Does Farmland Tenancy Improve Household Asset Allocation? Evidence from Rural China

Abstract

:1. Introduction

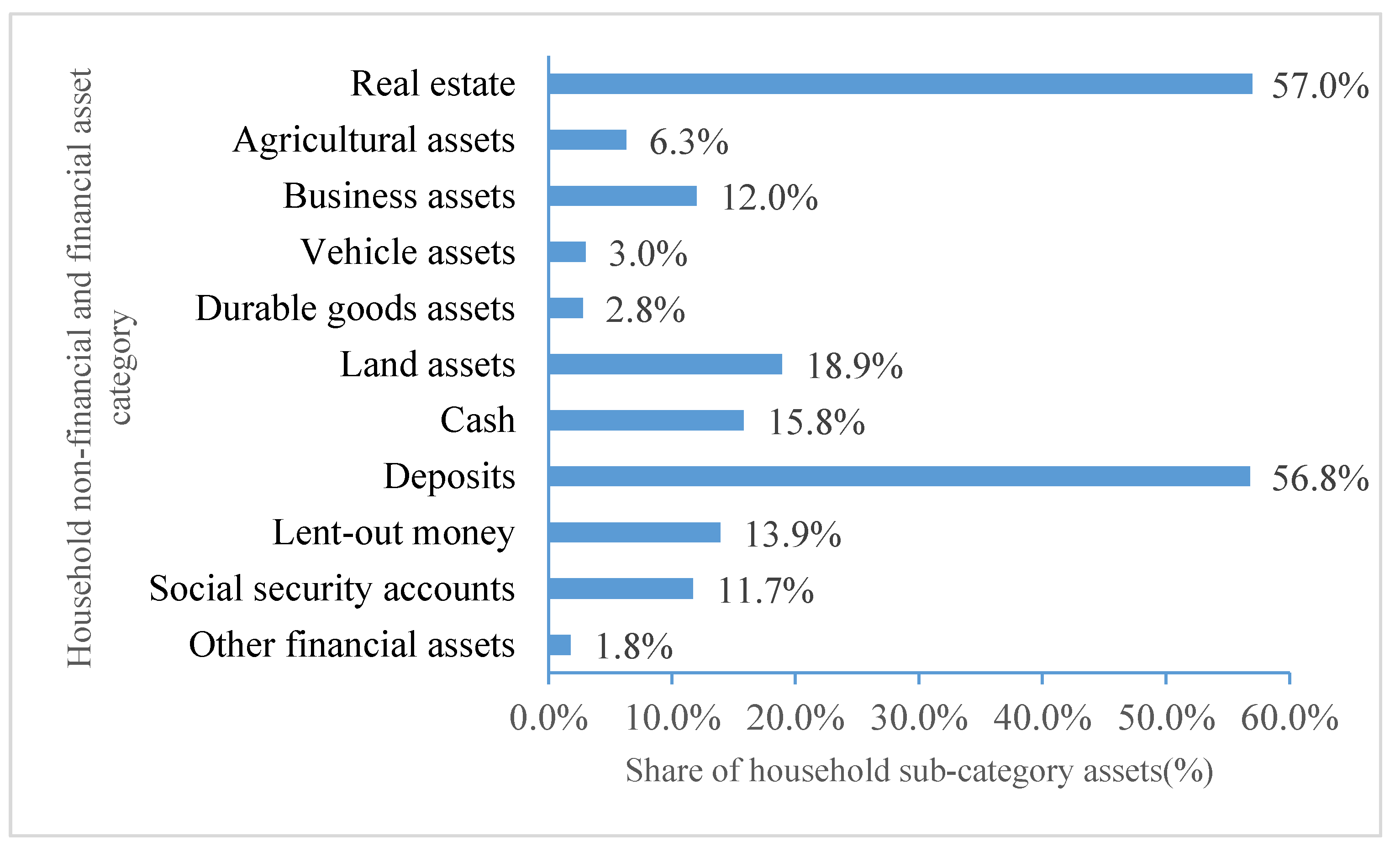

2. Evolution and Characteristics of China’s Farmland Rental Market and Household Assets

3. Theoretical Analysis

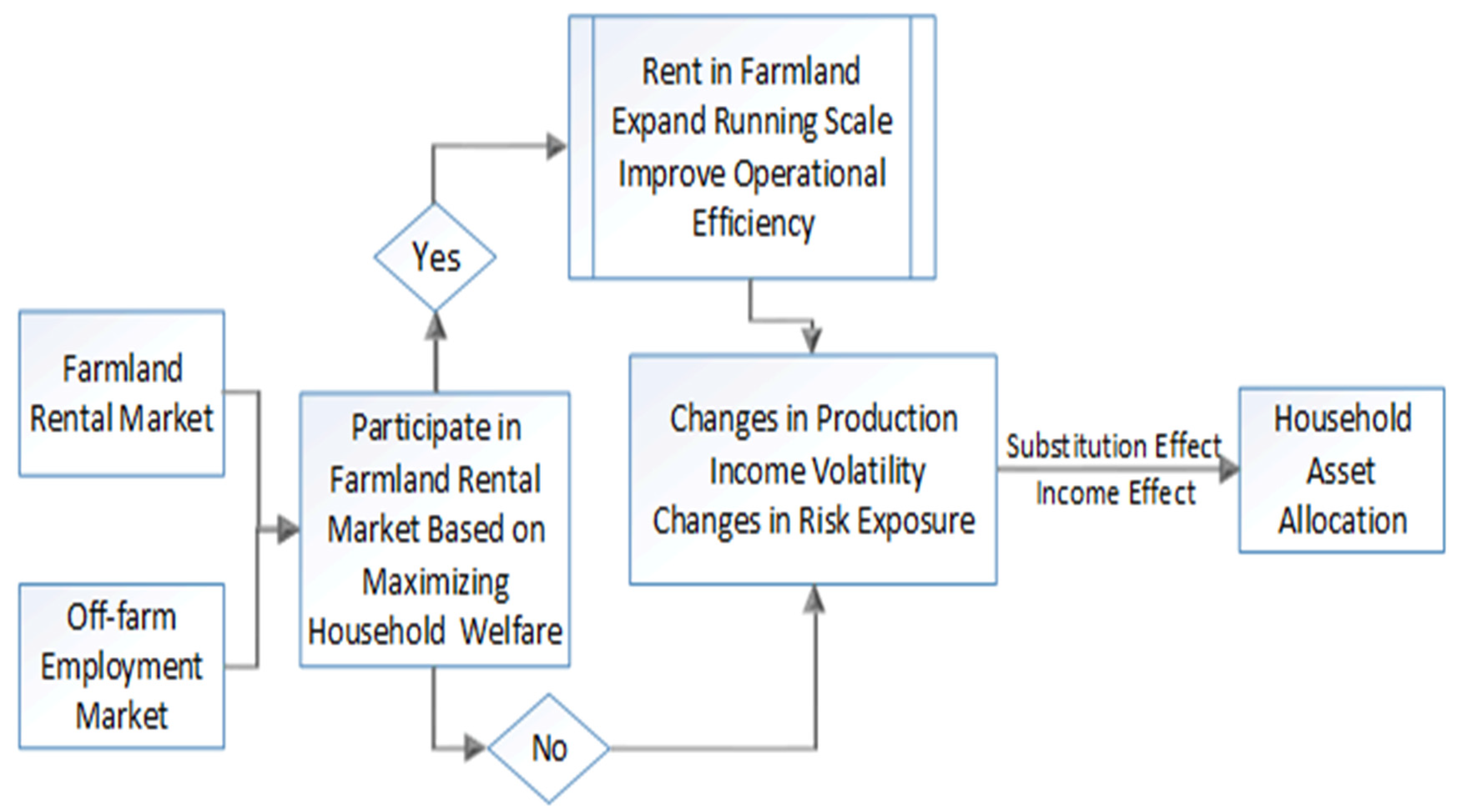

3.1. The Income Effect of Farmland Tenancy on Household Asset Allocation

3.2. The Substitution Effect of the Tenancy of Farmland on Household Asset Allocation

4. Methodology and Data

4.1. Methodology

4.2. Data Source

4.3. Variables Description

4.3.1. Dependent Variable

4.3.2. Core Explanatory Variable

4.3.3. Control Variables

5. Results and Discussion

5.1. Descriptive Statistics of the Research Variables

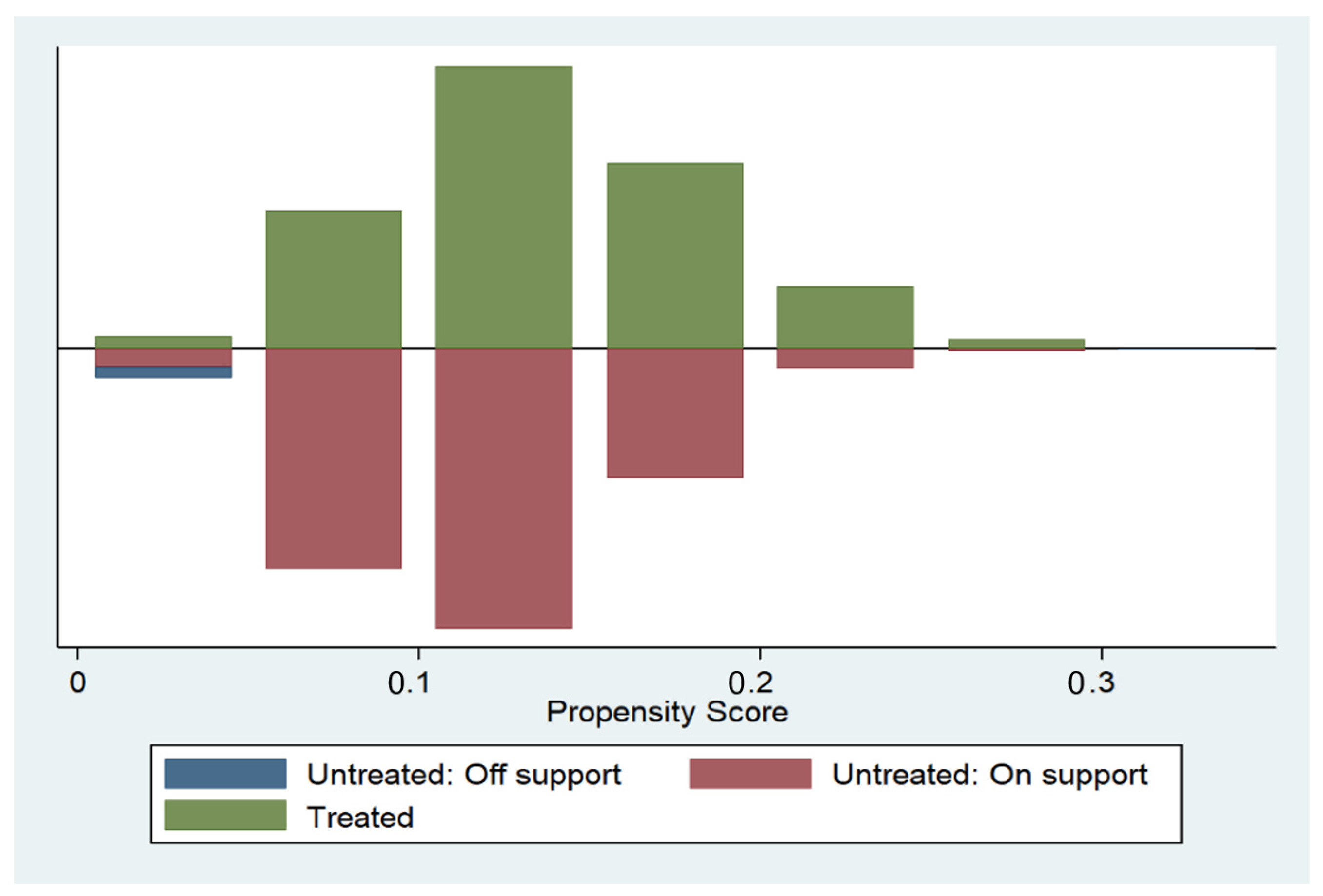

5.2. Propensity Score Matching Procedure

5.3. The Impacts of Farmland Tenancy on Household Asset Allocation

5.4. The Impacts on Household Asset Allocation with Different Tenancy Intensities in the Farmland Rental Market

5.5. Mechanisms for Farmland Tenancy Affecting Renting-In Household Asset Allocation

6. Conclusions and Policy Implications

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

| 1 | According to land transfer practice in rural China, there are five forms involved in the land transfer, transfer the possession of land, exchange, leasing subcontract, becoming a shareholder and other forms that comply with relevant laws and national policies. Here the transfer of cultivated land covers the above 5 forms and is defined by the Administrative Measures for the Transfer of Rural Land Management Rights before 2021. But the Administrative Measures for the Transfer of Rural Land Management Rights has been revised in 2021, and only leasing subcontract (transfer the possession of land), becoming a shareholder and other forms that comply with relevant laws and national policies are included in the land transfer. |

