3.2.1. E-Mobility

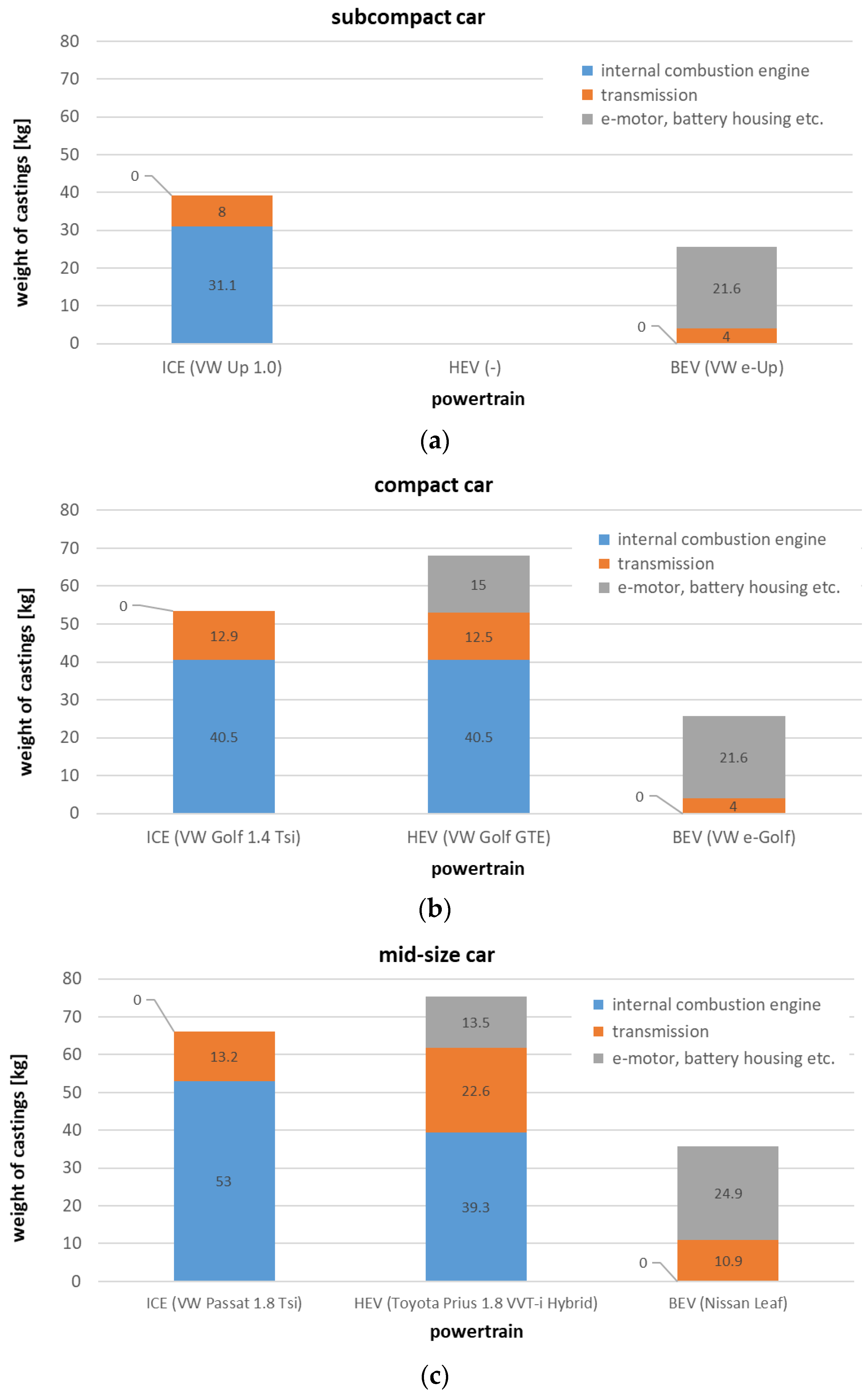

Currently, all signs indicate that for automotive applications, the internal combustion engine (ICE) has passed its prime. While it may not be obvious at first sight, this development does have consequences for the casting industry: the reader may just take a minute to consider how many parts of an ICE powertrain are actually cast, and how their number and cumulated weight compare to the corresponding figure for an electric power train. In two recent publications looking specifically at the impact on the German casting industry, Wilhelm et al. have gathered the respective data for small, compact and medium-sized cars, comparing ICE, hybrid (HEV) and battery electric vehicles (BEV) [

35,

36]. The respective data are summarized in

Figure 6 below for subcompact, compact and mid-size cars, also indicating, beyond the total weight of powertrain castings, the subsystem they belong to (engine, transmission, etc.).

Not surprisingly, the comparison shows that hybrid cars combining two propulsion systems lead to an increase in cast weight. However, since these may merely represent a transitory solution, the focus should remain on the truly significant contrast between ICE and BEV: Depending on vehicle size class, reductions between 35 and 52% on a weight basis are observed. Even though the study is certainly not fully representative, as it focusses on just one individual model per size class and powertrain variant, the tendency is clear and cannot be denied. In effect, this puts significant pressure on the casting industry and, specifically, on aluminum foundries, which heavily depend on the automotive industry—a pressure to which short- to mid-term factors such as the COVID-19 pandemic itself as well as its secondary consequences such as chip shortage and supply chain disruptions still add. Needless to say, the casting industry is responding to the E-mobility challenge. This is particularly evident in the case of a strong move towards structural castings, as these may provide compensation for the loss of production volume in powertrain components. Tesla has once again taken a lead by introducing the Gigacasting concept, but the trend as such is not limited to this manufacturer and will be discussed in more detail in the following

Section 3.2.2. Beyond this move to alternative products, aluminum foundries direct their attention to special requirements of components unique to the electric powertrain. On the one hand, this concerns housings for electric motors, power electronics and battery packs. On the other hand, it refers to applications where functional properties are at least as important as structural ones and where castability becomes an issue: rotor castings, for example.

