Serious Mortgage Arrears among Immigrant Descendant and Native Participants in a Low-Income Public Starter Mortgage Program: Evidence from Norway

Abstract

:1. Introduction

2. Mortgage Arrears among Vulnerable and Immigrant Homeowners

3. Homeownership and the Housing Market in Norway

4. The Starter Mortgage Program

5. Data and Methods

5.1. Data Sources and Matching

5.2. Serious Mortgage Arrears—Outcome Measure

5.3. Empirical Model Predicting Serious Mortgage Arrears

5.4. Analytical Approach

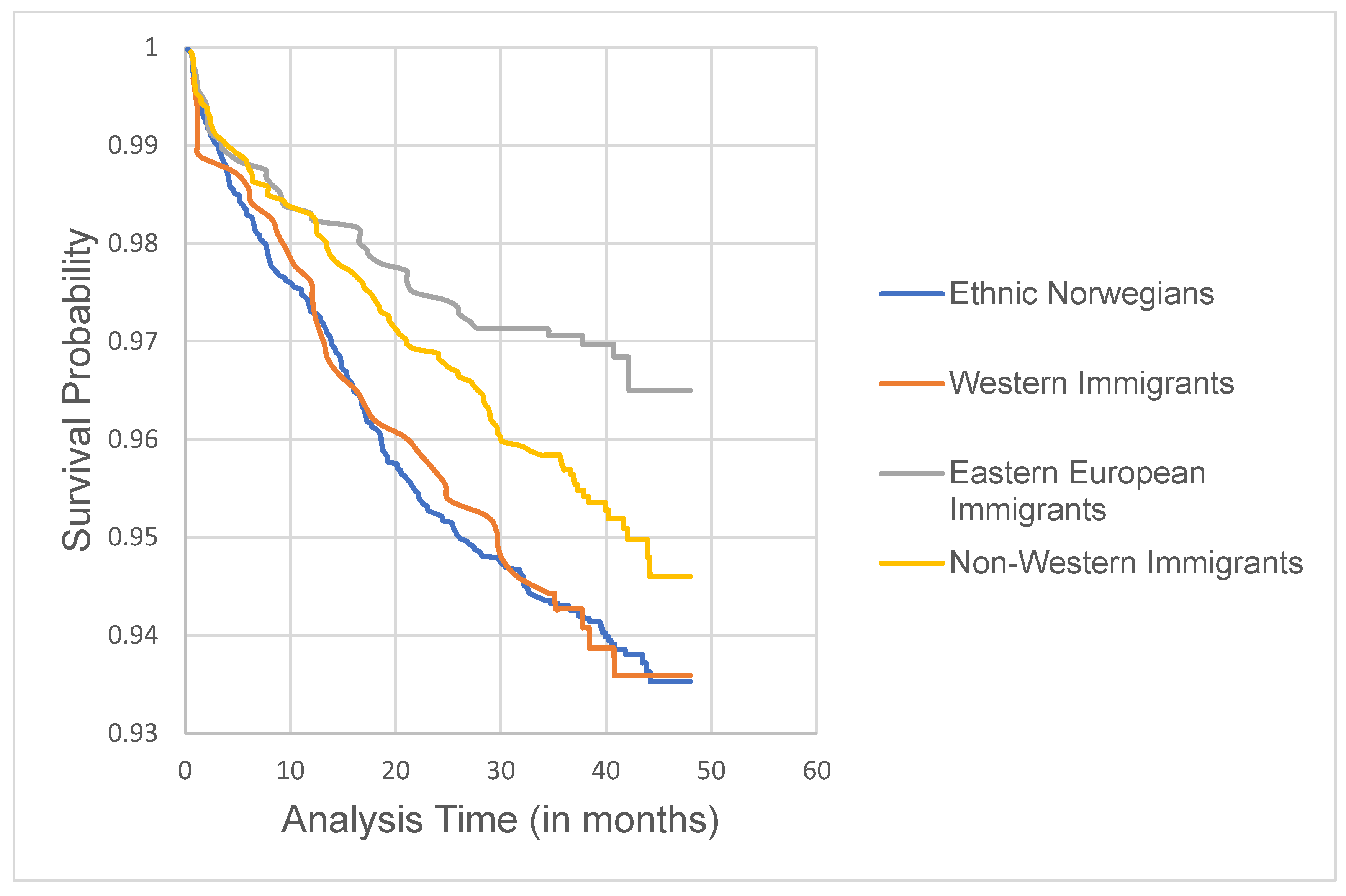

6. Results

7. Policy Discussion and Implications

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

| 1 | Given the relatively small samples sizes for immigrants from most countries, we have aggregated immigrant groups into larger regional categories using conventions employed by Statistics Norway [20]. Immigrant background pertains to all who have at least one foreign-born grandparent. Although this is notably a liberal definition of immigrant status, restricting the definition to all who are born abroad or who have at least one foreign-born parent changes the sample slightly only for Western immigrants, as most persons with Eastern European or non-Western background are immigrants or descendants (second generation). The choice of immigrant definition does not affect our results. For all official statistics, Statistics Norway maintains the definition of immigrant status as foreign-born, or native-born descendant of two foreign-born parents. “Western” includes countries in the EU/EEA outside of Eastern Europe, USA, Canada, Australia and New Zealand. “Eastern European” includes immigrants from EU/EEA countries in Eastern Europe. “Non-Western” includes countries in Asia, Africa, Latin America, Oceania except Australia and New Zealand, and Europe except the EU/EEA. |

| 2 | We first ran negative binomial models with random effects employed at the municipal (for Oslo borough) level, which corresponds to the administrative level at which the Starter Mortgage Program operates. The random effects negative binomial model was rejected for all groups but ethnic Norwegians, hence the standard negative binomial model was employed for the remaining three groups. See the modeling section for more details. |

| 3 | According to Statistics Norway [66], large fractions of immigrant men in Norway, especially from Eastern Europe, are employed in construction or other skilled trades; women are often employed in services such as cleaning, child care and elder care. |

| 4 | As of 1 January 2021, there are 356 municipalities in Norway, but during our study period 2005–2014, the number was 428. |

| 5 | In addition to home purchase, the starter mortgage may also be used for rebuilding/renovation, refinancing and construction. About 75% of the mortgages are used for home purchases. Our study focuses only on mortgages for first home purchases. |