| 2 | From the perspective of the supply and demand of the farmland rental market, the participation of the household’s farmland rental market mainly includes two types: leasing out farmland or tenancy of farmland. The former rent out their farmland management right, while the latter rent in the farmland management rights of others. |

| 3 | Because of the social security system in rural China, few households have retirement accounts. Therefore, retirement account assets were not considered in our study. |

| 4 | In combining the conventional literature with the practice of asset allocation in rural China the measurement of financial assets and risky assets have been adjusted slightly in our study. |

| 5 | 1 mu = 667 m2 or 0.067 ha. |

| 6 | 0.1140 is the arithmetic mean of the results of PSM-DID with KM and PSM-DID with LLRM. |

| 7 | 0.1050 is the results of PSM-DID with KM. |

| 8 | 2.1991 is the arithmetic mean of the results of PSM-DID with KM and PSM-DID with LLRM. |

| 9 | The results in parentheses are obtained by adopting kernel matching and bootstrap sampling 500 replications, and the results using local linear regression matching and bootstrap sampling 500 replications are still robust. The meaning of and are the same. |

References

- Doepke, M.; Schneider, M. Inflation and the Redistribution of Nominal Wealth. J. Politi-Econ. 2006, 114, 1069–1097. [Google Scholar] [CrossRef] [Green Version]

- Berloffa, G.; Modena, F. Income shocks, coping strategies, and consumption smoothing: An application to Indonesian data. J. Asian Econ. 2012, 24, 158–171. [Google Scholar] [CrossRef]

- Wei, S.-J.; Wu, W.; Zhang, L. Portfolio choices, Asset returns and wealth inequality: Evidence from China. Emerg. Mark. Rev. 2018, 38, 423–437. [Google Scholar] [CrossRef]

- You, J. Risk, under-investment in agricultural assets and dynamic asset poverty in rural China. China Econ. Rev. 2014, 29, 27–45. [Google Scholar] [CrossRef]

- Zhou, Y.; Li, X.; Liu, Y. Rural land system reforms in China: History, issues, measures and prospects. Land Use Policy 2019, 91, 104330. [Google Scholar] [CrossRef]