Housings for electric powertrain components—Common to the aforementioned housings in an electrical powertrain is the need for thermal management. The standard way of solving this issue is liquid cooling. This implies a need for cooling channels or water jackets integrated in the castings. Several solutions have been suggested in this respect—their advantages and disadvantages strongly depend on the application scenario, and naturally also on the component in question. Take an electric motor housing as an example [

37]: The straightforward way of realizing a water jacket here is a two-part design. Solutions range from a combination of two HPDC parts joined either by welding or via bolted joints (see, e.g., the Volkswagen E-Golf design) to casting and extrusion or sheet metal structure as in some Tesla models. In as far as two castings are concerned, by definition, this approach affords two complex HPDC tools. These are needed because of a lack of established, commercially available solutions for complex cores which can reliably sustain the loads exerted during the HPDC process ([Mic10], see the section on complexity in the upcoming second part of this study). A potential further drawback is the need for machining of sealing and joining surfaces. This partly applies to combinations of an inner casting with an outer sheet metal or extrusion, too, which however relinquishes the need for a second mold.

Since the use of cores proves difficult in HPDC, the embedding of hollow structures such as tubes has emerged as an alternative. The integration of steel tubes, e.g., as hydraulic lines in HPDC gearboxes is well-established (see, for example, ZF’s 8HP eight speed transmission housing [

38,

39]) and profits from the higher thermal stability and strength of the material. However, from a thermal point of view, the integration of aluminum tubes offering higher thermal conductivity and eliminating the mismatch in coefficients of thermal expansion (CTE) between fluid channel and casting would seem attractive. It has been shown, though, that embedded aluminum tubes reach temperatures in excess of 500 °C during casting, at which the remaining yield strength falls well below 20 MPa, leading to collapse and/or infiltration unless the tubes are supported by some means [

40]. Stabilizing fillers removed after casting can solve this problem. A well-known concept in this respect is the Combicore process, in the course of which an aluminum tube is filled with salt, then drawn to compact the filler, after which step bending or further forming operations, e.g., to realize local changes of the cross sectional shape, can be implemented. Tubes are available in a wide range of diameters and wall thickness and have been demonstrated to withstand pressure levels in excess of 1200 bar in HPDC [

41,

42]. A related concept employing a two-component system based on an outer salt layer and a sand core has recently been patented by MH Technologies [

43]. Here, permeability of the core eases filler removal, while stability has been demonstrated to match the Combicore approach [

44]. An advantage of any concept based on integrated tubes is that leakage does not depend solely on the soundness of the casting anymore—hence, e.g., the term ZLeak Tube

® (i.e., zero leak) adopted by MH Technologies for marketing their product (see

Figure 7). Instead of stabilization via temporary fillers, internal structuring, which may further improve heat transfer, can be applied. Beyond the use of extrusions, the flexibility of metal additive manufacturing processes allows for the respective structures to be optimized in terms of stability, thermal transfer and flow resistance [

40]: Currently, the realization of such highly performant solutions is blocked by cost issues, but the potential of the approach is undisputed (see the section on complexity in the second part of this study as well as

Section 3.2.3 below).

If HPDC is not mandatory and LPDC, sand casting or related processes can be employed, e.g., for smaller production rates, complex cores become an option. Examples of this kind have been demonstrated, e.g., by NEMAK [

45] or Volkswagen in its ID.4. Among these, the Volkswagen solution is of specific interest, as it combines three castings: two lids produced via HPDC and a shell made by LPDC. The geometry of the latter is such that in future variants, replacement with an extrusion might be considered. If this could in fact be realized, it would allow for comparatively simple scaling of motor sizes by increasing or decreasing the length of the extrusion and, accordingly, the rotor and stator dimensions. A further alternative to LPDC is low-pressure sand casting, as suggested by Jin et al., who employ hot and cold box sand cores to realize the water jacket [

46].

Transfer of the various techniques to housings for other components such as batteries or power electronics is possible, though for reasons of geometrical complexity, electric motor housings tend to be the greater challenge.

Common to all methods that rely on integrating a secondary structure in a casting instead of using a core is the problem of achieving optimal heat transfer across the added interface: gap formation between a casting and an insert is a common effect with detrimental consequences for cooling performance, as are intermetallic phases with disadvantageous thermal characteristics, e.g., in the Al-Cu system [

47,

48,

49]. Compound casting research attempts to alleviate these effect, e.g., via surface coating or microstructuring (see the second part of this study).

