Innovation-Driven Policies, Corporate Governance Structure and Total Factor Productivity in Chinese Sports Sector: Evidence from Listed Sports Firms

Abstract

:1. Introduction

- 1.

- Do innovation-driven policies promote or inhibit improvement of the total factor productivity of Chinese sports enterprises?

- 2.

- What is the relationship between the governance structure of sports enterprises and their total factor productivity?

- 3.

- How does governance structure influence the process of innovation-driven policies affecting the total factor productivity of sports enterprises?

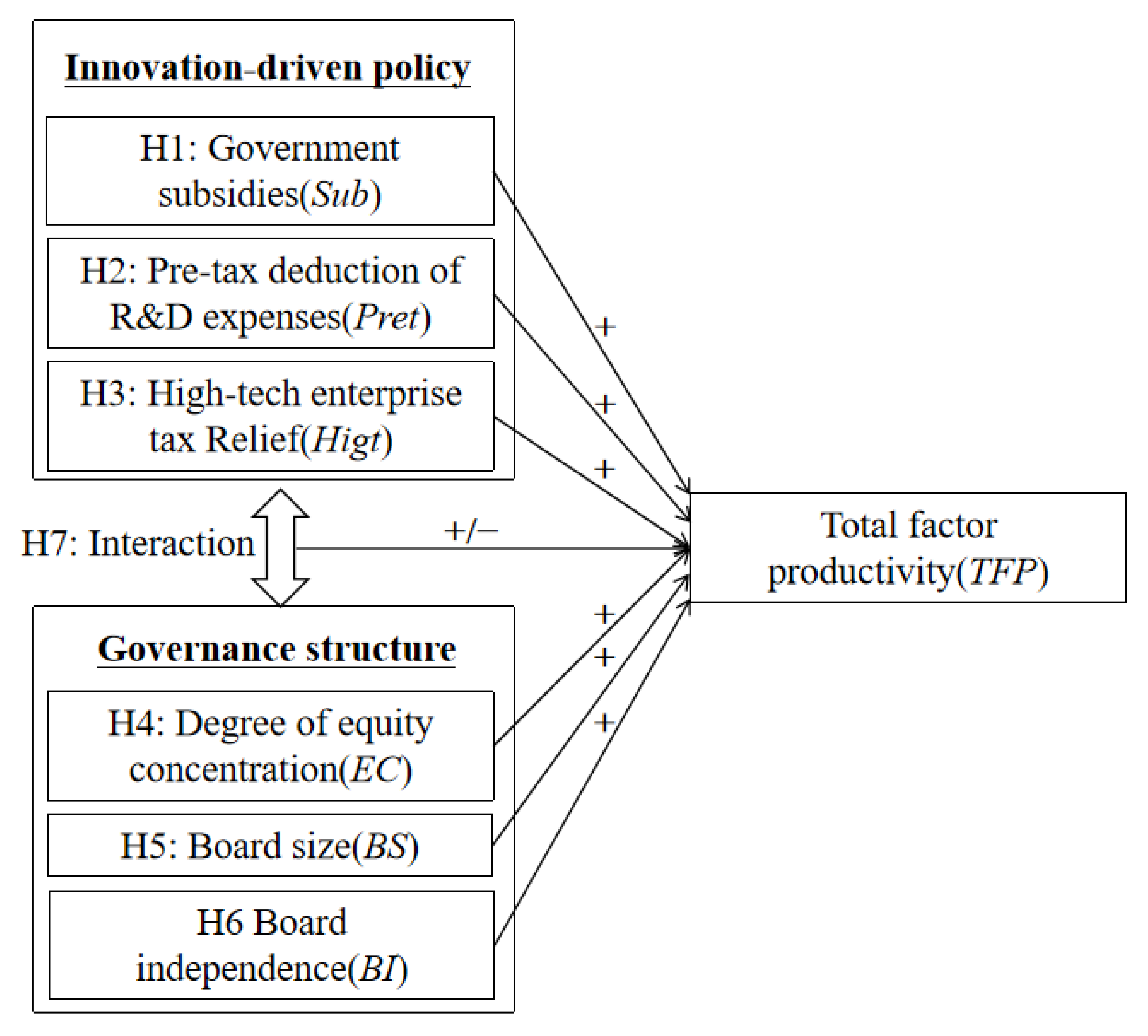

2. Theoretical Framework and Hypothesis Development

2.1. Innovation-Driven Policies Impacting Total Factor Productivity

2.1.1. Government Subsidies and Total Factor Productivity

