Strategic Information Suppression in Borrowing and Pre-Lending Cognition: Theory and Evidence †

Abstract

:“Good morning, Jordan Belfort with Investors’ Center in New York City. The reason I’m calling is that an extremely exciting investment opportunity crossed my desk today. Typically our firm recommends no more than five stocks per year: this is one of them. Aerotyne International is a cutting-edge tech firm out of the Midwest, awaiting imminent patent approval on a new generation of radar equipment…”Jordan Belfort in “The Wolf of Wall Street” (2013)

1. Introduction

Literature

2. Model

2.1. The Setup

- Stage 1: Nature moves.

- Stage 2: Borrower’s announcing stage.

- Stage 3: Lender’s cognition stage.

- Stage 4: Contracting stage.

“… what is needed… is to hold the seller liable for failures to reveal promptly not only the verifiable information that the seller knew, but also the information that it should have known under the circumstances.”

2.2. Analysis

2.3. Robustness

2.4. Welfare Comparative Statics

3. Evidence

3.1. Data Description

3.2. Empirical Analysis

4. Concluding Remarks

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

Appendix A.1. Equilibrium Loan Amount p When t < h

Appendix A.2. An Infinite-Horizon Bargaining Game Where the Lender Makes All the Offers

Appendix A.3. Multiple Lenders in the Pooling Equilibrium

Appendix A.4. The Case Where Assumption 1 Fails

Appendix A.5. Proof of Proposition 2

| 1 | Since 2013, the Financial Conduct Authority, taking over the responsibility of the Financial Services Authority, has created an alternative regulatory framework for both retail and wholesale financial services. |

| 2 | See Informed decisions? How consumers use Key Features: a synthesis of research on the use of product information at the point of sale, Financial Services Authority, November 2000. |

| 3 | See the article “Troubled Securities in Asia” in The Economist, 20 November 2008. |

| 4 | See the full story of Fanya: http://www.metalbulletin.com/fanya, accessed on 16 September 2022. |

| 5 | See http://letscrowdsmarter.com/ezubao-scam/, accessed on 16 September 2022. |

| 6 | See https://www.scmp.com/economy/china-economy/article/3115580/chinas-p2p-purge-leaves-millions-victims-out-cold-losses, accessed on 16 September 2022. |

| 7 | Benabou and Tirole [7] investigate how memory bias in equilibrium depends on the individual’s degree of present bias, while Tirole [8] studies how contractual incompleteness in equilibrium depends on parties’ cognitive capacity, time preference, the extent of hold-up problem, and bargaining power. Although two papers appear to be in different fields, regarding the approach, the former focuses on how one party influences the information structure of the other party, whereas the latter sheds light on how one party refines his own information structure. In our paper, we combine both issues in one model, and study how one party’s signal-jamming interacts with the other party’s information acquisition. |

| 8 | |

| 9 | The information advantage for borrowers is common in situations where borrowers understand their financial situation, loan purpose and repayment ability, and thus gain a detailed understanding of the appropriateness of the application. |

| 10 | Here, type-A borrower as a “good-type” agent has no signaling device at all. |

| 11 | This feature qualitatively differentiates our paper from Benabou and Tirole [7] in which the uninformed party’s information acquisition is absent. |

| 12 | If the borrower has the full bargaining power, there is no pure-strategy cognition in equilibrium. In addition, similar to footnote 13 in Tirole [8], since the lender exerts the cognitive efforts before contracting, off the equilibrium path, if the lender exerts less cognitive efforts the lender will reject the contract proposed by the borrower. Thus the payoff function of the lender is not smooth at the optimal cognitive level in the hypothetical equilibrium. Moreover, an arbitrary balance of bargaining power in Tirole still involves bargaining with symmetric information, whereas our model would incorporate both signaling and screening, and bargaining with asymmetric information is thereby beyond the scope of this paper, as a technical reason. |

