Methods for the Calculation of the Lost Profit in Construction Contracts

Abstract

:1. Introduction

2. Materials and Methods

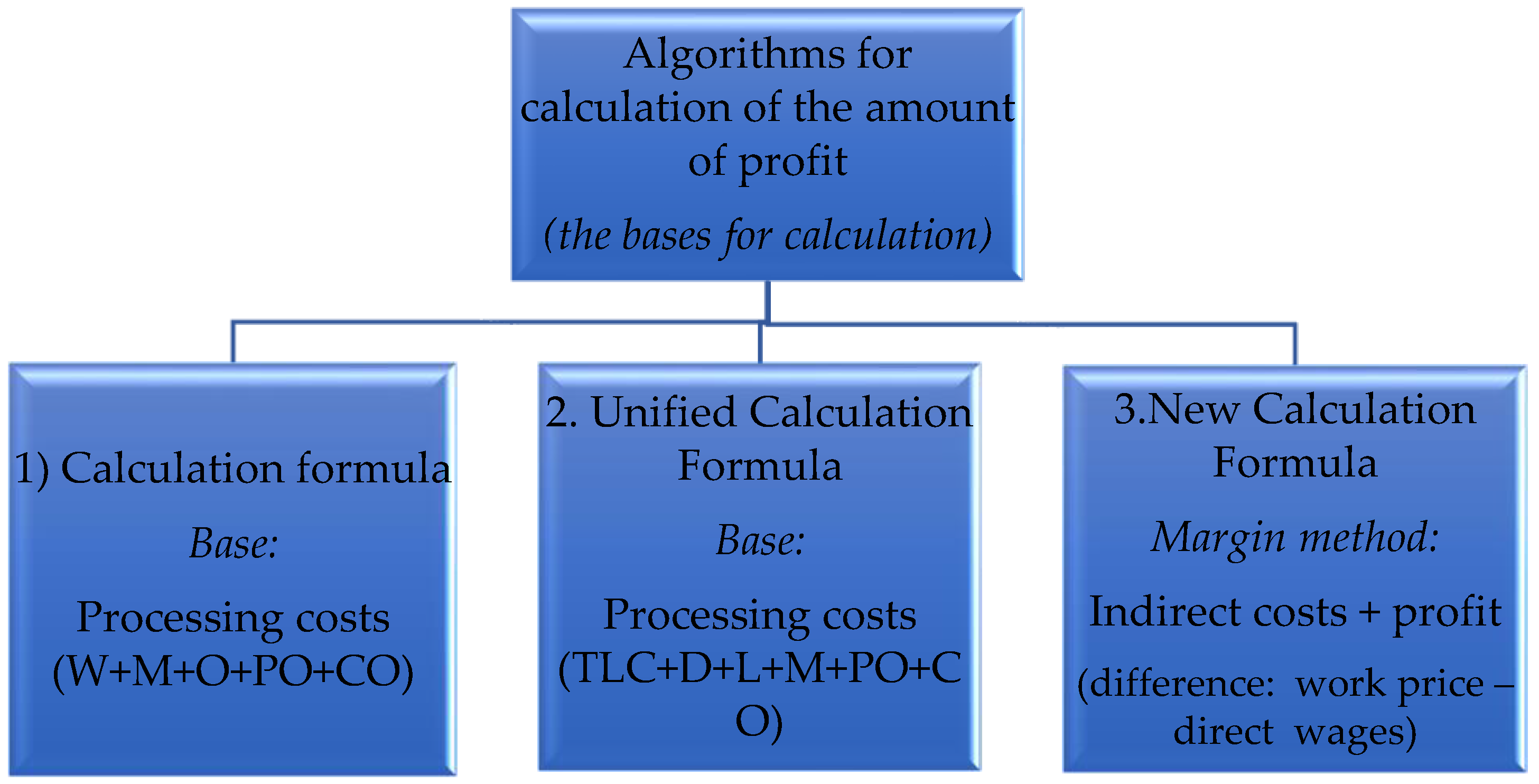

2.1. Algorithms of Profit Calculation