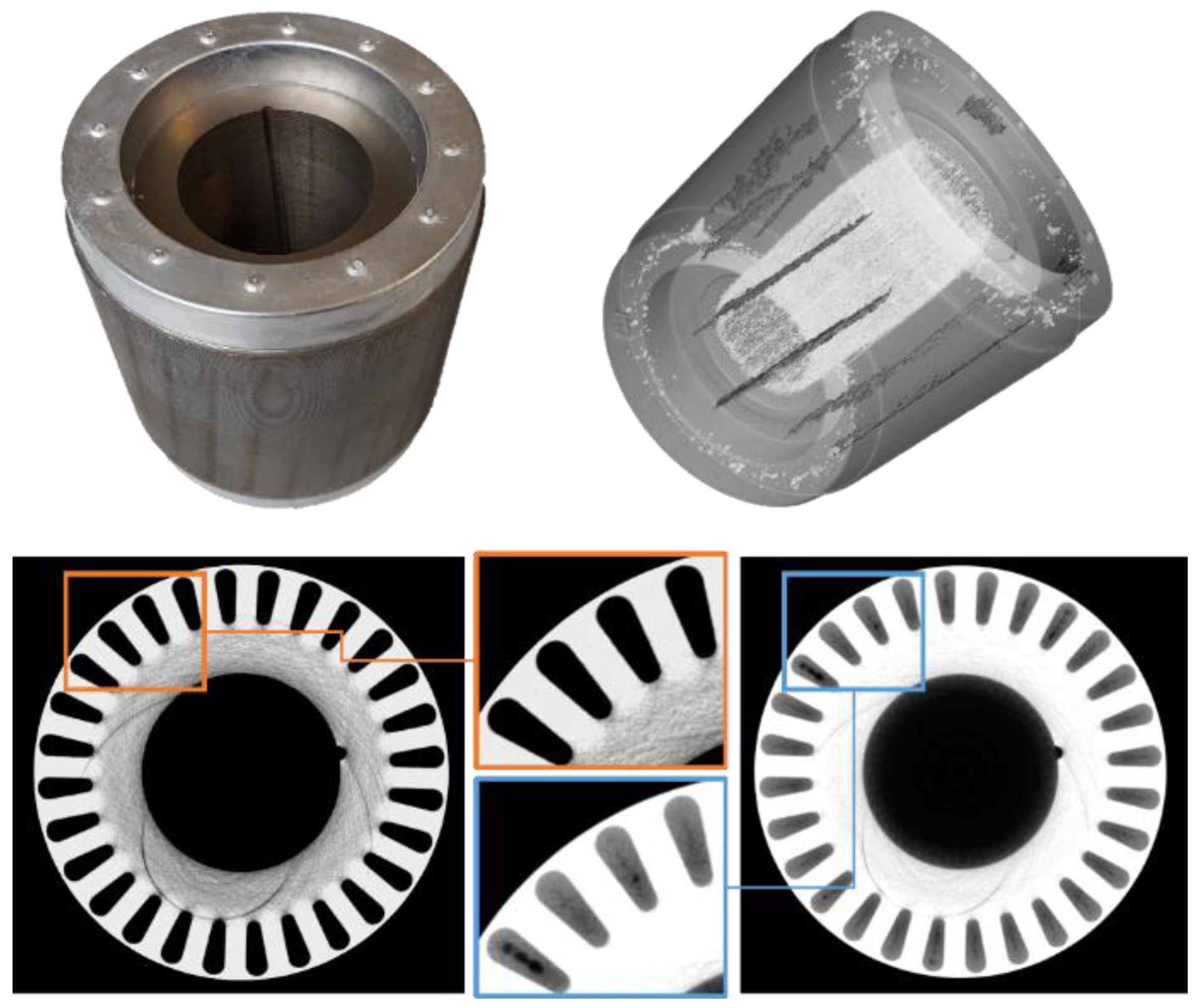

Rotor castings—Casting the short-circuit rings of an asynchronous electric motor’s rotor and the longitudinally connecting conductor bars between them is a challenge for two reasons at least: For one thing, what is required here is an alloy optimized not for its casting characteristics but for electrical conductivity. As the latter typically affords almost pure aluminum, the former is usually compromised. The issue is further complicated by the geometry of the casting, which almost inevitably leads to high levels of shrinkage porosity in the conductor bars, as these naturally solidify after the short circuit rings, making sufficient feeding almost impossible while potentially causing additional issues such as cold runs or flow front oxide layers hidden within the lamination stack [

50]. The former effect is further stressed by the fact that highly conductive and thus low alloyed materials exhibit excessive levels of shrinkage compared to conventional casting alloys. Yun et al. report up to 7% of shrinkage and typical fill factors of aluminum die cast rotors between 85 and 98% [

51]. To add to this, visualizing the porosity by X-ray computed tomography (CT) is rendered difficult by the extreme contrast in atomic number between steel and aluminum—however, advanced CT devices and reconstruction methods have recently been demonstrated to be capable of solving this problem ([

50], see

Figure 8 below). Against this background, alternative quality control approaches have been suggested, such as longitudinal X-ray scans along the axis of the bars [

51] or methods based on electromagnetic flux injection [

52]. An overview of such electromagnetic approaches is part of a study by Lee et al. [

53].

Porosity within rotor castings has both mechanical and electromagnetic effects. Mechanically, the stochastic distribution of porosity will cause mass-related unbalance, which needs to be compensated. Electromagnetic consequences include inhomogeneous current distributions in the conductor bars, resulting in distortions of electromagnetic fields, inhomogeneity of electromagnetic forces acting on the rotor and once more uneven rotation [

50]. Moreover, the direct impact of porosity and other casting defects on conductivity will reduce the efficiency of the device. Several studies have scrutinized such effects, concluding, e.g., that increasing fill factors from 67 to 100% corresponds to efficiencies ranging from approximately 90 to slightly above 92%. Even more significant is the thermal effect though, as conductor bar temperatures drop from 117 to 81 °C and stator winding temperatures drop from 97 to 81 °C in parallel [

51]: As the amount of thermal energy to be extracted drops, the dimensioning of the cooling system and potentially even the cooling method itself can be reconsidered, offering secondary weight savings.

With many problems unsolved, aluminum rotor casting remains a playing field for process and alloy development. Specifically in terms of alloys, combining conductivity near the limit of pure aluminum (235 W/(mK)) with sufficient strength and castability is an objective addressed via alloy design or process adjustment, including heat treatment. Examples of the alloy systems studied are summarized in

Table 3. In many publications, the focus is on replacing the Al-Si with the Al-Fe or Al-Ni eutectic system, plus variations on this theme. An advantage of these systems is the high volume percentage of eutectic at low Fe or Ni additions plus the low solubility of both elements in the α-Al phase, which guarantees a high purity and thus highly conductive primary phase. A further mechanism to improve conductivity is controlled precipitation of detrimental elements such as Cr, V, Zr and Ti, e.g., as borides [

54,

55]. A detailed discussion of the various alloy systems and the microstructural background of their specific properties has been put together by Kotiadis et al. [

56]. Kim et al. studied the influence of individual elementary additions of Si, Cu, Mg, Fe and Mn at levels between 0.2 and 2.0 wt.% on thermal conductivity of pure aluminum in search of high-conductivity HPDC alloys and developed more complex compositions from these initial experiments, which were also tested in terms of their fluidity [

57]. A more recent investigation by Abdo et al. covers combinations of Cu with the additional alloying elements Mg and Ag, including the combination of all three [

58].

Table 3.