| 6 | Effective for mortgages originated before 1 April 2014. Current guidelines do not list any particular beneficiaries, but state that the program should assist persons who have long-term problems accessing mortgage financing and have exhausted their potential to save for a downpayment. Exemptions from the latter may be granted for families with minor children and/or with particular social or health challenges, and for residents in public housing units. |

| 7 | The duty to dissuade is articulated in 46§47 [53]. Note that the applicant may still take out the loan even though they are advised against it. |

| 8 | The interest rate setting procedure for the State Housing Bank loan programs mimics those of e.g., the State Educational Loan Fund (student loans) and The Norwegian Public Service Pension Fund (mortgages for public sector employees). In addition, municipalities are allowed a 0.25 percentage point mark-up to cover their administrative costs. |

| 9 | Municipalities are fiscally responsible for the first 25% of any realized losses while the central government will absorb any additional losses. |

| 10 | Register data were not available for all mortgagors, and 61.8% of the cleaned sample was matched successfully. |

| 11 | We allow for minor discrepancies in the date and amount matching: matching is successful if the individual level ID matches and the dates are within 31 days of each other, grant amounts are within 5000 NOK of each other, and the loan amounts are within 40,000 NOK of each other across the two data sources. 1 USD = 5.817 2012 NOK [86]. |

| 12 | We also trim the house price distribution by dropping observations with the 1% lowest and highest home price values. |

| 13 | Unfortunately, the mortgage servicing firm assumed this task after 2006 in many municipalities, and the past payment histories for previously issued mortgages were not available. |

| 14 | Note that the observation period differs between 36 and 48 months, depending on the month of mortgage origination. Hence, numerous observations are censored between 36 and 48 months. |

| 15 | |

| 16 | Household equivalized income takes into account a household’s size and composition, and therefore is comparable across different households. The equivalized income is calculated by dividing the household’s total income by its equivalent size, in which the first adult is given weight 1, all additional persons aged 14 or over are given weight 0.5, and all children under the age of 14 are given weight 0.3, see [89]. |

| 17 | The annual income figures are highly serially correlated. We therefore average for years t0 (origination year) and t + 1, as income figures are available only through 2013. |

| 18 | Information on medical leave is only available through year t + 2 for all observations. |

| 19 | In Oslo, at the borough level. |

| 20 | For the standard negative binomial model, the dispersion parameter α is estimated along with the coefficient vector β. |

| 21 | The respective coefficients on Eijm are constrained to be equal to 1. |

| 22 | Although we acknowledge that mortgagors whose educational attainment is unknown have significantly higher expected 90-day delinquency among Western mortgage holders, and among Eastern European mortgage holders those with disability status have significantly fewer expected 90-days late payments. Note, however, that there very few observations with these characteristics in the respective country groups. |

| 23 | In previous estimations of our models, we employed calendar year fixed effects to control for climatic events that could affect utility costs, home repairs and maintenance required as well as other unmeasured user costs of owning. However, these were never significant. |

| 24 | Note that we have experimented with including variables to capture abrupt changes in the payment due from one month to the next, however, the estimated coefficients were never statistically significant. This indicates that the negative effect of interest-only debt servicing may not be immediate but rather lagged, or it may be cumulative or compounded over time, and in any case not necessarily tied to the precise point in time when the payment hike occurs. |

References

- Kemp, P. Housing benefit and welfare retrenchment in Britain. J. Soc. Policy 2000, 29, 263–279. [Google Scholar] [CrossRef]

- Retsinas, N.P.; Belsky, E.S. (Eds.) Low-Income Homeownership: Examining the Unexamined Goal; Brookings Institution Press: Washington, DC, USA; Harvard University Joint Center for Housing Studies: Cambridge, MA, USA, 2002. [Google Scholar]

- Yates, J. ‘The more things change?’: An overview of Australia’s recent home ownership policies. Eur. J. Hous. Policy 2003, 3, 1–33. [Google Scholar] [CrossRef]

- Doling, J.; Elsinga, M. (Eds.) Home Ownership: Getting in, Getting from, Getting out, Part I; Delft University Press: Amsterdam, The Netherlands, 2005. [Google Scholar]

- Poggio, T. Different patterns of ownership in Europe. In Proceedings of the Homeownership in Europe: Policy and Research Issues Conference, Delft, The Netherlands, 23–24 November 2006. [Google Scholar]

- Jones, A.; Elsinga, M.; Quilgars, D.; Toussaint, J. Homeowners’ perceptions of and responses to risk. Eur. J. Hous. Policy 2007, 7, 129–150. [Google Scholar] [CrossRef]

- Norris, M.; Coates, D.; Kane, F. Breaching the limits of owner occupation? Supporting low-income buyers in the inflated Irish housing market. Eur. J. Hous. Policy 2007, 7, 337–355. [Google Scholar] [CrossRef]

- Belsky, E.S.; Herbert, C.E.; Molinsky, J.H. (Eds.) Homeownership Built to Last: Balancing Access, Affordability, and Risk after the Housing Crisis; Brookings Institution Press: Washington, DC, USA; Harvard University Joint Center for Housing Studies: Cambridge, MA, USA, 2014. [Google Scholar]

- Filandri, M.; Olagnero, M. Housing inequality and social class in Europe. Hous. Stud. 2014, 29, 977–993. [Google Scholar] [CrossRef]

- McCarthy, Y. Disentangling the mortgage arrears crisis: The role of the labour market, income volatility and negative equity. J. Stat. Soc. Inq. Soc. Irel. 2014, 43, 71–90. [Google Scholar] [CrossRef]

- Dewilde, C.; de Decker, P. Changing inequalities in housing outcomes across Western Europe. Hous. Theory Soc. 2016, 33, 121–161. [Google Scholar] [CrossRef]

- Filandri, M.; Bertolini, S. Young people and home ownership in Europe. Int. J. Hous. Policy 2016, 16, 144–164. [Google Scholar] [CrossRef]

- Haffner, M.E.A.; Ong, R.; Smith, S.J.; Wood, G.A. The edges of home ownership—The borders of sustainability. Int. J. Hous. Policy 2017, 17, 169–176. [Google Scholar] [CrossRef]

- Clark, W.A.V. The aftermath of the General Financial Crisis for the ownership society: What happened to low-income homeowners in the United States? Int. J. Hous. Policy 2013, 13, 227–246. [Google Scholar] [CrossRef]

- Rohe, W.M.; Lindblad, M. Reexamining the social benefits of homeownership after the housing crisis. In Homeownership Built to Last; Belsky, E.S., Herbert, C.E., Molinsky, J.H., Eds.; Joint Center for Housing Studies: Cambridge, MA, USA, 2014; pp. 99–140. [Google Scholar]