2.1.2. Pre-Tax Deduction of R&D Expenses and Total Factor Productivity

2.1.3. High-Tech Enterprise Tax Relief and Total Factor Productivity

2.2. Impact of Governance Structure on Total Factor Productivity

2.2.1. Equity Concentration and Total Factor Productivity

2.2.2. Board Size and Total Factor Productivity

2.2.3. Board Independence and Total Factor Productivity

2.3. Moderating Effects of Governance Structure on the Relationship between Innovation-Driven Policies and Total Factor Productivity

3. Method

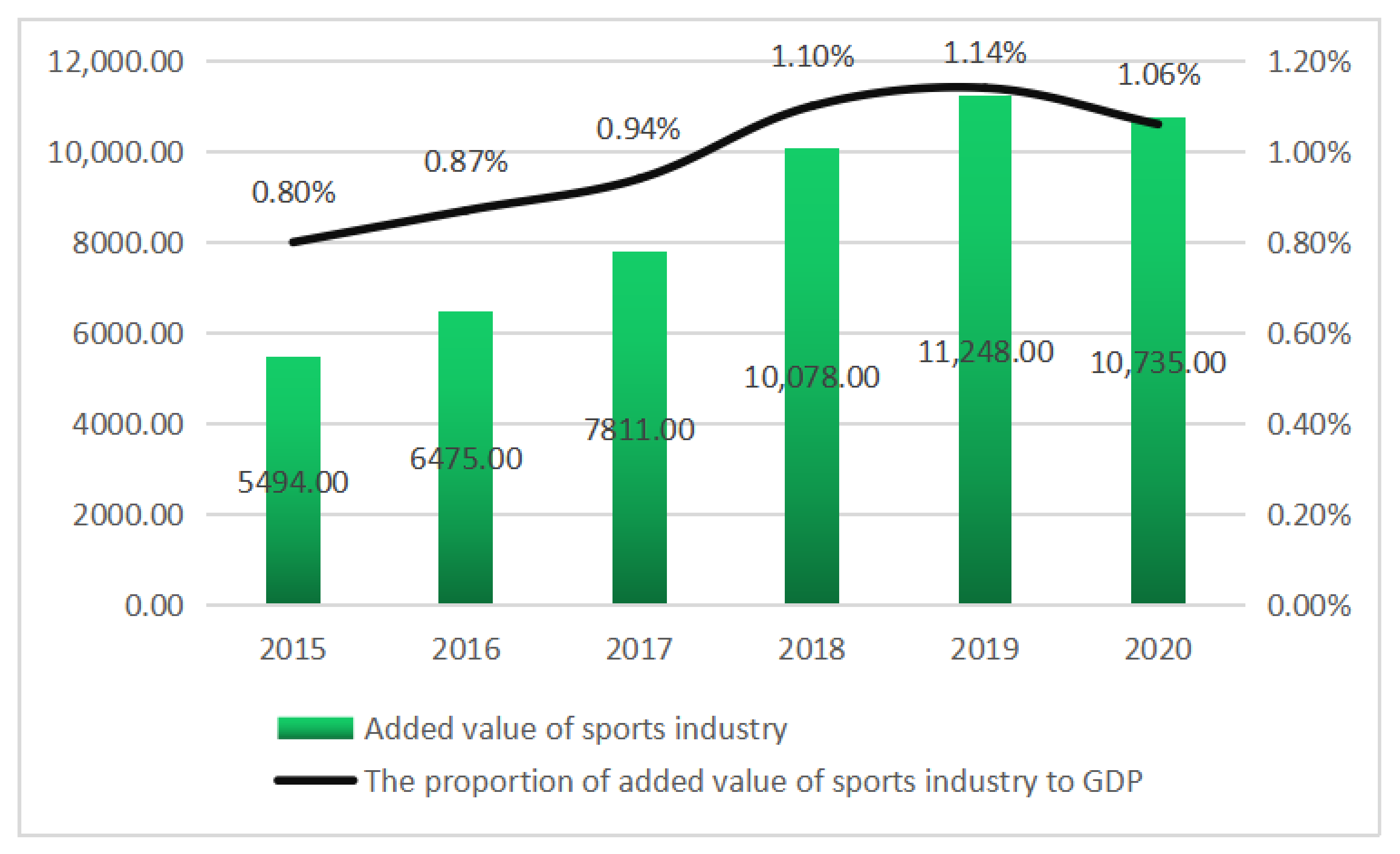

3.1. Research Context and Data

3.2. Research Variables

{kind=link}

{kind=link}

| Variables (Abbreviation) | Measurement | Reference |

|---|---|---|

| Total factor productivity (TFP) | Total factor productivity is evaluated based on mode | Zhu et al., 2014 [47] |