- Fei, R.; Lin, Z.; Chunga, J. How land transfer affects agricultural land use efficiency: Evidence from China’s agricultural sector. Land Use Policy 2021, 103, 105300. [Google Scholar] [CrossRef]

- Lu, X.-H.; Jiang, X.; Gong, M.-Q. How land transfer marketization influence on green total factor productivity from the approach of industrial structure? Evidence from China. Land Use Policy 2020, 95, 104610. [Google Scholar] [CrossRef]

- Carter, M.R.; Yao, Y. Local versus Global Separability in Agricultural Household Models: The Factor Price Equalization Effect of Land Transfer Rights. Am. J. Agric. Econ. 2002, 84, 702–715. [Google Scholar] [CrossRef]

- Jin, S.; Deininger, K. Land rental markets in the process of rural structural transformation: Productivity and equity impacts from China. J. Comp. Econ. 2009, 37, 629–646. [Google Scholar] [CrossRef] [Green Version]

- Daymard, A. Land rental market reforms: Can they increase outmigration from agriculture? Evidence from a quantitative model. World Dev. 2022, 154, 105865. [Google Scholar] [CrossRef]

- Betermier, S.; Jansson, T.; Parlour, C.; Walden, J. Hedging labor income risk. J. Financ. Econ. 2012, 105, 622–639. [Google Scholar] [CrossRef] [Green Version]

- Chang, Y.; Hong, J.H.; Karabarbounis, M.; Wang, Y.; Zhang, T. Income volatility and portfolio choices. Rev. Econ. Dyn. 2021, 44, 65–90. [Google Scholar] [CrossRef]

- Bodie, Z.; Merton, R.C.; Samuelson, W.F. Labor supply flexibility and portfolio choice in a life cycle model. J. Econ. Dyn. Control. 1992, 16, 427–449. [Google Scholar] [CrossRef] [Green Version]

- Campbell, J.Y. Household Finance. J. Financ. 2006, 61, 1553–1604. [Google Scholar] [CrossRef] [Green Version]

- Cardak, B.; Wilkins, R. The determinants of household risky asset holdings: Australian evidence on background risk and other factors. J. Bank. Financ. 2009, 33, 850–860. [Google Scholar] [CrossRef] [Green Version]