Exemplary aluminum alloy systems and alloys compared in terms of their thermal conductivity and strength.

| Alloy System Al- | Composition Al- [wt.%] | Thermal Cond. [W/mK] | Electr. Cond. 1 [%IACS] | UTS [MPa] | YS [MPa] | Elongation at Failure [%] | Ref. |

|---|

| pure Al | Al99.8 | 225.3 | - | 58 | - | 24.8 | [57] |

| | Al100 3 | 251 2 | 60.53 | 73 | 65.79 | - | [58] |

| Cu | 2Cu 3 | 237 2 | 57.16 | 150 | 95.48 | - | [58] |

| Cu-Ag | 2Cu-0.5Ag 3 | 230 2 | 55.42 | 183 | 113.53 | - | [58] |

| Cu-Mg | 2Cu-0.5Mg 3 | 214 2 | 51.68 | 260 | 232.64 | - | [58] |

| Cu-Mg-Ag | 2Cu-0.5Ag-0.5Mg 3 | 222 2 | 53.54 | 294 | 216.28 | - | [58] |

| Fe-Ni | 0.52Fe-0.53Ni | 241 2 | 58 | 88.7 | 37.7 | 23.2 | [59] |

| | 0.52Fe-1.03Ni | 228 2 | 55 | 89 | 42 | 14 | [59] |

| | 0.34Fe-1.55Ni | 224 2 | 54 | 93.2 | 45 | 13 | [59] |

| | 0.34Fe-2.06Ni | 220 2 | 53 | 102 | 46 | 10 | [59] |

| Si-Fe | 1Si-0.6Fe | 198.0 | - | 129 | - | 21 | [57] |

| | 1.96Si-0.62Fe | 185.7 | - | 131 | - | 18.4 | [57] |

| Si-Fe-Cu | 0.98Si-0.39Fe-1.12Cu | 181.6 | - | 152 | - | 18.7 | [57] |

| | 1.48Si-0.62Fe-0.59Cu | 172.7 | - | 151 | - | 19.9 | [57] |

| | 1.68Si-0.39Fe-0.24Cu | 185.7 | - | 128 | - | 21 | [57] |

| Si-Fe-Cu-Mg-Mn | 10.58Si-0.72Fe-2.03Cu-0.30Mg-0.13Mn | 117.6 | - | 228 | - | 2.3 | [57] |

Composition is not all, though: Li et al. have shown that extended heat treatment at 520 °C can be employed to boost thermal conductivity from 152 to 171 W/(mK) in common Al-7Si type casting alloys based on fragmentation, spheroidization and coarsening of the eutectic silicon [

60]. Similarly, the homogeneous distribution of smaller size precipitates and generally finer grain structures expressed, e.g., in secondary dendrite arm spacing (SDAS), have been reported to improve electrical and thermal conductivity [

61,

62,

63]. In terms of primary rather than secondary processes, a reduction in porosity can be achieved by limiting solidification shrinkage. Semi-solid processes offer just this, plus the advantage of laminar flow during mold filling, reducing a second source of porosity, entrapped gas. Rheocasting and other semi-solid techniques will be discussed in more detail in part two of this paper.

3.2.2. Automotive Structural Castings

As mentioned above, the E-mobility challenge has led to an increasing interest in structural castings. Tesla has strongly adopted this approach by producing front and rear bodies as single castings [

64,

65], labelling their technique Gigacasting, but in fact, the trend is both older and broader than that, as shall be shown further below. Nevertheless, as in the case of E-mobility in general, Tesla has opened the doors for a re-evaluation and potential adoption of such techniques, where the final aim, as suggested by Tesla, may be the casting of the complete automotive body structure in a single shot: this, at least, is what Tesla suggests in a recent, though rejected, patent application [

66]. What Tesla does today, however, is a stepwise introduction of rear and front underbodies of their Model 3 and Model Y as a single casting, replacing an assembly of altogether 70+ sheet metal parts and shortening manufacturing lines by, according to Musk, 300 robots each otherwise needed for assembly [