| Chen, 2014 [48] | ||

| Government subsidies (Sub) | Total government subsidy to support firms | Zhang and Guan, 2018 [18] |

| Pre-tax deduction of R&D expenses (Pret) | Pre-tax deduction of R&D expenses | Chen et al., 2020 [5] |

| High-tech enterprise tax relief (Higt) | Income tax relief amount of high-tech enterprise | Ding and Chen, 2022 [49] |

| Equity concentration (EC) | Shareholding of the top five largest shareholders | Chen et al., 2019 [11] |

| Board size (BS) | Number of members on board of directors | |

| Board independence (BI) | Percentage of independent directors | |

| Scale of asset (ASS) | Total assets | Chen et al., 2021 [50] |

| Asset–liability ratio (LEV) | Debt-to-asset ratio | |

| Intensity of R&D staff (RDP) | R&D staff ratio |

3.2.1. Dependent Variable

3.2.2. Independent Variables

3.2.3. Moderating Variables

3.2.4. Control Variables

3.3. Empirical Models

4. Results

4.1. Descriptive Statistics

4.2. Effects of Innovation-Driven Policies on Total Factor Productivity of Sports Firms

4.3. Effect of Governance Structure on Total Factor Productivity of Sports Firms

4.4. Effect of the Interaction between Innovation-Driven Policies and Corporate Governance Structure on Total Factor Productivity of Sports Firms

4.5. Robustness Tests

5. Discussion, Conclusions, and Suggestions

5.1. Discussion and Conclusions

5.2. Suggestions

6. Research Significance and Prospects

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Savić, Z.; Ranđelović, N.; Stojanović, N.; Stanković, V.; Šiljak, V. The Sports Industry and Achieving Top Sports Results. Facta Univ. Ser. Phys. Educ. Sport 2018, 15, 513. [Google Scholar] [CrossRef]

- Wei, D.; Lei, W. Dynamic Evaluation on Operational Efficiency of Publicly Traded Sports Companies Home and Abroad: DEA-Malmquist TFP Index. J. Wuhan Inst. Phys. Educ. 2012, 46, 31–35, 42. [Google Scholar]

- Solow, R.M. Technical Change and the Aggregate Production Function. Rev. Econ. Stat. 1957, 39, 312–320. [Google Scholar] [CrossRef]

- Baier, S.L.; Dwyer, G.P.; Tamura, R. How Important Are Capital and Total Factor Productivity for Economic Growth? Econ. Inq. 2006, 44, 23–49. [Google Scholar] [CrossRef]

- Chen, G.; Breedlove, J. The effect of innovation-driven policy on innovation efficiency: Based on the listed sports firms on Chinese new Third Board. Int. J. Sport. Mark. Spons. 2020, 21, 735–755. [Google Scholar] [CrossRef]

- Sung, B.; Choi, M.S.; Song, W.-Y. Exploring the Effects of Government Policies on Economic Performance: Evidence Using Panel Data for Korean Renewable Energy Technology Firms. Sustainability 2019, 11, 2253. [Google Scholar] [CrossRef]

- Carboni, O.A. The effect of public support on investment and R&D: An empirical evaluation on European manufacturing firms. Technol. Forecast. Soc. Change 2017, 117, 282–295. [Google Scholar]

- Chen, G.W.; Herrera, A.M.; Lugauer, S. Policy and misallocation: Evidence from Chinese firm-level data. Eur. Econ. Rev. 2022, 149, 104260. [Google Scholar] [CrossRef]

- Naciti, V.; Cesaroni, F.; Pulejo, L. Corporate governance and sustainability: A review of the existing literature. J. Manag. Gov. 2022, 26, 55–74. [Google Scholar] [CrossRef]