2.2. Methods of Calculation of Lost Profits in Our and Foreign Construction Practice

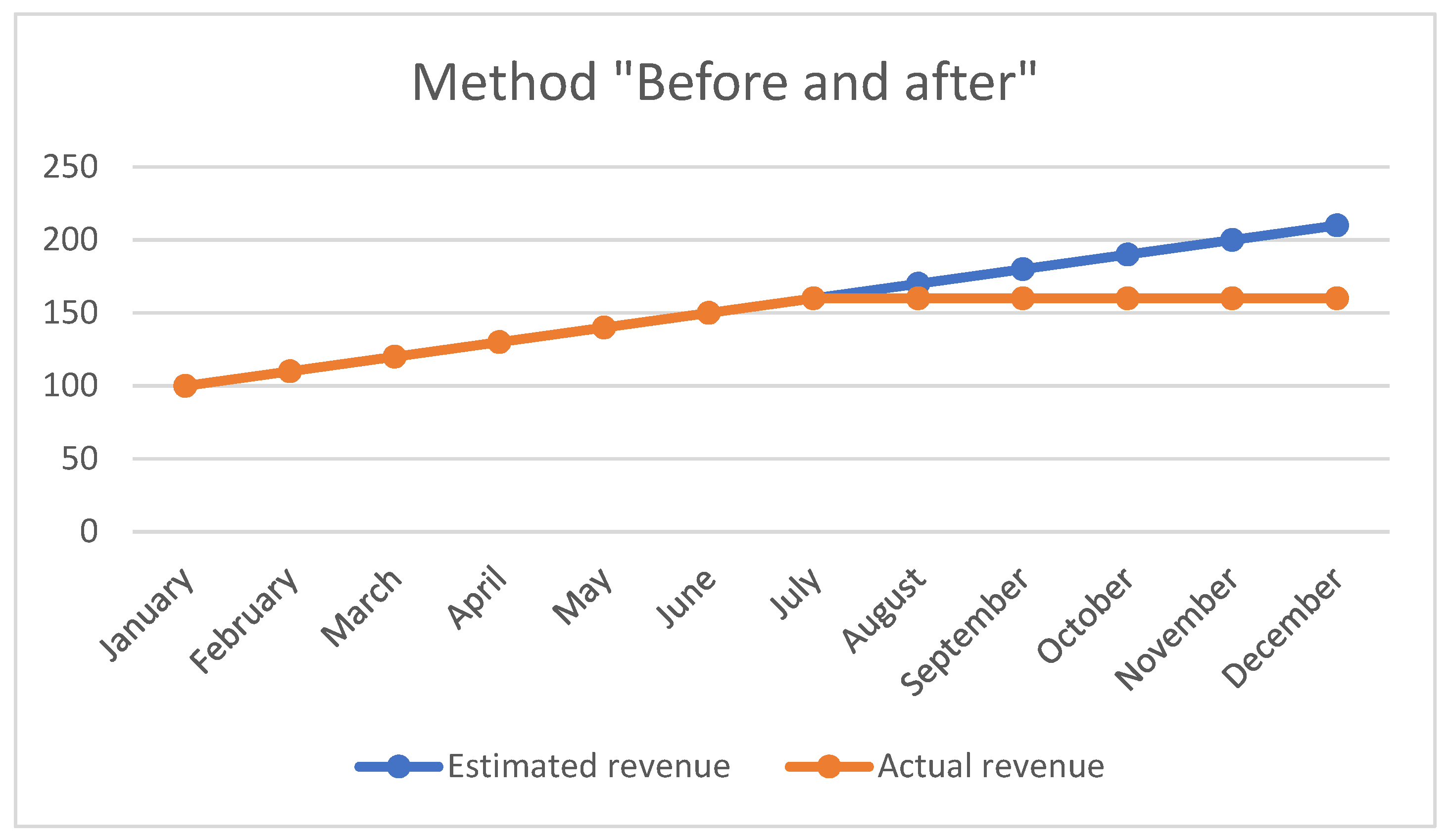

2.2.1. The “Before and After” Method

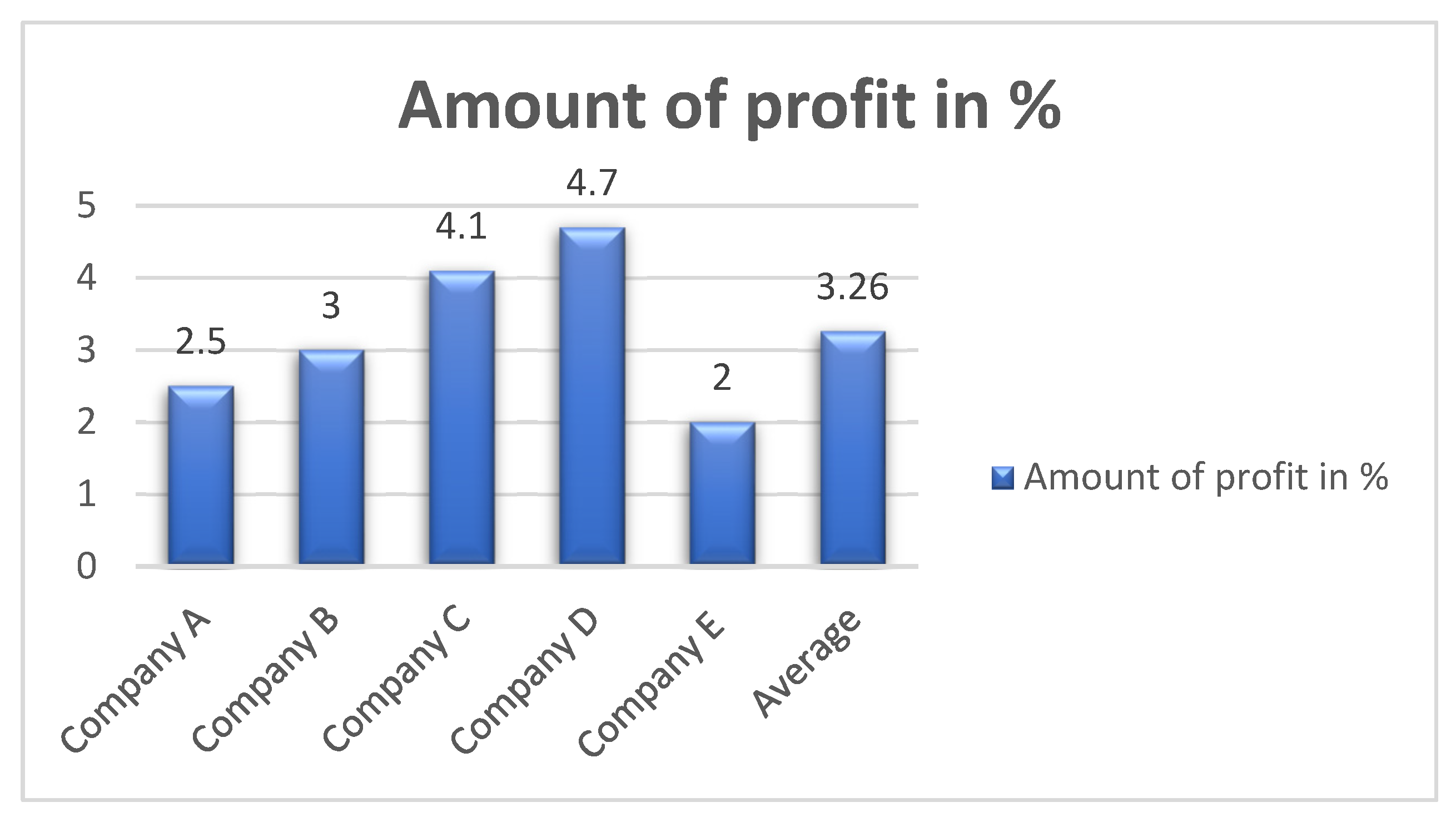

2.2.2. Comparison Method (Yardstick)