- Arestei, D.; Gallo, M. The determinants of households’ repayment difficulties on mortgage loans: Evidence from Italian microdata. Int. J. Consum. Stud 2016, 40, 453–465. [Google Scholar] [CrossRef]

- Lin, Z.; Liu, Y.; Xie, J. Immigrants and mortgage delinquency. Real Estate Econ. 2016, 44, 198–235. [Google Scholar] [CrossRef]

- Gutierrez, A.; Domenech, A. The mortgage crisis and evictions in Barcelona: Identifying the determinants of the spatial clustering of foreclosures. Eur. Plan. Stud. 2018, 26, 1939–1960. [Google Scholar] [CrossRef]

- Anacker, K.B. Analyzing rates of seriously delinquent mortgages in Asian census tracts in the United States. Urban Aff. Rev. 2019, 55, 616–638. [Google Scholar] [CrossRef]

- Statistics Norway. Immigrants and Norwegian-Born to Immigrant Parents. 2022. Available online: https://www.ssb.no/en/befolkning/innvandrere/statistikk/innvandrere-og-norskfodte-med-innvandrerforeldre (accessed on 1 April 2023).

- Stamsø, M.A. Housing and the welfare state in Norway. Scan. Polit. Stud. 2009, 32, 195–220. [Google Scholar] [CrossRef]

- Statistics Norway. Immigrants and Norwegian Born to Immigrant Parents by Country Background and Year. 2022. Available online: https://www.ssb.no/en/statbank/table/13055/tableViewLayout1/ (accessed on 1 April 2023).

- Santiago, A.M.; Leroux, J. Hogar dulce hogar? [Home sweet home?]: Prepurchase counseling and the experience of low-income Latinx homeowners in Denver. Cityscape. 2021, 23, 95–136. [Google Scholar]

- Quercia, R.G.; Stegman, M.A. Residential mortgage default: A review of the literature. J. Hous. Res. 1992, 3, 341–379. [Google Scholar]

- LaCour-Little, M. Mortgage termination risk: A review of the recent literature. J. Real Estate Lit. 2008, 16, 297–326. [Google Scholar] [CrossRef]

- Jones, T.; Sirmans, G.S. The underlying determinants of mortgage default. J. Real Estate Lit. 2015, 23, 167–205. [Google Scholar] [CrossRef]

- Tajaddini, R.; Gholipour, H.F. National culture and default on mortgages. Int. Rev. Financ. 2017, 17, 107–133. [Google Scholar] [CrossRef]

- Petra Gerlach, K.; Lyons, S. Determinants of mortgage arrears in Europe: Evidence from household microdata. Int. J. Hous. Policy 2018, 18, 545–567. [Google Scholar] [CrossRef]

- Goodman, L.S.; Ashworth, R.; Landy, B.; Yin, K. Negative equity trumps unemployment in predicting defaults. J. Fixed Income 2010, 19, 67–72. [Google Scholar] [CrossRef]

- Seiler, M.J. The effect of perceived lender characteristics and market conditions on strategic mortgage defaults. J. Real Estate Financ. Econ. 2014, 48, 256–270. [Google Scholar] [CrossRef]

- Foote, C.L.; Gerardi, K.; Willen, P.S. Negative equity and foreclosure: Theory and evidence. J. Urban Econ. 2008, 64, 234–245. [Google Scholar] [CrossRef]

- Foote, C.L.; Gerardi, K.; Willen, P.S. Reducing foreclosures: No easy answers. NBER Macroecon. Annu. 2009, 24, 89–138. [Google Scholar] [CrossRef]

- Ngene, G.M.; Hassan, M.K.; Hippler III, W.J.; Julio, I. Determinants of mortgage default rates: Pre-crisis and crisis period dynamics and stability. J. Hous. Res. 2016, 25, 39–64. [Google Scholar] [CrossRef]

- Linn, A.; Lyons, R. Three triggers?: Negative equity, income shocks and institutions as determinants of mortgage default. J. Real Estate Financ. Econ. 2020, 61, 549–575. [Google Scholar] [CrossRef]

- Tian, C.Y.; Quercia, R.G.; Riley, S. Unemployment as an adverse trigger event for mortgage default. J. Real Estate Financ. Econ. 2016, 52, 28–49. [Google Scholar] [CrossRef]

- Farrell, D.; Bhagat, K.; Zhao, C. Falling Behind: Band Data on the Role of Income and Savings in Mortgage Default. JP Morgan Chase Institute. 2018. Available online: https://www.jpmorganchase.com/institute/research/hosuehold-debt/insight-income-shocks-mortgage-default (accessed on 1 April 2023).

- Elul, R.; Souleles, N.; Chomsisengphet, S.; Glennon, D.; Hunt, R. What “triggers” mortgage default? Am. Econ. Rev. 2010, 100, 490–494. [Google Scholar] [CrossRef]

- Almaas, S.; Bystrøm, L.; Carlsen, F.; Su, X. Home Equity-Based Refinancing and Household Financial Difficulties: The Case of Norway. SSRN Electron. J. 2015. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2523025 (accessed on 1 April 2023). [CrossRef]

- Stanga, I.; Vlahu, R.; de Haan, J. Mortgage Delinquency Rates: A Cross-Country Perspective. 2018. Available online: https://voxeu.org/article/mortgage-delinquency-rates-cross-country-perspective (accessed on 1 April 2023).

- Wilkinson-Ryan, T. Breaching the mortgage contract: The behavioral economics of strategic default. Vanderbilt Law Rev. 2011, 64, 1547–1583. [Google Scholar]

- Aarland, K.; Santiago, A.M. Staying afloat or going under: Mortgage arrears in Norway’s Starter Mortgage Program. Norw. J. Hous. Res. 2023; in press. [Google Scholar]

- McCann, F.; O’Malley, T. Resolving Mortgage Distress after COVID-19: Some Lessons from the Last Crisis. European Systemic Risk Board. Working Paper No 121. 2021. Available online: https://www.esrb.europa.eu/pub/pdf/wp/esrb.wp121~5615b74291.en.pdf?f15190b53fd322639ac0e9c60a1287f2 (accessed on 1 April 2023).