- Cocco, J.F. Portfolio Choice in the Presence of Housing. Rev. Financ. Stud. 2004, 18, 535–567. [Google Scholar] [CrossRef]

- Guiso, L.; Sodini, P. Chapter 21—Household Finance: An Emerging Field. In Handbook of the Economics of Finance; Constantinides, G.M., Harris, M., Stulz, R.M., Eds.; Elsevier: Amsterdam, The Netherlands, 2013; Volume 2, pp. 1397–1532. [Google Scholar] [CrossRef] [Green Version]

- King, M.A.; Leape, J.I. Wealth and portfolio composition: Theory and evidence. J. Public Econ. 1998, 69, 155–193. [Google Scholar] [CrossRef] [Green Version]

- Heaton, J.; Lucas, D. Portfolio Choice and Asset Prices: The Importance of Entrepreneurial Risk. J. Financ. 2000, 55, 1163–1198. [Google Scholar] [CrossRef]

- Malmendier, U.; Nagel, S. Depression Babies: Do Macroeconomic Experiences Affect Risk Taking? Q. J. Econ. 2011, 126, 373–416. [Google Scholar] [CrossRef]

- Rosen, H.S.; Wu, S. Portfolio choice and health status. J. Financ. Econ. 2004, 72, 457–484. [Google Scholar] [CrossRef] [Green Version]

- Guiso, L.; Sapienza, P.; Zingales, L. Does Local Financial Development Matter? Q. J. Econ. 2004, 119, 929–969. [Google Scholar] [CrossRef]

- Park, J.S.; Suh, D. Uncertainty and household portfolio choice: Evidence from South Korea. Econ. Lett. 2019, 180, 21–24. [Google Scholar] [CrossRef]

- Perraudin, W.R.M. Inflation and Portfolio Choice. Staff Pap. -Int. Monet. Fund 1987, 34, 739. [Google Scholar] [CrossRef]

- Wang, N. Optimal consumption and asset allocation with unknown income growth. J. Monet. Econ. 2009, 56, 524–534. [Google Scholar] [CrossRef] [Green Version]

- Yin, Z.; Wu, Y.; Gan, L. Financial availability, financial market participation and household portfolio choice. Econ. Res. J. 2015, 50, 87–99. [Google Scholar]

- Yao, Y. The Development of the Land Lease Market in Rural China. Land Econ. 2000, 76, 252. [Google Scholar] [CrossRef]

- Gao, L.; Huang, J.; Rozelle, S. Rental markets for cultivated land and agricultural investments in China. Agric. Econ. 2012, 43, 391–403. [Google Scholar] [CrossRef]

- Xu, L.; Du, X. Land certification, rental market participation, and household welfare in rural China. Agric. Econ. 2021, 53, 52–71. [Google Scholar] [CrossRef]

- Kung, J.K.S.; Shimokawa, S. Land Reallocations, Passive Land Rental, and the Development of Rental Markets in Rural China; AgEcon Search: Foz do Iguacu, Brazil, 18 August 2012. [Google Scholar] [CrossRef]

- Wang, Y.; Li, X.; Li, W.; Tan, M. Land titling program and farmland rental market participation in China: Evidence from pilot provinces. Land Use Policy 2018, 74, 281–290. [Google Scholar] [CrossRef]

- Yang, X.; Wang, J.; Wills, I. Economic growth, commercialization, and institutional changes in rural China, 1979–1987. China Econ. Rev. 1992, 3, 1–37. [Google Scholar] [CrossRef]

- Huang, Z.; Zhou, J.; Huang, X. Does the transfer of farmland use rights increase farmers’ long-term intention to work in cities? Econ. Transit. Inst. Change 2021, 30, 373–392. [Google Scholar] [CrossRef]

- Vranken, L.; Swinnen, J. Land rental markets in transition: Theory and evidence from Hungary. World Dev. 2006, 34, 481–500. [Google Scholar] [CrossRef]

- Chang, H.; Dong, X.-Y.; MacPhail, F. Labor Migration and Time Use Patterns of the Left-behind Children and Elderly in Rural China. World Dev. 2011, 39, 2199–2210. [Google Scholar] [CrossRef]

- Feng, S.; Heerink, N.; Ruben, R.; Qu, F. Land rental market, off-farm employment and agricultural production in Southeast China: A plot-level case study. China Econ. Rev. 2010, 21, 598–606. [Google Scholar] [CrossRef]

- Jin, S.; Jayne, T.S. Land Rental Markets in Kenya: Implications for Efficiency, Equity, Household Income, and Poverty. Land Econ. 2013, 89, 246–271. [Google Scholar] [CrossRef]

- Yan, X.; Huo, X. Drivers of household entry and intensity in land rental market in rural China: Evidence from North Henan Province. China Agric. Econ. Rev. 2016, 8, 345–364. [Google Scholar] [CrossRef]

- Gao, L.; Sun, D.; Ma, C. The Impact of Farmland Transfers on Agricultural Investment in China: A Perspective of Transaction Cost Economics. China World Econ. 2019, 27, 93–109. [Google Scholar] [CrossRef] [Green Version]

- Ji, Y.; Yu, X.; Zhong, F. Machinery investment decision and off-farm employment in rural China. China Econ. Rev. 2012, 23, 71–80. [Google Scholar] [CrossRef] [Green Version]

- Qian, L.; Lu, H.; Gao, Q.; Lu, H. Household-owned farm machinery vs. outsourced machinery services: The impact of agricultural mechanization on the land leasing behavior of relatively large-scale farmers in China. Land Use Policy 2022, 115, 106008. [Google Scholar] [CrossRef]

- Bielecki, T.R.; Pliska, S.R.; Sherris, M. Risk sensitive asset allocation. J. Econ. Dyn. Control 2000, 24, 1145–1177. [Google Scholar] [CrossRef]