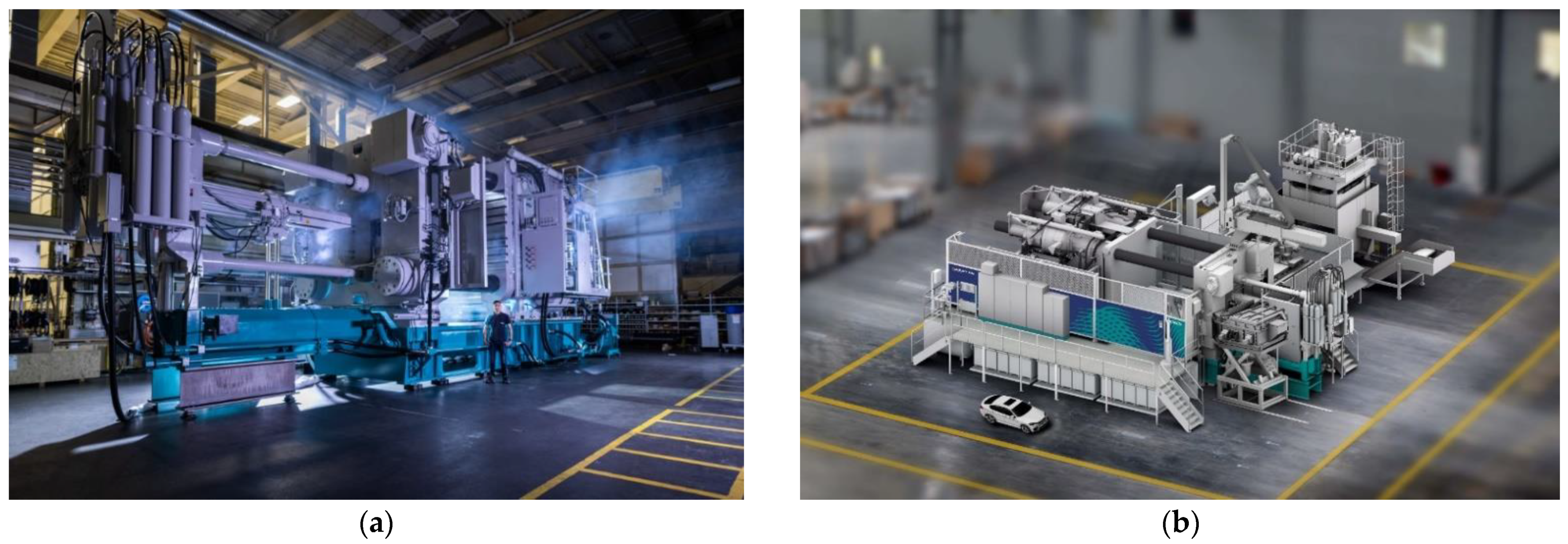

65]. A prerequisite of this technique is the introduction of HPDC machines of hitherto unknown dimensions. Within recent years, locking forces had largely been limited to roughly 4500 tons. When IDRA and their mother company LK Machinery offered machines that were capable of up to 6000 tons, the technological background for realizing Tesla’s single piece rear and front casting was there. Meanwhile, several other manufacturers of HPDC equipment have updated their product portfolios to include machines of similar or even larger sizes, including, e.g., Italpresse Gauss and Bühler. The current leader by size is Bühler, offering the Carat 840, which is rated at 84,000 kN locking force (see

Figure 9), while the company website, introducing the Carat 920, claims the locking force range of their machines only ends at 92,000 kN by now [

67]. However, rumors had been around earlier that either Tesla or one of its suppliers is acquiring machines offering at least 8000 tons [

65], and these seem to have materialized given the information that IDRA has shipped their first 9000 ton machine to Texas for use in Tesla’s Cybertruck production [

68]. Such messages, however, may be short-lived these days, as Volvo announces its own Mega-Casting approach [

69], Volkswagen apparently considers the same for its new Wolfsburg plant [

70] and LK Machinery promotes the development of a 12,000 t machine [

71]. The latter is being built for local customers, namely Hongtu Technology Co. Ltd., who already own a 6800 ton machine [

71], highlighting the fact that many Chinese (relative) newcomers in the automotive sector such as Nio, HiPhi and Xiaopeng seem willing to take up Gigacasting [

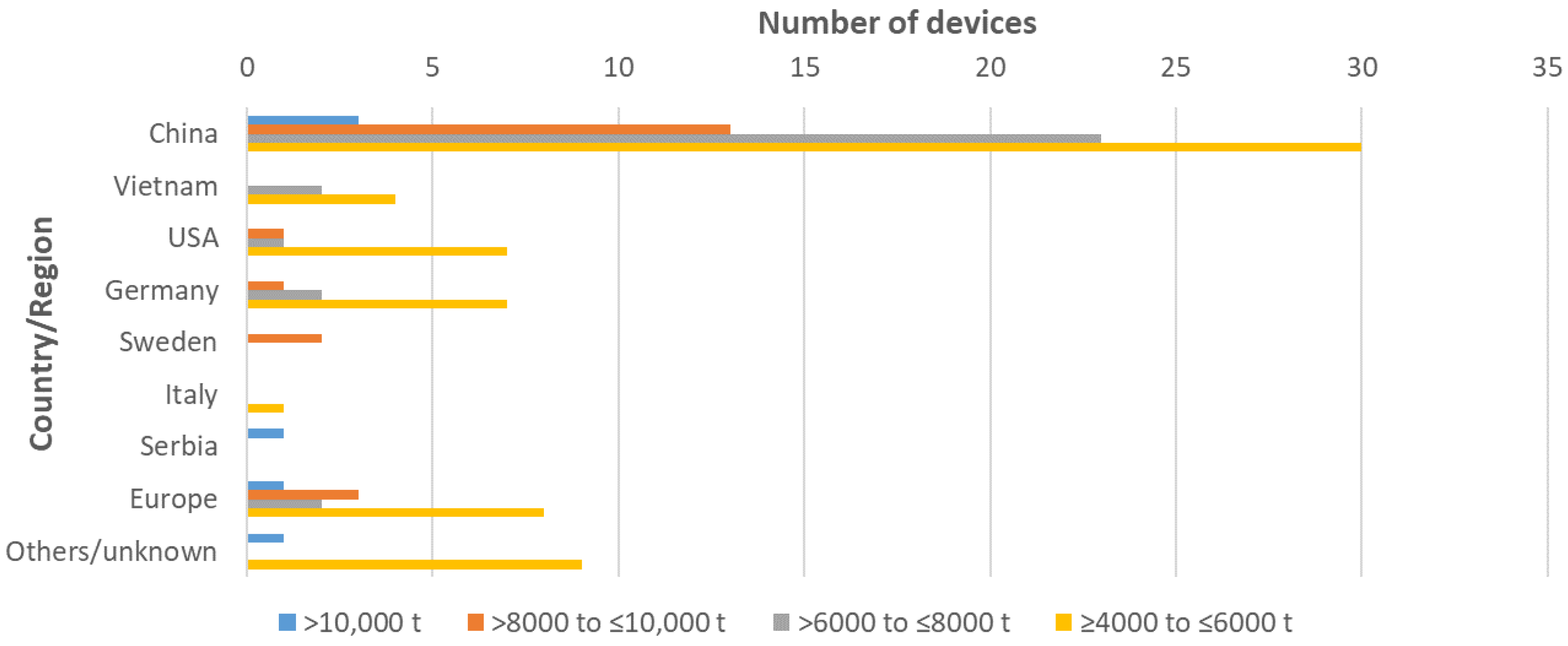

72]. This supports the observation that for obvious reasons (large investment costs and partial replacement of conventional assembly lines), Gigacasting generally lends itself more easily to greenfield rather than brownfield approaches and, thus, favors stakeholders in need of building up production from scratch, anyway. It is thus not surprising that an overview of recent installations of HPDC machines in the locking force range of 4000 tons and above offered by Gärtner and Zhou underlines that China clearly leads this trend (see

Figure 10 below). At the same time, new producers of HPDC equipment of this size are emerging in China besides the trendsetter LK/IDRA, including, e.g., Haitian, Yizumi and Lanson [

73]. An interesting side aspect is that while most of the equipment is in fact installed to supply the automotive industry with front or rear body structures as well as battery housings, 5G applications are emerging as a secondary market, e.g., in Vietnam.