- Pfeiffer, D.; Wong, K.; Ong, P.; de la Cruz-Viesca, M. Ethnically bounded homeownership: Qualitative insights on Los Angeles immigrant homeowners’ experiences during the U.S. Great Recession. Hous. Stud. 2017, 32, 319–335. [Google Scholar] [CrossRef]

- Kochar, R.; Gonzalez-Barrera, A.; Docterman, D. Through Boom or Bust: Minorities, Immigrants and Homeownership. 2009. Available online: https://www.pewresearch.org/hispanic/2009/05/12/through-boom-and-bust/ (accessed on 1 April 2023).

- Lee, C.; Greenlee, A. Impact of multiscale racial concentration on neighborhood foreclosure risk in immigrant gateway metropolitan areas. City Community 2020, 19, 352–373. [Google Scholar] [CrossRef]

- Simone, D.; Walks, A. Immigration, race, mortgage lending, and the geography of debt in Canada’s global cities. Geoforum 2019, 98, 286–299. [Google Scholar] [CrossRef]

- Torgersen, U. Housing: The wobbly pillar under the welfare state. Scand Hous Plan Res. 1987, 4, 116–126. [Google Scholar] [CrossRef]

- Stamsø, M.A. Grants for first-time homeowners in Norway: Distributional effects under different market and political conditions. Eur. J. Hous. Policy 2008, 8, 379–397. [Google Scholar] [CrossRef]

- Aarland, K.; Nordvik, V. Eierlinjen i norsk boligpolitikk—Ter boligeien på seg for stor risiko? [The ownership line in Norwegian housing policy]. Økon. Polit. 2010, 83, 51–65. [Google Scholar]

- Nordvik, V.; Sørvoll, J. Interpreting housing allowance: The Norwegian case. Hous. Theory Soc. 2014, 31, 353–369. [Google Scholar] [CrossRef]

- Sørvoll, J. Norsk Boligpolitikk i Forandring 1970–2010; NOVA: Oslo, Norway, 2011. [Google Scholar]

- Sørvoll, J. The Political Economy of Housing and the Welfare State in Scandinavia 1980–2008: Change, Continuity, and Paradoxes. Paper Presented at the Annual Meetings of the European Network for Housing Research. 2009. Available online: https://enhr.net/wp-content/uploads/2019/12/2009BTApaper.pdf (accessed on 1 April 2023).

- Circular to the Act on Social Services in Norwegian Labor and Welfare Agency, Section 3 § 15. Available online: https://lovdata.no/nav/lov/2009-12-18-131/kap2/%C2%A73 (accessed on 1 April 2023).

- Circular to the Act on Social Services in Norwegian Labor and Welfare Agency, Section 4 § 27. Available online: https://lovdata.no/nav/lov/2009-12-18-131/kap2/%C2%A74 (accessed on 1 April 2023).

- Norwegian State Housing Bank. Årsrapport 2016. (Annual Report 2016), 2016. Norway: Norway State Housing Bank. Available online: https://www.husbanken.no/-/media/om-husbanken/arsrapporter/husbanken-%C3%A5rsrapport-2016.pdf (accessed on 1 April 2023).

- Sandlie, H.C.; Sørvoll, J. Et velfungerende leiemarked? [A well functioning rental market?]. Tidsskr. Velferdsforskning 2017, 20, 45–59. [Google Scholar] [CrossRef]

- Bengtsson, B.; Ruonavaara, H.; Sørvoll, J. Home ownership, housing policy and path dependence in Finland, Norway and Sweden. In Housing Wealth and Welfare; Dewilde, C., Ronald, R., Eds.; Edward Elgar Publishing: Cheltenham, UK, 2017; pp. 60–84. [Google Scholar]

- Ministry of Culture and Equality. Equality and Anti-Discrimination Act. 2017. Available online: https://lovdata.no/dokument/NLE/lov/2017-06-16-51 (accessed on 1 April 2023).

- The World Bank. The Global Findex Database 2021. 2023. Available online: https://www.worldbank.org/en/publication/globalfindex/Data (accessed on 1 April 2023).

- Mak, V. Predatory formations: Post-financial crisis lessons for the US and Europe. Tilburg Law Rev. 2019, 24, 5–9. [Google Scholar] [CrossRef]

- Finansportalen. Mortgage. Available online: https://www.finansportalen.no/bank/boliglan/ (accessed on 1 April 2023).

- Ministry of Finance. The Norwegian Lending Regulation. Available online: https://www.regjeringen.no/en/topics/the-economy/finansmarkedene/utlansforskriften/id2791101/ (accessed on 1 April 2023).

- Norges Bank. Financial Stability Report 2022: Vulnerabilities and Risks. 2022. Available online: https://www.norges-bank.no/en/news-events/news-publications/Reports/Financial-Stability-report/2022-financial-stability-report/content/ (accessed on 1 April 2023).

- Statistics Norway. Tenure Status by Immigration Category, Residents 2015–2021. 2021. Available online: https://www.ssb.no/en/statbank/table/11036 (accessed on 1 April 2023).

- Statistics Norway. Lavere Eierandel Blant Innvandrerne (Lower Homeownership Share among Immigrants). 2017. Available online: https://www.ssb.no/bygg-bolig-og-eiendom/artikler-og-publikasjoner/lavere-eierandel-blant-innvandrerne (accessed on 1 April 2023).

- Statistics Norway. Employment among Immigrants, Register-Based. 2022. Available online: https://www.ssb.no/en/arbeid-og-lonn/sysselsetting/statistikk/sysselsetting-blant-innvandrere-registerbasert (accessed on 1 April 2023).

- Gjestvang, M. Financial Literacy among Immigrants. Master’s Thesis, Faculty of Business and Law, Department of Economics and Finance, University of Agder, Kristiansand, Norway, 2020. Available online: https://uia.brage.unit.no/uia-xmlui/bitstream/handle/11250/2679481/Maria%20Gjestvang.pdf?sequence=1 (accessed on 1 April 2023).

- Andersson, L.; Jakobsson, N.; Kotsadam, A. A field experiment of discrimination in the Norwegian housing market: Gender, class and ethnicity. Land Econ. 2012, 88, 233–240. [Google Scholar] [CrossRef]

- Beatty, K.; Sommervoll, E. Discrimination in rental markets: Evidence from Norway. J. Hous. Econ 2012, 21, 121–130. [Google Scholar] [CrossRef]

- Vassenden, A. Homeownership and symbolic boundaries: Exclusion of disadvantaged non-homeowners in the homeowner nation of Norway. Hous. Stud. 2014, 29, 760–780. [Google Scholar] [CrossRef]

- Søholt, S.; Astrup, K. Etniske Minoriteter og Forskjellsbehandling i Leiemarkedet [Ethnic Minorities and Unequal Treatment in the Rental Market]. NIBR-Report: 2; Norwegian Institute for Urban and Regional Research: Oslo, Norway, 2009; Available online: https://www.regjeringen.no/no/dokumenter/etniske-minoriteter-og-forskjellsbehandl/id548595/ (accessed on 1 April 2023).