- Li, R.; Wang, T.; Zhou, M. Entrepreneurship and household portfolio choice: Evidence from the China Household Finance Survey. J. Empir. Financ. 2020, 60, 1–15. [Google Scholar] [CrossRef]

- Kimball, M. Precautionary Motives for Holding Assets; NBER Working Papers; National Bureau of Economic Research, Inc.: Cambridge, MA, USA, 1991; p. 3586. [Google Scholar] [CrossRef]

- Fei, C.; Weijuan, Z. Land Transfer Incentive and Welfare Effect Research from Perspective of Farmers’ Behavior. Econ. Res. J. 2015, 50, 163–177. [Google Scholar]

- Peng, K.; Yang, C.; Chen, Y. Land transfer in rural China: Incentives, influencing factors and income effects. Appl. Econ. 2020, 52, 5477–5490. [Google Scholar] [CrossRef]

- Udimal, T.B.; Liu, E.; Luo, M.; Li, Y. Examining the effect of land transfer on landlords’ income in China: An application of the endogenous switching model. Heliyon 2020, 6, e05071. [Google Scholar] [CrossRef] [PubMed]

- Zhonghao, Q.; Xingwen, W. How does the transfer of farmland promote the increase of farmers’ income. Chin. Rural. Econ. 2016, 10, 39–50. [Google Scholar]

- Zhang, D.; Wang, W.; Zhou, W.; Zhang, X.; Zuo, J. The effect on poverty alleviation and income increase of rural land consolidation in different models: A China study. Land Use Policy 2020, 99, 104989. [Google Scholar] [CrossRef]

- Guiso, L.; Jappelli, T.; Terlizzese, D. Income Risk, Borrowing Constraints, and Portfolio Choice. Am. Econ. Rev. 1996, 86, 158–172. Available online: http://www.jstor.org/stable/2118260 (accessed on 11 September 2022).

- Xingqiang, H.; Wei, S.; Kaiguo, Z. Background Risk and Investors’ Participation in Risky Financial Assets. Econ. Res. J. 2009, 44, 119–130. [Google Scholar]

- Cong, S. The Impact of Agricultural Land Rights Policy on the Pure Technical Efficiency of Farmers’ Agricultural Production: Evidence from the Largest Wheat Planting Environment in China. J. Environ. Public Health 2022, 2022, 3487014. [Google Scholar] [CrossRef]

- Najafi, B.; Dastgerduei, S.T. Optimization of Machinery Use on Farms with Emphasis on Timeliness Costs. J. Agric. Sci. Technol. 2015, 17, 533–541. [Google Scholar] [CrossRef]

- Aiyagari, S.R. Uninsured Idiosyncratic Risk and Aggregate Saving. Q. J. Econ. 1994, 109, 659–684. [Google Scholar] [CrossRef] [Green Version]

- Berkowitz, M.K.; Qiu, J. A further look at household portfolio choice and health status. J. Bank. Financ. 2006, 30, 1201–1217. [Google Scholar] [CrossRef]

- Fan, E.; Zhao, R. Health status and portfolio choice: Causality or heterogeneity? J. Bank. Financ. 2009, 33, 1079–1088. [Google Scholar] [CrossRef]

- Heckman, J.J.; Ichimura, H.; Todd, P. Matching As An Econometric Evaluation Estimator. Rev. Econ. Stud. 1998, 65, 261–294. [Google Scholar] [CrossRef]

- Yogo, M. Portfolio choice in retirement: Health risk and the demand for annuities, housing, and risky assets. J. Monet. Econ. 2016, 80, 17–34. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Arthi, V.; Fenske, J. Intra-household labor allocation in colonial Nigeria. Explor. Econ. Hist. 2016, 60, 69–92. [Google Scholar] [CrossRef] [Green Version]

- Hennessy, T.; O’Brien, M. Is Off-Farm Income Driving On-Farm Investment? J. Farm Manag. 2008, 13, 235–246. Available online: https://ideas.repec.org/p/tea/wpaper/0704.html (accessed on 17 September 2022).

- Zhao, Y. Causes and Consequences of Return Migration: Recent Evidence from China. J. Comp. Econ. 2002, 30, 376–394. [Google Scholar] [CrossRef]

- Ampudia, M.; Ehrmann, M. Macroeconomic experiences and risk taking of euro area households. Eur. Econ. Rev. 2017, 91, 146–156. [Google Scholar] [CrossRef] [Green Version]

- Huang, K.; Deng, X.; Liu, Y.; Yong, Z.; Xu, D. Does off-Farm Migration of Female Laborers Inhibit Land Transfer? Evidence from Sichuan Province, China. Land 2020, 9, 14. [Google Scholar] [CrossRef] [Green Version]

- Gao, J.; Song, G.; Sun, X. Does labor migration affect rural land transfer? Evidence from China. Land Use Policy 2020, 99, 105096. [Google Scholar] [CrossRef]

- Becerril, J.; Abdulai, A. The Impact of Improved Maize Varieties on Poverty in Mexico: A Propensity Score-Matching Approach. World Dev. 2010, 38, 1024–1035. [Google Scholar] [CrossRef]

- Heckman, J.J.; Ichimura, H.; Todd, P.E. Matching As An Econometric Evaluation Estimator: Evidence from Evaluating a Job Training Programme. Rev. Econ. Stud. 1997, 64, 605–654. [Google Scholar] [CrossRef]

- Lechner, M. Program Heterogeneity and Propensity Score Matching: An Application to the Evaluation of Active Labor Market Policies. Rev. Econ. Stat. 2002, 84, 205–220. [Google Scholar] [CrossRef]

- Rosenbaum, P.R.; Rubin, D.B. Constructing a Control Group Using Multivariate Matched Sampling Methods That Incorporate the Propensity Score. Am. Stat. 1985, 39, 33. [Google Scholar] [CrossRef]