| 13 | Of course, after the borrower reveals the cost of understanding for the lender is not zero in reality. However, it should be much lower than the cost of learning by the lender alone. Thus, without loss of generality, we normalize the cost of understanding to zero. Further, the borrower may manipulate the understanding cost for the lender, i.e., by disclosing the eye-opening information only by lender’s request. In this case, we would rather interpret the borrower’s behavior as strategic information suppression (announcing A). |

| 14 | Besides the fine from the regulator, it is also natural to assume that the lender can sue the borrower and receive an additional transfer of T after the rest of the funded amounts turn out to be an uncollectible debt. Thus, the total penalty from information suppression is if the lender can provide the default notice. However, assuming a difference of the punishment amounts for uncollectible debt does not change our results qualitatively. Thus, for simplicity, we let . |

| 15 | We consider the case of multiple lenders in Appendix A.3 where an individual lender’s cognition may be reduced as a free-riding result. |

| 16 | The lender may consider the commitment of a fund-amount depending on the borrower’s announcement. However, since both the lender’s surprise and loss from are not contractible, we rule out the possibility of a contingent loan amount. |

| 17 | In Appendix A.4, we show that if this assumption fails, there is even no equilibrium in which the lender strictly prefers to contracting with only type- borrower or proposing nothing. |

| 18 | The negative result is akin to the Grossman-Stiglitz paradox, which says that there is no pure-strategy equilibrium of loan amount when acquiring quality-information is costly for consumers in the market (see Grossmann and Stiglitz, 1980) [42]. |

| 19 | Pooling equilibrium occurs if and only if

By strict convexity of , it is also equivalent to

|

| 20 | The feature of semi-separating equilibrium smacks of an inspection game. The lender is the counterpart of an inspector, and the borrower is the counterpart of an inspectee [43]. Nevertheless, they have some substantial differences. First, in our model, there are heterogeneous borrowers, and it is impossible for type-A borrower to suppress information. Hence, when the fraction of type-A borrower, namely , is high, there exists a pure-strategy equilibrium that is a pooling one. Second, there are two types of errors for the inspector in the statistical parlance. However, our model excludes the lender’s type I error, since describing implies that is appropriate. |

| 21 | Alternatively, we can reinterpret diversely unaware lenders as heterogeneous cognitive cost functions. One is as before. The other is such that and for where is a sufficiently large constant. The lender with the later function will never think and always contracts with the borrower as long as Assumption 1 is satisfied. Hence, there is no behavioral difference between these two interpretations, although the beliefs of the lenders in two interpretations are different. Thus, we can model completely unaware lenders “as-if” their cognitive costs are significantly high (see, e.g., Friedman (1953) [44] for the “as-if” justification.). |

| 22 | It is worth mentioning that the results in Proposition 2 are robust to the more general case with a direct dead-weight loss of information suppression . To see it, let the transaction cost be where is the expected welfare loss from information suppression. It is straightforward to see that and in the pooling equilibrium. In the semi-separating equilibrium, since is lower for a higher as shown in Appendix A.5, we still have that . Further, the sign of is ambiguous as well. Lastly, q is decreasing in so remains. |

| 23 | Data Availability Statement: A publicly available dataset was analyzed in this study. This dataset can be found here: https://doi.org/10.17632/wb3ndt69gf.3 (accessed on 16 September 2022). |

| 24 | See Korobkin (2003) [46] and Becher (2008). |

| 25 | Note that the pooling result is renegotiation-proof. |

References

- Gabaix, X.; Laibson, D. Shrouded Attributes, Consumer Myopia, and Information Suppression in Competitive Markets. Q. J. Econ. 2006, 121, 505–540. [Google Scholar] [CrossRef]

- Inderst, R.; Ottaviani, M. (Mis)selling through Agents. Am. Econ. Rev. 2009, 99, 883–908. [Google Scholar] [CrossRef]