- Skifter Anderson, H.; Magnusson Turner, L.; Sóholt, S. The special importance of housing policy for ethnic minorities: Evidence from a comparison of four Nordic countries. Int. J. Hous. Policy 2013, 13, 20–44. [Google Scholar] [CrossRef]

- Quereshi, M.A. Inclusive or elusive housing? Homeownership among Muslims in Norway. J. Muslims Eur. 2020, 9, 355–376. [Google Scholar] [CrossRef]

- Borchgrevink, K.; Birkvad, I.R. Religious norms and homeownership among Norwegian Muslim women. J. Ethn. Migr. Stud. 2022, 48, 1228–1245. [Google Scholar] [CrossRef]

- Norwegian State Housing Bank. Startlån [Starter Loan] 2010–2022. Available online: https://statistikk.husbanken.no/lan/startlan (accessed on 1 April 2023).

- Norwegian State Housing Bank. Annual Reports. 2005. Available online: https://biblioteket.husbanken.no/arkiv/dok/3113/annualreport05.pdf (accessed on 1 April 2023).

- Norwegian State Housing Bank. Annual Report 2004. Available online: https://biblioteket.husbanken.no/arkiv/dok/aarsmeld/2004/Annualreport2004.pdf (accessed on 1 April 2023).

- Statistics Norway. Table 07111: Immigrants and Norwegian-Born to Immigrant Parents, by Sex and Age. Groups of Country Background 2001–2022. 2022. Available online: https://www.ssb.no/en/statbank/list/innvbef (accessed on 1 April 2023).

- Government of Norway. Act on Financial Contracts and Financial Assignments. 2000. Available online: https://app.uio.no/ub/ujur/oversatte-lover/data/lov-19990625-046-eng.pdf (accessed on 1 April 2023).

- Ergungor, O.E.; Moulton, S. Beyond the transaction: Banks and mortgage default of low-income homebuyers. J. Money Credit Bank 2014, 46, 1721–1752. [Google Scholar] [CrossRef]

- Hembre, E.; Moulton, S.; Record, M. Low-income homeownership and the role of state subsidies: A comparative analysis of mortgage outcomes. J. Policy Anal. Manag. 2021, 40, 78–106. [Google Scholar] [CrossRef]

- Santiago, A.M.; Leroux, J. Does pre-purchase counseling help low-income buyers choose and sustain homeownership in socially mixed destination neighborhoods? J Urban Aff. 2022, 44, 416–438. [Google Scholar] [CrossRef]

- Norwegian State Housing Bank. Årsrapport 2019. Vedlegg 2 Analyse av Startlån. [Annual Report 2019. Appendix 2 Analysis of the Starter Mortgage Program]. 2019. Available online: https://husbanken.no/-/media/om-husbanken/arsrapporter/husbankens-aarsrapport-2019.pdf (accessed on 1 April 2023).

- Norwegian State Housing Bank. Årsrapport 2021. Vedlegg 2 Analyse av Startlån. [Annual Report 2021. Appendix 2 Analysis of the Starter Mortgage Program]. 2021. Available online: https://husbanken.no/-/media/om-husbanken/arsrapporter/husbankens-a%CC%8Arsrapport-2021-web-uu.pdf (accessed on 1 April 2023).

- Financial Supervisory Authority of Norway. Finansielt Utsyn. Juni 2021. Available online: https://www.finanstilsynet.no/nyhetsarkiv/pressemeldinger/2021/finansielt-utsyn---juni-2021/ (accessed on 1 April 2023).

- OECD. Exchange Rates (Indicator). 2023. Available online: https://doi.org/10.1787/037ed317-en (accessed on 2 April 2023).

- Santiago, A.M.; Aarland, K. The role of forebearance in sustaining low-income homeownership: Evidence from Norway. Cityscape 2023, 25, 253–274. [Google Scholar]

- Norwegian State Housing Bank. Årsrapport 2018. (Annual Report 2018). Norway: Norway State Housing Bank. 2018. Available online: https://husbanken.no/-/media/om-husbanken/arsrapporter/husbanken-rsrapport-2018.pdf (accessed on 1 April 2023).

- European Mortgage Federation. Hypostat Equivalized Income. 2019. Available online: https://ec.europa.eu/eurostat/statisticsexplained/index.php?title=Glossary:Equivalized_income (accessed on 1 April 2023).

- Colin Cameron, A.C.; Trivedi, P.K. Regression Analysis of Count Data, 2nd ed.; Econometric Society Monograph No.53; Cambridge University Press: Cambridge, UK, 2013. [Google Scholar]

{kind=link}

| Total | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | |

|---|---|---|---|---|---|---|---|---|

| Ethnic Norwegians | ||||||||

| N | 4163 | 105 | 167 | 231 | 389 | 699 | 1006 | 1566 |

| Share never late | 93.9% | 94.3% | 87.4% | 91.8% | 90.5% | 94.3% | 95.2% | 94.7% |

| Share late at least once | 6.1% | 5.7% | 12.6% | 8.2% | 9.5% | 5.7% | 4.8% | 5.3% |

| Western Immigrants | ||||||||

| N | 628 | 8 | 15 | 21 | 37 | 110 | 176 | 261 |

| Share never late | 93.8% | 87.5% | 73.3% | 100.0% | 89.2% | 93.6% | 92.6% | 96.2% |

| Share late at least once | 6.2% | 12.5% | 26.7% | 0.0% | 10.8% | 6.4% | 7.4% | 3.8% |

| Eastern European Immigrants | ||||||||

| N | 1359 | 7 | 23 | 55 | 104 | 261 | 377 | 532 |

| Share never late | 96.8% | 100.0% | 100.0% | 92.7% | 95.2% | 97.3% | 96.8% | 97.0% |

| Share late at least once | 3.2% | 0.0% | 0.0% | 7.3% | 4.8% | 2.7% | 3.2% | 3.0% |

| Non-Western Immigrants | ||||||||

| N | 2113 | 38 | 69 | 137 | 187 | 412 | 521 | 749 |

| Share never late | 95.1% | 92.1% | 92.8% | 93.4% | 94.1% | 96.1% | 95.6% | 95.2% |