Needless to say, the prerequisites for an economically viable implementation of the Gigacasting approach are not limited to the engineering problem of sufficiently high locking forces and controlling a process anyway dubbed stochastic at this scale: producing HPDC castings of this size has several side effects.

The number of toolmakers capable of producing the required tools is limited. Handling and transport of tools becomes a problem when a complete die easily exceeds a weight of 100 or even 150 tons. Furthermore, primary and peripheral machinery as well as dies develop into a massive investment, which is further increased by the fact that casting of such large parts does not necessarily fit into the cycle time slots typical in the automotive industry. This basically means that a need for several large-size casting lines may arise. For decentralized production and just-in-time delivery, the transport of large parts in sufficient numbers also becomes critical, specifically if the parts are of complex shape, as in this case, volume instead of weight may become the limiting factor for road transport. Investment costs as well as the transportation issue mean that economic viability is critical unless a greenfield approach is chosen, and the associated new foundries are located side by side with the automotive production and assembly plants. Not surprisingly, this is exactly what Tesla does by building new factories around the world and equipping them from the start with Gigacasting facilities. Volkswagen currently appears to follow a similar path with the suggested Trinity plant in the vicinity of its Wolfsburg headquarters [

70]. All the above issues point towards difficulties in realizing dual sourcing strategies: if the OEM, unlike Tesla, decides against taking production in its own hands, setting up more than one supplier for Gigacasting will face additional difficulties beyond technological ones as machines of 6000+ tons may remain scarce for quite some time and can likely not be installed in existing foundries. This said, the rapid take-up of the technology in China may cancel out this concern sooner than anticipated.

There are alternatives to Gigacasting, too, and they are justified: casting large components in one shot necessarily means that decisions on part geometry are not exclusively controlled by the loads that need to be borne by the final part but, to some degree, also by process requirements. This compromise between castability and strength may effectively mean that the weight optimum is missed by Gigacasting components. In any case, a large, single material component contradicts the lightweight design paradigm of putting each material in the place in which it is of optimal use for overall structural behavior. Furthermore, crashworthiness as well as repairability is an issue with cast structures. The original design of the Tesla Model Y rear body structure foresaw, among others, an extrusion screwed to a cast structure—the updated single-piece design realizes this section as part of the casting. Tesla has addressed crashworthiness issues in a recent patent, which describes geometrical adaptations meant to guarantee controlled collapse of such areas [

74]. However, these solutions inevitably add material to achieve what could have been achieved with an extrusion at less weight and most likely less scatter of properties. Thus, the question is whether it is possible to realize a “best of both worlds”-approach in which the advantages of Gigacasting, such as the reduction in component numbers and assembly operations, are consciously combined with property-based local selection of materials, cross-sectional geometries and dimensions while at the same time easing the casting process itself. What comes to mind in this respect are large-scale hybrid or compound casting approaches [

75,

76], which shall be discussed in Part II of this work. Furthermore, from a still somewhat theoretical point of view, rheocasting (also treated in more detail in the upcoming second part of this paper) may profit in this context from its lower requirements in terms of intensification pressure, as due to this, parts of identical size can be produced on smaller machines compared to conventional HPDC [

77]. Typical advantages of rheocasting such as low porosity and increased flow length come in as added benefits. One challenge that remains, however, is the reproducible production of slurry for shot weights of 100 kg and more, which has not surprisingly never been demonstrated yet for any of the commercialized rheocasting processes; after all, it still is quite a bit of a novelty for HPDC, too.

This said, automotive structural castings is certainly more than Gigacasting. Roos et al. recently published a White Paper related to this product class, highlighting the fact that their use, though originally limited to luxury class vehicles, has since spread to the middle class: good indicators of this are cast shock towers as well as longitudinal beams. Components of this type were found in 5.9 million vehicles in 2018, with a 50% rise to 8.9 million units expected until 2025. As a driver for an even broader introduction of structural automotive castings, the study identified three conditions, highlighting and partly also quantifying the expected benefits based on realistic case studies [

78]:

Improved thermal management of molds:

- ○

Reduction in cycle times by roughly 33%;

- ○

Increase in die life by up to 50%;

Choice of alloys—use of systems providing strength without heat treatment:

- ○

Elimination of process steps, with direct cost reductions estimated at 10%;

- ○

Elimination of sources of distortion and residual stress;

- ○

Improvement in the overall energy balance;

Lightweight solutions via improved product design:

- ○

Shifting of process boundaries towards a minimum thickness below 2.5 mm;

- ○

Use of advanced optimization tools fully exploiting the capabilities of material and process.

While the study mentions the increasing number of electric vehicles, it does not yet incorporate the impact of new vehicle structural concepts such as Gigacasting facilitated by the switch in powertrain technology and may thus still underestimate the real potential. In any case, especially the first two issues stressed by Roos et al. are probably even more relevant in a Gigacasting context, the practical implementation of which already now relinquishes heat treatment. New structural alloys that fulfill the respective requirement are under development. State-of-the-art solutions include the systems Al-Mg-Fe as well as Al-Mg-Si-Mn-Zr, of which the first is used in as cast state (e.g., AlMg4Fe2), while the second just affords a T5 treatment (e.g., AlMg6Si2MnZr [

78]). A broad overview of structural aluminum casting alloys has recently been published by Sigworth and Donahue: their focus remains on heat treatable alloys, but the disadvantages of these are explained and alternatives are described with a focus on commercially available compositions [

79].