- Inderst, R.; Ottaviani, M. How (Not) to Pay for Advice: A Framework for Consumer Financial Protection. J. Financ. Econ. 2012, 105, 393–411. [Google Scholar] [CrossRef]

- Gui, Z.; Huang, S.; Zhao, X. Financial Fraud and Investor Awareness; Monash Economics Working Papers 2021-06; Monash University, Department of Economics: Clayton, VIC, Australia, 2021. [Google Scholar]

- Williamson, O. The Economic Institutions of Capitalism: Firms, Markets, Relational Contracting; Free Press: New York, NY, USA, 1985. [Google Scholar]

- Hayek, F. The Use of Knowledge in Society. Am. Econ. Rev. 1945, 4, 519–530. [Google Scholar]

- Benabou, R.; Tirole, J. Self-Confidence and Personal Motivation. Q. J. Econ. 2002, 117, 871–915. [Google Scholar] [CrossRef]

- Tirole, J. Cognition and Incomplete Contracts. Am. Econ. Rev. 2009, 99, 265–294. [Google Scholar] [CrossRef]

- Grossman, S.; Hart, O. The Costs and Benefits of Ownership: A Theory of Vertical and Lateral Integration. J. Political Econ. 1986, 94, 691–719. [Google Scholar] [CrossRef]

- Hart, O.; Moore, J. Property Rights and the Nature of the Firm. J. Political Econ. 1990, 98, 1119–1158. [Google Scholar] [CrossRef]

- Maskin, E.; Tirole, J. Unforeseen Contingencies and Incomplete Contracts. Rev. Econ. Stud. 1999, 66, 83–114. [Google Scholar] [CrossRef]

- Dye, R. Costly Contract Contingencies. Int. Econ. Rev. 1985, 26, 233–250. [Google Scholar] [CrossRef]

- Anderlini, L.; Felli, L. Incomplete Contracts and Complexity Costs. Theory Decis. 1999, 46, 23–50. [Google Scholar] [CrossRef]

- Battigalli, P.; Maggi, G. Rigidity, Discretion, and the Costs of Writing Contracts. Am. Econ. Rev. 2002, 92, 798–817. [Google Scholar] [CrossRef]

- Aghion, P.; Bolton, P. Contracts as a Barrier to Entry. Am. Econ. Rev. 1987, 77, 388–401. [Google Scholar]

- Spier, K. Incomplete Contracts and Signaling. Rand J. Econ. 1992, 23, 432–443. [Google Scholar] [CrossRef]

- Hermalin, B.; Katz, M. Judicial Modification of Contracts between Sophisticated Parties: A More Complete View of Incomplete Contracts and Their Breach. J. Law Econ. Organ. 1993, 9, 230–255. [Google Scholar]

- Bernheim, D.; Whinston, M. Incomplete Contracts and Strategic Ambiguity. Am. Econ. Rev. 1998, 88, 902–932. [Google Scholar]

- Dessi, R. Contractual Execution, Strategic Incompleteness and Venture Capital. IDEI Working Paper 2009, 465, 9–75. [Google Scholar]

- Simon, H. A Bahavioral Model of Rational Choice. In Models of Man: Social and Rational; John Wiley and Sons: New York, NY, USA, 1957. [Google Scholar]

- Bolton, P.; Faure-Grimaud, A. Satisficing Contracts. Rev. Econ. Stud. 2010, 77, 937–971. [Google Scholar] [CrossRef]

- Pavan, A.; Tirole, J. Exposure to the Unexpected, Duty of Disclosure, and Contract Design; Toulouse School of Economics: Toulouse, France, 2022. [Google Scholar]

- Kahneman, D.; Tversky, A. Availability: A Heuristic for Judging Frequency and Probability. Cogn. Psychol. 1973, 5, 207–232. [Google Scholar]

- Eliaz, K.; Spiegler, R. Contracting with Diversely Naive Agents. Rev. Econ. Stud. 2006, 73, 689–714. [Google Scholar] [CrossRef]