| Share late at least once | 4.9% | 7.9% | 7.2% | 6.6% | 5.9% | 3.9% | 4.4% | 4.8% |

| Number of 90-Day Late Payments | ||||

|---|---|---|---|---|

| 1 | 2–4 | 5 or More | Total | |

| Full sample | ||||

| N | 190 | 159 | 91 | 440 |

| Share | 43% | 36% | 21% | |

| Ethnic Norwegians | ||||

| N | 98 | 98 | 58 | 254 |

| Share | 39% | 39% | 23% | |

| Western Immigrants | ||||

| N | 17 | 14 | 8 | 39 |

| Share | 44% | 36% | 21% | |

| Eastern European Immigrants | ||||

| N | 25 | 16 | 3 | 44 |

| Share | 57% | 36% | 7% | |

| Non-Western Immigrants | ||||

| N | 50 | 31 | 22 | 103 |

| Share | 49% | 30% | 21% | |

| Ethnic Norwegians | Western Immigrants | Eastern European Immigrants | Non-Western Immigrants | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Never Late through t + 3 | Late at Least Once through t + 3 | Never Late through t + 3 | Late at Least Once through t + 3 | Never Late through t + 3 | Late at Least Once through t + 3 | Never Late through t + 3 | Late at Least Once through t + 3 | |||||||||

| Mean | SD | Mean | SD | Mean | SD | Mean | SD | Mean | SD | Mean | SD | Mean | SD | Mean | SD | |

| Applicant and Household Characteristics | ||||||||||||||||

| Main applicant is female | 0.54 | 0.50 | 0.48 | 0.50 | 0.51 | 0.50 | 0.51 | 0.51 | 0.47 | 0.50 | 0.45 | 0.50 | 0.46 | 0.50 | 0.49 | 0.50 |

| Age of main applicant | 35.37 | 10.33 | 35.49 | 10.06 | 34.89 | 9.28 | 36.50 | 9.71 | 35.80 | 7.83 | 34.55 | 7.39 | 36.94 | 8.45 | 35.78 | 8.58 |

| Has co-applicant | 0.26 | 0.44 | 0.21 | 0.41 | 0.39 | 0.49 | 0.31 | 0.47 | 0.67 | 0.47 | 0.61 | 0.49 | 0.46 | 0.50 | 0.48 | 0.50 |

| Number of children at application | 0.51 | 0.83 | 0.72 | 0.98 | 0.56 | 0.86 | 0.69 | 0.89 | 0.84 | 0.95 | 1.18 | 1.15 | 1.04 | 1.24 | 1.12 | 1.35 |

| Main applicant is disabled | 0.22 | 0.42 | 0.18 | 0.38 | 0.14 | 0.35 | 0.13 | 0.34 | 0.01 | 0.11 | 0.00 | 0.00 | 0.07 | 0.26 | 0.05 | 0.22 |

| Educational attainment of main applicant (ref = high school degree or less) | ||||||||||||||||

| Education level is missing | 0.01 | 0.09 | 0.00 | 0.06 | 0.06 | 0.23 | 0.10 | 0.31 | 0.15 | 0.36 | 0.34 | 0.48 | 0.09 | 0.29 | 0.18 | 0.39 |

| University/college degree | 0.26 | 0.44 | 0.17 | 0.37 | 0.33 | 0.47 | 0.33 | 0.48 | 0.32 | 0.47 | 0.23 | 0.42 | 0.31 | 0.46 | 0.21 | 0.41 |

| Mortgage Terms at Time of Origination | ||||||||||||||||

| Purchased home is a single-family home (ref = no) | 0.24 | 0.43 | 0.35 | 0.48 | 0.27 | 0.44 | 0.31 | 0.47 | 0.26 | 0.44 | 0.27 | 0.45 | 0.10 | 0.30 | 0.14 | 0.34 |

| Startlån loan as share of total mortgage | 57.28 | 38.98 | 61.84 | 38.66 | 47.96 | 37.74 | 43.39 | 36.63 | 43.14 | 35.03 | 43.38 | 35.57 | 66.77 | 38.57 | 66.33 | 37.72 |

| Loan-to-value ratio for purchased property | 90.85 | 15.86 | 92.77 | 14.44 | 93.98 | 12.73 | 93.32 | 11.37 | 96.59 | 7.78 | 97.72 | 5.60 | 92.79 | 12.18 | 96.79 | 8.09 |

| Debt-to-income ratio for purchased property | 3.66 | 1.32 | 3.75 | 1.58 | 3.62 | 1.20 | 3.82 | 1.22 | 3.43 | 1.04 | 3.04 | 1.26 | 3.67 | 1.13 | 3.60 | 1.22 |

| Fixed-rate mortgage/FRM (ref = no) | 0.19 | 0.39 | 0.16 | 0.36 | 0.20 | 0.40 | 0.13 | 0.34 | 0.15 | 0.35 | 0.09 | 0.29 | 0.26 | 0.44 | 0.12 | 0.32 |

| Downpayment grant amount (in 1000 2012 NOK) | 66.00 | 158.51 | 60.31 | 137.10 | 41.38 | 122.89 | 51.52 | 115.67 | 17.65 | 90.66 | 6.86 | 45.50 | 61.42 | 170.99 | 33.10 | 107.51 |

| Interest-only servicing at origination (ref = no) | 0.09 | 0.28 | 0.14 | 0.35 | 0.05 | 0.21 | 0.18 | 0.39 | 0.04 | 0.19 | 0.07 | 0.25 | 0.04 | 0.19 | 0.07 | 0.25 |

| Household Financial Vulnerability and Economic Shocks | ||||||||||||||||

| Average equivalized household income in year t0 and t + 1 (in 1000 2012 NOK) | 372.04 | 135.71 | 349.99 | 133.86 | 407.46 | 135.08 | 358.76 | 118.81 | 378.68 | 106.60 | 326.48 | 87.58 | 348.79 | 123.29 | 331.74 | 101.76 |

| Average interest payments as a share of household income in year t0 and t + 1 | 11.20 | 4.58 | 12.94 | 6.35 | 10.60 | 4.35 | 14.44 | 10.97 | 9.49 | 4.25 | 9.91 | 3.74 | 9.83 | 4.91 | 12.69 | 6.38 |