- Nguyen, Q.K. The impact of risk governance structure on bank risk management effectiveness: Evidence from ASEAN countries. Heliyon 2022, 8, e11192. [Google Scholar] [CrossRef]

- Chen, G.; Zhang, J.J.; Pifer, N.D. Corporate Governance Structure, Financial Capability, and the R&D Intensity in Chinese Sports Sector: Evidence from Listed Sports Companies. Sustainability 2019, 11, 6810. [Google Scholar]

- Chen, C.; Lan, Q.; Gao, M.; Sun, Y. Green Total Factor Productivity Growth and Its Determinants in China’s Industrial Economy. Sustainability 2018, 10, 1052. [Google Scholar] [CrossRef]

- Chen, F.; Liu, J.; Liu, X.; Zhang, H. Static and Dynamic Evaluation of Financing Efficiency in Enterprises’ Low-Carbon Supply Chain: PCA–DEA–Malmquist Model Method. Sustainability 2023, 15, 2510. [Google Scholar]

- Zhao, W.; Xu, Y. Public Expenditure and Green Total Factor Productivity: Evidence from Chinese Prefecture-Level Cities. Int. J. Environ. Res. Public Health 2022, 19, 5755. [Google Scholar] [CrossRef] [PubMed]

- Wang, K.; Liu, L.; Deng, M.; Feng, Y. Internal Control, Environmental Uncertainty and Total Factor Productivity of Firms—Evidence from Chinese Capital Market. Sustainability 2023, 15, 736. [Google Scholar] [CrossRef]

- Xie, R.; Fu, W.; Yao, S.; Zhang, Q. Effects of financial agglomeration on green total factor productivity in Chinese cities: Insights from an empirical spatial Durbin model. Energy Econ. 2021, 101, 105449. [Google Scholar] [CrossRef]

- Guan, J.; Yam, R.C.M. Effects of government financial incentives on firms’ innovation performance in China: Evidences from Beijing in the 1990s. Res. Policy 2015, 44, 273–282. [Google Scholar] [CrossRef]

- Zhang, J.; Guan, J. The time-varying impacts of government incentives on innovation. Technol. Forecast. Soc. Change 2018, 135, 132–144. [Google Scholar] [CrossRef]

- Skuras, D.; Tsekouras, K.; Dimara, E.; Tzelepis, D. The Effects of Regional Capital Subsidies on Productivity Growth: A Case Study of the Greek Food and Beverage Manufacturing Industry. J. Reg. Sci. 2006, 46, 355–381. [Google Scholar] [CrossRef]

- Lee, E.; Walker, M.; Zeng, C. Do Chinese government subsidies affect firm value? Account. Organ. Soc. 2014, 39, 149–169. [Google Scholar] [CrossRef]

- Söderblom, A.; Samuelsson, M.; Wiklund, J.; Sandberg, R. Inside the black box of outcome additionality: Effects of early-stage government subsidies on resource accumulation and new venture performance. Res. Policy 2015, 44, 1501–1512. [Google Scholar] [CrossRef]

- Peng, H.; Liu, Y. How government subsidies promote the growth of entrepreneurial companies in clean energy industry: An empirical study in China. J. Clean. Prod. 2018, 188, 508–520. [Google Scholar]

- Kasahara, H.; Shimotsu, K.; Suzuki, M. Does an R&D tax credit affect R&D expenditure? The Japanese R&D tax credit reform in 2003. J. Jpn. Int. Econ. 2014, 31, 72–97. [Google Scholar]

- Andersen, D.C.; López, R. Do Tax Cuts Encourage Rent Seeking by Top Corporate Executives? Theory and Evidence. Contemp. Econ. Policy 2019, 37, 219–235. [Google Scholar]

- Howell, A. Firm R&D, innovation and easing financial constraints in China: Does corporate tax reform matter? Res. Policy 2016, 45, 1996–2007. [Google Scholar]

- Zheng, B.; Zhang, Z. Dose Decrease of Enterprise Income Tax Rate Affect Total Factor Productivity? Empirical Evidence of Chinese Listed Companies. Account. Res. 2018, 5, 13–20. [Google Scholar]

- Driver, C.; Guedes, M.J.C. Research and development, cash flow, agency and governance: UK large companies. Res. Policy 2012, 41, 1565–1577. [Google Scholar] [CrossRef]