- Zhou, J. Advertising, Misperceived Preferences, and Product Design; Yale School of Management: New Haven, CT, USA, 2008. [Google Scholar]

- Li, S.; Peitz, M.; Zhao, X. Vertically Differentiated Duopoly with Unaware Consumers. Math. Soc. Sci. 2014, 70, 59–67. [Google Scholar] [CrossRef]

- Young, B. Misperception and Cognition in Markets. Games 2022, 13, 71. [Google Scholar] [CrossRef]

- Li, S.; Peitz, M.; Zhao, X. Information Disclosure and Consumer Awareness. J. Econ. Behav. Organ. 2016, 128, 209–230. [Google Scholar] [CrossRef]

- Gui, Z.; Hu, X. Cognition and Product Customization; Wuhan University: Wuhan, China, 2022. [Google Scholar]

- von Thadden, E.L.; Zhao, X. Incentives for Unaware Agents. Rev. Econ. Stud. 2012, 79, 1151–1174. [Google Scholar] [CrossRef]

- Auster, S. Asymmetric Awareness and Moral Hazard. Games Econ. Behav. 2013, 82, 503–521. [Google Scholar] [CrossRef]

- Auster, S.; Pavoni, N. Limited Awareness and Financial Intermediation; University of Bonn: Bonn, Germany, 2020. [Google Scholar]

- Auster, S.; Pavoni, N. Optimal Delegation and Information Transmission under Limited Awareness; University of Bonn: Bonn, Germany, 2021. [Google Scholar]

- Lei, H.; Zhao, X. Delegation and Information Disclosure with Unforeseen Contingencies. B.E. J. Theor. Econ. 2021, 21, 637–656. [Google Scholar] [CrossRef]

- Spence, A.M. Job Market Signaling. Q. J. Econ. 1973, 87, 355–374. [Google Scholar] [CrossRef]

- Crawford, V.; Sobel, J. Strategic Information Transmission. Econometrica 1982, 50, 1431–1451. [Google Scholar] [CrossRef]

- Grossman, S. The Informational Role of Warranties and Private Disclosure about Product Quality. J. Law Econ. 1981, 24, 461–483. [Google Scholar] [CrossRef]

- Milgrom, P. Good News and Bad News: Representation Theorems and Applications. Bell J. Econ. 1981, 12, 380–391. [Google Scholar] [CrossRef]

- Milgrom, P.; Roberts, J. Relying on the Information of Interested Parties. Rand J. Econ. 1986, 17, 18–32. [Google Scholar] [CrossRef]

- Milgrom, P. What the Seller Won’t Tell You: Persuasion and Disclosure in Markets. J. Econ. Perspect. 2008, 22, 115–131. [Google Scholar] [CrossRef]

- Akerlof, G. The Market for Lemons: Quality Uncertainty and the Market Mechanism. Q. J. Econ. 1970, 84, 488–500. [Google Scholar] [CrossRef]

- Grossman, S.; Stiglitz, J. On the Impossibility of Informationally Efficient Markets. Am. Econ. Rev. 1980, 70, 393–408. [Google Scholar]

- Avenhaus, R.; von Stengel, B.; Zamir, S. Inspection Games. In Handbook of Game Theory; Elsevier: Amsterdam, The Netherlands, 2002; Volume 3, pp. 1947–1987. [Google Scholar]

- Friedman, M. The Methodology of Positive Economics. In Essays in Positive Economics; Friedman, M., Ed.; University of Chicago Press: Chicago, IL, USA, 1953. [Google Scholar]

- Atkinson, A.; Mckay, S.; Collard, S.; Kempson, E. Levels of Financial Capability in the UK. Public Money Manag. 2007, 3, 29–36. [Google Scholar] [CrossRef]

- Korobkin, R. Bounded Rationality, Standard Form Contracts, and Unconscionability. Univ. Chic. Law Rev. 2003, 70, 1203–1295. [Google Scholar] [CrossRef]