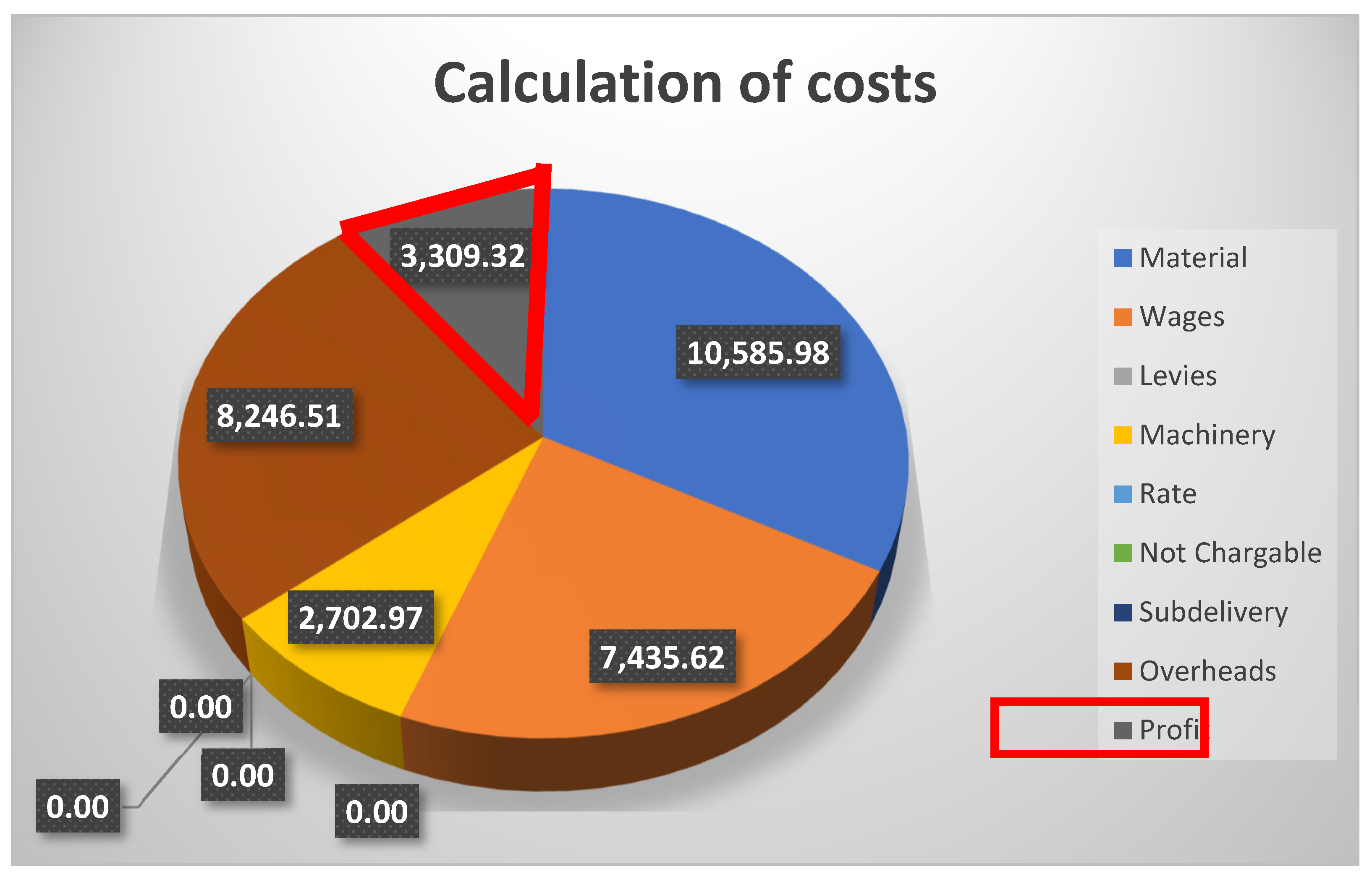

2.2.3. Method of Using Valuation Tools

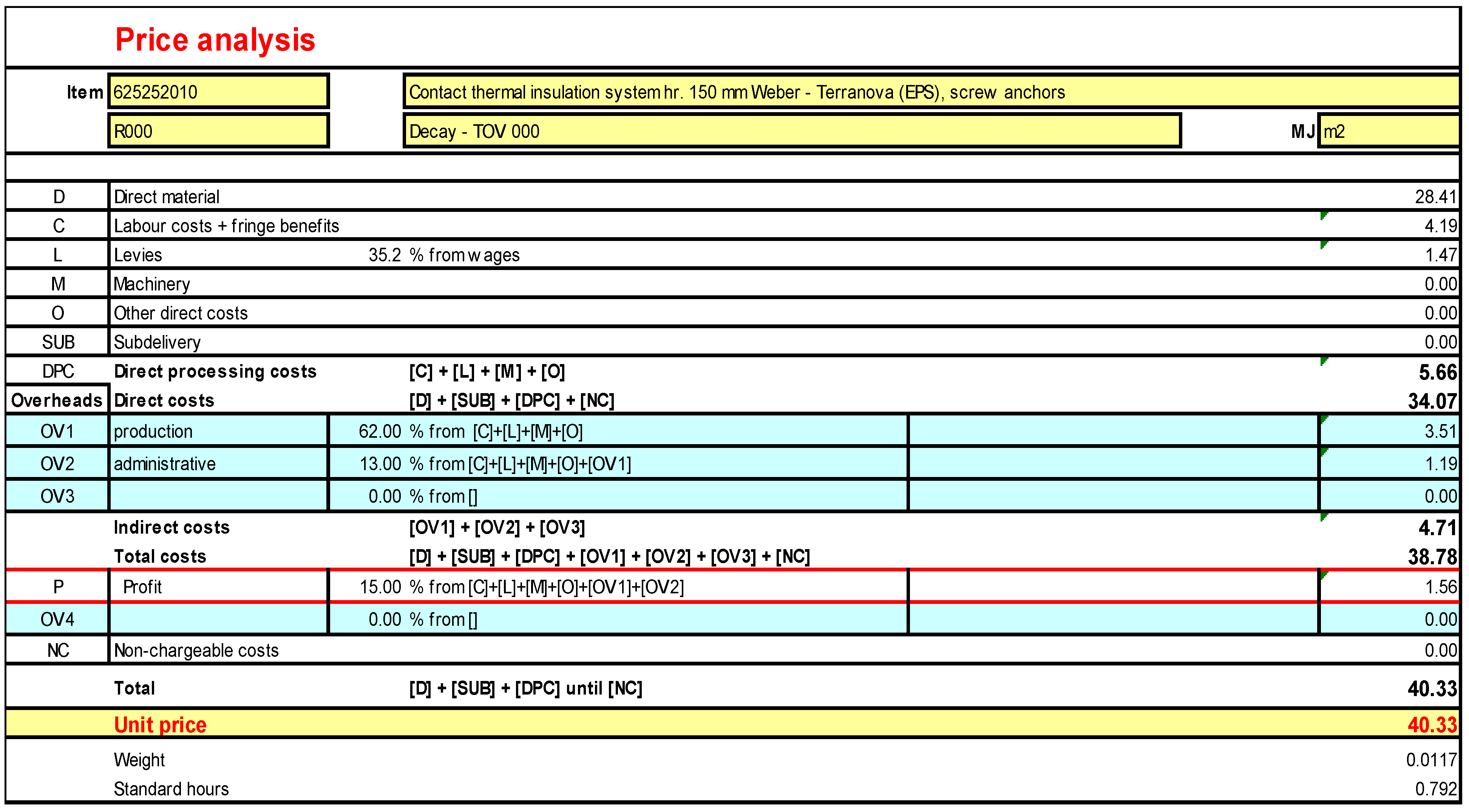

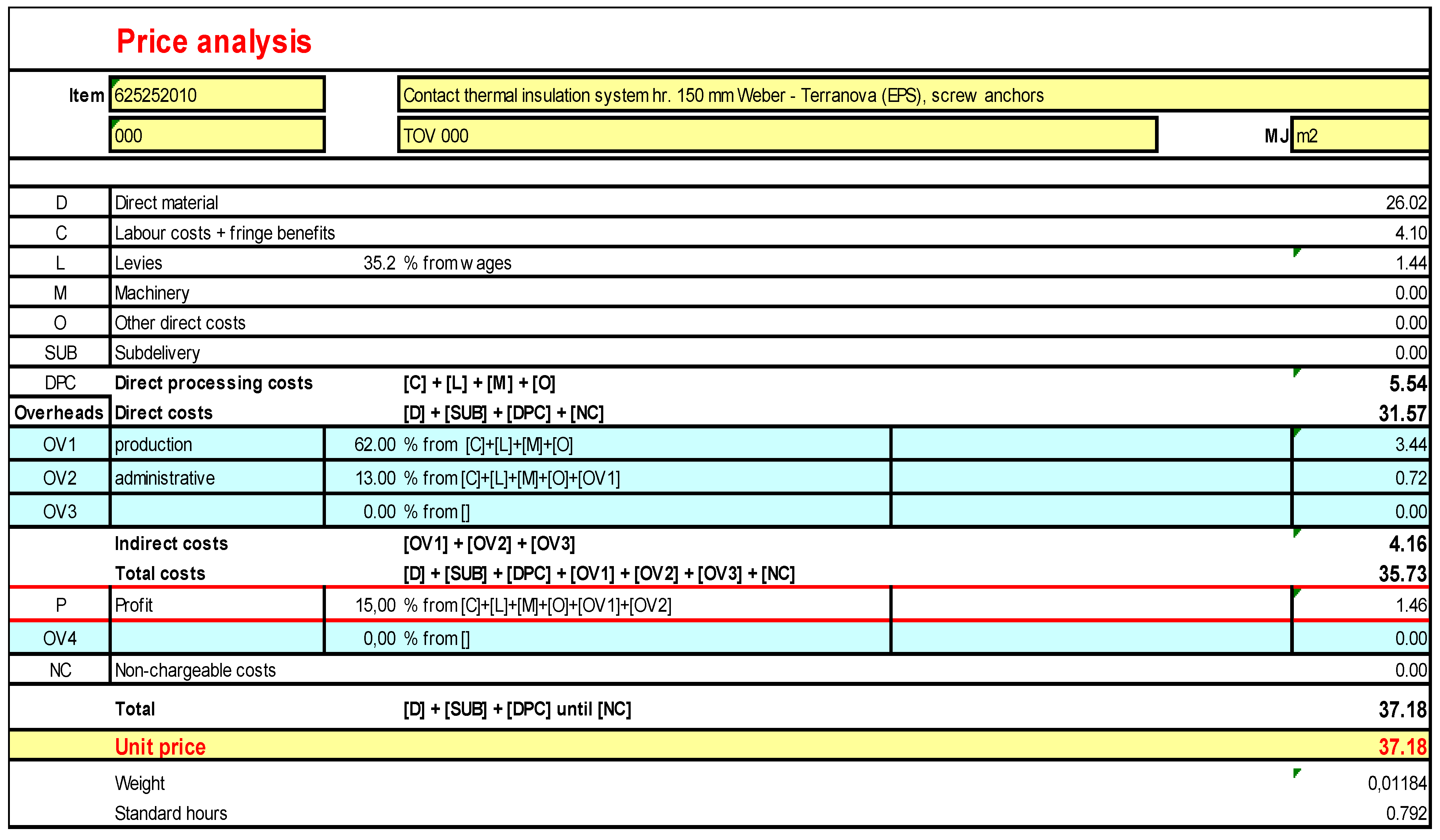

2.3. Model Example

2.3.1. Calculation of Lost Profits Using the Comparison Method