- Castro Martins, H. The Brazilian bankruptcy law reform, corporate ownership concentration, and risk-taking. Manag. Decis. Econ. 2020, 41, 562–573. [Google Scholar] [CrossRef]

- Shleifer, A.; Vishny, R.W. Large Shareholders and Corporate Control. J. Political Econ. 1986, 94, 461–488. [Google Scholar] [CrossRef]

- Jensen, M.C.; Meckling, W.H. Theory of the firm: Managerial behavior, agency costs and ownership structure. J. Financ. Econ. 1976, 3, 305–360. [Google Scholar] [CrossRef]

- Morck, R.; Shleifer, A.; Vishny, R.W. Management ownership and market valuation. J. Financ. Econ. 1988, 20, 293–315. [Google Scholar] [CrossRef]

- Li, W.; Li, H. Ownership Structure, Executive Ownership and Performance: Evidence from Private Listed Firms in China. Nankai Bus. Rev. 2006, 5, 4–10. [Google Scholar]

- Pfeffer, J. Canonical Analysis of the Relationship between an Organization’s Environment and Managerial Attitudes toward Subordinates and Workers. Hum. Relat. 1973, 26, 325–337. [Google Scholar] [CrossRef]

- Vincent, O.C.; Cramer, N. The relationship between firm performance and board characteristics in Ireland. Eur. Manag. J. 2009, 28, 387–399. [Google Scholar]

- Su, k.; Liu, H.; Zhang, H. Board size, social trust, and corporate risk taking: Evidence from China. Manag. Decis. Econ. 2019, 40, 596–609. [Google Scholar] [CrossRef]

- Ongsakul, V.; Treepongkaruna, s.; Jiraporn, P.; Uyar, A. Do firms adjust corporate governance in response to economic policy uncertainty? Evidence from board size. Financ. Res. Lett. 2020, 39, 101613. [Google Scholar] [CrossRef]

- Huang, V.S.; Wang, C.J. Corporate governance and risk-taking of Chinese firms: The role of board size. Int. Rev. Econ. Financ. 2015, 37, 96–113. [Google Scholar] [CrossRef]

- Cheng, M.; Lin, B.; Lu, R.; Wei, M. Non-controlling large shareholders in emerging markets: Evidence from China. J. Corp. Financ. 2020, 63, 101259. [Google Scholar]

- Wang, H.; Yue, H.; Zhang, X. Research on the Relationship between Corporate Governance Structure and Corporate Performance: A Perspective based on Corporate Total Factor Productivity. Shanghai J. Econ. 2019, 4, 17–27. [Google Scholar]

- Chen, Y.; Liu, B. An Empirical Analysis on the Relationship between the Development of Sporting Goods Family Business and Government Support. J. Shanghai Univ. Sport 2015, 39, 17–21. [Google Scholar]

- Tylecote, A.; Doo Cho, Y.; Zhang, W. National technological styles explained in terms of stakeholding patterns, enfranchisement and cultural differences: Britain and Japan. Technol. Anal. Strateg. Manag. 1998, 10, 423–436. [Google Scholar] [CrossRef]

- O’Connor, M.; Rafferty, M. Corporate Governance and Innovation. J. Financ. Quant. Anal. 2012, 47, 397–413. [Google Scholar] [CrossRef]

- Bates, T.W.; Kahle, K.M.; Stulz, R.M. Why Do U.S. Firms Hold So Much More Cash than They Used To? J. Financ. 2009, 64, 1985–2021. [Google Scholar] [CrossRef]

- Lacetera, N. Corporate Governance and the Governance of Innovation: The Case of Pharmaceutical Industry. J. Manag. Gov. 2001, 5, 29–59. [Google Scholar] [CrossRef]

- Partington, G.H. Dividend Policy and Its Relationship to Investment and Financing Policies: Empirical Evidence Using Irish Data. J. Bus. Financ. Account. 1985, 12, 531–542. [Google Scholar]

- Wright, P.; Ferris, S.P.; Sarin, A. Impact of Corporate Insider, Blockholder, and Institutional Equity Ownership on Firm Risk Taking. Acad. Manag. J. 1996, 39, 441–458. [Google Scholar] [CrossRef]