- Ayalew, H.; Admasu, Y.; Chamberlin, J. Is land certification pro-poor? Evidence from Ethiopia. Land Use Policy 2021, 107, 105483. [Google Scholar] [CrossRef]

- Ye, J.; Hongbin, L. Informal Finance and Farmers’ Borrowing Behaviors. J. Financ. Res. 2009, 4, 63–79. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variables | Definition and of Variables | 2013 Mean | 2015 Mean |

|---|---|---|---|

| Total assets | Total present value of financial assets and non-financial assets owned by households (CNY 10,000 a) | 25.3768 | 27.1686 |

| Non-financial assets | Total present value of non-financial assets owned by households, such as agricultural equipment, vehicles, consumer durables, housing, business and other nonfinancial assets (CNY 10,000 a) | 23.2196 | 25.1524 |

| Agricultural assets | Total present value of the agricultural special equipment owned by households (CNY 10,000 a) | 0.1607 | 0.2476 |

| Vehicle assets | Total present value of vehicles owned by households, such as bus and car (CNY 10,000 a) | 0.9212 | 1.1511 |

| Durable goods assets | Total present value of consumer durables owned by households, such as TV, refrigerator and washing machine (CNY 10,000 a) | 0.7031 | 0.9161 |

| Housing assets | Total present value of residential houses and commercial houses owned by households (CNY 10,000 a) | 12.7032 | 16.5975 |

| Business and others assets | Total present value of business assets and others non-financial assets owned by households (CNY 10,000 a) | 0.2045 | 1.0397 |

| Share of financial assets | Share of financial assets within assets (%) | 0.1273 | 0.0941 |

| Incidence of risky asset holdings | Whether the household have hold risky financial assets (1 = yes; 0 = no) | 0.0843 | 0.1034 |

| Share of risky assets | Share of risky assets within the financial assets (%) | 0.1454 | 0.1642 |

| Share of safe assets | Share of safe assets within the financial assets (%) | 0.5504 | 0.7270 |

| Farmland tenancy | Whether the household have participated in the farmland rental market and rent in farmland (1 = yes; 0 = no) | 0 | 0.1175 |

| Head age | The age of head of household is divided into six groups and five dummies are created, under 30 years old, 30~40 years old, 40~50 years old, 50~60 years old, 60~70 years old, and over 70 years old. When the head age is within the interval, the corresponding dummy is 1, otherwise it is 0. the group under the age of 30 is used as the benchmark. | – | – |

| Head age 30~40 | The age of head of household is between 30 years and 40 years, and includes 40 years (1 = Yes; 0 = No) | 0.0923 | 0.0695 |

| Head age 40~50 | The age of head of household is between 40 years and 50 years, and includes 50 years (1 = Yes; 0 = No) | 0.2792 | 0.2374 |

| Head age 50~60 | The age of head of household is between 50 years and 60 years, and includes 60 years (1 = Yes; 0 = No) | 0.2797 | 0.2839 |

| Head age 60~70 | The age of head of household is between 60 years and 70 years, and includes 70 years (1 = Yes; 0 = No) | 0.2426 | 0.2810 |

| Head age above the age of 70 | The age of head of household is above 70 years (1 = Yes; 0 = No) | 0.0881 | 0.1148 |

| Head gender | The gender of head of household (1 = male; 0 = female) | 0.8993 | 0.890 |

| Head marriage | Marital status of the head of household (1 =married, cohabitation and separation; 0 = no) | 0.9189 | 0.9117 |

| Head education | The education attained of head of household, 1~4 indicating never attended school, primary and junior high school, high school, college and above, respectively | 1.9960 | 1.9941 |

| Head farming | Whether the head of household has been farming (1 = yes; 0 = no) | 0.7012 | 0.6003 |

| Wealth | The total net wealth owned by the household, that is, the difference between the total assets and liabilities (CNY 10,000 a) | 23.3990 | 25.1111 |

| Wealth squared | The square of the net wealth owned by the household | 2651.52 | 2376.13 |

| Laborers | Number of household laborers aged between 18 and 60 years | 2.5845 | 2.3055 |

| Children | Number of children under the age of 16 | 0.7467 | 0.7655 |

| Farmland asset b | Total present value of contractual farmland owned by households (CNY 10,000 a) | 1.3642 | 1.0960 |

| Non-farm income b | Per capita non-farm employment income of households (CNY 10,000 a) | 0.2356 | 0.2619 |

| Business | Whether the household have been running business (1 = yes; 0 = no) | 0.0794 | 0.0977 |

| Risk aversion | Household’s level of risk aversion, 1~5 representing risk aversion from low to high, measured by the inquiry which investment project the household is more willing to choose if a funds is used for investment | 1.8138 | 1.4821 |

| Financial literacy | Financial literacy levels of household head, 1~3 representing financial literacy from low to high | 1.8001 | 1.7185 |

| Urban income b | Per capita urban income of the province in the then year (CNY 10,000 a) | 1.2203 | 1.3392 |

| Rent-in rate | Proportion of households rent-in land in the sample area | 0.1374 | 0.2548 |

| Rent-out rate | Proportion of households rent-out land in the sample area | 0.1440 | 0.3096 |

| Variables | Control Group A (Non-Participants/Non-Tenants) | Treated Group B (Participants/Tenants) | Difference in Mean (B2−B1) − (A2−A1) | |||

|---|---|---|---|---|---|---|

| Ex-Ante A1 | Ex-Post A2 | Ex-Ante B1 | Ex-Post B2 | |||

| Mean | Mean | Mean | Mean | Mean | t-Value | |

| Total assets | 25.3474 | 26.1899 | 23.0761 | 29.1664 | 5.2478 *** | 3.2083 |

| Non-financial assets | 23.2533 | 24.2916 | 21.1453 | 27.0075 | 1.6125 *** | 2.9916 |