3.2.3. Opportunity or Threat: Additive Manufacturing as Competing Technology

At first sight, the answer to the question whether additive manufacturing (AM) is a danger or a benefit for the casting industry seems straight forward—this is the perspective of the final products, where AM appears to excel in realizing geometries accessible to casting either not at all or only with great effort, e.g., depending on the casting process, via extensive use of sliders, cores or core packages. Recently, the topic has been discussed by Kang et al., who come to the conclusion that AM of metal parts is no challenge to casting in most fields due to deficient properties of parts [

80]. As will be shown later, there are doubts that this opinion can indeed be fully substantiated—with respect to strength at least, the opposite appears to be true [

81]. However, competitiveness of AM is somewhat limited by cost issues: metal AM, which is what is to be considered in this context, is predominantly a powder-based process, and powder is expensive. The disparity in the price of a standard casting alloy of AlSi10Mg-type as an ingot on the one hand and as a powder suitable for AM on the other is currently somewhere in between one and two orders of magnitude. Assuming that in the long run, AM powder prices may reach parity with those for PM powders, the remaining difference will still be one order of magnitude. At the same time productivity of the dominant metal AM process Laser Beam Melting (LBM) falls desperately short of, say, high-pressure die casting, with production volume per unit time being measured in cm

3/hour [

82]. This said, there are for sure other processes that have received less attention until recently but promise higher productivity, such as binder jetting [

83,

84,

85] or arc-based AM processes [

86].

Table 4 provides a rough overview of typical production rates based on and extending data previously collected by Lehmhus and Busse [

87].

Productivity advantages of some processes come at a cost, though: while arc-based AM processes such as WAAM achieve the highest build-up rates, the parts they produce typically require surface machining. Binder jetting on the other hand achieves geometrical resolutions and surface qualities similar to LBM and is projected to deliver build rates of up to the level of dm

3/h just like WAAM. However, what it provides at this rate is a green part that needs further processing steps known from many other powder metallurgical (PM) processes, such as the removal of the binder printed into the powder bed during shape generation and the sintering of the part to full density [

85,

99]. This alternative process chain also implies that the parts produced do not benefit from the microstructural effect of the extremely high cooling rates (10

4–10

6 K/s) typical of the LBM process. Consequently, the properties of binder jetting parts roughly match those of conventional PM parts, whereas LBM specimens exceed both these as well as those of cast materials: for a standard alloy of type AlSi10Mg, UTS for HPDC is in a range of 250 to 290 MPa in as cast and 290 to 360 MPa in the T6 state—which is only achievable with extra effort in HPDC—(AlSi10MnMg Silafont

®-36 [

100]), while for LBM, values between 250 and 436 MPa have been reported for as-fabricated materials in a review by Hitzler et al. [

101], with Lehmhus et al. gathering data indicating a UTS maximum as high as 500.7 MPa [

102]. Chen et al. call up 455 MPa in contrast, also reporting 190 MPa for PM-AlSi10Mg originating from a hot extrusion process following spark plasma sintering of the extrusion billet [

103]. Among the best references may be a study by Roth et al. using partially automated, high-throughput testing to compare large numbers of cast and LBM-fabricated test samples. The results showed a 20% increase in strength for LBM, but advantages in terms of elongation at failure for cast materials: the casting process used was gravity die casting in this case [

81].

An interesting side aspect of the AM vs. casting dilemma has been studied by Bekker and Verlinden, who contrast the environmental impact of WAAM to green sand casting and machining of stainless steel parts via a cradle-to-gate LCA. The result is a slight advantage for WAAM compared to sand casting and parity with machining at a material utilization ratio of 0.75. For WAAM, the machining step typically required after build-up is not included in the calculation though. Since the difference between casting and AM is low, it may safely be assumed that the widespread LPBF process would fare worse than casting due to the added step of powder production—typically via melt atomization, which necessitates remelting of the material—and the lower energy efficiency of the laser process [

104].

In conclusion, as a direct part-production process, AM certainly remains a technology to watch, though currently only for smaller-scale production, where the increased complexity of many casting processes such as the need for tools for both parts and—if applicable—cores gains additional weight in cost calculations relative to the material costs. Currently, this niche for AM in direct competition with casting is small, but it is likely to grow with AM productivity increase and material cost decrease. The development of software tools capable of identifying the respective limits for a given part geometry would thus be a rewarding task to support both industries. In any case, from today’s point of view, there is no indication that AM will one day fully replace casting. At the same time, the undeniable advantages of additive manufacturing can benefit casting processes, too: here, 3D-printed sand molds and cores as well as permanent casting tools come to mind. These will be discussed in the second part of this work in the context of complexity of castings. As a teaser, an idea of the capabilities of the process is conveyed by

Figure 11 below.

Another possible combination of casting and AM is the integration, by means of compound casting processes, of inserts that profit from the extreme geometrical flexibility of the AM process and, thus, provide added functionality to the cast part. A good example of this is the integration of cooling channels in high-pressure die cast housings, an application already discussed in

Section 3.2.1 above: here, AM can provide solutions optimized for (a) heat transfer, (b) flow resistance and (c) maintaining structural integrity during casting. Investigations along these lines have recently been performed by Lehmhus et al. with the aim of eliminating the filler otherwise indispensable for HPDC integration of aluminum tubes [

40]. A prerequisite for successful design of such structures is a deeper understanding of the high-temperature performance of AM materials to facilitate the prediction of stability as a function of process parameters [

102]. Besides this application, smart castings can profit from the capability of AM processes to encapsulate sensors or, more generally, electronic systems and thus prepare them for casting integration—a topic to be treated in the second part of this study [

105,

106].

3.2.4. Environmental Issues

Certainly, a boundary condition that increasingly affects the casting industry in full are environmental concerns and requirements derived from them. Casting is not necessarily a green technology. In fact, it has been called a “3D industry” by some—dark, dirty and dangerous. The main aspects of its environmental impact include energy consumption, direct emissions and waste.