- Zhu, J.; Zhan, S.; Shao, Y. Research on Total Factor Productivity Change and Its Influencing Factors of Sports Goods Manufacturing Industry in China. Sport. Sci. 2014, 35, 68–78, 105. [Google Scholar]

- Chen, P. Chinese Sports Sports Goods Manufacturing Industry Total Factor Productivity Changes and Its Decomposition: Based on the Non-parametric Malmquist Index Approach Empirical Research. China Sport. Sci. Technol. 2014, 50, 118–125. [Google Scholar]

- Ding, Y.; Chen, G. How Do Innovation-Driven Policies Help Sports Firms Sustain Growth? The Mediating Role of R&D Investment. Sustainability 2022, 14, 15688. [Google Scholar]

- Chen, G.; Mao, L.L.; Pifer, N.D.; Zhang, J.J. Innovation-driven development strategy and research development investment: A case study of Chinese sport firms. Asia Pac. J. Mark. Logist. 2021, 33, 1578–1595. [Google Scholar] [CrossRef]

- An, T.; Zhou, S.; Pi, J. The Stimulating Effects of R&D Subsidies on Independent Innovation of Chinese Enterprises. Econ. Res. J. 2009, 44, 87−98, 120. [Google Scholar]

- Crespi, G.; Giuliodori, D.; Giuliodori, R.; Rodriguez, A. The effectiveness of tax incentives for R&D in developing countries: The case of Argentina. Res. Policy 2016, 45, 2023–2035. [Google Scholar]

- Busom, I.; Corchuelo, B.; Martínez-Ros, E. Tax incentives… or subsidies for business R&D? Small Bus. Econ. 2014, 43, 571–596. [Google Scholar]

- Nguyen, Q.K. Ownership structure and bank risk-taking in ASEAN countries: A quantile regression approach. Cogent Econ. Financ. 2020, 8, 1809789. [Google Scholar] [CrossRef]

- Yermack, D. Higher market valuation of companies with a small board of directors. J. Financ. Econ. 1996, 40, 185–211. [Google Scholar] [CrossRef]

| Mean | Std.Dev. | Min | Max | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1. TFP | 0.149 | 0.165 | 0.000 | 1.000 | 1.000 | |||||||||

| 2. Sub | 10.879 | 5.536 | 0.000 | 17.836 | 0.091 | 1.000 | ||||||||

| 3. Pret | 3.622 | 5.879 | 0.000 | 16.516 | 0.134 | 0.269 | 1.000 | |||||||

| 4. Higt | 5.323 | 6.835 | 0.000 | 18.477 | 0.278 | 0.230 | 0.302 | 1.000 | ||||||

| 5. EC | 0.900 | 0.114 | 0.500 | 1.000 | −0.231 | −0.057 | −0.012 | −0.070 | 1.000 | |||||

| 6. BS | 1.688 | 0.189 | 0.693 | 2.565 | 0.167 | 0.133 | −0.042 | 0.161 | −0.334 | 1.000 | ||||

| 7. BI | 0.015 | 0.074 | 0.000 | 0.600 | 0.197 | 0.110 | 0.053 | 0.083 | −0.252 | 0.316 | 1.000 | |||

| 8. ASS | 18.238 | 1.416 | 13.561 | 22.454 | −0.179 | 0.009 | 0.026 | −0.152 | 0.118 | −0.077 | −0.056 | 1.000 | ||

| 9. LEV | 1.239 | 6.502 | 0.000 | 87.090 | −0.042 | −0.071 | −0.077 | −0.103 | 0.022 | −0.107 | −0.027 | −0.032 | 1.000 | |

| 10. RDP | 0.196 | 0.206 | 0.000 | 0.953 | 0.033 | 0.045 | 0.034 | 0.236 | −0.041 | 0.088 | −0.053 | −0.055 | −0.086 | 1.000 |