- Pavan, A.; Tirole, J. Conformity in Strategic Cognition; Toulouse School of Economics: Toulouse, France, 2022. [Google Scholar]

{kind=link}

{kind=link}

| Variable | N | Mean | Std.Dev. | Min | Max |

|---|---|---|---|---|---|

| Panel A: Selected variables | |||||

| c (Loan Description) | 816,274 | 0.098 | 0.297 | 0 | 1 |

| h (Funded Amount) | 816,274 | 14,996.04 | 8445.824 | 1000 | 35,000 |

| (Grade Level) | 816,274 | 2.814 | 1.304 | 1 | 7 |

| Interest Rate | 816,274 | 0.133 | 0.044 | 0.0532 | 0.29 |

| Debt-To-Income Ratio | 816,274 | 18.457 | 8.314 | 0.01 | 39.99 |

| Panel B: Loan Proportions by Characteristic | |||||

| Frequency | Proportion of Loans | ||||

| Credit Grade | |||||

| A | 131,387 | 16.10% | |||

| B | 232,549 | 28.49% | |||

| C | 231,107 | 28.31% | |||

| D | 129,792 | 15.9% | |||

| E | 65,572 | 8.03% | |||

| F | 21,058 | 2.58% | |||

| G | 4809 | 0.59% | |||

| Loan Length | |||||

| 36 months | 566,558 | 69.41% | |||

| 60 months | 249,716 | 30.59% | |||

| Purpose of loans | |||||

| Car | 6650 | 0.81% | |||

| Credit Card | 195,374 | 23.93% | |||

| Debt Consolidation | 488,766 | 59.88% | |||

| Home Improvement | 46,860 | 5.74% | |||

| House | 2996 | 0.37% | |||

| Major Purchase | 14,110 | 1.73% | |||

| Medical | 7446 | 0.91% | |||

| Moving | 4545 | 0.56% | |||

| Other | 36,647 | 4.49% | |||

| Renewable Energy | 432 | 0.05% | |||

| Small Business | 7442 | 0.91% | |||

| Vacation | 4130 | 0.51% | |||

| Wedding | 876 | 0.11% | |||

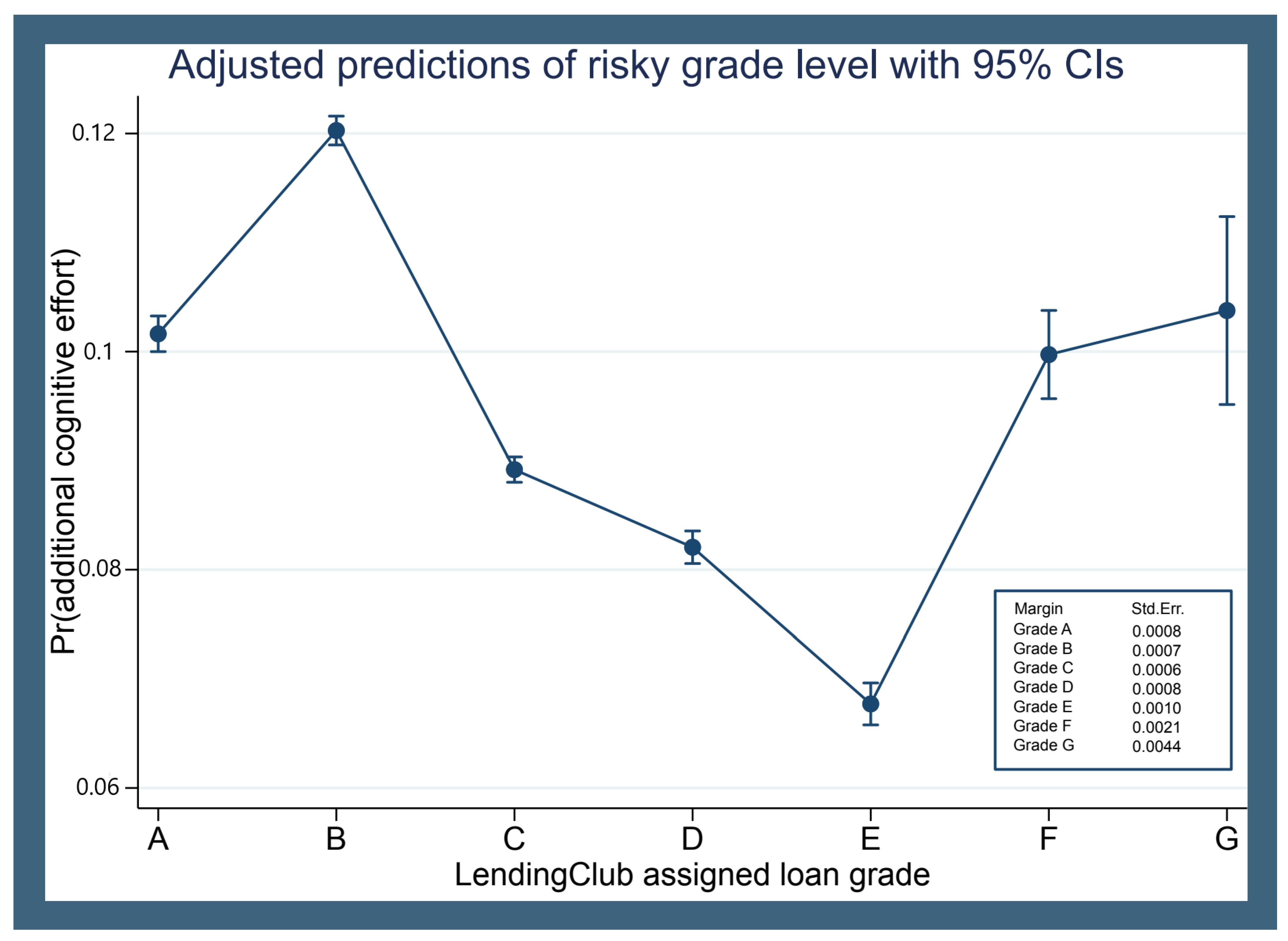

| VARIABLES | Pre-Lending Cognitive Effort | |||||

|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | |

| Grade A | 0.1016 *** | 0.1015 *** | 0.1017 *** | 0.1018 *** | ||

| (0.0008) | (0.0008) | (0.0008) | (0.0008) | |||