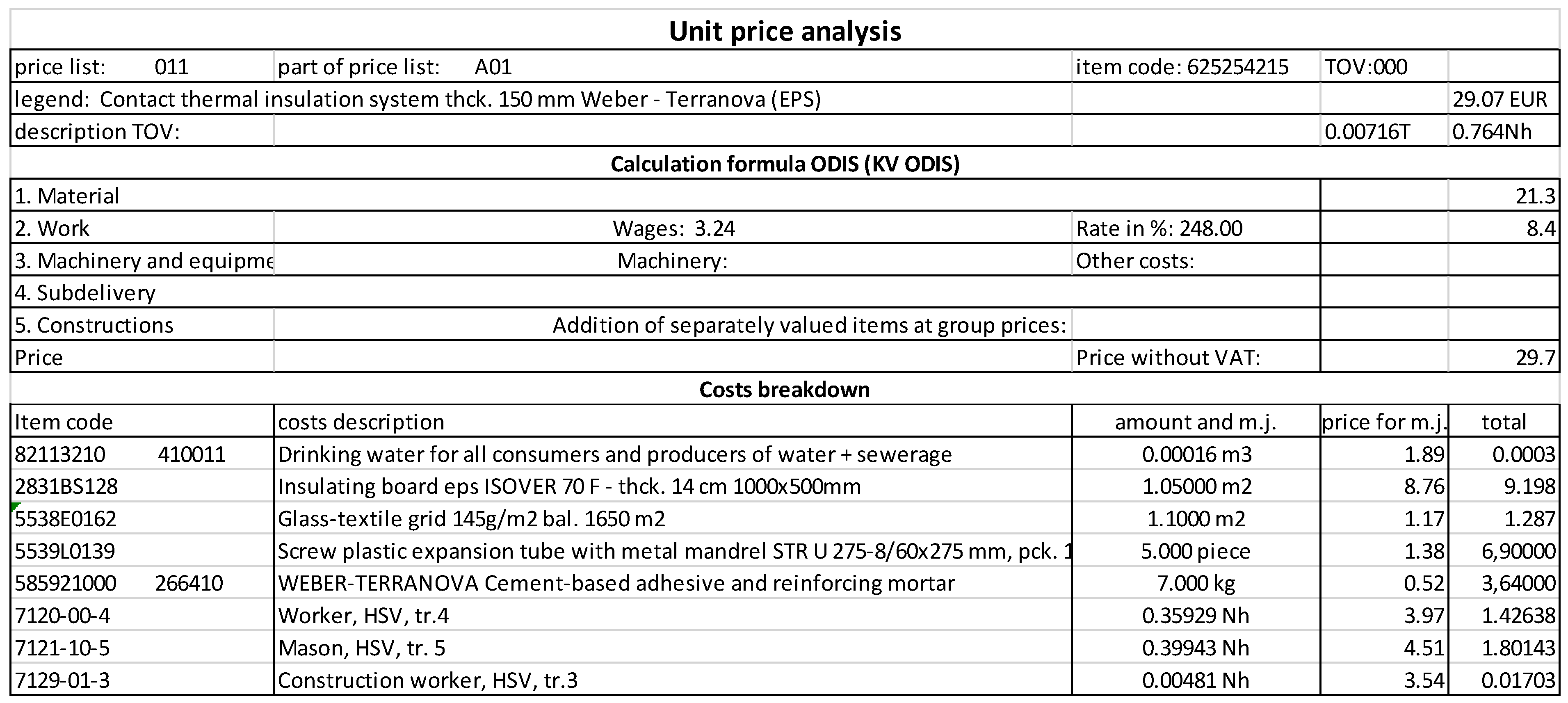

2.3.2. Calculation of Lost Profit Using the Valuation Tools Method (Cenkros 4)

- At the given price level (in the program, in the database II.Q/2017) we prepared a budget of unfinished construction work on the construction.

- From the budget, we found a calculated price of unfinished work of €32,280.

- We used the function “display of calculation structure” in the program, shown in Figure 8. From this graph, we can determine the amount of contract profit calculated by the software Cenkros

- Using the used calculation formula in the calculation structure of the cost and profit 10.25% of the residual price of work in progress, amounting to EUR 3309.