| Average welfare benefits as a share of household income in year t0 and t + 1 | 32.06 | 39.14 | 37.01 | 37.49 | 21.18 | 33.66 | 25.24 | 33.10 | 8.88 | 15.69 | 13.30 | 21.84 | 20.06 | 27.12 | 22.57 | 27.49 |

| Total number of months jobless from origination through t + 3 | 9.97 | 13.39 | 14.24 | 14.76 | 8.34 | 12.78 | 14.23 | 14.87 | 7.56 | 10.81 | 13.07 | 12.77 | 9.39 | 12.33 | 12.23 | 13.32 |

| Total number of months on medical leave from origination through t + 2 * | 1.84 | 4.01 | 2.51 | 4.43 | 1.63 | 3.60 | 3.25 | 5.44 | 2.03 | 4.09 | 2.93 | 4.54 | 2.06 | 4.09 | 3.25 | 4.98 |

| Mortgage Origination Cohort | ||||||||||||||||

| 2006 | 0.03 | 0.16 | 0.02 | 0.15 | 0.01 | 0.11 | 0.03 | 0.16 | 0.01 | 0.07 | 0.02 | 0.13 | 0.03 | 0.17 | ||

| 2007 | 0.04 | 0.19 | 0.08 | 0.28 | 0.02 | 0.14 | 0.10 | 0.31 | 0.02 | 0.13 | 0.03 | 0.18 | 0.05 | 0.22 | ||

| 2008 | 0.05 | 0.23 | 0.07 | 0.26 | 0.04 | 0.19 | 0.04 | 0.19 | 0.09 | 0.29 | 0.06 | 0.24 | 0.09 | 0.28 | ||

| 2009 | 0.09 | 0.29 | 0.15 | 0.35 | 0.06 | 0.23 | 0.10 | 0.31 | 0.08 | 0.26 | 0.11 | 0.32 | 0.09 | 0.28 | 0.11 | 0.31 |

| 2010 | 0.17 | 0.37 | 0.16 | 0.36 | 0.17 | 0.38 | 0.18 | 0.39 | 0.19 | 0.39 | 0.16 | 0.37 | 0.20 | 0.40 | 0.16 | 0.36 |

| 2011 | 0.25 | 0.43 | 0.19 | 0.39 | 0.28 | 0.45 | 0.33 | 0.48 | 0.28 | 0.45 | 0.27 | 0.45 | 0.25 | 0.43 | 0.22 | 0.42 |

| 2012 | 0.38 | 0.49 | 0.33 | 0.47 | 0.43 | 0.49 | 0.26 | 0.44 | 0.39 | 0.49 | 0.36 | 0.49 | 0.35 | 0.48 | 0.35 | 0.48 |

| N | 3909 | 254 | 589 | 39 | 1315 | 44 | 2010 | 103 | ||||||||

| Ethnic Norwegians | Western Immigrants | Eastern European Immigrants | Non-Western Immigrants | |||||

|---|---|---|---|---|---|---|---|---|

| IRR | IRR | IRR | IRR | |||||

| Applicant and Household Characteristics | ||||||||

| Main applicant is female | 0.673 | ** | 0.844 | 0.763 | 1.265 | |||

| Age of main applicant | 0.998 | 1.018 | 0.958 | 0.969 | ||||

| Has co-applicant | 0.731 | 0.349 | * | 0.740 | 0.353 | *** | ||

| Number of children at time of application | 1.244 | ** | 1.397 | 1.198 | 1.195 | |||

| Main applicant is disabled | 0.533 | ** | 0.525 | 0.000 | *** | 1.701 | ||

| Educational attainment of main applicant (ref = high school degree or less) | ||||||||

| Education level is missing b | 0.502 | 49.600 | *** | 2.416 | 1.259 | |||

| University/college degree | 0.634 | ** | 1.327 | 0.790 | 0.606 | |||

| Mortgage Terms at Time of Origination | ||||||||

| Purchased home is a single-family home (ref = no) | 1.511 | ** | 1.589 | 0.690 | 0.779 | |||

| Startlån loan as share of total mortgage | 1.005 | * | 0.986 | * | 0.995 | 1.007 | ** | |

| Loan-to-value ratio for purchased property | 1.018 | * | 0.995 | 1.051 | 1.174 | *** | ||

| Debt-to-income ratio for purchased property | 1.006 | 1.121 | 0.666 | * | 0.596 | *** | ||

| Fixed-rate mortgage/FRM (ref = no) | 0.841 | 0.272 | * | 0.883 | 0.332 | ** | ||

| Municipal downpayment grant amount (in 1000 2012 NOK) b | 1.001 | 1.004 | 1.000 | 1.006 | *** | |||

| Interest-only servicing at origination (ref = no) | 1.313 | 2.743 | 2.309 | 5.755 | * | |||

| Household Financial Vulnerability and Economic Shocks | ||||||||

| Average equivalized household income in year t0 and t + 1 (in 1000 2012 NOK) c | 1.000 | 0.996 | 0.995 | * | 0.998 | |||

| Average interest payments as a share of household income in year t0 and t + 1 | 1.049 | *** | 1.008 | 1.000 | 1.163 | *** | ||

| Average welfare benefits as a share of household income in year t0 and t + 1 | 1.006 | 1.002 | 1.005 | 1.008 | ||||

| Total number of months jobless from origination through t + 3 | 1.009 | 1.023 | 1.037 | ** | 0.990 | |||

| Total number of months on medical leave from origination through t + 2 d | 1.021 | 1.061 | 1.029 | 1.041 | ||||