Needless to say, not all potential corrective measures can be discussed here. It is noteworthy, though sometimes overlooked, that a reduction in energy needs can be achieved through advanced, higher efficiency production technologies. The effect may be direct, in the sense that the respective, adapted process requires less energy in itself compared to previous implementations, or indirect, if secondary processes are positively affected or reject rates and, thus, emissions relative to product weight are reduced. There are several other examples of how technological change can improve the foundry industry’s environmental balance—to name but a few, arbitrarily selected ones:

Use of inorganic binders in sand casting and production of sand cores will reduce workplace emissions, improve indoor air quality and greatly reduce the amount of waste foundry sand for which landfill is the only available form of disposal [

107,

108];

Reclamation and reuse of foundry sand will directly save natural sand resources, and limit waste as well as emissions and energy consumption linked to transport of new and waste sand [

109], etc.;

Microspraying in high-pressure die casting leads to less waste and workplace emissions and can, through better thermal control, improve part quality, reducing reject rates;

Heat treatment and other furnaces nowadays fired with natural gas may be

- ○

Adapted to work with—preferably green—hydrogen, an option that gained additional interest in the course of rising gas prizes caused by the Russian attack on Ukraine;

- ○

Be replaced by electric systems facilitating the direct use of renewable energy sources without requiring an energetically inefficient power-to-gas bypass;

Advanced process monitoring and control approaches based, e.g., on Industry 4.0 paradigms may enhance product quality and reduce reject rates, or allow fine-tuning of processes towards optimal energy efficiency.

The above examples are snapshots, no more. They do, however, underline that for a thorough evaluation of potentials, holistic approaches accounting for the whole process chain are needed. Such studies by now exist for several casting processes:

Already in 2001, Stephens et al. have provided an in-depth life cycle assessment (LCA) of aluminum casting, covering lost foam, semi-permanent mold and precision sand casting. Their results indicate environmental advantages of the lost foam process, which came out similar to semi-permanent mold casting but performed better than precision sand casting by a wide margin. The analysis covered factors such as energy consumption, amount of solid and liquid waste produced, CO

2 emissions, etc. per 1000 kg of degated casting weight and identified electrical energy needs as well as aluminum production and melting as major aspects determining the outcome [

110].

Liu et al. extended the scope of processes to HPDC, vacuum high-pressure die casting and semi-solid casting processes. Their study defines a system boundary that excludes aluminum alloy production as well as the product life cycle and end-of-life aspects, focusing on the actual manufacturing process and including all aspects related to this, such as die manufacturing or secondary processes beyond casting such as heat treatment, machining and surface treatment. Interestingly, the authors found higher environmental costs associated with structural parts compared to typical housings or engine blocks and question the formers’ environmental viability on this basis despite acknowledging their contribution to lightweight design. Furthermore, the author stress the importance of the melting and holding step for overall energy consumption and the fact that increasing yield by whatever means may be a silver bullet in terms of saving energy. However, the latter effect does not explain why the vacuum and semi-solid processes are scoring well in this comparison—instead, energy consumption of the die casting machine and extended die life turn out to be major factors [

111].

A narrower focus on HPDC is provided by Cecchel et al. using an automotive suspension cross beam as basis of their study, which is performed in accordance with ISO 14040:2006 [

112] and extends the previous example by also incorporating primary material production starting from raw material extraction. Not surprisingly, Cecchel et al. conclude that primary aluminum production accounts for the largest part of energy consumption, while the casting process itself only affords—though still significant—18%, and end-of-life recovery of aluminum scrap can gain a 42% benefit. This stresses the environmental necessity of relying in as much as is possible on secondary aluminum: together with considering the energy mix used in production of primary material wherever the latter is required, this will significantly reduce both energy consumption and carbon footprint [

113]. Recent figures imply that the average CO

2 equivalent for 1 kg of primary aluminum of the common alloy AlSi10Mg produced in Europe amounts to 9.76 kg, while the respective value for secondary material is 1.95 kg [

114]. The downside, however, is that with increasing use of aluminum in the automotive industry and many recycling paths being industry-centered, like in the case of beverage cans, the amount of aluminum scrap available does not match the increasing demand. The problem is further blown up by the fact that many vehicles do not see the end of their lifecycle in the producing countries but in others and are thus not available for closed loop recycling [

115]. This situation may cause a greenwashing effect in the sense that companies highlight secondary aluminum-based products, which, in order to be able to reach this status, have to clandestinely cannibalize other products and deprive them of their share of recycled material.

In the course of recent developments such as the attempts at slowing down climate change, environmental aspects have received increasing attention, and the findings associated with this attention may soon be cast into rules that the foundry industry has to observe: currently, the “Smitheries and Foundries” best available technology (BAT) reference document (BREF), which in its present form dates from 2005 [

116], is being revised under the auspices of the European Integrated Pollution Prevention and Control Bureau (EIPPCB) according to the so-called Sevilla process, with an initial draft available since February this year [

117]. Once finished and adopted by the European Commission, this document will contribute to defining standards to be maintained by the European foundry industry, covering all aspects of casting and directly related processes. Publication of the final document and adoption of the rules it sets is expected to take place before 2025.

However, though the European Union’s contribution to global production of castings is certainly relevant (EU members contribute a share well in excess of 10%, see

Section 2), global impact would still be limited unless countries such as China, India and the USA, which together stand for almost 60% of annual production, would join the effort. This, however, is apparently the case: Li et al. have published a detailed survey on energy consumption and CO

2 reduction measures as early as 2010, looking also into supporting political measures and comparing the Chinese approach in this respect to those adopted in other parts of the world [

118], Zhang et al. have provided an updated perspective on the greening of the Chinese foundry industry [

119], and similar efforts are known from the US. Initiatives such as this blend in with the overall national CO

2 reduction targets as well as the United Sustainable Development Goals formulated by the United Nations in their 2030 Agenda for Sustainable Development [

120]. Nevertheless, it remains to be seen whether any stricter EU regulations may be exported to other regions of the world via European companies’ role as customer of other countries’ foundry industry: Since the European market share typically exceeds local production by a notable amount, European enterprises can be expected to continue sourcing castings from abroad. Needless to say, sustainability comes at a cost, and this cost can only be balanced by the benefit aspired to if implementing regulations does not simply result in a shift in production to places where they do not bind—more so since such delocalization creates further CO

2 emissions during transport. Meanwhile, besides direct regulatory approaches, indirect effects are beginning to shape the industry, too. Among these are, e.g., the automotive companies’ increasing concern for their carbon footprint, which is handed down to their suppliers, further amplifying the latter’s individual efforts. As one example, ae group AG may be mentioned, who claim total CO

2 neutrality for their production reached, among others, by full reliance on secondary aluminum and sourcing of green energy [

121].

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}