3. Results

4. Discussion

- The Before and After Method using the contractor’s accounting documents to estimate the approximate percentage of profits. Due to the simplicity of calculation, this method is one of the most widely used abroad. However, it requires increased demands on the evidence of the economy divided into a specific construction contract.

- The Comparison Method (Yardstick) uses a comparative analysis to calculate the loss of profit, the principle of which is in comparison with the profitability of comparable companies.

- Method of using valuation tools calculates the lost profits by using valuation tools. Software Cenkros 4, ODIS Žilina or Calkulus.

5. Conclusions

- it is a criterion for deciding on the economy of a company;

- it is a tool for accumulating and creating funds for the development of the company;

- it is the basis of redistribution between the business and the state;

- it motivates every entrepreneur.

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Arditi, D.; Koksal, A.; Kale, S. Business failures in the construction industry. Eng. Constr. Arch. Manag. 2000, 7, 120–132. [Google Scholar] [CrossRef]

- Russell, J.S. Contractor Failure: Analysis. J. Perform. Constr. Facil. 1991, 5, 163–180. [Google Scholar] [CrossRef]

- Harmon, K.M.J. Conflicts between Owner and Contractors: Proposed Intervention Process. J. Manag. Eng. 2003, 19, 121–125. [Google Scholar] [CrossRef]

- Arditi, D.; Pattanakitchamroon, T. Analysis Methods in Time-Based Claims. J. Constr. Eng. Manag. 2008, 134, 242–252. [Google Scholar] [CrossRef]

- Alavipour, S.M.R.; Arditi, D. Optimizing Financing Cost in Construction Projects with Fixed Project Duration. J. Constr. Eng. Manag. 2018, 144, 04018012. [Google Scholar] [CrossRef]

- Głodziński, E. Efektywność Ekonomiczna–Dylematy Definiowania i Pomiaru; Zeszyty Naukowe Politechniki Śląskiej; Organizacja i zarządzanie Nr kol. 1919; Instytut Organizacji Systemów Produkcyjnych: Warsaw, Poland, 2014. [Google Scholar]

- Statistical Office of the Slovak Republic. 2019. Available online: https://slovak.statistics.sk (accessed on 12 September 2019).

- Ellingerová, H.; Ďubek, S. Rozpočtové náklady stavebného diela Budget Costs of the Construction work. Časopis znalostí společnosti (Journal of Knowledge society) 2017, 5, 12–21. [Google Scholar]

- Ďubek, S.; Ďubek, M. The Unpredictable Costs Part of Construction. Czech J. Civ. Eng. 2016, 2, 42–47. [Google Scholar]

- Mečiar, A.; Petro, M. Analýza nákladov na vykurovanie bytového domu panelovej sústavy BA-NKS v závislosti od hrúbky použitej tepelnej izolácie obvodového plášťa. Alm. Znalca 2015, 3, 3–5. [Google Scholar]

- Korytárová, J.; Pospíšilová, B. Evaluation of Investment Risks in CBA with Monte Carlo Method. Acta Univ. Agric. et Silvic. Mendel. Brun. 2015, 63, 245–251. Available online: https://10.11118/actaun201563010245 (accessed on 13 August 2019). [CrossRef] [Green Version]

- Hanák, T. Electronic Reverse Auctions in Public Sector Construction Procurement: Case Study of Czech Buyers and Suppliers. TEM J. Technol. Educ. Manag. Inform. 2018, 41–52. [Google Scholar] [CrossRef]

- Action, n. 513/1991 Zb.Obchodný zákonník. 1991. Section 3, § 379. Available online: http://www.zakonypreludi.sk/zz/1991-513 (accessed on 8 July 2019).

- Supreme Court. file no. 4 Cdo 319/2008, of 28 April 2010. 2010. Available online: https://otvorenesudy.sk›decrees›document (accessed on 22 August 2019).

