.

{kind=link}

{kind=link}

{kind=link}

{kind=link}