| Grade B | 0.1203 *** | 0.1207 *** | 0.1203 *** | 0.1207 *** | ||

| (0.0007) | (0.0007) | (0.0007) | (0.0007) | |||

| Grade C | 0.0892 *** | 0.0894 *** | 0.0893 *** | 0.0894 *** | ||

| (0.0006) | (0.0006) | (0.0006) | (0.0006) | |||

| Grade D | 0.0821 *** | 0.0821 *** | 0.0821 *** | 0.0819 *** | ||

| (0.0008) | (0.0008) | (0.0008) | (0.0008) | |||

| Grade E | 0.0677 *** | 0.067 *** | 0.0676 *** | 0.0668 *** | ||

| (0.0001) | (0.001) | (0.001) | (0.001) | |||

| Grade F | 0.0997 *** | 0.0983 *** | 0.0991 *** | 0.0978 *** | ||

| (0.0021) | (0.002) | (0.0021) | (0.0021) | |||

| Grade G | 0.1038 *** | 0.1014 *** | 0.1023 *** | 0.1003 *** | ||

| (0.0044) | (0.0043) | (0.0044) | (0.0043) | |||

| h (Funded Amount) | 0.0032 *** | 0.0054 *** | 0.0012 ** | 0.0041 *** | ||

| (0.0005) | (0.0005) | (0.0005) | (0.0005) | |||

| Credit Card | −0.0041 | −0.016 | −0.0065 * | |||

| (0.0037) | (0.0028) | (0.0038) | ||||

| Debt Consolidation | 0.0003 | −0.0034 | −0.002 | |||

| (0.0037) | (0.0038) | (0.0037) | ||||

| Home Improvement | −0.0053 | −0.0079 * | −0.0071 * | |||

| (0.0039) | (0.0039) | (0.0039) | ||||

| House | 0.0362 *** | 0.0255 *** | 0.0346 | |||

| (0.0073) | (0.0072) | (0.0074) | ||||

| Medical | −0.0398 *** | −0.0457 *** | −0.0401 *** | |||

| (0.0046) | (0.0046) | (0.0047) | ||||

| Moving | −0.0246 *** | −0.0345 *** | −0.0241 *** | |||

| (0.0054) | (0.0053) | (0.0055) | ||||

| Renewable Energy | −0.0019 | −0.0143 | −0.0016 | |||

| (0.0151) | (0.0141) | (0.0154) | ||||

| Small Business | 0.013 *** | −0.0005 | 0.0112 ** | |||

| (0.0053) | (0.0051) | (0.0053) | ||||

| Vacation | −0.0295 *** | −0.0361 *** | −0.0284 ** | |||

| (0.0054) | (0.0054) | (0.0056) | ||||

| Wedding | 0.2924 *** | 0.2719 *** | 0.2942 *** | |||

| (0.0169) | (0.0168) | (0.017) | ||||