| Agricultural assets | 0.1564 | 0.2366 | 0.2961 | 0.4866 | 0.1103 ** | 2.0992 |

| Vehicle assets | 0.9240 | 1.0459 | 0.8393 | 1.7000 | 0.7388 *** | 3.3206 |

| Durable goods assets | 0.5438 | 0.6908 | 0.5074 | 0.7610 | 0.1067 *** | 2.9135 |

| Housing assets | 12.4798 | 15.9908 | 10.5937 | 16.4176 | 2.3129 ** | 2.0839 |

| Business and others assets | 0.6196 | 1.1904 | 0.1414 | 2.2889 | 1.5766 *** | 3.2967 |

| Share of financial assets | 0.1265 | 0.0905 | 0.1320 | 0.0993 | 0.0032 | 0.4435 |

| Incidence of risky asset holdings | 0.0807 | 0.0944 | 0.0979 | 0.1235 | 0.012 | 0.9625 |

| Share of risky assets | 0.0309 | 0.0406 | 0.0386 | 0.0623 | 0.0135 ** | 2.0987 |

| Share of safe assets | 0.05631 | 0.7311 | 0.5396 | 0.7204 | 0.0145 | 0.8064 |

| Variables | Estimated Coefficients | S.E. |

|---|---|---|

| Head age 30~40 | −0.6707 * | 0.3889 |

| Head age 40~50 | −0.4682 | 0.3616 |

| Head age 50~60 | −0.5910 | 0.3633 |

| Head age 60~70 | −0.7895 ** | 0.3702 |

| Head age above the age of 70 | −0.8173 ** | 0.4099 |

| Head gender | 0.2035 | 0.1947 |

| Head marriage | 0.4609 * | 0.2410 |

| Head education | −0.2964 ** | 0.1153 |

| Head farming | 0.5459 *** | 0.1410 |

| Wealth | −0.0025 | 0.0024 |

| Wealth squared | 0.0000 | 0.0000 |

| Labors | 0.0699 * | 0.0493 |

| Children | 0.0569 | 0.0615 |

| Farmland asset a | −0.0385 | 0.0491 |

| Non-farm income a | −0.1016 | 0.1876 |

| Business | −0.2876 | 0.2261 |

| Risk aversion | 0.0058 | 0.0445 |

| Financial literacy | 0.0316 | 0.0471 |

| Urban income a | −0.2912 | 0.5240 |

| Rent-in rate | 1.2187 ** | 0.4833 |

| Rent-out rate | 0.1735 | 0.4021 |

| Constant | −1.8597 ** | 0.8260 |

| Observations | 3650 | |

| Prob > chi2 | 0.0000 | |

| Pseudo | 0.0250 | |

| Variables | Unmatched Mean | Matched Mean | ||||||

|---|---|---|---|---|---|---|---|---|

| Participants | Non-Participants | Bias (%) | t-Test: p Value | Participants | Non-Participants | Bias (%) | t-Test: p Value | |

| Head age 30~40 | 0.0863 | 0.0969 | −3.7 | 0.481 | 0.0863 | 0.0943 | −2.8 | 0.680 |

| Head age 40~50 | 0.3170 | 0.2811 | 7.9 | 0.121 | 0.3170 | 0.2882 | 6.3 | 0.358 |

| Head age 50~60 | 0.2914 | 0.2826 | 1.9 | 0.705 | 0.2914 | 0.2897 | 0.4 | 0.957 |

| Head age 60~70 | 0.2192 | 0.2410 | −5.2 | 0.318 | 0.2192 | 0.2373 | −4.3 | 0.527 |

| Head age above the age of 70 | 0.0629 | 0.0804 | −6.8 | 0.205 | 0.0629 | 0.0731 | −3.9 | 0.554 |

| Head gender | 0.9161 | 0.8966 | 6.7 | 0.208 | 0.9161 | 0.9059 | 3.5 | 0.600 |

| Head marriage | 0.9511 | 0.9168 | 13.8 | 0.014 | 0.9511 | 0.9351 | 6.4 | 0.313 |

| Head education | 1.9464 | 2.0059 | −11.8 | 0.025 | 1.9464 | 1.9883 | −8.3 | 0.214 |

| Head farming | 0.8159 | 0.7019 | 26.9 | 0.000 | 0.8159 | 0.7570 | 13.9 | 0.036 |

| Wealth | 21.058 | 23.412 | −4.9 | 0.326 | 21.058 | 21.552 | −1.0 | 0.874 |

| Wealth squared | 2979 | 2675.7 | 0.9 | 0.840 | 2979 | 2058.8 | 2.7 | 0.676 |

| Laborers | 2.7762 | 2.5932 | 14.8 | 0.004 | 2.7762 | 2.6670 | 8.8 | 0.192 |

| Children | 0.8345 | 0.7553 | 7.5 | 0.119 | 0.8345 | 0.7712 | 6.0 | 0.384 |

| Farmland asset a | 1.2891 | 1.3722 | −7.1 | 0.185 | 1.2891 | 1.3451 | −4.8 | 0.482 |

| Non-farm income a | 0.2128 | 0.2324 | −6.0 | 0.248 | 0.2128 | 0.2243 | −3.5 | 0.601 |

| Business | 0.0559 | 0.0780 | −8.8 | 0.105 | 0.0559 | 0.0678 | −4.7 | 0.472 |

| Risk aversion | 1.8298 | 1.8155 | 1.2 | 0.815 | 1.8298 | 1.8151 | 1.2 | 0.856 |

| Financial literacy | 1.8322 | 1.8009 | 2.8 | 0.584 | 1.8322 | 1.8093 | 2.0 | 0.768 |

| Urban income a | 1.2056 | 1.2187 | −12.5 | 0.021 | 1.2056 | 1.2136 | −7.7 | 0.250 |

| Rent-in rate | 0.1515 | 0.1335 | 16.5 | 0.001 | 0.1515 | 0.1345 | 15.6 | 0.020 |