- Idrus, A.; Nuruddin, M.F.; Rohman, M.A. Development of project cost contingency estimation model using risk analysis and fuzzy expert system. Expert Syst. Appl. 2011, 38, 1501–1508. [Google Scholar] [CrossRef]

- PMI (Project Management Institute). Practice Standard for Project Risk Management; Project Management Institute, Inc.: Newtown Square, PA, USA, 2009. [Google Scholar]

- Harper, C.M.; Molenaar, K.R.; Anderson, S.D.; Schexnayder, C. Synthesis of Performance Measures for Highway Cost Estimating. J. Manag. Eng. 2014, 30, 04014005. [Google Scholar] [CrossRef]

- Mak, S.; Picken, D.; Picken, S. Using Risk Analysis to Determine Construction Project Contingencies. J. Constr. Eng. Manag. 2000, 126, 130–136. [Google Scholar] [CrossRef]

- Gunhan, S.; Arditi, D. Budgeting Owner’s Construction Contingency. J. Constr. Eng. Manag. 2007, 133, 492–497. [Google Scholar] [CrossRef]

- Thal, A.E.; Cook, J.J.; White, E.D. Estimation of Cost Contingency for Air Force Construction Projects. J. Constr. Eng. Manag. 2010, 136, 1181–1188. [Google Scholar] [CrossRef]

- Khamooshi, H.; Cioffi, D.F. Program Risk Contingency Budget Planning. IEEE Trans. Eng. Manag. 2009, 56, 171–179. [Google Scholar] [CrossRef]

- Sonmez, R.; Ergin, A.; Birgonul, M.T. Quantitative methodology for determination of cost contingency in international projects. J. Manag. Eng. 2007, 23, 35–39. Available online: http://worldcat.org/issn/0742597X (accessed on 13 August 2019). [CrossRef]

- Benarroche, A. Claims for Lost Profits Are Difficult to Prove | Construction Claims, Levelset 30.4. 2019. Available online: https://www.levelset.com/blog/lost-profits/ (accessed on 17 August 2019).

- Apanavičienė, R.; Daugėlienė, A. New classification of construction companies: Overhead costs aspect / Naujas statybos įmoni ųklasifikavimas: Pridėtinių išlaidų aspektas. J. Civ. Eng. Manag. 2011, 17, 457–466. [Google Scholar] [CrossRef]

- Ďubek, S.; Jankovichová, E.; Ellingerová, H.; Piatka, J. Usage Analysis of the Information Systems for Valuation of the Construction Output. Proceedings of the 3rd International Conference on Engineering Sciences and Technologies (ESaT) 2018. [CrossRef]

- Software Cenkros 4. 2019. Company KROS a.s., Database II.Q 2017. Available online: https://www.kros.sk/cenkros/podpora/archiv-verzii-53929 (accessed on 1 August 2019).

- TREND Analyses, Zisky Stavebných Firiem. 2017. Available online: https://www.etrend.sk/clanky-autora/3-trend-analyses.html (accessed on 21 July 2017).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Company | Sales 2017 (Thousand Eur) | Profit After Tax 2017 (Thousand Eur) | Profit (%) |

|---|---|---|---|

| Strabag Pozemné a inžinierske staviteľstvo, s.r.o., Bratislava | 396,430 | 6,771 | 1.7080% |

| Doprastav, a.s., Bratislava | 290,979 | 29,355 | 10.0884% |

| Strabag s.r.o. Bratislava | 185,696 | 11,615 | 6.2548% |

| Eurovia SK, a.s. Košice | 167,522 | 112,317 | 67.0461% |

| Skanska SK, a.s. Bratislava | 111,425 | 595 | 0.5340% |

| Goldbeck, s.r.o. Bratislava | 103,126 | 6526 | 6.3282% |

| VUJE, a.s. Trnava | 90,038 | 5855 | 6.5028% |

| Váhostav-SK, a.s., Bratislava | 82,729 | 150 | 0.1813% |

| TSS Grade, a.s., Bratislava | 76,559 | 1470 | 1.9201% |

| Inžinierske stavby, a.s., Košice | 63,465 | 5827 | 9.1814% |

| DSC, a.s., Bratislava | 61,261 | 7336 | 11.9750% |

| Cesty Nitra, a.s., Nitra | 60,325 | 2981 | 4.9416% |

| Chemkostav, a.s., Michalovce | 59,306 | 737 | 1.2427% |

| HB Reavis Managment, s.r.o., Bratislava | 58,294 | −7395 | −12.6857% |

| Ingsteel, s.r.o., Bratislava | 57,083 | 675 | 1.1825% |

| AVERAGE PROFIT | 1,864,238 | 184,815 | 9.9137% |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Majer, R.; Ellingerová, H.; Gašparík, J. Methods for the Calculation of the Lost Profit in Construction Contracts. Buildings 2020, 10, 74. https://doi.org/10.3390/buildings10040074

Majer R, Ellingerová H, Gašparík J. Methods for the Calculation of the Lost Profit in Construction Contracts. Buildings. 2020; 10(4):74. https://doi.org/10.3390/buildings10040074

Chicago/Turabian StyleMajer, Radovan, Helena Ellingerová, and Jozef Gašparík. 2020. "Methods for the Calculation of the Lost Profit in Construction Contracts" Buildings 10, no. 4: 74. https://doi.org/10.3390/buildings10040074