| /ln_r | 0.594 | * | ||||||

| /ln_s | 1.939 | *** | ||||||

| /lnalpha | 2.647 | *** | 2.882 | *** | 3.322 | *** | ||

| N | 4163 | 628 | 1359 | 2113 | ||||

| Log-likelihood | −1419.3 | −201.4 | −239.0 | -577.2 | ||||

| Chi2 | 127.4 | 6736.7 | 3058.1 | 1224.2 | ||||

| p | 0.000 | 0.000 | 0.000 | 0.000 | ||||

| LR test vs. pooled model: | ||||||||

| Chi2 | 24.6 | |||||||

| Prob ≥ Chi2 | 0.000 | |||||||

| Never Late through t + 3 | Late at Least Once through t + 3 | |||

|---|---|---|---|---|

| Ethnic Norwegians | ||||

| Mean | Std. Dev. | Mean | Std. Dev. | |

| Household real gross wealth t0 | 158.29 | 84.27 | 155.15 | 77.77 |

| Household bank deposits t0 | 6.25 | 8.48 | 3.36 | 7.70 |

| Household other financial assets t0 | 1.81 | 6.55 | 1.17 | 2.83 |

| N | 2888 | 130 | ||

| 2010 | 614 | 29 | ||

| 2011 | 899 | 39 | ||

| 2012 | 1375 | 62 | ||

| Western Immigrants | ||||

| Household real gross wealth t0 | 171.82 | 89.47 | 158.93 | 89.80 |

| Household bank deposits t0 | 5.98 | 7.28 | 1.61 | 3.44 |

| Household other financial assets t0 | 1.46 | 3.28 | 1.38 | 3.67 |

| N | 490 | 24 | ||

| 2010 | 97 | 7 | ||

| 2011 | 160 | 10 | ||

| 2012 | 233 | 7 | ||

| Eastern European Immigrants | ||||

| Household real gross wealth t0 | 177.80 | 99.95 | 94.16 | 86.78 |

| Household bank deposits t0 | 6.09 | 11.03 | 3.95 | 7.28 |

| Household other financial assets t0 | 1.48 | 5.89 | 0.73 | 0.99 |

| N | 1103 | 26 | ||

| 2010 | 242 | 6 | ||

| 2011 | 358 | 7 | ||

| 2012 | 503 | 13 | ||

| Non-Western Immigrants | ||||

| Household real gross wealth t0 | 170.22 | 96.28 | 161.83 | 81.51 |

| Household bank deposits t0 | 6.32 | 8.82 | 2.73 | 4.34 |

| Household other financial assets t0 | 1.90 | 5.04 | 1.55 | 2.04 |

| N | 1547 | 60 | ||

| 2010 | 383 | 12 | ||

| 2011 | 476 | 17 | ||

| 2012 | 688 | 31 | ||

| Ethnic Norwegians | Western Immigrants | Eastern European Immigrants | Non-Western Immigrants | |||||

|---|---|---|---|---|---|---|---|---|

| IRR | IRR | IRR | IRR | |||||

| Applicant and Household Characteristics | ||||||||

| Main applicant is female | 0.634 | * | 1.578 | 1.034 | 1.014 | |||

| Age of main applicant | 1.000 | 1.022 | 0.960 | 0.961 | ||||

| Has co-applicant | 0.862 | 2.550 | 1.435 | 0.282 | ** | |||

| Number of children at time of application | 1.342 | ** | 0.651 | 0.750 | 1.610 | ** | ||

| Main applicant is disabled | 0.388 | * | 0.755 | 0.000 | *** | 0.904 | ||

| Educational attainment of main applicant (ref = high school degree or less) | ||||||||

| Education level is missing b | 0.000 | 27.938 | ** | 1.548 | 2.104 | |||

| University/college degree | 0.542 | * | 3.579 | 0.594 | 0.833 | |||

| Mortgage Terms at Time of Origination | ||||||||

| Purchased home is a single-family home (ref = no) | 1.533 | * | 2.762 | * | 0.752 | 0.764 | ||

| Startlån loan as share of total mortgage | 1.009 | ** | 0.992 | 0.999 | 1.004 | |||

| Loan-to-value ratio for purchased property | 1.016 | 0.998 | 1.145 | 1.206 | *** | |||

| Debt-to-income ratio for purchased property | 1.045 | 1.383 | 0.709 | 0.605 | *** | |||

| Fixed-rate mortgage/FRM (ref = no) | 0.795 | 0.693 | 1.021 | 0.407 | ||||

| Municipal downpayment grant amount (in 1000 2012 NOK) c | 1.001 | 1.004 | 1.008 | 1.009 | *** | |||

| Interest-only servicing at origination (ref = no) | 1.028 | 5.888 | * | 3.955 | * | 5.150 | * | |

| Household Financial Vulnerability and Economic Shocks | ||||||||

| Average equivalized household income in year t0 and t + 1 (in 1000 2012 NOK) c | 1.001 | 0.994 | 0.994 | 0.998 | ||||

| Average interest payments as share of household income in year t0 and t + 1 | 1.055 | *** | 1.017 | 0.999 | 1.149 | * | ||

| Average welfare benefits as share of household income in year t0 and t + 1 | 1.006 | 0.996 | 0.999 | 1.004 | ||||

| Total number of month jobless from origination through t + 3 | 1.006 | 1.025 | 1.053 | * | 0.981 | |||

| Total number of months on medical leave from origination through t + 2 d | 1.045 | * | 1.106 | * | 0.972 | 1.112 | * | |

| Household Assets | ||||||||

| Household real wealth t0 (in 10,000 2012 NOK) | 0.999 | 0.994 | * | 0.985 | *** | 0.993 | * | |

| Household other financial assets t0 (in 10,000 2012 NOK) | 0.974 | 1.111 | 0.872 | 0.990 | ||||

| Household bank deposits t0 (in 10,000 2012 NOK) | 0.947 | ** | 0.658 | 0.964 | 0.930 | ** | ||

| /ln_r | 0.836 | |||||||

| /ln_s | 2.376 | ** | ||||||

| /lnalpha | 2.149 | ** | 2.426 | *** | 3.569 | *** | ||

| N | 3018 | 514 | 1129 | 1607 | ||||

| Log-likelihood | −762.3 | −123.1 | −133.0 | −358.6 | ||||

| Chi2 | 95.6 | 205.1 | 3821.8 | 1445.5 | ||||

| p | 0.000 | 0.000 | 0.000 | 0.000 | ||||

| LR test vs. pooled model: | ||||||||

| Chi2 | 4.35 | |||||||

| Prob ≥ Chi2 | 0.019 | |||||||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Aarland, K.; Santiago, A.M. Serious Mortgage Arrears among Immigrant Descendant and Native Participants in a Low-Income Public Starter Mortgage Program: Evidence from Norway. Societies 2023, 13, 121. https://doi.org/10.3390/soc13050121

Aarland K, Santiago AM. Serious Mortgage Arrears among Immigrant Descendant and Native Participants in a Low-Income Public Starter Mortgage Program: Evidence from Norway. Societies. 2023; 13(5):121. https://doi.org/10.3390/soc13050121

Chicago/Turabian StyleAarland, Kristin, and Anna Maria Santiago. 2023. "Serious Mortgage Arrears among Immigrant Descendant and Native Participants in a Low-Income Public Starter Mortgage Program: Evidence from Norway" Societies 13, no. 5: 121. https://doi.org/10.3390/soc13050121