| Rent-out rate | 0.1446 | 0.1381 | 4.7 | 0.347 | 0.1446 | 0.137 | 5.5 | 0.419 |

| sample | Pseudo | LR chi2 | Mean Bias | |||||

| Unmatched | 0.025 | 65.50 | 0.000 | 8.2 | ||||

| Matched | 0.016 | 19.52 | 0.552 | 5.4 | ||||

| Dependent Variable | PSM-DID with KM a | PSM-DID with LLRM b | ||

|---|---|---|---|---|

| Difference | S.E. c | Difference | S.E. c | |

| Total assets | 4.3806 | 2.8236 | 4.5547 | 2.9980 |

| Non-financial assets | 4.0042 | 2.9987 | 4.1635 | 2.7332 |

| Agricultural assets | 0.1050 | 0.0862 | 0.0849 | 0.0748 |

| Vehicle assets | 0.6918 | 0.4467 | 0.9207 * | 0.4956 |

| Durable goods assets | 0.1111 ** | 0.0563 | 0.1169 ** | 0.0530 |

| Housing assets | 2.1003 * | 1.1529 | 2.2979 * | 1.1729 |

| Business and others assets | 1.5196 | 1.3630 | 1.5759 | 1.3095 |

| Share of financial assets | 0.0030 | 0.0104 | 0.0058 | 0.0108 |

| Incidence of risky asset holdings | 0.0055 | 0.0182 | 0.0088 | 0.0194 |

| Share of risky assets | 0.0101 | 0.0105 | 0.0110 | 0.0127 |

| Share of safe assets | 0.0121 | 0.0241 | 0.0063 | 0.0232 |

| Dependent Variable | PSM-DID with KM a | PSM-DID with LLRM b | ||||||

|---|---|---|---|---|---|---|---|---|

| Low Intensity | High Intensity | Low Intensity | High Intensity | |||||

| Difference | S.E. c | Difference | S.E. c | Difference | S.E. c | Difference | S.E. c | |

| Total assets | 1.2652 | 3.0609 | 14.3016 ** | 6.5076 | 1.2105 | 3.0954 | 14.2749 ** | 6.9391 |

| Non-financial assets | 1.2097 | 3.2643 | 12.9086 ** | 6.4492 | 1.0763 | 3.3281 | 12.9480 ** | 5.4560 |

| Agricultural assets | −0.0891 | 0.0677 | 0.7462 *** | 0.2790 | −0.0933 | 0.0647 | 0.6927 *** | 0.2453 |

| Vehicle assets | 0.3101 | 0.3815 | 2.0151 | 1.4469 | 0.5389 | 0.3544 | 2.1476 | 1.4539 |

| Durable goods assets | 0.0776 * | 0.0532 | 0.2260 | 0.1707 | 0.0920 * | 0.0561 | 0.2104 * | 0.1269 |

| Housing assets | 2.4030 * | 1.2567 | 0.7662 | 2.4127 | 2.3870 * | 1.2579 | 1.2871 | 2.4406 |

| Business and others assets | −0.1593 | 0.2316 | 6.9779 | 5.9921 | −0.0689 | 0.2131 | 7.0405 | 6.2871 |

| Share of financial assets | −0.0030 | 0.0124 | 0.0197 | 0.0155 | 0.0027 | 0.0122 | 0.0160 | 0.0124 |

| Incidence of risky asset holdings | −0.0172 | 0.0194 | 0.0786 ** | 0.0393 | −0.0127 | 0.0203 | 0.0720 ** | 0.0379 |

| Share of risky assets | −0.0042 | 0.0112 | 0.0558 * | 0.0298 | −0.0037 | 0.0109 | 0.0559 * | 0.0352 |

| Share of safe assets | 0.0253 | 0.0290 | −0.0241 | 0.0522 | 0.0166 | 0.0275 | −0.0254 | 0.0663 |

| Variables | Difference | |||||

|---|---|---|---|---|---|---|

| PSM-DID with KM a | PSM-DID with LLRM b | |||||

| The Overall | Low Intensity | High Intensity | The Overall | Low Intensity | High Intensity | |

| Household income d | 0.1527 | −0.1111 | 0.9967 | −0.0664 | −0.2074 | 0.7353 |

| (0.2815) | (0.2722) | (0.8518) | (0.3102) | (0.2501) | (0.9655) | |

| Incidence of household in debt owing to agricultural production | 0.0292 | 0.0345 | 0.0133 | 0.0394 | 0.0516 * | 0.0231 |

| (0.0258) | (0.0280) | (0.0563) | (0.0274) | (0.0279) | (0.0644) | |

| Household liabilities owing to agricultural production d | 0.3297 *** | 0.2249 ** | 0.6694 *** | 0.3283 *** | 0.2289 ** | 0.6522 ** |

| (0.1156) | (0.1109) | (0.3251) | (0.1150) | (0.1096) | (0.3193) | |

| The level of the household overall liabilities d | 0.1723 | 0.2676 | −0.2183 | 0.1983 | 0.2601 | −0.0999 |

| (0.3120) | (0.3086) | (0.6959) | (0.2751) | (0.3151) | (0.7257) | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Xu, L.; Chandio, A.A.; Wang, J.; Jiang, Y. Does Farmland Tenancy Improve Household Asset Allocation? Evidence from Rural China. Land 2023, 12, 98. https://doi.org/10.3390/land12010098

Xu L, Chandio AA, Wang J, Jiang Y. Does Farmland Tenancy Improve Household Asset Allocation? Evidence from Rural China. Land. 2023; 12(1):98. https://doi.org/10.3390/land12010098

Chicago/Turabian StyleXu, Lijuan, Abbas Ali Chandio, Jingyi Wang, and Yuansheng Jiang. 2023. "Does Farmland Tenancy Improve Household Asset Allocation? Evidence from Rural China" Land 12, no. 1: 98. https://doi.org/10.3390/land12010098