| Model 1 TFP | Model 2 TFP | Model 3 TFP | |

|---|---|---|---|

| Sub | 0.001 (0.001) | 0.000 (0.001) | |

| Pret | 0.002 (0.001) | 0.002 (0.001) | |

| Higt | 0.006 *** (0.001) | 0.005 ***(0.001) | |

| EC | −0.233 *** (0.068) | −0.233 *** (0.066) | |

| BS | 0.049 (0.042) | 0.033 (0.041) | |

| BI | 0.291 *** (0.103) | 0.255 ** (0.100) | |

| ASS | −0.017 *** (0.005) | −0.017 *** (0.005) | −0.014 *** (0.005) |

| LEV | 0.000 (0.001) | −0.001 (0.001) | 0.000 (0.001) |

| RDP | −0.029 (0.036) | 0.014 (0.035) | −0.026 (0.035) |

| _cons | 0.424 *** (0.095) | 0.587 *** (0.139) | 0.529 *** (0.135) |

| F-value | 9.15 *** | 8.98 *** | 9.88 *** |

| 0.1022 | 0.1006 | 0.1565 |

| Model 4 TFP | Model 5 TFP | Model 6 TFP | |

|---|---|---|---|

| EC-Sub | −0.001 (0.001) | ||

| EC-Pret | 0.001 (0.001) | ||

| EC-Higt | 0.006 *** (0.001) | ||

| BS-Sub | 0.001 (0.001) | ||

| BS-Pret | 0.001 * (0.001) | ||

| BS-Higt | 0.003 *** (0.001) | ||

| BI-Sub | 0.002 (0.010) | ||

| BI-Pret | 0.077 *** (0.016) | ||

| BI-Higt | 0.005 (0.015) | ||

| ASS | −0.018 *** (0.005) | −0.016 *** (0.005) | −0.019 *** (0.005) |

| LEV | −0.001 (0.001) | 0.000 (0.001) | −0.001 (0.001) |

| RDP | −0.022 (0.036) | −0.036 (0.035) | 0.002 (0.034) |

| _cons | 0.460 *** (0.096) | 0.406 *** (0.095) | 0.481 *** (0.092) |

| F-value | 7.03 *** | 11.03 *** | 11.88 *** |

| 0.080 | 0.121 | 0.129 |

| Model 7 | Model 8 TFP | Model 9 TFP | Model 10 TFP | |

|---|---|---|---|---|

| Sub | −0.000 (0.002) | −0.016 (0.022) | −0.003 (0.004) | −0.000 (0.001) |

| Pret | 0.002 (0.002) | 0.018 (0.020) | 0.002 (0.002) | 0.002 (0.001) |

| Higt | 0.005 *** (0.001) | 0.050 *** (0.019) | 0.069 *** (0.011) | 0.005 *** (0.001) |

| EC | −0.292 *** (0.776) | −0.299 *** (0.078) | −0.097 (0.160) | −0.243 *** (0.068) |

| BS | −0.057 (0.049) | −0.047 (0.049) | −0.081 (0.082) | 0.014 (0.045) |

| BI | 0.285 ** (0.118) | 0.296 ** (0.119) | 0.257 (0.184) | 0.292 *** (0.111) |

| ASS | −0.030 *** (0.006) | −0.031 *** (0.006) | −0.031 *** (0.010) | −0.014 *** (0.005) |

| LEV | 0.001 (0.001) | 0.001 (0.001) | 0.121 * (0.069) | −0.001 (0.002) |

| RDP | −0.009 (0.041) | 0.001 (0.041) | 0.098 (0.066) | −0.024 (0.035) |

| _cons | 1.047 *** (0.159) | 1.061 *** (0.160) | −0.032 (0.321) | 0.569 *** (0.143) |

| F-value | 9.31 *** | 8.46 *** | 9.54 *** | 9.77 *** |

| 0.1488 | 0.1372 | 0.3266 | 0.1551 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Guo, Z.; Chen, G.; Ding, Y. Innovation-Driven Policies, Corporate Governance Structure and Total Factor Productivity in Chinese Sports Sector: Evidence from Listed Sports Firms. Sustainability 2023, 15, 6991. https://doi.org/10.3390/su15086991

Guo Z, Chen G, Ding Y. Innovation-Driven Policies, Corporate Governance Structure and Total Factor Productivity in Chinese Sports Sector: Evidence from Listed Sports Firms. Sustainability. 2023; 15(8):6991. https://doi.org/10.3390/su15086991

Chicago/Turabian StyleGuo, Ziyu, Gang Chen, and Yang Ding. 2023. "Innovation-Driven Policies, Corporate Governance Structure and Total Factor Productivity in Chinese Sports Sector: Evidence from Listed Sports Firms" Sustainability 15, no. 8: 6991. https://doi.org/10.3390/su15086991