| Regions Control | YES | YES | YES | YES | ||

| Observations | 816,274 | 816,274 | 816,274 | 816,274 | 816,274 | 816,274 |

| Cognitive Effort | Std. Err. | Observations | p Values | |

|---|---|---|---|---|

| Mean | ||||

| Panel A: Grade A versus Grade B: | 0.000 | |||

| Grade A | 0.1016 | (0.0008) | 131,387 | |

| Grade B | 0.1202 | (0.0007) | 232,549 | |

| Panel B: Grade A versus Grade C: | 0.000 | |||

| Grade A | 0.1016 | (0.0008) | 131,387 | |

| Grade C | 0.0892 | (0.0006) | 231,107 | |

| Panel C: Grade A versus Grade D: | 0.000 | |||

| Grade A | 0.1016 | (0.0008) | 131,387 | |

| Grade D | 0.0821 | (0.0008) | 129,792 | |

| Panel D: Grade A versus Grade E: | 0.000 | |||

| Grade A | 0.1016 | (0.0008) | 131,387 | |

| Grade E | 0.0677 | (0.001) | 65,572 | |

| Panel E: Grade A versus Grade F: | 0.3948 | |||

| Grade A | 0.1016 | (0.0008) | 131,387 | |

| Grade F | 0.0997 | (0.0021) | 21,058 | |

| Panel F: Grade A versus Grade G: | 0.6308 | |||

| Grade A | 0.1016 | (0.0008) | 131,387 | |

| Grade G | 0.1038 | (0.0044) | 4809 | |

| Panel G: Grade F versus Grade G: | 0.4006 | |||

| Grade F | 0.0997 | (0.0021) | 232,549 | |

| Grade G | 0.1038 | (0.0044) | 4809 | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chen, Z.; Zhao, X. Strategic Information Suppression in Borrowing and Pre-Lending Cognition: Theory and Evidence. Games 2023, 14, 43. https://doi.org/10.3390/g14030043

Chen Z, Zhao X. Strategic Information Suppression in Borrowing and Pre-Lending Cognition: Theory and Evidence. Games. 2023; 14(3):43. https://doi.org/10.3390/g14030043

Chicago/Turabian StyleChen, Zhongwen, and Xiaojian Zhao. 2023. "Strategic Information Suppression in Borrowing and Pre-Lending Cognition: Theory and Evidence" Games 14, no. 3: 43. https://doi.org/10.3390/g14030043